Trending APAC telcos performance insights

- AI becomes pervasive for innovation across APAC telcos: APAC telcos are strategically investing in AI to enhance network efficiency, improve customer service, and create new revenue streams.

- South Korean telcos lead AI adoption in the region. SK Telecom aims to become an ‘AI hub’ in the Asia-Pacific and is targeting AI revenue of USD 1.8 billion by 2028. KT Corp, in partnership with Microsoft, aims to invest USD 1.8 billion (KRW 2.4 trillion) in AI, cloud, and infrastructure sectors, over the next five years. Through this partnership it aims to enhance its AI transformation business revenue from ~ KRW 269 billion in 2025 to ~KRW 1.4 trillion by 2029. LGUplus also plans to invest USD 2.1 billion (KRW 3 trillion) over the next four years to transform into an AI-driven company aiming to target USD 1.4 billion (KRW 2 trillion) in annual revenue by 2028.

- Other telcos such as Telstra, NTT Docomo, Globe Telecom, KDDI, IOH leverage AI for enhancing their telecom operations for use cases like network optimisation, IoT, energy efficiency, spam and fraud detection.

- Enterprise and beyond-connectivity services remain key revenue growth drivers: As enterprises increasingly rely on technology; by investing in data analytics, cybersecurity, and digital transformation capabilities, telcos are well-positioned to meet the rising demand for advanced ICT and AI solutions, becoming essential partners in their customers’ digital transformation journeys.

- Singtel, IOH, and SK Telecom are leveraging AI-powered cloud services to streamline processes and drive digital transformation. In China, digital transformation services continue to drive enterprise revenue for telcos, while financial services have fuelled SoftBank’s revenue growth in Japan.

- Twimbit estimates that the enterprise and beyond-connectivity segments will contribute approximately 30% and 40% to overall revenue, respectively, by 2028.

- Emerging countries to fuel 5G subscriber growth: While South Korea, China, and Japan have been leaders in 5G adoption, the ongoing rollout of 5G networks in other regional markets will further drive adoption.

- In the second wave of 5G deployments, particularly in India and Thailand, rapid expansion of network infrastructure has led to swift adoption rates. Network rollouts in countries such as Indonesia, Malaysia, Uzbekistan, Laos, Vietnam, and Myanmar will contribute to future 5G subscriber growth.

- Twimbit estimates 5G penetration in developed markets like Australia, South Korea, Japan, China, and Singapore to surpass 70% by 2028, with 5G subscribers in the region expected to grow from ~1.8 billion in 2024 to ~2.7 billion by 2028.

- Leadership transitions and strategic realignments signals adaptation to evolving digital priorities: Leadership changes and strategic shifts amongst telcos signal a proactive move to align with evolving digital priorities, future growth areas, and emerging technologies.

- Korean telcos are restructuring to prioritize AI and cloud services. For example, KT announced a restructuring in 2025, which includes the creation of two new subsidiaries, KT OSP (field operations and network management) and KT P&M (customer service), to focus on AI and cloud. SK Telecom is also undergoing a major restructuring in 2025, dividing it into seven business divisions to concentrate on two core areas: AI and communications.

- Globe Telecom has appointed Carl Raymond Cruz as CEO, with Juan Carlo Puno as CFO and Darius Delgado as CCO, to strengthen leadership for digital growth. LG U+ has appointed Hong Bum-shik as CEO to lead its AI-driven transformation.

- GSMA Open Gateway initiative to drive Network APIs adoption: GSMA Open Gateway provides consistent, interoperable APIs via the CAMARA repository, enabling seamless digital service integration across networks.

- In South Korea, SK Telecom, KT, and LG Uplus are at the forefront of network API adoption, supported by GSMA’s Open Gateway and Bridge Alliance. Additionally, APAC telcos Bharti Airtel, Reliance Jio, and Singtel have joined a global initiative to advance network APIs. Further, Bridge Alliance’s API Exchange (BAEx), backed by 13 Asia-Pacific operators, simplifies API deployment, fostering regional digital innovation. Operators like AIS, Maxis, and Singtel are creating regional API exchanges for network-based authentication.

- M&As continue to redefine the APAC telecom landscape: Telecom industry consolidation is accelerating as companies seek to improve economies of scale, enhance service portfolios, and boost operational efficiency to remain competitive in a digital-first environment.

- Telstra announced the acquisition of Boost Mobile to gain access to customers seeking more affordable mobile connectivity. MobileOne (M1) acquired a 70% stake in ADG to expand in Vietnam’s tech sector. The recent merger of XL Axiata and Smartfren Telecom into XLSmart Telecom creating a combined entity with an enterprise value of USD 6.5 billion further consolidates Indonesia’s mobile operator industry to three players.

Revenue analysis of APAC telcos: FY-2024

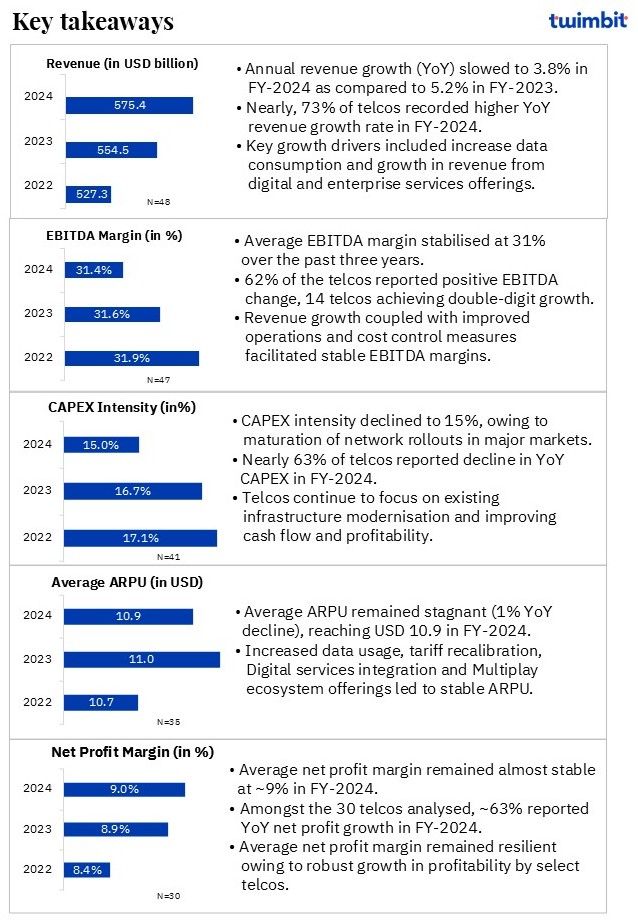

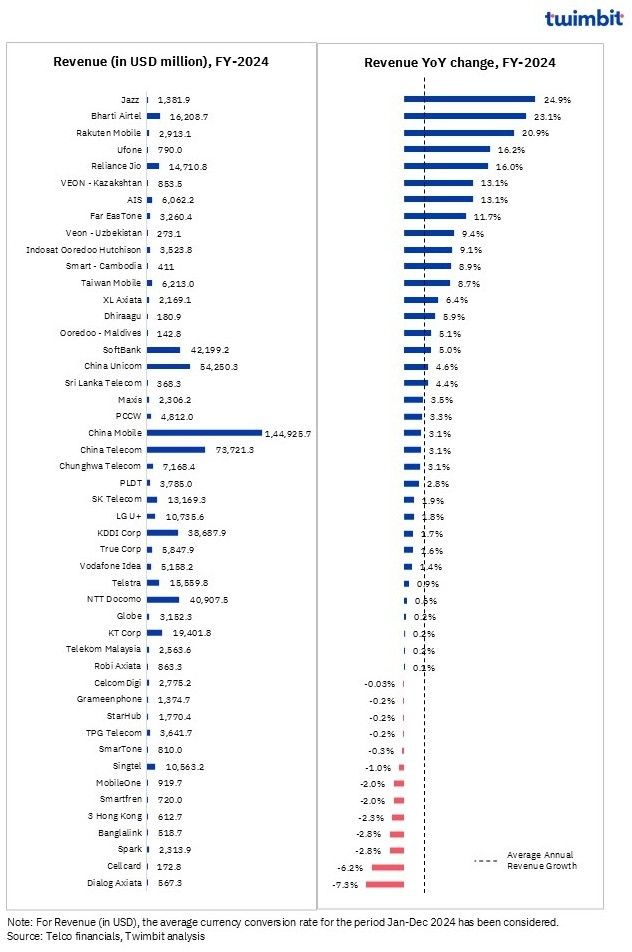

Average annual revenue growth for APAC telcos slowed from ~5.2% in FY-2023 to 3.8% in FY-2024

Approximately 73% of telcos achieved YoY revenue growth in FY-2024 (as compared to ~85% in FY-2023). The combined revenue of the 48 analysed telcos increased by ~USD 21 billion to ~USD 575.4 billion in FY-2024, with 8 telcos (around 17% of the total) of the total telcos exhibiting double-digit growth.

Exhibit 1: Revenue trends for APAC telcos, FY-2024

Key highlights

The Asia-Pacific telecom sector has seen varied revenue outcomes, driven by subscriber growth, tariff adjustments, digital service expansion, alongwith operational and macroeconomic challenges.

- Bharti Airtel: Revenue increased 23.1% YoY to USD 16.2 billion (INR 13.6 trillion) in FY-2024, supported by overall subscriber growth (including strong growth in postpaid subscribers), data monetization, Indus Towers consolidation and tariff optimization resulting in incremental ARPU. Data usage per customer surged to 24.5 GB/month.

- Reliance Jio: Revenue grew 16% YoY in FY-2024 to USD 14.7 billion (INR 1.2 trillion), driven by sustained tariff hikes and an improved subscriber mix. The rise in data consumption, with 5G subscribers reaching 170 million and data usage soaring to 32.3 GB per user per month, facilitated this growth.

- XL Axiata: Revenue grew 6.4% YoY to USD 2.2 billion (IDR 34.4 trillion), driven by 5.6% increase in subscriber count coupled with increased data consumption, leading to a higher blended ARPU.

- Ooredoo Maldives: With 5G now covering 60% of the population, the operator experienced consistent growth in both prepaid and postpaid subscriptions, contributing positively to mobile ARPU. This translates into 5.1% YoY revenue growth for FY-2024 to USD 142.8 million (QAR 520.2 million).

- Vodafone Idea: The telco experienced revenue growth of 1.4% YoY in FY-2024 through price increases. The recent launch of 5G services by the telco is like to have a positive impact on the revenue in the FY-2025.

- Digital and Enterprise services: The shift towards digital and enterprise services marked another significant theme, with telcos diversifying their offerings to capture new revenue streams.

- Jazz: Revenue surged by 24.9% YoY in FY-2024 to USD 1.4 billion (PKR 384.9 billion) led by a rise in 4G subscribers and a 77.5% increase in direct digital revenue, with JazzCash and Mobilink Microfinance Bank growing by 115.5% and 32.3%, respectively on YoY basis in Q4-2024.

- VEON – Kazakhstan: Revenue grew 13.1% YoY to USD 853.5 million (KZT 399.9 billion) in FY-2024, facilitated by 25.5% growth in digital revenue, supported by increased 4G penetration and rising adoption of its digital platforms across the subscriber base during the period.

- Rakuten Mobile: Revenue grew 20.9% YoY to USD 2.9 billion (JPY 440.7 billion), led by growth in the number of subscribers and an increase in ARPU in mobility segment as well as growth in Rakuten Symphony segment.

- SoftBank: SoftBank’s revenue increased 5% YoY in FY-2024 to USD 42.2 billion (JPY 6.4 trillion), facilitated by 16% growth in the enterprise segment led by business solutions offerings, signalling strong B2B demand.

- KDDI: Revenue grew 1.7% YoY in FY-2024 to USD 38.7 billion (JPY 5.9 trillion) with enterprise segment being a key revenue growth driver. Enterprise revenue increased 14.3% YoY in FY-2024, contributing 19.3% to total revenue, as compared to 17.2% in FY-2023.

- NTT Docomo: While mobile revenues declined due to legacy pressures, growth in Smart Life division helped sustain user engagement and offset top-line pressures, thereby facilitating 0.6% YoY growth in revenue for FY-2024.

- Chinese telcos have faced slowing revenue growth over the past three years due to challenges in monetizing 5G amid intense competition. However, they have sustained growth by focusing on enterprise and digital services, including smart cities, data centre, cloud, and AI. In FY-2024, China Unicom’s Computing and Digital Smart Applications (CDSA) saw a 9.6% YoY increase, whereas China Mobile’s Business Market segment grew 8.8% YoY. Industrial Digitalization revenue rose 5.5% YoY for China Telecom.

- Fixed Broadband and Converged Offerings: Fixed broadband and bundled service offerings have become a reliable revenue driver, especially in mature mobile markets where operators are extending into households and SMEs with converged connectivity solutions.

- AIS: Revenue grew 13.1% YoY to ~USD 6.1 billion (THB 213.7 billion), led by merger synergies. Fixed broadband revenue more than doubled (+116% YoY) following the integration of TTTBB; ARPU growth and customer acquisition also contributed to segment profitability.

- Far EasTone: Revenue grew 11.7% YoY to ~USD 3.3 billion (TWD 104. 6 billion) in FY-2024, as it continued to scale its ICT portfolio post-merger, enabling stronger bundling of enterprise and residential offerings, including 5G home broadband and cloud-enabled services.

- Taiwan Mobile: Reported record-high revenues in FY-2024, driven by the T Star merger and execution of its Telco+Tech strategy, which integrates mobile, fixed broadband, and digital services. Revenue grew 8.7% YoY to USD 6.2 billion (TWD 199.4 billion) in FY-2024.

- True Corp: Service revenue growth of 4.5% on YoY basis in FY-2024 lifted overall top-line growth to 1.6% on YoY basis to USD 5.8 billion (THB 206 billion), as the merged entity benefited from convergence between mobile, broadband, and pay-TV platforms.

- Macroeconomic and operational challenges: Several operators faced revenue pressure stemming from external factors (ranging from inflation, weak GDP growth to political instability and adverse weather) and increase in competition intensity.

- Dialog Axiata: Revenue dropped 7.3% YoY to USD 567.3 million (LKR 171.2 billion) in FY-2024, as the operator exited from low-margin hubbing and international voice segments in response to market inefficiencies.

- Cellcard: Revenue declined 6.2% YoY to USD 172.8 million (REILS 710 billion), owing to decline in telecom provisioning and subscription revenues, as macroeconomic conditions remained soft and subscriber churn increased owing to increased competition.

- Banglalink: Revenue trajectory weakened in the second half of FY-2024, largely due to political unrest and a deteriorating economic environment that dampened consumer spending. As a result, revenue declined 2.8% YoY basis in FY-2024 to USD 518.7 million (BDT59.8 billion).

- Spark: Revenue declined 2.8% on YoY basis to USD 2.3 billion (NZD 3.8 billion), as the telco experienced a decline in mobile and IT service revenues, highlighting saturation in the consumer base and reduced enterprise IT spending amidst cost pressures.

- StarHub: Decline in revenue from Mobile, Entertainment and Equipment sales revenue offset the growth in Enterprise segment, impacting the overall revenue, which declined by 0.2% on YoY basis to ~USD 1.8 billion (SGD 2.4 billion).

- Grameenphone: Revenue remained almost flat (0.2 decline) on YoY basis at USD 1.4 billion (BDT 158.4 billion) in FY-2024, amid elevated inflation, a weakening macroeconomic outlook, political unrest and increased cost pressures in Bangladesh’s telecom sector.

- Robi Axiata: Revenue remained flat in FY24 (0.1% growth) on YoY basis at USD 863.3 million (BDT 99.5 billion), reflecting the combined impact of socio-political disruptions, frequent flooding, and cautious consumer behaviour.

EBITDA analysis of APAC telcos: FY-2024

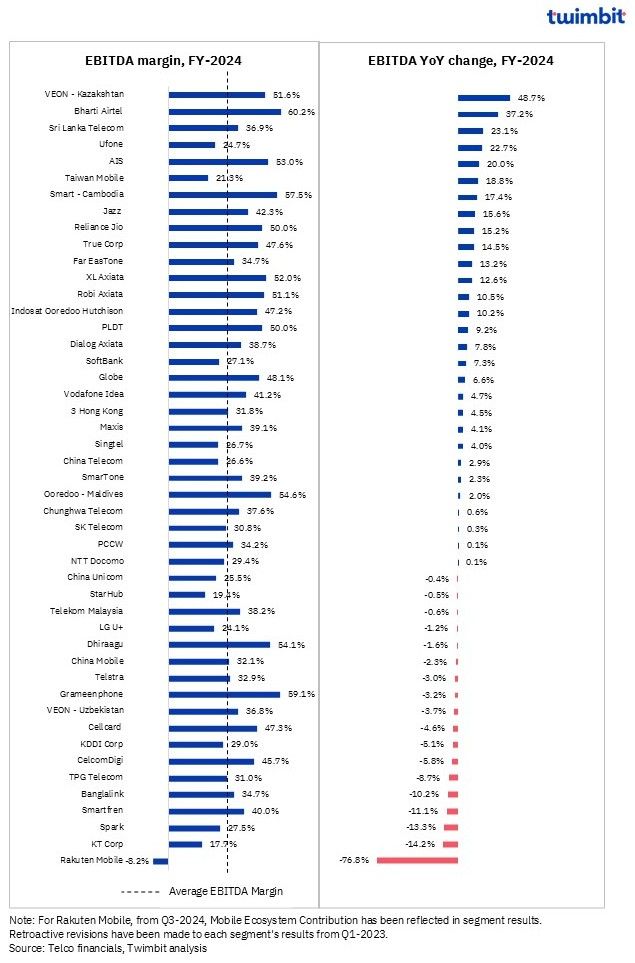

Average EBITDA margin for APAC telcos stabilised at ~31% in FY-2024

Revenue growth coupled with improved operations, cost control measures and operational efficiency initiatives resulted in YoY EBITDA growth for ~62% of the analysed telcos in FY-2024. Nearly 30 % of telcos reported a slight EBITDA variation, within a manageable range (-3% to +3%).

Exhibit 2: EBITDA and EBITDA margin trends for APAC telcos, FY-2024

Key highlights

In FY-2024, telecom operators across the Asia-Pacific region faced varied financial outcomes, with EBITDA performance acting as a key measure of operational resilience. While some telcos leveraged growth momentum and efficiency gains to expand margins, others struggled with elevated costs, restructuring, and macroeconomic headwinds.

- Revenue-led EBITDA growth: Select APAC telcos registering consistent topline growth (supported by subscriber gains, pricing strength, and diversified services)—were able to convert revenue into healthy earnings, maintaining or expanding EBITDA margins despite cost pressures.

- Sri Lanka Telecom: Delivered 23.1% YoY EBITDA growth in FY-2024, led by top-line revenue expansion and stable cost control, resulting in improved operating profitability.

- Smart – Cambodia: EBITDA increased 17.4% YoY in FY-2024, as a result of reductions in material, sales, and other direct costs, reinforcing efficiency across the board.

- Reliance Jio: EBITDA grew 15.2% YoY in FY-2024, driven by strong revenue momentum and optimal utilization of operating capacity, reflecting scale-driven efficiency.

- Globe: EBITDA grew 6.6% YoY in FY-2024, on the back of a 3% reduction in operating expenses, particularly through subsidy management.

- Mergers, Synergies, and Strategic integration: APAC telcos pursuing mergers or structural consolidation benefited from scale efficiencies, improved cost baselines, and expanded service portfolios—contributing to EBITDA growth despite regulatory and integration costs.

- Bharti Airtel: EBITDA increased 37.2% YoY in FY2024, supported by a robust revenue growth and alongwith positive impact of Indus Towers consolidation. A stable EBITDA margin reflected efficient cost management alongside revenue gains.

- AIS: EBITDA grew 20% YoY in FY-2024, driven by higher core service revenues, integration benefits from the TTTBB acquisition, and profit sharing from 3BBIF—alongside handset margin improvement.

- Taiwan Mobile: EBITDA grew 18.8% YoY in FY-2024, led by EBITDA growth across its three reporting segments- telecom, CATV and momo. The merger with T Star and the execution of its Telco+Tech strategy elevated EBITDA.

- True Corp: Improved EBITDA with 14.5% YoY growth in FY-2024, as topline growth converged with merger-driven synergies and process optimization initiatives.

- Far EasTone: EBITDA grew 13.2% YoY in FY-2024, benefitting from merger synergies and margin expansion across its telecom and digital business segments, including smart ICT and consumer digital services.

- Resilience amid inflation and cost pressures: In high-inflation or politically sensitive markets, the ability to grow or defend EBITDA indicated operational agility. The telcos maintained margin discipline despite external pressures by controlling costs and optimizing resource use.

- VEON – Kazakhstan: EBITDA grew 48.7% YoY in FY-2024, driven by revenue expansion, especially in direct digital services, which helped offset inflationary effects.

- Ufone: EBITDA increased 22.7% YoY in FY-2024, driven by growing mobile subscriber base and revenue growth outpacing inflation across key cost items.

- Jazz: Strong EBITDA performance stemmed from the growth of digital services and fintech offerings, offsetting inflation and cost pressures.

- Robi Axiata: Despite market challenges, EBITDA grew 10.5% YoY in FY-2024, on account of focused cost discipline and margin protection.

- IOH: EBITDA grew 10.2% YoY in FY-2024, driven by efficient revenue-to-earnings conversion and sustained growth in topline revenue.

- Margin pressures owing to higher costs and strategic spending: Several operators faced EBITDA erosion due to one-off charges, operational restructuring, or strategic investments in future-focused areas.

- KT Corp: EBITDA declined 14.2% YoY in FY-2024, amid rising operational expenses, notably from workforce restructuring, even as selling costs were reduced.

- Spark: EBITDA declined 13.3% YoY in FY-2024, as product costs, labor expenses, and general operating costs increased, narrowing earnings flexibility.

- TPG Telecom: EBITDA decline of 8.7% YoY in FY-2024 was due to $250 million non-cash impairment charge tied to decommissioning assets ahead of its mobile network-sharing deal with Optus

- Rakuten Mobile: Despite cost normalization leading to positive non-GAAP EBITDA in Q4-2024, full-year EBITDA remained negative—albeit improved from FY-2023.

CAPEX analysis of APAC telcos: FY-2024

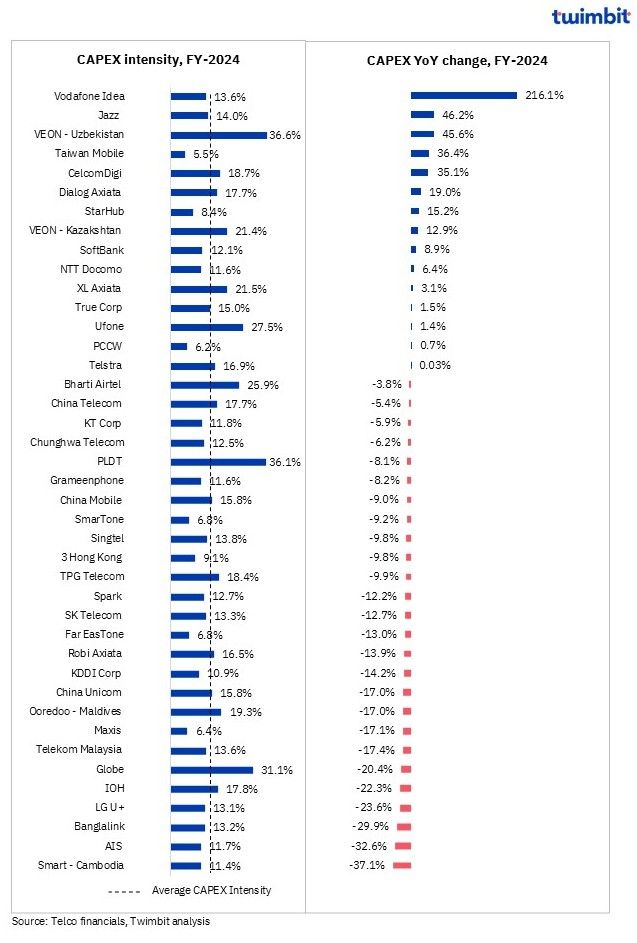

Average CAPEX intensity declined to 15% in FY-2024 as compared to 16.7% in FY-2023, as 4G/5G network deployment of leading telcos reaches completion

Nearly 63% of the 41 telcos analysed reported a YoY CAPEX decline in FY-2024. The maturation of 4G and 5G network rollouts in major markets alongwith telcos focussing on existing infrastructure modernisation and improving cash flow and profitability suggests CAPEX stabilisation or a potential decrease in the upcoming years.

Exhibit 3: CAPEX and CAPEX intensity trends for APAC telcos, FY-2024

Key highlights

As the telecom sector across the Asia-Pacific region evolves to meet shifting technological and economic demands, operators are navigating divergent investment paths. As the rollout of 4G and 5G networks reaches maturity across major APAC markets, few telcos are accelerating capex to build next-gen networks, while others are consolidating their infrastructure portfolios to optimize returns.

- Network expansion and 5G acceleration: In highly competitive and populous markets, expanding 4G/5G coverage remains essential. Operators are intensifying investments to improve connectivity, reduce network congestion, and meet the growing demand for data.

- Vodafone Idea: The telco initiated a three-year investment plan to expand both 4G and 5G services and expanded its coverage to 1.07 billion of country’s population by December 2024, from 1.03 billion in March. It also launched its 5G services in Mumbai in March 2025, signalling a re-entry into premium urban markets.

- Jazz: Raised capex by 46.2% YoY to USD 193.6 million (PKR 53.9 billion) in FY-2024, to focus on expanding its 4G footprint and enhancing digital product offerings. The operator’s capex intensity rose to 14% in FY-2024, underscoring its commitment to infrastructure-driven growth.

- VEON – Uzbekistan: CAPEX increased 45.6% YoY to USD 100 million (UZS 1.2 trillion) boosting capex intensity from 27.5% in FY-2023 to 36.6% in FY-2024. The investment accelerated 4G rollouts across the country to enhance service quality and coverage.

- Axiata group operating telcos namely Dialog Axiata and XL Axiata also reported CAPEX growth, facilitated by network expansion.

- Dialog Axiata: CAPEX increased 19% YoY to USD 100.4 million (LKR 30.3 billion) owing to continued investment in 4G, which led to an increase in BTS count from 7,900 in FY-2023 to 8,909 in FY-2024, as the operator deepens rural and suburban network reach.

- XL Axiata: The telco continued to maintain strong infrastructure growth, expanding its 4G BTS count from 104,993 in FY-2023 to 110,995 in FY-2024, reinforcing its nationwide coverage expansion plans.

- Advanced technology and Digital infrastructure investments: Operators are directing capex towards emerging technologies such as MIMO, AI, and computing infrastructure to enhance network efficiency, prepare for digital services, and build platforms for future monetization.

- Taiwan Mobile: CAPEX increased 36.4% YoY to USD 344 million (TWD 11 billion), owing to investments in both network consolidation and digital diversification through the acquisition of ICT firm Systex in Q3-2024, signalling a strategic extension beyond traditional telco operations.

- VEON – Kazakhstan: CAPEX increased by 12.9% YoY to USD 182.9 million (KZT 85.7 billion) led by targeted investments in massive MIMO and 4.9G wireless technology rollouts. This reflects a shift toward more advanced wireless capabilities to serve high-demand regions.

- SoftBank: CAPEX grew 8.9% YoY to USD 5.1 billion (JPY 775 billion), driven by investments primarily for AI computing infrastructure and network enhancements, driven by the LY Group. The investment marks a shift from connectivity toward computational capacity and digital enablement.

- True Corp: The telco increased its CAPEX spending by 1.5% YoY to ~USD 880 million (THB 30.9 billion), to modernize its network and improve customer experience following the merger in 2023, aiming to consolidate market share and service quality.

- Capital rebalancing after peak investment cycles: Several operators are reducing capital intensity after heavy spending in prior years. These adjustments aim to optimize the use of existing assets, control debt, and improve return on invested capital.

- Banglalink: The telco scaled down capital investment due to high infrastructure rollout in FY-2022, focusing now on asset efficiency and performance metrics. This resulted in CAPEX declining by 29.9% YoY to USD 68.5 million (BDT 7.9 billion).

- Maxis: The telco is prioritising critical investments that directly enhance integrated network capabilities resulting in CAPEX declining by 17.1% YoY to USD 147.5 million (MYR 674 million). This recalibration is part of a broader focus on operational efficiency.

- 3 Hong Kong: With major 5G upgrades completed, the operator has scaled back capex, enforcing strict cost controls and targeting high-impact investments only. This resulted in CAPEX declining by 9.8% YoY to USD 55.6 million (HKD 434 million) in FY-2024.

- Bharti Airtel: Capex declined 3.8% YoY to USD 4.2 billion (INR 350 billion) in FY-2024, following significant prior investments in 5G deployment across India, with the focus now shifting towards asset utilization and optimization.

- KDDI and AIS: Both operators have moderated their capex after reaching peak investment levels, leveraging mature network assets to maintain service standards without additional large-scale deployments.

- Strategic cost discipline and cash flow focus: Economic pressures and investor expectations are pushing operators to enforce tighter capital controls. The focus has shifted toward achieving positive free cash flows, maintaining shareholder returns, and avoiding overextension.

- Globe: The telco tightened capital outlays with a target to achieve positive free cash flows by 2025, resulting in CAPEX declining by 20.4% YoY to ~USD 981 million (PHP 56.2 billion). The approach favours a more balanced capital deployment model after years of aggressive infrastructure buildouts.

- Spark: Reduced spending across cloud, fixed networks, and data centres, reflecting a pause in large-scale investments and an emphasis on maintaining existing capabilities. This resulted in CAPEX decline by 12.2% YoY to ~USD 293 million (NZD 484 million) in FY-2024.

- China Unicom: Overall CAPEX reduced by 17% YoY to USD 8.5 billion (CNY 61.4 billion) in FY-2024, due to a 48% decline in connectivity spend. However, investment in computing power increased by 19%, reflecting a refined capital strategy favouring smarter infrastructure.

- PLDT: The telco continued its plan to taper capex and reduce intensity from a high of USD 1.7 billion in FY-2022 to between USD 50-53 billion (PHP 68-73 billion) in FY-2025. The initiative aims to support sustainable cash generation and financial stability.

- China Telecom: Capex declined by 5.4% YoY to USD 13 billion (CNY 93.5 billion) in FY-2024, with a significant drop in mobile network investments. The operator is reallocating funds to newer growth avenues, such as enterprise services.

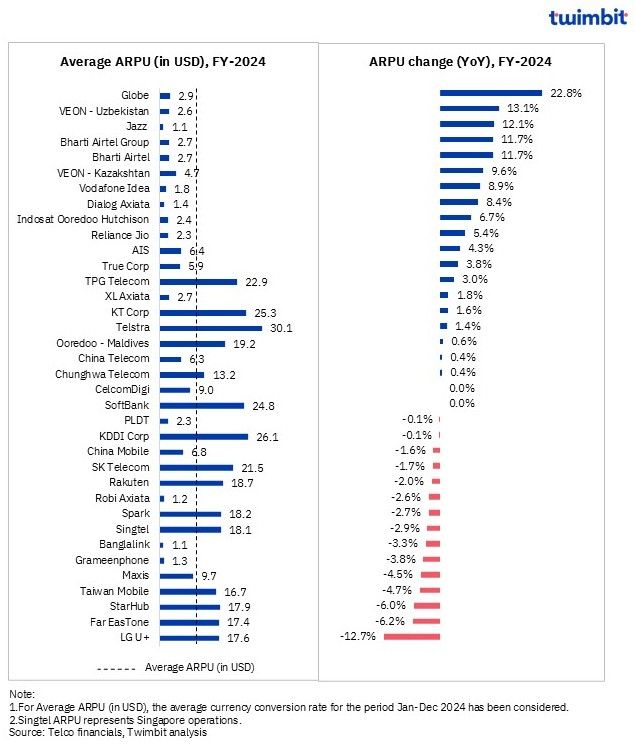

ARPU analysis of APAC telcos: FY-2024

Average ARPU remained stagnant (1% YoY decline), reaching USD 10.9 in FY-2024

The ARPU analysis for the 35 telcos analysed is as follows:

- Nearly 51% reported increased ARPU levels in FY-2024

- Nearly 40% reported higher YoY ARPU growth in FY-2024 compared to FY-2023

- Nearly 49% of the telcos % stabilized their ARPU levels in FY-2024, with YoY changes ranging from -3% to 3%

Exhibit 4: ARPU trends for APAC telcos, FY-2024

Key highlights

In FY-2024, ARPU emerged as a key indicator of strategic adaptability across APAC telecom markets. While some operators capitalized on network expansion and digital service integration to drive user value, others contended with the pressures of market saturation, intensifying competition, and broader economic uncertainty.

- Increased data usage, tariff recalibration and postpaid expansion: As subscriber growth slows, sustainable ARPU uplift depends increasingly on higher-value plans, improved customer mix, and optimized pricing structures.

- Globe: ARPU increased 22.8% YoY to USD 2.9 (PHP 163.5) in FY-2024, led by increased data usage, healthy subscriber mix which resulted in ARPU growth of 7% YoY from the post-paid segment during the year

- Bharti Airtel: ARPU grew 11.7% YoY to USD 2.7 (INR 224.4) in FY-2024, driven by growth in postpaid users, data monetization, and strategic price increments implemented in mid-2024. Monthly data usage per user reached 24.5 GB, reflecting deeper digital engagement.

- Vodafone Idea: ARPU improved 8.9% YoY to USD 1.8 (INR 152.8) in FY-2024, through 4G expansion, customer upgrades, and selective tariff increase, despite broader financial constraints.

- Reliance Jio: ARPU increased 5.4% YoY to USD 2.3 (INR 190.5) in FY-2024, supported by tariff hikes and a higher-quality subscriber base. With 170 million 5G users and average monthly usage of 32.3 GB, the operator monetized growing demand effectively.

- AIS: ARPU grew 4.3% YoY to USD 6.4 (THB 224.8) in FY-2024, aided by package restructuring, increased tourist activity, and personalized service bundling. Subscriber growth of 2.6% also supported topline stability.

- True Corporation: ARPU benefited from the removal of discounts and a strategic push to upsell users into higher-value plans. ARPU increased 3.8% YoY to USD 5.9 (THB 209.3) in FY-2024

- Digital integration and ecosystem buildout: Telcos are increasingly prioritizing beyond-connectivity services, building digital ecosystems—from fintech to content, to strengthen growth strategies, generate recurring revenue, and help reduce churn.

- VEON – Uzbekistan: ARPU grew 13.1% YoY to USD 2.6 (UZS 33,250) driven by a rise in multi-play customers and digital service adoption under its DO1440 strategy. Enhancements in the digital product portfolio played a pivotal role.

- Jazz: Increased 4G penetration and robust performance from JazzCash and MMBL bolstered ARPU, which grew by 12.1% YoY to USD 1.1 (PKR 300) in FY-2024. A diverse digital service mix proved to be a differentiator in revenue expansion.

- VEON – Kazakhstan: An expanding 4G user base and digital platforms such as BeeTV and Qazcode contributed to ARPU growth of 9.6% YoY to USD 4.7 (KZT 2,212) in FY-2024, aligning with the DO1440 framework.

- Indosat Ooredoo Hutchison: ARPU gains came from a focus on acquiring and retaining high-value subscribers across both prepaid and postpaid segments. ARPU grew 6.7% YoY to USD 2.4 (IDR 38,000) in FY-2024.

- Margin compression and revenue headwinds: Select telcos confronted political instability, economic stress, or intensified competition impacting top-line revenue and ARPU—even amid network investments and user base expansion.

- Taiwan Mobile: An 8% YoY decline in postpaid ARPU led to overall ARPU decline by 4.7% YoY to USD 16.7 (TWD 535.8) in FY-2024, underscoring pricing and retention challenges.

- StarHub: Declines in roaming, postpaid voice, IDD, and value-added services contributed to 6% YoY decline in ARPU reaching USD 17.9 (SGD 23.9) in FY-2024.

- Maxis: Competitive pressures drove down both prepaid and postpaid ARPU, highlighting continued strain in Malaysia’s market. ARPU declined 4.5% YoY to USD 9.7 (MYR 44.5) in FY-2024.

- Grameenphone: Challenging market conditions in H2-2024 led to a 3.8% YoY drop in ARPU, largely due to reduced data and bundle service contributions.

- Banglalink: ARPU declined 3.3% YoY to USD 1.1 (BDT 124) in FY-2024 amid political unrest, economic headwinds, and a reduction in 4G subscribers.

- China Mobile: Despite 19% growth in 5G subscribers, ARPU declined by 1.6% YoY to USD 6.8 (CNY 48.5) in FY-2024, reflecting falling data and voice traffic revenues.

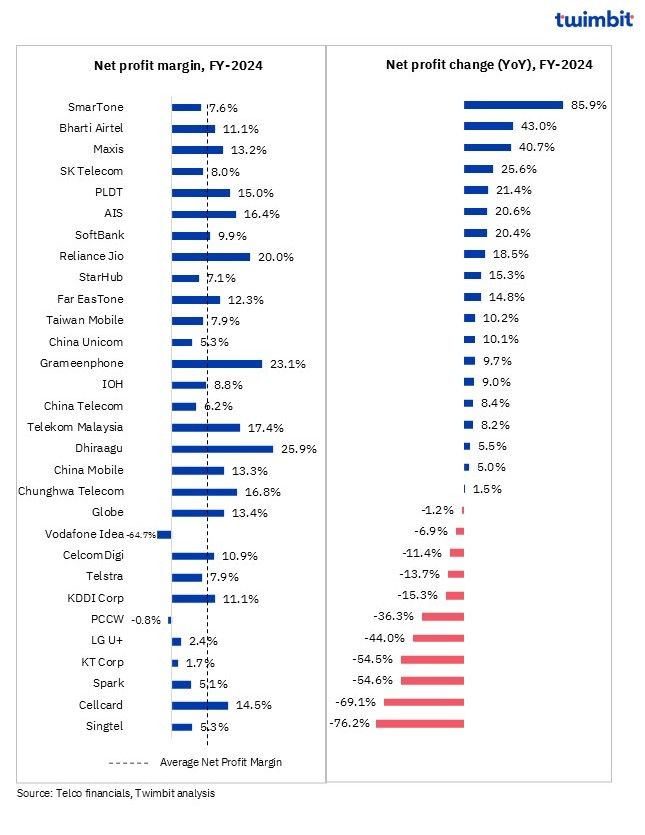

Profitability analysis of APAC telcos: FY-2024

Amongst the 30 telcos analysed, ~63% reported YoY net profit growth in FY-2024. The average net profit margin remained resilient at 9% level in FY-2024 as compared to 8.9% in FY-2023, owing to robust growth in profitability by select telcos.

Exhibit 5: Profitability trends for APAC telcos, FY-2024

Key highlights

APAC Telcos reported mixed profitability outcomes in FY-2024, shaped by a blend of revenue performance, strategic investments, one-off events, and cost controls.

- Profit growth from core operations and cost efficiency: Consistent profitability was achieved by select telcos balancing revenue growth with cost efficiency. These telcos focused on strengthening fundamentals while maintaining margin discipline.

- SmarTone: Profit surged in FY-2024, owing to reductions in staffing, inventory, and service delivery costs.

- Bharti Airtel: The telcos’ profit grew 43% YoY in FY-2024 to owing to increase in revenue coupled with exceptional gain from consolidating Indus Towers into Airtel in during Q4-2024.

- AIS: Net profit grew 20.6% YoY in FY-2024, driven by strong operating results and continued cost optimization.

- StarHub: Net income improved 15.3% YoY in FY-2024, through higher operating profits and reductions in financing, tax, and non-operating expenses.

- Maxis: Net income improved by 40.7% YoY in FY-2024, in alignment with a 3.5% YoY increase in revenue and better cost efficiency.

- IOH: Profit grew 9% YoY in FY-2024, owing to revenue gains and lower non-operating expenses, despite higher marketing and depreciation costs.

- China Unicom & China Mobile: Profitability improved as revenue growth outpaced expense increments, demonstrating strong cost control at scale.

- Diversification boosts bottom line: Select telcos expanding into fintech, AI, or adjacent digital sectors also reported bottom-line gains, reflecting the importance of broader ecosystem to enhance financial outcomes.

- SK Telecom: Profit rose 25.6% YoY in FY-2024, boosted by valuation gains from the merger of its AI chip subsidiary Sapeon Korea with Rebellions Inc., creating Rebellions—the first domestic AI chip unicorn.

- PLDT: Losses from PLDT’s fintech arm, Maya, declined during the year with Maya Innovations Holdings turning profitable in Dec 2024, driven by sustained gains from Maya Bank, which has been profitable since Sept 2024. Meanwhile, core telecom income rose 1.8% YoY, contributing to a 21.4% YoY surge in group profit for FY2024.

- SoftBank: Net income grew 20.4% YoY in FY-2024, as financial services turned profitable from Q2-2024, coupled with overall revenue growth.

- Taiwan Mobile: Net income grew 10.2% YoY in GY-2024, supported by EBIT gains from the T Star acquisition and improved rate plans.

- One-off events impacting profit: Short-term profitability was affected by tax changes, impairments, or accounting adjustments. Exceptional one-time events masked the underlying stability of core operations across selective telcos, artificially skewing their financial performance indicators.

- Singtel: Net profit declined in FY-2024, attributed to the absence of a one-off gain of ~USD 897 million (SGD 1.2 billion) from the previous year’s merger of its Indonesian associate Telkomsel with IndiHome.

- LG Uplus: Net income dropped 44% YoY in FY-2024 due to asset impairment related to its cable TV unit LG HelloVision.

- PCCW: Profit declined 36.3% YoY in FY-2024, despite operational growth, due to a 107% YoY increase in income tax liabilities.

- KDDI: Profit decreased 15.3% YoY in FY-2024, reflecting a one-off effect from the restructuring of subsidiaries and affiliates in the prior fiscal year.

- Margins pressured by cost headwinds: For some telcos, rising operating expenses and subdued revenue growth led to margin compression. These challenges highlighted vulnerabilities in cost structures.

- KT Corp: Profit fell as operating expenses outpaced modest revenue gains, limiting bottom-line growth.

- Spark: Net income declined amid shrinking revenue and increased labor, product, and other operating costs.

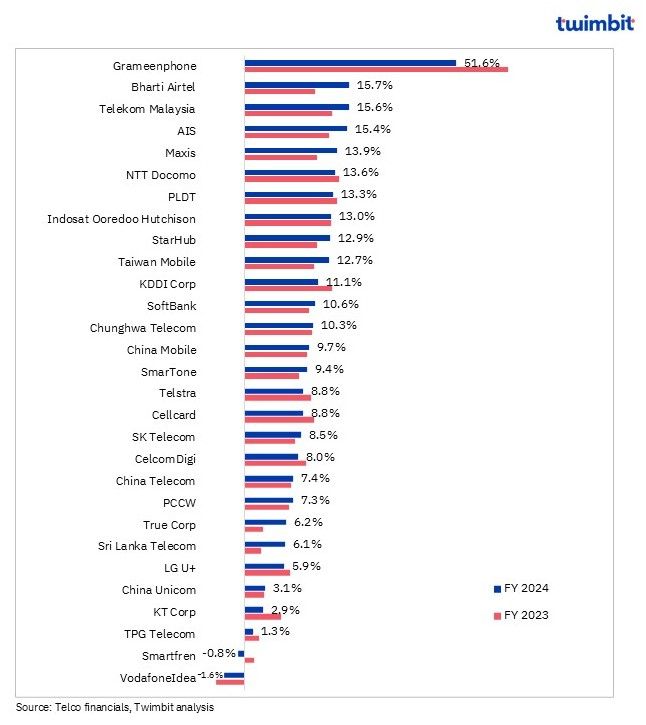

ROCE trends of APAC telcos: FY-2024

ROCE improves for APAC telcos in FY-2024, indicating better capital utilisation

ROCE improved for ~64% of the telcos in FY-2024, with median ROCE being 9.1% in FY-2024.

Growth in revenue alongwith increased profitability (due to a reduction in expenses) resulted in positive ROCE growth for majority of the telcos.

Exhibit 6: ROCE trends for APAC telcos, FY-2023 and FY-2024

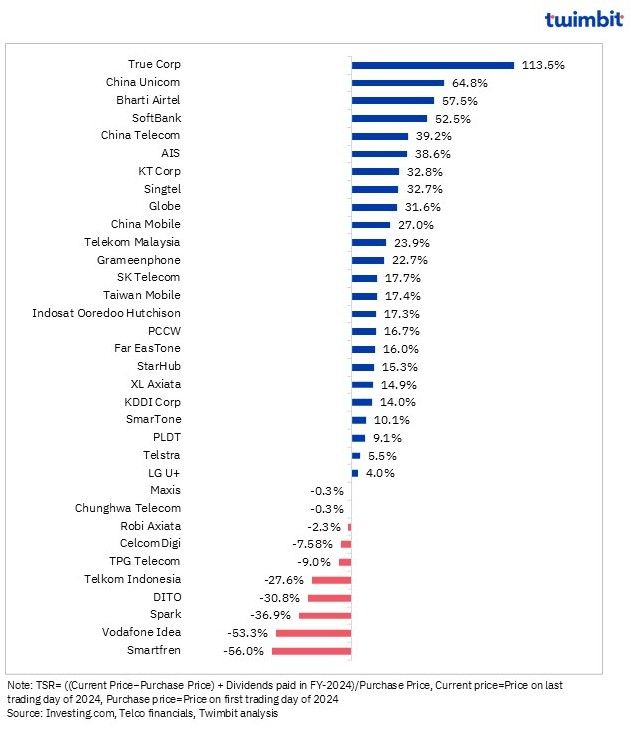

Total Shareholder Return of APAC telcos: FY-2024

Total Shareholder Return (TSR) remained positive for majority telcos in FY-2024, indicating better revenue growth and dividend payout

- Nearly 71% of the telcos reported positive Total Shareholder Return (TSR) in FY-2024.

- An increase in share prices, coupled with dividend payouts, enhanced TSR; 77% of the 23 dividend-paying telecom companies experienced positive TSR.

- Merger synergies facilitated stable growth in revenue, operating profit and Blended ARPU, alongwith stock’s undervaluation prior to merger might have encouraged sustained buying pressure throughout the year, resulting in high TSR for True Corp.

- China Unicom leads with a TSR of 64.8%, driven by its strong financial growth and pioneering role in 5G-Advanced technology.

- Bharti Airtel Group’s TSR of 57.5% reflects its successful 5G expansion and strong market position in India’s dynamic telecommunications sector.

Exhibit 7: TSR for APAC telcos, FY-2024

Key strategic developments: Q4-2024

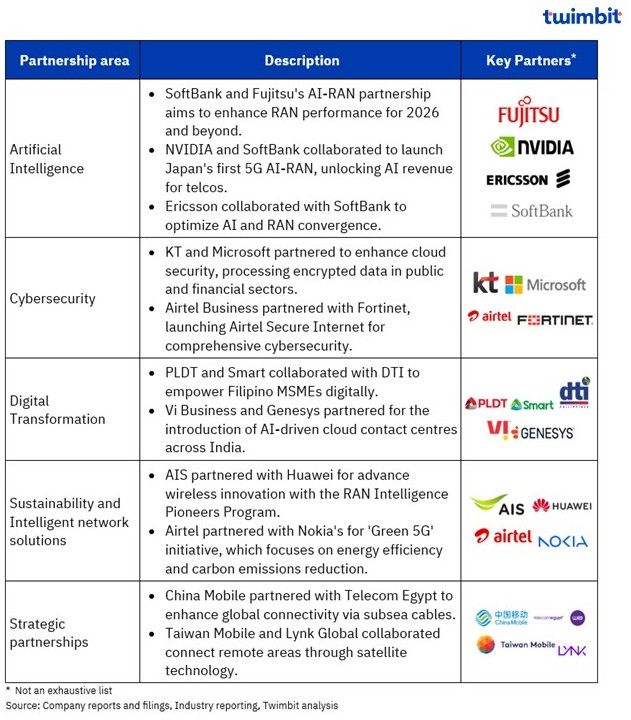

Key strategic partnerships and alliances: Q4-2024

APAC telcos actively pursue strategic partnerships focussing on AI integration, network infrastructure, digital transformation, and sustainability. These collaborations aim to enhance telecommunications capabilities, fostering industry innovation and growth across the region.

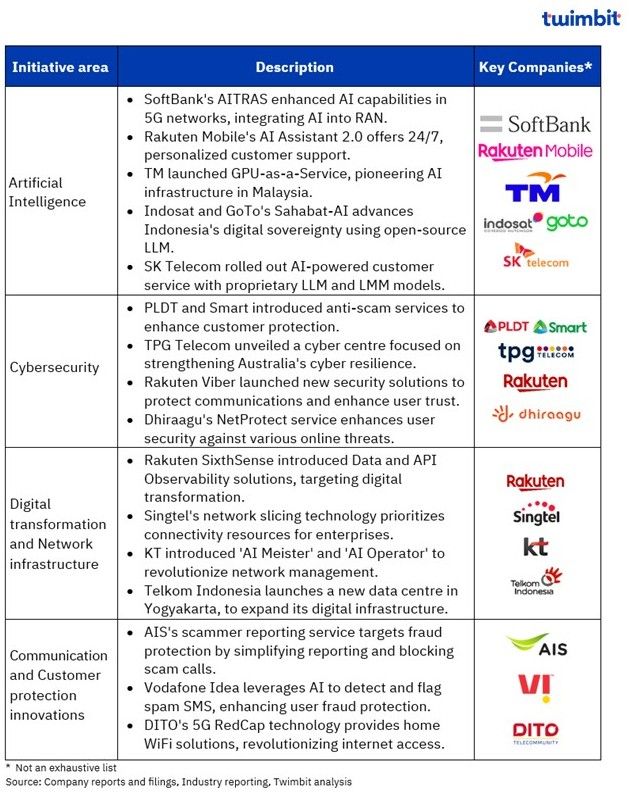

Key strategic initiatives: Q4-2024

Key advancements by APAC telcos emphasise AI deployments, cybersecurity measures, digital transformation, and network infrastructure developments, reflecting a transformative impact on the telecommunication industry within the region.

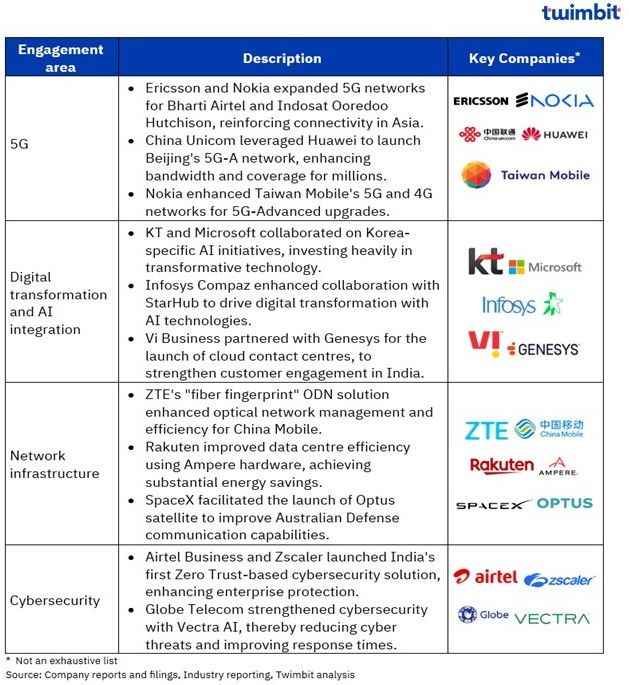

Key contract wins: Q4-2024

The telecom industry in the APAC is witnessing significant developments in 5G expansion, digital transformation initiatives, AI integration, and infrastructure enhancements. These advancements underscore a focus on connectivity, modernized operations, and enhanced service offerings globally.

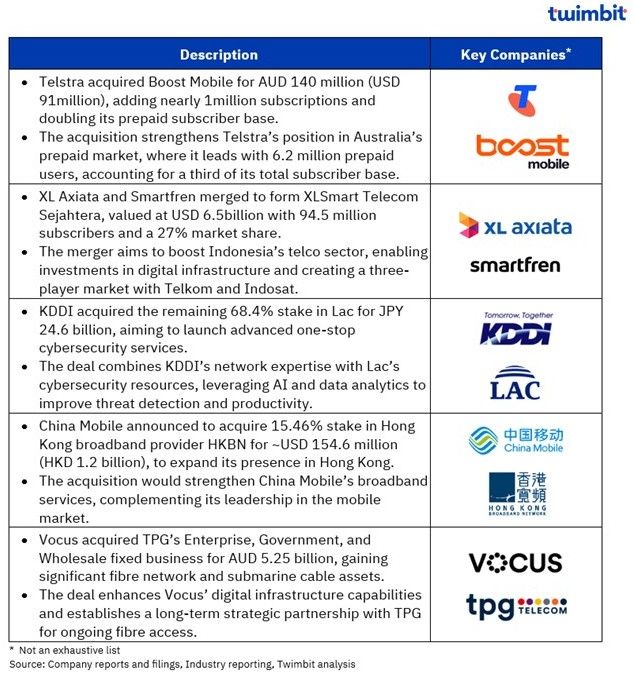

Key M&As and Divestures: Q4-2024

APAC telecom market continues to consolidate through strategic mergers and acquisitions with a view to strengthen market positions, expand digital infrastructure, and diversify services. Key deals highlight a focus on scalability, cross-border growth, and innovation in a competitive telecom landscape.

Research Methodology and Assumptions

- The report titled “APAC Telcos Performance Benchmarks: Winter 2025” sets out key observations and comparative analysis of telecommunications operators across the Asia-Pacific region for the period January – December 2024. The report includes performance metrics such as Revenue, EBITDA, Capital Expenditure (CAPEX), Average Revenue Per User (ARPU), Profitability, Return on Capital Employed (ROCE), and Total Shareholder Return (TSR).

- The analysis is based on publicly available information sourced from telecommunications companies and extensive secondary research. For the purposes of uniformity and comparability, Twimbit has applied a calendar year basis (1 January -31 December) to define the financial year (FY).

- To ensure consistency in financial comparisons across markets, all financial data has been translated into USD using a constant average exchange rate for the period 1 January – 31 December 2024.

- The report includes Revenue and EBITDA analysis for 48 and 47 telcos respectively. CAPEX and ARPU have been analysed for 41 and 35 telcos, respectively. Profitability assessments cover 30 telcos, while ROCE and TSR analyses include data for 28 and 35 telcos, respectively.

- Where applicable, blended mobile ARPU has been utilized to provide a comprehensive representation of operator performance across mobile service lines.

- The information presented in this report reflects data available at the time of preparation and publication. It may not capture events or developments occurring subsequent to the stated period. This report has been prepared for general informational purposes only and does not constitute, nor should it be construed as, investment advice or a recommendation to act.

Click here for more contents on telecom

Related APAC telcos performance insights

APAC Telcom Radar – Spring 2025

Global telecom vendor performance indicators – Autumn 2024