Bendigo and Adelaide Bank, an Australian financial institution headquartered in Victoria, was formed by amalgamating the two entities in November 2007. Today, the bank is commonly referred to as Bendigo, spanning its significant presence in Victoria and Queensland. Currently, it occupies 466 branches that provide banking, insurance, investment and superannuation services, aiming to simplify the customer experience, one step at a time.

Financial highlights

NPL (Non-Performing Loan)

The NPL saw a significant decline of 37.50% between FY21 and FY22 (Figure 1), with a continued decrease after improving asset quality post-pandemic.

LDR (Loan-to-Deposit Ratio)

Bendigo achieved an LDR of 104% in FY22 (Figure 1), staying significantly above the 90% threshold from 2018 to 2022. Although a high LDR indicates its capability to maximise interest-based earnings, it can also lead to negative impacts such as insufficient liquidity coverage.

CE (Cost-Efficiency Ratio)

Bendigo saw a spike in its CE, hitting 62.7% in FY20. Gradually, the bank decreased its CE ratio by a total of 5.32% from FY20 to FY22, leading to a current CE ratio of 59.4% (Figure 1). This decline indicates Bendigo’s improvements to its operations.

NIM (Net Interest Margin)

Traditionally, a high LDR leads to a high NIM, as the banks disburse more loans than their deposits, thereby earning more interest. However, Bendigo’s NIM has dropped significantly by 10.77% between FY21 and FY22, despite its high LDR of 104%. This decrease is because many banks across Australia provided relief aid through low-interest loans during COVID-19.

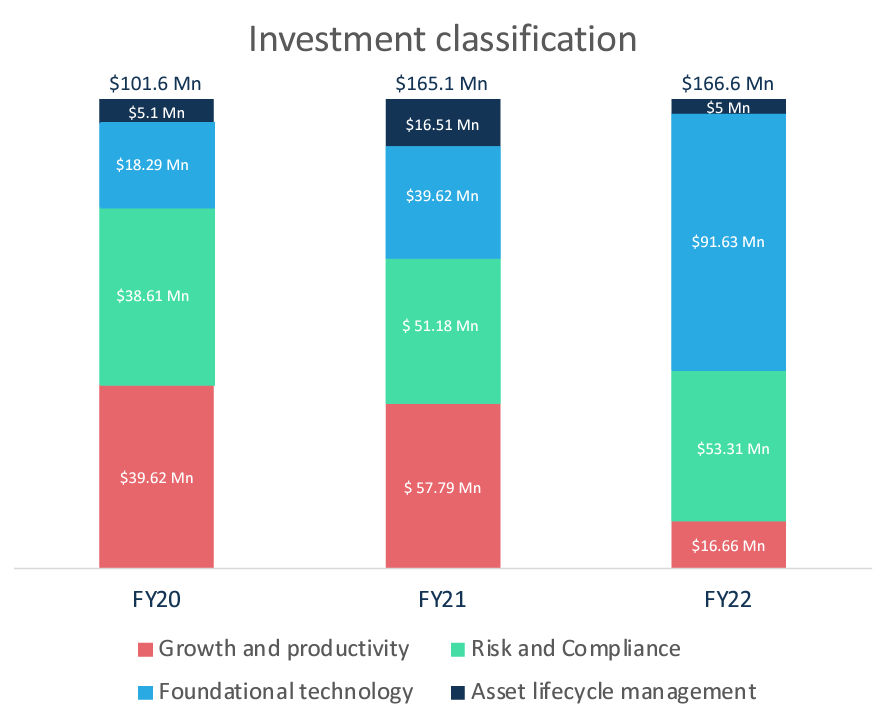

Bendigo Investment Highlights FY2022

- Bendigo categorises its investment spending into two categories – expended and capitalised.

- Expended costs are costs which are incurred this year and are recorded in the income statement.

- Capitalised costs are costs which will last beyond the current year, carrying economic value in the next year and are therefore recorded in the balance sheet.

- During FY22, the expended and capitalised costs were 39% and 61% of the total investment value, respectively.

Strategic Focus Areas

- #1 Reducing the cost to serve and simplifying business processes

Yearly reviews have allowed Bendigo to identify business opportunities to:

- Simplify its operating model

- Reduce risk

- Deliver cost savings

Since the onset of the strategy, the bank has been able to do the following to streamline its operating model:

- Opened Divestment of Bendigo Financial Planning in August 2019

- Operates Rural Bank Limited as a division of the Bendigo group with specialised services and products to Australia’s rural and urban areas

- Closed 23 branches and 15 agency outlets while the Community Bank partners opened four new customer service centres

- Assumed 100% ownership of the community sector banking integrated into the bank’s operating model

- Launched the Bendigo Complete Home Loan product encompassing 95 products to improve customer simplicity and flexibility

- Identified 400 applications for rationalization to remove duplication, reduce risk and increase stability and support while reducing technology applications by 12%

- #2 Core banking modernisation

Bendigo is continuously reducing the number of core banking systems and technology applications it operates as part of its transformation program:

- Launched one core banking system during FY2022, with seven to date, aligning its strategy to create one bank-wide platform by FY2024

- Reduced IT applications from 650 to 491, with further reduced projections of 325 over the next two years

- Operates 20% of its application via the cloud, intending to have 50% of apps on it by FY2024 end

- Reduced the average time for home loan purchasing from 22 days in FY2019 to 13 days in FY2022; the end goal being the time taken will reduce to less than one day by FY2024 through its partnership with Tic: Toc

- Improve automated credit decisioning from the current 10% to 90% by the end of FY2024 as part of digitalization

- #3 Making strategic alliances to grow adjacent revenue streams

Bendigo has established several strategic alliances to create several applications that help grow adjacent revenue streams, such as:

Bendigo Express

The platform is a digital home loan application and assessment process in partnership with Australian fintech Tic: Toc. Here, Bendigo Express uses AI to deliver significant efficiencies in home loan assessments. The proposition is Australia’s first fully digital loan offering providing customers with loans at competitive interest rates and online loan approval within 60 minutes. Since launch, the platform has processed more than AUD 4 Bn of applications.

PayTo

By maximising the real-time payment capabilities of the New Payments Platform, PayTo allows its users to:

- Access existing online and mobile banking accounts to gain new levels of control and transparency for digital payments

- Securely pre-authorise any one-off or recurring payments directly from their bank accounts.

- Access PayTo through existing online or mobile banking platforms to authorise or pause their bill payments, subscriptions, and one-off payments.

Up

Innovative technology and critical strategic partnerships offer customers more choices and better digital experiences. Hence, Bendigo built “Up”, Australia’s first digital-only bank, in collaboration with fintech firm, Ferocia. Since then, the proposition has surpassed initial expectations, amassing over 550,000 customers and AUD 1 Bn in deposits since its inception in 2018.

Up primarily focuses on millennials and Gen-Z and offers features which are relevant to them. Some of the initiatives taken by Up are – Savers, Maybuy, 2Up, Save Up challenge and up tracker.

Cloud strategy

- Engagement with Contino

With aims to deliver a cloud adoption framework and establish efficient DevOps models for immediate business benefits, Bendigo engaged Contino to access its dual delivery and upskilling approach. This model enabled Contigo consultants to facilitate and support the upskilling of Bendigo’s engineers with day-to-day delivery. Bendigo also used cloud tools to help a highly-skilled national team improve the reliability and performance of the bank’s systems. The outcome:

- Migration of 32 workloads into AWS under 30 days

- Improved customer experience

- Faster application deployment through automation

- Partnership with AWS

The partnership is part of a multi-cloud migration project to improve customer outcomes. With it, Bendigo aims to enhance its architecture to increase cost savings and improve the performance and availability of its digital offerings. For a start, Bendigo began running its nonproduct workloads on Amazon EC2 Spot Instances, where the bank achieved resiliency and scalability by implementing other AWS features for fault-tolerant workloads.

To date, Bendigo’s partnership with AWS has allowed the bank to:

- Reduce computing costs by 60%

- Increase workload resiliency by 30%

- Increase banking performance system by 20%

4 growth opportunities for Bendigo

- #1 Enhancement of the branch network

Agencies, corporate, and community-owned are what make up Bendigo’s branch network as of late. It added a new branch to its “branches of the future” initiative to enhance it, leading to six branches. On another note, Bendigo also wanted customers to have better transaction services. Thus, it renewed its partnership with Australia Post in FY2022 for an additional five years, allowing its customers better access to 3,500 post offices across Australia. The bank has also gone above and beyond to facilitate individuals with dementia by partnering with Dementia Australia to create dementia-friendly branches.

However, Bendigo is well aware of the digital phenomenon of online banking today. As a result, it has closed several physical branches because of their low footfall and close proximity to other branches. To counteract this situation, Bendigo has installed trainers and digital coaches to educate customers about the digital products and services that Bendigo offers.

- #2 Cost to serve

Despite closing 23 branches and 15 agency outlets, the occupancy costs of Bendigo have only decreased by 0.55% within the last financial year. The operating revenue has also significantly dipped by 9.24%, while non-interest income has declined by 44.82% between FY21 and FY22. The primary reason for this decline is a reduction in Homesafe’s unrealised revaluation gains resulting from its changes to the valuation assumptions. As a whole, this reduction reflects the changes in the fair value of investment property.

Meanwhile, cost per employee has reduced, leading to a staff increase from 4,483 in FY21 to 4,652 in FY22, a 3.77% increase. As a result, the bank has reduced employee costs from AUD 131,562 in FY21 to AUD 129,858 in FY22.

The current cost-to-income ratio for the bank stands at 59.4%, down from 60.3% in FY21.

- #3 Open Banking

As it stands, Bendigo only shares its customer data with accredited CDR (Customer Data Right) service providers who offer financial products or services, such as a budgeting or insurance comparison tool, which users access via an app or website.

Open banking changes that entirely. For starters, Bendigo can introduce salary on demand, a feature that is becoming increasingly popular with customers. In addition, with open banking, customers can access a wide range of products and services by data sharing with third-party financial service providers. This new form of sharing data helps customers save money on loans, mortgages, insurance plans and other banking services by comparing them with similar offerings from other service providers in a quicker and more accessible manner. Now, customers can consolidate their bank accounts into one app while attaining better visibility and control of their finances.

- #4 Buy Now Pay Later (BNPL)

Up (Bendigo’s digital-only bank) currently offers SNBL (Save Now, Buy Later). The service is called Maybuy. And while Bendigo argues that SNBL is better than BNPL, as customers will tend to avoid making impulsive purchases, which can lead them on the fast track to debt.

However, customers should have access to the flexibility that BNPL provides, especially when many expect the payment method to record a CAGR of 32.5% from 2022 to 2028. Bendigo can also utilise BNPL to increase customer engagement, wallet share and loyalty, creating a more convenient shopping experience. Bendigo can learn from CBA and NAB which offer ‘StepPay‘ and ‘NAB Now Pay Later‘ as their respective BNPL offerings. Both of these offerings allow customer to make payments in interest free instalments with an initial credit limit up to AUD 1000.

The way forward for Bendigo

Being among the few banks to have a very popular neobank among millennials and Gen-Z customers, Bendigo delivers fresh and exciting ways for customers to manage their finances and save for their financial goals. However, to stay afloat and thrive in the competitive banking industry, Bendigo needs to shift gears quickly, adopting BNPL and Open Banking as their key drivers for success.