National Australia Bank (NAB) is one of the largest financial services providers in Australia and is among the Big Four banks in Australia. NAB operates in nine countries, with Australia and New Zealand being the primary markets for the bank. NAB continuously finds technological innovations to make its operations simpler and faster to provide an exceptional customer experience and become Australia’s leading bank chosen by customers.

Operational efficiency at NAB in comparison with peer banks in Australia

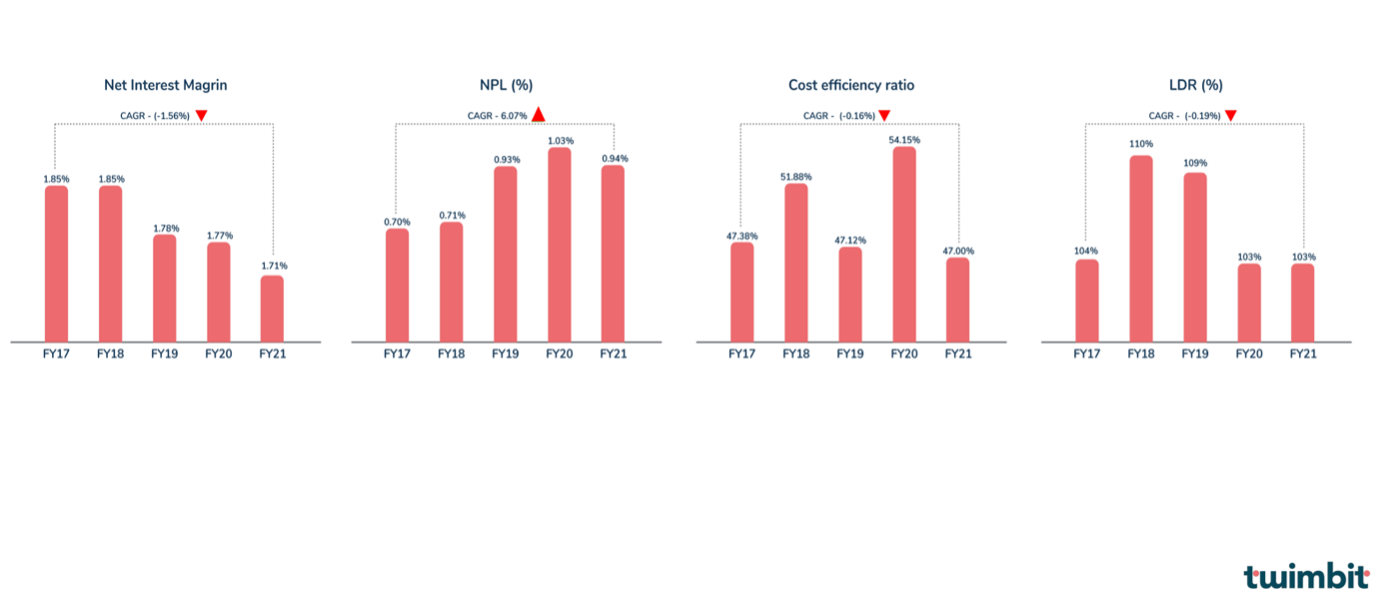

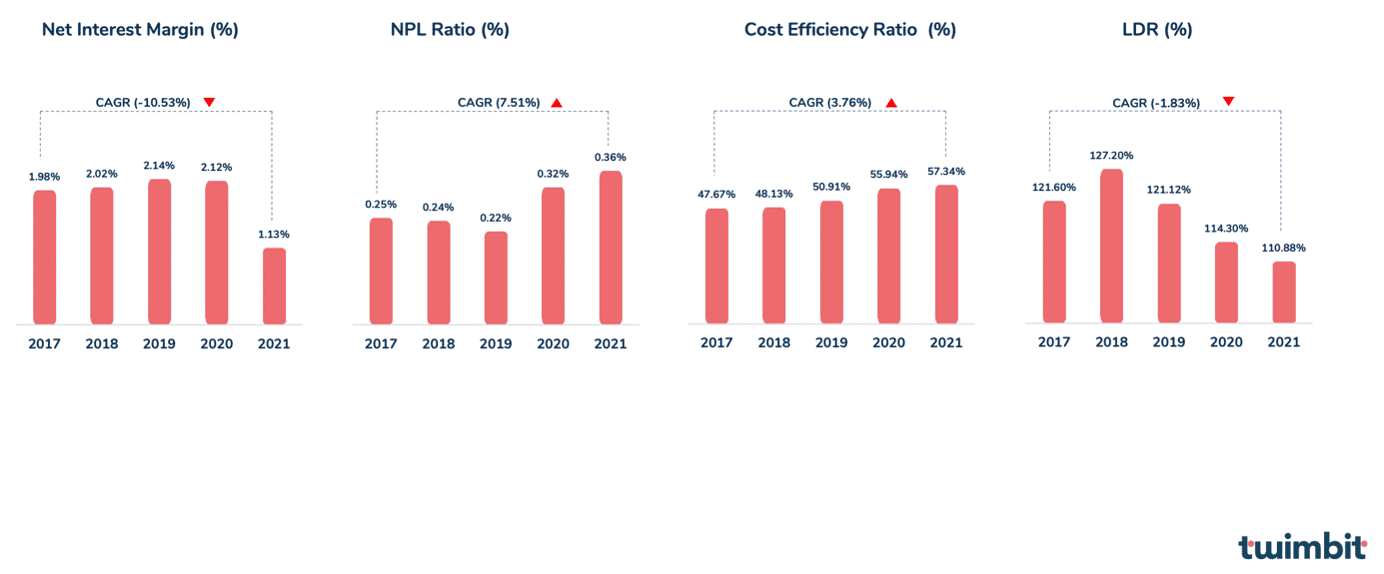

NAB’s net interest margin has seen a slight decline over the five years from FY17 to FY21 which suggests a decline in investment efficiencies at the bank. (Figure 1) This implies that the bank is making investments which are riskier and provide a lower. These inefficiencies are overshadowed when compared to the considerable decline in net interest margins of peer banks in Australia (Figure 2).

Australian banks generally have a higher cost-efficiency ratio when compared to peers in the APAC region. Despite this, NAB has a significantly lower cost-efficiency ratio at 47% in FY21 (Figure 1) which is more than 10% lower than its peers suggesting efficient operations at the bank. During the period analysed, NAB’s operational efficiency has increased, whereas, on average the Big Four’s operational efficiency is comparatively higher than the banks operating in Asia (Figure 2).

Future technology investments fuel growth for NAB

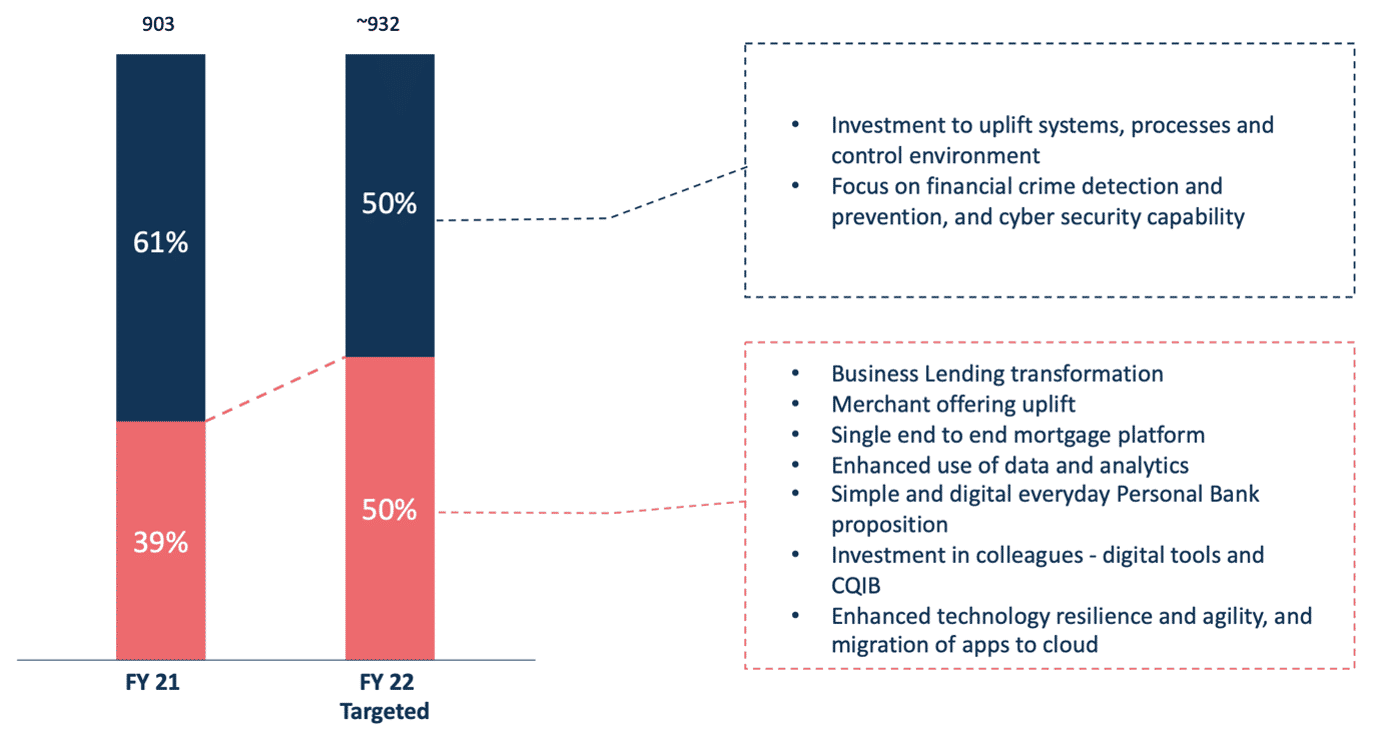

NAB targets to shift their investment spending to product simplification and growth using analytics and digital tools. In the past year, the bank’s focus has primarily been on the upliftment of systems & processes and crime detection & prevention (Figure 3).

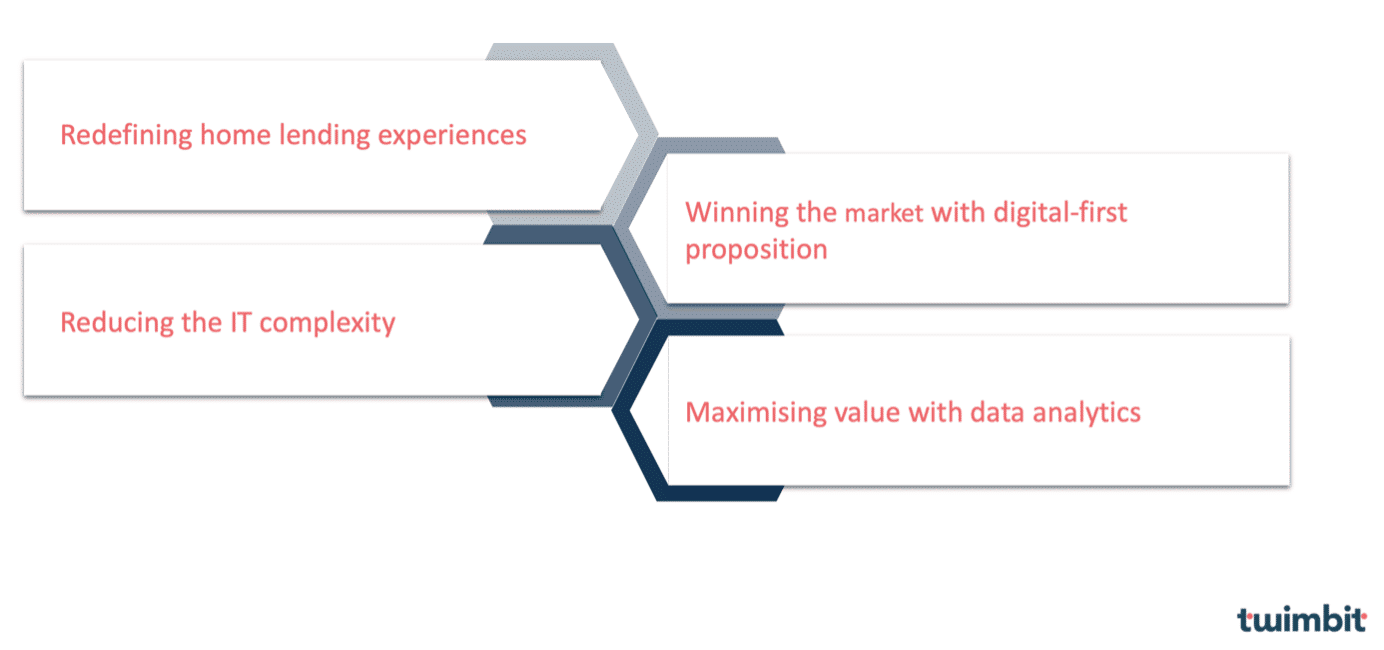

4 growth opportunities for NAB

- #1 Redefining home lending experiences

NAB has the third-highest market share in the housing lending business at 13.8%. The bank has taken initiatives to enhance its housing lending business using the ‘Simple Home Loan’ application tool. This has resulted in increased use of the mobile app to conduct simple modifications in home loans and appointment bookings. As many as 80% of home loan modifications are done through the bank’s mobile app. Streamlined application processing has resulted in 30% of the total applications being processed within an hour.

The next step for NAB is to further improve the customer experience through journey led mapping. It is about owning the customer journey by integrating real-estate marketplaces with financial products and advisory. This entails finding a potential property to buy providing them with personalised loans and price adjustments.

- #2 Winning the market with a digital-first proposition

NAB is second only to CBA in having the largest base of digitally active customers along with a high proportion of transactions being conducted digitally through the bank’s digital channels at 65%. It is to be noted that CBA only leads NAB minutely and considering that NAB is half the size of CBA in terms of market capitalisation is commendable for NAB.

NAB is the only bank among the big four to operate separate neobanks, namely, 86 400 and U Bank. Since no other bank among the big four has a strong presence in the neobanking scene, NAB can put this to their advantage. NAB can target millennials who are tech-versed and continue to build their digital presence.

- #3 Reducing the IT complexity

The bank makes considerable ICT spending to enhance the customer experience and simplify its operations. The ICT spend as a percentage of operating revenue stands at 12.75% which is much more than CBA’s 8.48%. The bank faces a dilemma of whether to buy or build its IT infrastructure in areas about platform customer migrations, high-speed application delivery and security. NAB needs to make a decision and identify which solutions are best served through third parties and make a buy decision, whereas for critical apps where it needs to make an organisation-wide digital strategy it should be done in house. This can lead to huge cost savings for NAB.

- #4 Maximising value of data with analytics

NAB uses data analytics to better regulate voice analytics & compliance, customer complaints, credit decisioning, financial difficulty support, fraud & insider crime detection and customer retention. Customer data is analysed and used while conducting customer service interactions, this has resulted in 80% of interactions done with the use of personalised information.

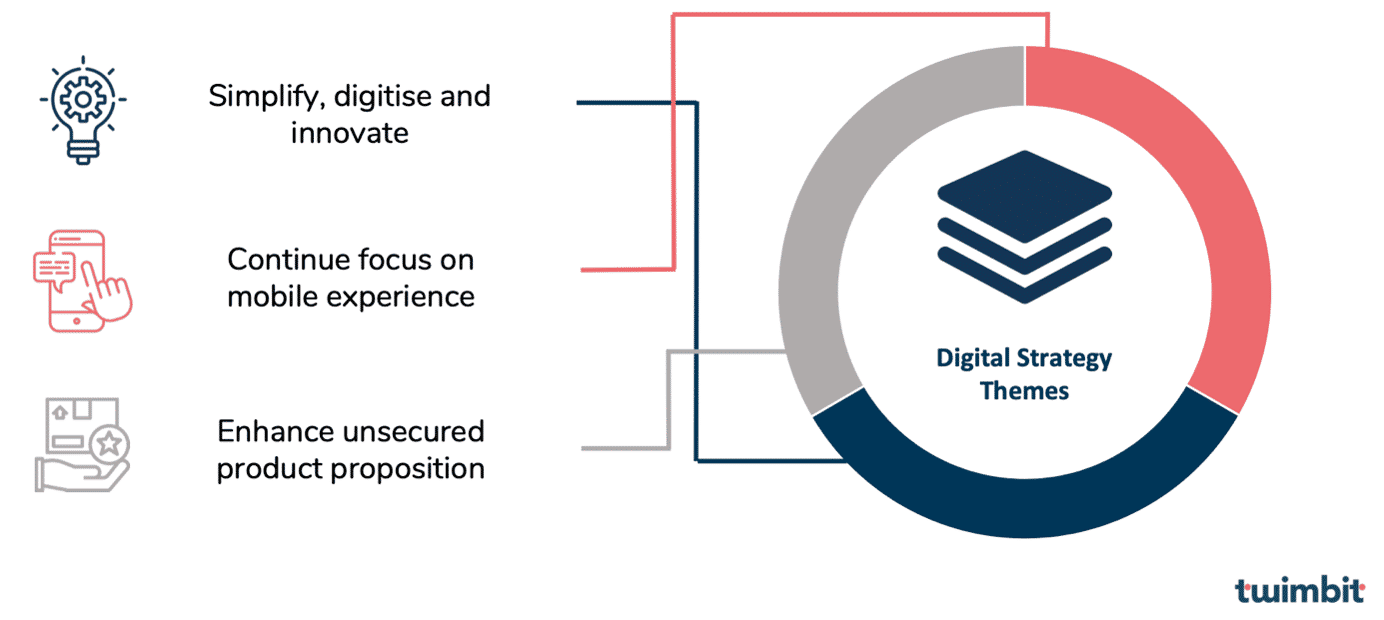

Digital strategy at NAB

NAB plans to deliver its digital strategy through three distinct pillars (Figure 5).

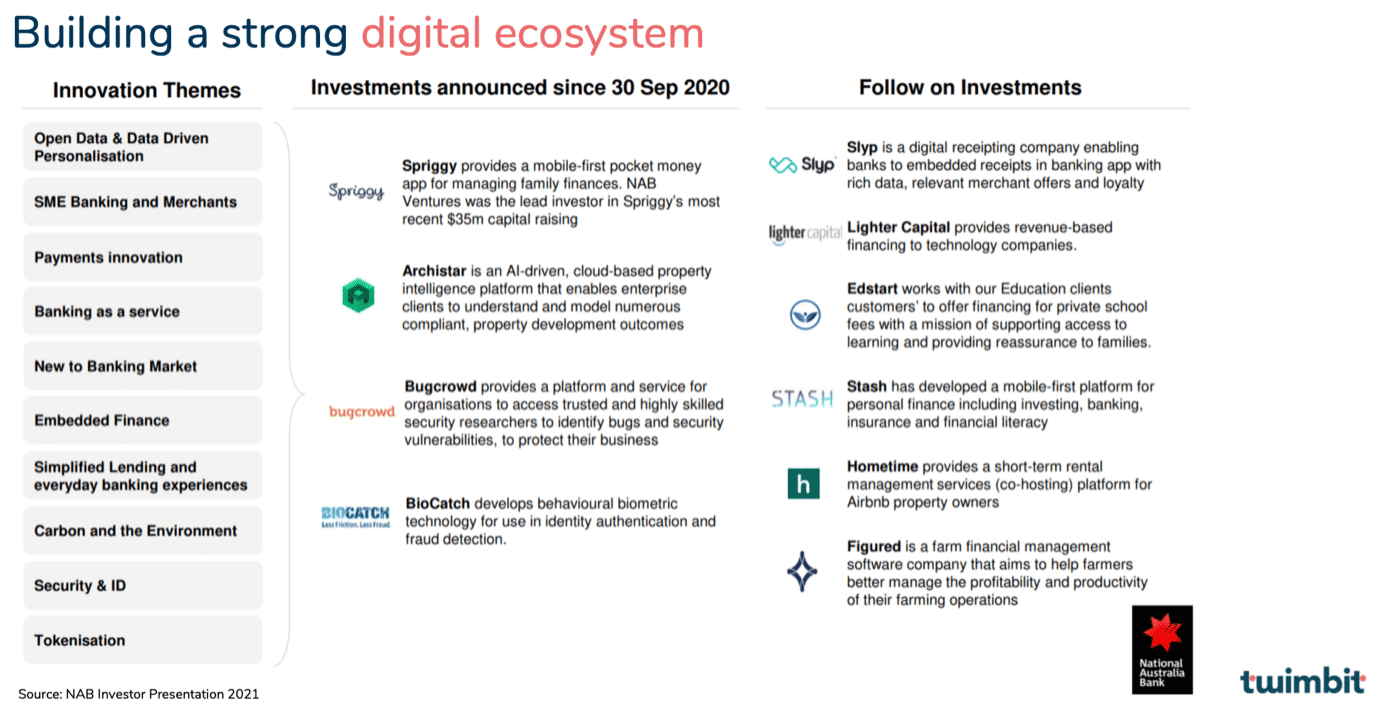

Building a strong digital ecosystem through partnerships

NAB makes investments to promote strategic priorities through its venture capital division called NAB Ventures. The division incubates & tests new and innovative customer propositions leveraging new developments in technology. NAB Ventures currently manages more than 20 investments spread across ten innovation themes (Figure 6).

Conclusion

NAB is in a good financial position, making good returns and operating efficiently. The bank’s operations are much more efficient than an average bank in the Australian banking industry as suggested by its low cost-efficiency ratio. The bank is making a shift towards productivity and growth by leveraging the use of data analytics to streamline the business processes and enhance the customer experience through simplification.

In the future, NAB is looking to:

- Simplify their IT infrastructure

- Reduce the number of product offerings by eliminating the products which do not provide strong revenue for the bank

- Implement data analytics in customer conversations and credit profiling

- Improve its digital presence through its acquired neobanks

- Streamline the housing lending business

For detailed insights, download our report.