With 39,196 employees across 1,337 branches in 36 countries, Australia and New Zealand Bank (ANZ) is one of the top 3 banks in Australia. Operating primarily in Australia and New Zealand, it has expanded to Asia, Europe, the United States, India and the United Arab Emirates.

Financial highlights

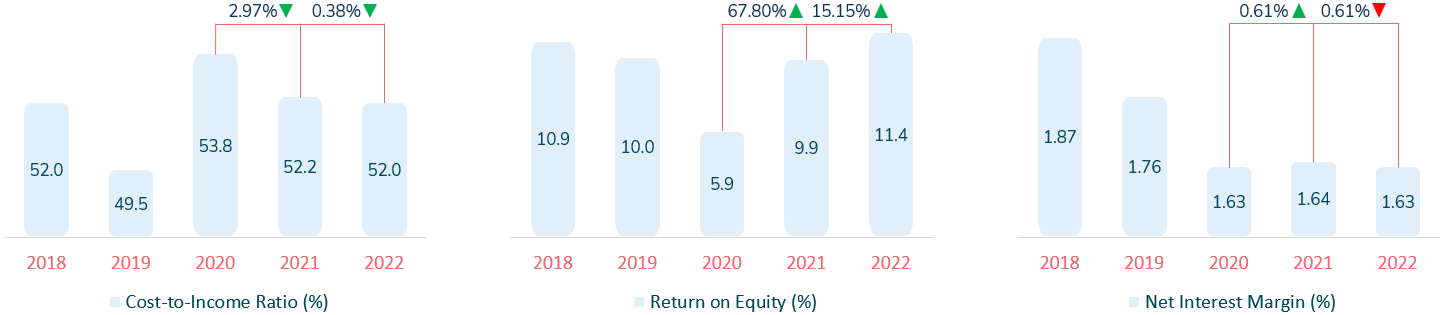

ANZ strives to be more cost-effective, as depicted by its steady decline in the cost-to-income ratio following its 2020 peak (Figure 1). Because of this, ANZ ascertained a positive relationship with the return on equity, creating higher returns for their shareholders. However, the net interest margin (NIM) reduced considerably in 2022, remaining constant because of the rising interest rate globally and in Australia.

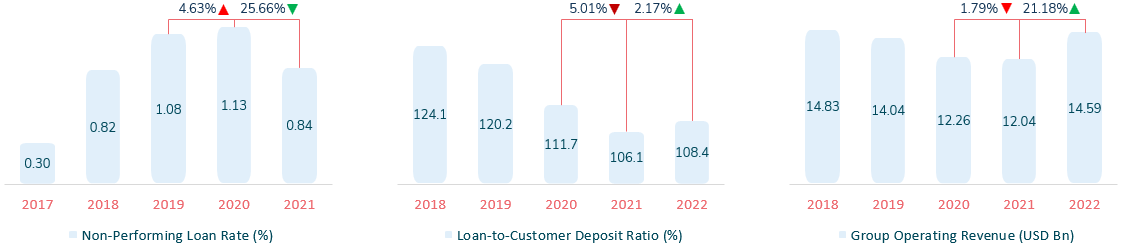

ANZ has reduced its non-performing loans from its 2021 peak (Figure 2). This reduction is likely due to ANZ tightening its loan policy, reflected in its loan-to-customers deposit ratio, which has progressively declined since 2018, with a slight increase in 2022. These combinations of cost-efficiency and prudent loan management have helped ANZ generate a rise of 21.18% in revenue for 2022 despite the slimmer NIM.

Strategic focus areas

- #1 Elevating customer experience with technology

In July 2022, ANZ launched ANZ Plus – the bank’s first dedicated digital bank targeting smartphone users. Available exclusively on the Google Play Store and Apple App Store, ANZ Plus conveys a branchless banking experience, with ANZ Plus account holders separate from the bank’s conventional account holders.

Despite a slow start in July, ANZ Plus users are slowly increasing towards the end of 2022. In addition to ANZ Plus, the bank also offers ANZ Buy Ready and First Home Coach to help potential home buyers with their journey.

ANZ Buy Ready – Online mortgage pre-approval loan that allows home buyers to obtain financing before viewing any property

ANZ First Home Coach – Free service that provides potential home buyers with a bank representative to ease and simplify the home-buying journey

ANZ emphasises that customers can use their suite of tools and services for free and are not obligated to do anything in return.

- #2 Contributing to society

ANZ is aware of the struggle that both Australians and New Zealanders undertake in acquiring a home, expanding its resources to increase the availability of suitable and affordable housing options. The goal the bank aspires to achieve is AUD 10 billion (USD 6.96 billion) of investment by 2030.

To ANZ, it is more than assisting customers in their home journey. It involves being with the customer throughout and even after the entire housing process. This includes informing the customer about their mortgage details, ensuring they have borrowed within their means, and maintaining resiliency to potential future events.

Since 2020, the bank has eased 1,446 customers in New Zealand into more affordable, accessible, and sustainable homes. The bank also ensures that its customers make the best financial decisions and actively promotes the nine principles of financial planning. On top of that, Saver Plus and MoneyMinded, the bank’s financial education programs, serve as strong insight stations for customers to derive the bank’s expertise when making their financial decisions.

- #3 Prioritising information security

Cyber security is paramount to ANZ’s operations. With a Security Operations Centre equipped with AI and professional analysts, the security at ANZ operates 24-7 to analyse millions of data events, whether infrequent or unusual.

In addition to periodic internal and independent third-party defence testing, ANZ cooperates with counterparts, governments, and associated entities worldwide to fight against cyber-security threats. The bank realises a proactive approach is necessary to protect its customers, employing an approach where information is vital on all service levels, from the bank to the customer. For instance, ANZ periodically runs customer-focused campaigns on the latest scam tactics and ensures its staff are well-informed on cyber-threat situations.

However, to tackle cyber-security awareness on a more extensive scope and regular basis, ANZ acts as the sponsor for the “Australian Computing Academy’s Schools Cyber Security Challenges”. Here, the bank co-produces cyber-security modules for students and teachers as part of the digital curriculum.

- #4 Championing employee experience

With a strong priority of enhancing the employee experience, TTM+, a six-month intensive program by ANZ, aims to educate its employees on critical areas encompassing security, cloud, and data. These are but one of many programs the bank has developed to help upskill employee capabilities.

Today, ANZ equips its data engineers with learning support to improve their capabilities and confidence in handling cloud-based platforms. Other programs include the Mindset 2030 program, which has educated approximately 1,000 employees on the current environmental risks. In addition, over 121,000 hours of learning have been supplemented to ANZ’s employees, focusing on developing digital-centric and adaptable leaders.

Mental health and employee well-being are prominent aspects of ANZ’s employee experience measures. Healthy Me, the bank’s digital app, has accompanied over 10,000 employees on their mental health journey, covering various topics via webinars and discussion sheets. Additionally, the bank provides financial and non-financial support to employees involved in accidents or facing health issues, regardless of whether or not it is work-related. Overall, ANZ is committed to supporting the well-being of its employees and helping them build their talents and capabilities.

- #5 Tackling climate change

Net zero emissions by 2025 – this is the main goal that ANZ aims to achieve, committing its finances to crucial sustainability areas, including resource extraction, basic materials and new technologies. Further capitalising on its purpose, the bank is laser-focused, enabling the transition towards lower emission buildings and assisting with sustainable food, beverage, commodity practices and supply chains.

With a focus on sustainability, ANZ also aims to work and partner with financial institutions focused on sustainability to create better solutions. It seeks to achieve this by facilitating the decarbonisation and electrification of the transportation value chain.

To support these efforts, ANZ has set a goal to fund and facilitate AUD 50 billion (USD 34.8 billion) of sustainable solutions by 2025. In FY 2022, the bank completed 140 transactions worth over AUD 18.09 billion (USD 12.59 billion). ANZ’s current portfolio, established in October 2019, has AUD 9.96 billion (USD 6.93 billion) capacity towards this goal.

Digital strategies

- #1 Helping customers adapt digitally

Online support for customers is paramount in the modern age for ANZ’s success, with the bank implementing several initiatives to make it easier for customers to receive assistance. One of these initiatives is “Message Us”, a feature within the ANZ app that allows account holders to interact in a secure and convenient messaging experience. Furthermore, the feature enables customers to ask questions regarding their accounts and home loans without needing a physical visit or phone call.

Adding onto “Message Us”, brokerage customers of the bank can utilise a new feature, “Broker Chat”, to attain priority responses on their query list. This live-chat facility allows brokers to ask common questions, such as the expected credit response date on an app, with little to no wait time for their queries to be answered.

With a further commitment to in-person support for its customers, ANZ has adopted a higher interest in the financial well-being of its customers due to the uptake of digital channels. To support this, the bank has rolled out new branches across 32 locations that focus on providing support and advice to customers on financial well-being rather than carrying out banking transactions. Lastly, to accommodate customers who prefer to visit a branch for more complex needs, ANZ has opened two ANZ Plus stores, committed to providing customers with the support they need, whether online or in-person.

- #2 Providing attractive online services

ANZ strives to provide digital services that will support customers to start, run or grow their businesses. These include:

ANZ GoBiz

- ANZ GoBiz is an online exclusive unsecured lending solution aimed at helping businesses flourish and manage their cash flow.

- Assesses a customer’s financial data, shared from a list of supported accounting software, to determine the creditworthiness of applicants.

- Promotes a fast and easy online application process that takes 20 minutes or less and includes assessing the business’s needs and suggesting the best solution.

- Apply up to AUD 500,000 (USD 347,948) in business loans and up to AUD 300,000 (USD 208,769) in business overdrafts.

ANZ Worldline Payment Solutions

- Market-leading point-of-sale and online payment solution towards ANZ’s commercial and institutional customers, including small businesses.

- Partners with Worldline SA, a French multinational payment and transactional services company, to replace ANZ’s Merchant Acquiring Business (MAB) solution.

- Further increases ANZ’s MAB solution’s competitiveness, security, and reliability to capture the expanding market of online payments following the COVID-19 pandemic.

- ANZ GoBiz and ANZ Worldline Payment Solutions aim to help businesses manage their finances, making online payments more convenient and secure.

#3 ANZ Plus

Today, managing your money can be a tedious affair. To solve this issue, ANZ launched ANZ Plus in 2022, the first branchless digital proposition for customers to access various smart tools. In essence, it acts as a new retail bank with a laser focus on improving the customers’ financial well-being. A key feature of ANZ Plus is the ability to easily save for multiple goals without the need to open a new account.

ANZ Plus experienced substantial growth in the number of savings goals created. More than 45% of active customers maximised full use of the functionality, as compared to less than 5% on the traditional platform.

Innovative products launched

- #1 Virtual cards

Easy and secure is the mainstay of ANZ’s virtual Single Use Card, a digital payment method that ANZ co-developed with Visa and payments technology provider, Conferma to provide a convenient and secure way to make online purchases.

With a one-time use, the card details stored by the merchant will not be usable, making it a safe alternative against a physical card or sharing sensitive payment information with merchants. Now, customers can immediately generate virtual cards from the ANZ application or online banking platform for online transactions.

They can also customise the card with a specific spending amount and expiration date, allowing them to set limits on their spending and prevent unauthorised charges. In short, customers can use the card for various online transactions, from shopping and booking travel to paying bills. In short, the ANZ virtual Single Use Card is a convenient and secure alternative to traditional payment methods.

- #2 ANZ Cashrewards and instalment plans

“Cashback Offers” prove that ANZ has taken into consideration the current trends to further boost the productivity of its ANZ application, introducing the feature for iPhone and Android users in November 2022. Powered by Cashrewards (one of Australia’s leading cashback programs), the feature enables cashback for users who purchase from participating merchants.

In addition to “Cashback Offers”, the introduction of ANZ Instalment Plans for eligible credit card customers allows customers to repay their purchase balance in smaller monthly chunks, making it easier to manage their finances. The repayment term can be chosen from 3, 6, or 12 months, making it convenient and flexible for customers to manage their credit card payments and stay on top of their finances.

- #3 ANZ Plus

Launched in July 2022, ANZ Plus is a dedicated digital bank application available exclusively on mobile platforms. The high savings interest rate of 3.50%, significantly higher than the country’s average of 2.85%, is one of ANZ Plus’s key highlights, drawing customers into the app.

The bank also offers separate account tabs for saving and spending with no monthly or withdrawal fees at major ATMs. Additionally, ANZ Plus offers cardless withdrawal at ANZ’s ATMs and access to professional financial planners for free.

Customers can also use a complementary digital card, which they can instantly add to their Apple Wallets. The targeted audience for ANZ Plus is young adults, from teenagers to millennials, who are seeking better financial planning tools with distinctive perks.

Technology initiatives

- #1 Blockchain-powered bank guarantees

ANZ joined a consortium to develop Lygon, a platform that aims to streamline the process of issuing bank guarantees for property rentals. The consortium includes IBM and Australia’s three largest banks and major property management companies. The goal of Lygon – reduce the time and effort required for bank guarantees, which can usually take up to four months using traditional methods, down to just one day.

To achieve this goal, the consortium began developing a prototype using IBM Blockchain technology, completing it in less than four months. The prototype’s success has enabled tenants to request guarantees online and landlords to reconcile rents digitally. Because of the standardised digital format, other banks and landlords became more eager to participate in the proof of concept.

To date, the development of Lygon has resulted in significant leaps for the financial industry and beyond. From reducing the environmental impact by eliminating the need for physical documents and courier deliveries to minimising the risks of errors and fraud, Lygon represents a significant step forward in streamlining and modernising financial processes.

- #2 Tokenised carbon credits

ANZ has announced that it has made the first-ever payment using an Australian bank-issued stablecoin denominated in Australian dollars (A$DC). The payment was created through a public permissionless blockchain transaction on the 24th of March, 2022. In addition, this payment between Victor Smorgon Group and BetaCarbon via a private digital asset management firm, Zerocap, enabled Victor Smorgon Group to purchase tokenised Australian carbon credits (BCAU) from BetaCarbon with the A$DC.

ANZ worked with Fireblocks, Chainalysis and OpenZeppelin to create the in-house smart contract-powered stablecoin, minted using an Ethereum Virtual Machine-compatible smart contract. The smart contract and supporting infrastructure were designed to adhere to industry best practices for secure digital asset custody and transaction screening.

ANZ plans to continue trials and explore how stablecoins can be used in other industries and for other customers. Nevertheless, this move represents a significant step forward in using digital currencies in the financial industry, potentially paving the way for more widespread adoption of stablecoins.

ANZ’s cloud strategy

ANZ New Zealand is on its way to modernising its banking platform. It achieved this by moving it to the FIS (Fidelity National Information Services) Modern Banking Platform. This move will make it the first bank outside the United States to utilise the platform deployed on Microsoft Azure.

ANZ can now leverage cloud-based technologies for core modernisation through this transition, creating a more convenient, frictionless digital banking service through a cloud-native architecture.

Looking to amplify its cloud data analysis, the bank has partnered with Google to aid the growing trend of transactional data. In addition, this partnership will help prepare ANZ for open banking since Google will use its cloud computing to offer better insights from customer data. As a result, ANZ will be free to formulate a more concise and well-developed strategy for open banking.

Growth opportunities

- #1 Cost to serve

ANZ has been consistently conducting its operations by increasing its operating revenues from FY2021 to FY2022. The key highlights for the bank include the following:

- 5.03% increase in net interest income

- 7.56% decline in fee & commission income

- 23.89% decline in other market income

The primary reason for these declines are the following:

- Fee changes in the Breakfree package

- Lower divestment of business segments

- Reduction of funds under management fees in the New Zealand division.

The staff expense at ANZ also increased from USD 3.41 Bn in FY2021 to USD 3.66 in FY2022. Despite the 2.55% decline in the number of employees, the cost per employee increased from USD 84,903.20 in FY2021 to USD 93,288.70 in FY2022.

Moving forward, ANZ should aim to rectify and improve upon two aspects – the Net Interest Margin (NIM) and the Loan-to-Deposit Ratio (LDR).

Potential solutions to help ANZ increase both aspects are as follows:

- Add new fee-generating products, including insurance products and mutual funds, to improve the NIM, which has currently witnessed a minimal decline of 0.61%

- Disburse more loans to offset the reserves kept in deposits to increase the current LDR (84.33), which is below the threshold value of 90%. This initiative will help generate more revenue in terms of interest, thus further increasing its NIM.

- #2 Banking in the Metaverse

ANZ Worldline Payment Solutions has leased a high-traffic plot of land from Bitcoin Suisse to host the ANZ Worldline Payment Solution Showroom. The showroom has already hosted several notable company events, including;

- Solis, the Swiss electrical goods brand

- The Chedi, the luxury hotel brand

- Naked Life Beverages, the Australian beverage company

The showroom is a valuable resource to showcase its market-leading point-of-sale and online payment solutions to its commercial and institutional customers, including small businesses.

Future suggestions view ANZ expanding their footprint in the Metaverse by following the leaders, JP Morgan and Union Bank, to learn more about ANZ. Moreover, ANZ can assign customer service staff or deploy chatbots in their virtual property to create an interactive customer experience.

The bank can also integrate its API into the Metaverse, unlocking an immersive VR banking experience where customers can perform day-to-day transactions in the virtual space. With that, ANZ can also help other businesses establish their presence in the Metaverse via dedicated programs.

The aspiration to create its own virtual currency is strong for ANZ, envisioning a future where customers can save or spend it within ANZ’s virtual bank. Taking a step further, ANZ can then instate virtual branches and ATMs in prime regions within the Metaverse to provide the same convenience of a physical customer to a virtual customer.

- #3 Buy Now Pay Later (BNPL)

ANZ currently offers two types of BNPL products for its credit card holders

ANZ Low Rate Visa

- The credit card offers up to 55 interest-free days on offline and online purchases with the card and a promotional 1.99% interest rate p.a. on balance transfer.

ANZ Instalment Plans

- ANZ Instalment Plans is a BNPL scheme offered to most ANZ credit card holders, allowing them to convert a sum of the spent amount on their credit card into a 3, 6, or 12-month loan.

- Includes no cancellation fees, no prepayment fees, and ease of application through the ANZ mobile app.

One of ANZ’s main competitors in the BNPL market is Afterpay, which offers its BNPL service through its own app, available in all major app stores. Afterpay offers a standard 6-week instalment plan for items purchased offline and online, providing a convenient virtual card for its customers to spend via Apple Pay and Google Pay. However, unlike ANZ, Afterpay does not charge interest on its BNPL services, instead charging partner merchants a service charge.

Areas of improvement that ANZ should focus on include:

- Combining its BNPL offering as one product that provides 55 days interest-free period and 3, 6 or 12-month instalments to match competitors such as Afterpay.

- Expanding its targeted audience and offering BNPL to existing customers or new customers.

- Leveraging its brand name and resources to get an edge against its competitors.

- #4 Leveraging blockchain

ANZ’s efforts in blockchain and cryptocurrency highlight the bank’s willingness to embrace new technologies and innovate in the financial sector. ANZ co-developed Lygon, which uses smart contracts to streamline ANZ’s bank guarantee signing process, potentially saving cost and reducing emissions. Furthermore, cryptocurrency technology proves to be the first in Australia’s issuance. Specifically, it was the first time a stablecoin was denominated in the Australian dollar to facilitate the purchase of tokenised carbon credits for their client.

With this, ANZ should take a step further in using smart contracts and developing cryptocurrency. For example, ANZ can continue transforming traditional physical contracts into smart contracts, such as internal documents, to smart contract documents powered by ANZ’s intranet for added security. In a similar context, ANZ can offer a commercial package for their institutional clients to transact with A$DC for a frictionless, secure and cheaper alternative to current methods, providing ANZ with an edge against ANZ’s competitors.

- #5 Open banking

Currently, ANZ is a data holder wherein the bank can share the Customer Data Rights (CDR) data with an accredited organisation when authorised to do so by the customer. To build up on this, ANZ has partnered with Frollo and is preparing to become an accredited data recipient, after which the bank will be able to collect and use the CDR data.

The benefits of open banking for ANZ:

- Lower transaction fees – Reducing transactional costs will result in lower operating costs of bank-to-bank settlements.

- Expand service offerings with APIs – Connect with other APIs and broaden their service offerings by offering solutions provided by Fintechs in a ready-to-go manner within their mobile app.

- ANZ can offer a Fintech’s specialised services to customers within their app

- Elevate customer engagement – By integrating open APIs into its existing infrastructure, ANZ can appeal to its existing customers who want their banks to provide more innovative offerings.

- ANZ will be able to attract more potential customers that desire to explore more than just the traditional services of a bank

Conclusion

Choosing to focus on what matters, ANZ has started to pick up after a rough year of dealing with the pandemic. This includes tackling climate change, contributing to society, prioritising information security, elevating the customer experience with technology and championing employee experience. ANZ has also not forgotten to innovate digital products such as ANZ Plus, virtual cards, ANZ Cashrewards and instalment plans. With that, ANZ still has some growth opportunities that will widen the gap with their competitors, from banking in the Metaverse and improving BNPL offerings to developing blockchain and capturing the emerging Islamic finance industry.

Check out our previous report here.