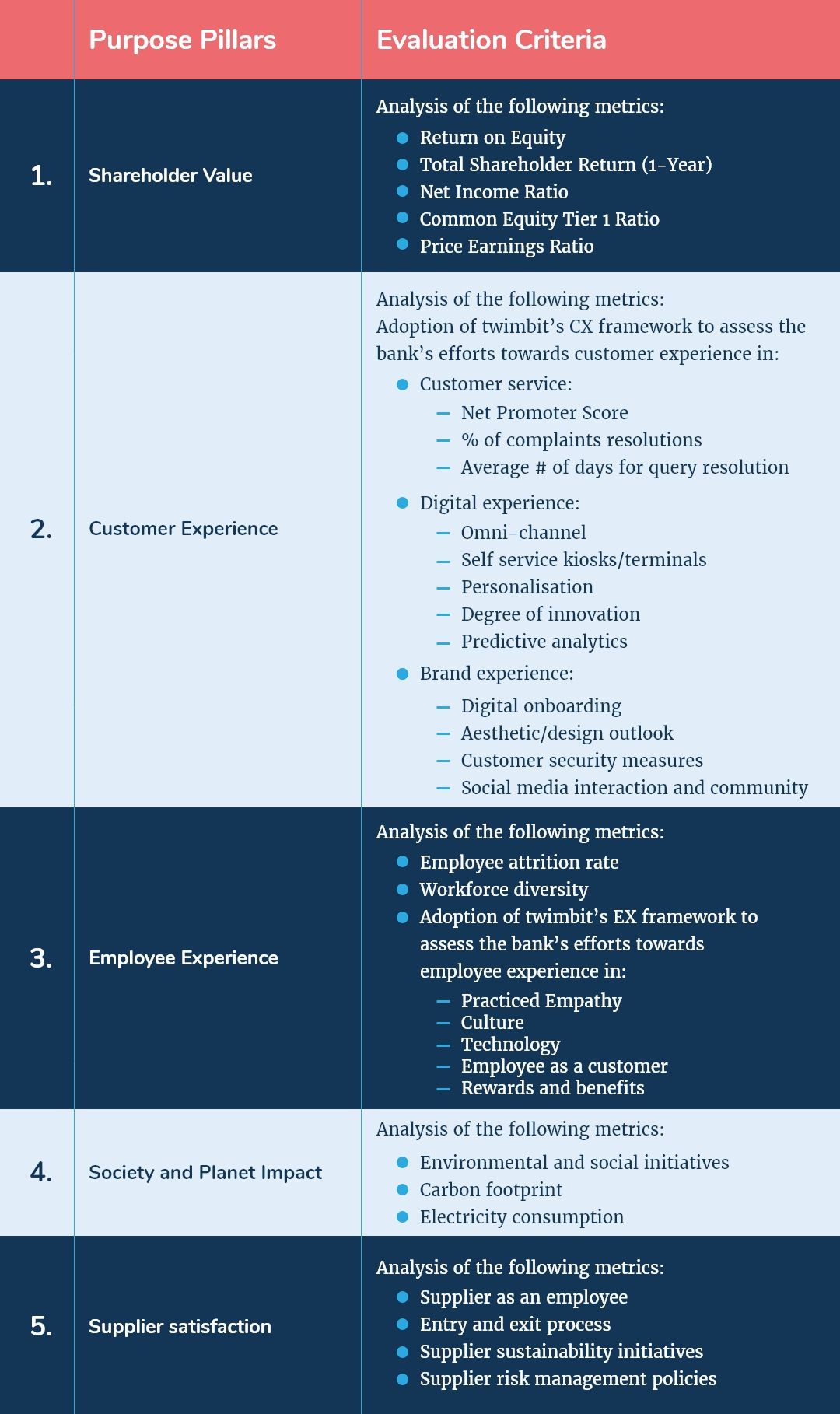

Company Insights

twimbit Purpose Benchmark

Source: Refer to the methodology in Appendix A below

DBS Group Holdings Ltd (Group financials) – An overview as of 31st December 2020

| Bank Name | DBS Group Holdings Ltd (DBS) |

| Headquarters | Singapore |

| Operating income (31st December 2020) | USD 11.04 billion |

| Net Profit after Tax (31st December 2020) | USD 3.57 billion |

| Total Assets | USD 488.8 billion |

| Number of employees | 29,000 |

| Countries of operation | 18 |

| Number of branches | 280 |

| Information and communication technology (ICT) spending (31st December 2020) | USD 827.1 million |

| Singapore’s Bank Ranking | 1st* |

| Number of customers | 10.94 million |

| Market capitalisation (31st December 2020) | USD 56.21 billion |

| Operating revenue CAGR growth (2016-2020) | 4.89% |

*Ranking source: CFI Institute

Shareholder value (31st December 2020)

| Return on equity (31st December 2020) | 9.1% |

| Total shareholders’ return – 1 year (31st December 2020) | 1% |

| Net income ratio | 32.32% |

| Common equity Tier 1 ratio | 13.9% |

| Price earnings ratio (31st December 2020) | 12.1% |

Awards

| 2020 | Global Finance: – Best Bank in the World 2020 – World’s Best Treasury and Cash Management Banks and Providers – Best Application/Use of Digital Technologies, in Treasury Management – Best Virtual Accounts Solution for Corporates |

| 2020 | Euromoney: Awards for Excellence: – Best Bank–Asia – Best Bank for Transaction Services – Asia |

DBS and its strategic focus area

For overall coverage, DBS adopted a 40-20-40 structure. The first 40% percent involved strategies around the key stakeholders, i.e., shareholders, customers, and employees. The next 20% had strategies around the digital transformation of the bank. The remaining 40% had the bank design strategies around the remaining key focus area. DBS also dialling up market coverage around new growth areas like digital platforms, start-ups, and growth companies.

- Customer experience

DBS focuses on creating joyful banking experiences for their customers. To achieve this objective, the bank zeroes in on customer needs and financial behaviour. The bank looks at their customer journeys from beginning to end and applies human-centred designs to develop relevant solutions. DBS believes that embedding themselves in the customer journey and embracing digital is a potent combination that will make banking increasingly simple and seamless. DBS aims to:

- Increase digital acquisition of customers and grow their digital channel share.

- Move towards hyper-personalisation by strengthening data analysis and AI capabilities.

- Grow and leverage ecosystem partnerships to provide invisible banking.

- Solidify the wealth management position in Asia through digitally engaged customers and by using onshore/offshore model.

Initiatives taken by DBS to enhance the customer experience in 2020 are:

- Launched NAV Planner in Singapore, an intuitive financial tool that has delivered more than 30 million hyper-personalised insights to customers using AI and predictive analytics.

- Boosted data platform with automation capabilities.

- Leveraged advanced analytics to offer personalised services to their customers.

- Enhanced the digital retail account opening process by reducing the number of clicks required to open an account from 27 to 15 clicks. This reduction makes the process the fastest in the Singapore banking industry.

- Launched the world’s largest banking API.

- Employee experience

The diversity of their employee’s experiences bolsters success for DBS. The bank believes that every individual possesses unique strengths and perspectives, all of which add value to their work. The bank empowers employees to pursue their varied interests, both professionally and personally.

The bank’s focus is to maintain employee engagement levels by:

- Driving a learning and development organisation to create a future-ready workforce

- Building a culture for employees to embrace innovation

- Promoting internal mobility, job rotations, cross-functional projects, and other experiential learning opportunities

- Giving greater flexibility in respect of required time and hours of work

- Training employees in emerging areas, such as design thinking, data and analytics, artificial intelligence (AI), machine learning (ML), and agile practices.

Initiatives taken by DBS to boost employee experience:

- Upskilling and reskilling their workforce for the future by launching an in-house digital training, ‘Future Tech Academy’, to keep the technology workforce updated with relevant cutting-edge skills.

- Helping employees boost their morale through a series of programmes to address their physical, emotional, and mental well-being by launching DBS’ TOGETHER movement.

- Organising a series of large-scale virtual learning events to promote continuous learning among the workforce to equip employees with skillsets of the future. DBS organised more than 120 learning sessions in 2020.

- Encouraging a culture of experimentation and thereby removing the stigma of failing—by giving awards for failing.

- DBS continues to democratise technology skill sets among employees. Over 18,000 DBS employees have completed data training, more than 3,000 employees of which have done the fundamentals of Artificial Intelligence (AI)/ Machine Learning (ML) through Amazon Web Services (AWS) DeepRacer, a gamified learning platform.

- DBS ensures fair financial value distribution among their employees through a 13% discretionary bonus paid to the employees via variable cash bonus and short-term incentives

- Organising innovative recruitment events such as Hack2Hire, Hacker-in-Her, and Paradigm Shift.

- These challenges help the bank recruit coders skilled at managing emerging and disruptive technologies across the cloud, ML, and big data.

- Society and planet impact

As a bank with extensive operations across Asia, it is crucial for DBS to manage their environmental footprint. As the bank grows their franchise, it is committed to conducting business more sustainably by incorporating innovative and simple-to-apply solutions to banking operations.

The bank is committed to minimising their environmental footprint by reducing consumption and improving overall efficiency:

- Building sustainable infrastructure:

- The bank is taking steps to enhance the existing measurement system to incorporate real-time energy monitoring and added data collection for its building operations

- 100% of DBS Singapore branches are Building and Construction Authority Green Mark Certified, with 62 branches certified as Green Mark Gold and above (as of 31 Dec 2019).

- As the first Asian bank and Singapore company to join the global renewable energy initiative, RE100, DBS has committed to utilising 100% renewable energy in all their markets, with an interim target of the same 100% in Singapore by 2030. To meet this commitment, DBS has adopted a four-prong approach to overall renewable strategy:

- Drastically reduce consumption by:

- Reducing energy consumption

- Transforming their space design

- Producing renewable energy wherever possible

- Purchasing renewable energy for energy needs

- Purchasing Renewable Energy Certificates (RECs)

- Drastically reduce consumption by:

- Branch transformation and branch network

Over the past years, DBS has consistently invested in technology platforms to become digital to the core. They aim to enhance customer satisfaction, experience, and engagements, making banking simpler, faster, and more intuitive. DBS has observed a trend where customers skew towards digital banking, with 95% of banking transactions done via the DBS digibank app or online. In November 2020, DBS announced their branch transformation across Singapore to provide customers with socially distanced and more personalised branch banking services:

- DBS planned to provide a phygital banking experience to their customers by boosting their self-service options while still providing face-to-face assistance and consultation. This plan will enable customers to complete more complex transactions, such as replacing their ATM or debit cards, outside traditional banking hours.

- DBS launched a lifestyle space for the tech generation, where digital banking and human connection complement one another. The branch has a “café and branch” concept, which features:

- An open layout, creating a relaxed atmosphere for customers with a café at the entrance.

- An industry-first VR corner for retirement planning, where customers get guidance on how to work towards their retirement lifestyles.

- Video Teller Machines (VTMs) or Branch Teller Machines (BTMs), enabling customers to complete more complex transactions safely and securely without human intervention.

- A humanoid robot, “Pepper”, to guide customers on how to use VTMs.

- A wealth planning manager who will provide personal financial planning consultations to help customers achieve financial wellness.

- The bank is planning to digitalise at least one-third of the bank’s branch network across all regions in the next 12-18 months.

- DBS is committed to supporting and serving those who are less digital savvy, including the elderly. As a result, DBS will continue to carry out workshops and literacy programmes to educate seniors on digital banking.

- Financial inclusivity

Through innovation and digital technologies, DBS has increased access to financial services, especially to traditionally underserved populations. The access includes extending credit to the previously unbanked and disbursing funds through mobile phones. The bank gives customers insights, knowledge, as well as access to data and easy banking, which empower DBS customers to make financial decisions on their own.

DBS has taken various initiatives by employing innovative digital solutions and forming strategic partnerships to serve the unbanked population, such as:

- Used data analytics to approve small ticket-sized loans at a faster pace online.

- Partnered with the Migrant Workers’ Centre and Centre for Domestic Employees to assist migrant workers in opening an online bank account, thereby ensuring timely salary crediting and fund remittances to their families back home.

- Launched POSB Smart Buddy, the world’s first in-school wearable savings and payments program. Since its launch in 2017, more than 60 schools and 28,000 students have onboarded the programme in Singapore.

- Cybersecurity

As banks continue to push the digitalisation of banking services, cybersecurity is one of the key risk concerns, including protecting systems and applications, as well as safe and secure delivery of internet and mobile services.

- DBS has a cybersecurity programme based on widely adopted security standards to provide the breadth of the control coverage. This programme is complemented with a cyber threat framework to provide the technical depth that ensures control effectiveness.

- The bank has multiple senior committees, such as the Group Operational Risk Committee, Risk Executive Committee, and the Board Risk Management Committee. The said committees provide oversight on cybersecurity risk matters.

The bank has taken the following initiatives to strengthen cybersecurity:

- DBS enhanced security monitoring and surveillance of malicious online activities, as scammers migrated to cyber measures, such as phishing, to defraud customers. Throughout 2020, DBS shut down 210 phishing websites, with more than 87% taken down within 48 hours.

- The bank delivered a general security awareness programme to more than 24,000 employees via the Information Security e-learning platform. CybrFIT, a gamified security awareness training, further augmented this annual training programme. The said programme delivered up-to-date security advisories and bite-size training on emerging and prevailing cyber threats.

- DBS invested in ML capabilities and security orchestration in a bid to stay ahead in the cyber-arms race, which enabled the team to heighten the monitoring of cyber threats events within their current level of resourcing.

- The bank implemented strong, multi-factor authentication and micro-segmentation to secure internal access to key applications and limit attack surfaces.

- The bank further developed their in-house:

- Risk-based vulnerability management programme to improve cyber risk prioritisation and mitigation efforts

- Crowdsourced cyber threat intelligence platform to provide predictive analysis of potential cyber threats and attacks.

Digital Strategy

DBS operates as a technology start-up company rather than a bank, keeping digital at the forefront of doing business, managing people, and driving sustainability. The bank follows a continuously evolving culture of building applications to keep pace with changes.

- DBS is driving automation in selected retail and corporate processes by improving straight-through processing and delivering instant fulfilment to the customers.

- DBS is incorporating data-driven decision-making and optimising end-to-end workflow processes.

- To strengthen the data infrastructure, implement a robust data governance framework, and become a data-driven bank, DBS has taken the following initiatives:

- DBS introduced data-driven operating models into management processes that incorporate data ingestion, access, and analytics protocols. These models enable the scalability of data capabilities in a coordinated and structured manner.

- DBS launched DBS Digital Exchange – the world’s first cryptocurrency exchange backed by a bank.

- DBS NAV Planner launched as one of the world’s most advanced financial planning solution. It leverages tech to democratise financial planning, thereby helping all Singaporeans better manage their money and grow their wealth.

- DBS launched an in-house human-robo advisor, DigiPortfolio, primarily for its wealth customers and consumer banking customers. It taps into financial expertise and investment opportunities.

- DBS has a chatbot driven by AI and ML capabilities. In 2020, DBS upgraded the chatbot by adding Natural Language Processing capabilities, allowing the chatbot to understand and process two languages (English and Traditional Chinese). Due to this, the Chatbot usage volume increased from 350,000 to 400,000 unique conversations, with 82% of requests self-fulfilled by customers.

- DBS is rolling out more self-service banking machines, such as Video Teller Machines (VTMs) or Branch Teller Machines (BTMs). The rollouts enable customers to complete more complex transactions safely and securely.

- DBS has also established the Platform Operating Model to future-proof its business and increase the agility of business outcomes.

- The bank uses digitalised and simplified end-to-end credit processing for advanced credit risk management using a combination of on-demand cloud-native design, analytics, and ML.

- In FY 2019, the bank launched DBS MAX, a seamless and instant payment collection solution for merchants across Singapore, Hong Kong, and India. DBS MAX saw rapid adoption of the solution, with more than 7,000 merchants generating approximately 200,000 transactions over a short 10-month period.

- The convenient payment and collection solutions for customers have reduced physical cash transactions, with retail banking and corporate banking achieving reductions by 14% and 23% in such transactions at DBS branches, respectively.

IT Strategy

DBS spent USD 827.1 million to strengthen their IT infrastructure. DBS has an “innovation radar” based on nine big themes. The set of disruptive trends and technologies include blockchain, AI, and multi-cloud adoption, which creates an ecosystem for constant innovation.

Initiatives by DBS in 2020 to strengthen their IT infrastructure include:

- DBS conducted end-to-end tests on contactless ATM and Video Teller Machine (VTM). The 5G contactless ATM combines different technologies that eliminate the need for physical cables and can have its place anywhere. With contactless VTMs, customers can be authenticated via facial verification using biometric data instead of an ATM card or PIN.

- DBS accelerated process automation through the OPPR (Operations Processes and Platform Re-engineering) programme, which enabled Straight-Through-Processing capability with 8% productivity saves year-on-year. This automation further helped the bank support increased processing volumes with the same staff strength over the last five years.

- DBS rearchitected backend and middleware layers of their operations in five key areas: Cloud, Blockchain, Data Analytics, AI/ ML, and Site Reliability Engineering (SRE):

- Cloud: DBS made a move towards a hybrid multi-cloud infrastructure from a virtual private cloud. The bank’s 99% applications are under cloud support. This migration helped DBS enable greater agility, reduce infrastructure costs, and improve the resiliency and scalability of apps.

- Blockchain: DBS will leverage blockchain technology to provide an ecosystem for fundraising. This ecosystem happens through asset tokenisation and secondary trading of digital assets through the DBS Digital Exchange. The bank has formed a new blockchain company along with JP Morgan and Temasek to co-create blockchain based platform for supporting use cases such as s FX Payment Versus Payment (PVP), Delivery versus Payment (DVP), Peer-to-Peer escrows, and even complementary services for Central Bank Digital Currencies (CBDCs)

- Data Analytics: DBS ADA (Advance DBS with AI) can handle high volume data easily. DBS has created a library of reusable assets for AI/ ML models and analytics to reduce the time and effort to deliver ML deployment and shorten the deployment lifecycle. This library facilitates DBS towards creating customer-driven investment recommendations and hyper-personalised banking.

- Machine Learning: DBS implemented predictive analytics through ML to aid in automating the capacity planning for critical systems. ML also improved traceability, detection, and recovery capability through quicker identification of bottlenecks in customer journeys. In 2021, the bank will focus on SRE-driven auto error remediation, predictive chaos testing, and capacity management.

5 Growth and Innovation opportunities

- #1 Cost to serve

DBS has a cost-to-income ratio of 42.2%, which is slightly higher than the industry average of 40%. DBS has reduced their cost-to-income ratio by 2.5% from 2016 to 2020, indicating that the bank is trying to maintain this ratio as low as possible. The relatively higher cost efficiency is due to a reduction in interest income during the pandemic phase.

The bank has dealt with a massive 6% drop in their net interest income. The reasons are as follows:

- Consumer Banking/ Wealth Management

- Total income declined by 8% to USD 4.36 billion. This drop was because of lowered interest rates, as well as low bancassurance and card fees (moderated by higher income from loans, deposit growth, and wealth management sales).

- Institutional Banking

- Total income declined by 5% to USD 4.34 billion, as the impact of lower interest rates more than offset higher income from loans, and treasury customer flows.

- Treasury Markets

- Income increased by 54% to USD 1.08 billion due to higher contributions from the interest rate, equity, foreign exchange, and credit activities.

- DBS total deposits rose significantly by 15% to USD 351.7 billion, reflecting their leading savings deposit and cash management franchises enhanced by digitalisation capabilities.

- DBS expenses were 2% lower at USD 4.65 billion as spending on general expenses, such as travel and advertising, declined. Staff costs stood at USD 2685 million, 27% of its total revenue as of December 2020. The costs slightly changed with an increase in base salaries due to a higher headcount offset by lower bonus accruals and government grants.

- The typical digital customer segment, which increased by 6 percentage points to 78% from 72% in 2019, drove the bank’s income significantly.

- There is an opportunity for DBS to manage their income in the low-interest rate environment by:

- A sound net interest margin management in a low-interest rate climate is achievable by identifying repayment risk in loans and attrition risk in deposits. DBS can use predictive behavioural models to revise their interest-rate risk models and hedging strategies continuously.

- Monitoring their contribution to operational profitability from non-interest fees and income from other sources closely.

- #2 Customer experience

DBS is continuously hunting for ideas to enhance customer experience. The bank has taken many initiatives to improve customer experience. These initiatives help the bank in increasing their overall customer engagement score (CES):

| 2019 | 2020 | |

| CES for Wealth Management | 4.19 | 4.22 |

| CES for Consumer Banking | 4.27 | 4.31 |

| CES for SME Banking | 4.30 | 4.32 |

Due to the rise in emerging technologies, there is an opportunity for DBS to enhance their customer experience:

- The bank can integrate Augmented and virtual reality (AR/VR) in the Digibank app by creating a virtual digital branch that the customers access using AR/VR glasses. This integration can help the bank in engaging customers by providing personalised insights and attention with virtual assistance. Customers could have a 360-degree view of the branch without visiting a physical branch location. These virtual branches will be able to offer the same services but in an exclusively VR environment.

- This move will enhance customer experience and reduce costs for the bank, as it no longer needs to invest in physical locations.

- The bank can use AR in Digibank, allowing customers to locate ATMs and nearby DBS branches, similar to the concept instituted by India’s Axis Bank.

- The bank can also offer financial data visualisation and budgeting through a smartphone-based augmented reality, which Westpac Banking Corporation is already doing.

- #3 Employee experience and productivity

- The bank has an employee engagement score of 84%, which is comparatively higher than other operating banks in Singapore. Apart from the employee engagement score, the bank should focus on people analytics. Directed focus on people analytics is vital is to check on the unconscious bias that may unfairly impact promotion and compensation decisions.

- As DBS operates as a technology company, it is crucial to improve the employee experience by channelising the bank’s efforts toward:

- Integrating data analytics and AI into their training and development delivery channels to get personal insights about each employee’s learning capabilities.

- Increasing the scope of the “Future Tech Academy” platform via personalised training and development programs for each employee segment. The expansion can include face-to-face scenario-based workshops, thus improving cohesion within the organisation.

- The bank should focus on rewards and recognitions, as well as career opportunities. There should be an incorporation of rewards and benefits beyond insurance, stock options, house rentals, and leases. Ideas include:

- Launching a Group-wide Recognition program to recognise people that make a significant contribution to the banks’ strategy as role models or through their purpose and values. This program will be a key enabler to reward outstanding performances and reinforce behaviours aligned to the company culture.

- Incubating in-house talent and synergies by allowing their employees to work on cross-departmental tasks as well as individual purpose-driven projects, therefore giving them sufficient autonomy and mobility within the company.

- Providing a clear career growth trajectory as a part of their purpose-driven human capital development strategy.

- Offering employees an opportunity to participate in decision-making and also trusting them with the autonomy needed to find the best paths to achieving success.

- Creating a monthly piggy bank for Netflix, Spotify, gyms facilities and the like.

- #4 Neo banking

- ‘Digibank’ by DBS holds a strong position in Singapore as a digital platform for all its customers and is now acquiring a favourable spot by positioning themselves as a neobank in India and Indonesia. As a future expansion strategy, DBS should replicate their Digibank model in emerging Asian economies, including Thailand, Bangladesh, Vietnam, The Philippines, and Sri Lanka, to tap the largely unbanked population. DBS has witnessed a 1% increase in overseas net profit from 28% in 2019 to 29% in 2020. Here is an opportunity for the bank to increase their net profit from overseas operation by 3-5% in the coming years.

- While Digibank has a strong technological infrastructure, it is not able to steal the show in countries like India and Indonesia. In India, Digibank is highly focused on screening the profile of a potential customer before making them a part of their customer pool by conducting a customer interview and in-person verification. This stringent screening creates disruption in their customer onboarding and leads to fallouts, resulting in an unfavourable proposition for the growing millennial population in the country. In Indonesia, Digibank competes with TMRW by UOB, who is a showstopper and a favourite among the population because of their millennial-centric approach and quirky emoticon-led User-Interface (UI). This challenge is an opportunity for DBS to revamp Digibank according to the needs of different target segments:

- The bank can consider altering the UI of Digibank from a premium persona to a relaxed and fun interface that resonates with the mindset of the millennial population.

- DBS can relax the norms of onboarding customers and integrate backend pre-evaluation of customer’s creditworthiness using an intelligent customer evaluation tool. The bank can further enhance the account opening experience by reducing human intervention, especially by incorporating in-app two-factor authentication for identity and ‘At home-video’ KYC. Such implementations will make the account opening process faster and easier for the customer.

- #5 Society and planet contribution

DBS has committed to RE100, an initiative to use 100% renewable electricity in all operating regions. The bank has set objectives to reduce the environmental footprint of their business activities. To achieve these objectives, the banks should focus on:

- Using green products, such as virtual cards, pulper cards, eco ink, and carbon control press machines. The usage of such items will help DBS reduce the direct impact of their business activities on the environment:

- Compensating for unavoidable emissions by launching projects in impoverished areas which help to preserve biodiversity, drive reforestation, and further local economic mobility

- Using eco-charges, smart sockets, programmable thermostats, and indoor motion sensors to reduce electricity consumption

- Introducing innovative banking services to encourage the consumption of renewable resources, such as low-interest loans and credit facilities for green building and renewable energy financing for SMEs

- Minimising the amount of paper and plastic waste within branches and instituting a ‘3R’ policy -reduce, reuse, and recycle for waste management:

- Ban on plastic use within office premises

- Use of own cups, bottles, and cutlery

- Recycled water used in washrooms and the pantry

- Reduction in paper used for documentation

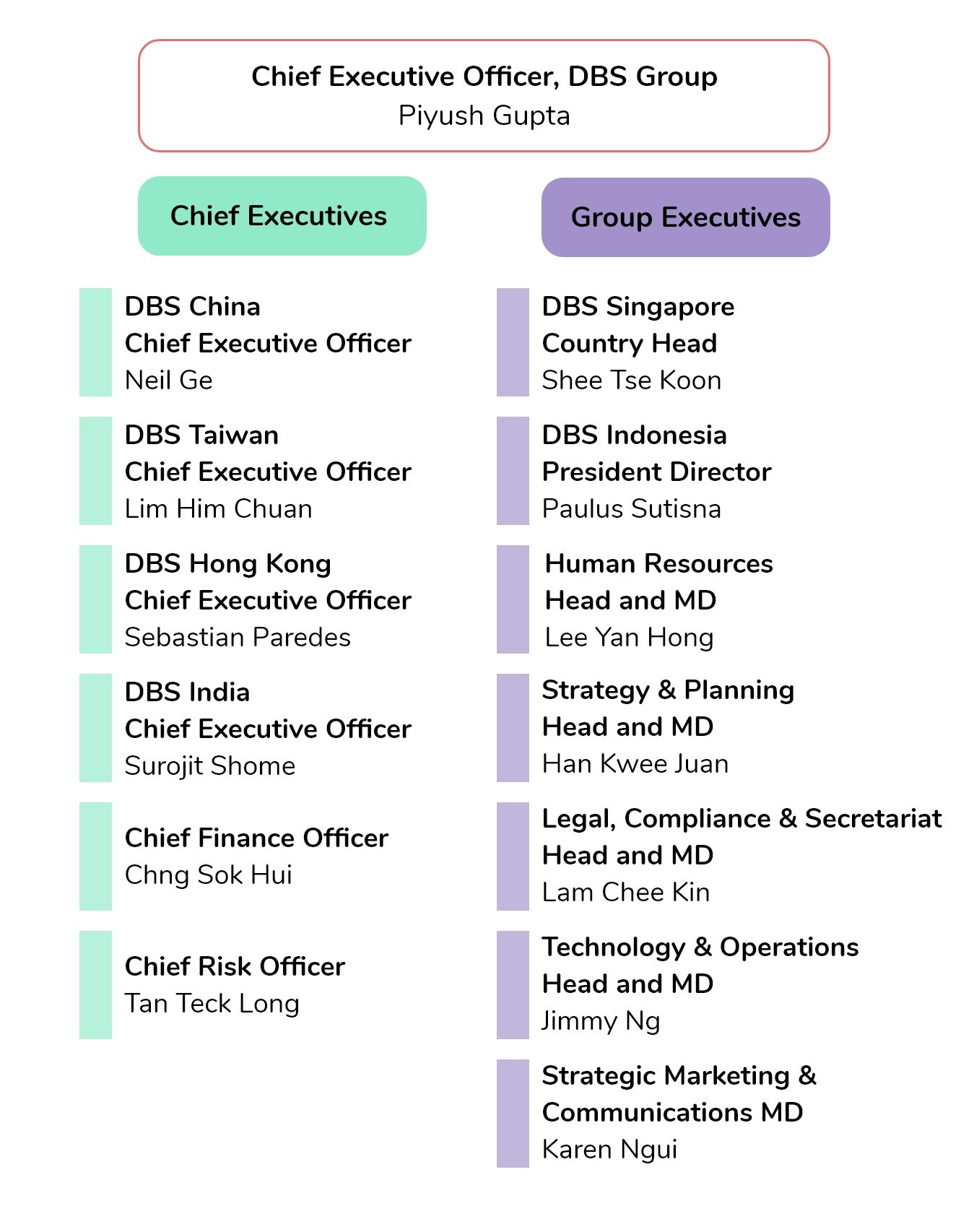

Organisation structure: Leadership

Executive Profile

Piyush Gupta

Group Chief Executive Officer

Piyush Gupta has held the position of Chief Executive Officer and the Director of DBS Group since 2009. Before DBS, Piyush had a 27-year-long career at Citigroup, where his last position was that of Chief Executive Officer for South-East Asia, Australia and New Zealand.

Gupta is the Vice-Chairman of the Institute of International Finance, Washington. He is also a member of the United Nations Secretary-General’s Task Force on Digital Financing of the Sustainable Development Goals, as well as Singapore’s Advisory Council on the Ethical Use of AI and Data, the McKinsey Advisory Council, and the Bretton Woods Committee – Advisory Council. Gupta also sits on the boards of Enterprise Singapore, Singapore’s National Research Foundation, and Singapore’s Council for Board Diversity. Gupta is a term trustee of the Singapore Indian Development Association (SINDA).

Quotes

- Sustainability agenda, Annual report 2020

Finally, banks will be pushed to having a sustainability agenda that addresses each of the ESG pillars and is integral to their strategy and operating models. We are already advanced on our journey of responsible banking, responsible business practices and creating social impact. Responsible banking includes being thoughtful about the financing we provide and the capital we help companies raise, focusing on financial inclusion for the unbanked and the underbanked, and creating a high level of trust in our services through transparency and fair dealing.

- Digital bank, Annual report 2020

The digitalisation of banking will accelerate even more. For example, we have been focused on completing the “last mile” gaps that came to light in our various customer journeys and sharpening tools to embed banking services into the customer context.

Digitalisation will bring additional growth prospects. The accelerated adoption of digital behaviours by customers creates opportunities for market share gains. There will also be new business opportunities, such as the Digital Exchange we launched in the fourth quarter.

Greater digital footprints will lead to increased use of data and Artificial Intelligence (AI) to improve customer experience. I am pleased that DBS has made enormous progress on this front in recent years. The change in work habits will lead to what I call the “future of work”.

Chng Sok Hui

Chief Financial Officer

Mrs Chng serves as the Chief Financial Officer (CFO) of DBS Group and is on the DBS Executive Committee. Before being appointed in October 2008, Mrs Chnge was Managing Director and the Head of Risk Management at DBS Group. She held the position for six years.

Sok Hui is the Chairman of the Board of DBS Bank India Limited. She serves on the Board of the Singapore Exchange Limited and chairs their Risk Management Committee. Mrs Chng is also a member of the Board of Changi Airport Group and chairs their Audit Committee. Additionally, she is a council member of the International Integrated Reporting Council and a member of the CareShield Life Council. Mrs Chng has previously served on the Boards of Bank of the Philippine Islands, The Inland Revenue Authority of Singapore, Housing & Development Board, Accounting Standards Council and, for ten years, as the Supervisor of the Board of DBS Bank (China) Limited.

Quote

- Business Execution, Annual report 2020

Despite the significant economic impact of the pandemic, business volumes for the year were higher or at least resilient, attesting to the quality of our broad-based franchise and nimble execution. The healthy business momentum together with a well-constructed balance sheet enabled us to offset the impact of lower interest rates, and total income remained stable at SGD 14.6 billion.

Jimmy Ng

MD and Head- Chief Information Officer/ Head of Group Technology and operations

Jimmy Ng is the Group Chief Information Officer and the Head of Group Technology & Operations at DBS Bank.

As Head of Group Technology & Operations at DBS, Jimmy manages more than 10,000 technology and operations professionals across the region. He is focused on reimagining banking so that DBS customers can live more and bank less. Prior to this, Jimmy was Deputy Head of Group Technology & Operations. He was responsible for running the bank’s first technology development centre outside Singapore, DBS Asia Hub 2, in Hyderabad. Jimmy also oversaw the bank’s Middle Office Technology and Enterprise Architecture/Site Reliability Engineering.

Quotes

- Strong digital infrastructure, Annual report 2020

The pandemic tested the readiness of both the ‘hardware’ and ‘heartware’ of organisations. We could respond nimbly because of our modern technology stack, enterprise adoption of Agile, and two-in-a-box platform-based organisational structure (where Business and Technology groups work together as equal partners).

To enhance the safety of our employees at the workplace, we used our data infrastructure, analytics capabilities and reusable library of Artificial Intelligence (AI)/ Machine Learning (ML) models to develop a contact-tracing app for employees in just three days. The data analytics also allowed us to monitor the density of people in our workplace and ensure adherence to safe distancing measures.

Tan Teck Long

Chief Risk Officer

Teck Long is Chief Risk Officer of DBS Group since July 2018.

Prior to this, Tan was the Group Head responsible for the bank’s large and mid-cap corporate customers globally. Tan has more than 25 years of banking experience, spanning Corporate Banking, Investment Banking and Risk Management. Between 2011 and 2015, Tan was the Head of Institutional Banking Group (China) and based in Shanghai.

Quotes

- Efforts to minimise portfolio risk, Annual report 2020

While asset quality remained healthy, given an uneven path for global economic recovery ahead, we remain cautious of the potential impact on our portfolio. We continue to leverage technology to tackle financial crime risk and strengthen our cyber security defense.

- Cyber security and data protection, Annual report 2020

As the bank adopts work from home measures, we expedited the implementation of our cyber security initiatives to mitigate potential incremental security threats from possible security risk exposures. We reinforced and scaled up the internal environment to ensure the network is secured and healthy for staff working remotely. Along with our digital transformation, we continue to invest in innovative security controls. We also believe that people are integral to overall cyber defence and further enhanced our staff security awareness through training.

We continue to strengthen our multi-layered cyber security defence with cyber security solutions, such as web isolation and content disarm and reconstruction, to protect our users from advanced cyber threats through the internet and email channels. We also enhanced the cyber security hygiene and control baselines of systems supporting essential banking services through stronger authentication, micro-network segmentation, and database monitoring.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

DBS Group Holdings Ltd, (2020, December 31). Group annual report 2020.

https://www.dbs.com/annualreports/2020/files/media/dbs-annual-report-2020.pdf

DBS Group Holdings Ltd, (2020, December 31). Sustainability Report 2020.

https://www.dbs.com/iwov-resources/images/sustainability/reporting/pdf/DBS%20Sustainability%20Report%202020.pdf?pid=sg-group-pweb-sustainability-pdf-dbs-sustainability-report-2020

DBS Group Holdings Ltd, (2020, December 31). Awards-accolades.

https://www.dbs.com/about-us/who-we-are/awards-accolades/default.page

DBS Group Holdings Ltd, (2020, December 31). Group management committee.

https://www.dbs.com/about-us/our-leadership/group-management-committee.page

Sourav Kumar, Research Intern, contributed to the research in conducting a preliminary literature review and conceptualising the article.