Executive summary

The first half of 2025 reaffirmed the enterprise segment as a central growth engine for telecom operators across Asia-Pacific. Enterprise revenues continued to rise, now contributing nearly one-quarter of total industry revenue, underscoring a clear structural shift away from consumer-driven models. This transition reflects the industry’s repositioning from pure connectivity providers to digital infrastructure and technology enablers, a redefinition of purpose that aligns with long-term transformation imperatives.

The most significant development has been the accelerated growth of non-connectivity revenues, including:

- Cloud, data centres, IoT, managed services, and cybersecurity, which collectively now account for over half of total enterprise revenue.

- These services are expanding faster than legacy network offerings, reinforcing the success of diversification strategies and the ongoing rebalancing of telecom business models.

This shift signifies that value creation is migrating decisively from traditional network services toward higher-margin, technology-driven platforms that enable enterprise digital transformation.

Growth patterns in H1-2025 were geographically broader than in prior years.

Strong performances came from multiple markets, reflecting the structural and widespread demand for cloud, AI integration, cybersecurity, and digital transformation.

However, performance divergence is evident:

- A leading cohort of operators achieved outsized growth by scaling digital platforms and monetizing adjacencies.

- Others lagged, weighed down by continued reliance on legacy voice and data services.

The result highlights the growing importance of execution quality, capital discipline, and speed of strategic pivot as key differentiators.

Operators are adopting varied but converging approaches to enterprise growth:

- Infrastructure-led models focused on cloud, data centres, and AI integration.

- Monetization-driven models that repurpose existing network assets to fund new digital ventures.

- Adjacency-focused models expanding into fintech, digital BPO, and IT services.

Each model reflects a distinct response to market maturity and capability depth but collectively points toward a single direction that enterprise diversification is a strategic necessity going forward.

The enterprise business is no longer a peripheral segment. It has become a core strategic pillar of the industry. Cloud and AI now anchor future revenue streams, IoT is embedding telcos deeper into vertical ecosystems while adjacencies are broadening both growth horizons and strategic resilience. The emerging winners will be those that combine scale with agility, building robust infrastructure while capturing ecosystem opportunities, cultivating sticky enterprise relationships, and delivering differentiated, technology-led solutions. The trajectory is clear: enterprise will define the next phase of telecom growth in Asia-Pacific.

Enterprise segment revenue analysis: H1-2025

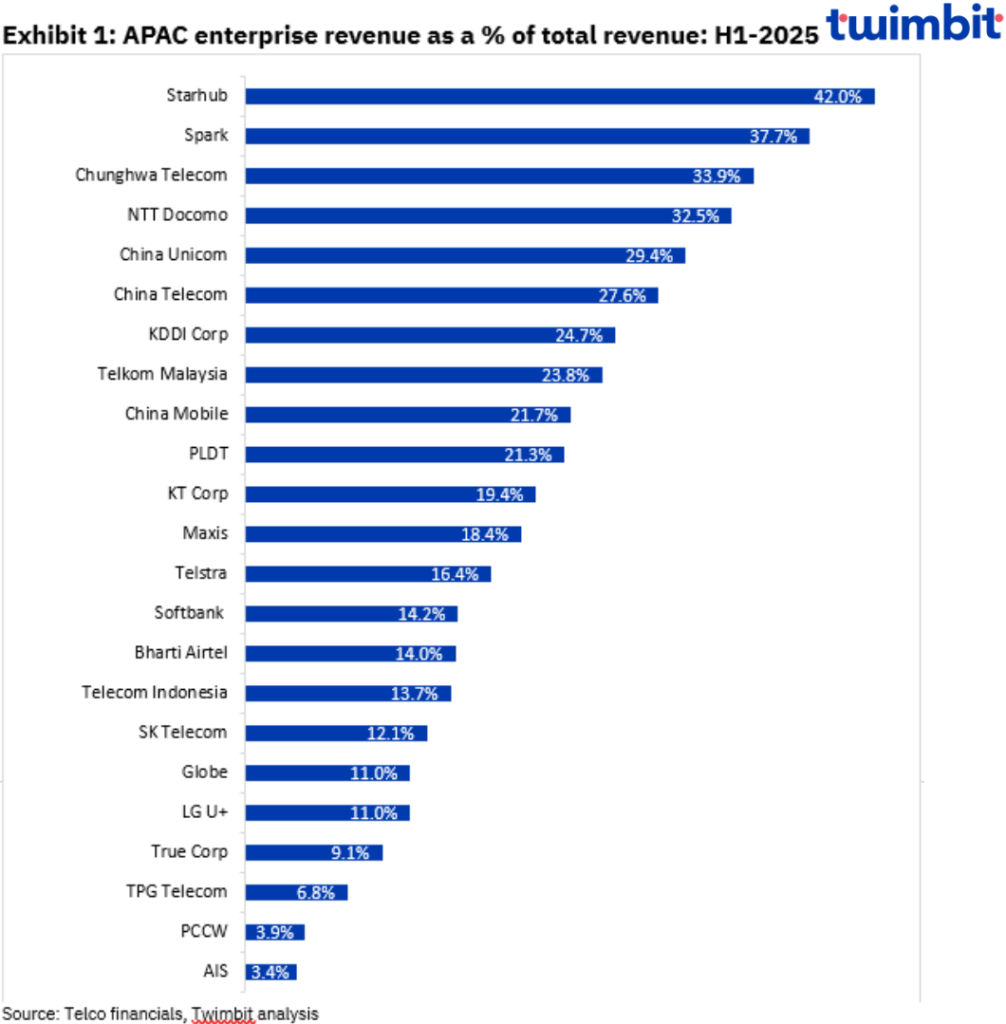

Enterprise segment contributed 22.3% of the total revenue for APAC telcos in H1-2025.

- Enterprise revenue for APAC telcos grew by 4.7% YoY, reaching ~USD 60.3 billion in H1-2025.

- The trends indicate that telcos are capitalizing on the potential growth opportunity by expanding beyond core consumer connectivity services into segments like high margin enterprise connectivity, cloud, IT services and transforming into a TechCo.

In contrast to H1-2024, when Japan-based operators led regional performance, growth in the latest half was more geographically diverse. The highest YoY achievers were distributed across multiple markets, with Australia, Japan, Hong Kong, Thailand, and Singapore all registering standout results.

Enterprise non-connectivity revenue analysis: H1-2025

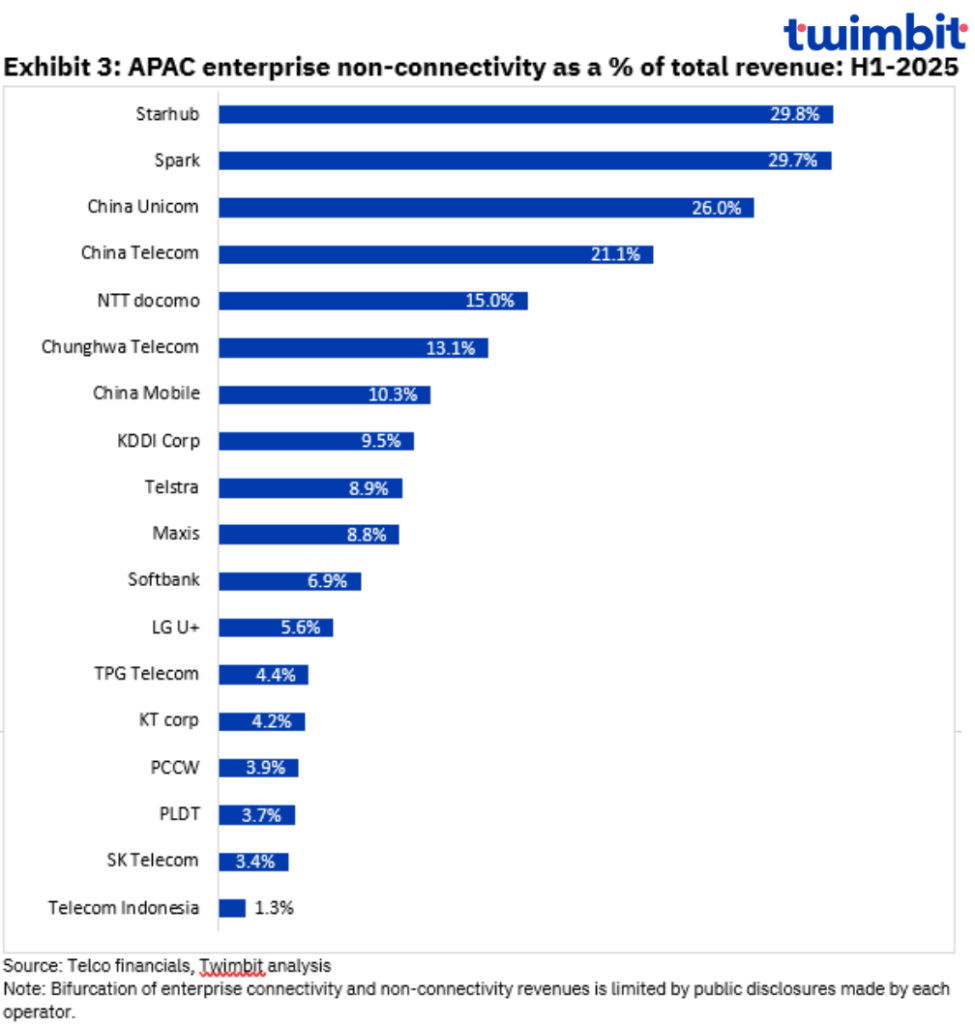

Enterprise non-connectivity revenue contribution increased 80 basis points (bps) on a YoY basis in H1-2025 to reach 13.0%.

- Enterprise non-connectivity segment revenue for APAC telcos grew 8.1% YoY to reach ~USD 32.7 billion in H1-2025, highlighting the increasing diversification of telco offerings beyond traditional connectivity services.

- Only six APAC operators generated material contributions from non-connectivity services, each surpassing the 13.0% average threshold. This concentration underscores the disproportionate impact of a limited set of players in pulling the regional average upward.

- Enterprise non-connectivity revenue contribution (for the telcos analysed) reached a significant ~54.3% share of total enterprise revenues in H1-2025, surpassing the previous high of ~49.6% in H1-2024.

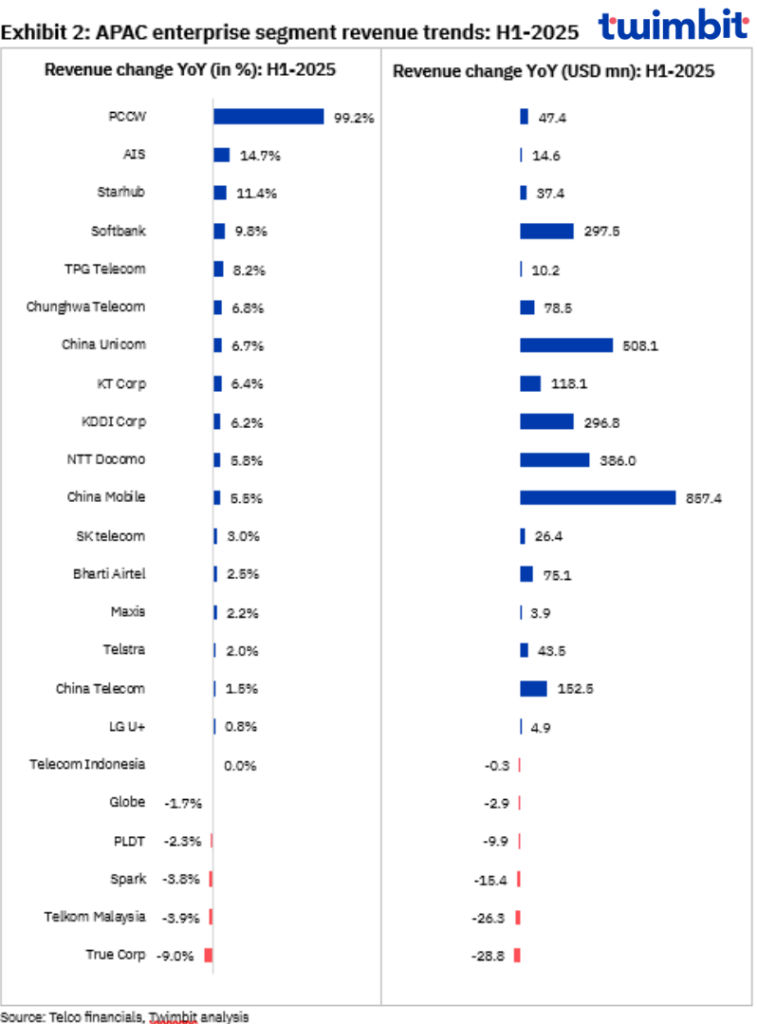

- Mirroring trends in enterprise revenues, non-connectivity growth in H1-2025 was more geographically diversified. PCCW, Chunghwa Telecom, SoftBank, StarHub, and SK Telecom recorded the strongest gains, marking a clear departure from H1-2024 trends, when outsized growth was concentrated primarily among Japanese and Chinese operators.

Notable trends and shifts across APAC: H1-2025

StarHub, and Spark reaffirmed their positions as the region’s leading diversifiers, with enterprise segments contributing 42.0%, and 37.7% of total revenues, respectively, well above the APAC average of 22.3%.

Starhub’s enterprise business remained a major revenue pillar in H1-2025, contributing approximately 42.0% of total revenues. Growth was underpinned by non-connectivity offerings, particularly managed services and cybersecurity, supported by favourable project timing recognition.

- Enterprise revenues rose 11.4% YoY in H1-2025 to USD 364.6 mn. While connectivity growth remained subdued, the decline was more than offset by ancillary enterprise services, underscoring their growing role as mainstream revenue drivers.

- The demand for enterprise connectivity and carrier voice services remained subdued, reflecting intensified competition driven by ongoing consolidation in Singapore’s telecom industry.

- The growth in non-consumer segment was driven by digital infrastructure project completions and heightened cybersecurity demand. As a regulated CII provider, it is building cross-sector trust and positioning managed services and cybersecurity as key growth engines beyond connectivity.

- StarHub undertook trials of Southeast Asia’s first 5G Cloud RAN under its Cloud Infinity strategy, advancing toward a hybrid multi cloud, cloud-native network. The operator also partnered with Red Hat, Dell, and Nokia, to enhance the efficiency of its enterprise segment.

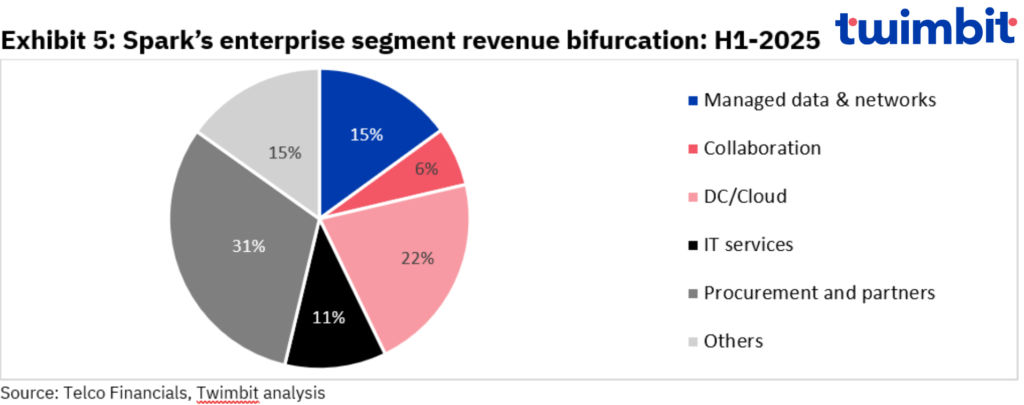

Spark’s enterprise business reported revenues of USD 391.7 mn in H1-2025, a 3.8% YoY decline. Despite the contraction, the segment maintained strategic significance, contributing 37.7% of total revenues, the second-highest share among APAC operators.

- The decline was driven by weaker IT and managed network services, as enterprises shifted from legacy products to lower-ARPU alternatives. Stronger collaboration revenues, supported by cloud contact centre demand and meeting room upgrades, partially offset the impact.

- Going forward, Spark agreed to sell a 75.0% stake in its data centre business to Pacific Equity Partners, securing capital for a 130MW+ pipeline while retaining 25.0% ownership, unlocking near-term value and sustaining long-term growth participation.

- The operator is pursuing strategic partnerships to accelerate enterprise transformation, with Spark’s collaboration with Infosys leveraging modern AI tools to drive innovation and deliver competitive differentiation in the enterprise segment.

Chinese telecom operators sustained their position as the industry leaders in absolute topline growth for another quarter. In the first half of 2025, all three major players reported an increase in enterprise revenues as a share of total revenue, underscoring the sector’s strategic pivot toward higher-value segments. This trajectory reflects both the growing demand for enterprise solutions and the operators’ ongoing efforts to diversify beyond traditional connectivity into more resilient and higher-margin businesses.

China Mobile delivered 5.5% YoY growth in enterprise revenues, reaching USD 16,346.3 mn in H1-2025. The segment contributed 21.7% of total revenues, up 120 basis points from 20.5% in H1-2024, highlighting the company’s continued shift toward higher-value segments and the growing importance of diversified services in its overall portfolio.

- Revenue growth was primarily driven by the cloud segment, which recorded an 11.3% YoY increase, rising from USD 6,970 mn in H1-2024 to USD 7,758.5 mn in H1-2025. This underscores cloud’s role as the key engine of China Mobile’s enterprise growth trajectory as it accounts for ~10.0% of total revenues.

- China Mobile is reshaping its cloud portfolio by targeting high-growth digital ecosystems and capturing early-mover advantages. It is scaling the “To V” market with over 69 mn smart connected vehicles and China’s first “vehicle-road-cloud” pilot, while expanding its commercial customer base by more than 10 mn packages.

- Growth in its Visual Internet business, now interconnecting nearly 90 mn video streams, alongside a 38.0% bid-winning share in the low-altitude economy and rapid DSSN deployment in seven pilot cities, underscores a deliberate pivot toward infrastructure leadership and diversified revenue streams in next-generation digital markets.

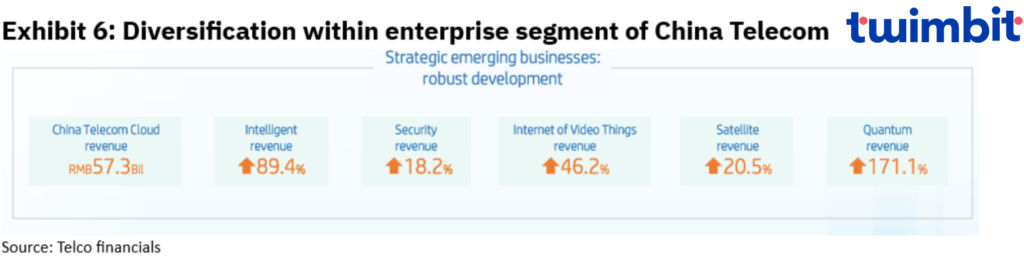

China Telecom reported a 1.5% YoY increase in enterprise revenues in H1-2025, with the segment contributing 27.6% of total revenues, up marginally from 27.5% in H1-2024. Net additions of USD 152.5 mn brought enterprise revenues to USD 10,351.7 mn, reinforcing the segment’s growing weight in the company’s overall portfolio.

- China telecom cloud revenue has been the major driver of this increase, experiencing a revenue increase of 3.8% YoY in H1-2025, while the segment’s contribution to total revenues increased to 21.1% in the same period.

- The operator is accelerating cloud transformation by scaling its “Xirang” platform to 77 EFLOPS, expanding AI training to 100,000 developers, supporting 80 research institutes, and securing leadership in computing power interconnection, reinforcing its position in China’s intelligent cloud ecosystem.

- The operator is among the region’s first to implement quantum technology, diversifying its enterprise portfolio with over 6 mn quantum communication subscribers, 3,000+ industry customers, and 30 mn visits to its Tianyan Quantum Cloud platform.

China Unicom reported a 6.7% YoY growth in enterprise revenues in H1-2025 to reach a total of USD 8,131.6 mn, contributing 29.4% of the total revenues. The contribution increased 150 basis points from 27.9% in H1-2024.

- The Computing and Digital Smart Applications (CDSA) revenues were driven by expanding cloud services, enhanced global data centre connectivity, and the development of intelligent computing hubs.

- Revenue growth in the cloud and data centre segments remained strong, with cloud up 4.6% YoY and data centres rising 9.4% YoY, supported by a 60.0% surge in AIDC contract value in H1-2025.

- The operator is sharpening its focus on intelligent services, including dataset management, delivery of large language model (LLM) services, and the development of industry-specific AI agents to capture emerging digital opportunities.

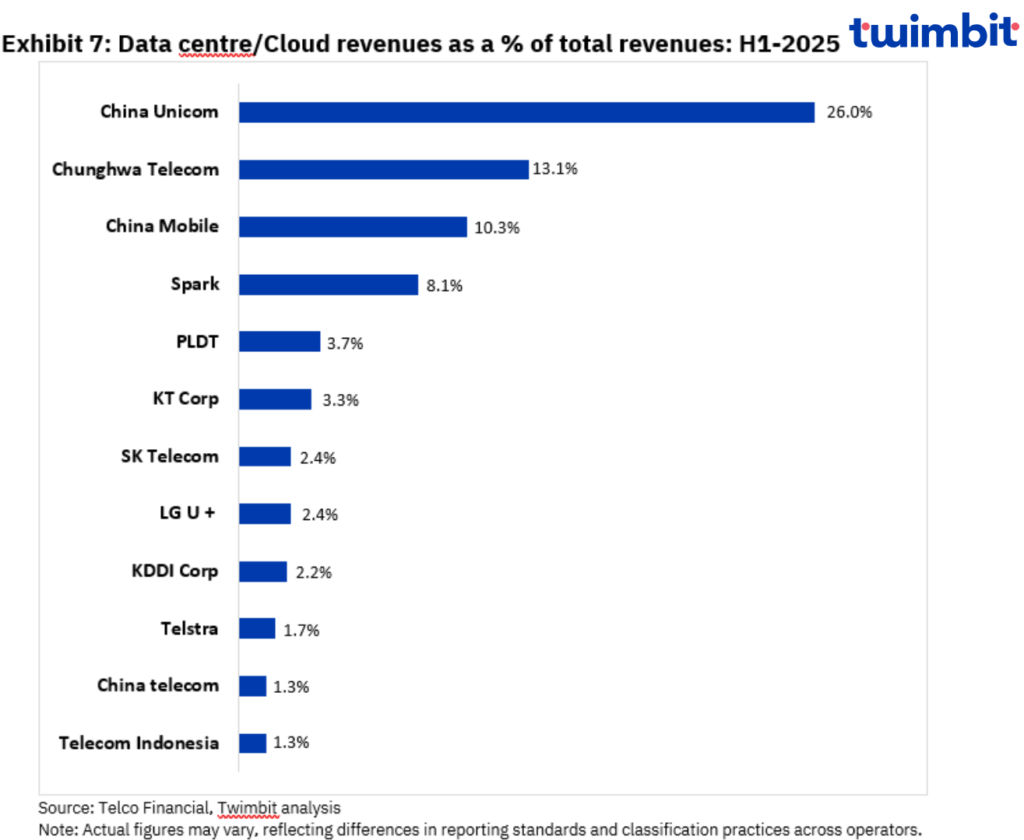

Data centres and cloud segment is emerging as one of the top performers in the non-connectivity enterprise & wholesale revenues. While Chinese telco operators are the leaders of capitalizing on the growth of cloud segment, operators like Chunghwa telecom, KT Corp and KDDI also have notable market share in the segment.

APAC telcos are recalibrating cloud and data-centre strategies through a blend of expansion, divestitures, and adjacencies. While some scale sovereign AI infrastructure, others monetize assets or embed digital BPO and fintech, collectively reinforcing enterprise growth and long-term digital leadership.

- Chinese telcos are accelerating cloud and data-centre scale through DSSN pilots, Link-Cloud platforms, and sovereign AI infrastructure, prioritizing capex efficiency and national digital policies over divestures. These moves strengthen leadership in data circulation while embedding AI-driven growth into core enterprise offerings.

- Chunghwa Telecom is deepening investments in AI-ready data centres and cloud-native platforms while expanding international smart solutions. By avoiding divestures, it reinforces domestic data leadership and positions itself to capture differentiated enterprise AI workloads with scale, resiliency, and integrated services.

- Spark executed a strategic 75% divestiture of its data-centre assets to Pacific Equity Partners, retaining a minority stake. This unlocks capital for network and AI-led enterprise expansion while ensuring long-term access to critical infrastructure through partnership.

- KDDI Corp is expanding domestic data-centre capacity and positioning digital BPO alongside cloud and IoT services. By embedding automation and AI within its infrastructure, KDDI is moving beyond scale to deliver enterprise differentiation and higher-value digital transformation solutions.

- KT Corp is leveraging KT Estate and KT Cloud to expand data-centre infrastructure, while integrating AI and fintech adjacency through BC Card. This dual investment strengthens recurring enterprise revenues and diversifies growth engines across infrastructure, digital services, and payments.

PCCW recorded the strongest enterprise momentum among peers in H1-2025, with segment revenues surging 99.2% YoY to USD 95.2 mn. Net additions of USD 47.4 mn highlight accelerated traction in enterprise solutions and move towards diversification beyond core telecom services.

- Although PCCW’s enterprise revenues nearly doubled in H1-2025 as compared to H1-2024, the segment still accounts for just 3.9% of total revenues, second lowest among peers, despite a 180 bps increase YoY.

- The increase was driven by major deal winnings by PCCW solutions, the IT services arm of PCCW group.

True Corp reported a 9.0% decline in enterprise revenues in H1-2025, for a total of USD 292.5 mn, with a net decline of USD 28.8 mn.

- The segment represented 9.6% of the total revenues, down 80 basis points from 10.4% in H1-2024.

- The decline is driven by lower revenues from spectrum arrangement, which basically includes network equipment rentals and a network outage reported by the operator in Q2-2025.

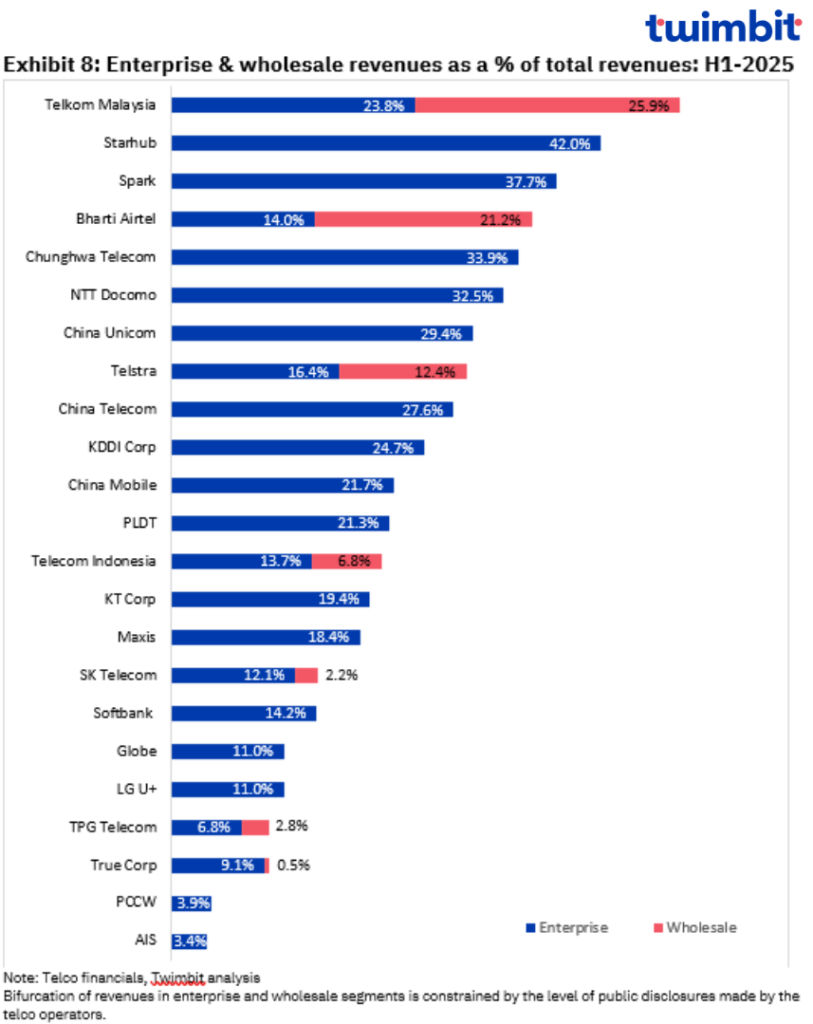

While most operators do not separately disclose interconnection and wholesale (carrier-to-carrier) revenues, some provide detailed disclosures. Including them within the enterprise segment slightly reshapes the overall picture. Enterprise & wholesale combined accounted for 23.6% of total industry revenues in H1-2025, underscoring their growing strategic weight. Telkom Malaysia, Bharti Airtel, and Telstra stand out as leaders in monetizing the wholesale segment, effectively leveraging network scale and cross-border connectivity to drive incremental enterprise value.

Telekom Malaysia leads the region in enterprise & wholesale penetration, with the segment accounting for 49.7% of total revenues in H1-2025, reaching a total of USD 648.8 mn.

- Despite its leadership position, Telekom Malaysia recorded a 3.9% YoY decline in H1-2025, with B2B revenues contracting 5.2% and carrier-to-carrier (C2C) wholesale revenues down 2.6% over the same period.

- The B2B segment experienced a decline due to a higher base effect as there was a one-off gain related to an arbitration settlement in Q2-2024.

- The C2C wholesale segment contracted in the first half, reflecting lower revenues from managed wavelength and IRU, coupled with a slowdown in global voice traffic.

- Telekom Malaysia is future proofing its non-consumer segment by scaling 4G/5G backhaul, expanding HSBB access, deploying AI at IPDC, and strengthening international capacity with submarine cables, data centres, and managed wavelength solutions for resilient digital infrastructure.

Research Methodology and Assumptions

- “APAC telcos enterprise business update: H1-2025” report provides a summarized view of enterprise segment revenue performance of leading telcos in the APAC region for the H1-2025 (Jan-June 2025).

- This report leverages secondary research methodologies and data provided by telecommunication companies (telcos) themselves. Twimbit employs a calendar year approach (January- December) for all telcos to ensure consistent comparison, regardless of their individual fiscal year ending periods.

- The research examined ~49 telcos across 20 Asia Pacific countries. Selection criteria included economic significance and reliable data availability. Enterprise segment revenue data was available for 23 telcos, whereas non-connectivity revenue was captured for 18 of those.

- For consistent analysis, a constant exchange rate (average for April – June 2025) has been applied when converting local currencies to USD.

- Enterprise segment revenue refers to services provided to business customers (large, medium, and small). It excludes consumer (B2C) revenue. The analysis considers the following sub-segments within the telco enterprise segment:

- Total Enterprise (Connectivity + Non-Connectivity): This includes voice, fixed-line, and data communications (leased lines, IP-VPN, SD-WAN, etc.) offered directly to enterprises. It also encompasses connectivity services like managed services, IoT specifically provided to businesses and

- Enterprise Non-Connectivity: This extends beyond core connectivity services and primarily includes cloud solutions, managed services (collaboration, contact centres, other IT services and applications), IoT, cybersecurity, etc. It excludes any connectivity solutions offered to business customers.

- The primary focus of the analysis was to understand the contribution of the enterprise segment’s performance and revenue to the telcos’ overall revenue. Additionally, a detailed peer comparison was conducted to identify leading telcos and their best practices.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers in case the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The data collected may be subject to reporting inconsistencies inherent to various telcos and hence can be leveraged for reference and guidance purpose. The analysis is based on publicly available information.

Read more:

Global telcos performance benchmarks: Summer 2025