Company Insights

twimbit Purpose Index

Purpose score- * Poor, ** Satisfactory, ***Good, **** Excellent, *****Outstanding

Source: Refer to the methodology in Appendix A below

Bendigo and Adelaide Bank (Group financials) – An overview as of 30th June 2020

| Bank name | Bendigo and Adelaide Bank |

| Headquarters | Bendigo, Australia |

| Operating income(30th June 2020) | USD 1.12 billion |

| Net Profit(30th June 2020) | USD 133.08 million |

| Total Assets(30th June 2020) | USD 52.4 billion |

| Employees | 5900+ |

| Country of operation | Australia |

| Number of branches | 707 |

| Information and communication technology (ICT) spend (30th June 2020) | USD 119 million |

| Bank ranking in a particular country | 5th in Australia |

| Number of customers | 1.9 million |

| Market capitalisation (30th June 2020) | USD 3.74 billion |

| Operating revenue CAGR growth (2016-2020) | 1.04% |

Note: All $ values indicate US Dollars

Conversion rate used 1 AUD = 0.69030 USD

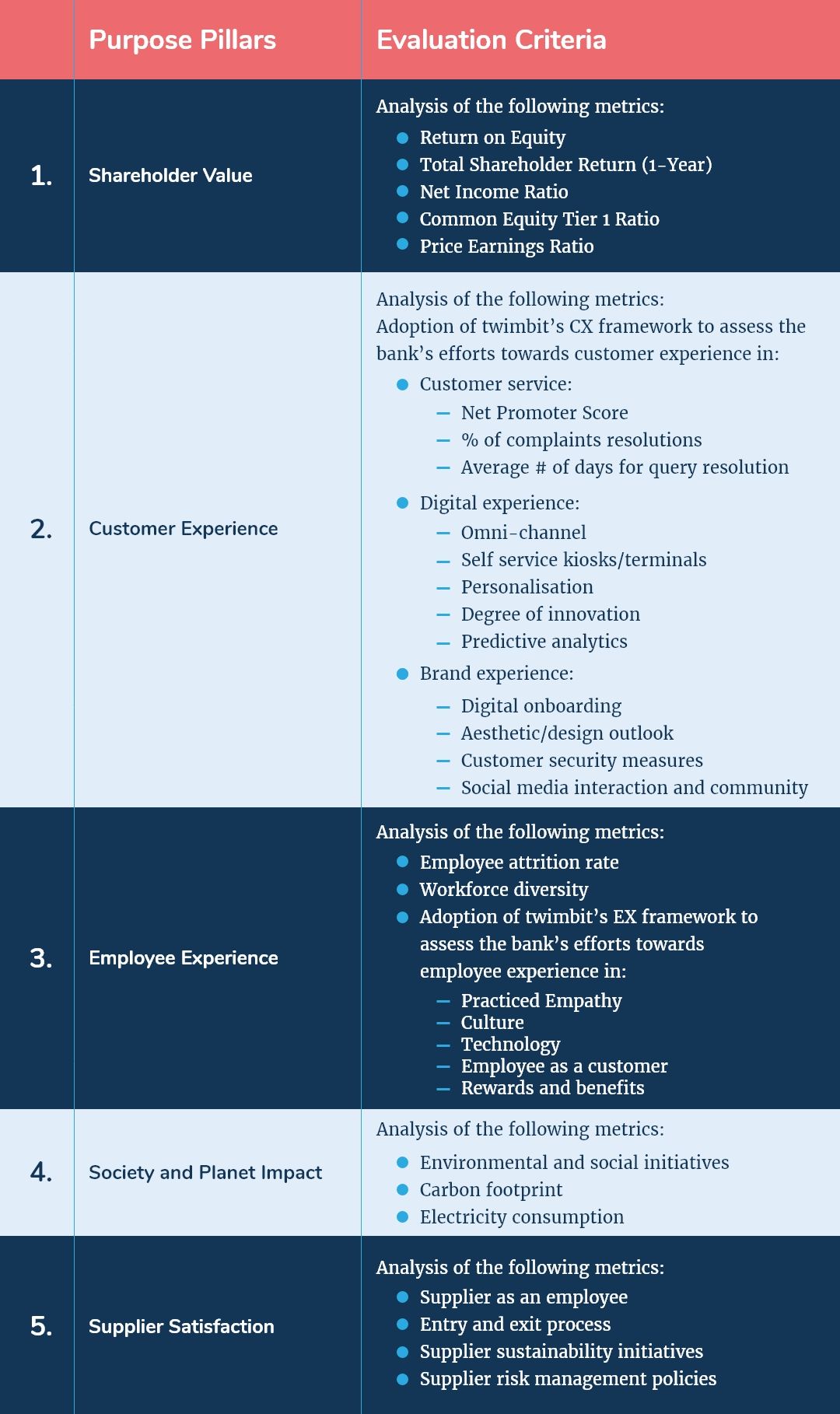

Shareholder value (30th June 2020)

| Return on Equity (as of 30th June 2020) | 5.36% |

| Total Shareholder Return (1-Year) | -0.09% |

| Net Income Ratio (as of 30th June 2020) | 11.79% |

| Common Equity Tier 1 Ratio (as of 30th June 2020) | 9.25% |

| Price Earnings Ratio (as of 30th June 2020) | 11.44 |

Bendigo and Adelaide Bank and its strategic focus areas

- Customer experience

As a part of its overall organisational transformation, Bendigo and Adelaide Bank (BEN) plans to improve customer experience (CX) through sustainable investments in its current capabilities. The bank aims to do so by:

- Introducing the ability to sign documents digitally, identify customers via video endpoints, and enable end-to-end digital onboarding to enhance overall customer experience.

- Upgrading commercial lending process by automating multiple touchpoints (branch, mobile) while ensuring compliance with a prudent lending criterion and the Banking Code of Conduct.

- Reimagining the future branch outlook to offer customers and communities a range of features, including a free ‘Retail Pop-Up Space’, an indoor community space – equipped with technology for community or business meetings, workshops or small events – and free Wi-Fi

- Building a centralised platform for omnichannel customer engagement. The aim is to extend and enhance CX by delivering tailored and relevant content at each step of the customer journey, regardless of the channel of engagement chosen.

- Launching the new Bendigo Complete Home Loan product – with an optional 100 per cent offset on all fixed and variable loans. It consolidates 95 products into one and improves customer simplicity and flexibility.

- Employee experience

- BEN places its focus on the following areas to create a healthy work environment where employees find a sense of belonging within the bank and its ambitions: Keeping employees informed and connected virtually through technology upgrades that support productivity and effective remote working, learning and collaboration

- Delivering an enhanced wellbeing solution through its newly launched Wellbeing content hub with the tools, programs, and services to support the physical, emotional, mental health, and safety of employees

- Launching BEN U, a corporate university that supports the modern learning methods and philosophy of ‘learning through programs, people and practice’

- Engaging more women in leadership and management roles to promote workplace equality and women leaders in banking and finance. The bank has over 34% women in senior management, and over 60% of the total workforce are women

- Financial inclusion

BEN aims to improve the accessibility of financial products to a maximum number of people, especially the underserved population:

- In collaboration with the Victorian State Government, BEN delivers programs such as HomesVic and the Federal Government’s First Home Loan Deposit Scheme.

- To eradicate financial abuse, the bank recently launched a new internal training module to equip its staff with more knowledge about financial abuse. The trained staff, in turn, provided extra care to customers who are most vulnerable to such abuse. BEN held awareness programs through a debit card initiative for customers to help them learn more about online and app-based banking.

- Society and planet impact

The bank aims to function in an environmentally and socially sustainable manner by:

- Communicating with shareholders and customers digitally through eShareholder documents and eStatements to cut down its paper usage. As of 2019, over 37% of the shareholders are registered electronically and receive paperless communications.

- Adopting the ‘Climate Change Action Plan’, which outlines the action the bank will take over the next three-year period. The plan will help improve climate outcomes, drive cultural change, engage people and customers, and enhance its climate change risk management framework.

- Neo banking

- Up – Australia’s first mobile-only digital bank results from BEN and fintech, Ferocia. Up aims to provide its customers with an innovative, tech-led banking experience.

- Since its launch in 2018, Up claims to be the highest-rated banking app in Australia, with over 250,000 customers (mostly millennials and GenZ). The numbers are likely to continue to grow via the in-app customer referral program.

- Up users have an option to create several savings account options called ‘Savers’ to help meet their financial goals.

- Up also provides a wide array of budgeting tools, including automatic spending categorisation, upcoming bill prediction, transaction tracking, balance notifications, and year-end financial reviews.

- Up charges zero markup fees on the existing exchange rate for overseas transactions, including international purchases. The bank allows free overseas ATM card usage without any additional charge.

- The app also allows its users to use Apple Pay™, Google Pay™ and Samsung Pay™ without a physical or virtual card, along with guaranteed security of transactions.

Up was able to garner customer support in its ambition to digitise customer journey by:

- Helping customers reduce environmental impact systematically as the bank reinvested more than USD 190 million of its profits into Australian communities.

- Simplifying the customer onboarding journey by reducing the entire sign-up process, along with identity verification, to just 3 minutes.

- Solidifying the Upsider community to enable peer-to-peer lending and payment transfers amongst fellow Upsiders.

- Redesigning its cards in a portrait orientation-consistent with its previous name, ‘Alt’

- Accommodating transactional security by accounting for payment abuse and allowing customers to use ‘Up Tools’ to set security boundaries.

- Rolling out annual personalised spending and saving reviews that are tailor-made for each customer.

Digital strategy

BEN is actively trying to build a robust digital infrastructure by:

- Simplifying and digitising key customer journeys by prioritising joining the bank, home, business, and agribusiness lending

- Simplifying operating structures and continue to expand capability around operating in an increasingly digital environment

- Delivering Open Banking in line with industry timelines and leveraging new capabilities into new customer offerings

- Extending Cloud and API capabilities and further leveraging cloud-based applications, services, and platforms

- Reducing the number of products and technology applications bank use to simplify the business

- Leveraging on its partners’ capability to accelerate the build-out of the bank’s key digital channels and offers

- Launching the new Bendigo Complete Home Loan product – with optional 100 per cent offset on all fixed and variable loans. It consolidates 95 products into one and improves customer simplicity and flexibility

- Bridging financial services to provide BEN customers with ongoing access to specialised financial planning services

- Tyro, an exclusive merchant-acquiring partner for its business banking customers

IT strategy

BEN is adopting new technologies to become more efficient and suit its customers’ evolving needs. It has invested in innovative technologies and leveraged vital strategic partnerships to offer customers more choices and a better digital experience:

- The bank’s future investments will focus on removing cost and complexity and creating a seamless banking experience for tomorrow’s customers. Investments will focus on core banking simplification, Open Banking, cloud, application simplification, customer journey digitisation, and the appointment of Boston Consulting Group as BEN continues to reshape its workforce to align with customer and growth needs.

- The bank’s partnership with Australian fintech Tic:Toc – the world’s first fully digital home loan platform gives the customers access to instant home loans via Bendigo Express. Tic:Toc uses AI technology to deliver significant efficiencies in home loan assessment compared to traditional processes. Since its launch, Tic:Toc processed USD 3.04 billion of applications.

- Reducing the number of technology applications from 684 to 601 (12% reduction) to remove duplication, save on costs, and reduce risk.

- Identifying more than 400 applications for rationalisation to remove duplication, reduce risk and increase stability and support.

BEN and its ICT contracts

- Ultradata – to enhance banking software capabilities and financial services

- Cuscal, Australia’s leading independent provider of payment solutions, including card and acquiring products, mobile payments, fraud prevention, EFT switching, and direct entry

- Partnership with TAS, an end-to-end cloud computing and banking solutions company to include cloud, infrastructure-as-a-service, managed services, software-as-a-service, and business services

8 Growth and Innovation Opportunities

- #1 Cost to serve

- The bank has an extremely high cost-to-income ratio of 63%, which is nearly 40% higher than its regional peers (the industry average is at 45%). The poor cost-efficiency results from unfavourable operating environments, including low interest rates, high spending on personnel, and low non-interest income due to COVID-19.

- The bank’s personnel cost accumulates to USD 437.8 million, which accounts for 34.7% of its total income. The said high cost creates an opportunity for the bank to reduce this particular cost base substantially through:

- The reduction of call centre use for customer query management and sales, and instead investing in AI-driven virtual assistants and chatbots for iterative functions

- Replacing man-hours with cognitive process automation of routine and daily back-end tasks

- Adopting a holistic cloud implementation strategy that centralises business for regular activities and eliminates data centre management

- The digitalisation of more functions and processes that are currently human-intensive, such as branch relationship management, cashier, and customer grievances

- The bank’s fee income declined by 8.1% due to an increase in competition. A sound net interest margin management in a low-interest rate climate is achievable by identifying repayment risk in loans and attrition risk in deposits:

- The bank can use predictive behavioural models to revise its interest-rate risk models and hedging strategies continuously.

- Increase focus on non-interest income and complementary revenue streams to offset the impact of high impairment charges.

- The bank should undergo a strategic realignment by cutting down non-profitable product lines from its product portfolio and focus on preserving its core lines of operation, i.e., consumer, wholesale and small business, and agribusiness

- #2 Transformation of the branch and its branch networks

- BEN operates in Australia with 509 bank branches and 548 ATMs along with its neobank Up. The bank is progressively optimising its branch network with a net reduction of 17 branches in 2020. Further optimisation of branch network can include:

- The bank has 20% of its branches in communities or towns where it is the only financial institution. An integrated phygital, i.e., a physical plus digital strategy, will help the bank preserve and grow its existing market share in these communities. BEN bank can achieve this by increasing the number of self-service digital kiosks enabled by interactive, video-call teller facilities, reducing the footfall in the physical branch. The bank can also consolidate community branches located within a 5-10 km radius to build a flagship community hub that supports all banking functions.

- BEN should continue its niche focus on agriculture and aim to transform its branches located with agriculturally reliant communities through digital propositions. Such propositions include empowering sector specialists with structured and forecasted data on price risks, digital loan applications, and a branch ecosystem that supposed the community in proximity for a competitive advantage.

- Furthermore, the bank should aim for an omnichannel branch operational model that takes care of customer needs and requirements through digital channels without compromising customer satisfaction and efficient product delivery.

- #3 Customer experience

- With creating an end-to-end customer journey as its focus, the bank should consider mitigating customer pain points at multiple levels. To create a refined customer experience, the bank should focus on the following areas:

- Product differentiation:

- BEN should focus on strengthening its lending product stack and building capabilities to support the unique needs of its dominant sector of operation – agriculture.

- Customers are less willing to transact digitally when it comes to complex financial products like agribusiness loans and investment products.

- Identify customer journey inflexion points of interest in securing a loan to pre-empt loan requirements and create a preliminary digital document kit.

- Reduce paper-intensive documentation and bottlenecks for approvals through a digital identity recognition and credit assessment program.

- Allow customers to apply and access loan application through the bank’s proprietary app.

- Support the customers with in-app virtual assistants for any immediate queries and updates on the application.

- Neobanking app:

- BEN can add interactive functionalities in the Up model beyond the neobank’s core products, such as customised debit and credit cards. Adding new banking solutions will increase the per capita consumption of services to more than five while still keeping the brand’s quirky and vibrant touch in mind. These services can include:

- Byte-sized wealth management products for quick and hassle-free investments

- Low-cost remittances in multiple geographies depending upon the value of the transaction

- Micro-insurances for car rides, food deliveries, cycles, pets, etc.

- Product differentiation:

- #4 Employee experience and productivity

- To nurture a productivity centric work environment, the bank should create a better work culture by moving beyond basic rewards and benefits and more towards treating the employee as a customer. It can use appropriate technologies for employee upskilling and development.

- BEN U, the bank’s corporate university initiative, has the ambition to train and educate employees and make them more people-centric and agile. The bank has significant room to improve its training delivery channels by:

- Expanding its cloud-connected devices to enable real-time tracking development modules delivery.

- Introducing virtual learning using augmented data insights on the learner’s existing knowledge and experience.

- Simplifying existing training modules into easily consumable content forms (like podcasts, short videos, etc.) so that employees can learn at their convenience, place and time.

- Furthermore, the bank can improve its existing rewards and benefits offerings and financial support by including:

- Comprehensive recognition mechanisms for the equitable distribution of rewards, benefits and promotions

- Financial Support for Single Parents

- Financial Support for Parents of Children with Special Needs

- Scholarship sponsorship for undergraduate hires

- Employee volunteering programmes sponsorships

- #5 Migration of workload to the cloud

- The bank leverages the IBM cloud development platform for creating, testing, and deploying customer-centric solutions. As part of this strategy, the bank can further scale its workload migration on the cloud by:

- Integrating its cloud infrastructure by extending data storage and data-driven activities across security, regulatory compliance, auditing and pan-organisation communication pipelines to transform the overall operational model.

- Decreasing data storage costs by reducing the capital expenditure on its in-house physical storage infrastructure.

- Creating a robust, tightly controlled delivery program that allows developers to scale and embed microservices in the cloud architecture.

- Providing complete end-to-end protection for all confidential data stored in the cloud. This protection enables the bank to maintain the customers’ trust and confidence in obtaining, analysing, and sharing their personal information.

- Responding to market shifts, such as black swan events – examples include Covid-19 and the entry of non-bank players to the banking environment with the grant of digital banking licenses.

- #6 Artificial Intelligence (AI) in everything

- BEN is keen on digitising the customer journey to ease its customer pain points. The bank has a significant scope to improve its operational processes by investing in AI and increasing its technological footprint.

- BEN should focus on the following AI themes as a part of its digital journey:

- Using Cognitive/Robotic process automation for credit underwriting processes which can accurately assess underbanked and unbanked customers (for example, millennials)

- Building predictive models at the front-end to help screen and detect fraudulent entries and prevent money laundering risks

- Using natural language processing (NLP) in research and analysis, customer document processing, and customer service activities (chatbots and virtual assistants)

- #7 Cybersecurity

- With data protection and cybersecurity as an essential area, especially with the increasing adoption of new technologies, BEN should aim for a resilient and agile cybersecurity framework. It can do so by incorporating the following in its existing cybersecurity model:

- Using AI to estimate and categorise various inherent risk levels associated with various technologies like APIs, Cloud, machine learning, etc.

- Using Cognitive process automation (CPA) to automate routine security tasks like identity access management, basic threat screening, controlling as well as reporting functions.

- Developing a holistic cybersecurity culture by investing in training, education and sensitisation of cybersecurity practices. This specific culture enables BEN staff to be aware of cyber threats like phishing, data manipulation, data breaches, and cyberattacks.

- With data migration to the cloud at its focus, the bank needs to strengthen and monitor data access at endpoints using machine learning algorithms that can report any anomaly.

- #8 Society and planet contribution

- To create a meaningful impact and fulfil its responsibility towards society as a stakeholder, the bank should inculcate the following in its sustainability strategy:

- Reduce excessive paper usage by adopting digital endpoints (for example, e-receipts in place of printed receipts) as well as recycling and upcycling existing waste wherever possible to reduce the burden on landfills.

- Responsible for community building by undertaking new community projects that enable accessibility of basic utilities and social services in rural communities, financial inclusion programmes for the unbanked and underbanked people, as well as health, education, employment, and environmental conservation programmes.

- Financing renewable projects that meet pre-defined sustainability targets and form meaningful long-term partnerships to drive sustainability agenda effectively and comprehensively.

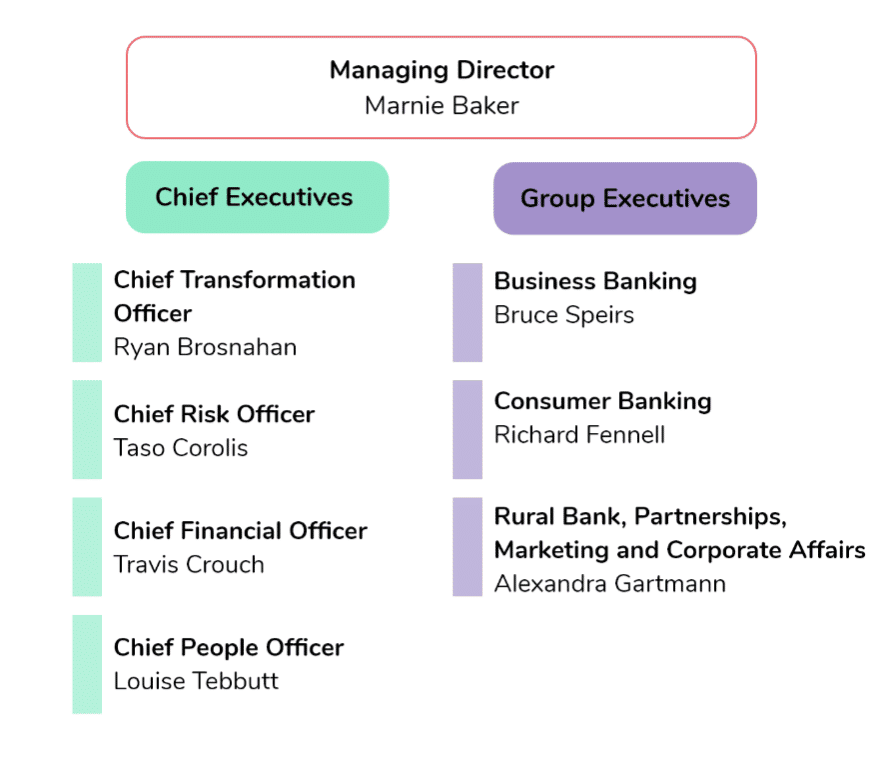

Organisation Structure: Leadership

Executive profile

Marnie Baker

CEO & Managing Director

Baker joined BEN in 1989 and became an executive of the Bank in 2000. She became the Managing Director in 2018.

Baker has more than 30 years of experience in financial services, with Retail Banking as a niche area of specialisation. Her experience also covers financial planning, trustee and custodial services, insurance sector, funds and portfolio management, treasury, risk & compliance, payment systems, information technology, change management, social media and digital technologies, legal and human resources.

Ryan Brosnahan

Chief Transformation Officer

Ryan Brosnahan is a relatively new addition to the BEN management team. He joined in 2019 as its chief transformation officer. Brosnahan is chiefly responsible for driving the bank’s organisational and technological transformation program in alignment with its strategy.

He has over 20 years of experience in the financial services industry, both within and outside Australia. Ryan has led significant growth and transformational change initiatives across multiple segments and businesses in financial services. He has a particular predilection towards the technology’s advent in the financial services sector.

Taso Corolis

Chief Risk Officer

Corolis joined BEN in 2011 and was in charge of analytics, reporting, compliance, and risk management within Group Risk. He came from Rural Bank (a division of Bendigo and Adelaide Bank), where he served as the Chief Risk Officer from 2008. He has approximately 20 years of experience in the financial services industry, which includes serving ten years in the capacity of senior executive roles for the Australian Prudential Regulation Authority (APRA).

Travis Crouch

Chief Financial Officer

Travis Crouch has been a part of BEN since 2001. For the last 17 years, Travis has managed various offices, such as the Head of Banking Products & Solutions, Head of Investor Relations and most recently, Divisional Financial Officer. Crouch was appointed Chief Financial Officer in 2018.

During his tenure at the bank, he has also managed various senior executive roles in Funds Transfer Pricing, Balance Sheet Management, and Capital. Travis has been the Chairman of the bank’s Pricing Committee since 2016.

Louise Tebbutt

Chief People Officer

Louise Tebbutt stepped into the role of Chief People Officer in October 2018, after more than 20 years in senior HR roles, primarily with Myer.

Tebbutt has over 20 years of experience at Myer, where he held several senior executive positions, the latest being that of Executive General Manager HR, Risk and Safety. At BEN, Tebbutt is responsible for streamlining the capability and performance of the team to support sustainable business growth. Louise lays special emphasis on augmenting organisational capability and promoting a culture of performance and accountability governed by the principle of shared common values.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on 5 purpose pillars and score each bank on them.

Endnotes

Bendigo and Adelaide Bank. (30th June 2020). Investor Presentation 2020

https://www.bendigoadelaide.com.au/investor-centre/financial-results/#2020

Bendigo and Adelaide Bank. (30th June 2020). Annual Review 2020

https://www.bendigoadelaide.com.au/globalassets/documents/bendigoadelaide/investorcentre/results-and-reporting/annual-reviews/annual-review-2020.pdf

Bendigo and Adelaide Bank. (30th June 2020). Annual Financial Report 2020

https://www.bendigoadelaide.com.au/globalassets/documents/bendigoadelaide/investorcentre/results-and-reporting/annual-reviews/annual-financial-report-2020.pdf

Bendigo and Adelaide Bank. (30th June 2020). Market Index

https://www.marketindex.com.au/asx/ben

Vinayak Gandhi, Research Intern, contributed to the research in conducting preliminary literature review and conceptualising the article.