Key Takeaways

- Annual revenue growth for APAC telcos moderated to 5.1% in FY-2023, reaching ~USD 588.7 billion. While this is lower than the approx 7% YoY growth in FY-2022, a positive note is that 88% of analysed telcos reported revenue growth, with four achieving double-digit increases.

- Revenue growth has primarily been across emerging markets (Bangladesh, India, Indonesia, Maldives), owing to increased data usage leading to ARPU uplift.

- ARPU levels across the region has been flat at ~USD 11 over the last 2 years. ARPU has been stagnant in developed markets with telcos inability to charge premium for 5G services has impeded the overall growth.

- Telcos are strategically shifting focus to the enterprise segment and non-connectivity revenue streams for growth. Enterprise revenue growth has outperformed the industry average growth rate for APAC telcos.

- Within the enterprise segment, cloud, analytics, managed services, and AI are key growth enablers. Additionally, telcos are offering financial services, content and media, and AR/VR, gaming offerings for incremental revenue from the consumer segment.

- Artificial Intelligence (AI) adoption surged in 2023, with leading players like SK Telecom, China Mobile, China Telecom, and Korea Telecom actively embracing the technology for enhanced operations.

- Average CAPEX intensity has declined in FY-2023, due to near completion of 5G network rollouts in major APAC markets. Only 47% of analysed telcos reported YoY Capex growth in FY-2023, compared to 59% in FY-2022.

- To improve profitability and efficiency, telcos are pursuing strategic cost rationalization and performance enhancement initiatives. The overall EBITDA margin remained stable at ~38% for 40 analysed telcos over the past two years.

- Telcos are shifting their focus to “beyond connectivity” offerings as a key driver of future revenue growth. Twimbit estimates this segment to account ~37.8% of overall revenue by 2027, signifying a strategic move beyond core services.

- Generative AI presents a significant opportunity to reignite growth. By leveraging AI, Telcos can enhance customer satisfaction, optimize operational costs, and generate entirely new revenue streams.

- Effectively managing network complexities necessitates digitalization of network management, to optimise performance and ensure efficient service delivery.

- Within the enterprise (B2B) segment, non-connectivity offerings are emerging as a critical growth strategy. By expanding their portfolio beyond core connectivity, telcos can cater to evolving enterprise needs with comprehensive solutions. Twimbit estimates enterprise segment to account for ~29% of overall telco revenue by FY-2027.

- 5G Fixed Wireless Access (FWA) offers a compelling solution to address last-mile connectivity challenges and monetize their existing 5G infrastructure. Twimbit estimates FWA connections in APAC region to exceed 200 million connections by FY-2027.

- Service personalization remains key for differentiation and revenue success. Data-driven insights and AI capabilities empower telcos to personalize offerings for each customer segment. This is gaining traction amongst leading teclos in the region.

Revenue analysis of APAC telcos: 2023

Average revenue growth for APAC telcos has slowed from ~7% in FY-2022 to 5.1% in FY-2023

Nearly 30% of the 42 telcos analysed recorded a higher YoY revenue growth rate in FY-2023 than in FY-2022. Despite the slowdown in YoY revenue growth rate, the 42 telcos generated a combined revenue of ~USD 588.7 billion, representing a YoY growth of ~USD 29 billion in FY-2023. Furthermore, 88% of the 42 telcos analysed reported positive revenue growth, with 4 telcos achieving double-digit growth.

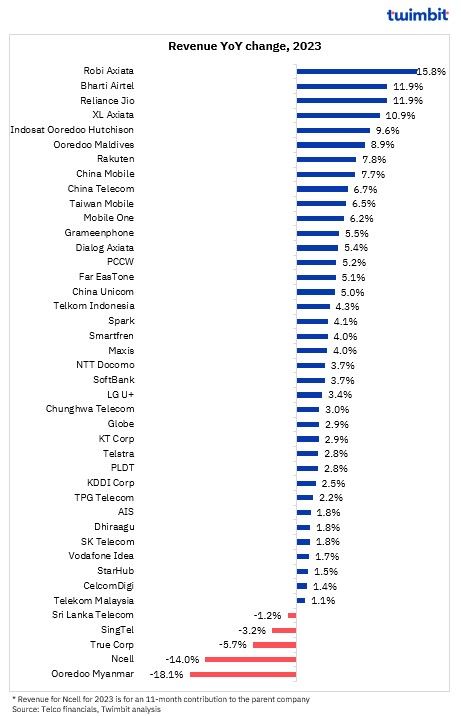

Exhibit 1: Revenue trends (% change) for APAC telcos (YoY basis), 2023

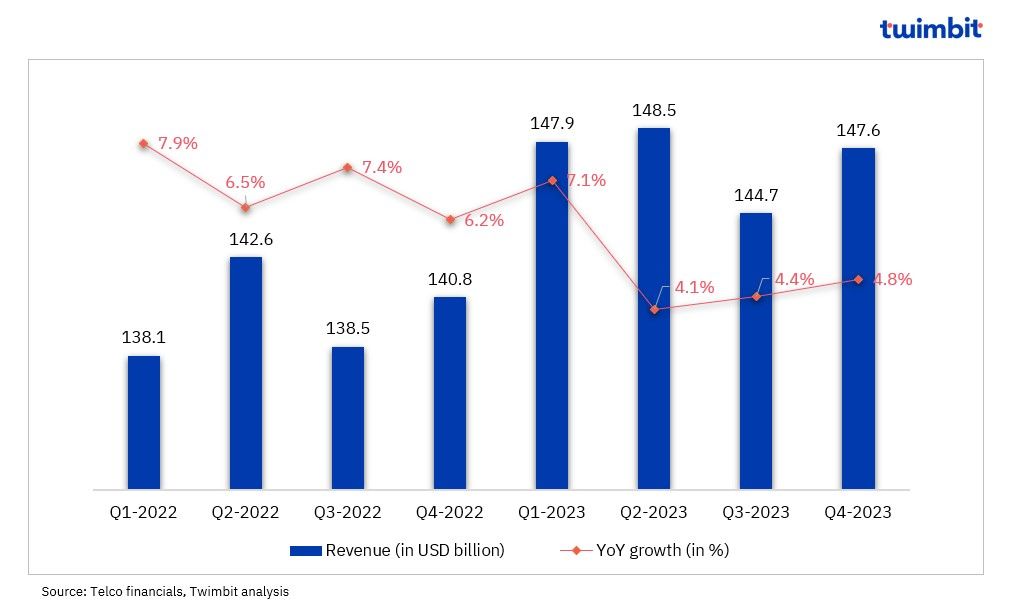

Exhibit 2: Revenue trends for APAC telcos, 2022-2023

Overall revenue grew by 5.1% YoY (lower than 7% YoY in FY-2022) to reach USD 588.7 billion in FY-2023. The ARPU level remains stagnant at ~USD 11, signifying the minimal impact of 5G offerings on revenue upliftment. The growth in overall revenue can be attributed to overall increase in subscriber count and improved adoption of non-connectivity services.

Robi Axiata

Robi Axiata achieved revenue growth of 15.8% YoY, reaching ~USD 920.3 million (BDT 99.4 billion) in FY-2023. This growth was primarily driven by robust subscriber growth and a significant ARPU increase.

- Subscriber count climbed 7.8% YoY to reach 58.7 million

- Blended ARPU witnessed an impressive 11.7% YoY growth to USD 1.3 (BDT 142)

- The proportion of data subscribers to the total subscriber base increased by 110 basis points to 76.2% in FY-2023

This surge in data usage resulted in a corresponding rise in data traffic, which grew by ~27% YoY to 3.3 billion GB. As a result, the data contribution to overall revenue climbed from 36.2% in FY-2022 to 46.1% in FY-2023.

Bharti Airtel

Bharti Airtel achieved revenue growth of 11.9% YoY, reaching ~USD 12.9 billion (INR 1,064.3 billion) in FY-2023. This growth reflected strong performance across all business segments.

- Mobile Services – 13.1% YoY revenue increase to ~USD 10 billion (INR 825.3 million), driven by a strategic focus on acquiring 4G/ 5G customers and uplifting ARPU levels

- Home Business – 24.2% YoY revenue increase, owing to 29.2% increase in the subscriber numbers, which reached ~7.3 million

- Digital Services – 3.3% YoY revenue increase with a ~1% rise in Digital TV customers during the same period to ~16.1 million

Additionally, Airtel Business revenue increased by 12.7% YoY. This increase was driven by growing revenue contribution from its converged portfolio offerings and data and core connectivity-related solutions.

Reliance Jio

Reliance Jio achieved revenue growth of 11.9% YoY, reaching USD ~12.8 billion (INR 1,061.5 billion) in FY-2023. An expanding subscriber base and ARPU improvements drove this growth.

- Reliance Jio reached a subscriber count of 470.9 million, with nearly 90 million being 5G subscribers

Strategic initiatives like JioBharat Phone and JioAirFiber were instrumental in attracting new subscribers and bolstering their digital services business revenue.

XL Axiata

XL Axiata achieved revenue growth of 10.9% YoY, reaching USD 2.1 billion (IDR 32.2 trillion) in FY-2023. This growth was driven by a sustained pricing environment and improved Data and Digital Services contribution.

- The uplift in ARPU levels from IDR 38,750 (USD 2.5) to IDR 41,400 (USD 2.7) contributed significantly to the overall revenue growth

- Data and 4G subscribers comprised 96% and 95% of their total subscriber base, respectively, which reached 57.5 million in FY-2023

Indosat Ooredoo Hutchinson (IOH)

IOH achieved revenue growth of 9.6% YoY, reaching USD 3.4 billion (IDR 51.2 trillion) in FY-2023, despite a decline of 3.4 million subscribers from FY-2022 to FY-2023.

- IOH recorded a total subscriber base of 98.8 million in FY-2023

- The focus on sustainable customer acquisition strategies and strategic price increases in new SIM cards enabled IOH to achieve higher overall revenue and ARPU growth

Furthermore, the growing adoption of 4G services led to increased data traffic, contributing incremental revenue per subscriber.

Ooredoo Myanmar

Ooredoo Myanmar reported a revenue decline of 18.1% YoY, reaching USD 233.6 million (QAR 850.2 million) in FY-2023. This decline was primarily caused by FOREX fluctuations and the country’s ongoing political instability.

However, a more positive perspective emerges when examining revenues in local currency. Ooredoo Myanmar recorded a commendable growth of ~3.9% YoY, driven by increased voice and fixed services revenue.

Ncell

Ncell reported a revenue decline of 14% YoY, reaching USD 259.1 million (NPR 34.2 billion) in FY-2023. This decline was primarily caused by the announcement of Axiata Group’s divestment away from Ncell. In response to the challenging business environment in Nepal, Axiata Group, the parent company of Ncell, has announced its intention to sell Ncell assets in November 2023. Axiata has also cited declining returns from Ncell as a contributing factor to the sale.

True Corp

True Corp reported a revenue decline of 5.7% YoY, reaching USD 5.8 billion (THB 202.9 billion) in FY-2023 due to a revenue decline in Product Sales (33.2% YoY) and Network Rentals (13.1% YoY).

While there was a minor incremental contribution from Interconnection revenue, it was not enough to offset these declines.

SingTel

SingTel also reported a revenue decline of 3.3% YoY, reaching USD 10.6 billion (SGD 14.3 billion) in FY-2023 due to:

- A revenue drop in their Optus (Australian) subsidiary and Singaporean operations

- The depreciation of the Australian Dollar (AUD)

- Intense competition in their core markets leading to ARPU pressure

- Weak corporate and consumer spending in Singapore

EBITDA analysis of APAC telcos: 2023

Average EBITDA margin for APAC telcos stabilised at 38.7% in FY-2023

The telcos’ intense focus on cost control measures and operational efficiency initiatives led to the stabilisation and healthy EBITDA growth for most APAC telcos. In FY-2023, almost 72% of the analysed telcos showed positive EBITDA changes, whereas only ~18% witnessed a marginal decline (up to 2%).

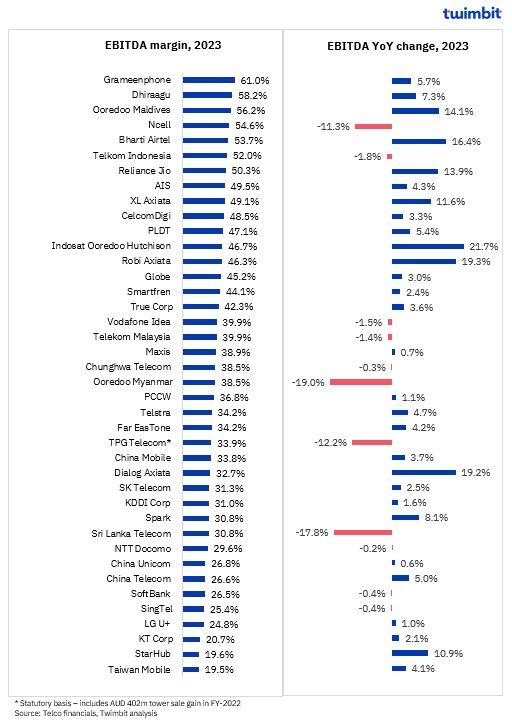

Exhibit 3: EBITDA and EBITDA margin trends for APAC telcos, 2023

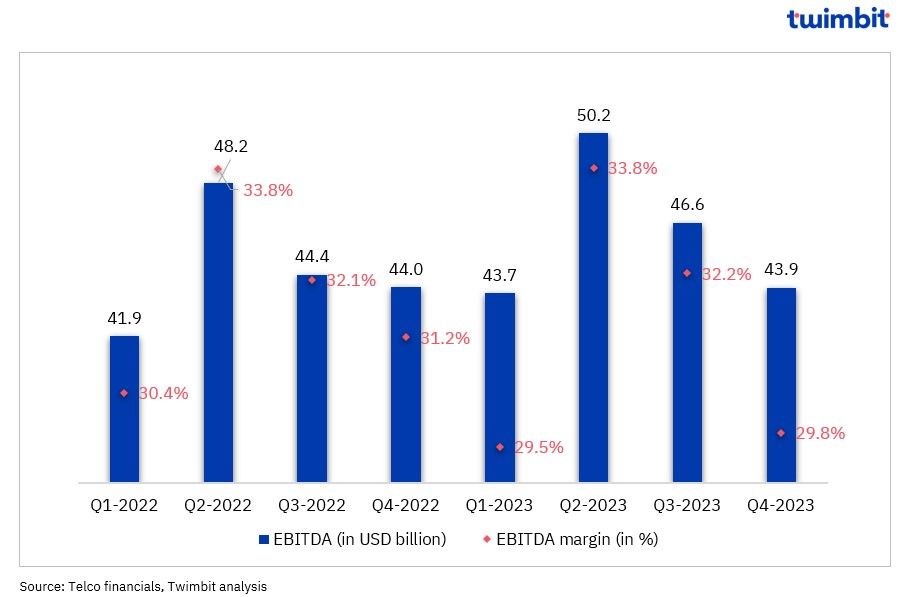

Exhibit 4: EBITDA trends for APAC telcos, 2022-2023

The overall EBITDA increased by 2.1% YoY to reach USD 184.4 billion in FY-2023, compared to 1.3% YoY in FY-2022. This signifies telcos’ impact on cost control measures.

- EBITDA margin reached 31.3% in FY-2023, as compared to 31.9% in FY-2022

The telcos are focusing on network optimisation and streamlining operations initiated by select telcos would further improve profit margins.

Grameenphone

Grameenphone maintained the highest EBITDA margin (61%) in FY-2023 despite a slight decrease of 30 basis points (bps) YoY, driven by a continued focus on:

- Driving top-line revenue growth

- Achieving operational efficiency improvements

Grameenphone also sustained its EBITDA growth trajectory for the 11th consecutive quarter, reaching USD 895.6 million (BDT 96.7 billion) in FY-2023. The telco’s ability to maintain strong growth demonstrates resilience amidst rising inflation and challenging macroeconomic conditions.

Dhiraagu

Dhiraagu’s EBITDA margin surged by 300 bps to reach 56.2% in FY-2023, signifying a remarkable turnaround. This impressive growth was fuelled by a 7.3% YoY increase in EBITDA, reaching USD 99.6 million (MVR 1.5 billion).

The strategic combination of top-line revenue growth and reduced operating costs was a key reason for this turnaround. This combination significantly contributed to the positive EBITDA and EBITDA margin expansion throughout the year.

Ooredoo Maldives

Ooredoo Maldives reported a substantial increase in EBITDA margin of 260 bps to reach 54.6% in FY-2023. This robust performance was further driven by a 14.1% YoY growth in EBITDA, reaching USD 76.4 million (QAR 278.2 million).

This growth can be attributed to both:

- Increase in overall revenue

- Successful cost-reduction strategy

This strategy involved implementing effective cost-control measures, including introducing and promoting digital offerings, to enhance operational efficiency.

Indosat Ooredoo Hutchinson (IOH)

IOH reported a significant increase in EBITDA growth of 21.7% YoY to ~USD 1.6 billion (IDR 24 trillion), driven by the telco’s commitment to:

- Cost optimisation initiatives

- Healthy overall revenue growth

This strategic approach translated to a notable increase in their EBITDA margin, which expanded from 42.1% in FY-2022 to 46.7% in FY-2023.

Robi Axiata

Robi Axiata achieved a 19.3% YoY growth in EBITDA during FY-2023, reaching approximately USD 425.7 million (BDT 46 billion). This success is attributed to their structured cost stewardship efforts.

These efforts resulted in margin expansion. Notably, their revenue growth rate outpaced the cost increase, leading to a 140 bps YoY increase in their EBITDA margin to 46.3% in FY-2023.

Dialog Axiata

Dialog Axiata’s EBITDA grew by 19.2% YoY in FY-2023, reaching USD 187.2 million (LKR 61.3 billion). A combination of factors drove this growth:

- Revenue growth

- Cost rescaling initiatives

- Subdued depreciation and amortisation (D&A) expenses due to controlled CAPEX spending

The combined effect of these strategies propelled their EBITDA margin to 32.7% in FY-2023, compared to 28.9% in FY-2022.

Bharti Airtel

Bharti Airtel reported an EBITDA growth of 16.1% in FY-2023, reaching USD 6.9 billion (INR 571.2 billion), owing to the cost efficiencies arising from its “War on Waste” program. Cost-rescaling initiatives include:

- Prioritising a ‘War on Waste’ program to streamline efficiencies and minimise environmental impact by eliminating waste across the organisation

- Deploying leading technologies to achieve this objective, which includes continuously evaluating and implementing solutions, leading to a reduction in operational waste

The combined effect of these strategies propelled their EBITDA margin from 51.6% in FY-2022, compared to 53.7% in FY-2023.

Ooredoo Myanmar

Ooredoo Myanmar’s EBITDA declined by 19% YoY, reaching USD 90 million (QAR 327.1 million). This decline is due to the challenging operating environment, which involved:

- Political instability

- Local currency depreciation and other factors

However, it is noteworthy that their EBITDA margin remained relatively stable at 38.5% in FY-2023. This stability can be attributed to the proportional decline in EBITDA and revenue.

Sri Lanka Telecom

Due to macroeconomic challenges, Sri Lanka Telecom’s EBITDA declined 17.8% YoY to USD 100 million (LKR 32.7 billion) in FY-2023. Other factors included the following:

- Increase in sales, marketing and administrative costs, which resulted in an overall cost increase, impacting the operating profit

- Decline in yearly revenue, which impacted the EBITDA growth

The impact of these factors also resulted in the EBITDA margin declining from 37.0% in FY-2022 to 30.8% in FY-2023.

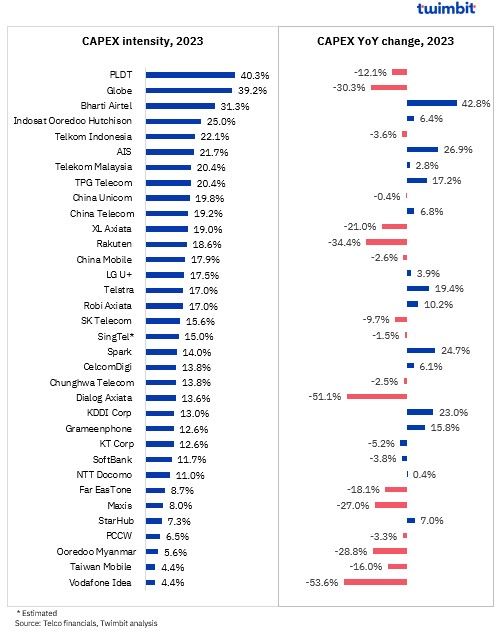

CAPEX analysis of APAC telcos: 2023

CAPEX intensity is ~17% for APAC, as telcos prune their network and infrastructure investments

Nearly 47% of the 34 telcos analysed reported YoY CAPEX growth in FY-2023 compared to ~59% in FY-2022.

The maturation of 4G and 5G network rollouts in major markets suggests that CAPEX is expected to stabilise or even decrease in the upcoming years.

Exhibit 5: CAPEX and CAPEX intensity trends for APAC telcos, 2023

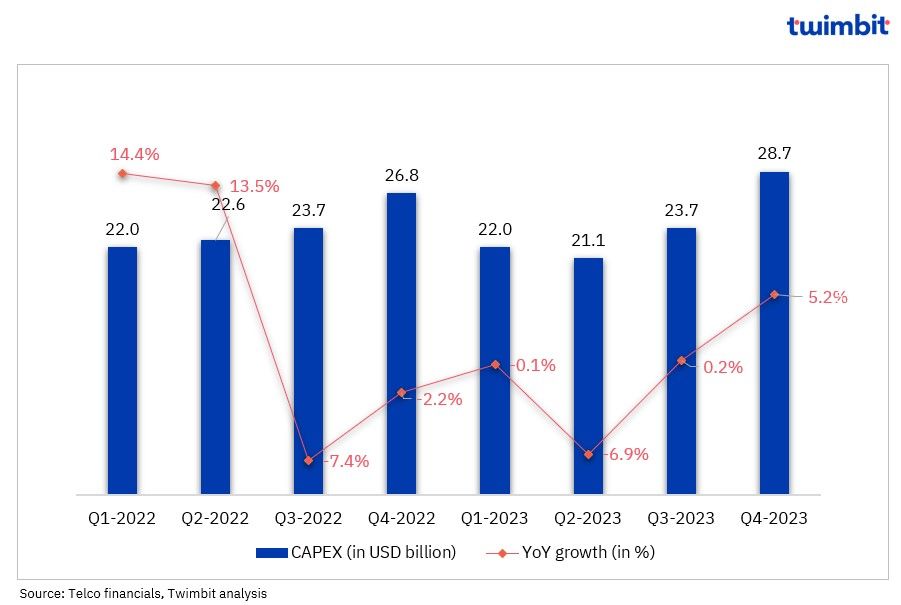

Exhibit 6: CAPEX trends for APAC telcos, 2022-2023

The overall CAPEX of the 34 APAC telcos registered a 0.1% YoY decline to ~USD 95 billion for FY-2023. This decline represents a significant deceleration compared to the 3.7% YoY growth observed in FY-2022.

Telco investments in 4G and 5G network deployments elevated CAPEX spending in Indonesia, Malaysia, the Philippines, Thailand, and China. Accelerated 5G rollouts in India and China further contributed to high CAPEX.

The overall CAPEX growth has declined in FY-2023. A significant decline was witnessed in Q2-2023, owing to a reduction in CAPEX from telcos like China Mobile, Rakuten, KDDI, Softbank, and Globe. Looking ahead, telcos’ CAPEX spending is expected to moderate in FY-2024, due to the completion of network deployments and upgrades across most of the countries. This shift reflects a strategic focus on monetising the significant investments made in recent years.

Bharti Airtel

Bharti Airtel reported a substantial CAPEX increase of 42.8% YoY to ~USD 4.0 billion (INR 333.4 billion) in FY-2023, representing 31.3% of their overall revenue. This growth reflects the telco’s commitment to expanding its 5G network and rolling out new 4G sites.

However, with the pan-India 5G network deployment nearing completion, the telco anticipates moderate CAPEX spending in the coming years. Notably, Bharti Airtel has also:

- Deployed ~45,000 towers in the last 12 months

- Ensured comprehensive connectivity across rural and urban areas

AIS

AIS reported a substantial CAPEX increase of 26.9% YoY to USD 1.2 billion (THB 41 billion in FY 2023), accounting for 21.7% of its overall revenue. Growth was primarily driven by its efforts to:

- Expand its 5G network

- Increase its overall 5G subscriber base

Looking ahead, AIS plans to moderate its CAPEX spending in FY-2024, targeting a range of USD 0.72 billion (THB 25 billion) – USD 0.75 billion (THB 26 billion). This strategic shift reflects their focus on optimising costs while strategically allocating resources. The planned CAPEX allocation will prioritise:

- Mobile network expansion (60%)

- Broadband expansion (28%)

- Enterprise and other areas (12%)

Spark

Spark’s CAPEX expenditure rose by 24.7% YoY to USD 338.4 billion (NZD 551 million) in FY-2023. This increase is primarily attributed to a rise in:

- Maintenance CAPEX incurred for cloud infrastructure, IT systems, fixed network

- International cable capacity upgrades

- Mobile network maintenance

Vodafone Idea (VI)

VI’s CAPEX declined by 53.5% YoY to USD 225.3 million (INR 18.6 billion) in FY-2023, as the telco continues to face revenue and subscriber challenges due to intense competition. Furthermore, the telco plans to launch 5G services within 6-7 months after securing funding.

This is followed with Vodafone Idea’s intention to finalise its 5G rollout strategy with technology partners. In short, the telco aims to capture 40% of its revenue from 5G services within the first 24-30 months of launch.

Dialog Axiata

Dialog Axiata’s CAPEX spending witnessed a significant decline of 51.1% YoY in FY-2023, reaching USD 78 million (LKR 25.5 billion).

This reduction stemmed from cost-rescaling initiatives and a strategic decrease in deploying new sites in 2023.

The telco achieved a 200-site increase in 4G base transceiver stations (BTS) in FY-2023 compared to 600 in FY-2022. Dialog Axiata also intends to acquire Airtel Lanka’s network and spectrum to reduce its CAPEX requirements further.

Rakuten

Rakuten’s CAPEX expenditure declined 34.4% YoY to USD 2.7 billion (JPY 385.9 billion) in FY-2023. This decrease was observed across all three of their reporting segments (Internet services, FinTech, and Mobile). The mobile segment reported a 43.1% YoY drop in CAPEX spending to USD 1.7 billion (JPY 238.5 million) in FY-2023.

Building upon this trend, Rakuten plans to reduce its mobile segment CAPEX in FY-2024 to below USD 713.5 million (JPY 100 billion).

Globe

Globe’s capital expenditure contracted 30.3% YoY to USD 1.3 billion (PHP 70.6 billion) in FY-2023. This reduction reflects their focus on streamlining spending, particularly within the Data and Core network segments. As a result, Globe’s CAPEX intensity significantly declined from 57.9% in FY-2022 to 39.2% in FY-2023.

Ooredoo Myanmar

Ooredoo Myanmar adopted a controlled spending approach in FY-2023, resulting in a 28.8% YoY decline in CAPEX to USD 13.1 million (QAR 47.9 million). This strategic cost management translated to a substantial decrease in their CAPEX intensity, dropping by 90 basis points YoY to 5.6% in FY-2023.

Maxis

Maxis strategically reduced its overall CAPEX expenditure by 27% YoY to USD 178.5 million (MYR 813.0 million) in FY-2023. This decline was achieved through a combination of selective investments in IT digitisation initiatives and targeted spending to support network capacity growth and fibre build-out initiatives.

Consequently, their CAPEX intensity also improved, declining from 11.4% in FY-2022 to ~8% in FY-2023.

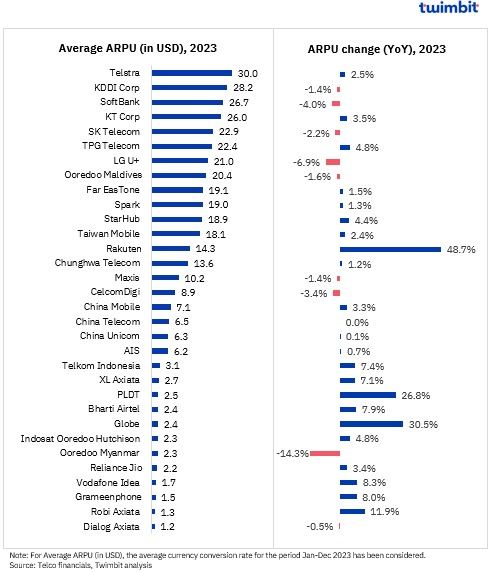

ARPU analysis of APAC telcos: 2023

ARPU level stabilises with ~72% of APAC telcos reporting growth in FY-2023

The ARPU analysis for the 32 telcos analysed are as follows:

- ~72% reported increased ARPU levels in FY-2023

- 47% reported higher YoY ARPU growth rates in FY-2023 than in FY-2022

- ~41% stabilised their ARPU levels in FY-2023, with YoY changes ranging from -3% to 3%

Exhibit 7: ARPU trends for APAC telcos, 2023

Below are the key highlights re ARPU growth in select markets:

- The Philippines: Outpaced the ARPU growth rate of other APAC telcos driven by increased data consumption and adoption of 5G

- Japan: Witnessed positive YoY ARPU growth, highlighting the impact of tariff reductions and regulatory interventions on ARPU levels

- India: Maintained ARPU growth at a moderate pace, driven by tariff adjustments

The stagnant ARPU across the 32 APAC telecom operators indicates that current 5G offerings and mobile service monetisation strategies have yet to help drive ARPU growth.

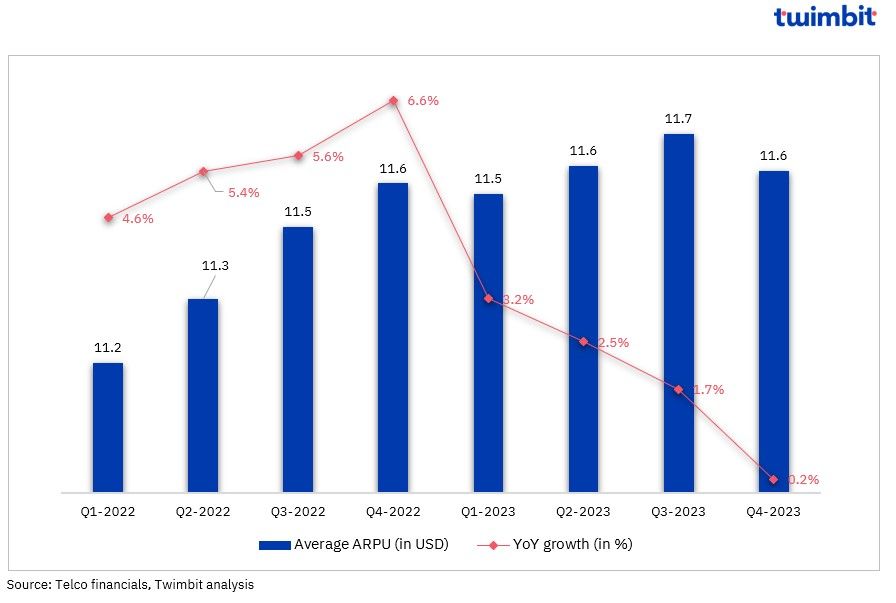

Exhibit 8: ARPU trends for APAC telcos, 2022-2023

Rakuten

Its strategic implementation of the SAIKYO Plan in June 2023 has yielded positive results, which include:

- Recording impressive ARPU growth of 48.7% YoY in FY-2023, reaching approximately USD 14.3 (JPY 2,000)

- Reducing churn rate from 1.93% in June-2023 to 1.13% in FY-2023

- Expanding Rakuten’s extensive 4G network coverage to reach 99.9% of the population in FY-2023, contributing significantly to its ARPU rise

Rakuten has seen improved customer satisfaction as a result of these initiatives.

Globe

Globe’s focus on nurturing good quality existing subscriber base is reflected in their 30.5% YoY increase in average ARPU to USD 2.4 (PHP 133.1) in FY-2023. As part of this strategic approach, Globe:

- Deactivated nearly 30 million SIM cards, primarily targeting inactive users

- Experienced ARPU growth in its postpaid, prepaid and TM segments by 2%, 24% and 34%, respectively

PLDT

PLDT’s average ARPU for FY-2023 reached USD 2.5 (PHP 138.6), representing a commendable YoY growth of 26.8%. This growth is primarily attributed to 2 key factors:

- Average mobile data usage per subscriber rose by ~19% YoY in FY-2023, reaching 11.0 GB

- Significant increase in 5G unique connected devices, reaching 5.2 million in December 2023, compared to ~3.1 million a year ago

Furthermore, growth in overall ARPU levels from Smart Postpaid subscribers also contributed to the positive trend.

Robi Axiata

Robi Axiata’s overall average ARPU increased by 11.9% YoY in FY-2023 to reach USD 1.3 (BDT 142). This growth in ARPU was achieved despite a 2.8% decline in postpaid ARPU due to the following:

- Robust 12.8% increase in prepaid APRU, which offset the decline in postpaid ARPU

- Notable rise in average data usage per subscriber, which increased by 19.1% YoY in FY-2023 to ~6.4 GB per month

Key suggestions and recommendations

1. “Beyond Connectivity” to take centre stage as telcos seek revenue diversification

Telecom operators are unlocking new value streams by strategically expanding to drive growth beyond core connectivity services. Traditionally reliant on connectivity offerings, telcos are increasingly shifting focus towards non-connectivity revenue streams, including financial services, content and media, mobile applications, extended reality (XR) content, and secure remote education solutions.

- China Mobile: The telco strengthened its MIGU Video platform and ventured into VR/AR cloud gaming and the metaverse. The digital content business revenue increased significantly 31.6% YoY to ~USD 4 billion (CNY 28 billion) in FY-2023, with cloud gaming across platforms reaching 120 million monthly active users.

- China Telecom: Capitalizing on its strong mobile subscriber base (408 million in FY-2023), China Telecom experienced a 12.4% YoY increase in mobile value-added services and application revenue, reaching USD 3.6 billion in FY-2023 (CNY 25.8 billion).

- AIS: The telco aims to transform into a “Cognitive Tech-Co” by focusing on video platforms, mobile money solutions, and digital marketplaces.

- TrueCorp: Through its subsidiaries, TrueCorp is expanding its enterprise presence by offering professional digital solutions and smart energy services.

For maximized success, telcos require a strategic selection of growth avenues which capitalize on their distinctive advantages and contribute value to the broader ecosystem. Twimbit estimates “Beyond Connectivity” revenue to reach 37.8% of total telco revenue by 2027, up from 26.9% in FY-2023, underlining the growing importance of this strategic shift.

2. Telcos to strategically adopt Generative AI to boost growth and efficiency

Telcos have been at the forefront in the adoption of Artificial Intelligence (AI) technologies. This strategic shift, characterized by a move from pilot projects to full-scale deployments, is driven by the potential of AI to unlock growth opportunities and enhance operational efficiency. This trend aligns with a broader movement of companies establishing ambitious visions for an AI-powered future.

Asian telecom operators are at the forefront of this transformation. Leading players such as SK Telecom, China Mobile, China Telecom, and Korea Telecom (KT) are actively embracing AI.

- SK Telecom: Its “AI Pyramid” strategy exemplifies this commitment, with 12% of investments towards AI. This investment is expected to triple to 33% by 2028. (to be tripled by 2028) to capture emerging AI opportunities.

- China Mobile: By applying AI to the 10,000 potential parameters associated with each antenna (including coverage attributes and historical traffic volumes), it has achieved a significant improvement in network performance, with a 13% increase in outdoor downlink speeds and a 30% boost in indoor speeds.

- China Telecom: Adopts a broader approach and utilising AI for various industry applications beyond core network optimisation. This includes applications in urban management, emergency monitoring, and smart manufacturing. Notably, China Telecom has released Xingchen, an open-sourced 100 billion-parameter large language model (LLM), which is being deployed internally for software development, network analysis, and business applications.

- KT Corp: Its AI initiative ventures in robotics, logistics, and contact centres have already yielded substantial returns (revenue of over USD 600 million). It plans to further invest USD 5.4 billion by 2027 to enhance its AI competitiveness.

Across various functions, generative AI offers a compelling value proposition:

- Customer Service: Improved experiences, increased agent productivity, and fully digital interactions

- Marketing & Sales: Hyper-personalized offerings, deeper customer understanding, and faster content creation

- Network Operations: Optimized configurations, enhanced labour efficiency, social media insights for customer understanding, and improved network planning through unstructured data analysis

- Information Technology (IT): Accelerated software development and migration, reduced technical debt, and unlocking previously resource-constrained capabilities

- Support Functions: Streamlined back-office operations and improved employee productivity

While Gen-AI presents exciting possibilities, it remains a nascent technology with challenges. Hence, telcos must be prepared to invest in development and implementation, ensuring responsible and ethical use of this powerful tool.

3. Telcos should digitalise their network management capabilities to manage evolving complexities

The APAC telecommunications landscape is experiencing a growing level of complexity driven by the rapid deployment of fibre, 4G LTE, and 5G technologies. While these advancements foster innovation, they also introduce challenges for network operators, including network sprawl management, compatibility issues across diverse services, and resource optimization difficulties.

In this evolving environment, standardized network approaches are becoming increasingly less feasible. To thrive, APAC telcos must adopt a two-pronged strategy: maximizing the value of existing network infrastructure while simultaneously pioneering the development of new services. This necessitates a comprehensive digital core transformation that leverages cloud computing, AI optimization, big data analytics, and robust cybersecurity measures

Leading telecommunications companies are already demonstrating the effectiveness of this approach. China Telecom, for example, has strategically shifted its resource allocation following significant investments in 5G infrastructure. This shift involves building GenAI, an AI platform designed to analyze diverse data sets and facilitate more effective network issue diagnosis. Similarly, Telstra is utilizing AI to automate fault detection and resolution processes, leading to improved customer service experiences.

Effectively managing network complexity is a critical strategic imperative for APAC telcos. Embracing digital transformation is essential for navigating this dynamic technological landscape and ensuring long-term success.

4. Enterprise non-connectivity offerings set to emerge as strategic revenue growth imperative

As the industry matures beyond basic digital adoption, B2B services will emerge as a vital differentiator to sustainable revenue streams. This transition necessitates an ideology shift from connectivity provider to technology solution provider. Telcos can achieve this evolution through internal innovation or strategic partnerships. Strategic acquisitions to bolster offerings can also be not dommed out. Partnerships foster robust ecosystems by integrating diverse service portfolios.

The development of B2B portfolios tailored to enterprise needs is crucial. This includes digitalising enabler offerings like cloud computing, cybersecurity solutions, data analytics, and AI.

Telcos such as China Mobile and China Telecom exemplifies the success of the strategy to gain ground in the enterprise business.

- China Mobile: Continue to focus on integrated development of its DICT (data, information and communications technology) capabilities. The DICT business segment revenue increased 14.2% YoY in FY-2023 to reach USD 27.2 billion (CNY 192.1 billion), with its corporate customer base increasing by ~5.2 million to reach 28.4 million

- China Telecom: Industrial Digitalisation offerings revenue increased by 11.8% YoY to reach USD 19.7 billion (CNY 138.9 billion) and its 5G networks covered more than 2,700 factories. It also continues to build up its capabilities for Intelligence Cloud to offer full-stack public cloud and hybrid cloud. Intelligent cloud revenue increased 67.9% YoY in FY-2023 to reach USD 13.8 billion (CNY 97.2 billion).

Twimbit estimates the enterprise segment’s contribution to telco revenue will reach a staggering 29.2% by FY-2027, compared to an estimated 23.1% for FY-2023.

5. Fixed wireless access (FWA) provides an opportunity for telcos to monetise their 5G network

Monetizing 5G offerings remains a challenge for telcos, due to a lack of compelling use cases. Enterprises are yet to be fully convinced of the promised efficiency and productivity gains associated with 5G services, while consumers primarily perceive the technology as offering faster data speeds. Consequently, 5G adoption rates across most countries have fallen short of initial expectations.

To address this challenge, telcos require a strategic shift in their business approach. This shift can encompass several key areas:

- Beyond Last-Mile Connectivity: Leveraging 5G’s capabilities to provide an alternative to fixed broadband, offering a solution for overcoming last-mile connectivity hurdles and unlocking new revenue streams.

- Collaboration with Content Partners: Partnering with digital content and media companies to develop and scale the adoption of revenue-generating applications specifically designed for 5G capabilities.

- Comprehensive Enterprise Solutions: Streamlining operations by offering comprehensive solutions to support enterprises throughout the deployment and post-deployment phases of 5G adoption.

Fixed Wireless Access (FWA) powered by 5G presents a promising solution in this context. By addressing last-mile connectivity challenges, FWA can open doors for additional revenue streams beyond traditional mobile services.

However, the true potential of 5G lies in its synergistic relationship with cloud computing, Internet of Things (IoT), and automation. This combination has the power to unlock transformative use cases across smart cities, Industry 4.0, and advanced IoT applications.

Looking ahead, the future of 5G FWA remains promising, with few of the South-east and South Asian countries like Philippines, Thailand and India already taking a lead in deployment of FWA technology. Twimbit estimates that FWA connections to grow by four-folds to exceed 200 million subscriptions by 2027. As the technology matures, consumer demand expands, and innovative use cases emerge, telcos will gradually see a return on their investments.

6. Telcos should alleviate focus on customer experience as a key success differentiator

Today, a superior customer experience (CX) is paramount for subscriber retention and acquisition. This encompasses personalised offerings, seamless omnichannel engagement, and proactive customer support. While technology remains the engine driving telco advancements, CX variables are still recognised as critical success factors. Telcos exemplify this by leveraging AI to elevate CX.

- China Mobile: Partnered to gain an understanding of customers through chatbot and speech analytics solutions from Fano Labs’ Accobot. The solution automatically responds to general inquiries and convert telephone recordings into text, effectively reducing the workload of frontline staff by ~25%

- Bharti Airtel: Developed its AI solution with NVIDIA to enhance the experience for all inbound calls

Research Methodology and Assumptions

- This report leverages data acquired from telecommunications companies and extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where Q1 signifies the January-March period.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate has been applied throughout the report. This rate represents the average USD exchange rate for the entire calendar year 2023 (January-December 2023).

- The report presents a comprehensive assessment of Revenue and EBITDA for 42 and 40 telecommunication companies, respectively. Additionally, CAPEX and ARPU analyses encompass data from 34 and 32 telcos, respectively.

- Blended mobile ARPU has been incorporated wherever relevant for a more holistic view.

Click here for more contents on telecom

Recommended by Twimbit

Thailand telecom market updates – 2024 edition