Top 8 key takeaways:

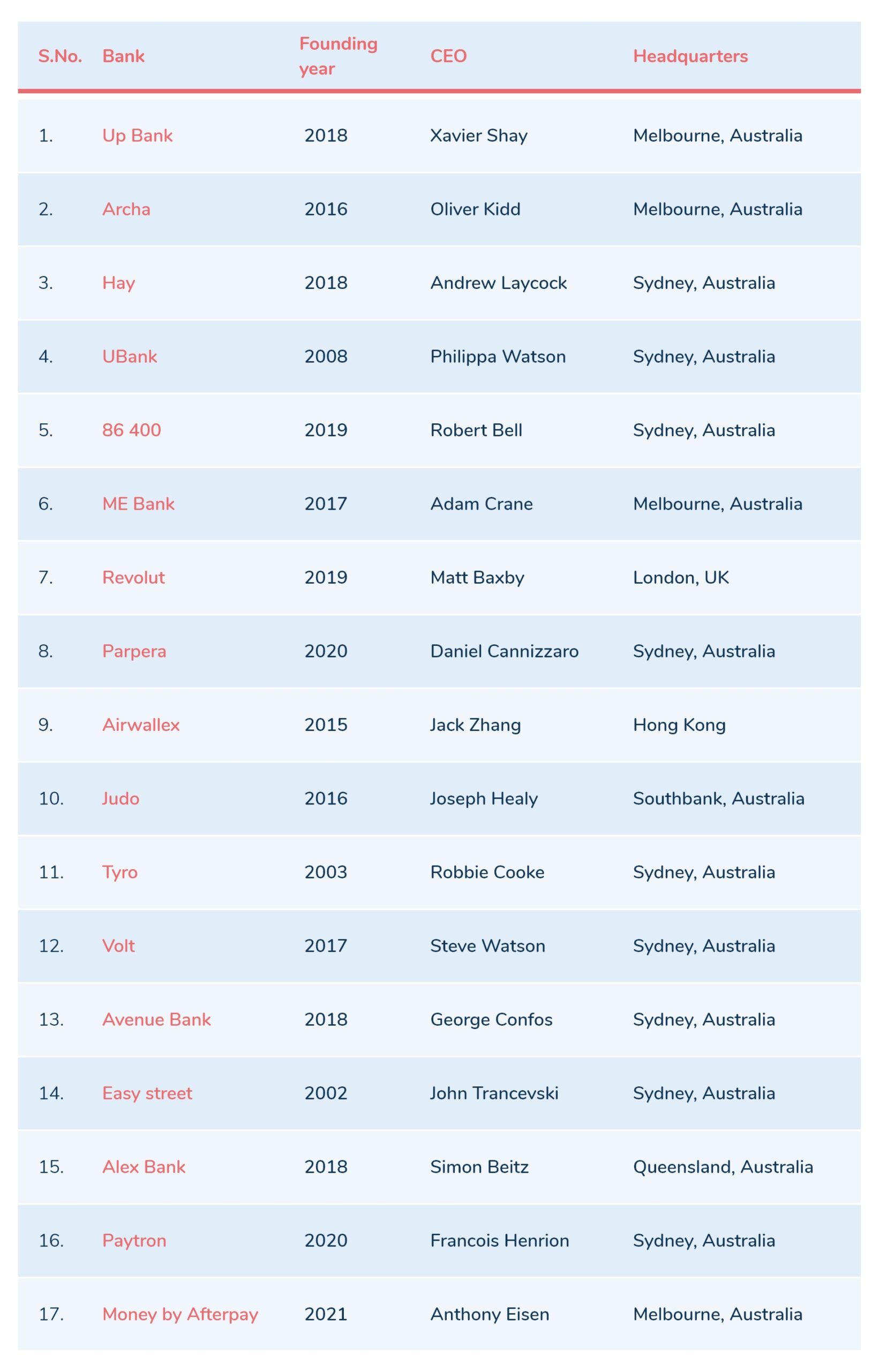

- There are 17 neobanks in Australia with a full/restricted ADI or an AFSL (Australian Financial Services License) license.

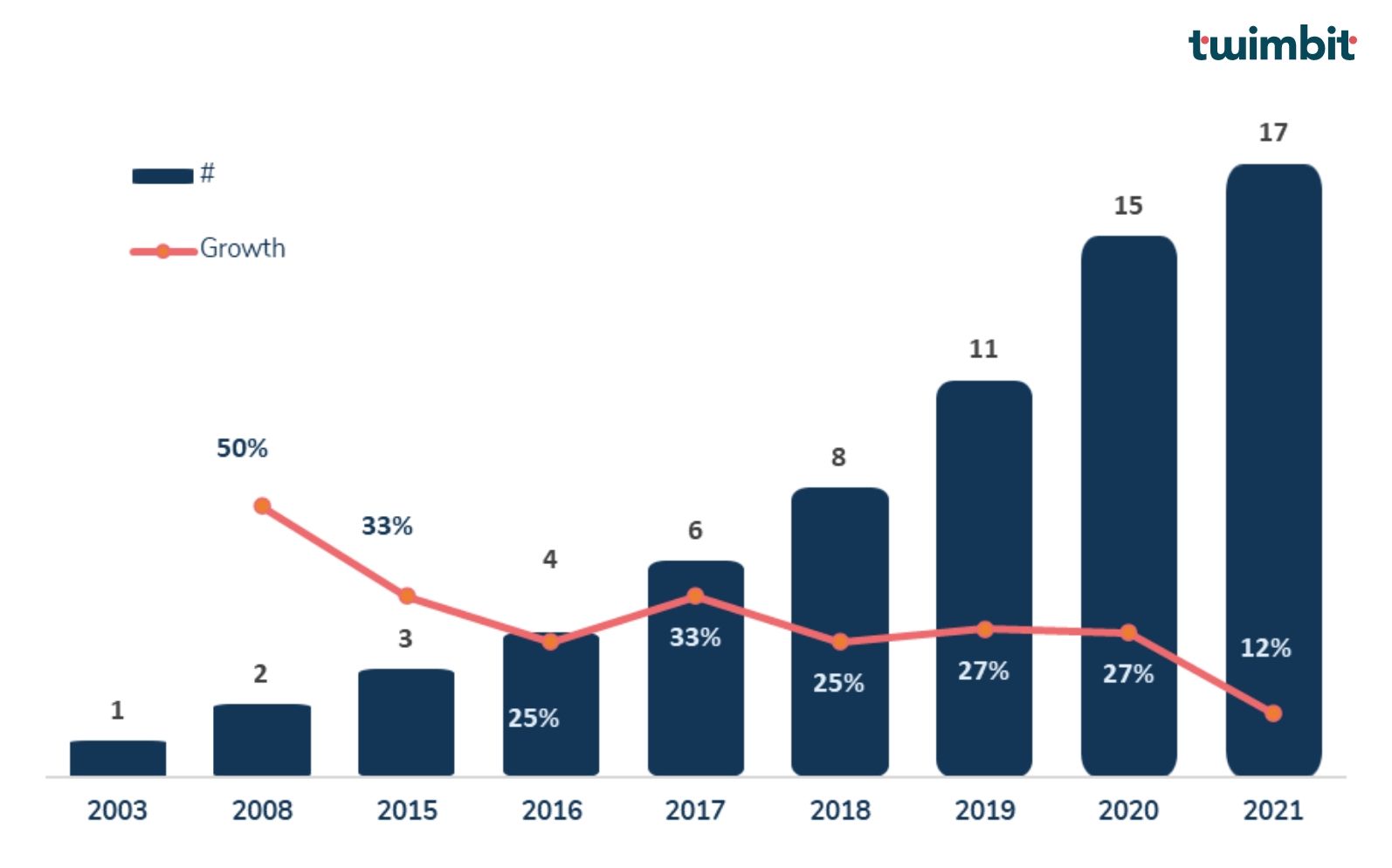

- Within the past four years, Australian neobanks doubled from 9 (2018) to 17 (2021).

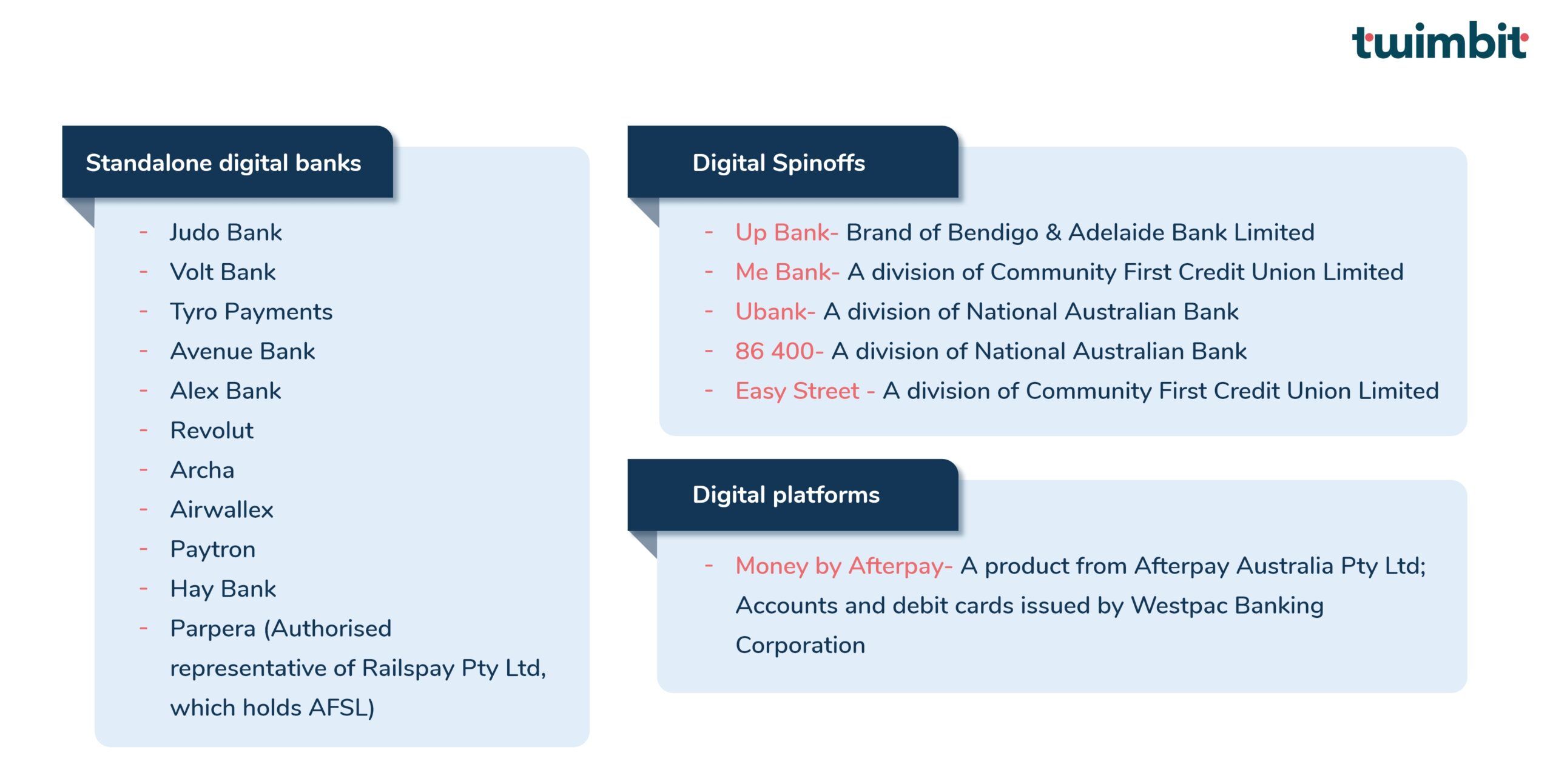

- Standalone digital banks constitute approximately 64.7% of total neobanks.

- Digital spinoff neobanks rank second at an estimated 29.4% of total neobanks.

- Digital platforms constitute approximately 5.88% of the total neobanks.

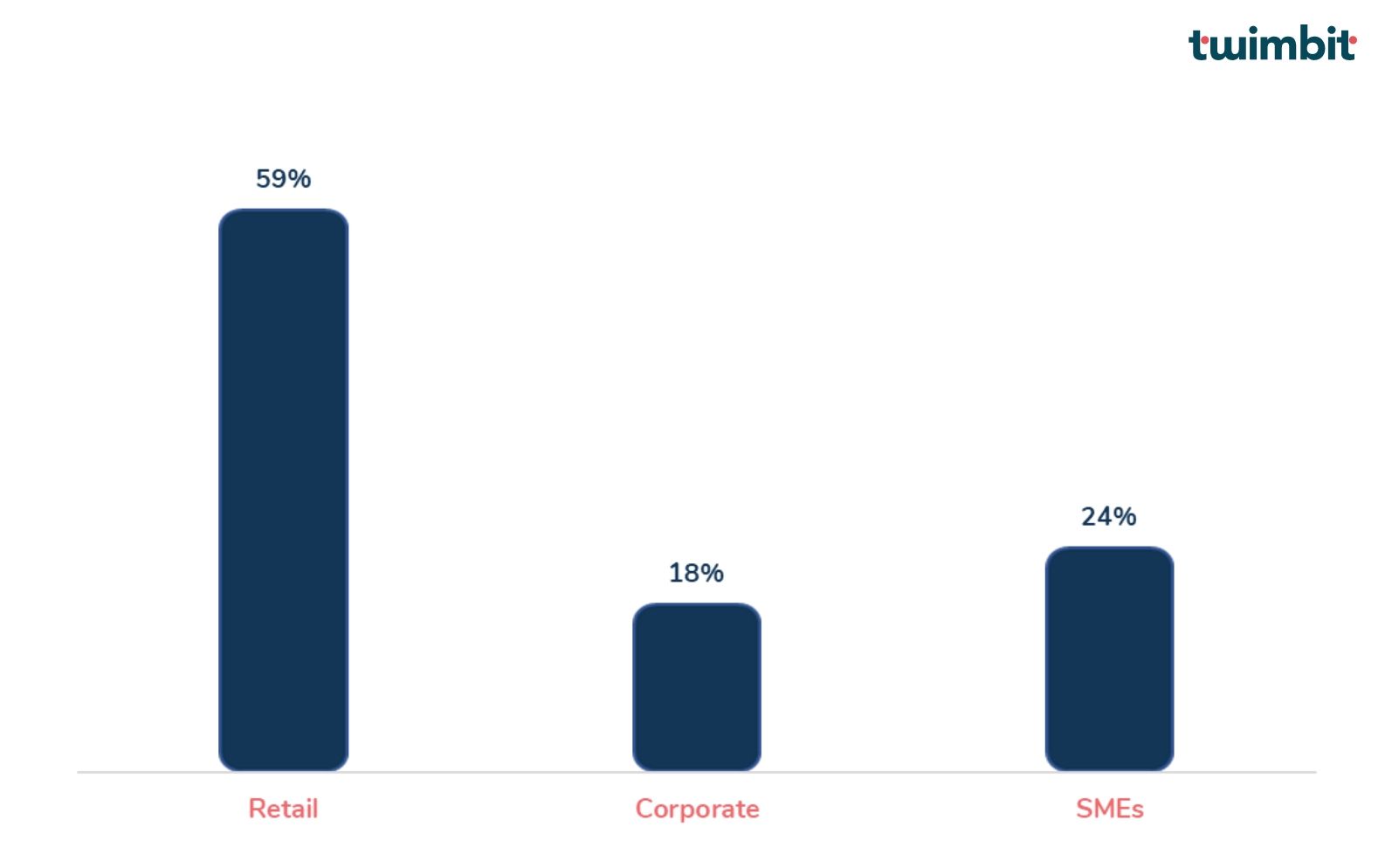

- In Australia, most neobanks focus on the retail customer segment (59%).

- Online payment services is the most popular service provided by 80% of banks, while remittance services is the least popular, with only 33% of banks providing them.

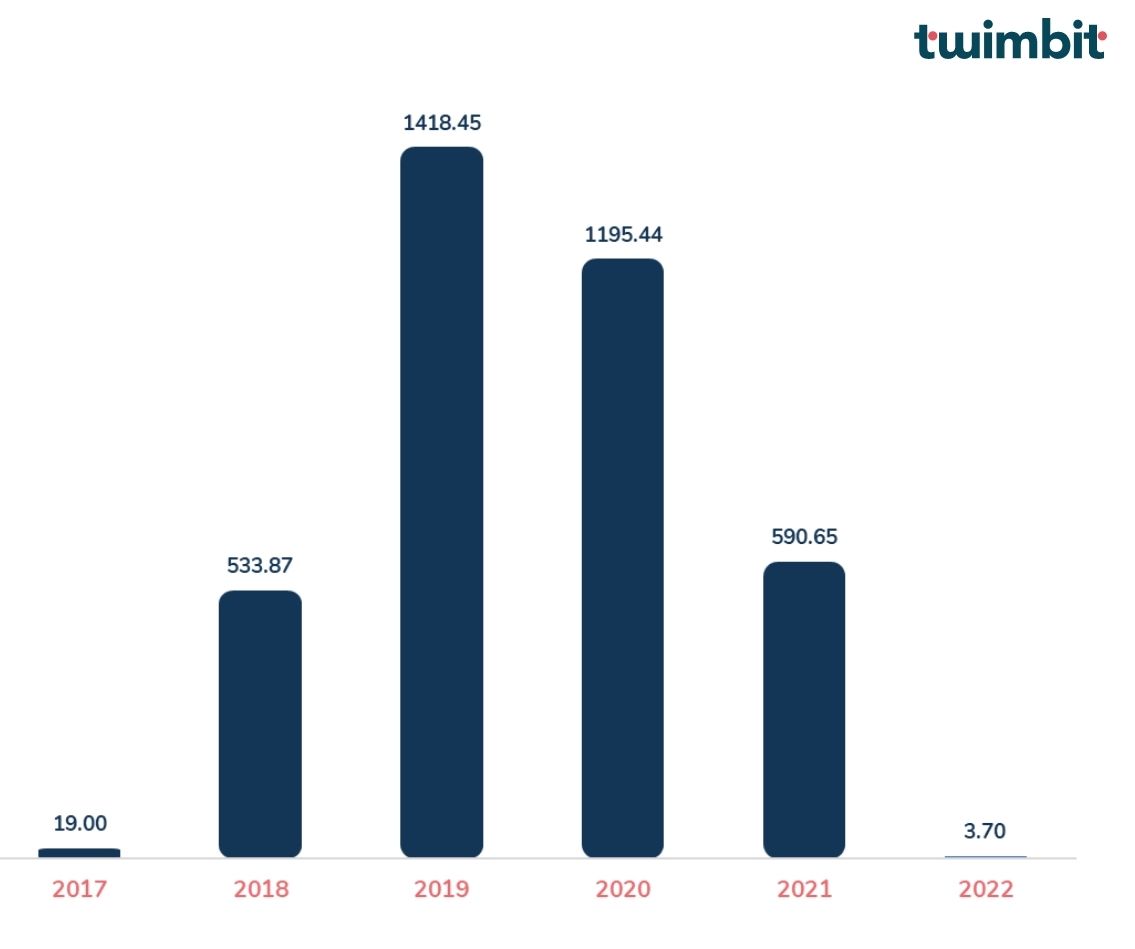

- Year 2019, saw the highest funding received by Australian neobanks amounting to about US$ 1418 Mn.

Growing regulatory scandals, uncertainty, and lack of trust in banking

Even after several years, the Australian banking industry is still reeling from the fallout of the long and tedious government-led inquiry into the sector. Whether it was Westpac’s 23 million+ breaches of anti-money laundering laws or the ANZ charging wrong fees to 3.4 million customers.

Although the Australian Prudential Regulation Authority (APRA) followed Australian Securities and Investments Commission (ASIC) in closing its investigation into WESTPAC over the AUSTRAC, traditional banks can never return to normal. To revive customers’ trust in the Australian banking and financial system, APRA introduced authorised deposit-taking institution (ADI) licenses for digital-only banks in 2018. Also, Australian regulatory authorities have significantly been receptive to the growth of new-age banking, prioritising customer data protection and complete transparency.

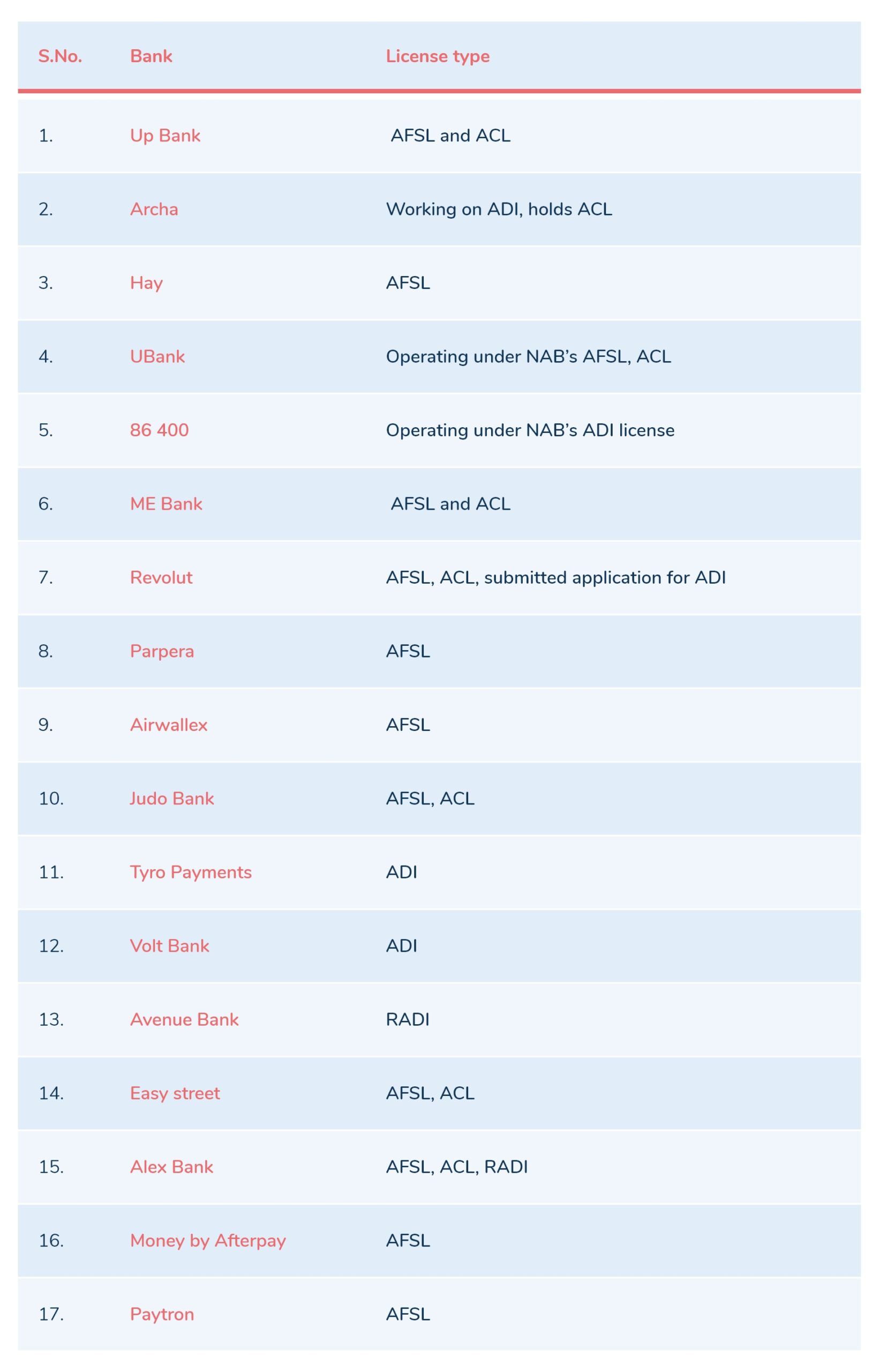

To date, there are 17 neobanks in Australia with a full/restricted ADI or an AFSL (Australian Financial Services License) license (Table 1).

Table 1: The rise of Australian neobanks

The year-on-year growth in the number of neobanks has been commendable (Graph 1). Within the past four years, Australian neobanks doubled from 9 (2018) to 17 (2021), with National Australian Bank (NAB) acquiring 86 400 and the Xinja collapse as of December 2020.

Graph 1: Growth in # of neobanks

The success of neobanks in Australia is significantly due to formal digital banking licenses. As a result, standalone digital banks are at the heart of neobanks in Australia.

- Standalone digital banks constitute approximately 64.7% of total neobanks

- Digital spinoff neobanks rank second at an estimated 29.4% of total neobanks

- Digital platforms constitute approximately 5.88% of the total neobanks

Figure 1: Types of neobanks in Australia

In Australia, most neobanks focus on the retail customer segment (59%). On the other hand, banks such as Airwallex, Judo Bank, Archa, and Parpera cater to businesses and SMEs. Yet, very few neobanks offer business-focused services.

Graph 2: Australian neobanks catering to the needs of different customer segmentation

| Retail customer segment neobanks | Businesses focused neobanks |

| Me Bank | Archa |

| Hay | Parpera |

| UBank | Airwallex |

| 86 400 | Judo Bank |

| Easy Street | Tyro Payments |

| Revolut (M) | Alex Bank |

| Douugh (M) | Avenue Bank |

| Volt Bank (M) | Paytron |

| Up Bank (M) | |

| Money by Afterpay |

Note: (M) in above table refers to millennials

Australian neobanks perform under strict regulatory guidance

Following the Xinja collapse in 2020, APRA raised the bar for all new and aspiring neobanks. It has instituted the most advanced and detailed regulatory frameworks for neobanks to launch their operations. Because of this, specific and targeted regulations help new-age banks to;

- solidify themselves in the market

- present a very clear product proposition

- develop both a sustainable and profitable business model in the long run

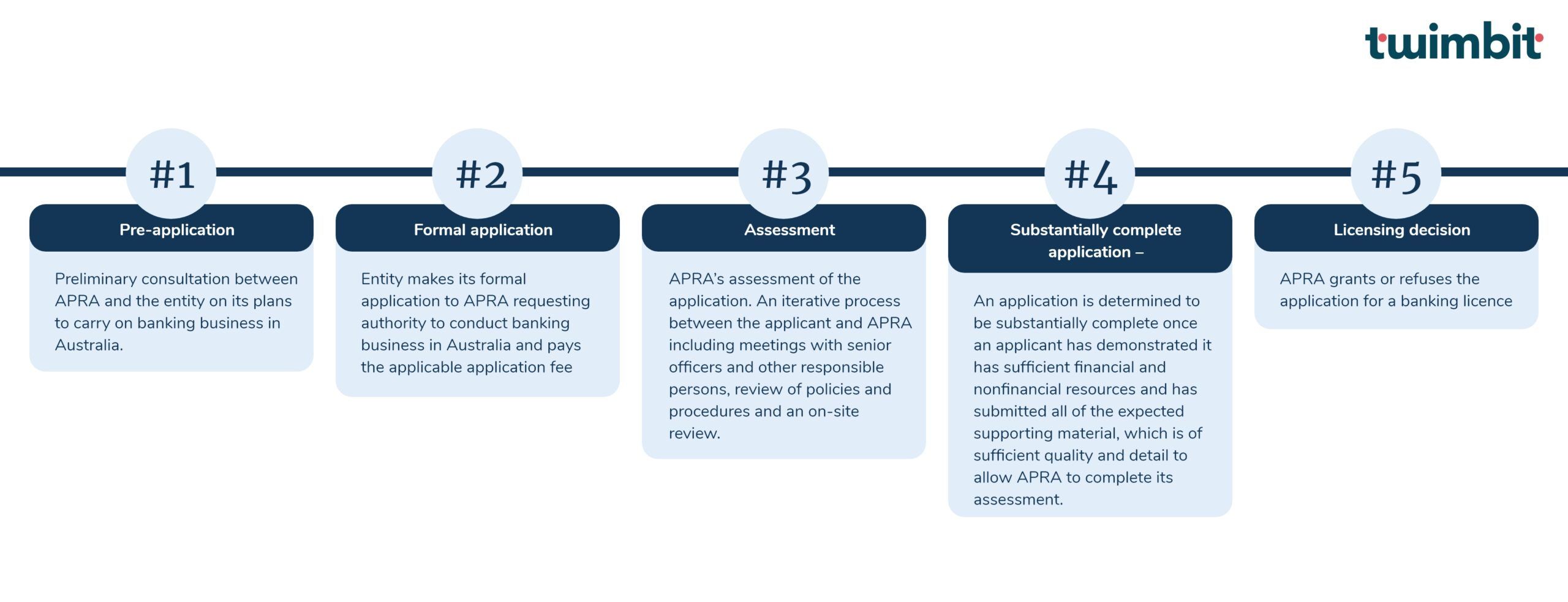

Authorised deposit-taking institution (ADI)

The APRA grants authorised ADI licenses to conduct any business governed by the ‘Banking Act 1959’. There are two pathways to the license:

Restricted ADIs: The prudential and supervisory approach of APRA to operating with a Restricted ADI license (where applicable). This pathway allows the institution to conduct limited banking operations for two years, intended to provide entities time to gather resources and capabilities to establish an ADI.

ADIs: The direct route allows the institution to conduct all banking operations and meet the requisite resources and capabilities for commencing the business. This route covers both new and established ADIs.

Following either the restricted or direct pathway to the licence, adjustments to APRA’s prudential and supervisory frameworks support building a sustainable business. APRA has also revised its approach to licensing and supervising new ADIs in 2021 (since the launch of the RADI licensing pathway in 2018).

This revised approach effectively targets key risks for new entrants, setting a higher bar for gaining a bank licence while enhancing competition by making it more likely new entrants can find their feet and gain a firm foothold in the market. New entrants will start from a stronger capital position and be ready to attract depositors and earn revenue immediately; they’ll receive additional supervisory attention from APRA until they’re firmly established; and should they ultimately not succeed, they will be better placed to exit the industry in an orderly fashion -John Lonsdale, APRA Deputy Chair, 2021

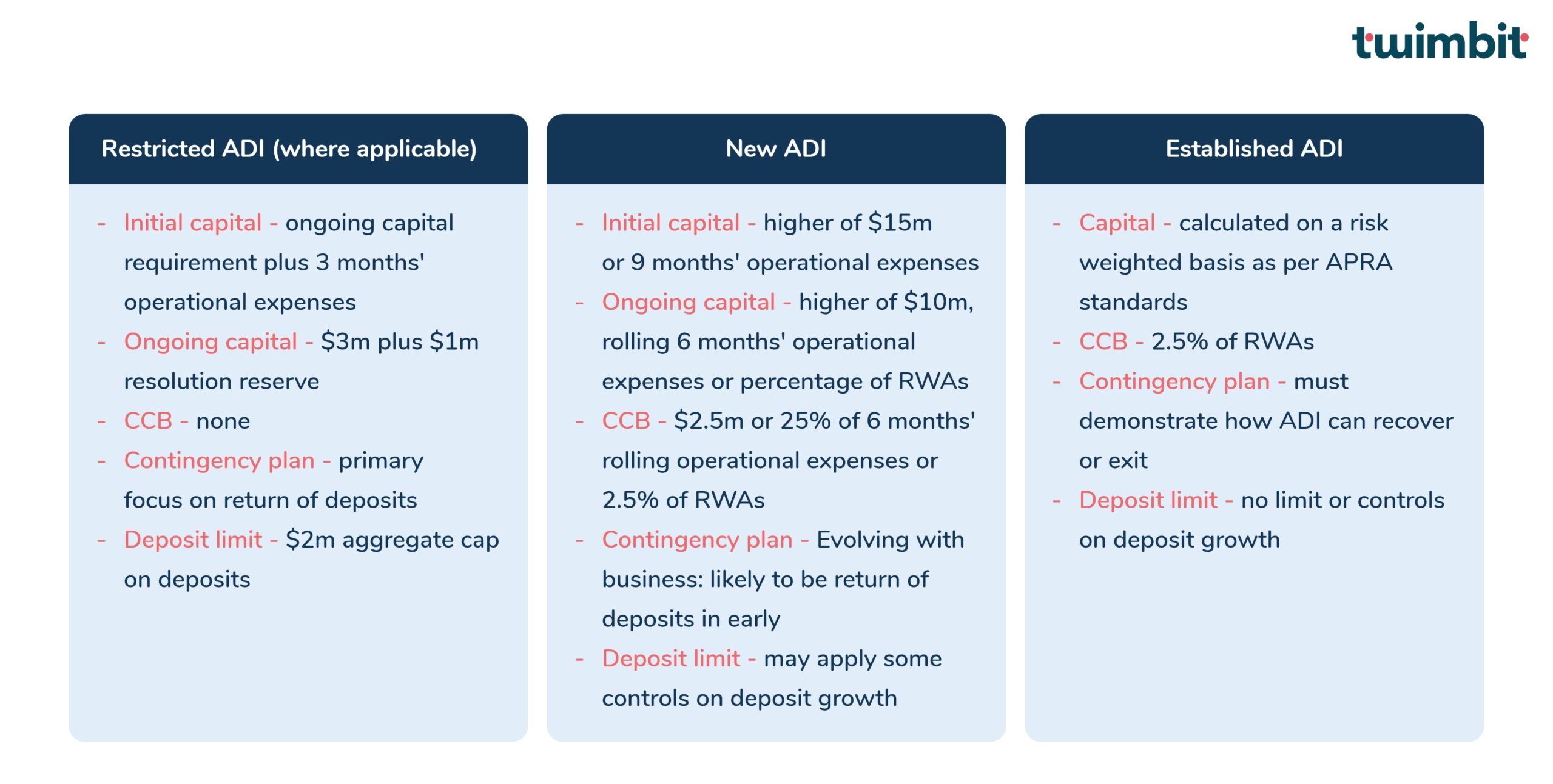

APRA’s ADI licensing approach

Table 2: Summary of key differences in applying APRA’s prudential network to each category of ADI

- To obtain their ADI license, restricted ADIs must achieve a limited launch of both an income-generating asset product and a deposit product.

- There is more clarity around capital requirements at different stages for new entrants, aimed to reduce volatility in capital levels and facilitate the transition to the methodology for established ADIs over time

- New entrants are expected to focus on deposits return as an option as part of advanced planning for a potential exit.

The new regulation covers obtaining a full banking license, a prerequisite for neobanks to garner funds from the public in Australia. The full license contrasts the APRA’s temporary, restricted credential. As of February 2021, there is one Restricted ADI on APRA’s register, while several Restricted ADIs have since transitioned to holding full ADI status since 2018 or handed back their licenses.

Australian Financial Services License (AFSL)

Australian Financial Services License (AFSL) is a license customarily required to be held by Australian businesses involved in the provision of financial services.

To be eligible for this license, the entity must:

- meet approved qualification and competency standards and/or have practical experience

- be fully sufficient in financial resources to execute the proposed business

- fulfil certain obligations as a licensee, such as training, compliance, insurance, and dispute resolution

Table 3: Neobank classification by license type

Australian neobanks can unlock a significant revenue opportunity with banking-as-a-service principles

Creating a seamless banking experience should be the top priority for Australian neobanks. Less than two-thirds (64%) of Australian banking customers agree that their primary bank’s mobile banking service permits them complete control. As a result, neobanks have a clear opportunity to rethink how they deliver products and services to capture a good proportion of the market segment. It is no longer about communicating with your customer in plain terms but seamlessly integrating banking services into their lives.

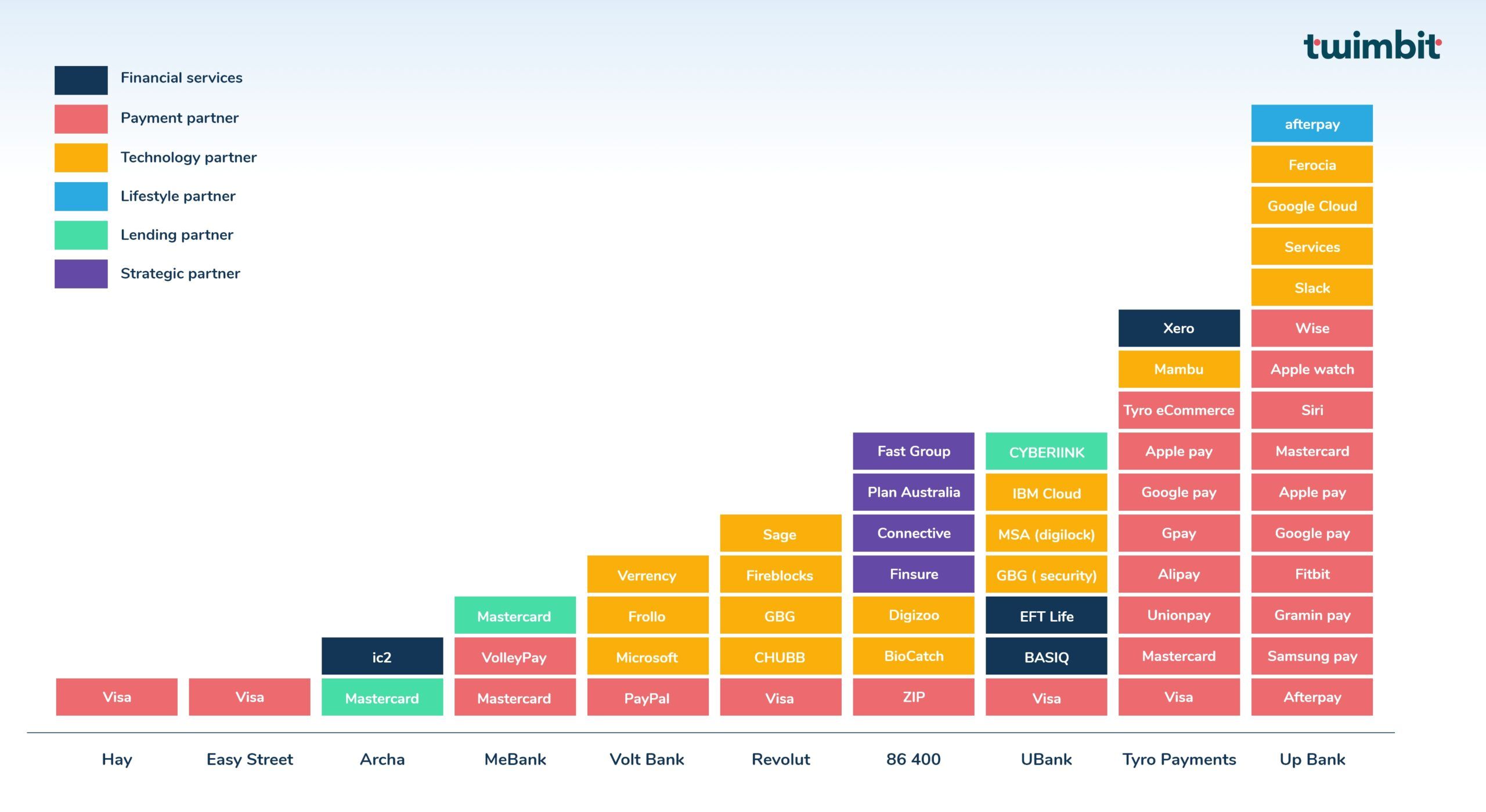

Additionally, providing top-state-of-the-art products and services must be a top priority for Australian neobanks. For this, partnering to create a strong ecosystem is vital. Most neobanks have built partner ecosystems to drive product efficiency and differentiation on their platform. It also acts as a revenue strategy for banks to earn fees from third-party service providers. To emphasise, we charted an illustrative list of partners these virtual banks are working with to expand revenue streams (Figure 2).

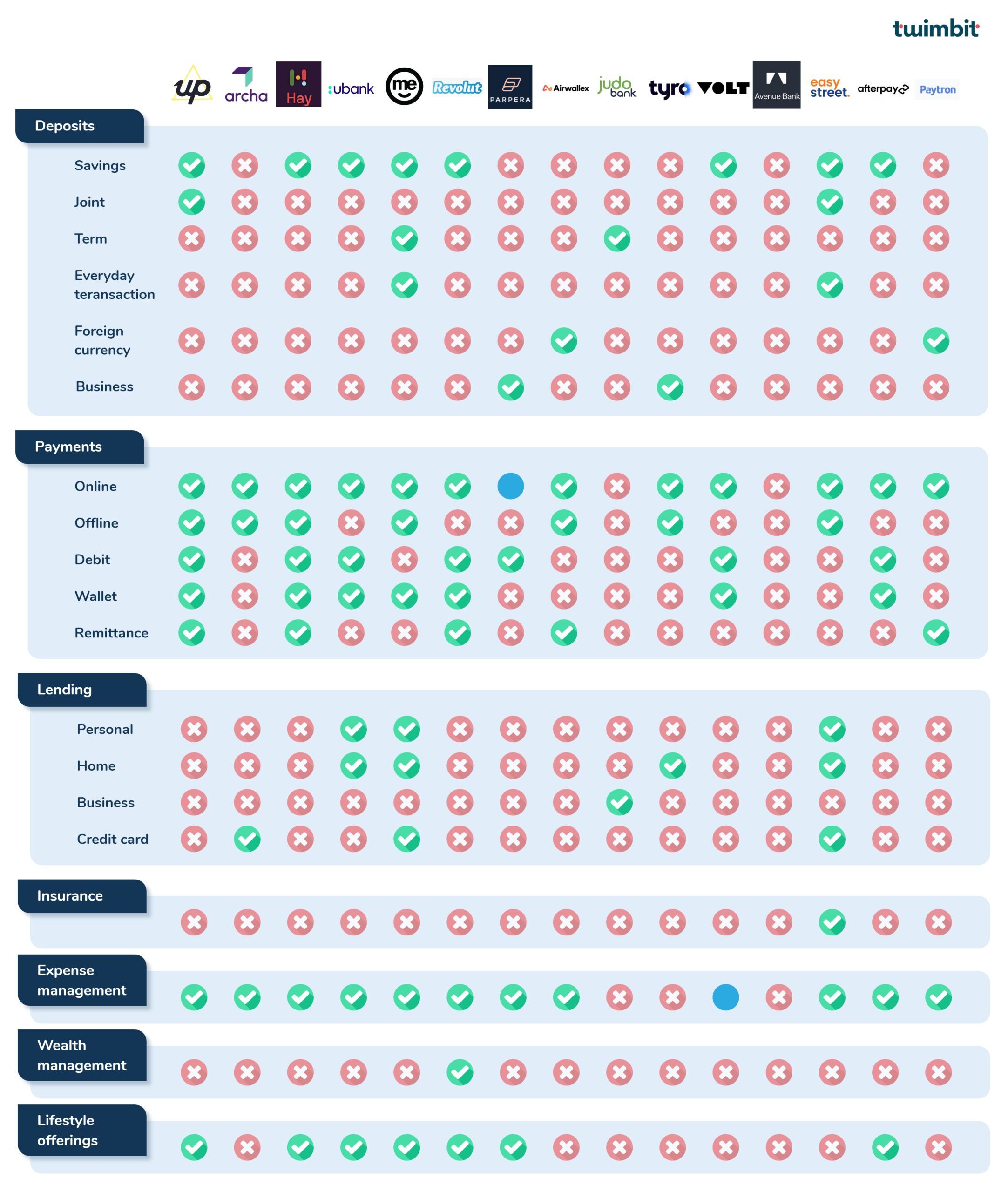

- Only Easy Street and Me bank provide three different types of deposit services, while the rest provide two or less than two types of deposit services

- Archa and Avenue bank are the only two banks that do not provide any deposit services

- 87% of banks are providing payment services in one way or another

- Judo Bank and Avenue Bank are the only two banks that do not provide any payment services

- Online payment services is the most popular service provided by 80% of banks, while remittance services is the least popular, with only 33% of banks providing them

- Easy Street is the only bank that provides insurance services, while Revolut is the only bank that provides wealth management services

Figure 2: Neobanks partner ecosystem

Product portfolio for Australia neobanks

Service offerings, viz, product stack of the neobanks is broadly classified into 10 distinct sub-categories for easy understanding and analysis.

Up Bank and Hay Bank deliver all five payment services (Figure 3). However, only Easy Street provides insurance services, whereas Revolut only offers wealth management services.

Figure 3: Product stack of 15 neobanks in Australia

Neobanks struggle to maintain profits and funding shrinks

Rising inflation and interest rates make it difficult for digital-only banks to compete with incumbents. Investors have favoured more established entities in this challenging environment, making fundraising for neobanks difficult.

After the recent downfall of Volt, Australian fintech investors and operators have warned incumbent banks that it is too early to celebrate the fall of the neobank wave. Agile start-ups still have much to do in order to compete with larger rivals.

Top 3 most funded neobanks in Australia

| Name | Funding amount (in USD) |

| Judo Bank | 1847.93 Mn |

| Airwallex | 1699 Mn |

| Tyro Payments | 96.18 Mn |

Neobanks can expect a substantial influx of funding to come. By far, the highest funding received was of US$ 1418 Mn in year 2019.

Graph 3: Year-wise funding (values in USD million)

Note: Year-wise funding in 2015 was USD 73 million, whereas no funds were raised during 2016.

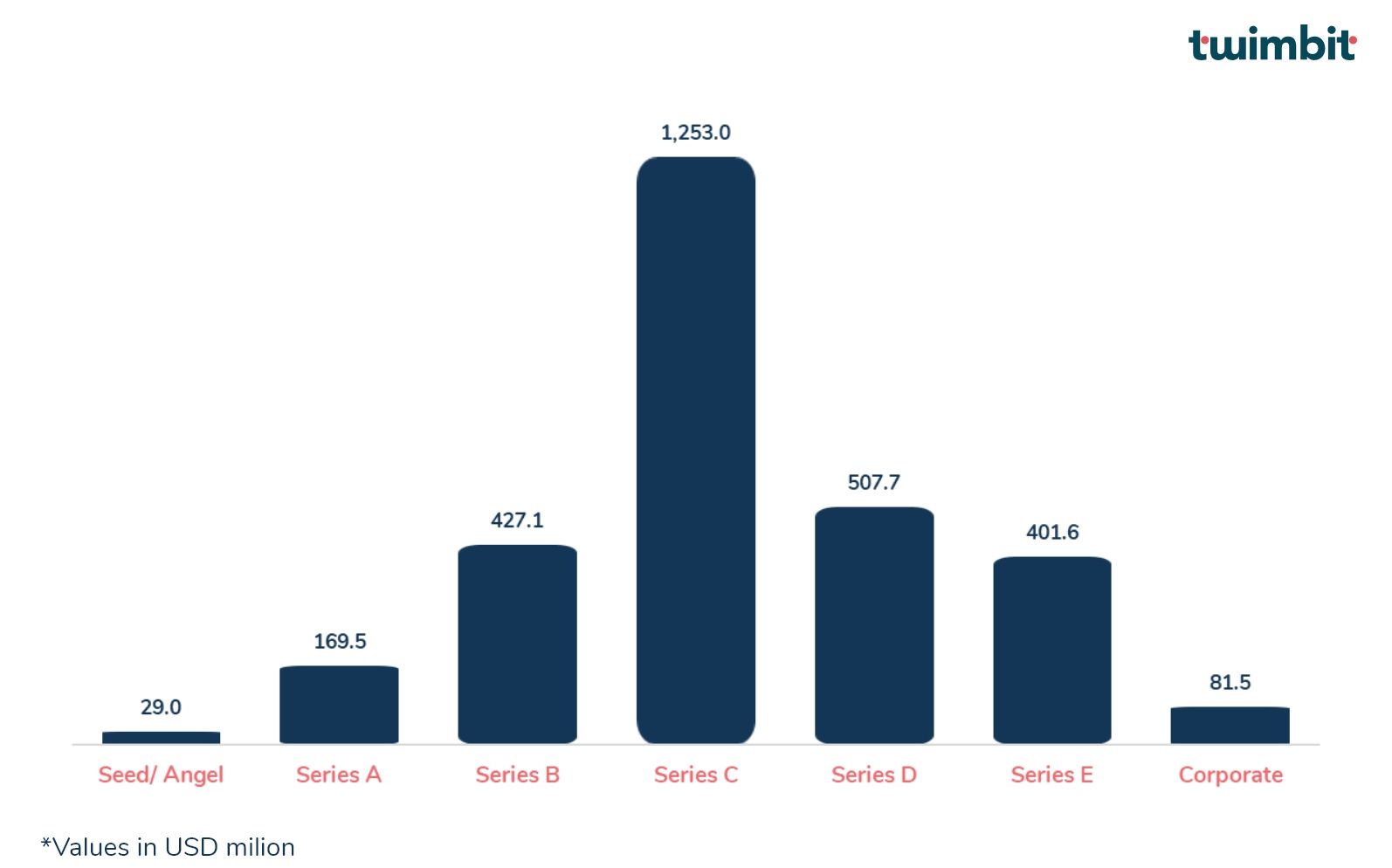

Based on each round, the maximum amount of funding (by value) flows in mid-rounds such as Series C.

Graph 4: Series-wise funding

Challenges and future outlook

Undoubtedly, Australia’s major banks face significant competition as technological change sweeps the financial world and new competitors target the industry’s high profits.

The APRA granted ADI licences to three start-up banks in 2019:

- 86 400

- Volt

- Xinja

They follow in the footsteps of UK digital banks that have developed a significant market niche. However, Xinja’s abrupt exit and NAB’s plan to buy 86 400 have highlighted the challenges that neobanks face. Simultaneously, equity markets place huge valuations on fintech firms that compete with banks for customers while purposefully avoiding the industry’s regulatory and capital demands — the most visible and local example being Afterpay.

Australia’s neobanks need to find new profitable products and consistent revenue streams to make a dent in a market dominated by existing lenders. The remaining neobanks and potential new entrants will need to be more innovative to survive.

Neobanks can start focusing more on younger customers willing to adopt digital services. Moreover, neobanks promote easy, real-time or purely digital lending and account opening, which many banks in Australia currently struggle with. Other products that neobanks could offer include spending analysis, foreign exchange and travel money without the markups seen at more traditional banks.

It has become clear that successful neobanks do not necessarily need their own banking licence to compete. Given the high costs and stringent capital requirements of being a licensed bank, more challenger banks can rent a license from smaller players such as regional banks, viz. the partnership between Up Bank and Bendigo. Other challenges for Australian neobanks lie in competing with major banks that have heavily invested in technology and digital channels.

Despite these obstacles, fintechs such as Revolut from the UK still aim for a banking license in the long run. However, it has initially focused on niches such as foreign exchange or cryptocurrency trading. Business-focused Judo Bank has also raised capital and increased its market share.

Regardless, the big four banks (ANZ, NAB, CBA and Westpac) are preparing to compete with their new rivals. Also, the CBA indicates an increase in technology spending. The banks’ aim – protect their profitable businesses from all potential challengers, including neobanks. Overall, the neobanking model’s future is to monetise its customers.

ANNEXURE

Funding details per neobank:

86 400

| Round | Year | Amount | Total funds raised |

| Series A | 2020 | USD 24.08M | USD 24.08M |

Note: NAB was acquired for AUD 220 Million in May 2021. Consolidation of 86 400 with UBank as both are operating under NAB.

Douugh

| Round | Year | Amount | Total funds raised |

| Seed round | 2016 | USD 1.2M | |

| Seed round 2 | 2017 | USD 1.4M | |

| Corporate round | 2021 | undisclosed | USD 2.6M |

Airwallex

| Round | Year | Amount | Total funds raised |

| Series A | 2017 | USD 13M | |

| Series A | 2017 | USD 6M | |

| Series B | 2018 | USD 80M | |

| Series C | 2019 | USD 100M | |

| Series D | 2020 | USD 160M | |

| Series D | 2020 | USD 40M | |

| Series D | 2021 | USD 100M | |

| Series E | 2021 | USD 200M | |

| Series E | 2021 | USD 100M | USD 802M |

Judo Bank

| Round | Year | Amount | Total funds raised |

| Series A | 2018 | USD 102.4M | |

| Debt financing | 2018 | USD 350M | |

| Debt financing | 2019 | USD 100M | |

| Series B | 2019 | USD 292.5M | |

| Debt financing | 2020 | USD 500M | |

| Series C | 2020 | USD 168.2M | |

| Series D | 2020 | USD 207.7M | |

| Debt financing | 2021 | USD 36.5M | |

| Venture round | 2021 | USD 90.6M | USD 1.8B |

Volt Bank

| Round | Year | Amount | Total funds raised |

| Corporate round | 2019 | USD 8.5M | |

| Series C | 2020 | USD 70M | |

| Series E | 2021 | USD 10.9M | USD 89.4M |

Tyro payments

| Round | Year | Amount | Total funds raised |

| Angel round | 2006 | USD 5.8M | |

| Angel round | 2007 | USD 280.7K | |

| Angel round | 2007 | USD 3.5M | |

| Angel round | 2007 | USD 2.1M | |

| Angel round | 2008 | USD 1.1M | |

| Angel round | 2008 | USD 3.9M | |

| Angel round | 2009 | USD 3.7M | |

| Angel round | 2011 | USD 2.7M | |

| Venture round | 2015 | USD 73M | |

| Secondary Market | 2019 | – | USD 103.9M |

Alex Bank

| Round | Year | Amount | Total funds raised |

| Seed round | 2018 | USD 1.5M | |

| Series A | 2019 | USD 9.9M | |

| Series A | 2019 | USD 7.3M | |

| Series A | 2020 | – | |

| Series A | 2020 | USD 2.6M | |

| Series B | 2020 | USD 13.4M | |

| Series B | 2020 | USD 7.4M | |

| Series B | 2021 | USD 5.9M | |

| Series C | 2021 | USD 14.6M | USD 62.6M |

Parpera

| Round | Year | Amount | Total funds raised |

| Equity crowdfunding | 2020 | USD 800K | |

| Seed round | 2021 | USD 949K | USD 1.7M |

Investors:

| Name | Investors |

| Airwallex | Lone pine capital, Greenoaks, Skip Capital, DST Global,Salesforce Venture, Sequoia Capital, Square Peg Capital, Tencent, Mastercard |

| Judo Bank | Credit Suisse, Goldman Sachs, Australian Office of Financial Management, SHAREHOLDERS – Bain Capital Credit, Myer Family Investments, the Abu Dhabi Capital Group, Ironbridge, SPF Investment Management, OPTrust and Tikehau Capital. |

| Volt Bank | Australian Finance Group, Collection House Group |

| Tyro Payments | Tiger Global Management, Ellerston Capital, TDM Asset Management, Mike Cannon Brookes |

| Alex Bank | Clinton Capital Partners, Washington H. Soul Pattinson, Regal Funds Management, Wunala Capital, and SG Hiscock & Company |

| Avenue Bank | Liberty Financial Group |

| Archa | BW Equities and Lazarus Corporate Finance. |

| Hay | Regal Funds Management |

| Parpera | Equitable Investors |

| Douugh | Monex Group |

| 86 400 | Morgan Stanley, now parent company is NAB |