With more than 630 branches and operations spanning 16 countries worldwide, CIMB is the second biggest bank in Malaysia. It operates in the 10 ASEAN countries, with Malaysia, Indonesia, and Thailand being the home markets, while having a strong presence in China, Hong Kong, the United Kingdom, India, the USA, and South Korea.

Operational efficiency at CIMB

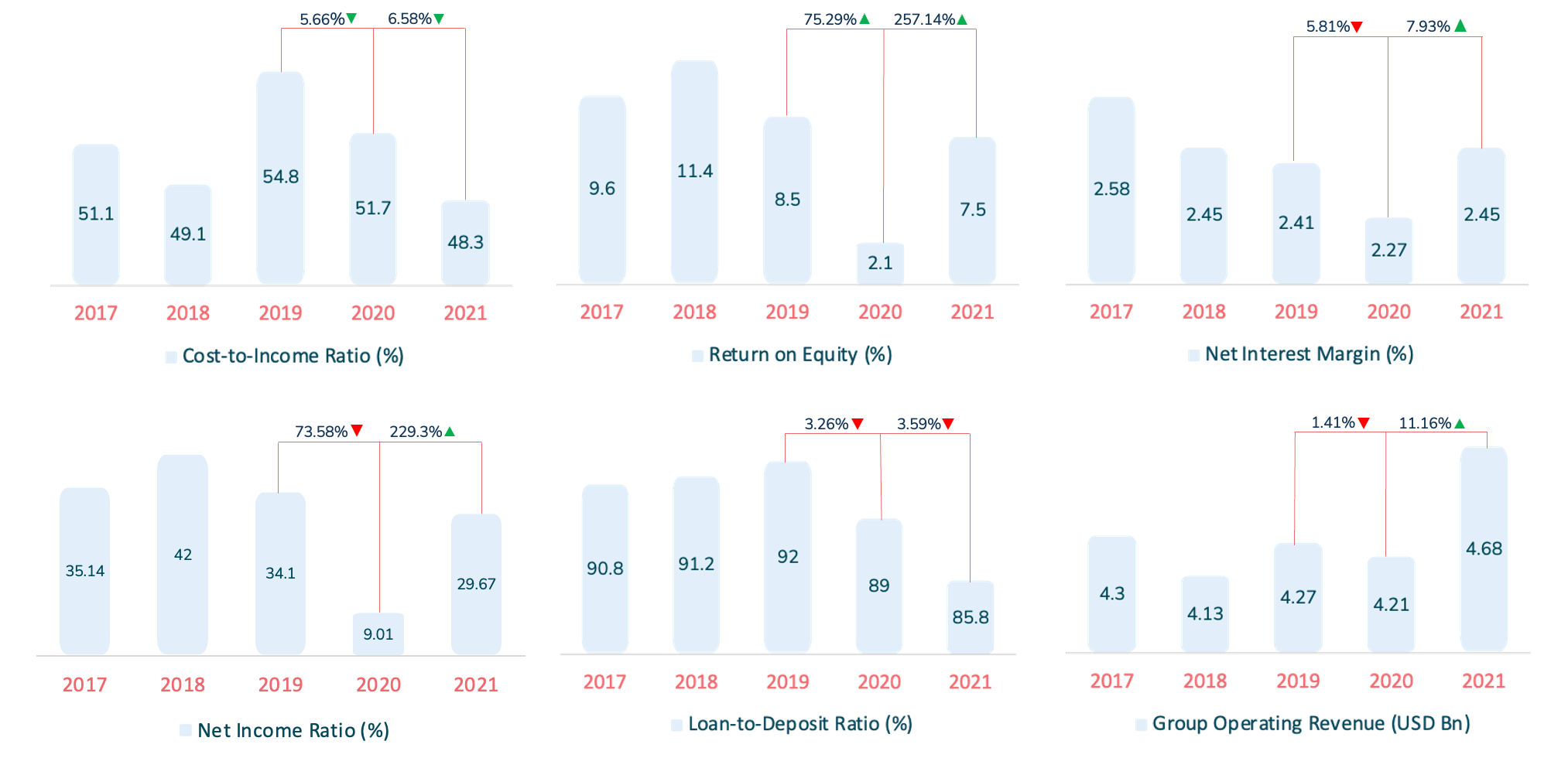

The decline of the LDR (loan-to-deposit) ratio by 3.59% from the previous year demonstrates a downward trend. Despite this, the LDR ratio is within the ideal range of 80%-90% (Figure 1).

With cost efficiency as the driving force, CIMB has achieved a record-low CIR (cost-to-income) ratio of 48.3%, improving by 6.58%. In 2021, Malaysian banks reported an average CIR ratio of 43.43, indicating that CIMB is slightly above the industry average.

CIMB’s ROE (return on equity) also significantly improved to 7.5% from 2021, owing to the bank’s focus on profitable markets and the recalibration of segments lacking competitive advantage.

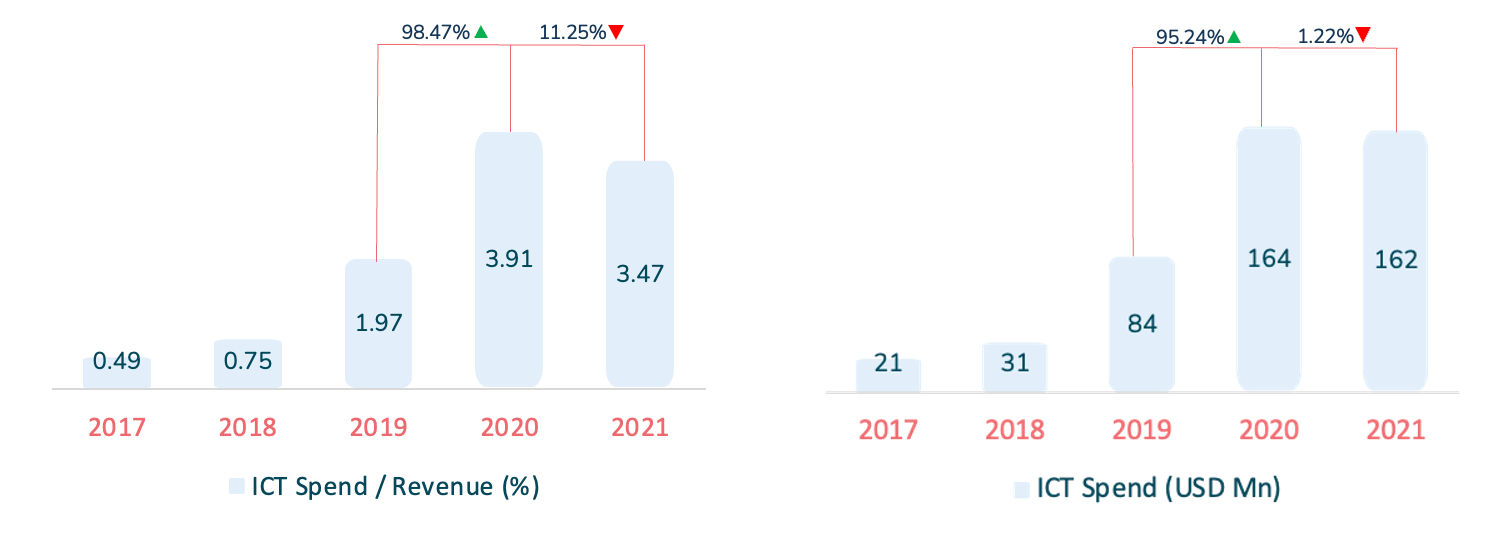

CIMB significantly increased its ICT expenditure in FY2020 from the previous year (Figure 2). The bank’s ICT expenditure appears to have stabilised between FY2020 and FY2021. This corresponds with CIMB’s digital initiatives in FY2020, which were more numerous compared to the digital initiatives in FY2021.

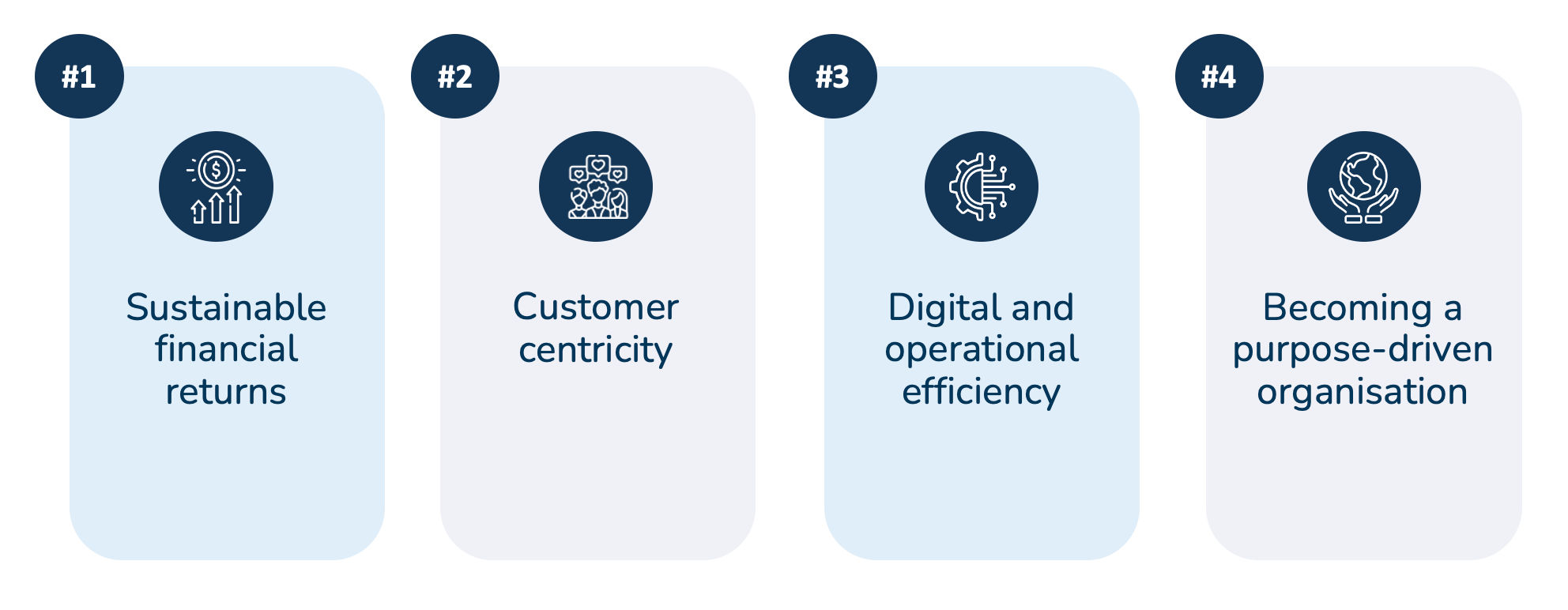

CIMB’s strategic focus areas

- #1 Sustainable financial returns

CIMB has lagged behind its peers in terms of ROE. Nevertheless, the bank persevered, focusing on core growth areas, which resulted in improved ROE.

Simultaneously, the bank continued to improve its digital financial services. Because of this, CIMB achieved strong digital engagement, increasing its total digital transactions by 47.4% year-over-year (YoY).

CIMB zeroed in on Preferred and Wealth customer segments by introducing new Islamic wealth management propositions with enhanced offerings. CIMB’s Preferred Islamic customer base recorded YoY growth of 25% through these initiatives.

- #2 Customer centricity

Customer centricity is at the heart of CIMB. To strengthen customers’ trust, CIMB has improved its turnaround time and service excellence and executed a more proactive approach to management for high system uptime and stability. Additionally, the bank invested in personalisation efforts to boost customer engagement through tailored segment-driven solutions.

- #3 Digital and operational efficiency

Aware of the paradigm shift towards digital transactions, CIMB recognised the need for digital and operational efficiency. Previously, the bank sustained technology and operational investments to focus on infrastructure and platform reliability. However, the perspective shift is precisely what CIMB needed to refocus its efforts in the right place.

The bank looks to change things up, prioritising proactive management and front and back-office process automation. Taking a step further, CIMB aims to upgrade their system, leveraging AI and ML for customer experience and anti-money laundering. With a digital-first mindset, CIMB’s future beams bright, with the bank expecting an increase in capital expenditure for continuous improvements in this segment.

- #4 Becoming a purpose-driven organisation

CIMB established the Group Sustainability and Governance Committee to provide stronger oversight of the Group’s sustainability journey. It also became the first ASEAN bank to join the United Nation’s Net-Zero Banking Alliance. Alongside this, CIMB mandated the acknowledgement of the Vendor Code of Conduct for new vendors.

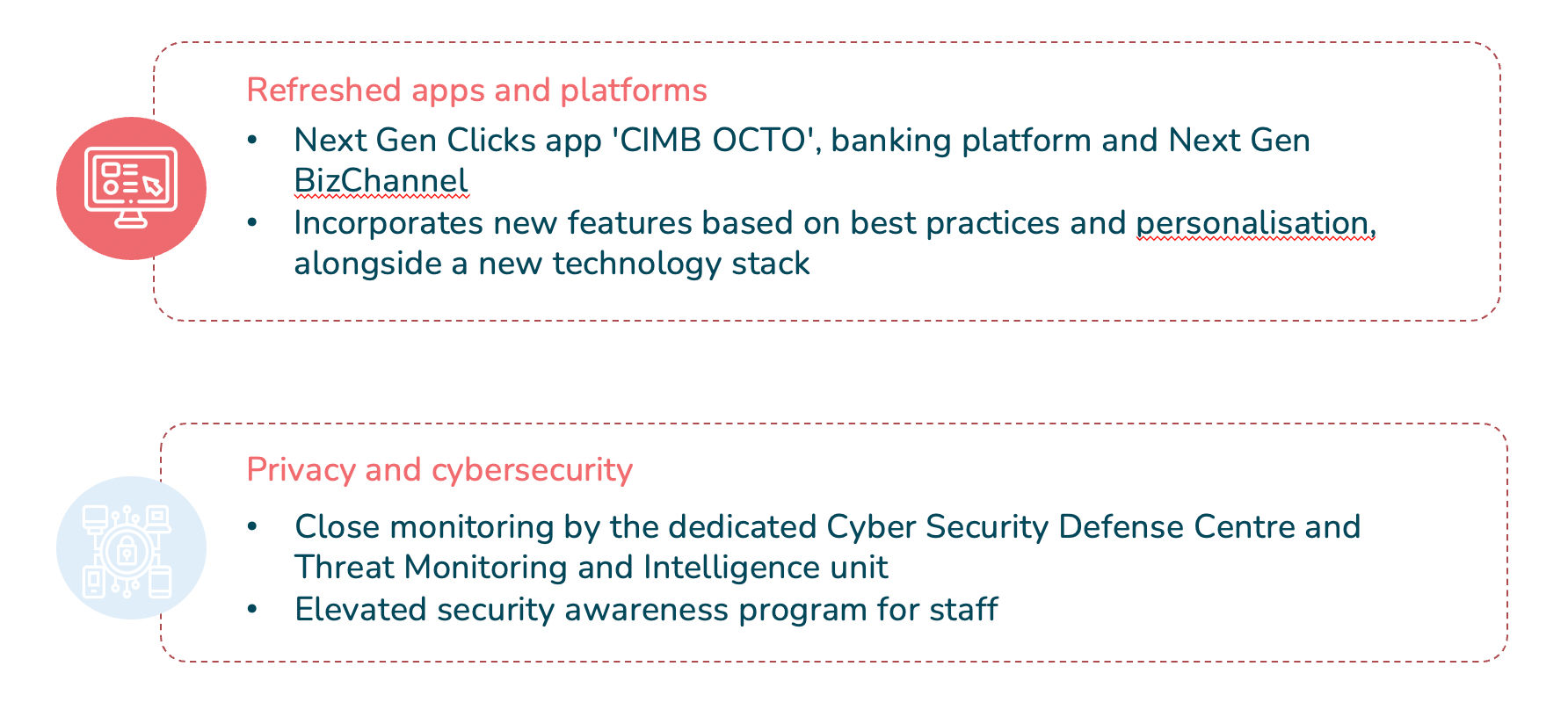

CIMB’s digital strategy

CIMB plans to deliver its digital strategy through the following (Figure 4).

CIMB’s technology innovation

- #1 OctoSavers-i

CIMB’s OctoSavers-i is the first fully digital savings account from CIMB. Launched alongside the new CIMB Octo Debit Mastercard, the account opening and onboarding process is done online under 5 steps, upon which the customer’s debit card is mailed directly to them. This ensures a convenient branchless experience. Additionally, users can earn points and instant rewards through a gamified experience (missions and challenges).

- #2 EVA chatbot for SME customers

EVA is the first conversational and real-time commercial banking NLP-powered chatbot in Malaysia. Its 24/7 availability provides SME customers with instant, consistent answers. The chatbot also functions as an electronic relationship manager, as its built-in Eligibility Check feature efficiently digitalises an otherwise long process of engaging with a sales representative.

Growth opportunities at CIMB

- #1 Customer experience

The bank increased its NPS by leveraging big data analytics for refined targeting and customer experience. CIMB also rolled out 70 personalised programs with approximately 20 million communications disseminated monthly to Malaysian customers.

Building upon this, the bank should enable fully online account opening journeys across all account types. Currently, this feature is limited to OctoSavers-i accounts.

Additionally, CIMB should incorporate personalised and predictive insights into its web platform and mobile banking apps to better meet customers’ needs. CIMB can also consider launching a lifestyle app to cover customers’ needs all under one hub.

- #2 Branch transformation

CIMB currently operates 630 retail branches across 8 countries, most of which are in Malaysia, Indonesia, and Thailand. In 2021, CIMB optimised the branch network by identifying underserved areas and fine-tuning the distribution of self-service terminals. The bank also leveraged geospatial analytics to plan current and future touchpoints.

Despite this, CIMB’s branch experience is still very much run-of-the-mill. The bank should explore innovative branch models to deliver a community hub experience, consequently boosting social engagement.

CIMB can go a step further, introducing robot-powered self-service branches and cardless ATM withdrawals for increased efficiency at retail branches.

- #3 Digitise for the future

CIMB is well on its way to a future-ready digital journey. The bank has leveraged Alibaba Cloud to empower digital transformation and is using the cloud to enhance the speed-to-market of digital and digitalisation solutions. On top of that, CIMB completed a core stack refresh and facilitated a transition towards cloud-based platforms.

CIMB should also widen its cloud capabilities throughout the bank, facilitating operational cost reductions. Following the footsteps of major Singaporean banks is an excellent start for CIMB to adopt a hybrid cloud strategy to catalyse innovation and enhance scalability.

- #4 AI in everything

CIMB has integrated AI and ML models in risk, fraud, and anti-money laundering efforts, in addition to utilising automation in enhanced decision-making and risk assessments. As a result, fraud prediction accuracy improved by 13%-15%, and CIMB reported a revenue contribution of approximately 6% from big data and advanced analytics to Malaysia, Indonesia, Singapore, and Thailand through acquisition, portfolio management, and personalisation initiatives.

CIMB can continue its efforts to integrate AI and ML into customer touchpoints. For example, CIMB can implement digital biometric customer verification, money management solutions, as well as savings and investment recommendations.

CIMB should also expand automation into other processes to increase operational efficiency, such as customer onboarding.

- #5 Open banking

As of writing, CIMB currently has two active API platforms which cater to Indonesia and Singapore. The former has been active since 2019.

In June 2021, CIMB Vietnam partnered with Finhay to launch a co-branded debit card with a virtual account. The account can be opened and maintained directly from the Finhay app.

CIMB has yet to fully capture the opportunity in open banking due to its limited rollout in specific countries. For example, the bank should expand its API sandbox access to Malaysia and Thailand or launch a developer platform that spans the MIST region.

Beyond open banking, CIMB should look into more opportunities for embedded finance through ecosystem partnerships within ASEAN.

Conclusion

CIMB is making steady progress in its growth journey, as witnessed by the bank’s financial performance recovery, where all financial profitability targets were either met or exceeded. Regarding customer experience, it has plenty of room to grow, with the bank’s performance only beginning to rebound. CIMB can concurrently explore new opportunities within enhanced branch experience and the open banking landscape.