The banking industry is witnessing tremendous growth and innovation with banks becoming digitally-relevant and forward, unlocking incredible opportunities. In our recent twimbit Open House, we uncovered disruption-causing factors and came up with 9 innovation opportunities to define the bank of tomorrow.

The key takeaways were that the banks need to:

- Increase cost efficiency

- Adopt one of the three distinct models of platformification

- Embrace virtual branch experiences

- Value of digital ecosystem is the new measure of success

- Exceptional employee experience is a must

To get a deeper understanding, find our presentation below.

Atif – Hello everyone, it’s great to be here, and today we are talking about the Bank of tomorrow and the 9 innovation opportunities. I am Atif!

Shrestha – Hi, I am Shrestha and together at twimbit, we studied over 40 top banks in the Asia-Pacific region from China all the way to Australia. We studied their performances, we looked at what made them successful and what challenges they faced and based on that, we have come up with 9 innovation opportunities that the banks can leverage to become the Bank of tomorrow.

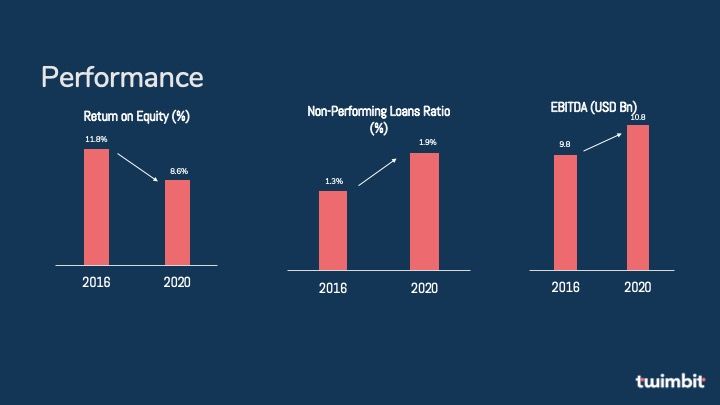

Atif – But before that, let us see how the banks have been performing up till now. Over the last five years, return on equity has declined, non-performing loans have increased from 1.3% to 1.9%, and some of this may be due to the COVID pandemic. Operating revenue has increased 4.5%, while EBITDA has only increased by 1%.

Atif – Overall, we have witnessed a huge transformation in the financial services industry, and we are yet to unlock a US$10 trillion consumption growth in Asia over the next decade.

Shrestha – Well, Atif, don’t you think the banks have kept innovation at the backfoot, but now is the time to transform. But I think they might face stiff competition from a new breed of fintechs as well as the global technology giants.

Shrestha – So, how will they stay relevant and ensure sustainable growth till the end of the decade? Will they be marginalised from the innovation just like the telecom service providers missed the opportunities with the internet businesses?

Atif – So, what does the future look like? What will be the Bank of tomorrow? To understand the Bank of tomorrow, let’s go in the future to 2030.

Bank of Tomorrow

Shrestha – Let us shift gears and take the role of Jenny and Ron.

Shrestha – Hi! I am Jenny, your employee experience manager, and I help employees get the best out of them and support the growth of the bank.

Atif – And I’m Ron, the customer experience manager. My goal is to make every customer experience an absolutely frictionless and efficient one. And together, we will tell you the story of how banks have completely transformed themselves.

Atif – Jenny, 2021 had us facing changes, and in order to survive, we had to choose between the three strategic choices and adopt one of the three distinct models to become as we are today. These included bank as a utility, deep expertise bank, and financial supermarket.

Shrestha – For us to realise this vision of the bank of tomorrow, we focused on these 9 innovation opportunities.

Shrestha – But Ron, how did that go?

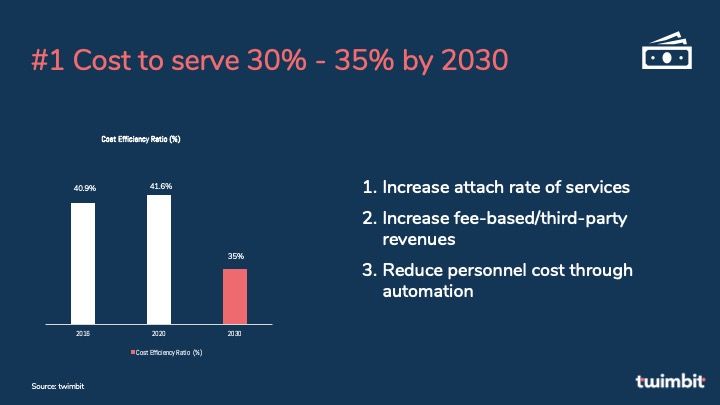

Atif – Jenny, let’s begin with the first one – cost-efficiency became extremely critical to sustaining long-term profitability. The cost-efficiency went over 40% for most banks in Asia in 2020, and we were able to bring this down to 35%; this also helped us improve our return on equity and interest margins.

Atif – We achieved this through increasing our attach rate of services, increasing our non-interest income, and reducing our personnel cost through automation, i.e., us.

Atif – So what’s next, Jenny?

Shrestha – We changed the branch experience that we provided to our customers, and we did this by transforming ourselves and creating virtual branches. This is where we came into the picture and brought the bank on the fingertips of the customers, without the need for them to leave their houses.

Shrestha – But Ron, how did we measure success?

Atif – Well Jenny, the Bank of tomorrow instated new success measures of customer experience.

Atif – Digital engagement value measured the success of how I engaged and sustained my customers in the long run.

Atif – Digital efficiency value measured the operational success of serving the day-to-day needs of my customers.

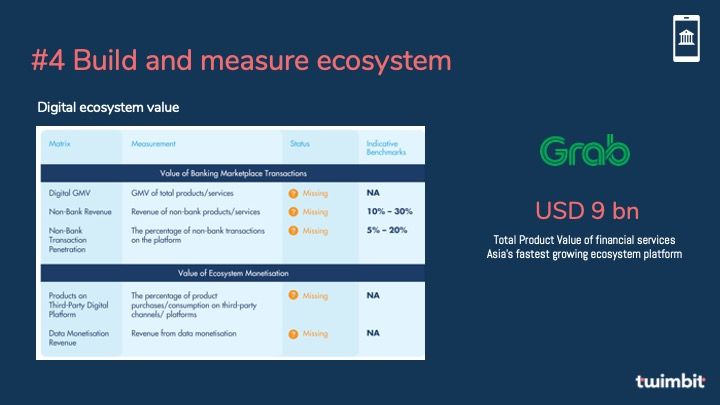

Atif – Hey Jenny, how did we unlock the value of the growing ecosystem around us?

Shrestha – Ron, we did so by evaluating the value of banking marketplace transactions and monetising our ecosystem by increasing our third-party portfolio and revenue from non-bank sources.

Shrestha – Did you know, in 2020, one of our fintech partners, GRAB, became Asia’s fastest-growing ecosystem platform by serving USD 9 BN worth of total product value of financial services.

Atif – While we did all this, the central pillar of success lies with you, Jenny, by driving exceptional employee experience.

Shrestha – That’s true Ron, and why I say this is because exceptional growth is achieved if you create and support digitally forward and relevant organisation. I think one of the best decisions that we made was to invest in employee experience and transform end-to-end employee journeys. In fact, DBS ranked at number 1 among the banks to achieve exceptional employee experience.

Atif – Well, the story doesn’t end here.

Shrestha – That’s right! We invested a lot in ICT, which grew at a rate of 13.9%. The reason is that we wanted to build the Bank of tomorrow on a scalable foundation through Cloud.

Shrestha – With the changing behavioural dynamics and the rise of the GenZ and millennial population, we leveraged the opportunity of BNPL.

Shrestha – We improved our intelligence about customers, employees, products, and operations through AI.

Shrestha – Finally, we gave back to the society, empowered communities, and promoted sustainable green financing for success.

Atif – Well, this is Ron and Jenny signing off, and we will e-meet you again as you visit our Bank of tomorrow.

Shrestha – Thank you, and gain more insights on the Bank of tomorrow by scanning the code below and subscribe to our twimbit insights.