Introduction

Maintaining reputable customer service and experience is key to sustaining a concrete competitive advantage in the highly dynamic and digitally evolving banking industry. Leading APAC banks are growing their ICT spend at a CAGR 14.6% in the last 10 years, exceeding USD 23 Bn 2021 to continuously enhance their digital capabilities and orchestrate frictionless experiences1.

The value creation now lies in the cultivation of hyper-personalised and frictionless digitalised experiences. Delivering exceptional customer experiences begin right at the need for a bank account, identifying the types to opening the account and transacting. For many banks, understanding onboarding efficiency and how that improves customer acquisition and retention is essential with the growing competition from platform-based neobanks in India.

In this report, the twimbit analyst team helps Chief Executive Officers (CEO), Chief Experience Officers (CXO), Chief Product Officers (CPO), Chief Marketing Officers (CMO), and business leaders of banking industry like you understand the importance of creating a customer-centric journey. We outline the top initiatives taken by leading Indian banks in four customer experience benchmark parameters, going across three customer experience milestones to build long-term relationships.

Methodology

- STEP 1

We opened real accounts and enrolled for the basic saving account as well for instant digital account with India’s top 10 private and public banks – Kotak 811, HDFC, ICICI, Axis, IndusInd, SBI, Canara, BOB, PNB and Union bank- during November to December 2021.

- STEP 2

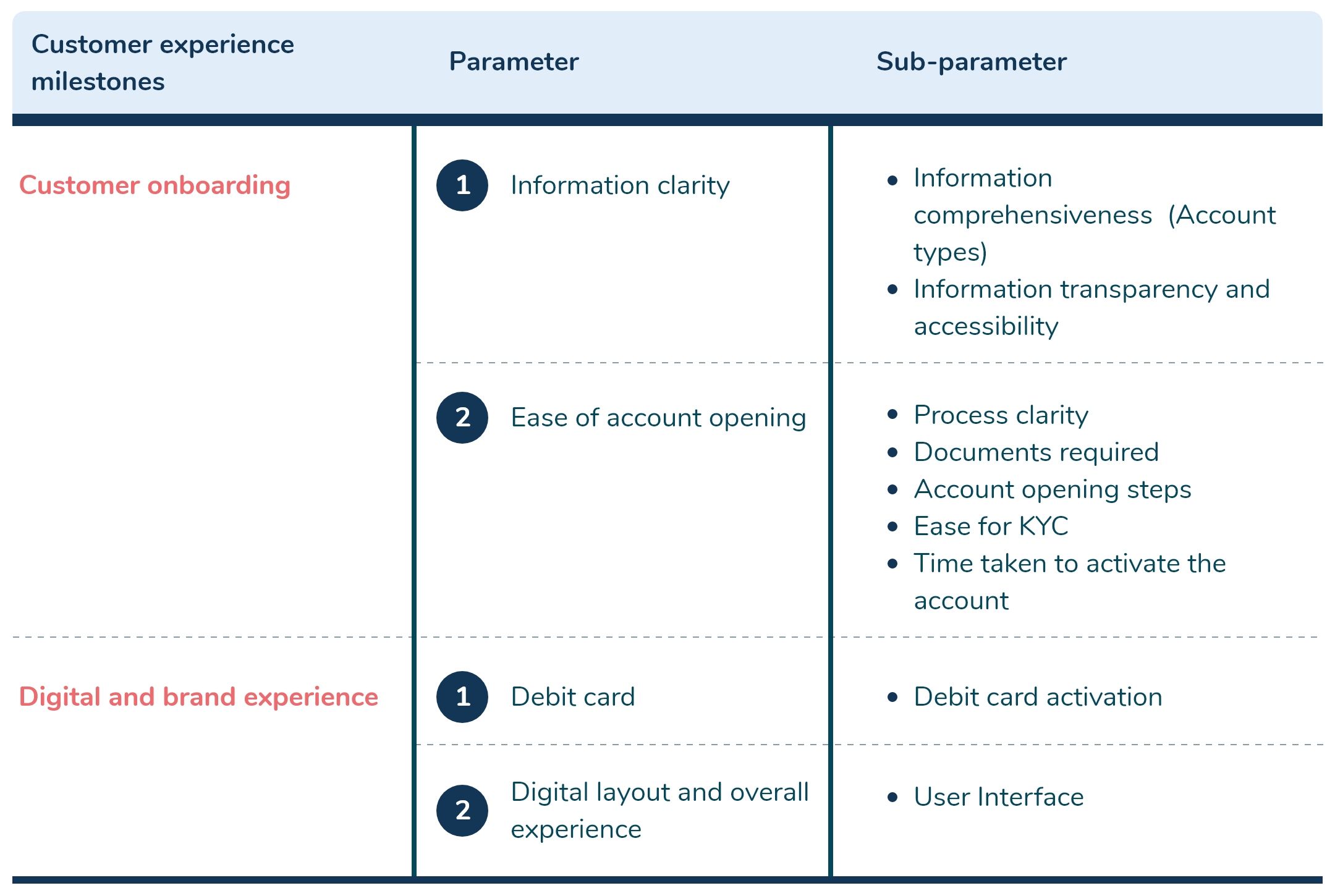

We developed a framework for the detailed evaluation of the banks to finalise our ranking. The framework assesses how a bank performed based on 4 parameters and 9 sub-parameters, capturing 2 key customer experience milestones vital in delivering a stellar customer experience (Table 1).

- STEP 3

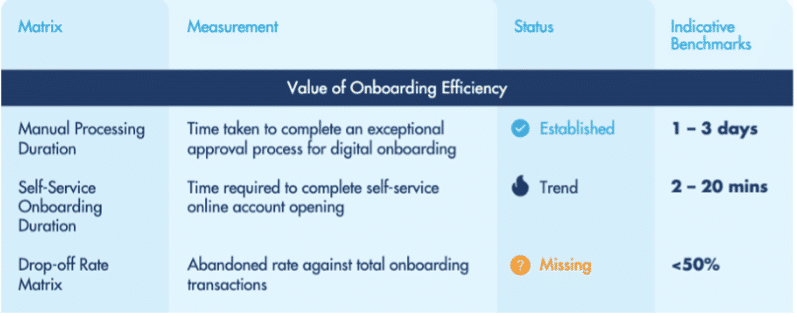

We score each bank on a scale of 1 to 5 based on convenience, accessibility, and uniqueness. We also recorded our observations based on “Temenos model of measuring digital success“2 by considering digital efficiency value metrics for establishing successful customer experience

Digital efficiency is about helping a bank to automate and optimize the operations to enhance the customer journey and experience. However, most banks do not emphasise enough on measuring the success of efforts to boost efficiencies across key processes, including new account opening, purchasing products via digital channels, and performing transactions.

twimbit’s top 10 Banks to ace CX

CX framework analysis for each parameter

1. Information clarity

We analysed the information clarity experience based on two parameters:

- Information comprehensiveness (Account types)

- Information transparency and accessibility

- 1.1 Information comprehensiveness (Account types)

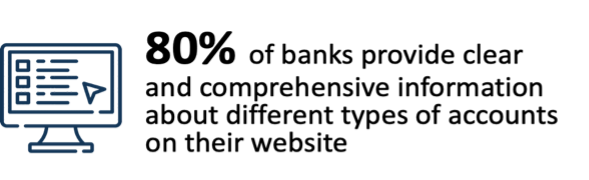

This section looks at the type of information provided on the bank’s website and how comprehensive it is. We see all banks in India offer a summary of different types of account on their website. Details include basic information about the account such as minimum balance requirement, saving interest rate, debit card facility, net banking and document requirements for opening the account.

Other information relates to whether account can be opened in online/offline mode, WhatsApp banking facility, enabling UPI, value added offers, extra/hidden fees and charges in form of inter-bank transactions, maintenance fees etc.

- Analyst tip: Banks can provide WhatsApp chat/ chatbot option right on the front page to solve any query that arise during information clarity step.

- 1.2 Information transparency and accessibility

1.2.1 Web

Information search should be intuitive and easy, with a clear call-to-action (CTA). Kotak 811, BOB, HDFC, SBI and IndusInd provide relevant information with transparency and ease of accessibility without any hiccups. For PNB and Union bank we notice that either the product allocation or details are hard to access, or they lack a CTA.

- Analyst tip: Banks need to ensure a rigorous governance metric to monitor and update their website performance that minimises website crashes, excessive loading time, and reduce abandonment rates.

By providing an absolute clarity of information relating to types of saving account along with additional information like cheque book facility, UPI and WhatsApp banking services, BOB clearly stood out among all other 9 banks.

1.2.2 App

It’s not just essential to have good products; it’s equally crucial to ensure that the mediums where customers get to know and interact with your brand are captivating. In this case, it’s your banking app.

Mobile banking app which redirects to browser for any related query prove as a friction-bound experience for its users, deteriorating mobile app purpose. Kotak 811, HDFC, SBI and IndusInd banks provide facility of account opening within mobile banking app without redirecting it to the web browser.

Among all banks, Union bank app does not facilitate account opening through the app or even redirection to the web browser.

2. Ease of account opening

We analysed the ease of account opening experience based on five parameters:

- Process clarity

- Documents required

- Account opening steps

- Ease for KYC

- Time taken to complete the a/c activation process

- 2.1 Process clarity

We are in the middle of a pandemic and the era of ultimate convenience. In this section, banks with a fully digital account opening process will come up top.

Even though it’s not a complete digital journey, PNB and Union bank enable customers to kickstart the journey online and later require to make branch visits. A process termed as digital but still involves visiting branch even once degrades seamless banking experience.

- Analyst tip: Banks must clearly state information relating to forms requirement and documents submission either on the website or app before requiring one to visit branch for account opening.

- 2.2 Documents required

Gone are the days when you need to fill forms, requiring self-attested documents hardcopy and passport photographs. Today, most banks only asks for a PAN card and Aadhaar card as a proof of identity.

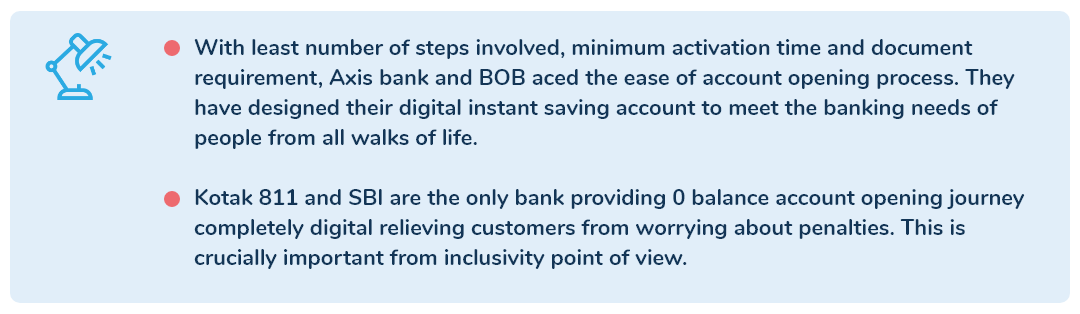

BOB is the only bank that facilitates frictionless experience by only requiring Aadhar as a mandatory document for account opening.

- 2.3 Account opening steps

Banks like Axis, BOB and PNB have gone a step ahead and eliminated the unnecessary steps involved during account opening process with the overall process completed in 4 to 5 steps, proving a great option for customers who like to bank digitally.

- Analyst Tip: If a banking App can instantly retrieve a customer’s personal details from its past log in history, the verification time and the number of steps are low.

While opening an account, few banks allow customers to set MPIN to log in seamlessly and start using mobile banking App. This further removes the hurdle of signing in again.

- 2.4 Ease for KYC

Using eKYC is more transparent, cost-effective and reduces the burden on customers in complying with KYC requirements for opening new accounts.

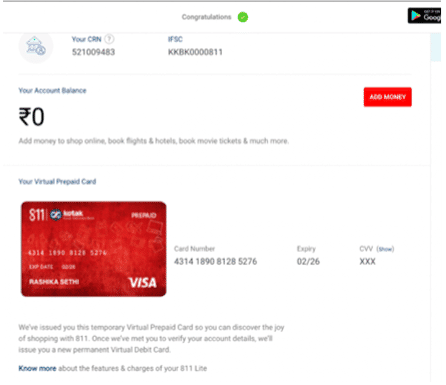

Kotak 811 lite have expedited this process by facilitating a one-step verification, where the customer simply has to enter Aadhar details for Aadhar linked OTP KYC and get instant account opened that later can be converted to full-KYC Kotak 811 account.

- 2.5 Time taken to activate the account

This parameter looks at customers’ activation experience, starting from the account opening process. Customers prefer to get instant access to their accounts. Therefore, banks should facilitate quick activation and allow customers to start making transactions and transfers instantly.

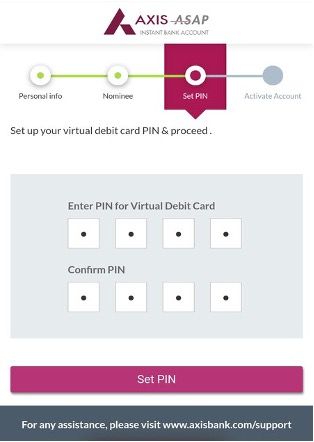

Only Axis bank account activation process was seamless, as it was a complete online customer onboarding experience that took less than 24 hrs time. The other bank with an end-to-end digital account opening process, took around 3-5 days.

By looking at the time required to complete the online onboarding process, we measured the bank’s Onboarding Efficiency, specifically the “Self-Service Onboarding Duration”, based on the “Temenos model of measuring digital success”2.

3. Debit card

We analysed the debit card experience based on one parameter:

- Debit card activation

Many banks have started providing virtual debit card after completing application process of account opening digitally but very few banks provide virtual debit card with instant activation option. Customers prefer to get instant access to their debit cards.

HDFC Instant saving account facilitates complete account opening journey digitally, but does not offer debit card or cheque book. With option to manage transactions and cash withdrawals digitally, it does not provide an instant debit card like others. In case, one wish to have an Insta debit card, one needs to visit the branch for applying it.

If HDFC can start offering virtual debit card with instant activation for Insta account, it can prove as major success for customers who are looking for instant digital account with debit card facility.

- Analyst tip: In case of physical card, banks can facilitate contactless card delivery in a short period to create a seamless customer journey. Instant update to customers through email or an alternative phone number on deliveries ensures that the debit card reaches them at their convenience.

Bank can leverage the opportunity of incorporating your brand theme and colour to create attractive and safe packaging of debit card. Personalised debit card customisation proves as a great traffic booster for online banking services.

Neobanks create brand resonance by instilling attractive, innovative, and journey-led packaging for their customers. One of the Indian neobank translates the entire card activation journey in a mission to a planet that invokes curiosity and excitement in activation and knowing the rewards.

4. Design layout and digital experience

We analysed the design layout and digital experience based on one parameter:

- 4.1 User interface – Website

Visual graphics and quirky designs play an integral role. Advanced design website with soothing colour scheme and interactive features enhances the overall digital experience of customers. Furthermore, wireframes and user flow charts facilitates ease of information consumption.

Websites of traditional banks have been operating with the same interface without any significant transformation, reducing the overall experience.

Only 4 out of 10 banks provide advanced design experience for their users, rest all are still operating with basic or average layout making not so easy for their users to understand.

- 4.2 User interface – App

Mobile application designing is another area where you can promote your brand voice to increase customer retention rates, brand reputation, and platform engagement. You can employ UI/UX techniques such as:

i. Personalisation: Hyper-personalisation of existing features plays a key role in increasing brand loyalty and customer engagement. Customers should have complete control over planning their journey. While customers have an option to choose their best-fit products, there is no in-app personalisation option. Some examples of in-app personalisation include:

- Choosing app designs and themes

- Scanning any QR code

- Biometric verification or authentic Face ID feature

- Choosing the presentation of the account balance

- Personalize reminders

- In-app messaging

- Smart push notifications

ii. Gamification: Gamified dashboards can make mundane tasks such as recharges, paying bills, credit health and tracking deposits fun and engaging. The secret to app engagement lies in variable rewards. Most of the leading neobanks, reward customers with badges or stickers when they complete tasks.

iii. Animations and themes: Following a brand theme with a variety of in-app animations such as endowed progress, onboarding, feedback, and splash animations and transitions will make the customer journey fun and engaging.

Traditional banks have lot to learn from neobanks by integrating technology at its core. By providing better and advanced range of financial services with easy-to-use app, latest technology stack and user friendly design, traditional banks can level up their game of banking in this digital era.

Increasing customer satisfaction with excellent customer support in banking

While completing the account opening journey, we also analysed the customer service experience of banks considering few parameters.

Banks offer a multitude of customer support mediums. Customers can contact their banking service provider to clarify queries and complaints using various communication modes including: email, In-app live chats/call with customer executives, Interactive voice response, WhatsApp banking etc.

WhatsApp banking allows customers to connect via a familiar channel ensuring uninterrupted and safe banking, any time at any place.

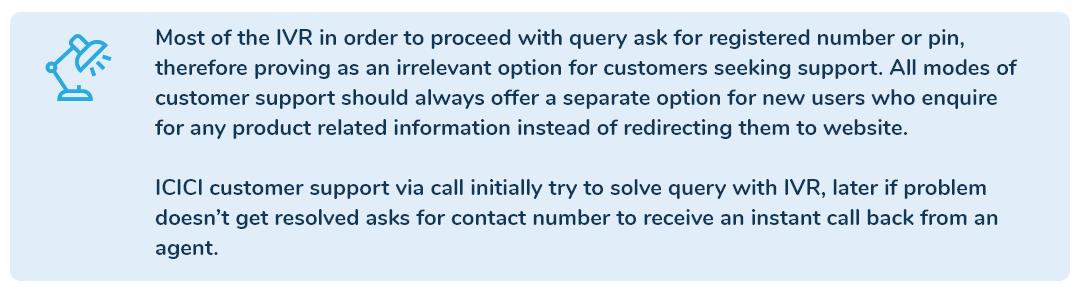

In addition to email and hotline services, banks are adopting AI-driven chatbots to handle the large influx of queries and complaints enabling decrease in average response time and increase in Net Promoter Score (NPS). Moreover, chatbots also boost accuracy and complexity over time. With benefits, comes the challenges. Chatbots are unable to solve all queries, lacking human touch and misunderstanding user sentiment which ultimately annoys the users and prove as meaningless.

Therefore to avoid this, it is important to have an option to transfer to an agent/ receive a call back at any point in conversation.

In order to reduce traffic, banks also provide a detailed FAQ section, complete with pictures, tutorial videos or an Interactive Voice Recognition (IVR). These steps allow customers to clarify their queries and issues efficiently without having to interact with a customer support agent.

On average, banks in India offer half of the listed customer service methods.

Analyst critique and recommendations

Kotak811 took the lead in all aspects of the customer experience journey. It exemplifies account opening process by providing comprehensive information, minimum document requirement, easy KYC and instant virtual debit card.

In this digital era, many traditional Indian banks will evolve to compete with neo banks to adopt more customer-centric approach where they will integrate technology and AI to offer more efficient and personalised banking services through smartphones and other devices.

This will require them to build a powerful customer experience platform. Improving engagement rates will become a critical measure of success. Therefore, it is imperative for Indian banking service providers like you to focus on curating an engaging and frictionless digital journey that highlights your brand values to target a larger segment of the market and increase customer acquisition and retention rates. Our analyst team sees four distinct opportunities for you to create a CX journey that is superior:

- Digital zero balance account

Most banks these days set a minimum limit of Rs 10,000 per account to be maintained. Maintaining a minimal balance in an account is one of the most challenging chores for retirees and low-income individuals. Account holders who find it hard to maintain their balances might open a Zero Balance Savings Account.

Few banks provide an option to open a zero-balance account under PMJDY (Pradhan Mantri Jan Dhan Yojana), but the account opening process under this scheme is completely offline. Therefore all banks should start providing option for 0 balance account which can be opened online just like Kotak 811 and SBI.

- Virtual debit card with instant activation

Virtual debit cards give you access to a variety of online deals on food, shopping, and restaurants, among other things. Bonus points can be earned via a virtual debit card and redeemed online using the bank’s mobile app. The challenge comes at activation point. Banks like Kotak 811 and Axis provide virtual debit card with instant activation whereas few banks are still operating with traditional method of delivering physical debit card within 7 working days timeframe.

- Account opening via app

Banking apps need to start facilitating complete account opening journey starting from information clarity to getting debit card activated with having customer support present at every step. Banking apps redirecting customers to web browsers for all steps degrades user app experience.

- Personlisation, animation and gamification in App

Customers nowadays, particularly millennials and generation Z, easily get bored. Many banking apps are solely concerned with transactional activities such as account opening, deposits etc. In the digital world, there is no such thing as a personal connection.As a result, only something exciting and challenging will keep them interested. Game designs like Badges, awards, points, scoreboards, and other design elements will arouse curiosity and provide a sense of control.

All this will provide superior customer experience through product innovations and technology to address a particular aspect of banking, such as account opening, savings, or investing just like neobanks.

7- point checklist to elevate your bank’s customer experience:

- Product information – Customers should be able to find all important information related to opening and maintaining the chosen bank account and the services that come with it on the bank’s website/App.

- Crucial details to include – eligibility criteria for account opening, the minimal balance needed to maintain the account, charges and bank rates

- Services provided with the account – internet banking possibilities, frequency of bank statements, debit card or ATM services

- Documents needed to open an account

- Exact steps to take to open an account

- Information design – We all like things that come easy; this applies to getting information too. Customers should not have to dig for details regarding your products.

- Website – A website with simple user-friendly layout, easy navigation and providing all relevant information on single landing page creates a seamless customer journey.

- App – Customers must have the flexibility to attain all necessary information of the respective bank via mobile banking app. Mobile apps should facilitate account opening by providing information with navigation guide which is easy to consume including a clear call to action (CTA) for customers

- Account opening process – Banks with a clear account opening process using infographics and detailed instructions avoid confusion on the most challenging part of the customer journey. Normalised by neobanks in neighbouring countries, a fully digital customer onboarding process can elevate your customers’ experience.

- Reducing the number of steps to activate an account – enhances the user experience and increase the efficiency value for the banks. Precise information, external obstructions, technical difficulties, and additional steps affects customer satisfaction.

- Enabling a branch appointment system – provide customers with certainty and eliminate unneeded queuing time

- Documents required – Bringing a bunch of documents to the bank is at best a hassle, at worst, an annoyance. In India, consider a KYC system that only requires a customer’s Aadhar.

- Debit card – Banks must provide its customers detailed information about debit card which includes card fees including taxes, process of placing a request, activation process and time consumption.

- Design layout and digital experience – If fintech disruptors have one thing in common, it is the trendy design of their websites and apps. While its crucial to have good products, ensuring that the mediums where customers get to know and interact with your brand captivate them is also equally important – in this case, it’s your website or app.

- Customer support – When customers require support, there is a good chance that they are feeling frustrated and would like to immediate assistance. Therefore:

- Other than traditional options, include self-service mediums (such as chatbots), and

- Adopt up-and-coming social media channels to provide help

- The right metrics to track CX success – As the customer onboarding process is shifting to digital, consider tracking the Onboarding Efficiency of your digital account opening system. A few measures to consider are:

- The abandonment rate against total onboarding attempts

- Time required to complete the digital self-service account opening process

Endnotes:

1Twimbit (2022). State of top APAC banks. https://twimbit.com/insights/state-of-top-apac-banks-2022

2Temenos (2021). Digital bank of tomorrow: Part 2 Missing measures of digital success. https://www.temenos.com/insights/white-papers-reports/missing-measures-of-digital-success/.