Introduction

Apps like Swiggy, Uber, Dunzo, Urban Clap are building a connected ecosystem to cater all aspects a customer’s daily needs. We also see similar ease and frictionless experience now inspiring banking and financial services industry. New-age digital-only banks are building products and services around everyday customer journeys. These neobanks, as we know them, are bringing monumental change on how banking products and services are delivered, managed, and measured for their customers.

Customers want a banking experience the same way they order food over Zomato or book an Ola cab via a mobile app. Because neobanks operate similar to platform companies, their DNA is far more compatible with today’s fast-paced customer mindset than the incumbents. As new mobile banking application features and upgrades are released, greater convenience, speed and financial insights follow. And as customers ourselves, we want tailored, relevant content, a seamless omnichannel and gamified experience that continuously engages us at every touchpoint with our bank.

Neobanks are masters of change, embodying a customer-centric approach to building a hyper-personalised, integrated, and secure banking experience. The leaders of neobanks have a clear vision and are laser-focused on reshaping the customer banking experience. The goal – build immersive and frictionless experiences while educating customers with the right services and making it accessible throughout the journey. Harnessing the data and technology strengths creates interactive journeys.

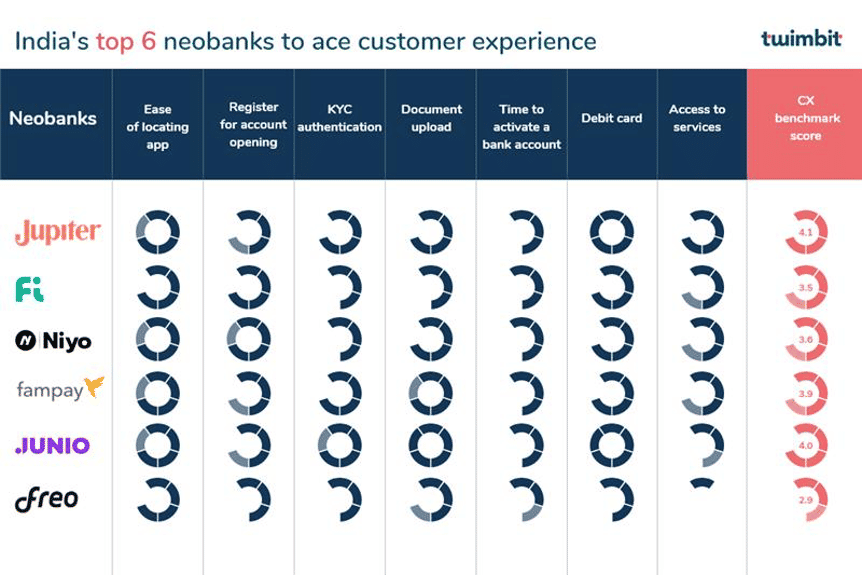

Our report outlines the best practices of the top 6 neobanks in India that ace customer experience (CX) and why they have become the customers’ bank of choice. We also want to assist Chief Executive Officers (CEO), Chief Product Officers (CPO), and business leaders of existing and upcoming neobanks grasp the importance of building a neobank on the principles of delivering exceptional CX.

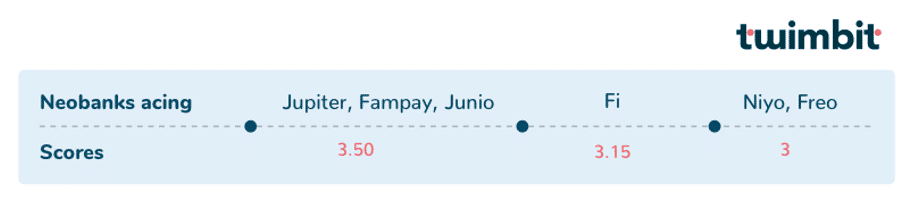

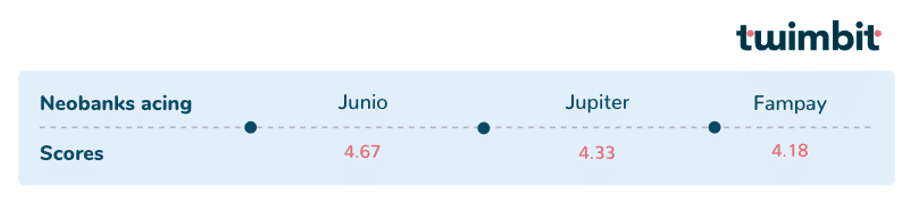

twimbit CX benchmark score for India’s top 6 neobanks

*Finin and NEO are yet to start with onboarding

Methodology

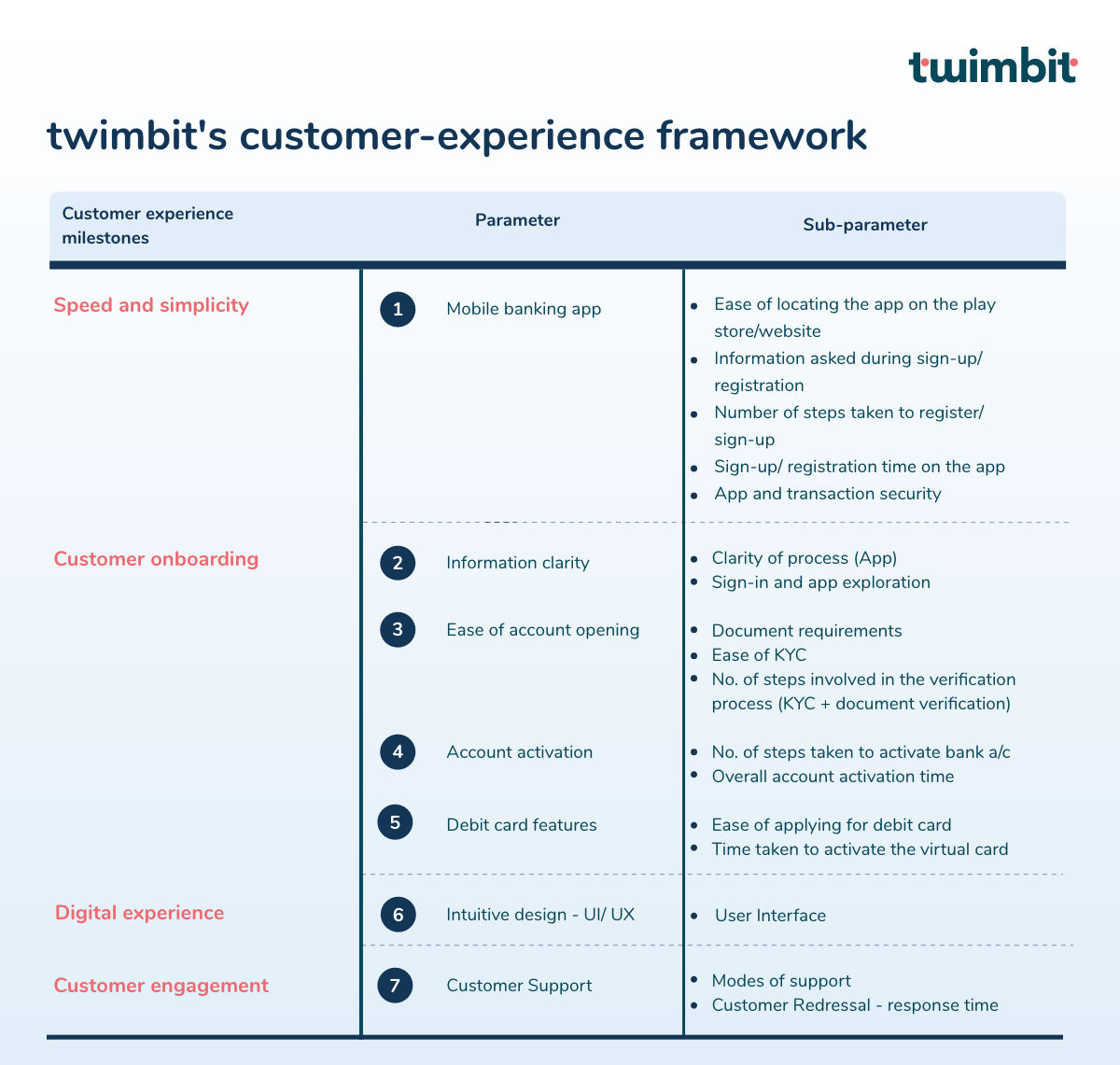

twimbit’s analyst team created 4 focus groups to open real accounts with 6 Indian neobanks offering retail banking services to evaluate their CX capabilities in the account opening and transaction processes. The customer journey comprises a 7-point framework covering 4 CX banking pillars of success for customer growth and engagement.

The 4 CX pillars

- Speed and simplicity

- Customer onboarding

- Digital experience

- Customer engagement

Step 1: Based on our analysis of 13 neobanks on our CX framework, we finalised the top 6 retail neobanks that ace customer experience in India.

Step 2: We developed a 7-point framework to help set the customer experience standard for neobanks across the country.

Step 3: We evaluated our neobanks across 7 parameters and 16 sub-parameters (Table 2) on a scale of 1 to 5, measuring their responsiveness to increasing customer expectations.

*Sub-attributes have pre-defined scaling for better distinction between a neobank’s services.

Critical customer expectations when it comes to digital banking experience are:

- Easy accessibility – Make banking apps easy to use and simple to access, resulting in frictionless onboarding, low abandonment rates, and seamless navigation.

- Real-time assistance – 60% of customers believe real-time support, such as humanised bots, remote phone calls and video chats, is crucial for instilling customer attention and loyalty.

- Personalised services – Banks should begin tracking customer journeys individually to build products tailored to customer needs because personalised services and relevant products hook customers.

- Data security – Customer security is paramount to building trust mechanisms, and banks can achieve this by communicating clear use cases of customer data and advocating the efficacy of digital banking.

A deep dive on 9 CX parameters for each of the 6 neobanks

- CX pillar 1 – Speed and simplicity

#1 Mobile banking app

We analysed the mobile banking app experience based on 5 sub-parameters

- Ease of locating the app on the play store/website

- Information asked during sign-up/ registration

- Number of steps taken to register/sign up

- Sign-up/registration time on the app

- App and transaction security

Our study indicates that all 6 neobanks have IOS and Android support. Moreover, finding these apps on the app store or play store has been a straightforward experience. Although, there are occasions when customers face difficulties in finding these apps, especially when they are different apps within the same neobank (NiyoX/Niyo Global or Freo Pay/Freo Save). Users here might need to search for the website to understand and overcome the issue.

Another critical aspect which we have discovered for a better customer experience is app size. The smaller the app, the more of a hit it is among customers, as it requires minimum download time with limited app permissions. For instance, the Junio mobile app on Android is about 20 MB, whereas the Fi mobile app on Android is the largest at 39 MB.

4 out of 6 neobanks ask customers to verify their mobile number via OTP or email identification. The neobanks could also ask customers to verify it via SIM card by SMS verification during the sign-up process. Meanwhile, neobanks, such as “Fampay” and “Junio”, execute customer verification through mobile numbers via OTP. The average number of steps taken to sign-up in a mobile banking app ranges between 4-6 steps, allowing customers to complete the sign-up process in approximately 2 minutes.

Security is the primary factor for neobanks. Banking applications must strive to enable a secure customer onboarding experience and protect personal information during every customer session on the app. The application should also be hacker-proof and immune to cyber-attacks. Currently, all neobanking apps offer biometric verification every time users sign in, whereas the Junio app has PIN-based sign-in, which diminishes the user experience.

- CX pillar 2 – Customer onboarding

#2 Information clarity

We analysed information clarity based on 2 sub-parameters

- Sign-in and app exploration

- Clarity of account opening and document uploading process in the app

New users should feel welcome; excited even at the prospects that the home page of a mobile app could deliver in terms of value. And if the first screen of the mobile app is a sign-up form, then maybe neobanks have got it all wrong. Rather than forcing new users to input their data or immediately sign up, the app must demonstrate its value and allow users to explore its features freely before registering. Currently, all six neobanks do not allow users to explore the app before signing up.

In addition, neobanks need to be more straightforward in the account opening process. Our report indicates that only 4 of the 6 neobanks explicitly underline the necessary steps. Ideally, banks should cover all aspects, such as the number of steps, types of documents needed, and other areas before a user starts the account opening process.

#3 Ease of account opening

We analysed ease of account opening based on 3 sub-parameters

- Document requirement

- Ease of KYC

- No. of steps involved in the verification process (KYC + document verification)

Verifying the customer’s identity is a critical factor in building a sense of security and trust with the neobank. There are various types of KYC authorisations that a neobank uses:

- At-home verification by agent

- Digital KYC (Live photo + Photos of the officially valid documents)

- Digital KYC + Aadhaar based eKYC

- Video KYC

- Aadhar based eKYC

Irrespective of the KYC authorisation type, customers must submit their identity proof for verification. Most neobanks require a maximum of two identity documents: the Aadhar card and the Pan card. Certain banks can fetch Pan card or Aadhar card details through the mobile number; in this case, the customer only needs to upload one of the two documents. Some banks require additional documents, such as a driving license, voter ID, and passport, for verification.

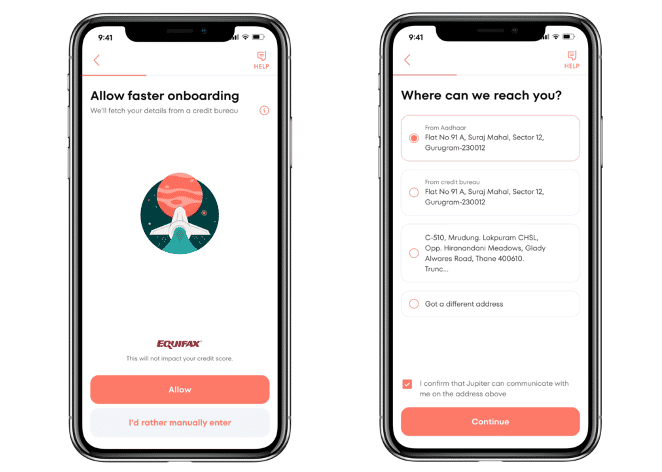

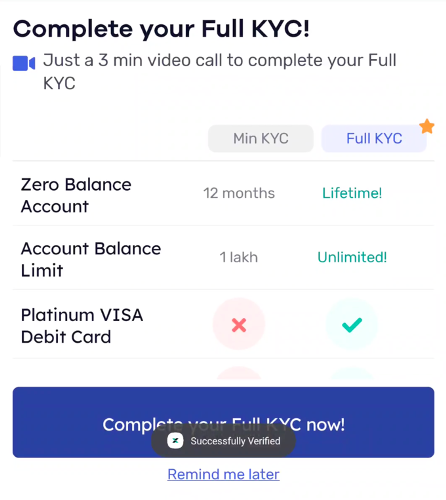

Frictionless KYC authentication happens by linking the mobile number with an Aadhar card or Pan card and obtaining details from the centralised database. This level of authentication removes the step for the customer to upload documents onto the app. Instead, an OTP verifies the auto-fetched details. Fampay and Junio only require Aadhar and PAN card details for verification, making KYC verification a seamless process for their users.

In contrast, Fi and Freo’s KYC verification process is quite challenging as the user needs to click a selfie, read numbers loudly, etc. Then, the stinger – all these steps are for partial KYC, in which the user later gets an option for full KYC via Video KYC or scheduling an agent visit.

Post-registration takes less than an hour to a maximum of 5 working days for a neobank to verify its customer’s details and activate the account for services. All neobanks offer non-chargeable zero-balance accounts with the ability to start transacting instantly. In addition, the customer can top up their account using any of their existing accounts, incentivising the customer to make the neobank their primary transactional account.

The key success measure for a neobank lies in its capability to support account registration, KYC verification, and account activation within 5 minutes.

#4 Account Activation

We analysed account activation experience based on 2 sub-parameters

- Total number of steps taken to open a bank a/c

- Overall time taken to activate a bank account

A customer can experience the most friction while registering to open an account. On average, it takes 4 – 10 steps to register for a neobank account. However, registration for an account does not necessarily enable account activation. An account is active for transactions and benefits after customer verification happens digitally, offline or both.

Based on the analysis, Fampay and Junio execute the overall account opening process in less than four steps, while Fi and Freo involve more than ten steps. Ideally, neobanks should target to complete their account opening process with activation within an average of 6-8 steps.

These steps include registration on the app, filling out information and uploading identity documents for verification. According to the analysis, it currently takes an average of less than 5 minutes to open an account.

There are instances when an account registers in less than two minutes, regardless of the number of steps. For example, Fampay and Junio take only 2 minutes for an account to open and activate (both these neobanks are focused on the teenage demographic and require less information and documents).

#5 Debit card features

We analysed debit card features based on 2 sub-parameters

- Ease of applying for debit card

- Time taken to activate the virtual card

A customised card, a metal card, and a portrait card are some of the choices the customer can avail of, and it also depends upon what the bank offers its customers.

The choice to choose a different material besides plastic appeals broadly to the millennials and the GenZ population, as they are susceptible to the extensive use of non-environment-friendly materials and their carbon emissions. As a result, virtual cards and metal cards have become extremely popular in these segments, with neobanks charging for physical cards to promote environmental sustainability and digital transactions.

Today, most neobanks provide a virtual debit card immediately after the account opening process is complete. The availability of a virtual debit card with instant activation and clear CTA to apply for a physical debit card on the same landing page provides a seamless user experience..

Based on our analysis, all neobanks provide virtual debit cards with instant activation after the account opening. On the other hand, 5/6 neobanks give a clear CTA to apply for a physical debit card on the same screen, unlike Freo, as it is still under the process of providing an option to apply for a physical debit card.

- CX pillar 3 – Digital experience

#6 Intuitive design – UI/ UX

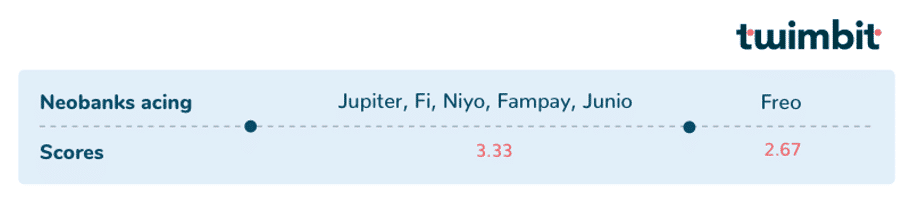

Jupiter and Junio ace the digital experience with their quirky design and graphics, interactive features, visual aesthetics, and easy flow, whereas the Freo app has an average layout but clear CTAs.

A well-designed mobile banking app is the first thing customers evaluate when interacting with the it. But how can banks provide customers with a user-friendly experience that meets all their needs? The following tips will help neobanks do that:

1. Let users customise the app interface

Users may customise the app’s user interface (UI) and user experience (UX) to meet their demands. For example, allowing users to pick their preferred text size and icon positioning will enable them to engage with the app software in the most comfortable way possible.

2. Provide an omnichannel experience

Users may access banking information on various devices, including smartphones with different screen sizes, tablets, and smartwatches. This level of access provides a seamless user experience across different devices, enabling customers to pick up from where they left off.

3. Make the user interface as basic as possible

Complex data and functionalities are often present in online banking applications. The capability to create a basic and minimalist design that organises design components helps to avoid overburdening the application interface. This design requires banks to understand which functionality is important to customers, so you can design straightforward interphase that suits your customers’ needs.

4. Make a trendy and appealing design

Users tend to form a first impression in 50 milliseconds. Therefore, create a contemporary and aesthetically engaging interface design to guarantee a favourable first impression and a smooth user experience. Avoid overcrowding the interface with pictures, symbols, and text while creating a financial app which can confuse users and make navigation more difficult. Banks should seek to maintain a sense of equilibrium, as it is the most important guideline of modern and attractive design.

- CX pillar 4 – Customer engagement

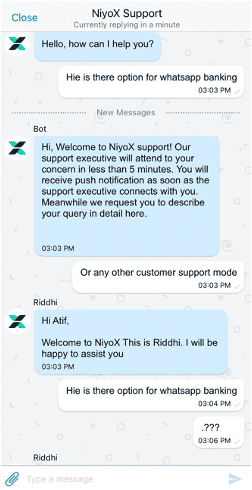

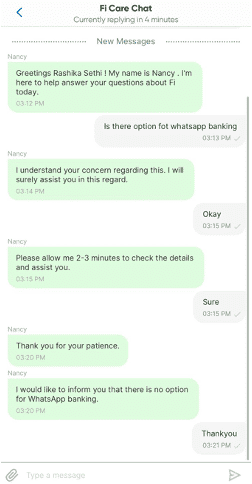

#7 Customer Support

We analysed customer support experience based on 2 sub-parameters

- Modes of customer support

- Customer redressal – response time

You no longer have to be held up in phone queues or read through long pages of FAQs; chatbots and real-time virtual assistance are drastically changing how neobanks interact with customers. Virtual assistance in banking brings convenience, speed, reduced friction, and powered accessibility to customers. The fascinating thing about it is perhaps the ubiquity and ease that it brings. Banking assistants can be available 24×7 and across multiple channels such as WhatsApp, Facebook Messenger, and emails.

In our study, Fi has the maximum number of customer support options including concern wise FAQ section, quick guides, call and chat whereas Freo just offer FAQ as a support option for the customer.

Another hallmark of poor customer service is the untimely responses to customer requests. Customers want to feel valued and know their business is appreciated. Therefore, customers will likely move elsewhere if they feel neglected.

Jupiter chatbot response fastest in terms of support. It also offer options of frequently asked queries to save time and increase efficiency.

Conclusion

The advancements in technology have taken user experience to a whole new level. One of the biggest challenges for banking is creating and developing a banking ecosystem that organically presents numerous products and services in a flow. The idea is to embed multiple add-ons to the banking platform to serve the customer’s needs.

Open banking has enabled neobanks to gain customer data and availed a wide range of opportunities to provide additional services and products, resulting in added value to the customer. The next step for neobanks is to embrace the SUPERAPP strategy that drives embedded experiences and widen the spectrum of wallet share between the neobank and the third party partner.

References

https://life.jupiter.money/opening-a-jupiter-account-a-behind-the-scenes-look-at-design-5e7bb4cd6347