The first quarter (Q1 2021) of this year has provided some cheer for telcos in Asia Pacific, with the industry recording higher growth as compared to the same period in 2020. In our ongoing analysis of telcos across the region we studied the performance of 37 operators and summarise below the 5 key takeaways from our detailed analysis.

#1 Asia’s top 6 telco’s see impressive growth in revenues, the industry registers 8.4% growth

- The industry added USD 10.3 billion in revenues in Q1 2021 compared to USD 600 million in the same period last year. The biggest six telcos added USD 8.6 billion of the new additional revenues driven largely by increase in number of 5G subscriptions and device sales.

- China and Japan markets continued to be the highest contributors in new revenue growth. Net addition of USD 6,020 million and USD 2,610 million year on year was recorded respectively for these countries.

- The three main Japanese operators commenced 5G commercial services in early March of 2020, and this has had a direct impact on the top line.

- The Chinese market, which is one of the early adopters of 5G, is expected to reach the 500 million 5G subscribers mark in 2021. 20% of total mobile subscribers in China are already using 5G packages.

Figure 1: Net addition in revenues for top 6 telco’s, Q1 2021

| Operator | Country | Revenue 1Q21 USD billion | Change in revenue (1Q21 vs 1Q20) | Change in revenue (1Q20 vs 1Q19) |

| China Mobile | China | 31.7 | 9.4% | -2.00% |

| China Telecom | China | 17.1 | 12.7% | -1.40% |

| China Unicom | China | 13.1 | 11.4% | 0.93% |

| Softbank (telecom) | Japan | 12.7 | 12.5% | 3.39% |

| KDDI Corp | Japan | 12.6 | 4.1% | 1.98% |

| NTT Docomo | Japan | 11.0 | 6.8% | -4.38% |

| Total | 98.4 | 9.61% | -0.62 | |

| Total of 37 telcos | 133.6 | 8.41% | 0.48 |

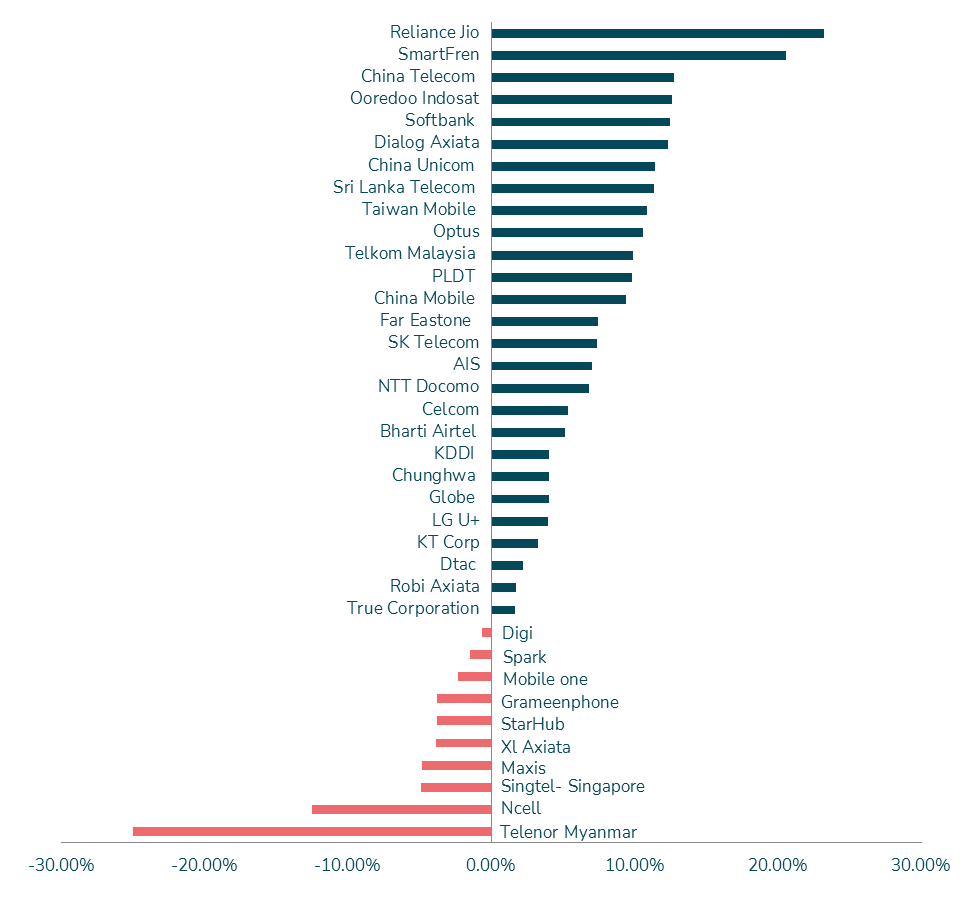

- The addition of 4G customers was the driving force in earnings for Indian operators. Reliance Jio was the biggest benefactor and registered the highest jump of 23.2% (Y-o-Y) in revenue, up by USD 482 million.

- Ooredoo Indosat recorded the highest change in EBITDA of 42.52% to USD 237 million. Customer base growth of 6.8% (Y-o-Y) coupled with cost optimization worked well for the operator.

- Rising tensions in Myanmar had an adverse effect on Telenor’s performance. The political instability placed from February has placed restrictions on the use of mobile internet.

- Axiata’s Ncell performed poorly because of limitations in the scope of the spectrum and competitive intensity.

- Performance of Maxis was impacted by the pandemic. The Movement Control Order in Malaysia since 13th January 2021 has impacted the company’s performance.

Figure 2: % revenue change for Asia Pacific telecom service providers, Q1 2021

#2 Operators continue focus on cost optimization

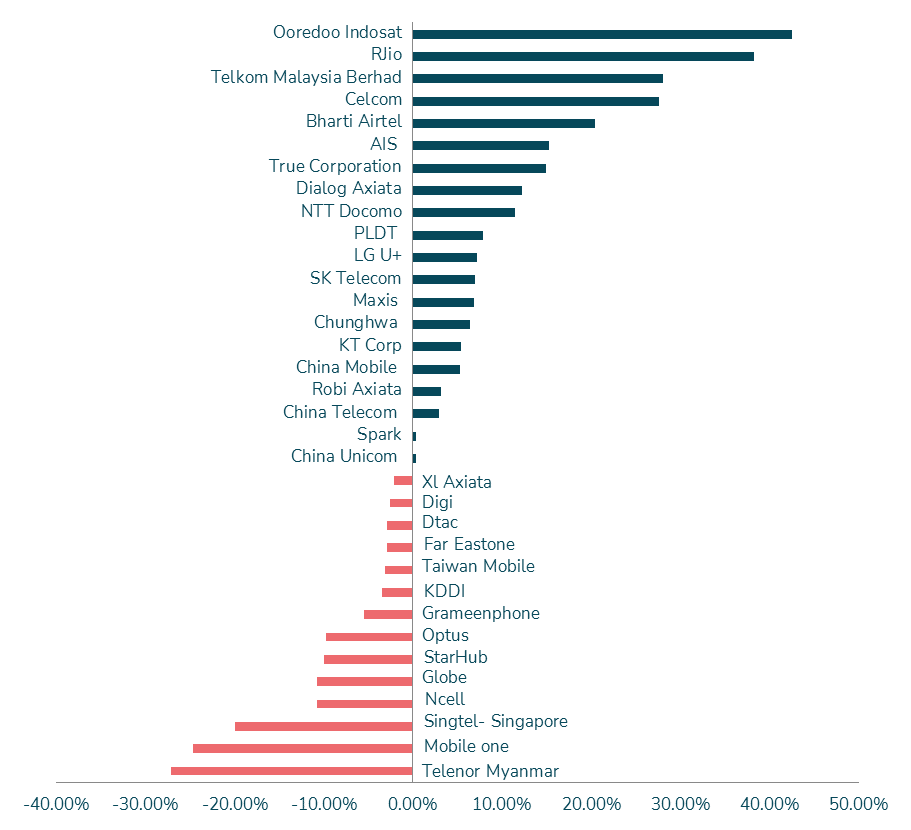

- Performance of telcos in countries of New Zealand, Singapore and Australia were adversely impacted by lower tourist arrivals, lack of business travel and also limitations on the flow of international students.

- To compensate for the impact on roaming revenues these operators have optimized their cost structures. We have seen a decline in their operating expenditures (OPEX).

- Spark telecom in New Zealand ensured lower bad debts for the year, cut on travel expenses, higher marketing efficiency and increased capitalisation of labour. This resulted in a lower OPEX of USD 928 million, down by 2.3% for 6 months ending 31 March. In 2017, Spark included cost optimisation as one of its pillars in their three-year strategy. Since then, operator has reduced gross USD 163 million in cost.

- For Singtel, OPEX fell by 1.4% to USD 493 million for 6 months ending 31 March. TV content cost reduced because of diligence in contract negotiations with vendors. Cost improvement was also seen through digitalisation. Starhub’s OPEX reduced by 2.1% to USD 331 million.

Figure 3: % EBITDA change for Asia Pacific telecom service providers, Q1 2021

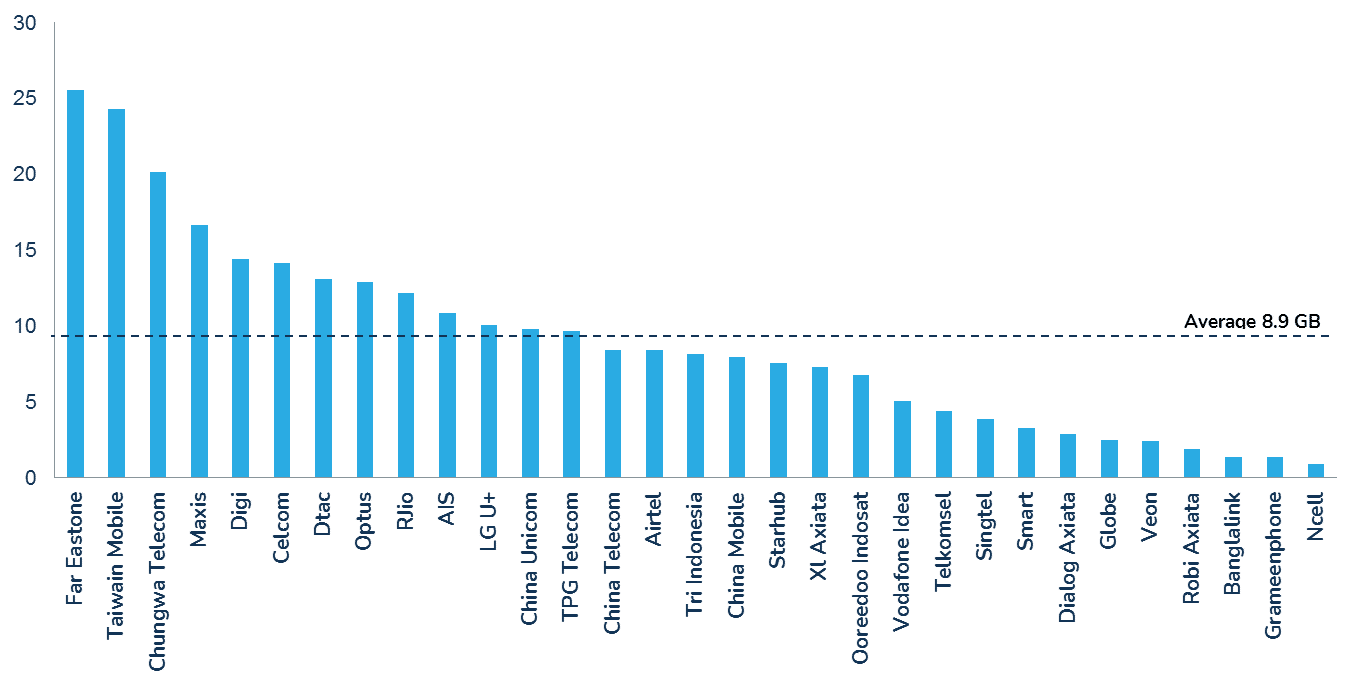

#3 Taiwan leads in mobile data consumption, followed by Malaysia

- On average, data of 23GB was consumed in a month, per SIM card in Taiwan. This was the highest in the Asia Pacific region in 2020. Commercialisation of 5G is one of the key drivers for high data consumption. Research by Opensignal confirms that mobile data consumption shoots up by 2.7 times for a 5G user compared to a 4G user.

- Consumers in Taiwan enjoy 5G services with a very nominal addition to the tariffs of 4G plans. Based on the operator’s data, a 5G post-paid plan for Chungwa telecom ranges from USD22 to USD98.

- In Malaysia, the regulating authorities announced full lockdowns and hence a trend towards higher data consumption was seen. Initially, operators faced challenges in catering to the spike in demand. They responded quickly and put out unlimited mobile plans for users. Maxis recently launched a family pack for 4 with unlimited calls, SMS and data along with a home fiber network connection for USD 72 per month. In 2020, 16.7GB was consumed per SIM card in a month.

Figure 4: Average data consumed per month/SIM in 2020*

*Excludes Japan

#4 Mixed impact on APRU for operators offering 5G services

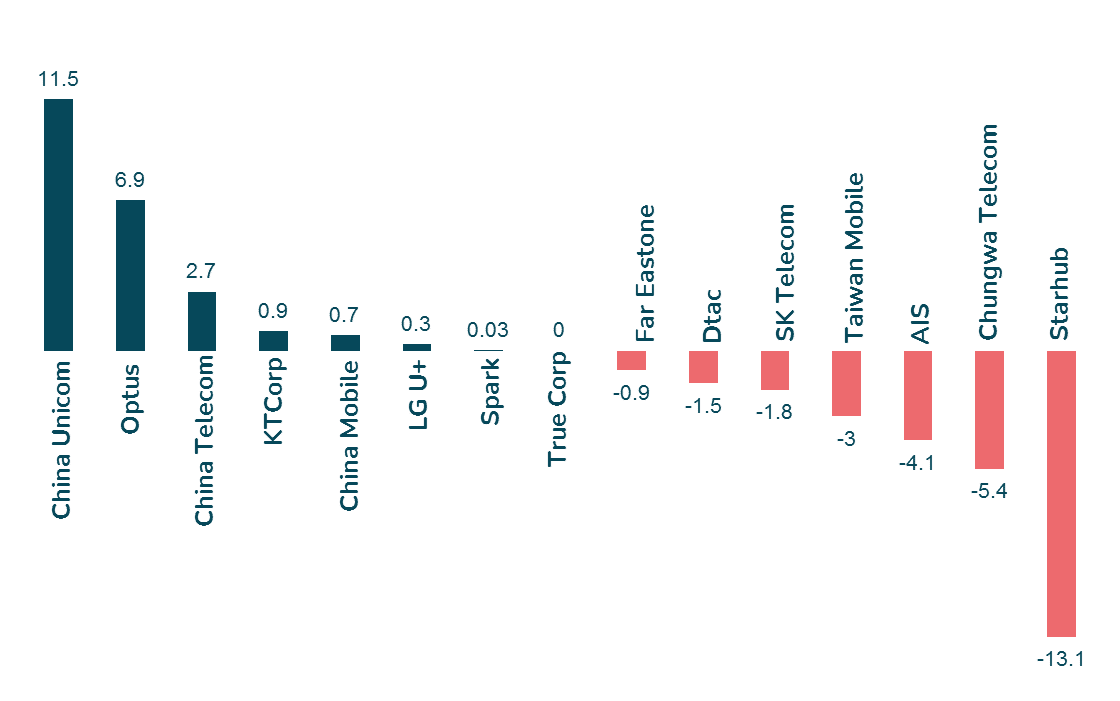

- South Korean operators celebrated their two-year anniversary for 5G in the first quarter of 2021. The operators enjoyed a massive gain in their 5G subscriber base driven by applications such as AR/VR, cloud gaming, smart education and home training.

- China leads the world in 5G and operators have seen a growth in their Mobile ARPU. A combination of factors like favourable government support, infrastructure optimisation and network sharing models to reduce costs have augured well for the Chinese operators.

- While the number of mobile customers declined from 10.44 million to 9.97 million due to strict border closures in Australia, Optus managed to have a growth in Mobile ARPU. The penetration of Optus choice plans increased resulting in higher post-paid revenues. These plans range from USD 30 to USD 60 monthly.

- Service providers in a few countries have struggled to see an uplift in mobile ARPU despite the introduction of 5G largely because of the nominal pricing difference in 5G plans compared to 4G. The majority of operators sold 5G plans at no premium or charging a one-time fee. AIS in Thailand did not get a good response to the newly launched 5G services. The interest of consumers was seen to be inclined towards low pricing packages. The Management discussion and analysis of Advanced Info Services quoted

Although the industry attempted to uplift ARPU by introducing larger unlimited package, the new acquisition remained concentrated on smaller packages as consumers affected by sluggish economy are seeking for value-for-money.

Figure 5: % mobile ARPU change for Asia Pacific telecom service providers, Q1 2021

#5 Revenue from sale of handsets supports overall revenue growth

5G handset sales have been a revenue driver for service providers as consumers upgraded to benefit from the high-speed network. The reduced latency or lower lag has been an encouragement for mobile gamers to switch to 5G mobile phones. China Mobile, the service provider with most 5G users globally, benefitted with a 67% growth in revenues from device sales.

Read here for previous update: Top 10 APAC telecom service providers to ace growth in 2020