People.. were poor not because they were stupid or lazy. They worked all day long, doing complex physical tasks. They were poor because the financial institution in the country did not help them widen their economic base. – Muhammad Yunus, Founder- Grameen Bank, Bangladesh

Introduction

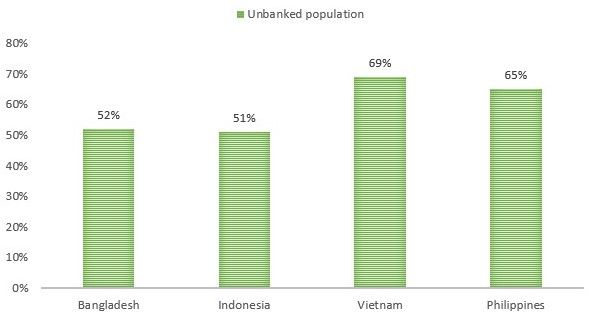

The fulfilment of financial inclusion is still far in this rapidly changing and exponentially growing 21st century. While there is a segment of the society accessing new-age developments like Use now-Pay later and Digi-cards, there is a segment still struggling to even have their own bank account. This inability to open a bank account is reducing their means to have savings, make investments, and obtain credit. What is concerning here is that the latter constitutes a majority of the population in various countries of the Asia Pacific region. (Figure 1)

Figure 1: Country-wise split of unbanked adults as a percentage of total adults, 2017-2018

Source: The World Bank, Twimbit analysis

The need for financial inclusion

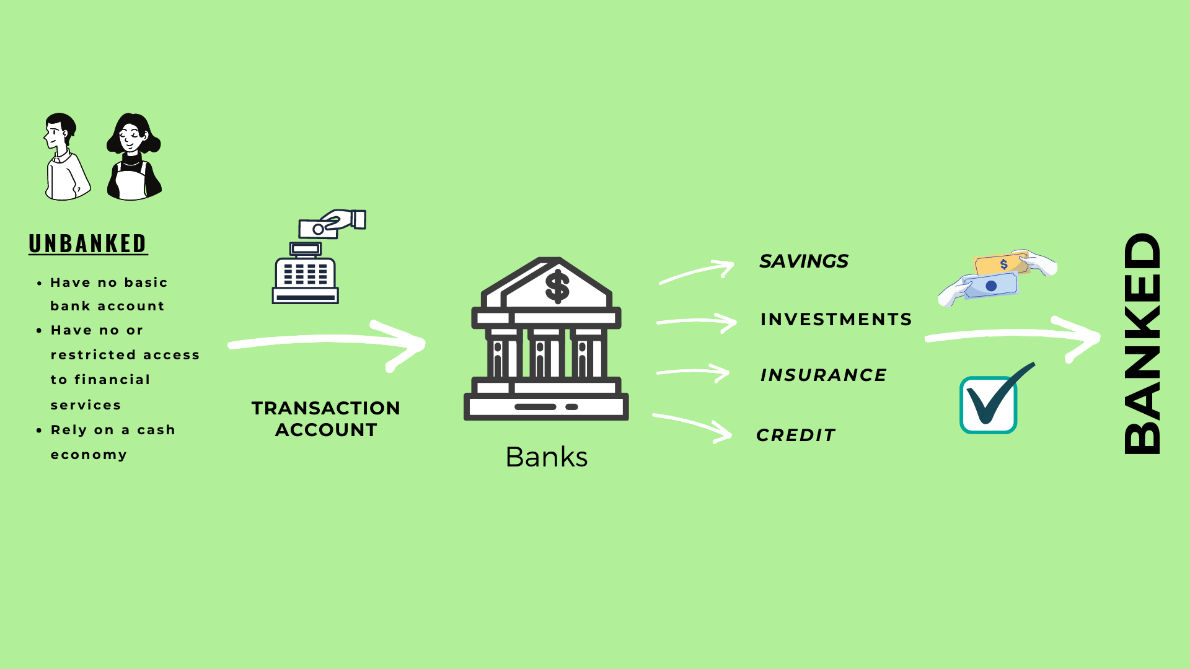

Opening a bank account is the first step toward financial inclusion as it uplifts the unserved and underserved segments in four key ways:

- Savings open doors to good education and lifestyle

- Investments enable a secure future

- Insurance gives access to better healthcare, vehicle protection, and electronics

- Credit helps grow businesses and increases personal well-being

Figure 1: Financial Inclusion Gateway

To understand how banks can drive financial inclusion, we conducted a detailed research on 30 banks spanning Asia Pacific countries. Based on our research, we have a learning list of ten banks that are successfully achieving financial inclusion in their respective country of business. While these banks continue contributing toward uplifting the society, others can learn, ideate, and apply similar practices.

Selection Criteria

In selecting the top 10, we identify banks that have a legacy and a unique financial inclusion strategy, demonstrating evidence of success.

Inclusion

We have set four board criteria to determine the top 10:

- Economic impact: Operational success was measured by the number of customers served, numbers of accounts operated, FI accounts (if any), FI loans, etc.

- Environmental impact: Market penetration and presence

- Technological impact: Digital adoption and dispersion

- Social impact: financial inclusion strategies, literacy drives, and lives impacted

Exclusion

For this research, we have excluded political and legal impact which supports or opposes the enablement of financial inclusion in a country.

Top 10 bank enabling financial inclusion in Asia Pacific (In alphabetical order)

| Agricultural Bank of China (ABC), China |

| Bank highlights |

| Bank BRI, Indonesia |

| Bank highlights |

| Dutch Bangla Bank, Bangladesh |

| Bank highlights |

| Grameen Bank, Bangladesh |

| Bank highlights |

| HDFC Bank, India |

| Bank highlights |

| ICICI Bank, India |

| Bank highlights |

| India Post Payments Bank, India |

| Bank highlights |

| Postal Savings Bank of China, China |

| Bank highlights |

| Punjab National Bank (PNB), India |

| Bank highlights |

| State Bank of India (SBI), India |

| Bank highlights |

5 factors hindering inclusion

Individuals either choose or are forced to stay unbanked. Our research shows that there are five key reasons for Asia-Pacific’s unbanked population.

- Level of wealth

- Financial illiteracy

- Know-your-customer remediation

- Conservatism

- Inaccessibility and dependency

Their reasons can vary but, in the end, they all lose the same thing. They lose an opportunity: an opportunity to save, an opportunity to invest, and an opportunity to grow.

6 key actions to drive financial inclusion

6 key teachings we derive from our analysis of the aforementioned ten banks driving financial inclusion, to help other banks promote and imbibe them as a growth opportunity, are:

- Conduct financial literacy drives to educate individuals on the know-how, and the benefits of banking.

- Create a kiosk banking model to build touchpoints in rural areas and remote locations.

- Embrace agent banking or a business correspondent model of banking to enable door-to-door and network-based banking based on trust and security.

- Give access to hassle-free loans and bite-size low-cost loans to meet the specific needs of an individual.

- Invest in mobile banking applications supporting vernacular languages to increase digital adoption.

- Partner with telecom, social media companies and fintech companies, such as Paytm, Grabpay, Alipay to reach out to mass customers and understand customer behaviour.

I dream of a Digital India where mobile and e-banking ensures financial inclusion – Shri Narendra Modi (Prime Minister, India)