We see four drivers in BNPL contributing to its exponential growth, both in the transactional volume of online/POS payments and the market share across payment methods. Understanding and capitalizing on these drivers can help banks, merchants, fintechs, and those interested in working on BNPL capabilities identify growth opportunities.

#1 The shift in consumer values and behaviour for D2C brands

Consumers reimagine the consumption of products and services in a new light, especially after the black swan event of COVID-19. Four inflexions define this new light:

- Ultra-convenience: Shop anytime, anywhere online with doorstep delivery

- Time efficiency: Eradicate the dependency on physical store timings

- Cost-effectiveness: Low-cost alternate payment and lending methods, along with incentives and rewards

- Personalisation: Platform-driven virtual stores with customised recommendations and shopping reviews

According to a Google report on Brand.com and marketplace, 41% of brand website shoppers in SEA said brand websites give them an immersive experience. Customers find it motivating to make purchases at sites that provide easy navigation and simple product specifications, including photos and videos.

Therefore, consumers need payment solutions, like BNPL, that enable deferred payments, even for small purchases or to make purchases that otherwise do not fit their budget. This eliminates the friction arising from archaic payments methods, such as debit/credit card charges, high-cost EMIs, interest payments, or even credit card limits.

#2 Need for super-apps

Consumers are no longer excited about juggling between multiple apps but enjoy the benefit of consuming a variety of services through an integrated lifestyle app. The customers of today seek simple, orchestrated experiences, largely driven by ecosystems. Integrating BNPL solutions into retail marketplaces helps in servicing the end-to-end customer journey, enabling customers to make informed shopping decisions. Further, BNPL empowers the customer to create personalised shopping carts, spanning across merchants/retailers and serving multiple customer needs (from travel to apparel to grocery) without the pressure of hidden or unwanted costs.

For example, Alipay is not just a payment service provider, but also a social commerce platform that enables its customers to access a plethora of lifestyle products/services in a single app. It brings in the flexibility, easy, customer-insight led BNPL payment option in partnership with Klarna (a Global BNPL leader). The retail marketplace increased (its) per capita consumption of services for customers, and improved the overall customer experience. Paytm in India, Grab in SEA, Kakao in South Korea are more examples in Asia that exemplify social commerce.

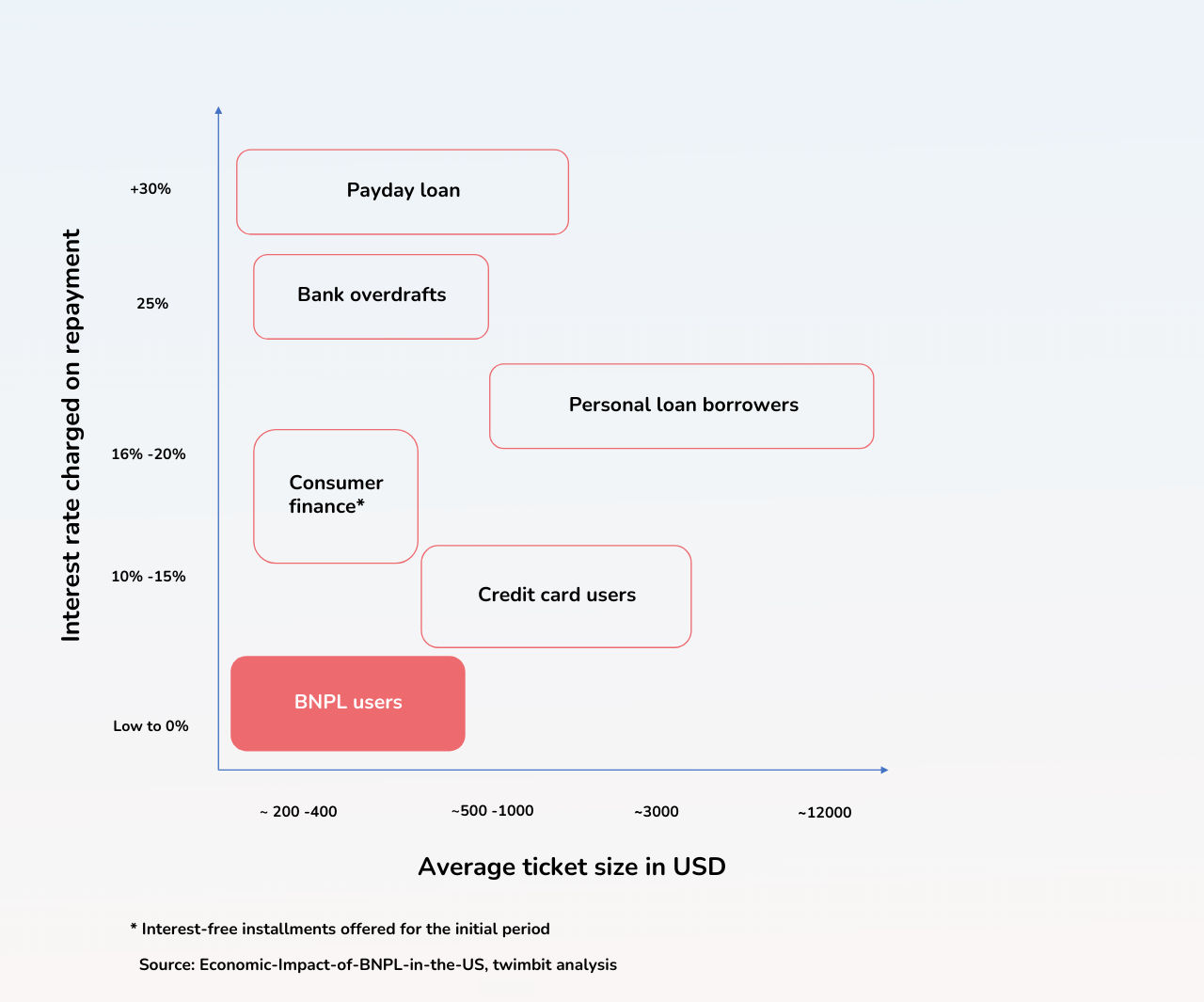

#3 Access to interest-free credit and the rise of a budgetary mindset

To date, credit card dominates as a favourable payment method among the Asia Pacific population by contributing to 29% of total purchases. However, the exponential growth of e-commerce during COVID-19 resulted in a sharp decline in credit card utilisation due to its cost-infused EMIs, high-interest repayment cycles, and annual maintenance fees.

Figure 1: Supporting market expansion

Consumers resort to BNPL, a payment method that gives them greater control over their spending and easy access to credit compared to traditional lending methods. It provides the ability to make purchases that a consumer can adjust to their financial needs and allows real-time tracking of spend categories at no upfront cost.

#4 Increase in revenue opportunities for merchants and banks/fintechs

There is a paradigm shift in SME owners’/merchants’ preference toward digital payment and lending options. These options enable the merchants to access a larger customer pool and drive low-cost acquisition, especially those that are credit or cash-constrained at a time. The options develop a force for inclusion in emerging Asian economies with large underbanked and unbanked populations that rely on expensive loan and credit options to make small-ticket purchases.

Banks or fintechs that offer BNPL capabilities directly impact the top-line growth through the merchant fees associated with every partner merchant. The fees range between 2% to 5% of the transaction value.

Way forward

It is evident with the existence of these value drivers that customers are willing to exercise BNPL options when making their purchases. We expect BNPL to cross USD 1 trillion in spend value by the end of 2022, giving an opportunity to existing and potential players to thrive on it.

The opportunity will further expand in this decade with the inclusion of new digital customers, joining from non-metros and rural areas in the Asia Pacific region. It should be a mission-critical priority for banks, neobanks, and fintechs to act fast and pave an entry path into the BNPL market, capitalising on the massive revenue opportunity. Merchants and big-box retailers must lead with analytics on customer behaviour and preferences to continuously determine new product/service segments for BNPL solutions, including bundling, re-bundling or unbundling products/services across categories.