Market Highlights

- Real GDP

- Grow by 5.5% in FY2023-24.

- The total outstanding loans of Indian banks stood at USD 1.59 trillion (50.3% of the GDP) in September 2022.

- Credit Growth

- Targeting a credit growth for Indian banks of 13.5% in FY2023-24.

- Driven by demand from retail, non-banking financial institutions and large corporates.

However, SME loans can risk banks’ asset quality as the segment is the most vulnerable to rising interest rates. On the other hand, the non-performing loans expect to continue declining due to recoveries and write-offs of legacy problem loans.

- Yields on Indian government securities

- Increased significantly when the Reserve Bank of India hiked the interest rates by 250 basis points to 6.50% since May 2022.

As a result, this is causing losses for bond investors as the price drops with increases in yields. The RBI is expected to increase the interest rate by 25 basis points. As per RBI, the treasury losses due to rising interest rates could be partially offset by the interest and non-interest incomes of the banks.

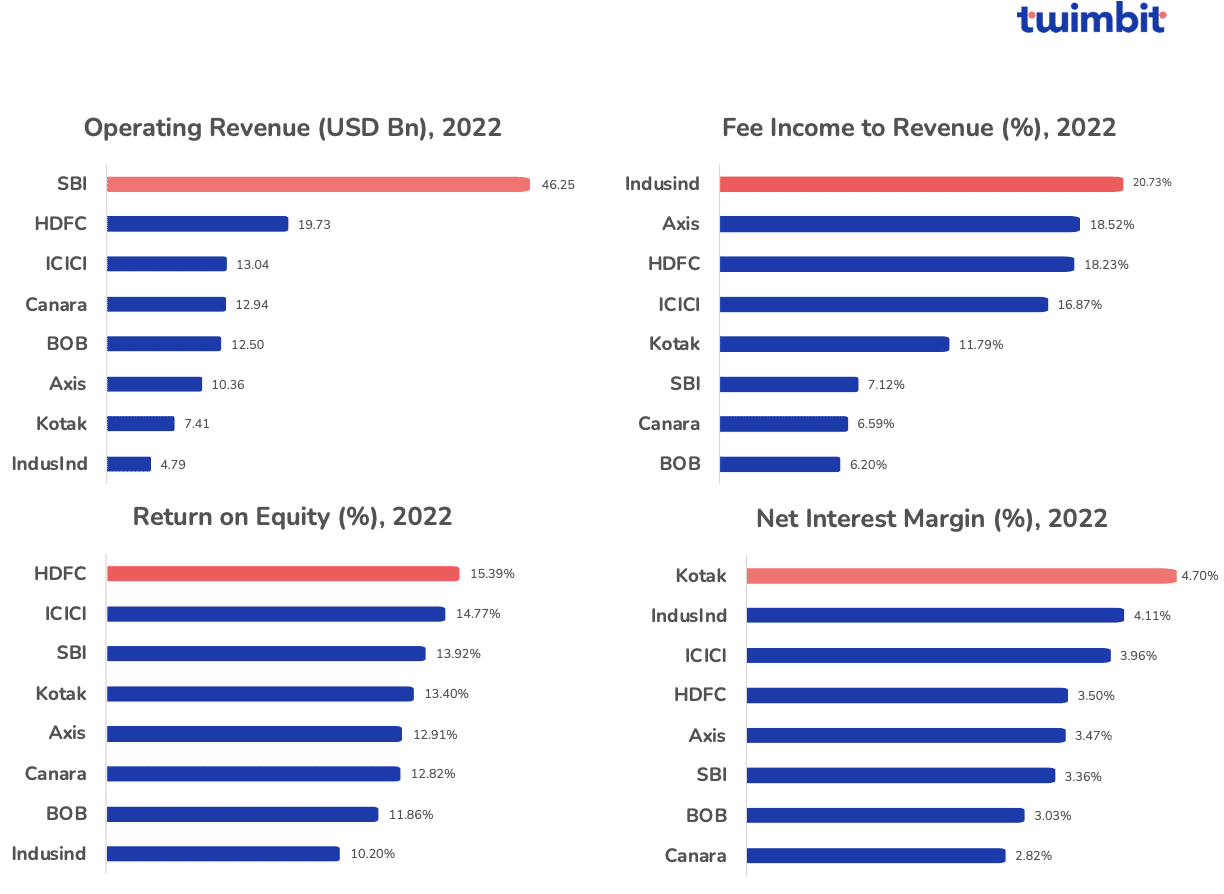

- Operating revenue

All Indian banks are below the APAC average of USD 27.17 Bn, with only SBI above the average. However, the APAC average has increased due to the disproportionate revenue sizes of Chinese Banks.

- Fee income to revenue

APAC average is 12.06% for fee income to revenue, with only IndusInd, Axis, HDFC and ICICI Bank above the average. However, the fee income to revenue has been increasing for Indian Banks because of the following factors:

- The adoption of digital transformation to tap into new revenue streams.

- The integration of BaaS (Banking as a service) and open finance

Cumulatively, these factors lead to higher CASA ratios and revenue from fees.

- Return on equity

All Indian banks apart from IndusInd are above the APAC average of 11.77%, suggesting the following for their high ROE.

- Efficient use of equity capital to generate profits

- Interest rate hikes by the Reserve Bank of India lead to maintaining higher net interest margins (NIM)

The banks directly transferred the hike in interest rate to their loan portfolio and the low cost of holding deposits, boosting the NIM. As a result, 7 of the 8 banks analysed have a NIM above the APAC average of 3%.

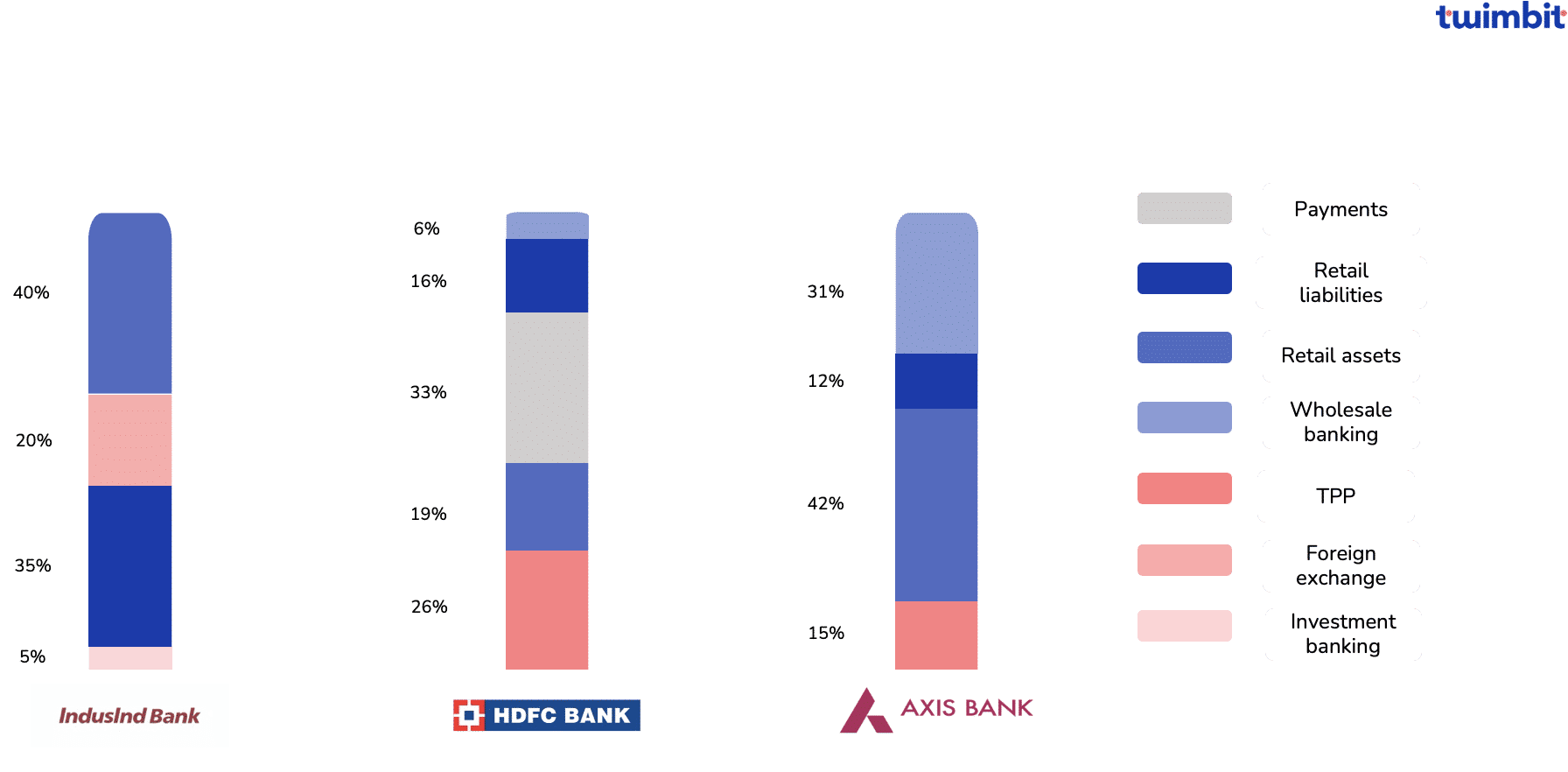

Top 3 Indian Banks to champion fee-based income via digital channels

Top three Indian banks to champion fee-based income

- IndusInd

- 21% of their revenue from fee-based income

- Derived primarily from retail assets and liabilities

- HDFC

- 18% of their revenue from fee-based income

- Derived primarily from third-party providers and payments]

- Highest fee-based income in terms of dollar value at USD 3595 million

- Axis Bank

- 19% of their revenue from fee-based income

- Derived primarily from wholesale banking revenue at 31%

Biggest challenges for Indian Banks

- Declining net interest margins

- Repo rate hikes by the Reserve Bank of India have fully transmitted to home loans.

- Asset-liability mismatch caused by slow deposit growth and aggressive credit climb builds pressure on NIM.

The repo rate hike seems to have peaked, and any reduction in this rate will lead to a simultaneous decrease in the interest rates of loans. Banks have already stretched home loan tenures to keep loans unimpaired to keep the EMIs intact.

- Rising operating costs

- Indian-private sector banks increased their branch network from 14,893 in 2021 to 16,189 in 2022.

- HDFC intends to double its branch network over the next three to five years, adding 1,500 to 2,000 branches annually.

India’s further expansion of its branch operations has increased the average operating costs. The increase is from an average of USD 2.26 Bn in 2018 to USD 3.81 Bn in 2022, resulting in an annual increase of 15.27%.

Top initiatives by Indian Banks

- ICICI Bank – Growing digital propositions

ICICI Bank has numerous initiatives for all its customer bases, with over 600 APIs for retail banking and over 85 for corporate banking.

- iMobile Pay – ICICI’s super app for retail customers has more than 400 services ranging from banking services (savings account, Demat, loans, credit cards) to payment services (scan to pay, recharges, bookings, shopping offers) and e-gift cards (for over 50 top brands)

- ICICI STACK – allows for a super merchant account with zero balance and swipe-based benefit

- The bank provides digital POS solutions through Easypay (POS, UPI, Cards, etc.)

- Buy Now Pay Later (BNPL) service through credit and debit card EMI

- The proposition has recorded 69% growth in spending and 41% growth in active merchants

- Embedded banking for MSMEs – uses one-to-one client ERP integration using APIs

- Plug-and-play cloud-hosted applications which can be installed on the client’s desktop

- Pre-integrated cloud-based connected banking solutions for accounting and payrolls

- Kotak 811 – Kotak’s digital-only bank

With over 750 million smartphone users, this digital initiative aims to target 52% population below 30. In addition, Kotak Mahindra Bank has gradually transformed from a digital acquisition and fulfilment engine into a semi-autonomous digital bank.

- Focused on exponential growth, engagement & cross-sell.

- 12.3 million (71% of total) customer base in Kotak 811 as of March 2022

- More than 6.2 million monthly active users

With Kotak 811, customers can now open a full-service, zero balance digital bank account in under five minutes using their mobile phone or web browser.

- Axis Bank – Corporate digital transformation

Axis Bank’s digital transformation

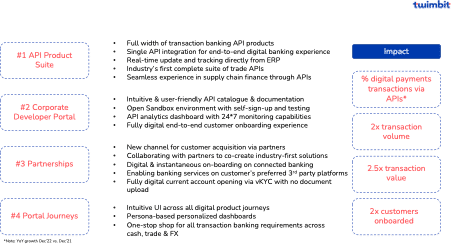

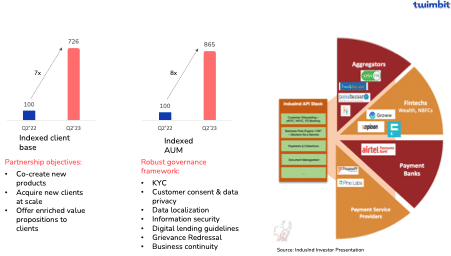

- IndusInd Bank – Building partnership-led business models leveraging APIs

IndusInd Bank’s API stack

- HDFC Bank – Digital future readiness

To develop and offer the best-in-class products and services, HDFC has adopted a factory approach centred on the innovation of intellectual properties. Furthermore, the bank is set to improve its average customer uptime and enhance the anywhere banking experience. To help achieve this, the bank is investing in core technology transformation to strengthen its tech foundations and infrastructure security and resilience.

HDFC has 1,400+ internal APIs with 70% growth in published partner APIs in the last two years. The API transformation program is designed to enhance API orchestration.

Increased competition is leading to diverse opportunities for HDFC Bank in payments

HDFC has 1,400+ internal APIs with 70% growth in published partner APIs in the last two years. The API transformation program is designed to enhance API orchestration.

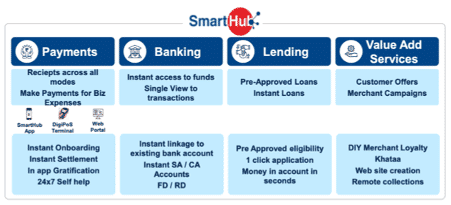

SmartHub Vyapaar 2.0

SmartHub Vyapaar 2.0 – Integrated mobile merchant ecosystem:

- A one-stop digital banking solution for SMEs designed to provide SMEs with a range of financial services and digital tools to help manage their businesses efficiently.

- Allows the SME to deal with all the financial products in one app.

ICT Priorities for Indian Banks

- #1 Strengthening technology foundation and core modernisation

- Updating legacy systems and other critical IT structure

- Adopting a cloud-first, cloud-native approach for all customer touchpoints

- Implementing hybrid landing zones to support a multi-cloud architecture

- Formulating ecosystems powered by partnerships to generate new revenue streams

- #2 Resiliency and cybersecurity

- Implementing advanced security measures like AIML-based security and monitoring tools for application and network ecosystems to identify potential liquidity, market risks, and security breaches

- Conducting automation in disaster recovery (DR) resiliency to reduce recovery time objective (RTO)

- #3 Leveraging data analytics

- Utilise customer analytics for better insights and extensive personalisation

- Integrate the personalised engine to implement multi-dimensional recommendations based on customer attributes

- Conduct automated decision-making models to reduce the turnaround time, such as automated loan processing with predetermined creditworthiness levels

Growth Opportunities for Indian Banks

Upon closely analysing the top 8 Indian banks, we uncovered 3 growth opportunities which will help them grow and overcome the challenges that the banks currently face.

- #1 Enhancement of the branch network

- Private sector banks added 1,296 branches in 2022, with HDFC and Axis Bank accounting for 734 and 164 branches, respectively.

- The private sector banks are adopting an omnichannel sales model with investments in branches and technology.

Banks in India should follow Bendigo’s approach of closing branches with low footfall and consolidating branches within proximity into a flagship digitalised branch.

On the other hand, Indian private-sector banks lack a presence in rural locations despite their aggressive branch expansion. Regardless, these banks plan to achieve the following:

- HDFC – Double its branch network in the next 3 to 5 years

- DBS-owned Lakshmi Vilas Bank – Expand to smaller cities currently dominated by state-owned banks

- Kotak Mahindra Bank – Aims to grow its digital footprint and offer the human touch.

Banks should also migrate over-the-counter services to digital self-service kiosks like OCBC and HLB did with their next-gen ATMs and in-branch tablets allowing customers to do essential banking functions.

- #2 Establishing partnerships for new revenue streams

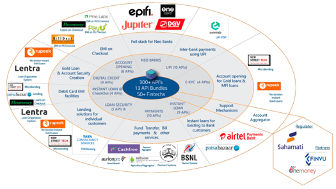

Federal Bank’s fintech landscape

Fee-based income is limited to general banking services and commissions for most Indian banks. However, Yes Bank and Federal Bank have created ecosystems to generate revenue through partnerships.

Yes Bank

- An expansive API ecosystem of 450+ APIs and 30+ fintech partnerships

- 15 more upcoming partnerships

Yes Bank adopts a one-bank approach, leveraging its strengths of existing digital assets.

Moving forward, other Indian banks should also establish ecosystems and partnerships to diversify their revenue streams and eliminate their dependence on interest income as their primary source of income. This is because interest income tends to become erratic since it fluctuates with interest rates.

Federal Bank

- A fintech landscape comprising 300+ APIs offered to 50+ fintech in 13 bundles (Exhibit 7).

Ecosystems are an efficient way for banks to monetise their internal capabilities and partnering with third-party providers will allow banks to disaggregate and securely market their products and services to the customer base of their partners and tap into new revenue streams.

Another recommendation that Indian banks can follow is CommBank’s approach of partnering with Backr, which helps small business owners with links and APIs to various jobs and services.

- #3 Potential to increase revenues

Bank Credit

- Growing at 15% per annum in 2023

The push for better government infrastructure and higher working capital demands have incentivised banks to expand their lending portfolio.

Retail Loans

- Expects to continue growing for another 2 quarters

Despite the RBI suspending the increase in repo rates and increasing interest rates during May 2022, the demand for home loans stays robust.

MSME Segment

- Grow due to the government’s “Atmanirbhar Bharat” initiative and the Productivity Linked Incentive Scheme

Corporate Credit

- Comprises 45% of overall credit

- Expected to grow at an annual average rate of 11% till March 2024

- Driven by additional working capital requirements due to high inflation and a move from bond markets to bank loans due to interest rate movements

Overall, Indian banks were able to post striking results in 2022 and are expected to continue on this trajectory in 2023. Furthermore, the NPAs are expected to decrease to around 5% in 2023 and 4% in 2024. However, to enjoy earnings generated from loans, banks need to keep an eye on deposits which are lagging due to low interest and a lack of incentive for consumers to save.

To know about the State of Australian Banks in 2023, click here.

To know about the State of Malaysian Banks in 2023, click here.

To know about the State of Singapore Banks in 2023, click here.

To know about the State of Vietnamese Banks in 2023, click here.

To know about the State of APAC Banks in 2023, click here.