Market highlights

- The escalation of contagion risks amid global turmoil in the Malaysian economy will affect banks’ revenue cycles and net interest margin growth.

- Rising interest rates and funding costs are expected to slow credit growth to 4 – 5%.

- High household deposits add funding stability, contributing ~36% to total system-wide deposits.

- Net interest margins (NIM) are expected to drop by 5 – 10 basis points from the current ~2%.

- The NIM decline will be balanced by tax rate normalisation.

- A pick-up in the net interest income (NII) could also potentially offset NIM compression due to higher savings rates and intense competition among banks.

- Malaysian banks enjoy non-performing loans (NPL), which are lower than most APAC regions.

- The current average NPL for Malaysian banks stands at 1.7%.

- NPLs expect to increase by 50 – 60 basis points in 2023 and 2024 due to the vulnerability of low-income households and SMEs to rising interest rates.

- Fee income distribution for Malaysian banks is restricted to traditional fees. However, there is a significant opportunity with open banking among banks and financial services.

Key challenges

- #1 Rising non-performing loans

- NPLs in Malaysia aim to increase by 50 – 60 basis points in 2023 and 2024.

- The top banks reported a 10 – 25 basis point increase in their NPLs during 2022.

- SMEs, unsecured loans and corporate loans drive the increase in NPLs.

- Low-income households and SMEs are vulnerable to rising costs, which could moderately increase the NPLs.

- #2 High household debt

- Household debts in Malaysia are among the highest in the Asia Pacific.

- Household debts accounted for 81% of the country’s nominal GDP in December 2022 at USD 330 billion.

- The high household debt stems partially because homeowners struggle to make repayments, leading to increased credit risk for banks.

- The increase will likely reduce loan growth as people are reluctant to take additional loans.

Financial highlights

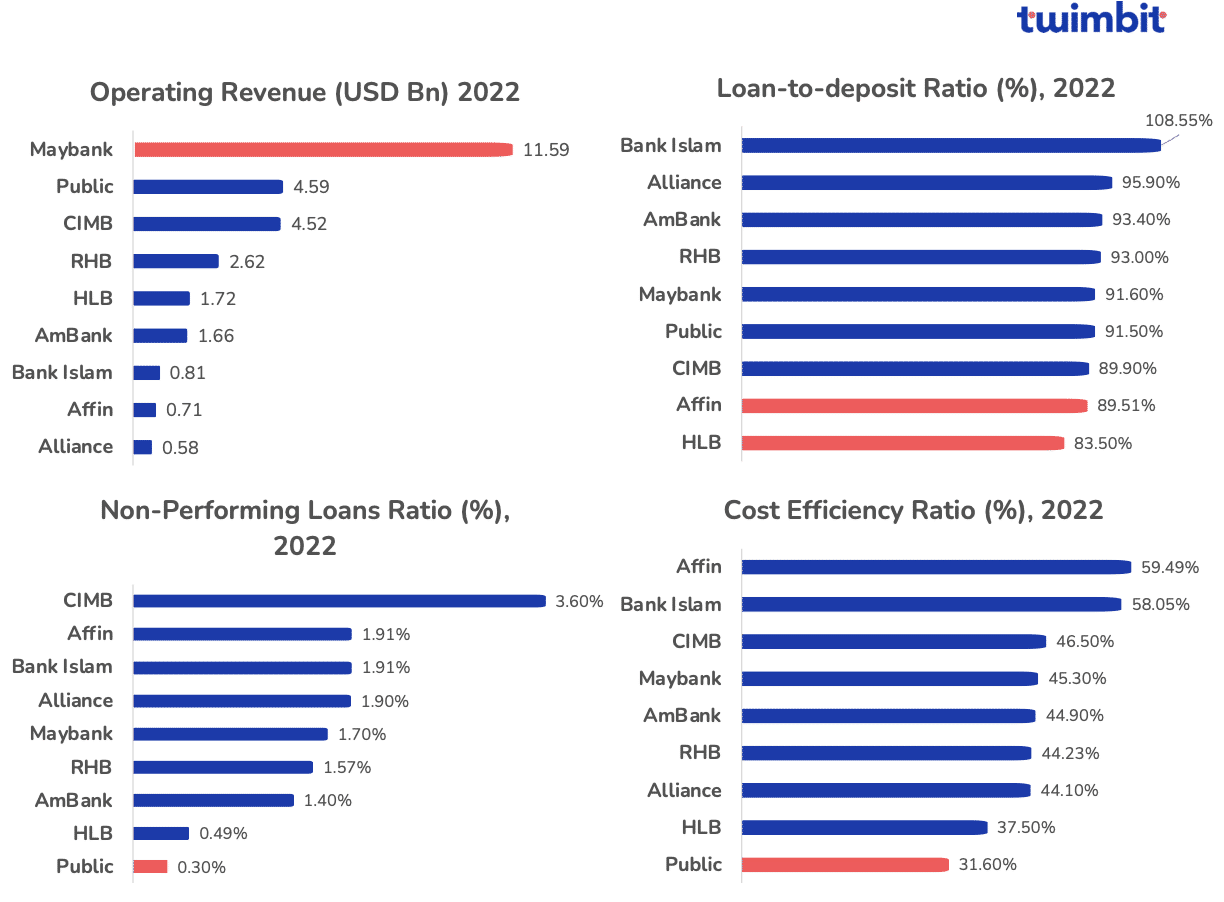

- Operating revenue

- The average operating revenue in APAC is USD 27.17 billion.

- No Malaysian banks have their revenue at par or above this average.

- Apart from CIMB and Public Bank, none of the banks in Malaysia has their fee income to revenue proportions above the APAC average of 12.06%.

- Loan-to-deposit ratio

- The average loan-to-deposit ratio for Malaysian banks is 93%, well above the threshold value of 80 – 90%.

- The net interest margins of all these banks are below the APAC average of 3%.

- The NPL is below the APAC average of 2.14% for all but CIMB which stands at 3.6%.

- Public Bank and HLB have impressive NPL ratios at 0.3% and 0.49%, respectively.

- Cost efficiency

- The cost efficiency ranges from 31 – 60%, averaging 45.7%, slightly above the APAC average of 45.3%.

Top initiatives by Malaysian banks

- #1 Public Bank

Payment ecosystem:

- Public Bank became the first Malaysian bank to launch DuitNow online banking/wallets and QR-based cross-border payments.

- Public Bank accepted QR international payments from Indonesia, Singapore and Thailand.

Collaboration with Carsome:

- The bank entered a Memorandum of Understanding (MoU) to offer stock financing and end financing solutions for vehicles to member car dealers and individual buyers who have successfully secured bids through the Carsome online portals.

- The collaboration allows Public Bank to interface with Carsome’s online platform, streamlining vehicle financing and minimising documentation for successful bids.

Empowering SMEs:

- The bank has partnered with digital solution providers in the PB Enterprise Digital SME Assist program.

- The partnership offers customers various digital business solutions, including human resource management, property management, cloud-based accounting and payroll solutions.

- #2 HLB

HLB ConnectFirst:

- Provide a consolidated view of customer payments, transactions and accounts through a new digital banking platform.

- The platform’s launch resulted in a year-on-year customer growth of 11% to nearly 100,000, with an average of 1.5 million monthly transactions.

Apply@HLB:

- HLB became the first Malaysian bank to offer its customers end-to-end digital onboarding without the need to visit a branch or use a self-service terminal.

- The app resulted in a six-fold increase in accounts opened through the channel compared to 2021.

HLB BizBuddy:

- The app allows business owners to accept customer payments through various QR code options.

- Businesses can monitor, track and analyse real-time transactions to gain valuable insights.

- HLB enables instant refunds in case of same-day purchase cancellations, creating a seamless and efficient customer experience.

CX Lab:

- CX Lab promotes cross-departmental cooperation with conducive product idea generation and prototyping settings.

- Businesses can gather insights through various techniques, including A/B testing, gaze tracking, and quantitative, ethnographic, and qualitative research.

- CX Lab can act upon comprehensive consumer insights to better address consumer needs.

- In FY2022, CX Lab conducted;

- 27 customer research projects

- 59 usability testing sessions

- 13 post-launch evaluation initiatives

- #3 Maybank

ATM Cash-out:

- Malaysia’s first contactless cash withdrawal service.

- Customers can withdraw cash by scanning a QR code on Maybank ATMs using the MAE app.

Home2u:

- Home2u is integrated within the MAE app and is Malaysia’s first digital home financing solution that offers a seamless home-buying experience.

- Customers can browse properties and get home loan approvals within 10 seconds.

- Customers can also choose contractors to help set up their homes after purchase, providing end-to-end support in the home-buying experience.

Partnership with Apple:

- Maybank is one of the first Malaysian banks to partner with Apple and introduce Apple Pay nationwide.

- The partnership enables Maybank and Maybank Islamic Mastercard and Visa credit, debit and prepaid card users to make contactless payments via their iPhone or Apple Watch in Malaysia and Singapore.

- #4 AmBank

Fintech Partnerships:

- Established Fintech partnerships via Payment Service Agents (PSAs) for PayNet’s RPP products and services.

- Provided customised solutions to Fintech partners (Money Service Businesses “MSB”) for digitising inward remittance through DuitNow transactions using APIs.

- Expanded and introduced DuitNow QR services through API for smooth reconciliation with the dynamic DuitNow QR.

- Introduced hybrid e-wallets that combine current accounts with cross-border, multi-currency payment solutions in partnership with Merchantrade Asia.

Enhancing digital efforts:

- The bank’s digital account opening platform allows end-to-end digital account opening for SMEs and retail customers.

- The platform became Malaysia’s first fully end-to-end eKYC business current account opening for SMEs.

- The ‘One-Touch’ mobile app is for drivers on the road in the event of any road emergency.

- The ‘OneUp’ mobile app provides agents with up-to-date sales information or performance management modules and allows call-to-actions.

- #5 CIMB

CIMB Octo:

- The bank launched its first fully digital savings account and introduced the CIMB Octo Debit Mastercard as part of its strategy to expand the CASA base.

- The account opening and onboarding process is conducted entirely online under five steps.

- Customers receive their debit cards directly through the mail, offering a convenient branchless experience.

- Users can engage in a gamified experience with missions and challenges, allowing them to earn points and receive instant rewards.

EVA chatbot for SMEs:

- EVA is Malaysia’s first Natural Language Processing (NLP) powered chatbot for commercial banking, offering conversational and real-time interactions.

- SME customers can access EVA 24/7, receiving instant and consistent answers to their queries.

- EVA acts as an electronic relationship manager, assisting SMEs in selecting suitable financial relief assistance for their business needs.

- EVA’s Eligibility Check feature digitises and streamlines the lengthy process of engaging with a sales representative.

Growth opportunities

- #1 Digital-only banks

Neobanks have been disrupting traditional banks with superior customer experience, ease of use, and popularity among the younger generation, attracting a large customer base at lower acquisition and service delivery costs.

Malaysia’s nascent neobank sector presents a significant opportunity for local banks to leverage, with an expected 14.24% CAGR growth between 2023 and 2027.

Recently, Bank Negara Malaysia has announced five digital banking licenses approved by the Ministry of Finance Malaysia. The licenses have been split into two categories and are given to the following consortiums:

- Financial Services Act 2013 (FSA):

- Boost Holding and RHB Bank consortium

- GXS Bank and Kuok Brothers consortium

- Sea Group and YTL Digital Capital consortium

- Islamic Financial Services Act 2013 (IFSA):

- AEON Financial Service Co., Ltd., AEON Credit Service (M) Berhad and MoneyLion Inc. consortium

- KAF Investment Bank consortium

- #2 Buy Now Pay Later (BNPL)

BNPL is fast becoming a popular payment choice among APAC consumers. Hence, BNPL fintech companies are offering this lucrative payment option, which is currently dominating the market share of traditional bank fees.

The Malaysian BNPL payment adoption seeks to grow at a CAGR of 35.4% between 2022 and 2028 and reach USD 6.88 billion by 2028.

None of Malaysia’s top banks currently offer a true BNPL service. The closest to this is AmBank and CIMB, who both offer an instalment service on their credit cards. For instance, AmBank’s AmFlexi-Pay charges a 6% interest rate, while CIMB’s Easy Payment Plan (EPP) does not charge any interest.

A competitive BNPL offering will help Malaysian banks in the following ways:

- Attract younger customers who prefer flexible payment options.

- Increase customer engagement with user-friendly payment experiences.

- Form new merchant partnerships to strengthen and expand market reach.

- Increase revenues and improve profitability.

- Improve cross-selling of other products and services by utilising customer data and insights from BNPL transactions.

- #3 Open banking

As the NIM for Malaysian banks continues to decline with slow loan growth and high household debt, banks need to find new revenue streams from non-interest sources to maintain profitability.

Open banking can help Malaysian banks generate fee income in the following ways:

- Account aggregation

Account aggregation enables customers to consolidate their financial information from multiple accounts across different institutions into a single platform or app. Because of this, customers can view all their financial information in one place, helping banks become a central hub for managing finances.

A current example of account aggregation being implemented in Malaysia is PhonePe, an API-based account aggregation service.

- PhonePe enables users to manage their finances, track transactions, transfer funds, and make payments seamlessly from the PhonePe app.

- Streamlined payments and transfers

Open banking simplifies payment processes and facilitates faster and more secure transfers. Banks can offer customers the ability to initiate payments directly from their accounts using open banking APIs. This self-serve capability eliminates the need for traditional payment methods and reduces transaction costs.

A current example of this is PayTm.

- Paytm leverages open banking APIs for faster and real-time transactions, improving payment and transfer speed for users.

- Lending and credit scoring

Banks can leverage open banking to enhance their lending processes by utilising customer financial data for accurate credit assessments and personalised loan products. This will provide secure access to customer financial information.

A leading example is MYbank, which uses open APIs and collaborations with other financial institutions to gain access to consumer financial information.

- MYBank conducts better assessments when identifying the creditworthiness of borrowers.

- Identity verification

Open banking simplifies the account verification and KYC processes for banks. Banks can verify customers’ identities more efficiently and securely by accessing customer financial data through open banking APIs. It also enables secure sharing of customer data for identity verification purposes.

For instance, CIMB Bank Philippines has already embraced open banking, leveraging Junio’s AI-powered end-to-end identity verification and authentication solution.

- Real-time fraud prevention

Open banking APIs enable banks to enhance their fraud prevention capabilities because of the API’s real-time capability to analyse customer financial data. In addition, banks can also detect suspicious transactions or patterns and take proactive measures to prevent fraud.

A notable example is CommBank, which is equipped with a fraud detection engine and driven by Al, with real-time decline and hold intervention capabilities.

To know about the State of Australian Banks in 2023, click here.

To know about the State of Indian Banks in 2023, click here.

To know about the State of Singapore Banks in 2023, click here.

To know about the State of Vietnamese Banks in 2023, click here.

To know about the State of APAC Banks in 2023, click here.