Company Insights

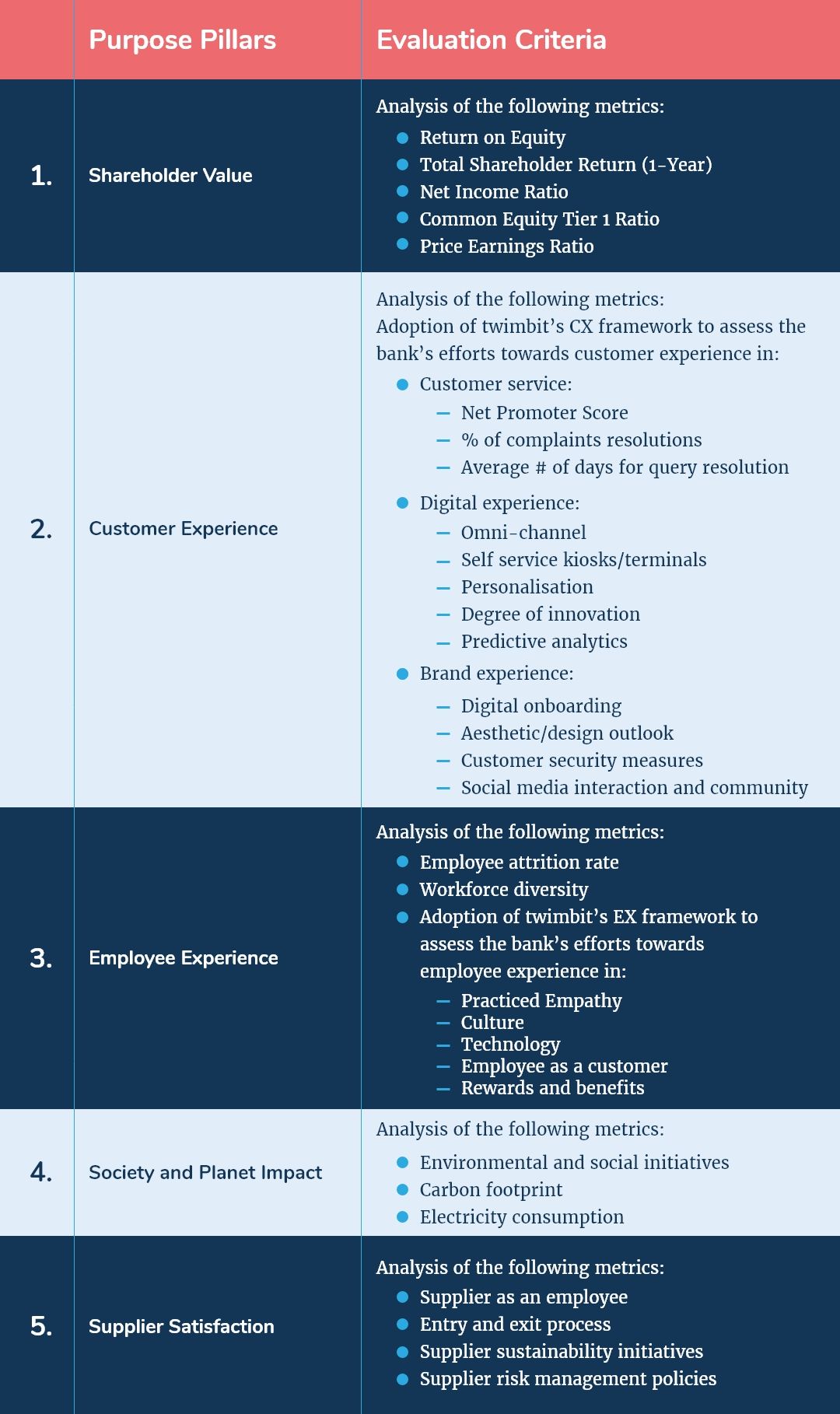

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Bank of Queensland (Group financials) – An overview as of 31st August 2020

| Bank name | Bank of Queensland (BOQ) |

| Headquarters | Brisbane, Australia |

| Operating income (31st August 2020) | USD 811.5 million |

| Profit after tax (Net Profit) (31st August 2020) | USD 84.83 million |

| Total Assets | USD 41.88 billion |

| Employees | 2,098 |

| Country of operation | Australia |

| Number of branches | 165 |

| Information and communication technology (ICT) spend (31st August 2020) | USD 150.49 million |

| Bank ranking in a particular country | 6th in Australia |

| Number of customers | 910,000 |

| Market capitalisation (31st August 2020) | USD 2.31 billion |

| Operating revenue CAGR growth (2016-2020) | -0.25% |

Australia’s Conversion: AUD to USD conversion at 0.7377

Shareholder value (31st August 2020)

| Return on Equity (31st August 2020) | 2.84% |

| Total Shareholder Return (1-Year) | -29.80% |

| Net Income Ratio | 10.49% |

| Common Equity Tier 1 Ratio | 9.78% |

| Price Earnings Ratio (31st August 2020) | 30.96 |

BOQ and its strategic focus areas

- Financial performance and growth

- To have a strong and sustainable growth rate in the long run, the Bank of Queensland (BOQ) intends to maintain a group-wide deposit-to-loan ratio of more than 70%.

- To build and maintain solid financial and risk positions, the bank aims to generate a capital investment of USD 73.77 million per annum for the next two years.

- To improve risk-based pricing and margin management, thereby increasing profitability and optimising the bank’s plans to deliver productivity benefits.

- BOQ had a CET1 (Common Equity Tier 1) ratio of 9.78 per cent, which is strong enough to absorb shocks from the prevailing economic climate.

Initiatives taken by BOQ to uplift financial performance and growth in 2019 and 2020:

- Raised capital of USD 250.82 million pre-COVID-19 to boost growth and expansion initiatives

- Maintained a deposit to loan ratio of 74%

- Governed risk and compliance systems to combat defaults

- Set sustainable growth targets in (Cash) earnings per share (EPS) from FY2021 onwards.

- Customer experience

- BOQ aspires to build a distinctive purpose-led culture with empathy to guide its customers fairly and have optimum decisions available for its customers.

- The bank intends to become a leader by improving customer experience (CX) through a flexible and resilient digital infrastructure. The CX improvements go along with smart data insights that drive customer relationships and experiences.

- Virgin Money Australia (VMA)- The bank’s digital-first (neobank) retail financial services company aims to provide a sophisticated digital and mobile app experience (Note: BOQ acquired VMA in 2013, and it operates as a standalone brand within the bank). The bank conducted a soft launch in December 2020 as Phase 1 of VMA services.

- With the aim of providing the right products to meet its customers’ dynamic needs, the bank’s product simplification aims to enhance the product knowledge of its distribution teams and reduce product risk.

- BOQ identifies customers who may be experiencing financial hardship by contacting customers in arrears and including details of the bank’s hardship programs on its website.

- BOQ adopts a ‘find it, fix it’ complaints culture, with the aim of empowering its frontline teams and customer relations specialists to resolve customer complaints quickly.

- BOQ has a Vulnerability program to provide simple yet robust processes to support customers experiencing financial vulnerability and provide them with affordable products and services.

BOQ and its customer performance measures for FY2020:

| Overall Retail Net Promoter Score (NPS) | 17 |

| Mortgage NPS Score | -2 |

| Mortgage NPS rank | 5th |

| Mobile Banking NPS score | 3 |

| Mobile Banking NPS rank | 10th |

| Internet banking NPS rank | 6th |

| SME customer NPS score | Micro: +8; Small: 0; Medium: +2 |

| Change in the number of products for sale | 14% reduction |

Initiatives taken by BOQ to enhance the customer experience in 2019-2020:

- During FY2020, BOQ managed to reduce the number of retail products available for sale by 14%. It also removed the St Andrew’s insurance products from being sold to new customers. This program has plans to continue into FY2021 to reduce the bank’s products available for sale by 50%.

- The bank made tangible changes to its home lending process, which helped them significantly reduce the ‘time to yes’ for its customers from more than four days to a single day. BOQ achieved a home lending growth of more than USD 374.75 million in FY2020.

- BOQ improved its ranking from 5th position to 3rd on customer net promotor scores and was named the 2020 MOZO People’s Choice Award winner in the Excellent Customer Service category.

- It built a new contact centre telephony platform, a new Customer Relationship Management (CRM) tool, and developed a broker portal, which has enhanced CX.

- BOQ established the Home Buying Transformation program to make its home loan process simpler and faster for customers looking to buy or refinance their property.

- Employee experience

1. BOQ plans on creating a resilient, adaptable, empowered, diverse, and inclusive workforce with a strong sense of purpose and ethics.

- One of the key focus areas for improving employee experience is organising regular training and development programs for employees and increasing emphasis on flexible working and workforce wellbeing.

- Gender equality seems to be a key inclusion focus for BOQ. The bank continued to set KPIs on gender targets and conduct gender pay reviews in each remuneration cycle to address the gender pay gap. BOQ also supports its people through the parental leave journey and maintains an equitable talent pipeline constructively.

- Owner-managed branches:

- Under this model, about 60% of BOQ branches are under the task of Owner Managers, who are agents and franchisees of BOQ. They are authorised to conduct BOQ business.

- Owner Managers are managers of the branch who also own their branch business. As small-business owners, they have the freedom to personally manage their customer relationships and the incentive to drive their business’s success. These relationships extend into the broader community, with the Owner Managers supporting local charities, schools and sporting organisations. They are also strong advocates for their local business and professional communities.

- Development & recognition:

- BOQ has a recognition and reward program called the “Prove It’s Possible Awards”. The program recognises employees from every division who exhibit outstanding demonstration in their core values.

- Financial wellbeing:

- Discounts through various gym and health providers

- Access to online information sessions on how to best manage their general health

- Flu vaccinations program available to all staff

- Fee-free transaction accounts, discounted insurance, credit cards, home lending, personal lending, and salary packaging

- Attractive superannuation plan

- Online and onsite information sessions

- Salary sacrifice options, including superannuation, airline memberships, car parking, and novated leases

- Discounts on a wide range of items, such as travel, cars, local business offers, and entertainment Books

- A BOQ Share Plan which is available on an annual basis.

- Health & wellbeing of employees:

- Physical WHS (work, health, and safety) ‘health checks’ for all its branches Delivery of risk and safety leadership training

- Proactive focus on injury management for both non-work and work-related injuries and illness

- BOQ Group wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs

- Ergonomic design standards applied to the corporate office and branch design, branch conversions, and site refurbishments

- Framework to ensure WHS standards are maintained for employees working from home or remotely

Initiatives taken by BOQ to enhance capabilities and promote a healthy work environment in 2019-2020:

- Launched a new groupwide recognition program, ‘ThankQ’, to recognise the people that make a significant contribution to its strategy, role model, and their purpose and values. This program will be a key enabler to reward outstanding performance and reinforce behaviours aligned to the company culture.

- The bank launched a refreshed approach to senior talent and succession to ensure that its efforts focus on attracting and retaining the best talent.

- In August 2020, BOQ launched the first of their pulse surveys. The aim was to track the impact of its culture-change initiatives and to ascertain current levels of employee engagement.

- Implemented a plan of action to manage COVID-19 hardships and deferrals.

- Improved the employee engagement score to 59% in 2019-2020 from 56% in 2018-2019.

- Society and planet impact

- BOQ supports the transition to a net-zero carbon economy consistent with the Paris Agreement to keep global warming well below 2 degrees Celsius. It is further trying to limit the temperature to 1.5 degrees Celsius, which is above pre-industrial levels.

- To reinforce its commitment to climate change and transparency of reporting, in FY2020, BOQ evolved its reporting further. The changes are in alignment with the final recommendations of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD).

- The bank is in regular communication with its community partners and rolls out several community volunteering and fundraising initiatives throughout the year.

- BOQ aims to build a roadmap to 100% renewable energy, reduce its carbon footprint, and actively support its customers to transition to the lower-carbon economy.

Key initiatives undertaken by BOQ to create environmental impact include:

- Trialled solar panels and LED lighting in branches and successfully reducing carbon emissions between 20-45%.

- Reduced travel through greater use of technology and online-based collaboration tools.

- Introduced e-statements, estimated to save more than 600,000 sheets of paper a year.

- Introduced electronic invoice processing, making paper invoices obsolete.

- Moved from monthly to quarterly statements and consolidated customer statements into a single envelope, saving around 1.5 million envelopes per year.

- Recovered and redeployed 100 unused computers through an IT amnesty program.

- Committed to cease funding equipment directly involved in the extraction of fossil fuels by FY2024.

Digital Strategy

BOQ devised a multi-year roadmap for its digital journey. It outlines the key initiatives and milestones that will help them achieve digital transformation from FY2021-FY2024. As a part of its digital journey, BOQ is focusing on the following areas:

- Digital bank: BOQ plans to launch a new platform with transaction and savings accounts for Virgin Money Australia (VMA), its digital bank. This platform will help BOQ migrate its customers onto the digital bank platform built for VMA. The said platform will further enable BOQ to leverage and form a strong foundation for a broader BOQ digital bank in its subsequent phases of work.

- Application Program Interface (API): BOQ has continued to develop its internal and external API to support its digital transformation journey.

- Automation of processes: To improve operational productivity, efficiency and customer experience across multiple business segments within the bank, BOQ plans to inculcate Robotic Process Automation (RPA) to automate its processes.

- BOQ is also stepping towards adopting Intelligent Automation technologies. It plans to use Artificial Intelligence (AI) and Machine Learning (ML) to understand and replicate human judgement. The said applications are from knowledge acquired via training on previously collected data and insights.

- Partnerships: BOQ has local and international partnerships in place with fintechs through their relationship with FinTech Australia, River City Labs and Plug and Play in Silicon Valley. There is also a broader ecosystem to help them quickly adapt, test, and deliver for its stakeholders.

- Cybersecurity and customer data privacy

- BOQ plans to operate effectively in an elevated cyber risk environment by strengthening its cybersecurity function in combination with its cybersecurity service providers.

- BOQ intends to have more control and visibility over how it protects customer data and assets. The bank aims to have better flexibility and agility to ensure that its cybersecurity evolves as cyber threats become more sophisticated.

- To support data protection, the BOQ cybersecurity team collaborates with industry-leading threat intelligence partners and other security teams from financial services organisations. This move helps it keep abreast of trends related to cyber-criminal activities.

- Additionally, BOQ has established a new and enhanced governance framework that ensures that cyber-related issues or risks are dealt with effectively and efficiently.

- BOQ is also investing in automation and threat intelligence to implement more proactive methods of managing cyber threats.

Initiatives taken by BOQ for its digital strategy:

- BOQ introduces digital processing in lending, thereby improving turnaround time and reducing the cost of loan origination

- The bank enhances credit decisions with an automated credit bureau check in less than 30 seconds

- BOQ delivers a comprehensive digital transformation through the implementation of digital and cloud-based technologies. This transformation started with its investment in VMA, a new digital bank

- Launched and scaled ‘Pocket Banker’, which gives its customers and branch staff the ability to communicate via video or chat and share documents digitally.

- Enabled digital automation solutions within its contact centre for customers who wished to retrieve information on their account balances and recent transactions.

IT Strategy

- BOQ focuses on three things: the modernisation of infrastructure, transitioning to a cloud-based digital banking platform, and increasing process automation. With these three things at focus, the bank’s IT strategy is as follows:

- To migrate its key data centres to private cloud — consequently improving automation, stability, risk, and scalability

- Build a next-gen core banking platform, which includes capabilities like the cloud-based VMA digital bank, transactions, savings, credit cards, lending, and term deposits, among others

- Drive efficiency across the business and provide customers with intelligent analytics and data insights

- Technology expenses of USD 115.82 million for FY2020 increased by USD 23.6 million (26 per cent) compared to FY2019.

- Investments in systems to comply with regulatory obligations and technology structure drove the increase significantly, including costs associated with anti-money laundering tools and the transition of data centres as part of the bank’s infrastructure modernisation program. It also included new technology services to support the bank’s transformation program.

- Initiatives taken by BOQ to support its IT strategy in 2019-2020:

- Migration of data centres to the cloud

- Cybersecurity and customer data privacy: BOQ invested in automation and threat intelligence to implement proactive methods of managing cyber threats

- Automation and robotics: BOQ started exploring Robotics Process Automation (RPA) and other solutions involving machine learning and artificial intelligence

BOQ and its ICT contracts

- With Fiserv, to enable the debit card program for BOQ and VMA.

- Alongside Octet, to provide B2B supply chain finance products to the bank.

- With FinnOne from Nucleus Software, to digitally transform the bank’s banking operations and enhance customer experience.

- Alongside Temenos banking software, to simplify its digital business model and drive operational efficiencies.

9 Growth and Innovation Opportunities

- #1 Cost to serve

- BOQ has a cost to income ratio of 54.2 per cent, resulting from the material provision for expected credit losses (ECL). The said losses came from the impact of the COVID-19 pandemic on its customers and a write-down in its technology investment.

- The bank’s total operating expenses increased by USD 28.77 million to USD 438.19 million, i.e., a 7% rise from FY2019 to FY2020. This spike was primarily due to increased investments in risk, regulatory programs, and technology projects.

- Administration expenses of USD 24.24 million for FY2020 increased by USD 3.03 million or by 14 per cent compared to 2019. This growth was primarily due to the costs of external support for risk and regulatory projects, COVID-19-related modelling, and an increase in group insurance costs.

- COVID-19 left a significant scar on the bank’s operational performance. Its statutory net profit after tax fell from USD 219.8 million to USD 84.83 million, i.e., a reduction of 61% compared to FY2019. Increased impairment expense, lowered net interest margins(NIM), higher operating expenses, and a 50% reduction in term deposits significantly offset the inflows BOQ received from savings and investment accounts, as well as its retail consumer deposits.

- To sustain itself in a low-interest-rate environment while functioning with a low-cost deposit portfolio, the bank needs to:

- Use data analytics for risk intermediation to check for repayment risk in loans and attrition risks in deposits.

- Control its loan impairment charges (which bumped up to USD 129.1 million, i.e., 154 per cent compared to FY2019 by preserving its capital and strengthening its risk intermediation.

- Focus on non-interest income (which reduced by 14% compared to FY2019) to make up for the losses faced on the net interest income and deposits front.

- To make up for the 1.91 % decline in NIM, BOQ should:

- Continue to expand its home lending business segment, which shows strong business values and a promising growth rate

- Roll out loan repricing schemes within limits prescribed by APRA (The Australian Prudential Regulation Authority)

- #2 Transformation of the branch and its branch networks

- The Bank of Queensland, Australia has around 165 bank branches, 566 BOQ ATMs, and 1009 rediATMs (the rediATM network allows the customers of its partner financial institutions to use any of over 1,700 rediATMs across Australia without being charged a direct ATM fee). The total occupancy costs including leases expenses, depreciation, maintentaince, and owner-managed branches associated with this infrastructure translates to USD 28.77 million, i.e., 3.6 % of its total income.

- The bank has a unique opportunity to build a highly sophisticated omnichannel experience to transform its existing branch model by:

- Introducing video-customer relationship managers to reduce customer wait time, especially during times when there is heavy foot traffic in the branch.

- Making OMB (Owner Managed Branches) more digitally relevant by training Owner Managers in digital skills to leverage their understanding of the local communities uniquely. This move can be coupled with relevant data insights to deliver high quality and personalised customer service.

- Making most of its banking services like loan applications, cashing in cheques, etc., accessible through digital channels. This step could relieve the customers of the pain of physically visiting the branch.

- BOQ can further create a phygital (physical and digital) branch and make its branch future-ready, sustainable, and profitable by:

- Shifting workloads to self-service kiosks, which can provide a host of services outside the ambit of normal office hours without employing additional staff.

- Introducing live customer dashboards which can alert bankers when customers make transactions at ATMs. This step uniquely positions them to offer support, personalised offers, and reduce customers’ pain points.

- Transforming the bank’s interiors by having dedicated spaces for self-service zones, smart ATMs, indoor community space (like cafes, customer lounges, etc.) equipped with technology and free WiFi for community or business meetings.

- #3 Customer experience

- To deliver products and services that help customers make better financial decisions, the bank should focus on:

- Diversifying and strengthening its lending product stack and building capabilities to cater to the unique needs of the customer segment. This move will also help the bank sustain its deposit and loan growth rates.

- Automating routine customer query management by introducing chatbots and virtual assistants. These digital features can handle customer queries on a real-time basis across all of the bank’s digital platforms.

- With uplifting the NPS (Net Promoter Score) score as its key focus area, BOQ could work actively towards building customer loyalty by:

- Increasing accessibility of its services by integrating banking products and services across all its phygital channels.

- Using AI to take active cognisance of past, present, and prospective customer needs to deliver personalised services in the mortgage and customer segment. Doing so would connect BOQ customers to their required financial needs optimally.

- Giving the customers flexibility of choice by offering microloans and investment products in their retail banking segment.

- #4 Employee experience and productivity

- Employee expenses grew to USD 208.76 million in FY2020 from USD 198.4 million in FY2019. This increase was largely due to investments in risk and regulatory programs as well as strategic technology projects in FY2020.

- One of the key focus areas of the bank’s people strategy is workforce empowerment and capability building. To ensure proactive capability building and systematic succession of employees into high responsibility roles, the bank should focus on:

- Moving from mandatory compliance learning modules to a more personalised training and knowledge delivery pipeline.

- Developing a platform-based learning ecosystem that connects people with the requisite information in real-time, thereby ensuring active value addition and capabilities expansion.

- Incorporating AI in training sessions will help the bank understand different learning styles and preferences, learning needs and aspirations, and the most effective pedagogical approaches. Such steps will further enable the bank to streamline and increase the efficiency of the staff training and learning processes.

- Pan-organisation training of both front-end and back-end employees in analytical-driven activities makes them future-ready for transition into AI and ML.

- ‘ThankQ’ is a reward and recognition program that stands to be a key enabler for rewarding excellence in performance and good behaviour. The bank can further use people analytics to check that unconscious bias does not unfairly impact promotion and compensation decisions.

- #5 Migration of workload to the cloud

- With the bank’s broader goal of transitioning its customers from old to new cloud-based core services platform, it needs to refactor the hybrid cloud strategy by optimising it with Infrastructure as a Service (IaaS), thereby making servers, software, data centre space, or network equipment as a fully-outsourced service.

- BOQ could focus on moving more of its operational activities to the cloud platform. The bank can incorporate customer behaviour analytics and customer relationship management into its cloud framework by leveraging the capabilities of its digital partner- Deloitte Digital.

- To fulfil its regulatory and compliance responsibilities and to protect customer confidentiality, the bank needs to keep sensitive data within firewalls and constantly revisit its cloud security approach. It could also retain sensitive data in the private portion of its cloud.

- #6 Neo banking

- BOQ witnessed a significant drop in Virgin savings account and Virgin credit card ratings, primarily due to long transaction time, complex application procedures, and long application approval time.

- The bank should aim towards making the application process efficient and simple by:

- Integrating customer data from its legacy banking channels and leveraging open banking to access historical customer transaction data and credit history

- Using the same data to automate the application approval process at the back-end. This step further help BOQ build a robust customer remediation process.

- The bank needs to revamp its fee structure. Such a revamp is especially meaningful for Virgin credit cardholders who pay off their credit dues on time to earn Velocity points yet are have annual fees and cardholder fees charged to them.

- Virgin money should also introduce GenZ and millennial-specific product ranges, like customisable credit and debit card designs, personalised saving accounts, and affordable student loans (for example, FRANK by OCBC has a wide array of design offerings. The bank charges USD 0 as its annual fee and offers affordable student loans and investment avenues. The product is made specifically for the more dynamic and quirky younger generation).

- To create a more immersive customer journey, the bank should move from its current minimalist and intuitive platform towards a more interactive, gamified and dynamic user interface.

- The bank can introduce interactive dashboards, create an online community or hub, blogs or resources on financial literacy, and introduce member badges and stickers to create a unique brand name for itself.

- #7 Artificial Intelligence (AI) in everything

- The bank needs to proactively use data-driven AI to personalise its reward programs-Velocity points and Virgin perks. It can do so by using predictive analytics to forecast its customers’ reward redemption preferences.

- This move can benefit the bank in two ways- it can increase customer engagement with Virgin Money Go accounts and improve its overall sale of financial products by gaining customer trust.

- The bank can use cognitive process automation (CPA) to automate labour-intensive processes, especially regulatory and compliance areas, to automatically screen and detect regulatory changes. This step could ensure that BOQ remains fully updated on the current compliance norms.

- To make its current data silos in the cloud conducive for analytics and algorithmic forecasting, the bank should filter and break down data into microsegments. This step would further help the bank understand its operational inefficiencies better.

- The bank can further use natural language processing (NLP) in deploying chatbot and automating customer application approval and processing.

- #8 Cybersecurity

- The bank needs to develop new risk capabilities to account for non-financial risk, especially with respect to black swan events like the recent case of Australian bushfires and COVID-19.

- BOQ needs to periodically redefine its risk appetite, detect both new potential risks and existing inefficiencies in controls, and devise a dynamic risk management approach accordingly.

- It can use advanced analytics and natural language processing (NLP) for credit underwriting to identify potentially high-risk accounts.

- An increased incorporation of AI calls for specific attention to account for a host of security concerns like privacy violations, erroneous automated processes, and discrepancies in model outcomes.

- #9 Society and planet contribution

- Considering the dynamic and extreme weather events (droughts and bushfires in Australia) of FY2020 and the COVID-19 pandemic, it makes it categorically imperative for the bank to lay a special focus on climate change and the environment.

- BOQ has already ceased funding equipment directly involved in the extraction of fossil fuels by 2023. So, to move towards building a roadmap to 100% renewable energy, the bank should consider setting clear sustainability targets for every clean energy project it finances.BOQ could devise a timeline to track the attainment of these pre-decided targets periodically.

- Paper usage is its most significant wastage. Apart from reducing paper usage through technology enhancements, the bank should ensure that it meets current and future paper needs with paper printed through carbon-neutral press machines and eco-materials.

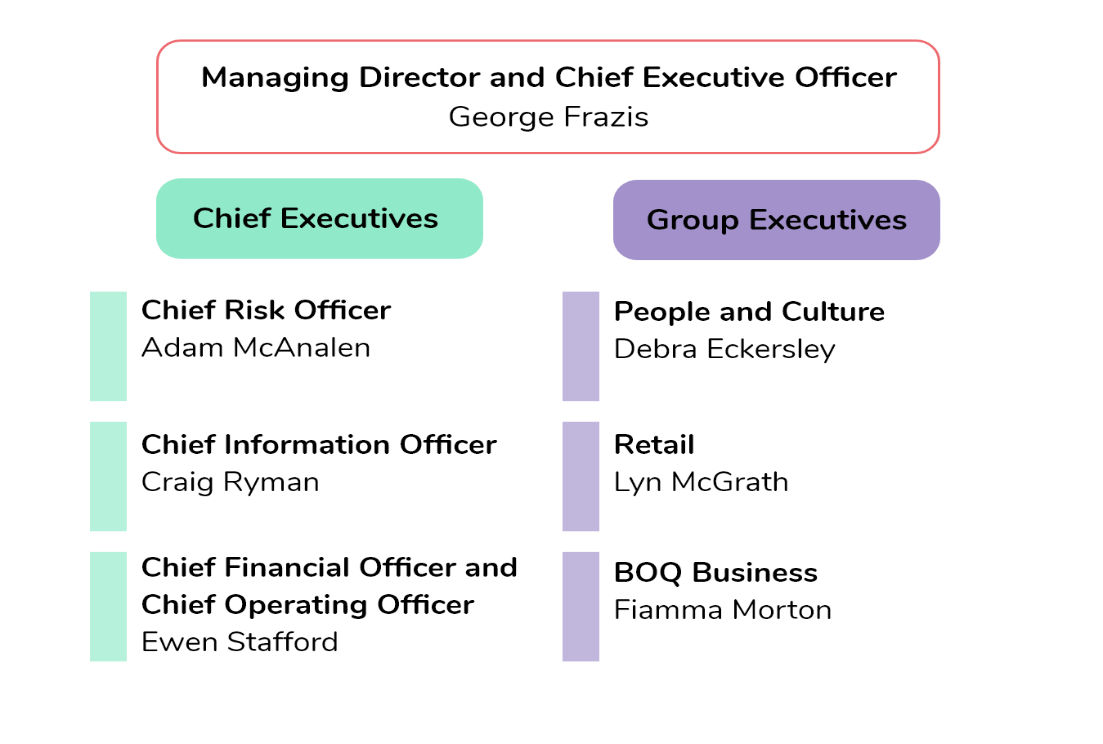

Organisation structure: Leadership

Executive Summary

George Frazis

Managing Director and Chief Executive Officer

George Frazis joined BOQ as its Managing Director and CEO in September 2019 and has over 26 years experience in corporate experience.

He has a long history in Banking and Finance, having worked in the industry for the past 17 years. Most recently, Frazis was Chief Executive of the Consumer Bank at Westpac Group. Prior to that, Frazis served as CEO, St. George Banking Group and Chief Executive, Westpac New Zealand Limited. He has held senior executive roles at the National Australia Bank, Commonwealth Bank of Australia, and Air New Zealand. Frazis started his career as an officer in the Royal Australian Air Force.

Quotes

- Employee experience, Annual Report 2020

As we responded to COVID-19, our internal focus was on ensuring our people could work safely and in new ways. Despite the challenging environment, the focus on empathy throughout the business saw employee engagement increase by 3 per cent during the year.

- Digital strategy, Annual Report 2020

The digital projects already completed are providing a strategic pathway for the Retail Bank’s migration to the digital platform. The VMA digital bank build will benefit from of an existing customer base and the support of the BOQ Group.

Adam McAnalen

Chief Risk Officer

Adam McAnalen was appointed Chief Risk Officer of BOQ in June 2019. Before he was appointed Chief Risk Officer, Adam held several senior leadership roles across the Business and Retail Banking, Finance, Operations and Risk divisions of BOQ.

His previous roles include CEO of BOQ Finance, CRO for BOQ Business, and General Manager Retail Credit, where he led the bank’s retail credit risk strategy, scorecards, decision-making, collection, and recovery operations.

Before joining BOQ, McAnalen held several senior Commercial and Business Banking roles at Westpac Banking Corporation. He has been a member of the bank’s Executive Credit Committee since April 2016 and is a signatory of the Banking Finance Oath.

Craig Ryman

Chief Information Officer

Craig Ryman joined BOQ as Chief Information Officer in July 2020. He has over 20 years of experience in financial services, leading technology transformation programs.

Ryman joined BOQ from AMP Limited, where he held Group Executive roles as Chief Information Officer and Chief Operating Officer. During this time, he had responsibility for critical business functions, including Technology, Operations, Strategic Sourcing, Corporate Real Estate, and Innovation. Ryman has a proven track record in transformational change.

Ryman is a well-regarded technology leader known for establishing visionary and innovative strategies that re-invent operating environments and future proof the foundations for a technology-enabled and customer-focused enterprise.

Ewen Stafford

Chief Financial Officer and Chief Operating Officer

Ewen Stafford joined BOQ as Chief Financial Officer and Chief Operating Officer in November 2019. He has more than 30 years of corporate experience across financial services, telecommunications, eCommerce and logistics, commercial property, and professional services.

Stafford joined BOQ Group from Deloitte, where he was a Strategy Consulting Partner and led the Banking & Capital Markets sector for Australia. Prior to this, he held executive roles across a range of ASX-listed private and government business enterprises, including Australia Post, Telstra, NAB and Loan Market/Ray White.

Stafford is a Fellow Chartered Accountant and a Fellow of the Australian Institute of Company Directors. He also holds a Master of Business Administration from the University of Adelaide and a Bachelor of Arts (Accountancy) from the University of South Australia.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Bank of Queensland Limited, (2020, August 31). Annual report 2020.

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/2020/annual-report-2020.pdf

Bank of Queensland Limited, (2020, August 31). Sustainability report 2020.

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/2020/sustainability-report-2020.pdf

Bank of Queensland Limited, (2020, August 31). Shareholder centre.

https://www.boq.com.au/Shareholder-centre/sustainability/adapting-to-change

https://www.boq.com.au/Shareholder-centre/sustainability/sustainability-people-and-culture#:~:text=We%20offer%20our%20employees%20a,online%20and%20onsite%20information%20sessions.

Vinayak Gandhi, Research Intern, contributed to the research in conducting a preliminary literature review and conceptualising the article.