Executive Summary

- The cumulative Beyond connectivity revenues of the 23 telcos analysed accounted for 24.5% of their cumulative total revenues in H1 2023, up from 22.6% in H1 2022

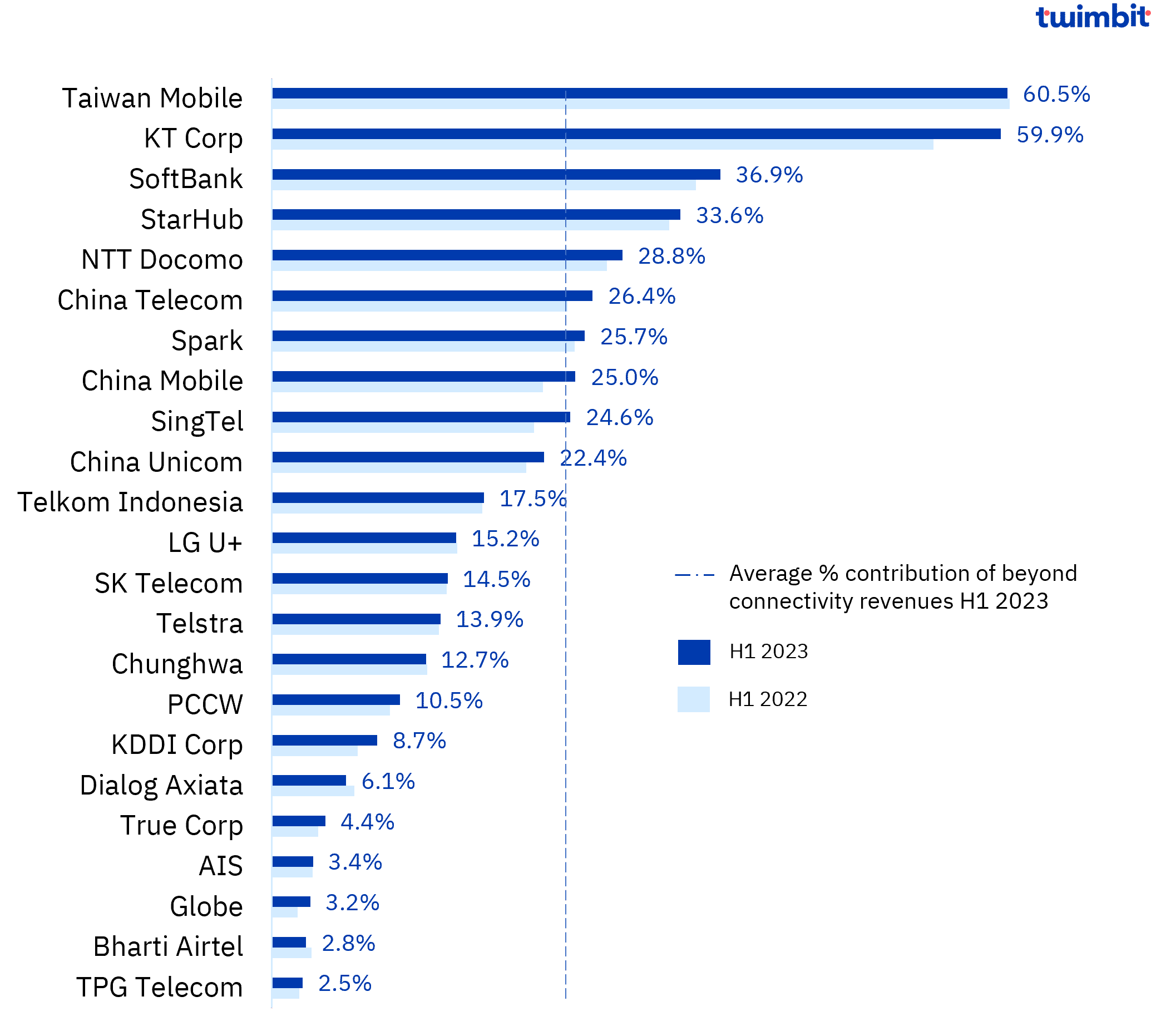

- Top Telcos: Eight telcos surpassed the 25 percent threshold in beyond connectivity revenue contribution exceeding of their total revenues, showcasing their diversification into a broad range of services. Taiwan Mobile led with an astonishing 61.7% of its revenues originating from beyond connectivity services, followed closely by KT Corp at 59.9%.

Exhibit 1: Contribution of beyond connectivity revenue to total revenue, H1 2023 (%)

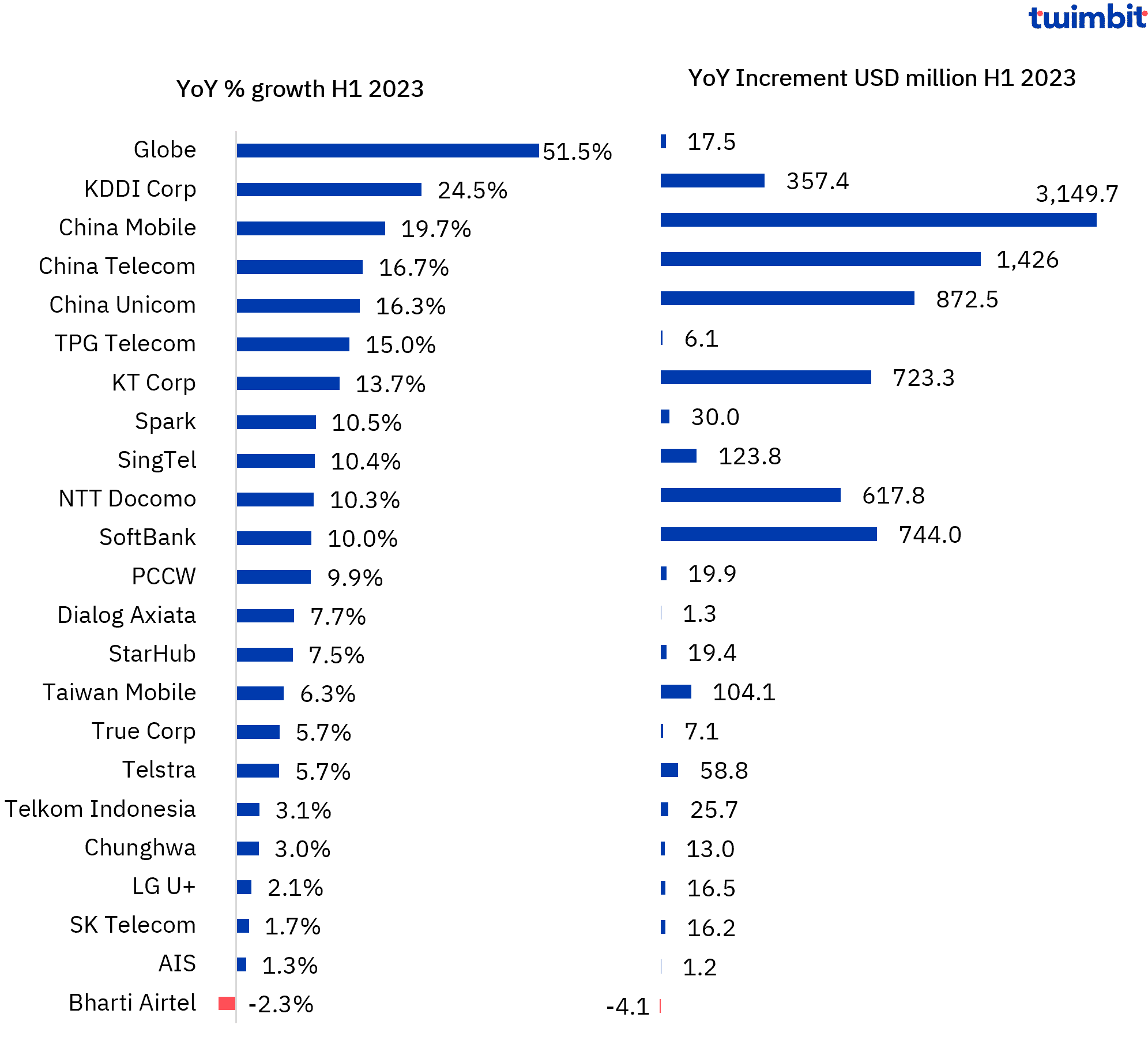

- Growth in beyond connectivity revenues: Beyond connectivity revenues for APAC telcos covered in this analysis witnessed a growth of 14.3% YoY in H1 2023, reaching USD 66.6 billion. In contrast, the overall revenue growth for the 23 telcos stood at 5.4% YoY in H1 2023, totalling USD 271.3 billion.

- Value of incremental revenues: The telcos added USD 8.4 billion beyond connectivity revenues in H1 2023 over H1 2022. China Mobile led the way with the highest incremental beyond connectivity revenue growth of USD 3.2 billion, reaching a total of USD 19.2 billion, representing a robust 19.7% YoY growth in H1 2023.

- Growth across the board: 22 out of the 23 telcos, which report beyond connectivity revenues achieved growth in H1 2023. Globe led the way with the highest growth rate of 51.5% YoY, resulting in beyond connectivity revenues of USD 17.5 million.

Exhibit 2: Percentage growth and increment in beyond connectivity revenues in H1 2023 YoY

Taiwan Mobile leverages automated logistics technology for its e-commerce segment

Taiwan Mobile continued its dominance in beyond connectivity revenues, reporting a remarkable 60.5% contribution to total revenues, amounting to USD 1.8 billion (TWD 53.4 billion). Within this, the e-commerce segment (momo) made a substantial 58.1% contribution, while Pay TV, content, and channel leasing accounted for 2.4%. Taiwan Mobile’s e-commerce revenue far surpassed that of any other regional telco.

As of Q2 2023, it had built 55 warehouses (+4 YoY). It also has ambitious plans- southern distribution center slated to launch early next year, followed by a central distribution center in subsequent years. momo has introduced leading automated logistics technology, offering high-density storage, simplified processes, and lower error rates.

Exhibit 3: momo north district automated logistics center

Taiwan Mobile is also focusing on enhancing its customer loyalty program, introducing new use cases for momo coin and momobile bundle users. The inaugural momobile members day on May 20th‘ 2023 featured a plethora of exclusive deals for momobile users.

Furthermore, Taiwan Mobile ventured into the Telco Finance sector with the launch of “OP Pay Later” in Q1 2023. It is a Buy Now, Pay Later service that utilizes their extensive user base, data, and AI models to determine ideal credit limits for customers.

KT Corp shines with producing original content and entertainment services

KT Corp stood out as one of the most diversified telcos in the region, offering a portfolio encompassing content media, OTT services, financial and payment services, Cloud, IoT, AI, and commerce-related services. Their contribution from beyond connectivity services surged from 54.4% in H1 2022 to an impressive 59.9% in H1 2023, amounting to USD 6 billion (KRW 7.8 trillion)

In the media segment, IPTV growth was fueled by a high ARPU subscriber base. Subsidiaries KT Studio Genie and Sky TV produced 7 original dramas and 5 entertainment programs in the first half of the year, solidifying their presence in the media and content market.

Exhibit 4: KT Corp content and media value chain

In just one year since its inception, KT Cloud has established itself as South Korea’s leading DX (Digital Transformation) company with a valuation of USD 3.2 billion (KRW 4 trillion). Furthermore, KT’s AI cloud business has surged, with a remarkable 18.5% YoY revenue increase in Q2 2023, totalling USD 123 million (KRW 153.8 billion).

In the financial payments sector, BC Card (a leading South Korean financial services company) recorded a 5.9% YoY revenue increase in Q2 2023, reaching USD 839.4 million (KRW 1,049.2 billion). This growth stems from higher credit card acquiring volume and ongoing new business development, including BC branded cards and lending services.

SoftBank’s financial segment, PayPay, achieves the profitability milestone

SoftBank emerged as another well-rounded telco with beyond connectivity revenues reaching USD 8.2 billion (JPY 1.1 trillion), constituting 36.9% of total revenues, and growing at a steady 10% YoY in H1 2023.

They strategically repositioned their “Yahoo! JAPAN / LINE segment” as Media and E-commerce (EC), accounting for 26% of total revenue. Their financial services division, coupled with PayPay’s first profitable quarter in Q2 2023, contributed to this impressive growth.

Exhibit 5: SoftBank portfolio of financial services

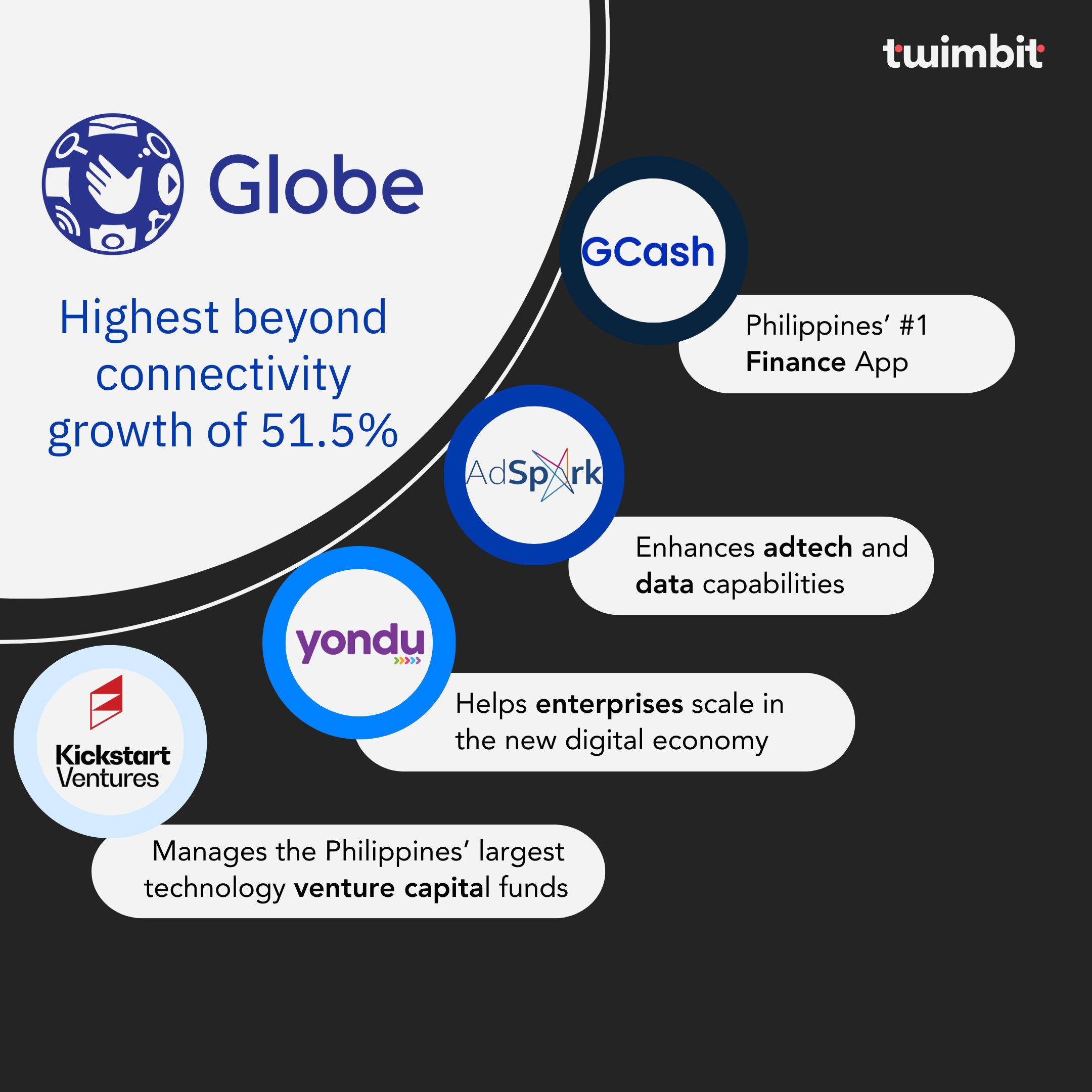

Globe Telecom’s Gcash is the leading finance app in Philippines

Globe experienced the most rapid growth in beyond connectivity revenue of 51.5% YoY in H1 2023, resulting in PHP 2.8 billion (USD 51.5 million) and accounting for 3.2% of total revenues.

Globe’s financial services segment, particularly GCash, established itself as the leading finance app in the Philippines. It is 5 times larger than the next e-wallet company in the country. With a vast user base, extensive network of 6 million merchants, and comprehensive suite of digital financial services, GCash has made significant strides in providing accessible finance solutions. Additionally, it has gone beyond the borders and now offers payments in 13 countries through GCash Global Pay

Furthermore, Globe’s ideology of transformation from a telco to a techco company has expanded its vison. The telco offers unique digital services- digital marketing, venture capital funding for startups, virtual healthcare, e-commerce, business outsourcing, adtech, edutech, media, entertainment, etc

Exhibit 6: Beyond connectivity eco-system of Globe

KDDI notes great success in global data center and BPO market

KDDI witnessed a robust growth of 24.5% YoY in H1 2023 in its beyond connectivity revenues amounting to USD 1.8 billion (JPY 244.9 billion. This was primarily attributed to its Next core business, amounting to USD 1.6 billion (JPY 217 billion), witnessing a strong growth of 19.9% YoY in H1 2023.

KDDI excelled in IoT services, the total connections reached 34.5 million in Q2 2023 (+8.5 million YoY). In the Business and infrastructure services segment, it primarily focuses on Connectivity Data Center (DC) Business Expansion and Contact Center / BPO Service Integration.

Under the BPO segment, KDDI formed a new company i.e. Altius Link, which is a s a joint venture between KDDI and Mitsui & Co. The new company will help in the improvement of CX proposal through digital contact center and in global expansion including North America and Asia.

Exhibit 7: KDDI forming Altius Link

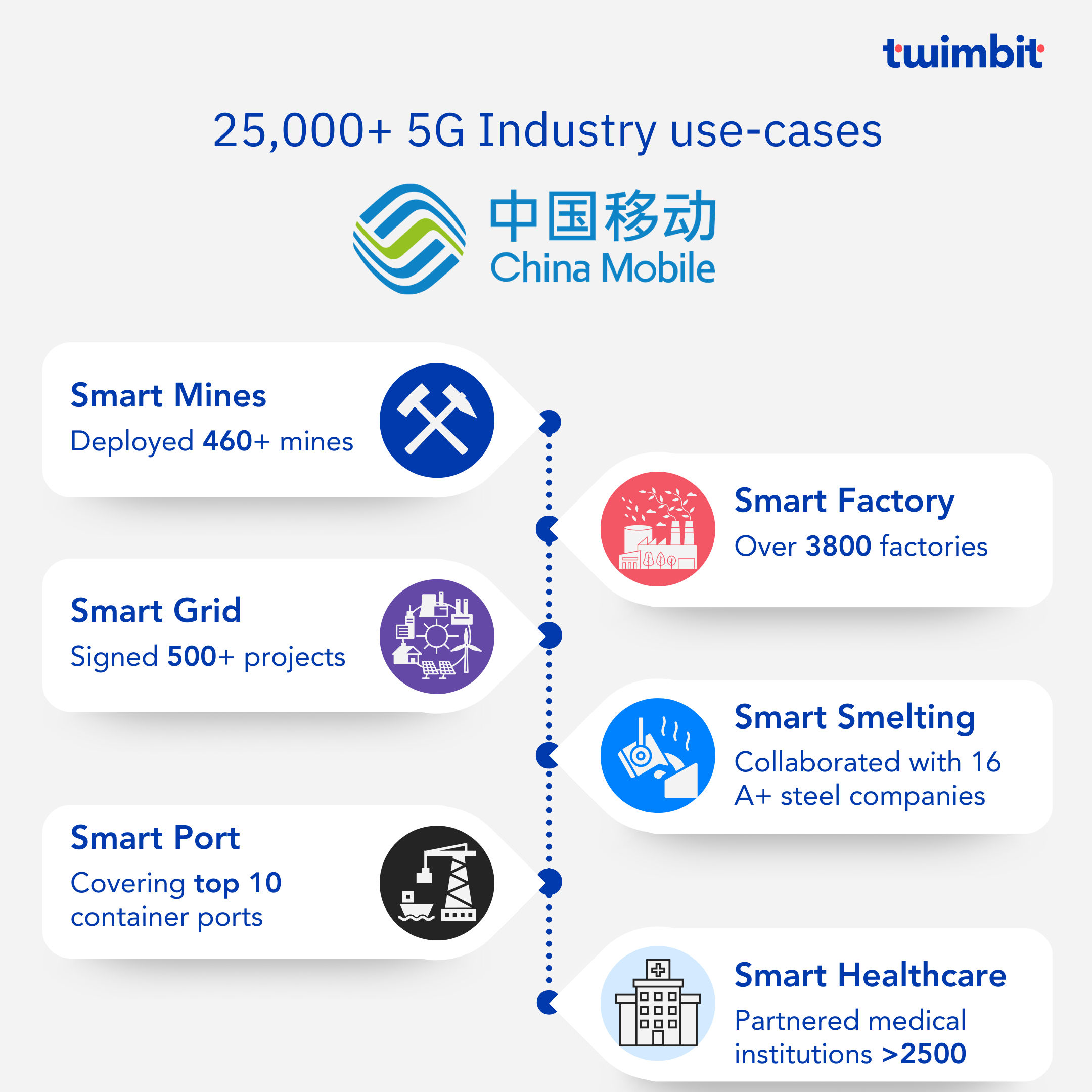

China Mobile continues to lead in transforming enterprises

China Mobile emerged as a leader in beyond connectivity services, adding the highest incremental revenue of USD 3.2 billion, culminating in a total of USD 19.2 billion. Its leadership position spans across enterprise services, Digital TV, content services, smart home solutions, and financial technology.

In H1 2023, China Mobile’s enterprise market revenue reached USD 15.1 billion (RMB 104.4 billion), driven by strategic investments in integrated networks, cloud, and DICT (data, information, and communications technology) development.

China Mobile achieved an impressive 80.5% YoY revenue growth in its mobile cloud segment, reaching USD 6.1 billion (RMB 42.2 billion) in H1 2023. The company had secured over 3,000 major mobile cloud contracts during this period, with a substantial contribution coming in from IaaS and PaaS. Notably, China Mobile’s IaaS revenue market share now ranks among the top three in China.

Furthermore, China Mobile entered over 25,000 5G commercial project agreements across multiple sectors. This surge in 5G projects propelled the value of DICT contracts to USD 3 billion (RMB 20.9 billion) in H1 2023, representing a robust 28% YoY growth

Exhibit 8: China Mobile 5G use cases

China Telecom integrating AI and IoT to go further in beyond connectivity

In H1 2023, China Telecom’s beyond connectivity revenues reached USD 9.9 billion (RMB 68.8 billion), marking a significant increase of 16.7% YoY. This revenue primarily comes from the enterprise segment. It witnessed a 92% increase in contract revenue generated from enterprise 5G solutions, further augmented by a 75% rise in IoT revenue.

A significant driver of this growth was also the strategic deployment of AI, Big Data, and edge cloud technologies in conjunction with the existing 5G enterprise solutions. This approach resulted in the acquisition of approximately ~6,000 new contracted 5G 2B projects (independent private networks) during H1 2023, contributing to a cumulative total of around ~20,000 5G 2B customers.

China Unicom excels in big data and security services

In H1 2023, Chinese Unicom achieved noteworthy performance in the enterprise market, with beyond connectivity revenues surging to USD 6.2 billion (RMB 43 billion). This impressive growth of 16.3% YoY was primarily driven by a substantial 36% increase in Unicom cloud revenue.

Chinese Unicom maintained its dominance in Big Data with an increase of 54% YoY in Big Data revenue in H1 2023. Additionally, the company experienced significant growth in its Big Security (Network security services) segment, with revenue soaring by an impressive 178% on a YoY basis. Notably, Chinese Unicom’s security cloud market now offers more than 80 products, showcasing the company’s commitment to providing robust security solutions in the enterprise sector

Research Methodology and Assumptions

- Data collection has been done leveraging secondary research methodologies and the information provided by the respective telcos. Twimbit follows the calendar year approach for the analysis in this report (meaning H1 is equivalent to the period Jan-June of the year).

- The term “non-connectivity” as employed in previous reports has undergone a revision, now it is designated as “beyond connectivity,” with the intention of standardizing its usage in all forthcoming reports.

- As a part of the research, 50 telcos across 18 Asia Pacific countries were studied. The countries were selected based on their economic significance and the availability of reliable data for the telcos.

- 23 out of the 50 telcos have reported their beyond connectivity revenue. Telcos with beyond connectivity revenue contributing less than 2% to total revenue are not included in our analysis.

- Beyond connectivity services in this report exclude traditional voice, data, fixed-line, broadband, and enterprise connectivity services (e.g., IP-VPN, SD-WAN). These services are categorized into four primary buckets, which include, but are not limited to:

- Enterprise Non-connectivity: Managed services, Cloud, Cybersecurity, IoT.

- Content and Media: Pay TV, IPTV, OTT services, Content leasing, entertainment services.

- Payments and E-commerce: Financial services (wallet, banking, insurance, investing), Retail business.

- Others: Any service beyond the above categories deemed as beyond connectivity (e.g., Digital marketing, Analytics, Tele-Health).

- The data from prior reports may exhibit variances when compared to the figures presented in this report. This discrepancy arises from meticulous approach, which excludes all previous assumptions and estimations when calculating beyond connectivity revenue. This report exclusively relies on direct disclosures from telco.

- Some supplementary methodologies have been employed in the computation of revenue for certain telcos:

- KT Corp subsidiaries are included, while calculating the financials for telco.

- Inter segment revenue for Taiwan Mobile’s is considered while calculating the percentage contribution of beyond connectivity revenues.

- If any inter-segment overlap exists in telco reporting, reported revenue is considered for data integrity.

- To account for changes in reporting methodologies, we have calculated the ratio of enterprise and beyond connectivity for Q2 2023/2022 and adjusted it for H1 2023/2022 for SingTel and NTT Docomo.

Here is a comprehensive report on the B2B revenues for telcos- APAC telcos enterprise business update H1 2023

Read how 40+ APAC telcos perfromed in Q2 2023- APAC Telcos Update Q2 2023

Explore our content on Telecoms