Key Takeaways

- APAC telcos generated approximately USD 139 billion in Q3-2023, but YoY revenue growth slowed to 3.5% (overall average basis), marking the slowest quarterly increase in the past six quarters.

- Although Q3-2023 saw a slowdown in overall revenue growth, five telcos achieved double-digit gains, and 84% of the analysed telcos maintained positive momentum. This highlights the industry’s resilience and continued opportunities for growth.

- During Q3-2023, on an average basis, APAC telcos maintained robust EBITDA margins of 38.5% by implementing effective cost control measures and operational efficiency initiatives. Notably, 78% of the analysed companies exhibited positive EBITDA growth, which highlights the success of these strategies.

- The completion of 4G and 5G network rollouts in major markets is impacting CAPEX. 60% of APAC telcos experienced a decline in CAPEX during Q3-2023. This shift signals a focus on optimizing existing infrastructure and exploring new revenue streams.

- Significant CAPEX increases were observed at Ooredoo Maldives and KDDI Corp, indicating ongoing investments in network expansion and modernization in these markets.

- ARPU levels for about 50% of the APAC telcos in Q3-2023 remained relatively stable, with year-over-year changes ranging from a slight decline of 3% to a modest increase of 3%. This suggests that ARPU growth in some markets may be plateauing.

- Indian telecom operators experienced a moderation in ARPU growth, due to increased competition.

- Telecommunications companies based in Japan have managed to maintain the highest average ARPU in the region. Furthermore, they have reported consistent growth in ARPU during the first three quarters of 2023. This indicates that the impact of regulatory interventions and tariff reductions is diminishing on the ARPU levels in the Japanese market.

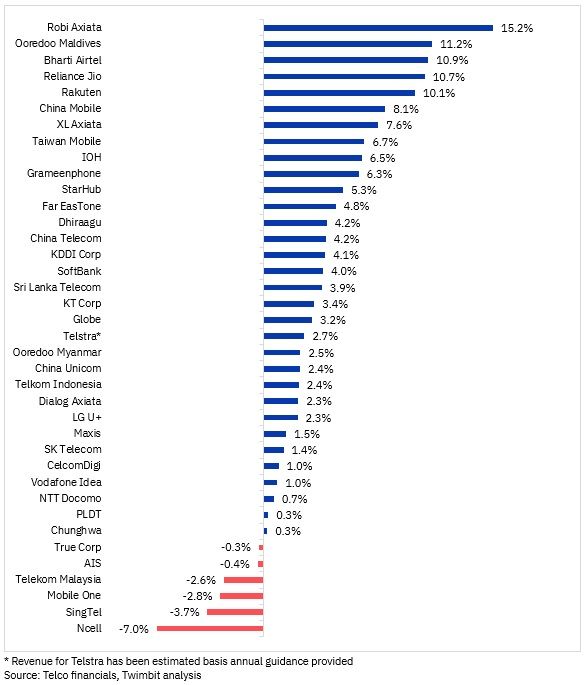

Revenue analysis of APAC telcos: Q3-2023

Revenue growth for majority of telcos continue in Q3-2023

In Q3-2023, telecom companies in the APAC region saw a slowdown in revenue growth, with the average increase dropping to 3.5% year-over-year (YoY), which is the lowest rate recorded in the last six quarters. However, despite this slowdown, the combined revenue of the 38 analysed telcos amounted to approximately USD 139 billion, which represents a YoY increase of around USD 6 billion. Notably, five telcos achieved double-digit growth, and approximately 84% of the analysed telcos reported positive revenue changes.

Exhibit 1: Revenue trends (% change) for APAC telcos (YoY basis), Q3-2023

Robi Axiata

- Robi Axiata has once again outperformed its peers in the APAC region and has emerged as the fastest growing APAC Telco for the second consecutive quarter. The company’s revenue in Q3-2023 grew by 15.2% YoY, reaching approximately USD 232.5 million (BDT 25.4 billion), driven by an increase in 4G subscribers and data revenue.

- Data revenue increased by 33.9% and reached ~USD 96 million (BDT 10.5 billion) in Q3-2023. Data consumption also increased by 16.8% (YoY basis) and reached 6.8 GB during the same period. The rise in data consumption was driven by an increase in 4G data users, which grew by 23.5% to reach 34.2 million in Q3-2023.

Ooredoo Maldives

- Ooredoo Maldives’ revenue grew by 11.2% to nearly USD 34 million (~MVR 524 million) driven by the increased revenue generated from its mobile and fixed broadband enterprise businesses.

Bharti Airtel

- Bharti Airtel’s Q3-2023 revenue grew by 10.9% to reach ~USD 3.3 billion (INR 269.9 billion), driven by an 11.0% increase in mobile services India revenues on account of 4G/5G customer additions and increased ARPU.

- Airtel Business revenue increased by 9.5%, supported by synergies from connectivity solutions, while its Home business revenue rose by 23.3% due to robust customer growth.

Reliance Jio

- Reliance Jio demonstrated a YoY revenue growth of 10.7%, achieving ~USD 3.2 billion (INR 268.7 billion) in Q3-2023.

- Jio’s sustained growth can be attributed to its strategic expansion of digital platforms and consistent ability to attract new subscribers. The recent launch of Jio True5G, which specifically targets the youth segment, has further strengthened Jio’s competitive edge. This, in turn, has fuelled the adoption of premium devices on its network.

- Reliance Jio has made remarkable progress in its enterprise services portfolio, it has extended its reach to more than 85% of large enterprises in India. This assertion is further supported by Jio’s impressive government bid success rate, which exceeds 80%, and its connectivity partnerships with over 400 Banking, Financial Services, and Insurance (BFSI) accounts, including the top 20 banks.

Rakuten

- Rakuten Group achieved double-digit revenue growth in Q3-2023, reaching its highest revenue ever with consolidated revenue of ~USD 3.6 billion (Yen 518.4 billion).

- This growth is attributed to reduced losses in the mobile business and growth in non-connectivity business revenue from segments like Rakuten Travel, Rakuten Bank, and Rakuten Securities.

- Also, Rakuten’s mobile business grew by 5%, on account of steady growth in subscriber base and ARPU

Ncell

- Ncell’s Q3-2023 revenue declined 7.0% YoY to USD 74.3 million (~NPR 9.7 billion) primarily due to a drop in voice segment revenue.

- The economic decline in Nepal has been observed across various sectors, which coincided with the country’s official entry into recession in April 2023. The market conditions were challenging due to the diminishing foreign currency reserves, a slowdown in multiple economic sectors, and a reported government deficit of ~USD 3 billion.

- In response to the challenging business environment in Nepal, Axiata Group, the parent company of Ncell, has announced its intention to sell Ncell assets in November 2023. This decision is in line with Axiata’s strategic priorities and aims to bolster its future growth prospects. Axiata has also cited declining returns from Ncell as a contributing factor to the sale.

Singtel

- Singtel’s Q3-2023 revenue decreased by 3.7% YoY to ~USD 3.3 billion (SGD 3.5 billion), due to a decline in Optus and Singtel’s Singapore operations. Singtel’s overall revenue growth has declined for the past eight consecutive quarters on a YoY basis.

- During Q3-2023, Optus revenue declined by 5.9% YoY to USD 1.3 billion (SGD 1.8 billion), while Singtel Singapore’s revenue decreased by 4.7% YoY to USD 0.7 billion (SGD 0.9 billion).

Telekom Malaysia

- Telekom Malaysia (TM) faced market challenges in Q3-2023, impacting its consumer segment with stagnant revenue and its enterprise segment with declining sales. Consequently, overall revenue decreased by 2.6% YoY.

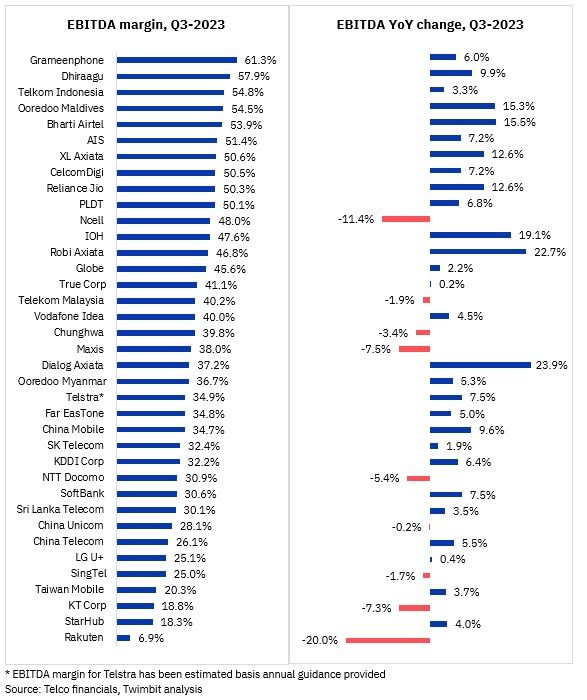

EBITDA analysis of APAC telcos: Q3-2023

EBITDA for APAC telcos continue to increase in Q3-2023

During Q3-2023, telecommunication companies in the Asia-Pacific region achieved their highest average EBITDA margin in the last six quarters, which was a robust 38.5%. This remarkable achievement can be attributed to the telcos’ intensified focus on cost control measures and operational efficiency initiatives, resulting in healthy EBITDA growth for the majority of them. It is noteworthy that almost 78% of the analysed APAC telcos showed positive EBITDA changes during this period.

Exhibit 2: EBITDA and EBITDA margin trends for APAC telcos (YoY basis), Q3-2023

Grameenphone

- Navigating a challenging macroeconomic climate plagued by inflation, energy price hikes, and dwindling foreign currency reserves, Grameenphone remained committed to operational excellence and top-line growth.

- Despite a small decrease of 20 basis points in EBITDA margin, Grameenphone achieved the highest margin of 61.3% among APAC telcos in Q3-2023. This impressive performance can be attributed to the company’s strong focus on both revenue growth and operational efficiency improvements.

Dhiraagu

- Dhiraagu’s EBITDA margin increased to 57.9% in Q3-2023, up 300 basis points from Q3-2022, with a 9.9% rise in EBITDA. This growth in EBITDA margin was also driven by revenue growth.

Telkom Indonesia

- Telkom Indonesia’s EBITDA margin increased by 60 basis points to 54.8% in Q3-2023. Thanks to unwavering dedication and resolute efforts, Telkom has successfully emerged as a leader in digital telecommunications. This accomplishment signifies a crucial moment, paving the way for a future marked by tangible outcomes and transformative impact.

- IndiHome’s fixed broadband service has been the primary driver of the company’s growth, while Telkomsel’s digital business continues to strengthen over time. In Q3-2023, IndiHome revenue increased by 4.8%, and Telkomsel’s digital business revenue increased by 6.3% on YoY basis.

Ooredoo Maldives

- During Q3-2023, the company’s EBITDA margin increased to 54.5% due to effective cost controls and higher revenue, resulting in a 15.3% increase in EBITDA.

Maxis

- Maxis’s EBITDA dropped by 7.5% to reach USD 200.8 million (MYR 929 million), primarily due to restructuring costs associated with cost optimization programs aimed at enhancing operational efficiency.

- EBITDA margin declined by 370 basis point to reach 38% in Q3-2023.

KT Corp

- The EBITDA of KT Corp has decreased by 7.3%, which has resulted in a decline of EBITDA margin by 220 basis points to 18.8% in Q3-2023. This decline can be attributed to the “wage negotiation results and content sourcing cost smoothing” which have caused KT’s net profit to decrease by 11.6%.

Rakuten

- Rakuten has seen a significant improvement in its revenue, which can be attributed to reduced losses in the mobile business and an increase in revenue for core domestic e-commerce businesses such as Rakuten Travel, Rakuten Bank, and Rakuten Securities. As a result, the company has reported positive EBITDA for Q3 2023.

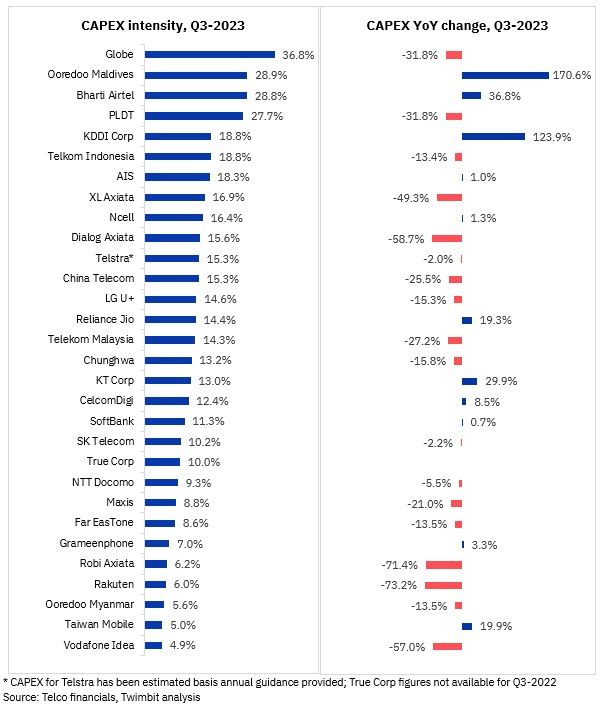

CAPEX analysis of APAC telcos: Q3-2023

Capex accounts for ~15% of overall revenue for APAC telcos in Q3-2023

During Q3-2023, a significant change in APAC telco CAPEX occurred. Almost 60% of the companies analysed reduced their spending compared to the same period in the previous year. This trend is likely due to the 4G and 5G network rollouts maturing in major markets. This suggests that CAPEX is expected to stabilize or even decrease in the upcoming years

Exhibit 3: CAPEX and CAPEX intensity trends for APAC telcos (YoY basis), Q3-2023

Ooredoo Maldives

- Ooredoo Maldives has increased its CAPEX spending by 170.6%, which accounts for 28.9% of its revenue. This decision was made by Ooredoo Group to establish an efficient network infrastructure in the Maldives, which will further enhance its revenue growth.

KDDI Corp

- KDDI Corp increased its CAPEX spending by 123.9% after acquiring a portfolio of urban data centers in downtown Toronto from Allied Properties REIT.

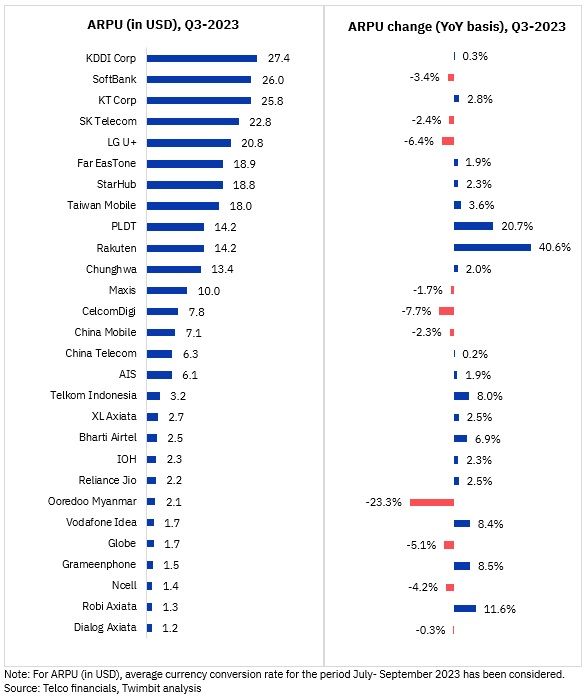

ARPU analysis of APAC telcos: Q3-2023

ARPU level stabilises whereas telcos in Japan witness marginal ARPU growth

- Nearly half of the analysed telcos had stable ARPU levels in Q3-2023, with YoY changes ranging from -3% to 3%. This suggests a plateauing trend in some markets.

- Indian telcos maintained ARPU growth at a moderated pace due to increased competition.

- In Japan, consistent quarterly increases in ARPU throughout 2023 suggest that the impact of tariff reductions and regulatory interventions on ARPU levels is diminishing.

- During Q3 2023, Rakuten, PLDT, and Robi Axiata saw impressive double-digit growth in ARPU, with 40.6%, 20.7%, and 11.6% respectively. Other noteworthy performers include Grameenphone (8.5%), Vodafone Idea (8.4%), Telkom Indonesia (8.0%), and Bharti Airtel (6.9%).

Exhibit 4: ARPU trends for APAC telcos (YoY basis), Q3-2023

Rakuten

- ARPU levels have been growing strongly due to increased data consumption driven by the SAIKYO Plan (meaning “Strongest Plan”), launched in June 2023. The SAIKYO plan has also led to a reduction in the churn rate, with the adjusted churn rate (including both B2C and B2B customers) being 1.44% in Q3-2023.

- ARPU grew on account of B2C data consumption growth owing to seasonal uplift in late July and August.

- The telco anticipates an increase in B2B ARPU starting Q4-2023 due to upcoming options in October 2023 and the expansion of offerings.

PLDT

- PLDT reported a 20.7% increase in ARPU in Q3-2023 as compared to the same period last year. This growth was driven by the increase in 5G average monthly data traffic, which rose by approximately 80% (YoY basis) to reach 56 PB. This increase was due to the rise in 5G unique connected devices, which reached 4.3 million in Q3-2023 compared to 2.5 million a year ago.

Robi Axiata

- The telecom companies reported an 11.6% increase in ARPU in Q3-2023 on a YoY basis. This growth in Q3-2023 data revenue (33.9% on YoY basis and 6.2% compared to the previous quarter) led to the increase in ARPU.

Grameenphone

- In Q3-2023, Grameenphone’s ARPU levels saw an increase due to a 22.1% YoY increase in average monthly data usage per user to approximately 7GB.

Research Methodology and Assumptions

- The information presented in this report has been collected through secondary research methods and by obtaining data from the telecommunications companies. Twimbit has analysed the data in this report using the calendar year approach. It should be noted that Q1 refers to the period from January to March.

- For accurate analysis, we have used a constant currency conversion rate to convert from local currency to USD, with the USD rate being the average for July-September 2023.

- The report assesses the Revenue and EBITDA of 38 and 37 telcos respectively, as Vodafone does not report EBITDA every quarter. For CAPEX and ARPU, the analysis covers 30 and 28 telcos respectively.

- Blended mobile ARPU is considered for the analysis, wherever applicable.

Explore more content on telecoms: here

Recommended by Twimbit