Financial inclusion helps lift people out of poverty and can help speed economic development. It can draw more women into the mainstream of economic activity, harnessing their contributions to society. – Sri Mulyani Indrawati, Minister of Finance of Indonesia, former head of the World Bank Group

What is financial inclusion

Financial inclusion is a set of measures put in place to overcome the challenge of inaccessibility, unawareness, and illiteracy in banking and financial products and services among individuals, resulting in an unbanked and/or underserved population. It encompasses a range of financial and non-financial products and services made available to individuals with none to the limited supply of money and are in dire need of it.

The need for financial inclusion

Both the banking industry and policymakers agree that financial inclusion is pivotal in reducing poverty and boosting prosperity. The Chinese government, for example, has coined the term ‘Sannong’ which is an inclusive term for the three rural issues- farmers, agriculture, and rural areas, and it thus advises banks to have financial inclusion policies in and around it. The Reserve Bank of India on the other hand has a “National Strategy’ for financial inclusion.

While advances in the banking industry such as ‘digital payments’ and ‘use-now & pay-later’ have worked wonders for a section of the society, yet, over 35% of the world’s adult population still has no access to basic banking services.

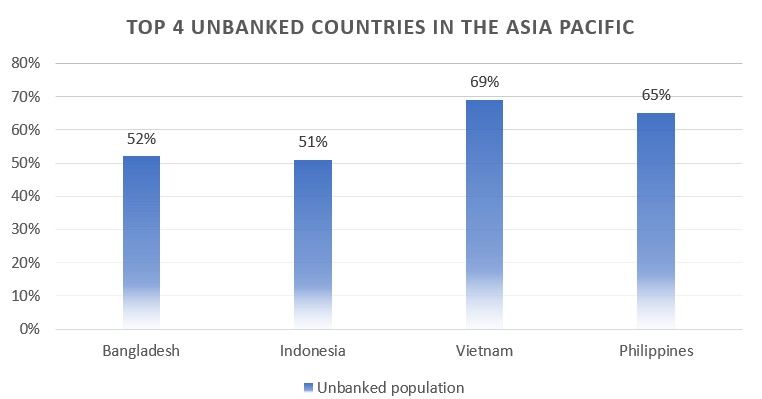

There is still an alarming figure of the unbanked population in the Asia Pacific, where countries such as Vietnam and The Philippines respectively have 69% and 65% of the population still unbanked. However, close to a hundred percent of the population residing in Singapore, Japan, Taiwan, Australia, and New Zealand have access to a bank account and financial services.

The reasons may differ, but the core issues lie in the following:

- Variation in income levels

- Adoption of technology

- Structural reforms

Why is financial inclusion important for banks

Financial inclusion and societal welfare run parallel to each other. However, inclusion offers deep business value to the banks. Banks provide financial services and products to a variety of customers, resulting in:

- Increased market share

- Loan distribution, and

- Revenue growth

The State Bank of India, for example, has over 155 million FI account holders making up 35% of their entire customer base. Further, it will also help the banks in the developing Asian economies to push up their attach rate which is currently close to one.

What does the checklist aim to achieve

It aims to help banks in achieving 5 all-encompassing financial inclusion objectives:

- Awareness

- Accessibility

- Sustainability

- Financial literacy

- Financial planning

Twimbit’s 5-point checklist to build a robust financial inclusion model

Based on our in-depth research on the strategies employed by various banks in the Asia Pacific region to nurture financial inclusion, we have developed a 5-point checklist and they are:

Agent banking:

For ages, reach has been a hindrance to financial inclusion. Building and running a banking infrastructure in a remote location is costly and tedious for the banks. Agent banking helps banks overcome the barrier of reachability in a cost-effective manner. Banking agents are individuals/outlets appointed by banks to provide banking services in areas that are too out of the way. With the introduction of biometric verification supported by seamless internet connectivity, the agent banking practice is on the rise. It allows agents to quickly open bank accounts and provide essential banking services such as-

- Deposits

- Money transfers

- Withdrawals

Learning example: Bank BRI

- Bank BRI appoints its customers as banking agents, thus adding a layer of trust as their existing customers act as a flag-bearer for their services. To date, the bank has over 4,20,000 agents covering over 49,200 villages in Indonesia. Read the entire case study here- How Bank BRI developed a financial inclusion infrastructure in Indonesia

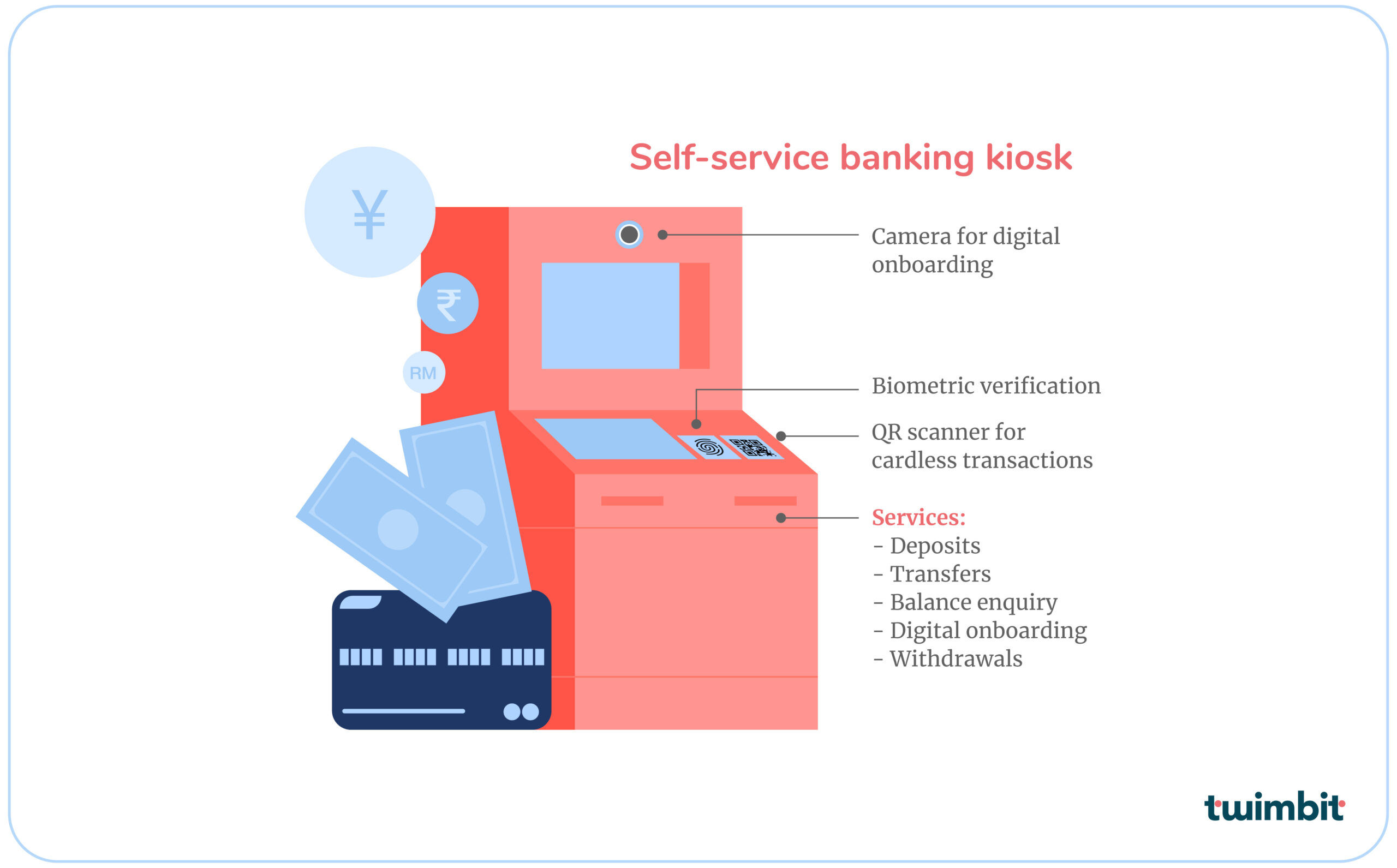

Self-service banking kiosk:

Self-service banking kiosks, a mechanism that helps banks deliver a 24*7 service to individuals, farmers, and businesses. From a business standpoint, self-service banking kiosks offer solutions to key problems such as reach, cost of service/operations, and time-consuming infrastructural development. They are easy to set up and are equipped with internet connectivity from the get-go. Lower internet costs in major Asia-Pacific countries automatically mean low operational costs for the banks.

Learning Example: State Bank of India

- SBI sets up a kiosk-like structure in the village or an area where the bank lacks presence. These kiosks are known as Customer Service Points and provide services such as transfers, KYC, withdrawals, and deposits, among others. These kiosks heavily contributed to the Rs. 2,27,469 crore financial inclusion transactions. Read the entire case study here. – State Bank of India- pioneering ‘Kiosk Banking’

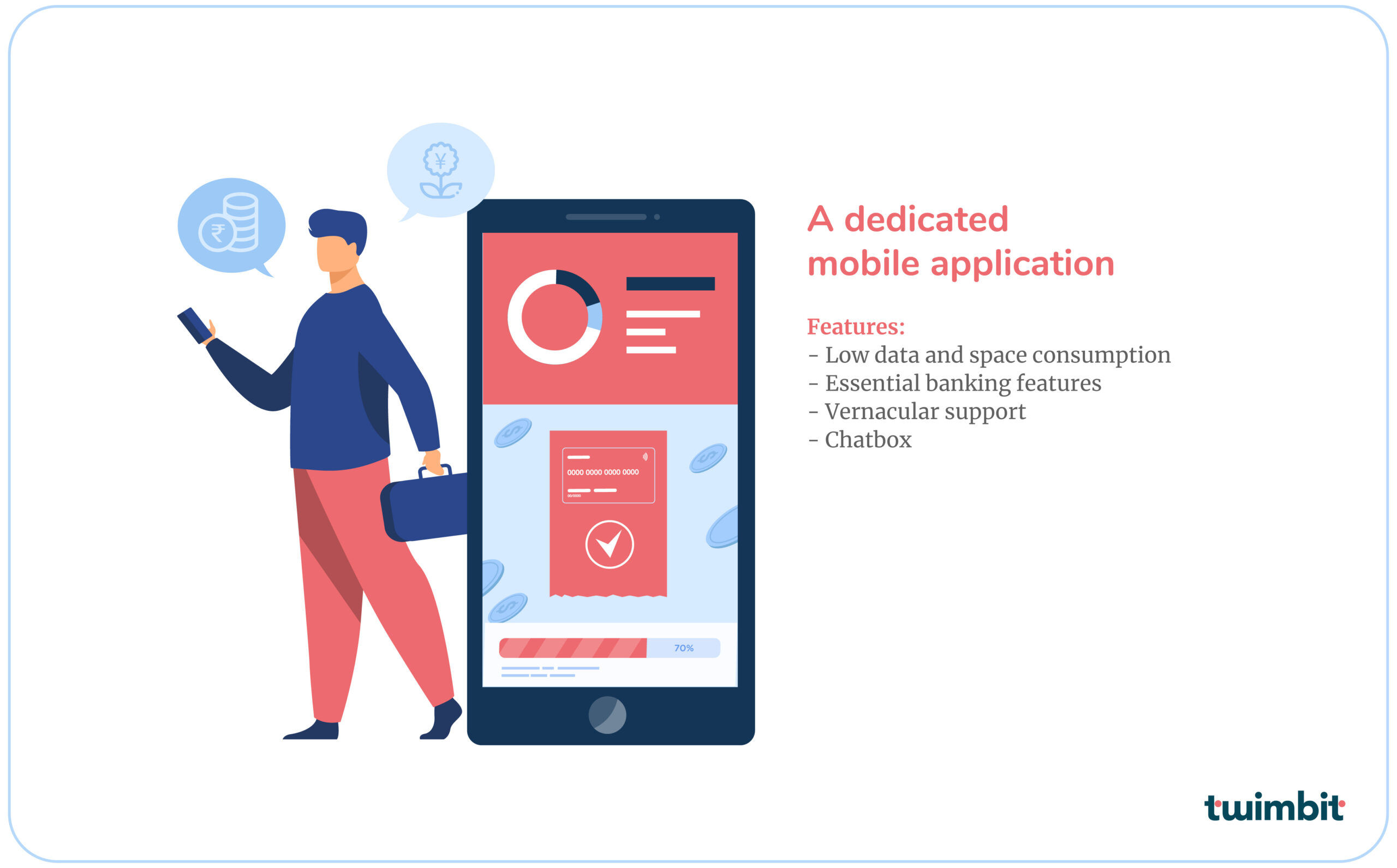

A dedicated mobile application for financial inclusion:

The demand for smartphones is on the rise. This offers banks an opportunity to drive up the use and utility of mobile-first banking applications. Furthermore, the unbanked, rural populations comprise of millennials that are growing up. This demographic is drawn towards smartphones, making it mission-critical for banks to engage the millennials through a dedicated banking application. Additionally, vernacular support increases the adaptability of the applications due to the ease of understanding and comfort.

Learning example: Dutch Bangla Bank

- Dutch Bangla Bank, with its financial inclusion-dedicated mobile banking app ‘Rocket’, introduced banking services to 17 million individuals. Read the entire case study here – Dutch Bangla Bank- penetrate digitally to include financially

Digital lending and financing:

In the times to come, banks will face tough competition from fintechs, delivering zero-collateral paperless loans. Banks must make efforts to combat three unique challenges:

- Penny-sized lending to individuals

- Agriculture and equipment financing to farmers

- Payment gateway and business loans to SMEs and MSMEs

Learning example: Grameen Bank

- Aiming to eradicate poverty from Bangladesh, Grameen Bank offers zero-collateral paperless loans to the needy. To date, it has served more than 9 million customers and has a presence in 97% of Bangladesh. Read the entire case study here- How Grameen Bank Bangladesh creates collateral-free credit options to reach the rural population

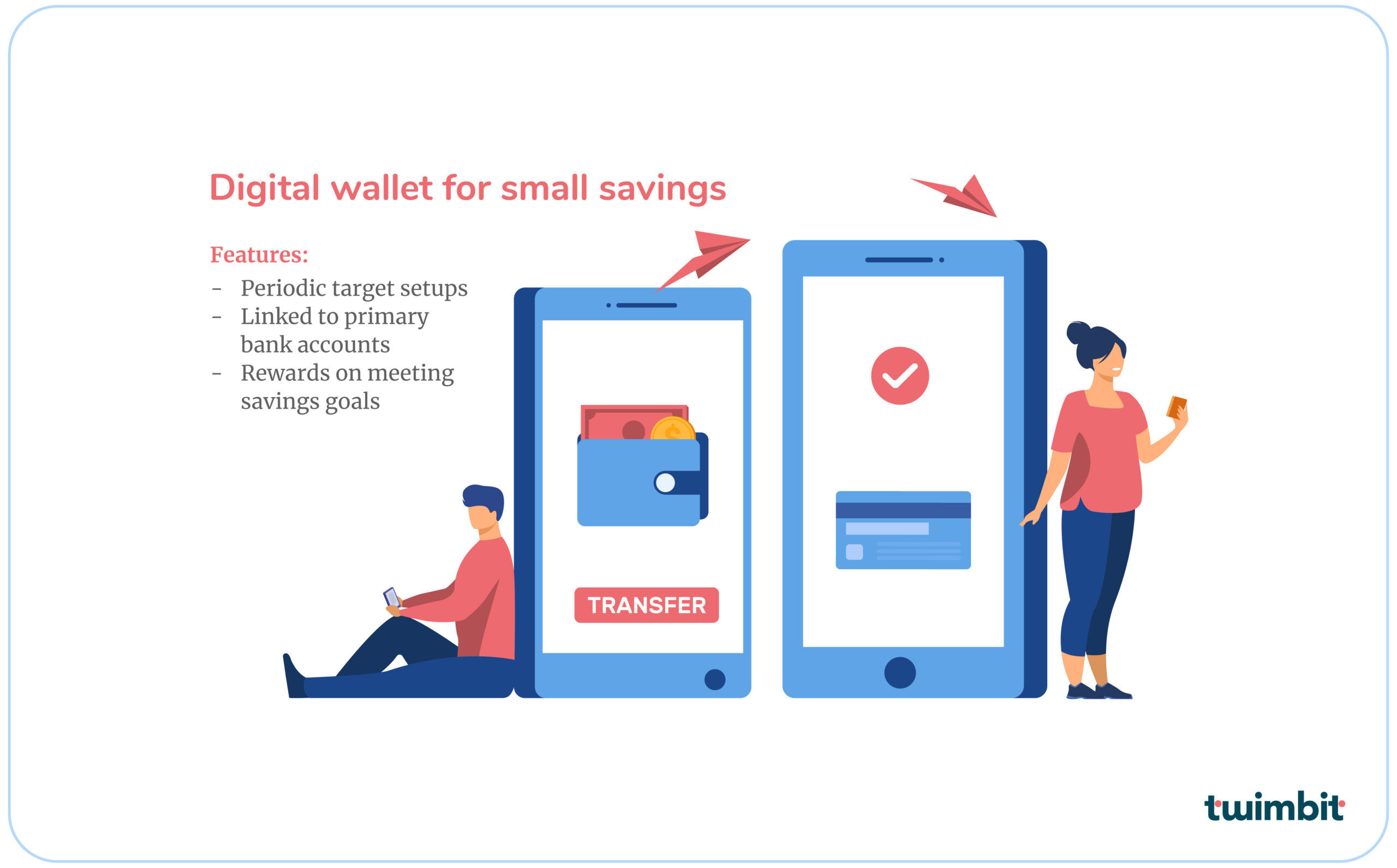

Digital wallet for small savings:

To inculcate the habit of savings, digital wallets that allow customers to set periodic savings targets should be offered. These wallets can then be linked to the primary bank account, where the customer can transfer his periodic savings after his goal has been met.

Learning example: Bank BRI

- Bank BRI distributes deposit boxes, ‘Teman Simpedes’, to the customers, with a universal key available only to the BRILink Agents. The money collected in ‘Teman Simpedes’ is deposited by the agents into the savings bank account of the customer. In an introductory phase, over one lakh of these ‘Teman Simpedes’ were distributed. Read the entire case study here- How Bank BRI developed a financial inclusion infrastructure in Indonesia

Conclusion

Financial inclusion is a means to an end, but not the end itself. A robust financial inclusion model will enable banks to deliver inclusive growth- that of an individual and that of the economy. The benefits of which are as follows:

- Awareness: Banking services open the gateway to savings and investment, improving the overall well-being of individuals and families.

- Sustainability: Financial Inclusion includes micro-financing schemes that empower individuals to kick start businesses and create jobs driving up economic prosperity.

- Accessibility: Savings, investments, and payment gateways cultivates a sense of equality in society, and thus, equality within communities and families.

- Literacy: Financial literacy helps individuals and families make informed decisions. This minimizes their chances of being monetarily exploited.

- Financial security: Investments and access to quick credit provide a sense of security to the individuals. Banks and various financial institutions offer a buffet of secured investment options to their customers. These investments can quickly be liquidated at times of need.