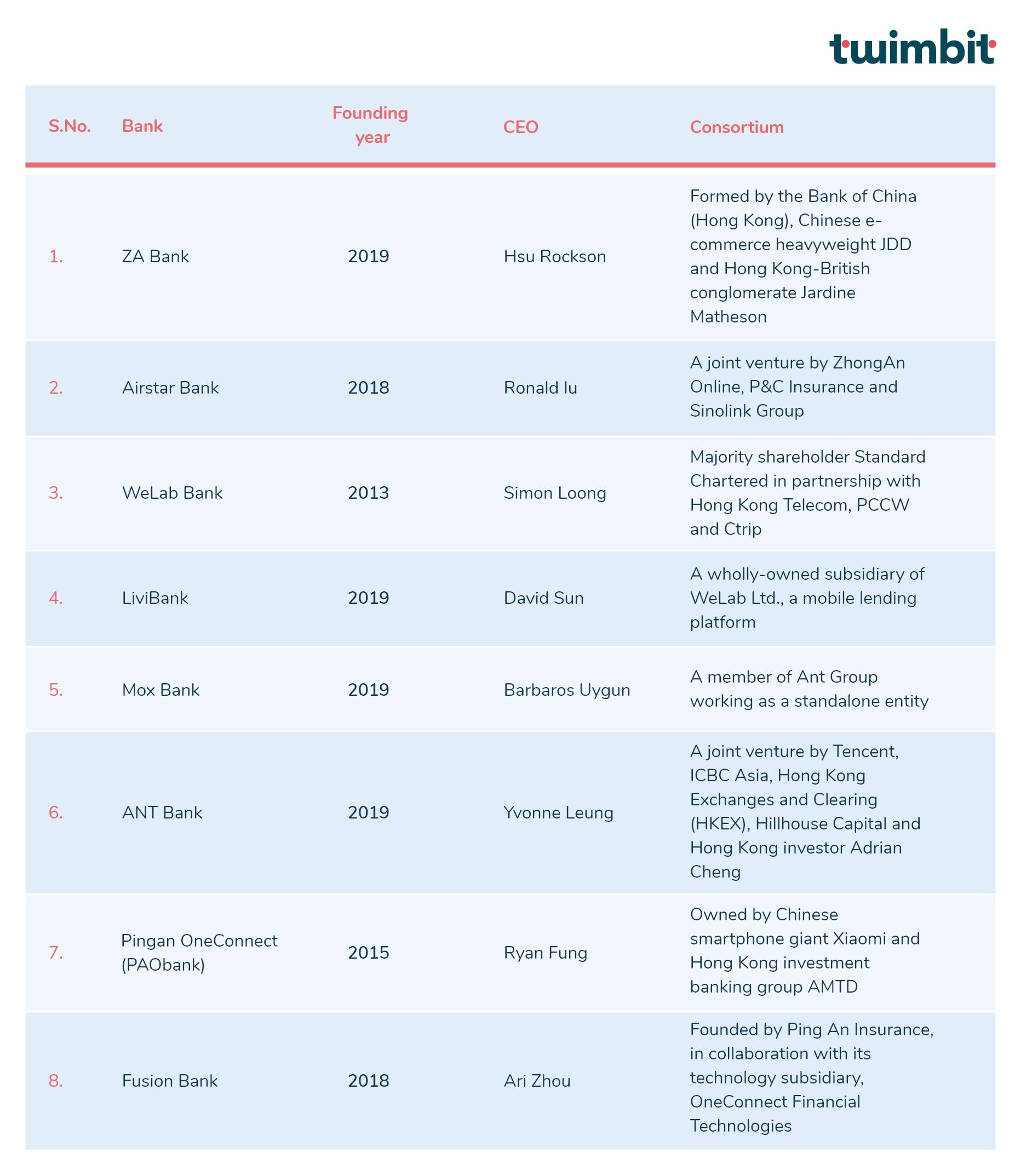

To keep pace with the growing digital dexterity, the need for innovative products and the increased access to financial services for the underserved population, the Hong Kong Monetary Authority (HKMA) announced eight virtual bank licenses in 2018 (Table 1). As per HKMA, a “virtual bank” is a bank that delivers retail banking services through the internet or other forms of electronic channels instead of physical branches.

The launch of virtual banks in Hong Kong, which is a key component of the Smart Banking Initiatives, will certainly facilitate financial innovation, enhanced customer experience and financial inclusion.

Mr Norman Chan, Chief Executive of the HKMA, 2019

Table 1: Snapshot of Hong Kong virtual banks (ranked by launch dates)

The banks use their strong pedigree from incumbents like Bank of China, ICBC, Standard Chartered, and AMTD Group (Table 1). In addition, a few virtual banks can even sway capability from the top technology and telecom giants, Tencent, Xiaomi, and Ant Group. Hence, after 3 years, they finally began to make a mark in the industry, establishing themselves as global examples of neobanks.

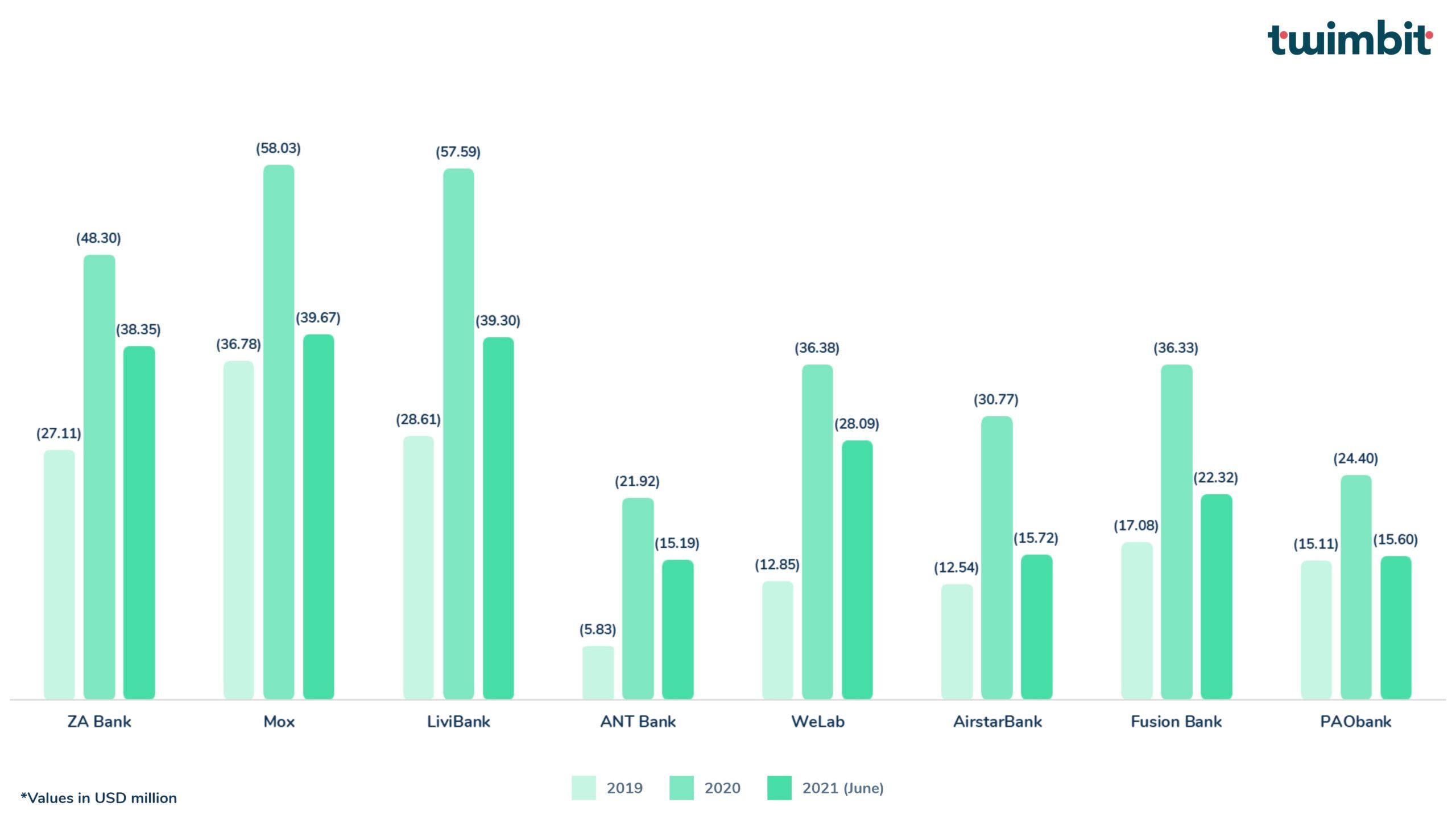

Despite the strong consortium companies at play, virtual banks still face stiff competition from the incumbents, ones who have accelerated their digital transformation initiatives amid covid-19. Since their inception, these virtual banks have been struggling to sustain a positive cash flow. The ambivalence lies in which customer segment virtual banks should position themselves in. Also, rising competition from the incumbents proves to affect their profitability (Figure 2).

Figure 2: Virtual banks are struggling to become profitable- Net Loss (Mn, USD) 2019-2021

Note: Figures for 2021 are reflective till 30 June 2021.

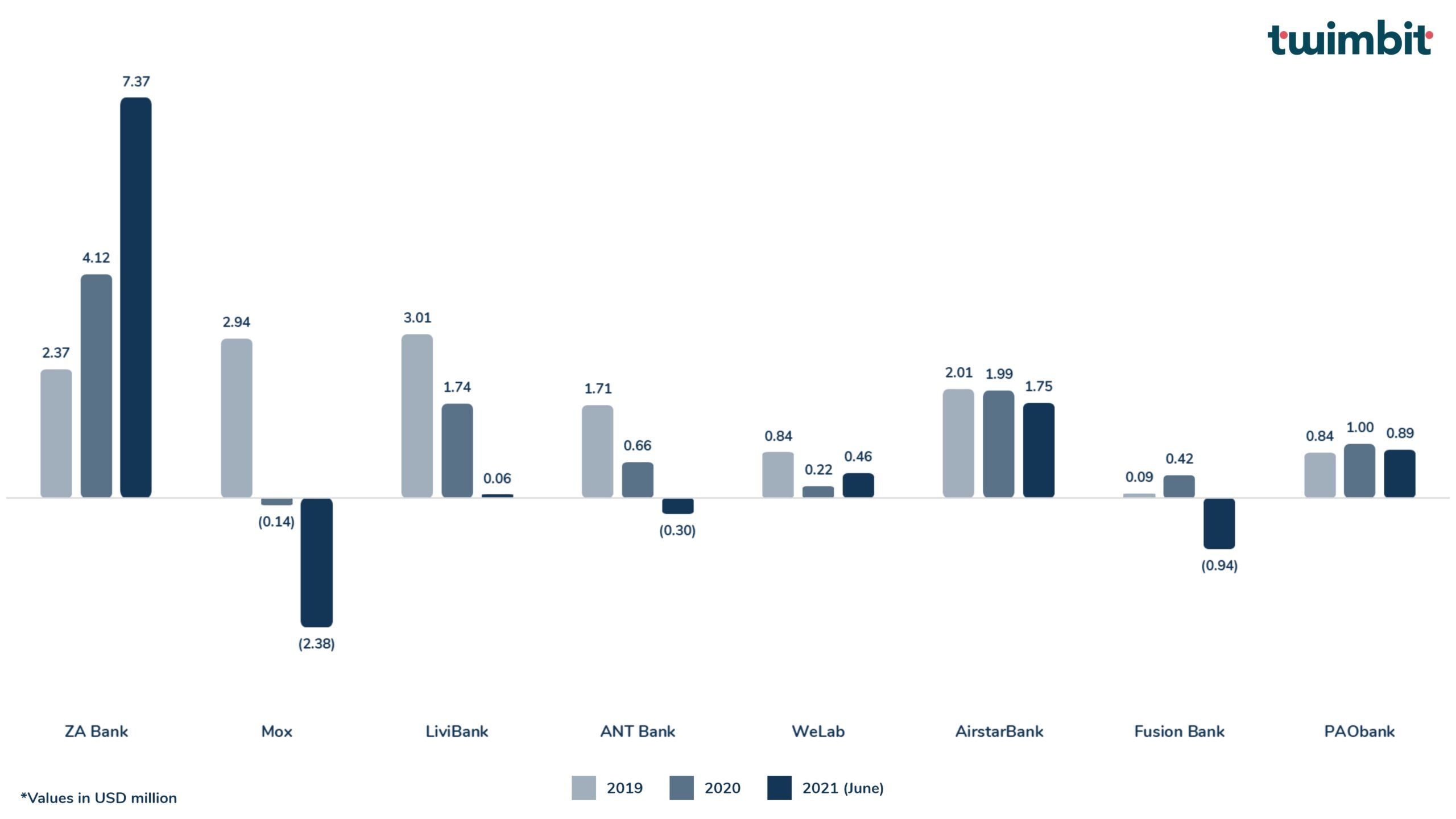

On average, the yearly revenue for a neobank in 2020 was USD 1.2 Mn (Figure 4). According to the HKMA, in September 2021, the eight virtual banks opened 1.1 million accounts with a deposit value of USD 3.08 Bn (0.2% of the country’s total). Combined, ZA Bank and Mox Bank account for over two-thirds of the total deposits. Their target is to break even in early 2024.

Figure 3: Sub-optimal operating revenues to sustain the business

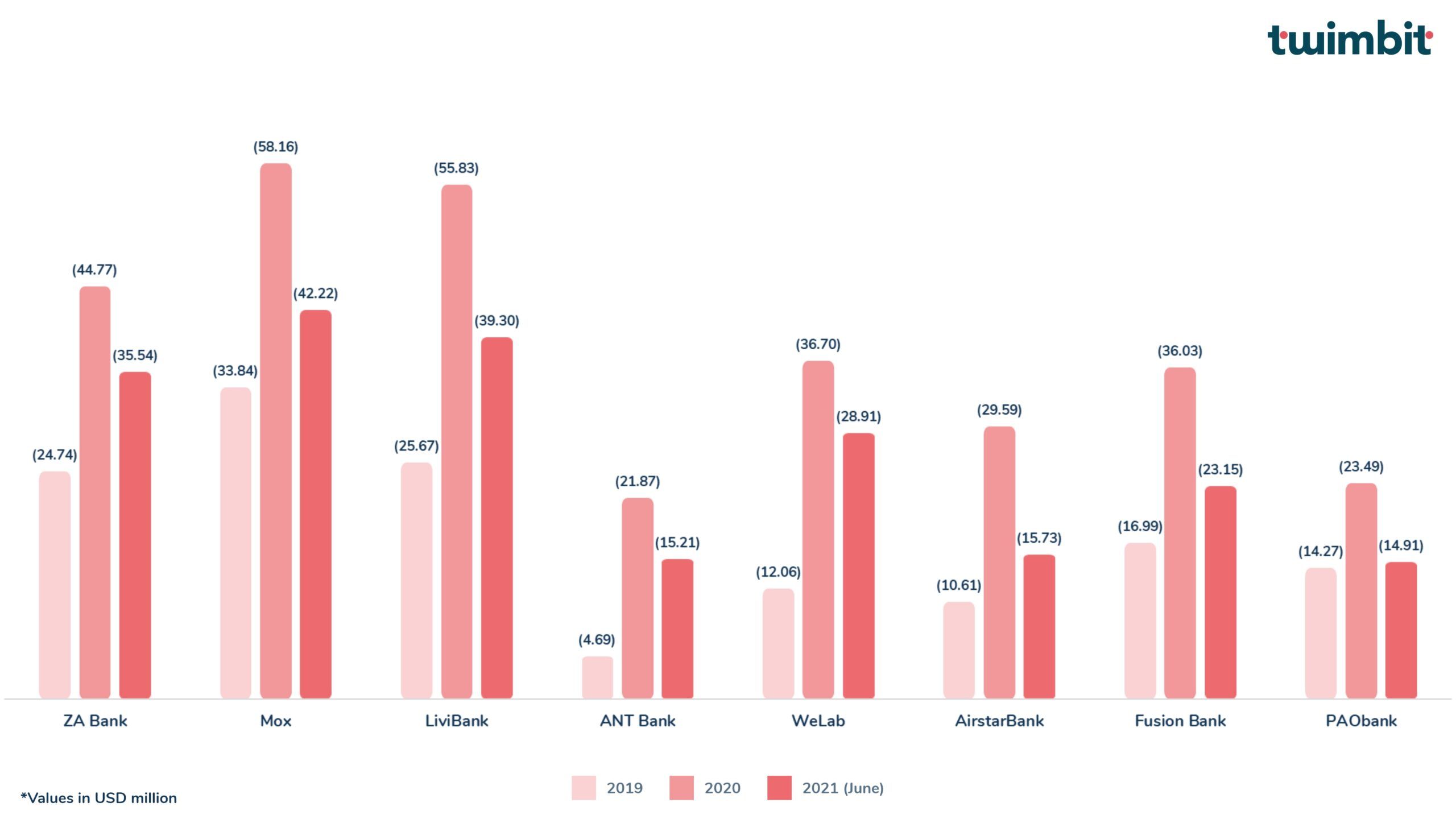

The neobanks report an average operating expense (OPEX) of USD 39 Mn in 2020 (Figure 4). The highest cost categories for these neobanks are staff fees, premises, computer costs, equipment and marketing expenses. The current burn rate for these neobanks is relatively high and is likely to [KX1] impact their sustainability in the next 5 years. Hence, it is becoming a big challenge for them to maintain a positive cash flow or establish a path for continued revenue growth.

Figure 4: OPEX more than 30 times the revenue

Becoming a journey-led virtual bank can carve the path to success

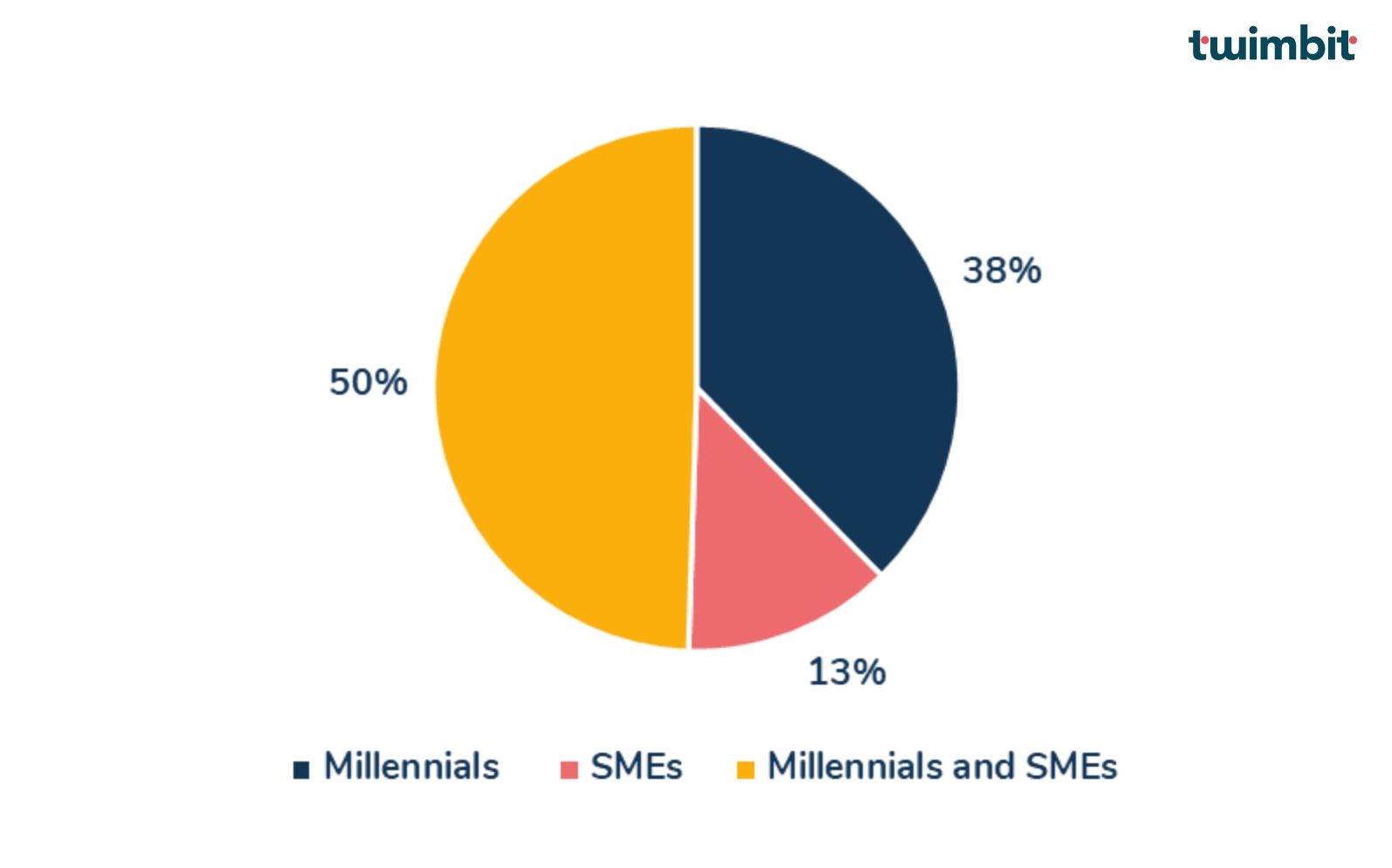

We see the key customer segment for who the virtual banks are for – the young, digital-savvy professionals and the affluent mass population of Hong Kong, who mostly fall under the age bracket of 24-45 years (Figure 5). Despite its initial shaky years, Hong Kong and its virtual banks have received a phenomenal response from its customers, ranking at #3 in the global neobank adoption rate. As of September 2021, 18% of Hong Kong have a neobank account.

Figure 5: More than 80% of virtual banks are serving the millennial population

In terms of customer acquisition, the highly banked population of Hong Kong presents a unique challenge for virtual banks, encouraging them to position themselves as customer journey owners. They need to do this when pushing the customer to either shift from traditional banks or to change the customers’ mindsets toward attaching a virtual bank product to their portfolio. Hong Kong has an excellent opportunity as it is a hub for a young population with high net-worth that prefers fast-paced, journey-led, and personalised offerings.

The country is also a home for trade-based and e-commerce SMEs that regularly need and benefit from trade financing and working capital. In Hong Kong alone, there are 340,000 SMEs, constituting more than 98% of business establishments. PAO Bank and ANT bank have built strong propositions to support the SME segment with immediate credit facility and digital disbursement at low cost.

While traditional banks are driving on deposit values and large balance sheets, the market opportunity for virtual banks is to dive into a niche pool and target specific segments.

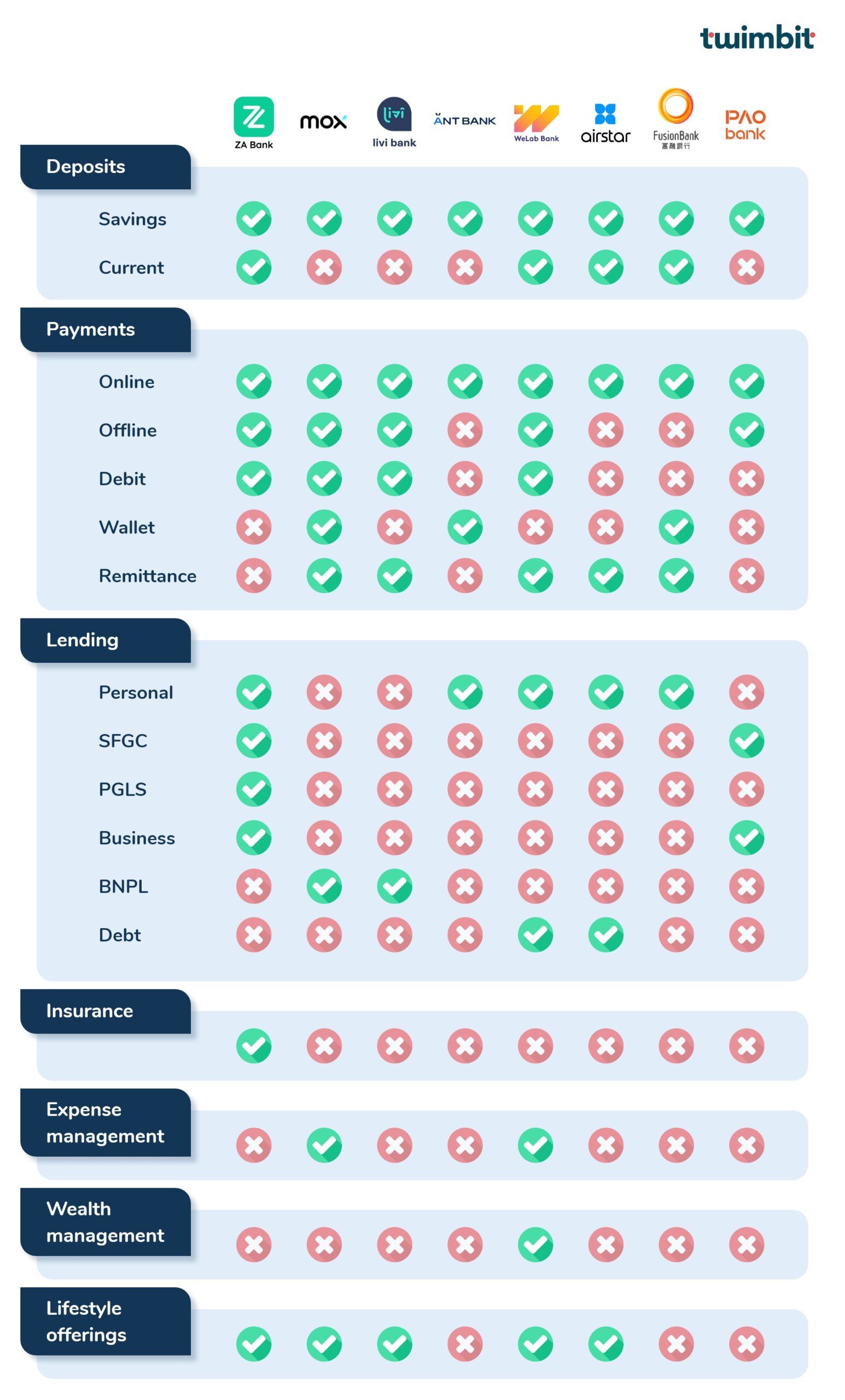

The overall product portfolio for virtual banks still depends on deposit-taking and payment offerings with limited penetration in the lending market. ZA Bank introduces the maximum lending products with retail and SME loans and guarantee schemes. Lending solutions are a gateway for building solid and consistent revenue streams for the banks. As they are still in their early phase of operations, the first step is to project a healthy CASA (Current Account Savings Account) ratio to start lending money to their customers.

Figure 6: Product stack of 8 virtual banks in Hong Kong

- PLGS – Personal Loan Guarantee Scheme

- BNPL – Buy Now Pay Later

- SFGS – SME Financing Guarantee Scheme

*Mox, welab, and livi have applied for Securities License

Expanding product portfolio through partnerships

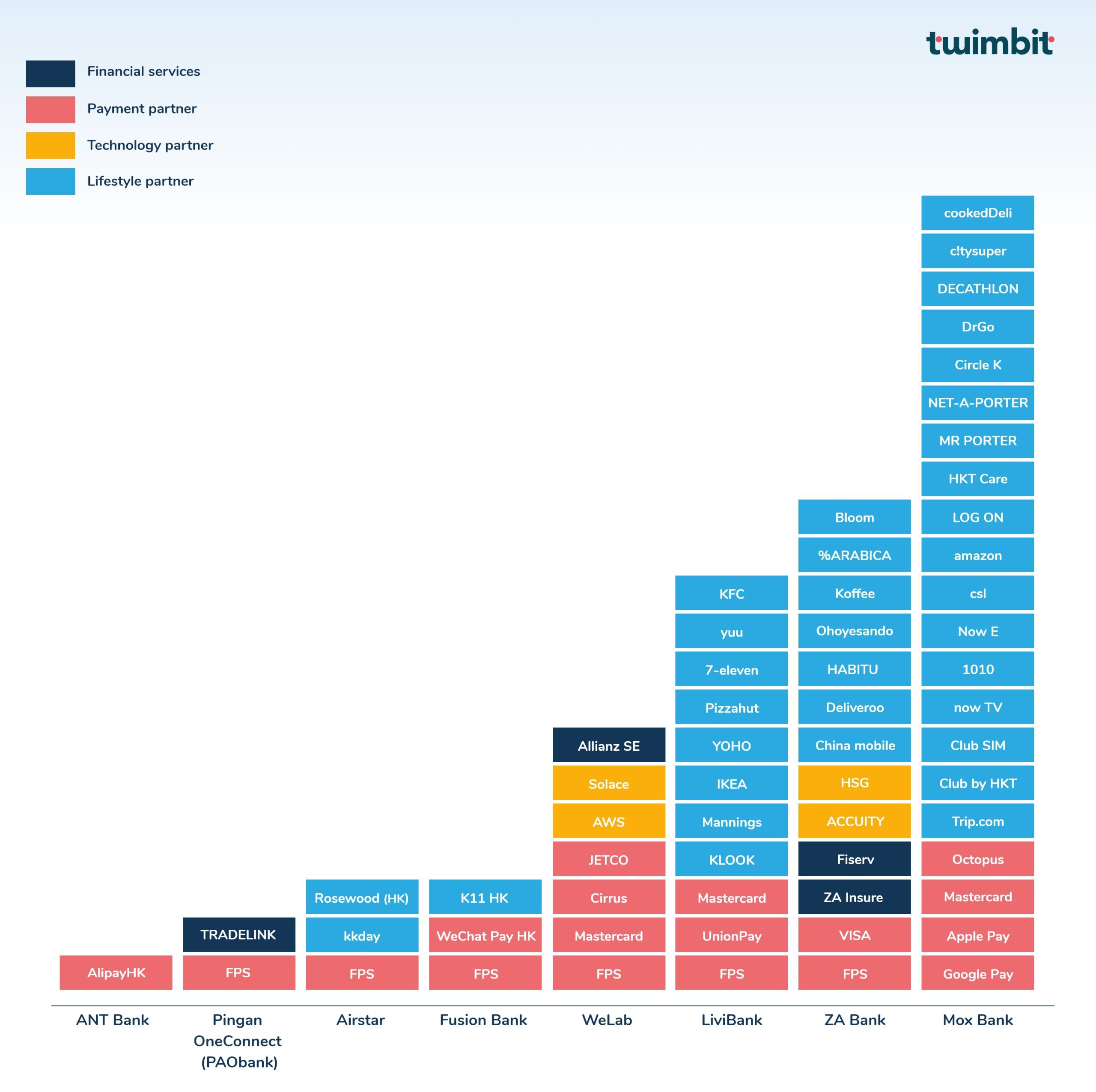

Most virtual banks have built partner ecosystems to drive product efficiency and differentiation on their platform. It also acts as a revenue strategy for the banks to earn fees from third-party service providers. PAO Bank is no different, building a suite of white-labelled API fintech solutions to help financial institutions easily plug and play them in their systems. To emphasise, we charted an illustrative list of some of the partners these virtual banks are working with to expand revenue streams (Figure 7).

Figure 7: Virtual bank partner ecosystem

Note: The sub-categorisation under each segment

- Financial services

- Wealth management

- Insurance partner

- Expense management partner

- Business management partner

- Payment Partner –

- Payment gateway

- Wallets

- Debit card

- QR Payment

- ATM

- Technology partner –

- FinTech

- Cloud

- E-KYC

- Lifestyle partner –

- Travel

- E-commerce

- Entertainment

Conclusion

Hong Kong is among the early entrants in neobanking, a frontrunner for digital innovation. Coming in hot with high-speed delivery and personalised offerings, the eight virtual banks are certainly creating their own market among the young, affluent population. But the competition from the incumbents fiercely delays the much-needed breakthrough for these virtual banks. Moreover, the negative gap between expenses and revenue has put immense pressure on profitability and sustainability. For virtual banks to win, they need a well-defined path that works on freemium or fee-based cost models and one that can scale across products and third-party ecosystems. The bright side for virtual banks is the agility and scale with which they can work on data to build hyper-personalised and targeted customer offerings. In turn, this will help establish powerful ecosystems that deliver financial services across customer journeys and go beyond to offer lifestyle solutions.

Appendix

Virtual banks had to undergo a stringent evaluation process to gain a license

The Hong Kong Monetary Authority (HKMA) came up with a detailed licensing framework to establish virtual banks:

- Must be incorporated in Hong Kong (Not required for conventional banks)

- Must have at least one physical office to handle customer complaints

- Must provide an exit plan at the time of their application for authorisation to ensure that they would be able to unwind the business in an orderly manner (if required)

- Must be members of the deposit protection scheme

- Are subject to prohibitions on minimum balance requirements and predatory practices such as extremely low prices or excessively high interest rates

Table 6: Additional criteria for authorisation as a licensed bank

Source: https://www.charltonslaw.com/virtual-bank-hkma-new-guideline/

Consortium-led virtual banks fund inhouse than seeking market investments

In Hong Kong, shareholders fund seven out of eight virtual banks, reflecting a strong network of consortiums controlling a sizable portion of the market. WeLab Bank is the only bank thus far which has raised money via various rounds of market funding.

Established in 2013, WeLab quickly became Hong Kong’s first fintech unicorn with an estimated value of over USD 1 billion. Since 2015, WeLab has raised more than USD 650 million. The latest of which, a Series C1 round in 2021 led by Allianz, brought in around USD 75 million.

Allianz, which led the Series C1 round, is an asset management and insurance firm working with WeLab. Together, they will be acting as a bank and fintech solution provider to jointly develop and distribute investment and insurance solutions for digital banks across Asia. These products will diversify WeLab’s current product offerings and further establish it in the market.

Table 7: WeLab bank funding

Note: Following the Series C1 funding round in 2021, a consortium led by WeLab has raised US$ 240 million from existing and new investors. An amount which the company claimed to be the largest fintech funding in Indonesia last year. The raised amount is going to go towards acquiring Bank Jasa Jakarta (BJJ), an Indonesian commercial bank. With this deal, WeLab plans big to launch a digital bank to capture Indonesia’s enormous unbanked population within the second half of this year.