Company insights

twimbit’s Purpose Index

Source: Refer to the methodology in Appendix A below

State Bank of India (Group financials)- An overview as of 31st March 2021

| Bank Name | State Bank of India (SBI) |

| Headquarters | Mumbai |

| Operating revenue | USD 42.16 billion |

| Group net profit | USD 2.78 billion |

| Total assets | USD 619 billion |

| Employees | 245,652 |

| Countries in operation | 31 |

| Number of branches | 22,219 |

| ICT spend | USD 944 million |

| Number of customers | 459.2 million |

| Market capitalisation | USD 3.83 trillion |

| Operating revenue CAGR growth (2016-2020) | 7.9% |

2. Conversion rate to USD as of 31st March 2021 – 0.01366 USD

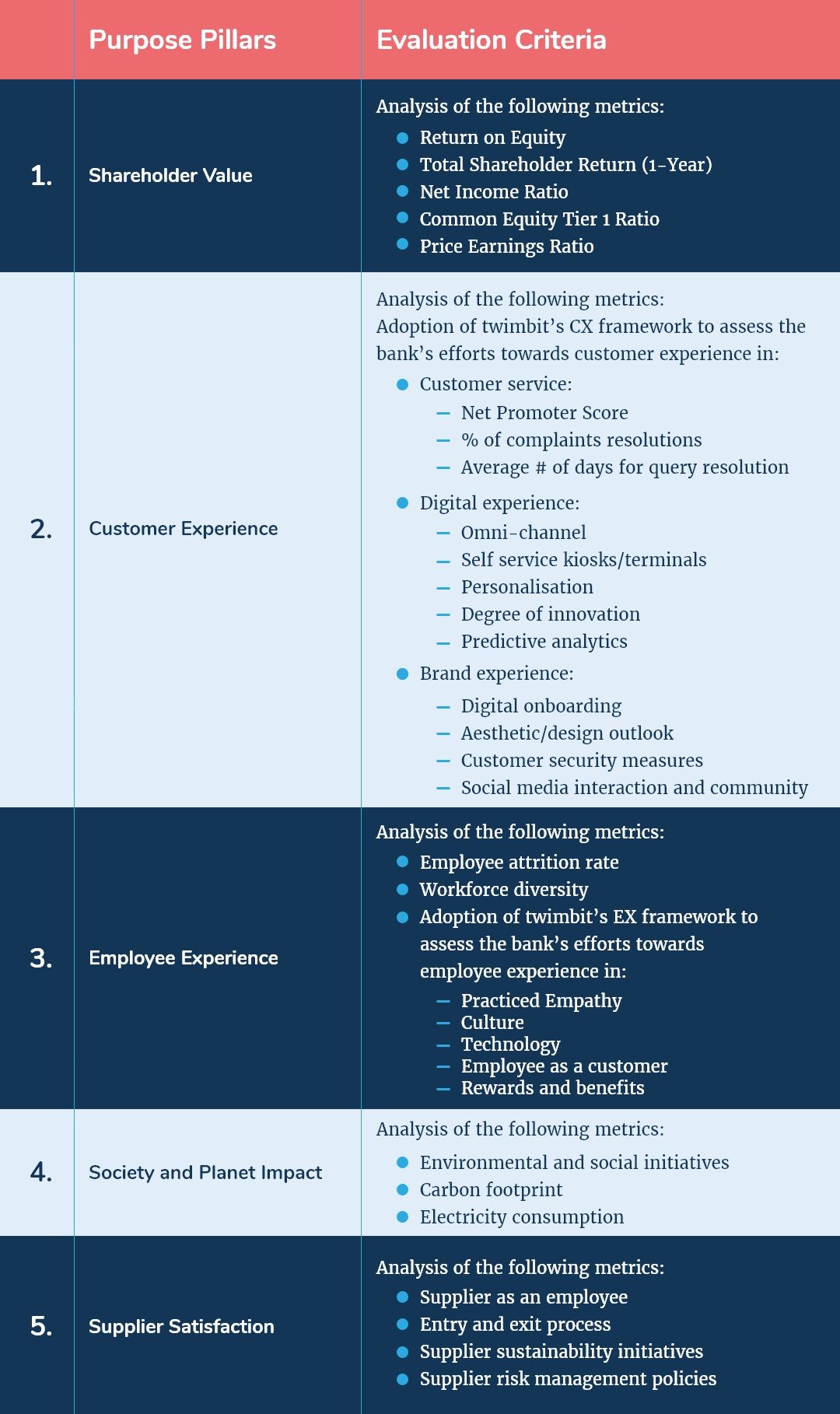

Shareholder value (31st March 2021)

| Return on equity (as of 31st March 2021) | 9.94 % |

| Total shareholder return (1-Year) | 5.69% |

| Net income ratio | 53.60% |

| Common equity Tier 1 ratio | 10.02% |

| Price-earnings ratio (as of 31st March 2021) | 15.32 |

2. The P/E ratio is in the trailing method till 16th August 2021

Awards

| 2020 | Asian Banker Magazine, Singapore: “Best Transaction Bank in India” (4th consecutive year in a row), “Best Payment Bank in India” (2nd consecutive year) in 2020. SBI Foundation: Grant Thornton SABERA 2020 Awards for agriculture and rural development, Corona Warriors Award by the Governor of Maharashtra for healthcare, and the ICC Social impact Awards 2021 for Empowering the Rural Population. APLMA (Asia Pacific Loan Market Association): “Syndicated Loan House of the Year” – India Global Finance Magazine: “The Best Trade Finance Provider (India) –2021” for the 9th consecutive year Department of Official Language, Ministry of Home Affairs, Government of India: State Bank of India’s home magazine ‘Prayas’ has been conferred with Kirti Puraskar for the 4th time. Brandon Hall Excellence awards 2020: “Best Use of Blended Learning”, “Best Learning Program Supporting a Change Transformation Business Strategy”, “Best Unique or Innovative Learning & Development Program”, “Best Advance in Technology for Crisis Management” for e-RBCs and “Best Advance in Social Learning Technology” for e-Gyanshala. |

SBI and its strategic focus areas

SBI aspires to take the stakeholder approach in building its future growth within the banking industry. The bank wants to move forward by strengthening its financial position through the key pillars of resilience, people and technology.

Hence, it struck a balance between nourishing business resilience and being compassionate in this new normal. It continues to innovate to serve its stakeholders better and be a reliable partner to bank with. Overall, SBI has reinforced its digital presence, invested in the people and continues to enhance its services to cater to the varied requests of its customers.

SBI intends to adopt the following strategies to achieve its objectives:

- Acceleration of the digital agenda to expand the scope and reach of SBI YONO

- Leveraging advanced analytics for deeper insights on internal operational data, thereby providing quality data to operating units and helping them in decision-making

- Exploring opportunities for corporate lending to businesses in promising sectors to contain the bank’s risk and diversify its portfolio

Throughout the year, SBI undertook these initiatives to achieve its long-term objectives:

- Introduced three new products – Agri Infrastructure Fund (AIF), Animal Husbandry Infrastructure Development Fund (AHIDF) and PM Formalization of Micro Food Processing Enterprises (PM FME) – to amplify investment credit portfolios in the agricultural sector

- Launched “PM SVANidhi Loans” to support street vendors during the pandemic and thus extended its services to a new segment

- Established Guaranteed Emergency Credit Line (GECL) 1.0 & 2.0 to provide financial help to units affected by the pandemic

- Facilitated quick, remedial measures for corporates with proven probable-stressed portfolios after various analyses; carried out for industries such as NBFC, Construction, Textiles, Ports, Shipping, Hotels, etc. to help these business groups make informed credit decisions

- Divested stake in non-core assets and sanctioned investments of USD 81.96 million in Private Equity/Alternative Investment Funds

- Integrated the Loan Origination System (LOS) with Vidya Lakshmi Portal (VLP), a government portal to warrant better tracking and faster sanctioning of education loan applications

- Introduced CRM, an integrated platform to help it engage with customers throughout their life cycles and be more customer-centric

- Formed an “ABBFF Review Committee” under its MD’s chairmanship to monitor the progress of staff accountability examination (in respect of large-value frauds of USD 6.8 million and above), with the progress for cases reviewed every two weeks/bi-monthly.

- Customer experience

In its endeavour to be the bank of choice, SBI focuses on customer experience. Accordingly, the bank embraced digital readiness to serve the diverse needs of its customers. It aims to become the top choice for corporate and retail clients.

Therefore, SBI took the following initiatives to enhance its customers’ banking experience:

New products and services

- Introduced YONO – PAPL (Pre-Approved Personal Loan), PAXC (Pre-Approved Xpress Credit), PAPNL (Pre-Approved Pension Loan), INSTA Top-up for Xpress Credit, and Insta Top-up for Pension Loan to create an easy banking experience

- Launched a unified configuration of YONO Business Corporate Banking, which gives customers Single Sign-On access to five applications, namely CINB, CMP, SCFU, eTrade and eForex for corporate clients

- Provided online onboarding to new digital customers for CINB, e-Trade and e-Forex

- Offered Debit Card-authenticated onboarding and a Pre-Approved Merchant Loan, which is a digital loan product for Saral customers

- Initiated an online account opening facility for non-individual accounts like Sole Proprietorships, Partnerships, and HUF entities

- Provided shopping deals on a single platform with merchants like Redbus, Medlife, Kisan Store, Amazon, Yatra, Cleartrip, Myntra, Flipkart, Uber, OLA, Zoomcar, IRCTC, VLCC, Agricart, BigHaat, etc.

- Shortlisted top-rated premier and reputed institutions to extend education loans under the Scholar Loan scheme (with relaxed norms and concessional interest rates) to enhance student loan experiences

- Launched a new product called the SPL PAPL scheme for customers in dire need of money to get the equivalent of 3 months’ salary as an advance

- Deployed CTS-enabled Self Service Cheque Deposit Kiosks (CDK) to help customers deposit CTS cheques, hassle-free

- Introduced a Smart CDK functionality in its YONO application to help customers deposit cheques in bulk through reference numbers, anywhere and anytime

New features in existing products

- Introduced new features such as:

- Multi-Device Login: Implemented the KO (Kiosk Operator) family concept, consisting of one KO and five sub-KOs. It enables the Customer Service Point (CSP) to offer its services through multiple nodes simultaneously. The feature also allows the CSP to provide service through more than one device (maximum of six) using a single code, replicating a branch setup.

- EMV enablement on MATM: Enabled Micro-ATMs (MATMs) in the BC (Business Correspondent) channel to accept EMV chip cards, which helps in reducing risks associated with magnetic stripe cards.

- Passbook Printing for FI & non-FI customers: All customers can update their passbooks by validating barcode at the CSP outlet, which helps in decluttering the branches

- Voice prompt: SBI rolled out Voice Prompts in Hindi, English, Tamil, and Telugu for customers performing transactions at CSP outlets, which mitigates the risk for illiterate and semi-literate customers, as they can now hear the transaction details performed for their accounts.

Special projects

- SBI initiated numerous special projects to ensure customer convenience. A few of these projects are:

- Foreign Inward remittance to the Prime Minister Cares (PM Cares) account: Launched developments in the Rupee Flash Application programming interface (API) platform and the Rupee Express Application to allow foreign inward donations into specially designed PM Cares Account to fight the pandemic

- Parking payment through FASTag(electronic toll collection system): Integrated the GMR International Airport Parking facility at Hyderabad with a NETC (National Electronic Toll Collection) SBI FASTag; initiated by NPCI (National Payments Corporation of India), it enables customers to pay parking charges through FASTag

- I-Meeting application: Extended the I-Meeting application to 17 local head offices for conducting their quarterly local body meetings

- CKYC Signzy Scanning Solution: An AI-Based scanning application for error-free and speedy scanning of customer documents in CKYC (Central Know Your Customers) formats

- Pension Seva: Revamped the Registration in Pension Seva through mobile OTP (One Time Password); it enables pensioners to use a range of facilities without visiting the branch

- Issuance of immediate PRAN (Permanent Retirement Account Number) Card: Introduced Photo and signature upload facility at branches for NPS (New Pension System) registration to facilitate immediate PRAN Card issuance by CRA (Central Record Keeping Agency) to the subscribers without waiting for the physical copy of their application

- CKYC for FI Accounts: Started CKYC process per regulatory compliance for Financial Inclusion accounts

- Aadhaar Masking: Implemented Aadhaar Masking per compliance at CKYC and other channels

Customer service initiatives

- Established Circle Complaints Resolution Centres (CCRC) to improve the resolution quality of customer grievances

- Conducted virtual customer meetings to get feedback for the improvement of its services

- Held programmes in all branches to sensitise the branches towards providing good customer service

- Implemented the concept of floor managers in more than 2400 branches across the country for enhanced customer satisfaction

Doorstep services

- Extended Doorstep services through Education Loan Counsellors (ELCs) at select cities to increase penetration through Global Ed-vantage Education Loans, a flagship product

- Provided doorstep banking services for:

- Cash Deposits,

- Cash Withdrawals,

- Pick-ups of Cheque Book Requisition Slips,

- Pick-ups of Cheques for Collection / Clearing,

- Life Certificates viaJeevan Pramaan,

- Pick up of IT/ Govt/ GST Challan with Cheque,

- Delivery of Statement of Account,

- Term Deposit Advice, TDS and Form 16 Certificates through its agents to all customers at over 100 banking centres

- Made Doorstep banking services available for senior citizens above 70 years of age at all centres nationwide

Initiatives for NRI customers

- SBI has taken the following initiatives to enhance the banking experience for its NRI customers:

- Missed Call Banking Services through the SBI Quick App – Customers can get account balances and mini statements by giving a missed call from their registered mobile numbers

- Extended financial transactions such as NEFT (National Electronic Funds Transfer)/RTGS (Real-Time Gross Settlement) through the YONO application

Business banking

The bank encapsulates the journey of Corporate and SME Loans through its Loan Life Cycle Management System (LLMS). This system automates and standardises the life cycle of the credit process, enhances risk management, and improves user experience and turnaround time (TAT). SBI came up with new products under this system:

- Pre-Approved Business Loan (PABL): PABL is a pre-approved digital loan product for current account clients, based on the cash flows in the account. SBI grants this loan to cover the diverse needs of its clients, related to their businesses. Therefore, the clients can open a dropline overdraft account without any primary guarantee or collateral.

- Guaranteed Emergency Credit Line (GECL) 1.0 & 2.0: Through these products, the bank provides additional credit lines to existing, eligible borrowers through an ad hoc structure, namely the Guaranteed Emergency Credit Line (GECL), to address the current crisis.

- Employee experience

SBI believes it is essential to have robust human capital dedicated to facing challenges head-on while providing quality customer service. This measure is vital to ensure the consistent and sustainable growth of the bank.

The bank thinks HR is pivotal to help it face new challenges related to knowledge, technology, and the dynamic trends of the economy. In addition, its team of over 475 in-house educators and banking professionals implemented new approaches to train and upskill our personnel via online techniques at the 6 Apex Training Institutes (ATIs) and 51 Regional Institutes (SBILDs).

Moving forward, SBI will continue to invest in employee wellbeing and productivity enhancement to realise its growth potential.

The bank undertook the following initiatives to improve employee experience in 2020:

- Inclusion of ‘STEPS’ (Service, Transparency, Ethics, Politeness and Sustainability) in the annual performance appraisal system (CDS)

- The bank undertook some productivity initiatives, which include the following:

- Adopted a branch workforce model to ensure optimal utilisation of human resources, consisting of productivity parameters like work drivers of operations, transaction load factors, number of advance accounts, and feedback from operating units.

- Streamlined the promotion and transfer process to completion in the first quarter of the financial year. This helps give assurance and stability to branches and focus on business activities during the rest of the year. All these promotion exercises were via video conferencing.

- Ensured a data-backed performance evaluation process through Career Development System (CDS) under project ‘Saksham’. It guarantees accountability, performance visibility and alignment between individual and organisational goals. It also helps in developing employees through a comprehensive annual competency mapping framework.

- Defined career paths for employees under seven job categories, i.e., Finance and Accounts, Treasury and Forex, Credit & Risk, Marketing and Operations, Sales, HR, IT and Analytics on a Scale of II to V to ensure extensive domain knowledge and foster expertise

- Put the ‘SBI GEMS’ mechanism in place to promote recognition and kept records of such recognition

- Organised webinars like ‘Put Your Mind at Ease’ to help the employees with time and stress management

- The bank took the following initiatives for its recruitment processes:

- Extensive use of digital platforms such as social media handles and platforms like LinkedIn, Naukari.com, and iim.jobs. This enables the bank to reach out to a broader pool of tech-savvy candidates. Additionally, the bank also has tie-ups with professional bodies (such as the ICAI) for specialist positions.

- Utilised an IT platform and conducted recruitment processes through video conferencing to complete the processes in a time-bound manner

- The bank initiated payment of a fixed Ex-Gratia amount to the bereaved family of deceased employees. This payment includes one year’s salary, financial support for the education of children aged 3-21 years up to graduation and USD 16,000-40,000 in different grades.

- SBI increased loan limits for its employees and provided flexibility to help them acquire assets easily.

- For pandemic relief measures, the bank took the following steps:

- Reimbursed the expenses incurred on COVID-19 Tests and Treatment and sanctioned special leaves for employees in quarantine.

- Introduced cash compensation for family members of deceased employees who were at the forefront of operations

- Set up a robust and comprehensive “Work from Anywhere Policy” to ensure work-life balance and also save overhead costs

- In terms of caring for retired employees, the bank took the following initiatives:

- Launched “e-Pharmacy” to provide a domiciliary facility for retired employees. It has also made arrangements with M/S Apollo Life to provide pharmacy services to these members, with an annual payment plan through an application named ‘URWORLD’.

- Rolled out a facility to obtain life certificates through ‘Video-based identification’ from the MyHRMS application. This helps staff pensioners to submit the certificate without visiting the branch.

- The bank significantly reduced training expenses and broadened the knowledge horizons of its staff through the following initiatives:

- Used “Blended Learning” strategies with videos, pre-reads, quizzes, and webinars to foster interest and learning retention

- Coached faculties through simulations and training to deliver engaging online lectures

- Onboarded all training personnel and other stakeholders on a single virtual platform

- Instituted an in-house automated and centralised training calendar management system

- Launched a comprehensive common training program for all the newly recruited employees of its public sector banks

- SBI offers all its employees (including senior management) the following:

- e-RBC – Role based certifications for around 200,000 employees. The bank migrated these certifications to the e-platform by creating digital repositories of tutorials, webinars and assessments.

- e-Lessons – Ten gamified e-lessons for compliance and digital skill-building to promote business practices that align with the bank’s new paradigm

- For top executives, SBI offers the following:

- Online Assessment Centre: An OAC-based assessment of leadership competencies. Each participant received individual development plans consisting of areas such as strength and leadership. In addition, they were also offered Massive Online Open Courses (MOOC) based on competency needs.

- Immersive credit skilling: Provided intensive training in solution-oriented credit decision making to business leaders holding the DGM rank

- Introduced collaborative programmes with organisations such as FEDAI, ICAI & CARE to help the employees stay abreast during the pandemic and increase industry associations

- Entered an MoU for strategic collaboration in Executive education as well as several other MoUs under ‘University Connect’ to train students

- Launched ‘Samunnati’, a coaching intervention for branches to make them goal-driven and competitive. It is an Action Research model which involves a dynamic approach towards problem identification, planning, action and impact assessment.

- Rolled out a hybrid event (part online and part physical+online quiz) called ‘SBI Wizards’ to foster positivity among the employees

- Undertook podcasts like “SBICB-On-Air”, along with webinars on “building mental resilience”, “staying fit” and reflective exercises such as “Samya – A time to ponder”, as well as virtual power talks by experts and programmes on inclusive workplaces such as “Samya-leave no one behind.”

- Enhanced operational knowledge of employees with case study discussion boards, an online quizzing portal and the askSBI search engine

- Rolled out ‘Anweshan’ – an e-publication to spread best practices of businesses for better decisions

- Society and planet impact

SBI is heavily inclined towards corporate social responsibility. The bank spent USD 19.79 million on CSR activities. It wants to work towards community development, environmental sustainability, and the welfare of socially and economically backward society sections.

Most of the activities by the bank in 2020 revolved around healthcare, education, livelihood, sports, environmental sustainability and the empowerment of women, youth and senior citizens. SBI undertook the following initiatives to create a lasting social impact:

For COVID-19 relief

- Donated USD 4.1 million towards COVID-19 relief measures (such as providing food, supporting initiatives for students’ mental wellbeing, distributing PPE kits, procuring ventilators and other equipment) and also tied up with ECHO India to build the capacity of healthcare workers and supported R&D projects with the Indian Institute of Science (IISC)

- Supported the Mumbai Police Foundation by donating USD 136,000 for the welfare of the families of Covid warriors who died on duty

- Put USD 1.5 million towards the PMCares fund to support the COVID-19? vaccination drive

Community development

- Donated USD 136,000 to the Apollo Hospitals Educational and Research Foundation to help them set up medical rooms at six centres (a collaboration with OYO)

- Provided education grants worth USD 1.4 million to daughters of ex-servicemen/war-veterans/ war-widows for a year under the government campaign called ‘Beti Bachao Beti Padhao’

- Supported the education and welfare of young girls through various NGOs

- Funded the Target Olympic Podium scheme and also donated USD 683,000 to the National Sports Development Fund to help athletes participating in the Olympics

- Supported healthcare across the country through financial donations, donations of ambulances and various high-end medical equipment, setting up operation theatres, and supporting treatment for patients who needed financial help

- Provided financial help for an education programme for 100 specially-abled children in Karnataka

- Made donations to Kat-Katha NGO, which works for the empowerment and education of trafficked women and children

- Established Rural Self Employment Training Institutes (RSETIs) all over the country to mitigate the unemployment problem among youths

- Provided sanitary napkin vending machines, machines for plastic recycling, and dumper bins across the country under the ‘Swachh Bharat’ government initiative

- Donated lab equipment and constructed disabled-friendly toilets at the Leprosy Mission Trust

- Supported a tree plantation drive organised by the Green Leaf Trust in Ahmedabad

- Donated to Prabhav Foundation for a tree plantation drive in New Delhi

- Set up a stitch training centre for women at Shri Sewa Bharti Siksha Samiti in Indore

- Set up a computer library with workstations and software at The Hindu Women’s Welfare Society (Shradhaanand Mahilashram)

- Constructed a dormitory for poor and underprivileged women with the help of Khirpai Ramakrishna Sarada Sevashrama

- Donated prosthetics legs, wheelchairs, braille kits, and other equipment for the welfare of persons with disabilities

- Employee Volunteering through the SBI Children’s Welfare Fund: The bank has a welfare fund for children that runs with the help of voluntary contributions from the bank’s personnel. This fund focuses on the betterment of underprivileged children and orphans.

Environmental Sustainability

- Adopted tigers and endangered animals for one year through zoological parks

- Supported the installation of bird perching stands at Kolleru Wildlife Sanctuary for the welfare of rare bird species

- Planted 15,500 saplings across the coastal areas affected by the ‘Amphan’ cyclone in West Bengal

- All ATIs & SBILDs follow eco-friendly practices, such as vermicomposting for recycling bio-degradable wastes, captive Sewage Treatment Plants (STPs) with recyclers and solar panels or solar plants. The aim was to reduce conventional-source power consumption and rainwater harvesting. SBI has also banned single-use plastic and ensured all its premises are ‘Plastic-free zones’.

Digital strategy

SBI has committed to digital transformation and continues to invest in cutting edge technological solutions. The bank aims to be the most digitally enabled bank in India and wants to push the boundaries of physical presence to phygital presence (physical and digital presence).

The bank’s YONO app has grown significantly in volume and crossed 70.5 million downloads, with a user base of 37.09 million. It caters to the financial, banking, and lifestyle needs of customers. YONO has an intuitive, convenient and user-friendly interface that helps in providing an enhanced digital experience for SBI customers.

The bank took the following initiatives to enhance the YONO app:

- Introduced features which allow customers to get pre-approved loans online and get immediate disbursement with zero paperwork from the comfort of their homes

- Launched YONO Quick Pay, which offers convenient payments or fund transfers without logging into the main application

- Added new features such as KCC review, P-segment gold loan, instant account opening via e-KYC authentication based on Aadhar OTP and pre-approved agricultural loan (SAFAL)

- Instituted YONO Krishi with features like Agri gold loan as well as YONO Mandi and YONO Mitra to cater to farmers

YONO Business

The products provided by YONO Business for MSME, corporate and government customers focus on the following three pillars of digital transformation:

- One Bank One Platform, which creates an omnichannel digital platform that integrates CMP, Corporate INB, e-Trade, e-Forex and Supply Chain Finance under a single login

- Digital bank offering seamless end-to-end digitised customer journeys

- New-age banking to future-proof technology priorities, like API banking

These three pillars have their foundations based on different working methods (cross-functional garage construction), modern technical architecture and skills (agility, product management) to support the transformation.

YONO Business serves the various banking interface requirements of all types of non-personal entities in a digital manner, directly from small enterprises or SMEs to large multinational companies and central and state governments.

It has features such as:

- A streamlined and intuitive onboarding process for new digital customers

- A new omnibus document to replace the previous old document process, thus eliminating multiple visits to branch offices

- Digital onboarding for non-appointed customers through the YONO Business Branch interface

- Corporate user management as an end-to-end digital journey to the Corporate Administrator for user management, ensuring security and convenience

- An intuitive company dashboard with real-time integration of A&L account position, fund flow position, letter of credit expiry dates, instalment payment due-date alerts and notifications, and other features

- Redesigned import LC journey and Forex rate booking within 15-20 minutes without the need to visit the branch

- Additional products for existing customers

Other digital initiatives of SBI consist of:

- SBI e-Trade: It is also called Customer Enterprise (CE) and is a centralised application connected with EE and Core Banking System to meet the demands of business customers for domestic and international trade finance. It has features such as a corporate group level view of all sub-companies, a one-view trade portfolio dashboard, notifications and alerts, digital document submission, etc.

- Mobile banking: The bank’s mobile banking department handles quite a few customer-facing mobile applications and services. These services include:

- UPI (Unified Payments Interface), which combines multiple bank accounts, merges several banking features, which helps in integrating seamless fund routing and merchant payments into a single mobile application (of any partner bank).

- YONO Lite: The bank introduced features such as cheque lodgement through a positive pay system, a QR-Code based ATM cash withdrawal, RTGS 24*7, an SIA Chatbot, and applying for IPO, Debit card issuance tracking through YONO lite.

- SBI Quick: The bank launched facilities such as cheque lodgement through positive pay system, Missed call and SMS-based loan lead generation for home loans, car loans, personal loan, gold loan, Mobile Top-up and Recharge facility, SBI Samadhaan consolidation in SBI Quick app for its customers

- Digitisation of the Stressed Asset Recovery Group (SARG): Digitised various formats and processes of SARG on the LLMS platform through an end-to-end process. This has led to the standardisation of proposal formats, process flows, and the creation of corporate memory. SBI established the sanctions committee in LLMS.

IT strategy

SBI uses technology in its value proposition, including business, designing products, streamlining processes, and improving delivery to credit monitoring. It is always looking for ways to be technologically relevant and become a smart bank to partner with.

Post this pandemic, SBI has made technology an essential part of its infrastructure to maintain its productivity and efficiency. This move also helps them cater to its customers’ broad range of banking needs without making them step outside.

The bank took the following initiatives throughout 2020:

Functional features

- The bank deployed a Virtual Private Network (VPN) to enable Work from Anywhere (WFA) and ensure business goes on as usual

- Set up 600 4G connectivity connections for mobile van ATMs to ensure easy cash withdrawals during peak periods of the pandemic

- Replaced unreliable and high-latency network links with low-latency wired and terrestrial wireless links to improve network experience and minimise branch isolations

- In the process of establishing two advanced network operating centres based on artificial intelligence (AI)/machine learning (ML) and analytics (NOC1 and NOC2)

Ease of use features

- It acts as a payment aggregator and payment gateway (ePay & PG), a unique PCIDSS-certified secure platform to facilitate seamless e-commerce transactions between businesses, merchants, customers, and financial institutions for various types of payment. The platform works through the Payment Aggregator (SBI ePay) and Payment Gateway (SBIPG) applications by integrating thousands of merchants on the one hand and a multitude of payment channels such as banks, wallets and cards on the other. SBIPG processes all debit/credit card transactions from Payment Aggregators, SB Collect, SBIMOPS and YONO

- Carried out more than 19,592 merchant integrations to strengthen its e-collection, e-payment and e-commerce ecosystem

- Created online e-Mandates to pay EMI and other recurring amounts

- Introduced Cash Management Product, a technology driven platform that handles businesses such as government payments, cash and cheque deposits, VAN based collection of cash, cheques and e-collections, a Digi-dealer mobile app, and liquidity and mandate management. SBI is heavily promoting API based integrations for validating dealer data and pushing MIS

- Introduced YONO QR-based cash withdrawal on SBI MVS (Multi-Vendor Software) ATMs/ADWMs using the YONO Lite Application

Security features

- Initiated features like the generation of green PINS on SBI ADWMs, regular generation of green PINs, blocking of debit cards and issuance of replacement cards via IVR, and card issuance tracking for customers through INB

- Installed Multi-Vendor Software (MVS) and End Point Security (EPS) software to implement BIOS password, disable USB ports, update the operating system, EMV card readers, anti-skimming devices and other software to make ATMs secure

- Rolled out new features like OTP over email to Resident Indians, SMSs in Hindi, and a Real-Time Multiple Demand Loan for e-commerce transactions

- Enhanced security of customer accounts by introducing Captcha when logging in (image and voice), provision to block/unblock INB access, possibility to activate/deactivate UPI as a payment method.

SBI has also come up with various other IT solutions:

- Data warehouse: In order to cope with the ever-increasing data volume, the bank is implementing a first-class data warehouse solution, the “next generation data warehouse”, which aims to become the only source of truth for all data purposes of the bank. SBI is implementing an advanced analytical platform with components such as a data lake and virtualisation layer to improve its analytical capabilities.

- Data governance: The bank has established a company-wide data governance structure in the form of a data governance committee (DGC) at the corporate centre, business vertical, circle, and AO levels and has received support from data governance officers (DGO) at all levels. This strong data governance ensures sustainable growth and compliance with evolving data protection regulatory laws.

- Business Intelligence Department: Following the single source of truth (SSOT) principle, the bank decided to set the Business Intelligence Department (BID) as the SSOT for all types of reports/dashboards (regulatory and MIS). BID has developed various dashboards covering all key business areas that the bank needs to adopt for optimal use. Introducing these centralised dashboards will also reduce reliance on multiple data sources, reducing data stress on operating officials.

- Analytics: The bank continues to use and improve its analytical skills through AI/ML to increase efficiency, reduce risk and grow its business. Some projects completed using analytics during 2020 are:

- Digital lending: Business growth from e2e Digital lending through products such as a Two -wheeler loan, pre-approved personal and business loans, and POS online EMI, among others. In addition, the bank has developed a new AI-based model for SME New to Bank (NTB) customers.

- Risk mitigation using AI-driven models: Set up a fraud-prone branch model to identify high-risk branches. In addition, SBO deployed a suspicious-ATM-chargeback model with EWS to identify suspicious chargeback claims and detect early signs of stress in its borrowers. The bank also initiated an Intelligent Sampling of Vouchers (ISMOVVR) model for the identification of outlier vouchers for re-verification and to prevent frauds

- Operational efficiency: Carried out ATM network optimisation and Staff Optimisation through the footfall model (strategies to optimise the number of personnel working in a branch) and ATM win-back model (strategies to increase the number of customers using the ATM network), respectively. The bank also adopted an ML-based charges model to prescribe branches for proper classification and an NLP-based ML model to control income leakage.

- Centralised SWIFT Interface Gateway (CSIG): It is a centralised messaging system for cross-border transactions on the SWIFT network. It is an integrated web-based messaging software that runs centrally and is accessible through interface and branch channels, facilitating the electronic exchange of financial and non-financial messages.

Security strategy

The bank has put in place a robust cybersecurity framework. The bank has a cybersecurity wing, which specializes in ethical hacking of Internet applications. This is a proactive measure to fill gaps in applications before they are discovered and eventually exploited by outsiders. The framework includes:

- Approved standard operating procedures (SOPs) for internal ethical hacking of the bank’s infrastructure by employees. The bank has also established the Next Gen Global Cyber Security Operations Center (NGGCSOC). In addition, it has adopted advanced technologies like AI/ML capabilities to strengthen the bank’s cyber security status.

- The bank implemented a proactive risk management (PRM) solution to combat attacks such as phishing, credit card fraud, online banking fraud, and mobile banking fraud.

- The bank has fully complied with all 21 mandatory controls and ten advisory controls required by SWIFT.

ICT contracts

- Partnership with Hyperverge for its AI-powered video banking solution, which makes online account opening easy

- Collaborated with NPCI (National Payments Corporation of India) to launch “RuPay SoftPoS”, which helps to transform NFC-enabled smartphones into merchant Point of Sale (PoS) terminals

- Tied up with JPMorgan for its blockchain technology to speed up overseas transactions

- Associated with Titan Company to introduce contactless payment watches called ‘Titan Pay’, powered by YONO SBI

- Joined hands with Shivrai Technologies to make digital banking accessible to farmers

- Reached an agreement with Hitachi Payment Services Pvt Ltd to roll out a digital payment platform

9 Growth and Innovation Opportunities

- #1 Cost to serve

SBI saw an increase in its operating profit with USD 9.8 billion in 2020 compared to USD 9.3 billion in 2019. While that is good for the bank, it has also seen a significant increase of 9.95% in operating expenses from USD 10.27 billion in 2019 to USD 11.29 billion in 2020. The bank’s cost to income ratio has marginally increased from 52.46% in 2019 to 53.60% in 2020.

The bank witnessed an increase in personnel cost in 2020 to USD 6.95 billion from USD 6.24 billion in 2019. However, there was an overall decrease of 3,796 in the workforce count from 249,448 in 2020 to 245,652 in 2021. A possible inference can be that the bank laid of non-performing staff and added employees with specialised competencies to support its digital growth objectives. Hence, there was an increase in the bank’s personnel cost.

Branch maintenance expenses decreased compared to the previous year, from USD 729 million to USD 717 million.

On the other hand, insurance and other expenses continued to increase in comparison to 2020. On the other hand, the repairs expenses and advertisement expenses also decreased compared to last year.

There was a slight increase in the net interest margin compared to the previous year (from 3.19% to 3.26%) and a decrease in gross NPA to 4.98% from 6.15%, which seems like a good sign for SBI.

While the bank is making efforts to become digitally efficient internally and externally – it must take stringent measures to manage its operating expenses. SBI can concentrate on the following significant areas to optimise cost efficiency:

- In a low-interest-rate environment, SBI should detect payback risk in loans and attrition risk in deposits to manage a good net interest margin. In addition, SBI can use predictive behavioural models to continuously adjust the bank’s interest-rate risk estimates and hedging strategies.

- The bank can focus on non-interest income and complementary revenue streams to offset the impact of substantial NPA provisions.

- SBI can consolidate vendors to decrease costs and also maintain vendor relationships to gets optimal prices and thus cut costs in the long run

- It can Increase focus on retail and SME business with tight control on the asset quality, as these are the businesses with the maximum market share

- SBI can apply RPA-enabled audit trails for red-flagging any high-cost inflexions by implementing transaction-level transparency.

- #2 Transformation of the branch and its branch networks

SBI pushed development patterns towards outlet transformation and smart operation. The bank has 71,968 operating BCs, around 22,219 branches and 62,617 ATMs, including 13,237 Automated Deposit & Withdrawal Machines (ADWMs). The bank also introduced SWAYAMs (self-passbook printing kiosks) spread across 15,857 branches. This includes 8,181 kiosks in ATM rooms/e-lobbies/Through the Wall (TTW) available outside SBI branch lounges for extended hours.

From 2019 to 2020, SBI reduced its physical network costs from USD 153 million to USD 152 million. On the other hand, the number of branches increased from 22141 to 22219 in comparison to 2019. One can infer that this decrease in maintenance cost might be due to the adoption of the branch workforce model, the reduction in personnel (from 249,448 in 2020 to 245,652 in 2021), and subsequent costs for the same.

This move provides a reduction in the maintenance cost of branch networks. The bank should continue its efforts to reduce any non-performing branches or ATMs and focus on transforming the network through:

- SBI can replace ATMs and increase the number of ADWMs, making it easier for consumers and also save costs at the same time.

- The bank should transform high business volume and high-customer-headcount branches into flagship digitalised community hubs that enhance the in-branch experience and redefine customer engagement. In order to accomplish this, SBI should:

- Introduce smart counters – They can move many services done by personnel to smart counters, reducing the need for human tellers to work in bank branches. Furthermore, smart branch technology enables a personalised sales strategy and 24/7 access to the bank branch.

- It can establish an omnichannel user experience, one that will link SBI Internet Banking, Mobile Banking and physical branches with Virtual Assistants and other automation processes. This holistic channel will provide customers with a consistent experience, whether online, on a mobile device, or at the branch. It will also result in higher efficiency at the bank branches.

- While bank staff are necessary for high-traffic, high-visibility urban locations, SBI can establish fully self-serviced branches for greater physical footprint penetration at lower costs. These branches will be able to provide complete services through video conferencing.

- #3 Customer experience

The bank is leveraging CRM tools to use analytics and AI to transform structural banking into digital banking. These digital tools will garner a positive customer experience in the future. SBI has a diverse and robust portfolio of products and services and leverages technology to deliver and manage them in a personalised and customer-centric manner. The bank can further leverage its capabilities through AI and can work in these areas to optimise the customer experience journey:

- The bank should move towards providing an omnichannel experience to its customers so that they have the same digital and physical experience

- SBI provides customer support 24/7. It can, however, work on the day-complaint resolution by prioritising Chatbots, virtual assistants, and video conferencing to increase the number of complaints handled.

- It can provide insights for customers into their saving and spending patterns with specific recommendations to help them meet their financial goals

- A gamified user interface to make the customer experience interactive rather than monotonous

- Introduce virtual assistants and chatbots to handle front-end customers

- Introduce a different platform to serve the high-net-worth individuals with more sophisticated investment needs

- AI-powered voice banking to offer proactive, personalised, and automated money management

- Introduce a digital investment dashboard that gives their high-net-worth clients an integrated view of their portfolios at a glance, allowing them to track and manage their wealth in real-time

- #4 Employee experience and productivity

SBI has made significant investments in employee development and offers a flexible work atmosphere. However, the bank should consider offering the following strategies:

- Expand its employee wellbeing plan with targeted mental, emotional, spiritual, and physical wellbeing programs through:

- Gender-neutral parental leave

- Childcare facilities

- Counselling services

- Domestic & family violence workplace support for women

- Health and wellbeing support through online portals with 24/7 availability

- Use an AI chatbot and a virtual recruitment assistant to match suitable candidates with high-skill jobs

- Provide hassle-free student loans to new hires for controlling attrition rates among the said hires, hence increasing employee loyalty

- Employees experiencing financial hardship should have access to a confidential service provided by a team of dedicated specialists, and the bank can put aside a special fund for such conditions to help them

- #5 Migration of workload to the cloud

SBI invests nearly USD 20,000 for data centre hosting and cloud hosting monthly. It can invest in cloud technology to further amplify its capabilities by using these strategies:

- SBI should use a cloud-based platform to streamline various talent management and HR-related tasks.

- In order to increase efficiency, cloud adoption can prove to be an imperative move, as it improves on a variety of additional activities that go beyond the customer and employee experience. For example, the bank can extend data storage and data-driven activities across security, regulatory compliance, auditing, and pan-organisation communication pipelines to modernise its overall operating model.

- The bank’s long-term strategy should be to move most of its operations to the public cloud. This move enables SBI to secure end-to-end encryption on all its confidential data in the cloud, as well as achieve higher scalability and cost-efficiency.

- #6 Neo banking

SBI has added significant features into its mobile banking app to make it more appealing. Still, it needs a transformational neo banking strategy to keep pace with other rising neo banks in India. SBI must continue positioning SBI YONO as a millennial and Gen Z digital banking platform. This can be done by:

- Collaborating with a suitable fintech firm to effectively position themselves among millennials

- Introduce in-app virtual assistant to deliver proactive notifications, budgetary recommendations, as well as lending and investment choices to customers

- Attempt to hyper-personalise its products to fulfil customers’ unstated and hidden demands.

- Introduce customised debit cards, credit cards, and virtual cards

- Introducing bite-sized loan and investment solutions, giving customers more flexibility when navigating through product possibilities.

- Gamifying numerous consumer touchpoints. These include awarding badges for increased product usage, providing loyal customers with discount coupons, creating a leader board between friends and co-workers based on product purchases, and showcasing trending products.

- Enable multi-currency accounts with zero to minimal cross border remittance fees

- The bank should aim towards integrating customer data from its legacy banking channels and leverage open banking to access historical customer transaction data and credit history

- It could also use the same data to automate the application approval process at the back-end. This step will further help SBI to build a robust customer remediation process.

- The bank can introduce interactive dashboards, create an online community or hub, and have blogs or resources on financial literacy to create a unique brand name for itself.

- #7 Cybersecurity

SBI has a strong cybersecurity framework in place, and it has taken proactive steps to safeguard customers against security risks. However, despite taking these steps, the bank’s customers have recently been the target of phishing attacks through suspicious text messages. Therefore, the bank can take the following initiatives to avoid such scams and strengthen its cybersecurity:

- Enhance security monitoring and the surveillance of malicious online activities as scammers migrate to cyber measures, such as phishing, to defraud customers.

- Deliver a general security awareness programme to employees via an e-learning platform

- Invest in ML capabilities and security orchestration in a bid to stay ahead in the cyber arms race

- Implement robust and multi-factor authentication and micro-segmentation to secure internal access to key applications and limit attack surfaces

- The bank can further develop its in-house:

- Risk-based vulnerability management programme to improve cyber risk prioritisation and mitigation efforts

- Crowdsource its cyber threat intelligence platform to provide predictive analysis of potential cyber threats and attacks

- #8 Artificial Intelligence (AI) in everything

SBI is at an early stage of adopting AI into its business model. As it is still at the nascent stage, the bank should begin with:

- Automating labour-intensive back-end and iterative daily tasks like customer onboarding, document collation, book-keeping, sales recording, etc., through RPA. This automation will reduce labour redundancy and increase the overall operational efficiency of the bank.

- Developing a sophisticated and forward-looking credit profiling method for business banking customers. It can use predictive analytics to assess loan credibility beyond financial statement analysis. Other essential criteria that can be a part of the profiling mechanism include economic KPIs, market and industry trends, bank and system facility overviews, and more.

- Leveraging its data analytics capabilities to seek contextualised data insights that the bank can use to innovate its product offerings and delivery channels.

- Have AI-based marketing of products and targeted campaigns based on the past behaviour of customers

- Extend AI services beyond banking and focus on customer problems, rather than just financial needs to become a trusted advisory service beyond banking

- #9 Society and planet contribution

SBI has steered activities around healthcare, education, livelihood, sports, environment sustainability and empowerment of women, youth and senior citizens. However, it should aim to reduce its carbon footprint by using the following strategies:

- Building on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid

- Utilise energy-efficient devices by making one-time investments and saving costs in the long-term

- Use excess energy during low or off-peak times to decrease energy usage

- Reduce its carbon footprint by switching to pulper cards, eco ink and carbon control press machines

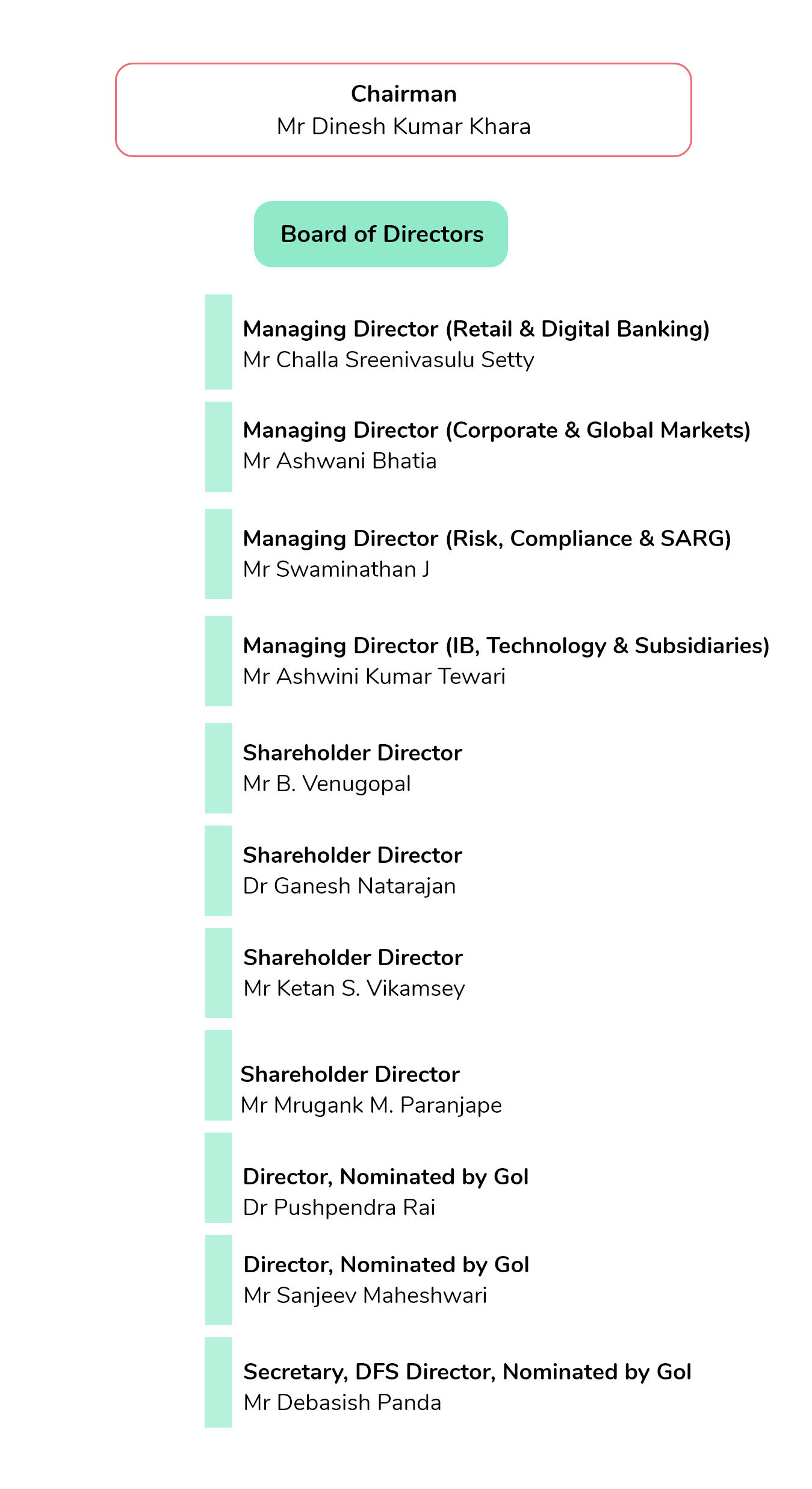

Organisation structure: Leadership

Executive Profile

Mr Dinesh Kumar Khara

Chairman

Mr Khara is the Chairman of the State Bank of India. He joined as a Probationary Officer back in 1984 and has over 36 years in all facets of banking. Mr Khara has an MBA degree from FMS New Delhi and a postgraduate in Commerce from the Delhi School of Economics. Besides that, Mr Khara is a Certified Associate from the Indian Institute of Bankers (CAIIB).

Quote

- Technology and Innovation, Annual Report 2021

At State Bank of India, we are leveraging technology in every aspect of the value proposition: from business, designing products, streamlining processes, and improving delivery

Mr Challa Sreenivasulu Setty

Managing Director (Retail & Digital Banking)

Shri Challa Sreenivasulu Setty is the Managing Director of State Bank of India, and he looks after Retail & Digital Banking. He has a BSc in Agriculture and is a Certified Associate of the Indian Institute of Bankers. He started his career with the bank as a Probationary Officer as well. In over three decades, he has gained rich experience in corporate credit, retail banking and banking in developed markets.

Mr Ashwani Bhatia

Managing Director (Corporate Banking & Global Markets)

Mr Ashwani Bhatia has been MD of SBI since August 2020. In his current job role, he looks after the Corporate Banking & Global Markets verticals. He started his career with the bank as a Probationary Officer. Mr Bhatia is a Graduate in Physics & Mathematics from Dayalbagh University, Agra and is an MBA from Poddar Institute of Management, Jaipur

Mr Swaminathan J.

Managing Director (Risk, Compliance & Stressed Assets Resolution Group)

Mr Swaminathan has a career spanning an extensive 32 years with SBI. He has held various assignments across Finance, Corporate and International Banking, Trade Finance, Retail and Digital Banking and Branch Management. Mr Swaminathan is a Certified Anti-Money Laundering Specialist (CAMS) and also a Certified Documentary Credit Specialist (CDCS).

Mr Ashwini Kumar Tewari

Managing Director (International Banking, Technology & Subsidiaries)

Ashwini Kumar Tewari started his career in SBI as a Probationary Officer. He is the Managing Director of SBI, handling the portfolio of International Banking, Information Technology and Associates & Subsidiaries of the Bank. He has a degree in electrical engineer, and he is also a Certified Associate of the Indian Institute of Bankers (CAIIB), a Certified Financial Planner (CFP). He also has a Certificate Course in Management from XLRI.

Mr B. Venugopal

Shareholder Director

Mr Shri B. Venugopal is a director re-elected by the shareholders. A graduate of the University of Kerala in Commerce and Cost Accounting, he is the Independent Director on the Boards of SBI as well as National Commodities and Derivatives Exchange Ltd (NCDEX).

Dr Ganesh Natarajan

Shareholder Director

Dr Natarajan is a director elected by the shareholders. He is the Chairman of Pune City Connect and Social Venture Partners India and received the Distinguished Alumnus Award from NITIE and IIT Bombay. Dr Natarajan is also the founder and chairman of 5F World, a platform for Global consulting and Investing in Digital Skills and Digital Transformation.

Mr Ketan S. Vikamsey

Shareholder Director

Mr Vikamsey is a director elected by the shareholders. He is the chairman of the HLB India Federation. He has a lot of experience in audit of large banks, manufacturing concerns, Investment Banks, Insurance Companies and Mutual Funds.

Mr Mrugank M. Paranjape

Shareholder Director

Mr Paranjape is a director elected by the shareholders. He has a B.Tech degree from IIT, Mumbai and a PGDM from IIM Ahmedabad. Mr Paranjape has over three decades of experience in Banking, Capital Markets, Asset Management and Stock Broking, covering varied functional and geographic areas. He is currently serving as the MD & CEO of NCDEX eMarkets Limited.

Dr Pushpendra Rai

Director Nominated by Gol

Dr Rai is a director nominated by the Central Government, and he has around 38 years of professional experience in both national and international institutions. He has a PhD from IIT, Delhi, and postgraduate degrees from Harvard University and the University of Lucknow. Dr Rai has lectured extensively worldwide.

Mr Sanjeev Maheshwari

Director Nominated by GoI

Mr Sanjeev Maheshwari is a director nominated by the Central Government. He is a Chartered Accountant and Insolvency Resolution Professional with over three decades’ worth of experience in Audit, Taxation and Management Consultancy.

Mr Debasish Panda

Secretary, DFS Director, Nominated by GoI

Mr Debasish Panda is a director nominated by the Central Government. He is the Secretary to the Dept of Financial Services, Ministry of Finance, Government of India. He has Post-Graduation degrees in Physics, Developmental Management and an M. Phil degree in Environmental Sciences.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

State Bank of India, (2021, March 31). Annual Report 2021

https://sbi.co.in/documents/17826/24401/100621-SBI+AR+2021.pdf/d6140d38-deb4-f2bc-1e5b-67f88e27a0dd?t=1623305095334

State Bank of India, (2021, March 31). International Operations

https://sbi.co.in/corporate/AR1920/download_center/english/11-3.13-International%20Banking%20Operations.pdf

State Bank of India, (2021, March 31). Investor Presentation 2021

https://sbi.co.in/documents/17836/4840865/210521-Analyst+PPT+Q4FY21.pdf/32e83025-b60d-a2a2-9a8e-a7dfbea7ca09?t=1621585332152

State Bank of India, (2021, March 31). Sustainability Report 2021

https://sbi.co.in/documents/17826/24401/140621-Sustainability+Report%28SR%29+year+2020-21.pdf/ba271367-9542-e96a-0589-2968954b2e17?t=1623659643326

Wall Street Journal. State Bank of India financials. Retrieved August 27, 2021 from

https://www.wsj.com/market-data/quotes/IN/500112

CurrentAffairsAdda247. State Bank of India. Retrieved August 27, 2021 from

https://currentaffairs.adda247.com/?s=sbi