Key Takeaways

- The average Year-on-Year (YoY) revenue growth for APAC telcos has declined, from ~5.5% in Q1-2023 to ~3.3% in Q1-2024.

- Despite the slowdown in growth, 38 telcos in Q1-2024 achieved a combined revenue of USD 142.8 billion. Around 77% of these telcos reported positive revenue growth, with 7 recording YoY gains exceeding 10%.

- The average EBITDA margin stabilized at 38.1% in Q1-2024, reflecting a focus on cost-containment measures, operational efficiency, and sustained top-line growth.

- About 72% of the 35 analysed telcos reported positive changes in EBITDA during Q1-2024. Only ~9% witnessed a marginal decline, limited to a maximum of -3%.

- Average CAPEX intensity declined significantly from 15.3% in Q1-2023 to 12.6% in Q1-2024. The maturation of 4G and 5G network deployments in India and China resulted in lower CAPEX allocation.

- Of the 28 analysed telcos, only ~36% reported YoY CAPEX growth in Q1-2024 compared to ~54% in Q1- 2023.

- Among the 29 analysed telcos, ~62% reported YoY ARPU growth in Q1-2024. With, 28% achieved higher ARPU growth in Q1-2024 compared to Q1-2023.

- The expansion of 4G/5G networks, ARPU improvement initiatives, and increasing demand for data services have contributed to consistent ARPU growth.

Revenue analysis of APAC telcos: Q1-2024

Average revenue growth for APAC telcos slowed from ~5.5% in Q1-2023 to ~3.3% in Q1-2024

The 38 telcos achieved a combined revenue of USD 142.8 billion (YoY net new revenues of ~USD 4.8 billion) in Q1 2024.

About 77% of the telcos reported positive revenue growth, with 7 achieving double-digit growth.

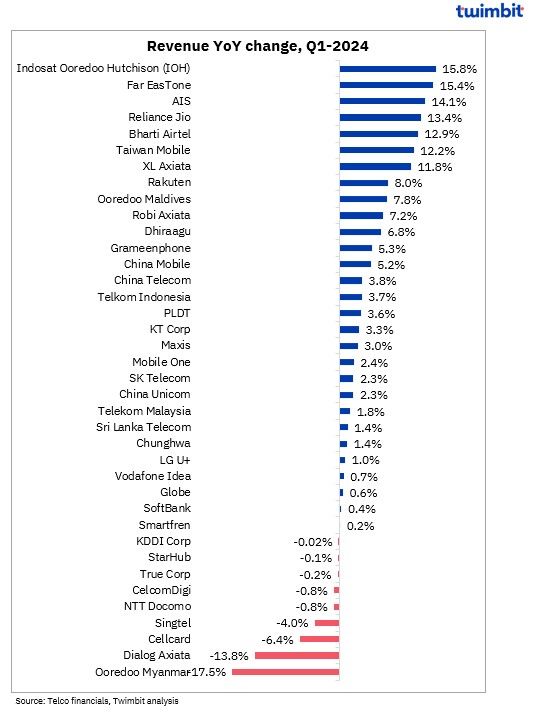

Exhibit 1: Revenue trends (% change) for APAC telcos (YoY basis), Q1 2024

Indosat Ooredoo Hutchinson (IOH)

IOH posted revenues of USD 883.1 million (IDR 13.8 trillion) with a 15.8% YoY growth in Q1 2024, driven by:

- Cellular Revenues rose 13.6% YoY to USD 744 million (IDR 11.7 trillion), with data revenue growth offsetting declines in voice and value-added services.

- MIDI Revenues increased 35.5% YoY to USD 125.8 million (IDR 1.9 trillion), led by higher revenues in IT Services and fixed connectivity.

- Fixed Telecommunication Revenues fell 10.7% YoY to USD 13.2 million (IDR 207.2 billion) due to a drop in international call revenues.

- Subscriber count increased 2.3% YoY to 100.8 million.

- The 4G BTS count reached approximately 184k, driven by network infrastructure enhancements, rising data traffic, and higher incremental revenue per subscriber.

FarEasTone

Revenue rose 15.4% YoY to USD 819.2 million (TWD 25.7 billion) in Q1 2024, driven by:

- Mobile service revenue grew 18.3% YoY to USD 572.7 million (TWD 18 billion).

- Average mobile subscriber count increased 26.6% YoY to ~9.1 million.

- Postpaid 5G penetration increased from 37% in FY 2023 to 39% in Q1 2024.

- “New Economy Business” revenue (big data, AI, and IoT) increased 12% YoY.

- Enterprise segment (54% of revenue) saw revenue growth of 18% YoY from ICT business and 52% YoY from security services.

- Consumer segment (46% of revenue) saw revenue growth of 15% YoY from digital video and 12% YoY from digital video, handset insurance, and payment services.

AIS

AIS achieved a 14.1% YoY revenue increase to USD 1.5 billion (THB 53.3 billion), driven by:

- Growth in Fixed Broadband (FBB): Fixed broadband revenue rose ~163% YoY to USD 199.7 million (THB 7.118 billion) in Q1 2024.

- Consolidation of TTTBB’s revenue and expansion of the broadband business with high-quality subscribers.

FBB subscribers increased by 112.3% YoY to 4.8 million in Q1 2024 due to:

- FBB ARPU increased 21.9% YoY to USD 13.9 (THB 496) from a focus on comprehensive packages.

- Revival in the Mobile Business: Mobile revenue rose 3.7% YoY to USD 851.1 million (THB 30.339 billion) in Q1 2024. ARPU also increased due to:

- Focus on value-based packages.

- Cross-selling with value-added services.

- Increased 5G adoption from tourism recovery.

Despite the 2.4% YoY decline in subscribers to 45 million in Q1 2024, the ~67% YoY rise in blended ARPU to USD 6.3 (THB 224) supported the mobile revenue growth.

- Increased Revenue contribution from Enterprise Non-Mobile & Others Segment: Revenue rose ~27% YoY to USD 561.1 million (THB 2 billion), driven by connectivity service and TTTBB’s revenue recognition.

Reliance Jio

Reliance Jio achieved a 13.4% YoY revenue increase to USD ~3.5 billion (INR 288.7 billion) in Q1 2024, driven by:

- 481.1 million subscribers, including 108 million 5G subscribers.

- Strategic initiatives such as IPL Dhan Dhana Dhan (a plan offering two months of free services on a two-month Rs 234 recharge) for new JioBharat device users.

- JioAirFiber coverage expanded to ~5,900 cities/towns with pan India coverage expected soon.

Bharti Airtel

Bharti Airtel reported a 12.9% YoY revenue increase to ~USD 3.4 billion (INR 285.1 billion) in Q1 2024.

- Mobile Services: Revenue grew 12.9% YoY to ~USD 2.7 billion (INR 220.657 billion), with 4G/5G customers comprising ~72% of the mobile customer base.

- Home Business: Revenue rose ~20% YoY to USD 158.4 million (INR 13.1 billion), driven by a 26% increase in home customers, reaching ~7.6 million.

- Digital TV Services: Revenue increased 5.5% YoY to USD 926.2 million (INR 7.7 billion), 1.3% increase in customers to ~16.1 million.

Airtel Business revenue also rose by 14.1% YoY to USD 657.6 million (INR 54.616 billion), driven by contributions from converged portfolio offerings and data and core connectivity solutions.

Taiwan Mobile

Taiwan Mobile reported a 12.2% YoY revenue increase to USD 1.5 billion (TWD 48.3 billion) in Q1 2024.

- Mobile service: Revenue increased 27.2% YoY to USD 508.5 million (~TWD 16 billion).

- Revenue contribution from T Star (first quarter post-merger).

- 7.1% YoY ARPU increase in TWM’s existing smartphone postpaid users and recovery in roaming revenue.

- momo segment: Revenue grew ~7% YoY to USD (TWD 26.878 billion) driven by a 7% YoY increase in the active user base.

These segments helped offset the partial decline in its CATV revenue.

XL Axiata

XL Axiata achieved an 11.8% YoY revenue increase to USD 482 million (IDR 8.4 trillion) in Q1 2024.

- ARPU rose from USD 2.6 (IDR 40,000) in Q1 2023 to USD 2.8 (IDR 44,000) in Q1 2024.

- The total subscriber base reached 57.6 million, with data and 4G subscribers comprising 97% and 4G subscribers 95% of the total base.

Ooredoo Myanmar

Ooredoo Myanmar’s revenue declined 17.5% YoY to USD 50.7 million (QAR 184.6 million) in Q1-2024 due to FOREX fluctuations. However, in local currency, the telco recorded 14% YoY revenue growth, driven by customer growth and increased B2C mobile voice and gaming revenue.

Dialog Axiata

Dialog Axiata revenue declined 13.8% YoY to USD 138 million (LKR 43.1 billion) in Q1 2024 impacted by a strategic shift away from low-margin business and reduced hobbling revenues. Other factors include:

- A 5% YoY decline in the overall mobile subscriber count to 17.2 million.

- A marginal 0.3% YoY decline to USD 1.2 (LKR372).

Cellcard

Cellcard revenue fell 6.4% YoY to USD 43.1 million (REILS 175.6 billion) in Q1 2024.

- Revenue from telecom services provisioning decreased 6.6% YoY to USD 41.8 million (REILS 170.1 billion).

- Connection and subscription revenue experienced a slight decline of 0.1% YoY to USD 0.9 million (REILS 3.8 billion).

Singtel

Singtel Group revenue decreased 4.0% YoY to USD 2.6 billion (SGD 3.5 billion) in Q1 2024 due to:

- Lack of contributions from Trustwave.

- Depreciation of the Australian Dollar (AUD).

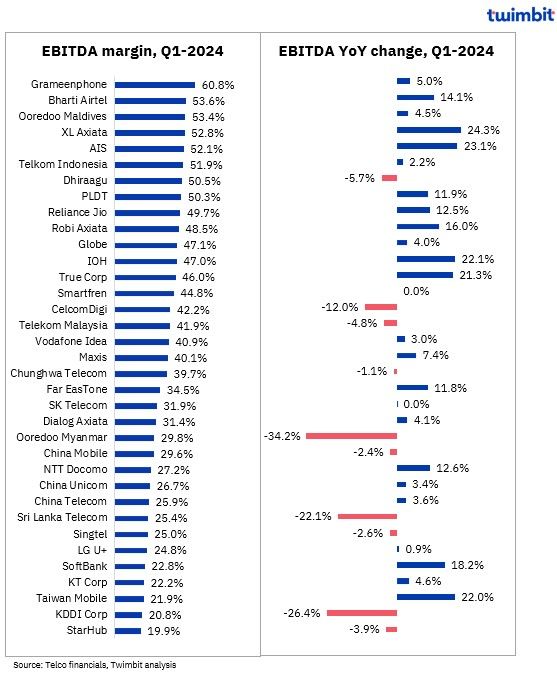

EBITDA analysis of APAC telcos: Q1-2024

Average EBITDA margin for APAC telcos stabilized at 38.1% in Q1-2024

A focus on cost control initiatives, improved operational efficiency, and top-line growth has resulted in robust EBITDA growth for most APAC telcos. In Q1 2024, nearly 72% of the analysed telcos reported positive EBITDA changes, while only ~9% experienced a slight decline (up to 3%).

Exhibit 2: EBITDA and EBITDA margin trends for APAC telcos, Q1 2024

Grameenphone

Grameenphone recorded the highest EBITDA margin at 60.8% with a 50-bps increase in Q1 2024 driven by top-line revenue growth and operational efficiency gains.

Grameenphone maintained its EBITDA growth rate for the 12th consecutive quarter despite rising inflation and macroeconomic challenges. EBITDA rose 5% YoY to USD 218.3 million (BDT23.9 billion) in Q1 2024.

Bharti Airtel

Bharti Airtel reported an EBITDA margin of 53.6% in Q1 2024. EBITDA increased 14.1% YoY to USD 1.8 billion (INR 152.9 billion), driven by higher revenue despite a rise in operating expenses.

Ooredoo Maldives

Ooredoo Maldives reported an EBITDA margin of 53.4% in Q1 2024. EBITDA increased 4.5% YoY to USD 19.2 million (QAR 69.9 million), driven by higher margin service revenue.

XL Axiata

XL Axiata reported a 24.3% YoY increase in EBITDA to USD 284.3 million (~IDR 4.5 trillion) in Q1 2024, driven by cost rationalization measures that reduced direct cost-of-sales and marketing expenses.

Higher contributions from data and digital services supported revenue growth, resulting in a 530 bps YoY increase in EBITDA margin to 52.8% in Q1 2024.

AIS

AIS reported a 23.1% YoY increase in EBITDA to USD 43.3 million (THB 27.7 billion) in Q1 2024, driven by revenue growth, improved sales margin, and cost efficiency.

The consolidation of core service revenue and the TTTBB boosted the EBITDA margin by 380bps YoY to 52.1% in Q1 2024.

Indosat Ooredoo Hutchinson (IOH)

IOH reported a 22.1% YoY increase in EBITDA to USD 415.5 million (IDR 6.5 trillion) in Q1 2024, driven by top-line growth and cost optimization initiatives. The EBITDA margin increased by 240bps YoY to 47% in Q1 2024.

Taiwan Mobile

Taiwan Mobile reported a 22% YoY increase in EBITDA to USD 337 million (TWD 10.6 billion) in Q1 2024, driven by the merger with T-Star.

Expanded scale, the realization of merger synergies, and EBITDA growth across operating segments (Telecom, momo, CATV) led to a ~180 bps increase in EBITDA margin to 21.9% in Q1 2024.

Ooredoo Myanmar

EBITDA for Ooredoo Myanmar declined by 34.2% YoY to USD 15.1 million (QAR 55.1 million) in Q1 2024 due to rising fuel costs. In local currency terms, EBITDA fell by 10% YoY, impacted by a negative FX movement.

Consequently, the EBITDA margin decreased by 760 bps YoY to 29.8% in Q1 2024.

Sri Lanka Telecom

Sri Lanka Telecom’s EBITDA declined 22.2% YoY to USD 21.8 million (LKR 6.8 billion) in Q1 2024 due to a 2% YoY decline in operating costs.

The EBITDA margin dropped from 33% in Q1 2023 to 25.4% in Q1 2024 due to:

- A 0.2% increase in sales and marketing costs.

- A 3.3% rise in administrative costs.

KDDI

KDDI’s EBITDA declined by 26.4% YoY to ~USD 2.1 billion (JPY 309.3 billion) in Q1 2024. Operating income decreased due to a 27.7% YoY increase in SG&A (Selling, General and Administrative) expenses, which rose to USD 3.2 billion (JPY 473.8 billion). Consequently, the EBITDA margin fell from 28.2% in Q1 2023 to 20.8% in Q1 2024.

CAPEX analysis of APAC telcos: Q1-2024

Average CAPEX intensity declined from 15.3% in Q1-2023 to 12.6% in Q1-2024, as 4G/5G network deployment of leading telcos reaches completion phase

Nearly 36% of the 28 telcos analysed reported YoY CAPEX growth in Q1 2024 compared to ~54% in Q1 2023.

The maturation of 4G and 5G network rollouts in major markets suggests CAPEX stabilisation or a potential decrease in the upcoming years.

Exhibit 3: CAPEX and CAPEX intensity trends for APAC telcos, Q1 2024

CelcomDigi

CAPEX nearly doubled growing 194% YoY in Q1 2024 to reach USD 67.3 million (MYR 318 million) driven by:

- Aggressive network integration and modernization initiatives.

- Expected to surpass the 50% completion mark in 7 states and complete the initiative in Penang by Q2 2024.

- 4G (LTE) coverage increased from 96.4% in Q1 2023 to 96.8% in Q1 2024.

- 4G Plus (LTE-A) coverage increased from 90.3% in Q1-2023 to 92.2% in Q1 2024.

CAPEX intensity rose from 3.4% in Q1-2023 to 10.1% in Q1 2024.

Robi Axiata

CAPEX increased 69.6% YoY in Q1 2024 to USD 33.4 million (BDT 3.7 billion) as the telco expanded its 4G network coverage.

- The overall count of 4G BTS increased 9.8% YoY to 17,394 in Q1 2024.

CAPEX intensity increased by 580 bps YoY to reach 14.6% in Q1 2024.

Ooredoo Myanmar

CAPEX grew 54% YoY to reach USD 2.2 million (QAR 8 million) in Q1 2024 due to project timings. Consequently, CAPEX intensity increased by 200 bps to 4.1% in Q1 2024.

SK Telecom

CAPEX increased 49.7% YoY to USD 238.5 million (KRW 317 billion) in Q1 2024 driven by continued focus on accelerating the execution of its AI Pyramid Strategy and data centre business with AI.

CAPEX intensity increased from 4.8% in Q1 2023 to 7.1% in Q1 2024.

XL Axiata

CAPEX increased 45.6% YoY to USD 131.3 million (IDR 2.1 trillion) in Q1 2024, driven by increased spending to expand the 4G coverage.

- The number of 4G BTS rose 14.3% YoY to 107,906 in Q1 2024.

CAPEX intensity increased by 570 bps to reach 24.7% in Q1 2024.

True Corp

CAPEX declined 79.7% YoY to USD 99.9 million (THB 3.6 billion), due to:

- Benefits realized from the merger between True and Dtac.

- Focus on network rollout from CAPEX acquired in the previous years.

CAPEX intensity plummeted from 34.1% in Q1 2023 to 6.9% in Q1 2024.

Ooredoo Maldives

CAPEX declined 64.1% YoY to USD 0.8 million (QAR 2.8 million), due to higher costs incurred last year for strategic projects like the Disaster Recovery site and Subsea Cable.

CAPEX intensity decreased by 430 bps YoY to 2.1% in Q1 2024.

Telekom Malaysia

CAPEX declined by 49.5% YoY to USD 43.2 million (MYR 204 million) in Q1 2024, due to:

- Access network element spending decreased from USD 61 million (MYR 288 million) in Q1 2023 to USD 17.6 million (MYR 83 million) in Q1 2024.

- Core network element spending declined 6.7% YoY to USD 14.8 million (MYR 70 million).

CAPEX intensity declined from 14.5% in Q1 2023 to 7.2% in Q1 2024.

Dialog Axiata

CAPEX declined 37.5% YoY to USD 10.5 million (LKR 3.3 billion). Consequently, CAPEX intensity decreased by 290 bps YoY to 7.6% in Q1 2024.

Telkom Indonesia

CAPEX declined 31.1% YoY to USD 325.5 million (IDR 5.1 trillion), reducing CAPEX intensity from 20.5% in Q1 2023 to 13.6% in Q1 2024.

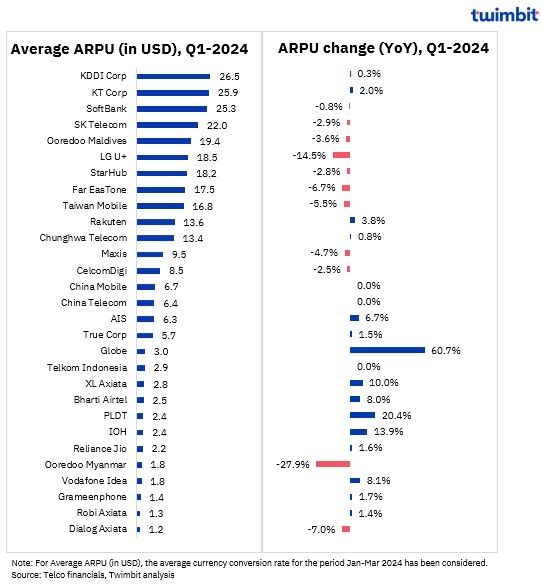

ARPU analysis of APAC telcos: Q1-2024

ARPU stabilizes with ~62% of telcos reporting YoY growth in Q1-2024

The ARPU analysis for the 29 telcos analysed is as follows:

- ~62% reported increased ARPU levels in Q1 2024.

- Nearly 28% reported higher YoY ARPU growth in Q1 2024 compared to Q1 2023.

- ~31% stabilized their ARPU levels in Q1 2024, with YoY changes ranging from -3% to 3%.

Exhibit 4: ARPU trends for APAC telcos, Q1 2024

Globe

The blended ARPU increased 60.7% YoY to USD 3 (PHP 167.1) in Q1 2024.

- Postpaid ARPU rose ~3% YoY to USD 15.6 (PHP 876).

- Globe Prepaid ARPU increased ~56% YoY to USD 2.7 (PHP 152).

- Prepaid ARPU for TM customers grew ~75% to USD 2.1 (PHP 115).

Increased smartphone usage and data-intensive applications increased the revenue contribution of mobile data to overall mobile service from ~80% in Q1 2023 to ~82% in Q1 2024.

PLDT

The blended ARPU increased by 20.4% YoY to USD 2.4 (PHP 167.1) in Q1 2024.

- Smart postpaid ARPU increased by 4.3% YoY to USD 12.6 (PHP 703) in Q1 2024.

- Smart prepaid ARPU increased by 18.7% YoY to USD 2.2 (PHP 125).

- Prepaid ARPU for TNT customers increased by 23.2% YoY to USD 1.9 (PHP 106).

IOH

The blended ARPU increased by 13.9% YoY to USD 2.4 (IDR 37500) in Q1 2024.

- Continued network expansion with 4G BTS up 20.8% YoY to ~184,000, led to increased data growth.

- Postpaid ARPU rose 25.5% YoY to USD 5.5 (IDR 85,900).

- Prepaid ARPU increased 13.9% YoY to USD 2.3 (IDR 36,500).

XL Axiata

The blended ARPU increased 10% YoY to USD 2.8 (IDR 44,000) in Q1 2024, driven by rationale pricing initiatives.

Research Methodology and Assumptions

- The “APAC telcos performance benchmarks: Spring 2024” report provides key findings regarding the performance of telcos for key financial metrics, including Revenue, EBITDA, CAPEX, and ARPU for January-March 2024.

- This report uses data from telecommunications companies and extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the January-December period.

- To ensure consistency and accurate comparisons, a constant currency conversion rate representing the average USD exchange rate for January-March 2024.

- The report offers a comprehensive assessment of Revenue and EBITDA for 38 and 35 telecommunication companies, respectively. Additionally, it includes CAPEX and ARPU analyses for 28 and 29 telcos, respectively.

- Blended mobile ARPU has been included where relevant for a more holistic view.

Click here for more contents on telecom

Recommended by Twimbit

Thailand telecom market updates – 2024 edition