How did Apple enter the financial services industry?

When the first iPhone launched in 2007, it was revolutionary. Apple had successfully broken the code, capturing the hearts of many with a minimalist interface and intuitive navigation.

Fortunately, that’s not where the story ends for the famous tech giant we know today. With a constant eye on making difficult processes easy, Apple turned its eyes to its next biggest target – the BFSI industry.

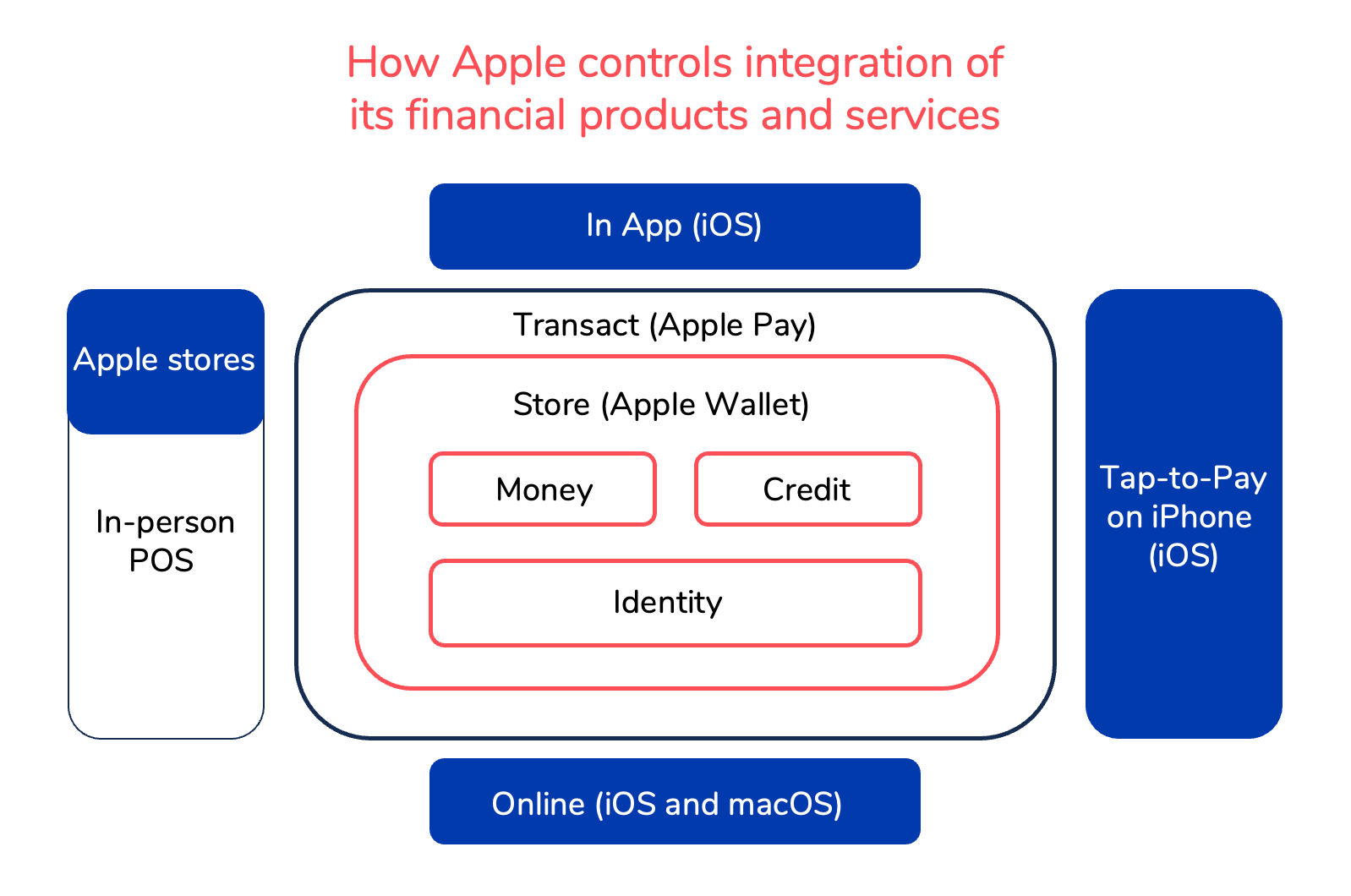

At the time, Apple and banking were two entities that did not go hand in hand. Yet, it dove deep into the fire, challenging many banks with its roster of financial services. Since then, Apple has continued to develop and expand its roster to integrate across the iPhone and other Apple-related products.

This includes:

- Apple Wallet

A digital wallet for storing payment cards, boarding passes and tickets on Apple devices.

- Apple Pay

A convenient mobile payment service for users to make contactless payments.

- Apple Card

A credit card by Apple in partnership with Goldman Sachs that offers seamless integration with the Apple Wallet app.

- Apple Cash (offered with Green Dot)

A peer-to-peer payment service within iMessage that enables users to receive, send and request money from other Apple users.

- Apple Pay Later

A BNPL service offering that splits the user’s total payments into 4 payments over 6 weeks with no interests or fees.

- Apple Pay Monthly Instalments

A BNPL service offering that splits the user’s annual payment into interest-free monthly instalments.

- Apple Tap to Pay on iPhone

A financial service that transforms the iPhone into a POS (Point-of-Sales) terminal for businesses to accept Apple Pay, contactless credit and debit card transactions seamlessly and securely.

These services have fundamentally changed how users pay today. Because of this, Apple has experienced exponential growth while discovering new and easy ways of integrating finance into its products and services.

- Exhibit 1

From the surface, Apple appeared to be on the verge of dominating the banking industry with an iron fist. Everything just seemed to work.

However, recent external factors have led to the Silicon Valley giant facing a few hitches, such as the launch of its new high-yield Savings Account. Despite its successful launch, the First Republic Bank failed to capitalise on this opportunity due to unprecedented deposit outflows.

Thus, it was fortunate that Goldman Sachs, a banking partner of Apple, came to the rescue. By rapidly pulling in consumer funds, it began to target Apple’s 113 million iPhone owners to ensure the continued success of Apple’s Savings Account.

Goldman Sachs, the entry point for Apple into core banking services

Apple’s entry into banking proved impossible for many simply because of its inability to attain an official banking license. Hence, the next best option proved to be collaboration. Its ideal target partner – Goldman Sachs.

Inadvertently, it was Apple’s greatest decision yet. Not only did this strategic decision pay off in spades, as seen with the company’s future endeavours (Savings Account), but it also provided the leverage necessary for financial expansion. Now, Apple could freely circumvent the regulatory constraints often associated with traditional banks.

From a technical standpoint, this meant that it operated itself as a front for Goldman Sachs Bank USA, which holds a state charter and is FDIC-insured. Meanwhile, in fintechs, Apple functioned similarly to a neobank, much like Chime, Revolut and Monzo.

However, unlike the latter, it had one unparalleled advantage over the others – its global brand popularity and presence. This alone effectively acted as the banking partner’s extensive branch network.

Hence, as we move into a more digitally-centric future, many predict that this dynamic duo will be one of the first to set the groundwork for what a highly formidable fintech powerhouse could look like in America.

- Exhibit 2

Why did Apple venture into banking?

On closer inspection, Apple’s decision to enter the BFSI industry was not merely an experiment to venture into unknown territory. Instead, its entry into savings represents a natural extension of its end-to-end financial ecosystem. Today, the company has shifted its focus to driving sales revenue rather than accumulating deposits.

Moving forward in the BFSI industry, it hopes to captivate its user base akin to the success of its Apple ecosystem[1], as it intends to achieve this by stimulating its financial economy. The end goal – encourage as many potential customers to make continuous purchases of Apple’s financial service products.

Starbucks applied a similar approach, enabling its app funds only for purchases at its own stores. However, Apple’s track record in financial services has been a mixed result.

A key reason for this undesirable track record could be the company’s APY (Annual Percentage Yield[2]) of 4.15%. Although it is more than 10x the national average, other banks are willing to offer higher yields than the Silicon Valley giant.

- Exhibit 3

Comparing Apple’s saving a/c 4.15% yield with 17 other banks

| Bank name | Interest rate |

| CFG Bank | 5.02% APY |

| Newtek Bank | 5.00% APY |

| UFB Direct | 4.81% APY |

| Primis Bank | 4.77% APY |

| Vio Bank | 4.77% APY |

| CIT Bank | 4.75% APY |

| BankPurely | 4.75% APY |

| iGObanking | 4.75% APY |

| Bask Bank | 4.65% APY |

| Popular Direct | 4.65% APY |

| Salem Direct Bank | 4.61% APY |

| Upgrade | 4.56% APY |

| Western State Bank | 4.55% APY |

| Bread Savings | 4.50% APY |

| First Foundation Bank | 4.50% APY |

| Ivy Bank | 4.50% APY |

| TotalDirectBank | 4.50% APY |

Yet, its low APY does not appear to hinder the majority of Apple’s demographic, with favouring interest towards the tech giant. This is because Apple’s level of certifiable convenience, transparency and brand trust carries its value higher than other banks, which is a surefire reason why it will experience significant demand moving forward.

Why will Apple succeed in the BFSI industry?

Apple is bound to accumulate great success in the BFSI industry because of two key factors; its wealth of customer data and the ability to drive an efficient economy of scale.

- Apple’s vast customer data fuels the engine for product innovation

With access to personal schedules, browsing history, email content and other data, Apple possesses a wealth of information about its customer base. Customer data is vital for Apple to enhance its services better.

These could include assisting users with budgeting, securing financing for a car, selecting an insurance provider, or cancelling subscriptions they may have forgotten about.

In banking, Apple could gain insight into the user’s cash flow with adequate tracking and use this information to provide personalised financial products. If used correctly, this depth of understanding would give Apple a decisive advantage in the financial services space.

The current challenge is that the services provided, such as Apple Pay and Apple Card, only exist for Apple users. Unfortunately, this leaves a comprehensive portion of Android users unable to access its financial services.

- Apple’s partnership with Goldman Sachs empowers its economies of scale

An efficient economy of scale equates to higher productivity with lower costs. More often than not, this is where regional and smaller banks lack economies of scale.

In particular, small and midsize banks have been facing withdrawals this year. This is because savers are beginning to look for higher returns elsewhere, moving their financials to safe havens, such as JP Morgan Chase & Co.

However, Apple has been facilitating payments via its Apple Pay digital wallet since 2014, making its entry into financial product offerings more recent. Furthermore, the partnership with Goldman Sachs has enabled the tech powerhouse to improve its Apple Savings Accounts.

As a result, the service is built on the Goldman Sachs licensing framework, indicating a robust, compliant system that will drive more efficient economies of scale.

What can non-banking firms learn from Apple’s entry into the BFSI industry?

Apple’s endeavour into the BFSI industry has attracted significant money to flow into their savings account, charting a 10x higher rate than other American banks.

Its performance has been nothing short of a masterclass, maximising the potential advantages of the current banking crisis while benefiting from the cascading effects of the US banks’ failures. For instance, in under 4 days, the Apple Savings Account had already received approximately USD 1 billion in deposits.

Apple’s success in breaching the financial services space is a lesson for many non-bank firms aspiring to enter the banking industry and offer a high-yield savings account.

In short, there are 4 key lessons that non-bank firms should adopt to unlock significant growth opportunities in the BFSI industry.

- Collaboration for digital synergies

Companies should first aim to identify their strengths and weaknesses. This will help them better leverage their synergies between different companies and industries. As a result, this can lead to unique value propositions and greater digital synergies for CASA growth.

For instance, Amazon, JP Morgan Chase and Berkshire Hathaway unveiled a non-profit initiative in 2022. It aims to revolutionise healthcare for its combined 1.2 million employees. This endeavour has sparked the potential for significant change in how large companies can manage their healthcare provisions.

- Enhancing the banking experience

Similar to any industry, customer-centricity is vital for sustainability and growth. This is why non-banking firms looking to enter the banking industry should prioritise customer-centric innovation.

For instance, Apple’s suite of financial services demonstrates the simplicity and seamlessness of a mobile financial experience. Moreover, it sets the standard of what an excellent user experience can look like in financial services.

- Innovation through new business models and ecosystem integration

Non-banking firms should not be afraid when venturing into unknown territory. Instead, they should immediately explore new ways to expand its ecosystem while identifying potential strategic collaborations. These can range from how non-bank firms can better leverage their technologies to streamlining their processes for greater customer value.

For instance, Myntra can emulate the success of Alibaba and JD.com and its extensive ecosystems by partnering with PhonePe. This potential partnership with PhonePe will enable Myntra to leverage its effective networks, high customer base and quality brand image. Meanwhile, platform businesses like Uber and Airbnb should aim to expand their services in the financial space by offering loans, insurance or payment solutions.

- Focus on harnessing data-driven insights for greater personalisation

Companies should maximise their customer data, harnessing its information to drive growth. By leveraging customer data intelligently, companies can gain valuable insights into consumer behaviour, financial trends and market opportunities.

A clear example is Apple’s licensing framework, resulting from the partnership between the tech giant and Goldman Sachs.

What the future holds for Apple

Apple’s efforts to breach the banking industry have been exemplary, from its extensive roster of financial services that changes how customers pay today to its strategic partnership with Goldman Sachs to overcome the banking crisis. Block by block, Apple inches closer to building its undisputed finance empire that’s bound to disrupt the BFSI industry as we know it.

Appendix

Features of Apple savings a/c:

- Only for Apple card users

- Grow Daily Cash rewards (Apple’s name for the small cashback amounts you get for using Apple Card) with a high-yield Savings account from Goldman Sachs

- High-yield APY of 4.15 percent — a rate more than 10 times the national average. FDIC’s latest national average – 0.37% APY. Bank of America offers a measly 0.01% APY. But as Apple said its APY can change at any time.

- No opening fees

- No minimum deposits, and

- No minimum balance requirements

- Maximum balance limit of $250,000.

- Easy to set up and manage savings account directly from Apple card in wallet

- Joint account ownership is not possible.

- Individual transfers must be between $1 and $10,000. One can also only transfer up to $20,000 from the account every seven days.

- 2% cashback on every purchase with Apple Pay, and 3% on all purchases made directly with Apple.

Benefits:

- Users get more value out of their favourite Apple card benefit- Daily cash

- Helps users to lead healthier financial lives, and

- Building Savings into Apple Card in Wallet enables users to spend, send, and save Daily Cash directly and seamlessly — all from one place.

How it works:

- All future Daily Cash earned by the user will be automatically deposited into the account

- Daily Cash destination can be changed at any time

- No limit on how much Daily Cash users can earn

- Option to deposit additional funds into savings account through a linked bank account, or from Apple Cash balance

- Access to an easy-to-use savings dashboard in wallet

- Users can also withdraw funds at any time through the Savings dashboard with no fees

What you need to open and maintain an account:

- Be an owner or co-owner of an active Apple Card account and add Apple Card to your iPhone

- Be at least 18 years or older

- Have a social security number or individual taxpayer identification number

- Be a U.S. resident with a valid, physical U.S. address

- Set up two-factor authentication for your Apple ID and update to the latest version of iOS.

References

[1] The Apple ecosystem is an interconnected system of Apple-related devices, ranging from its iPhone to the Apple Watch.

[2] The Annual Percentage Yield is the real rate of return earned on an investment, while taking into account the effect of compounding interest