Company Insights

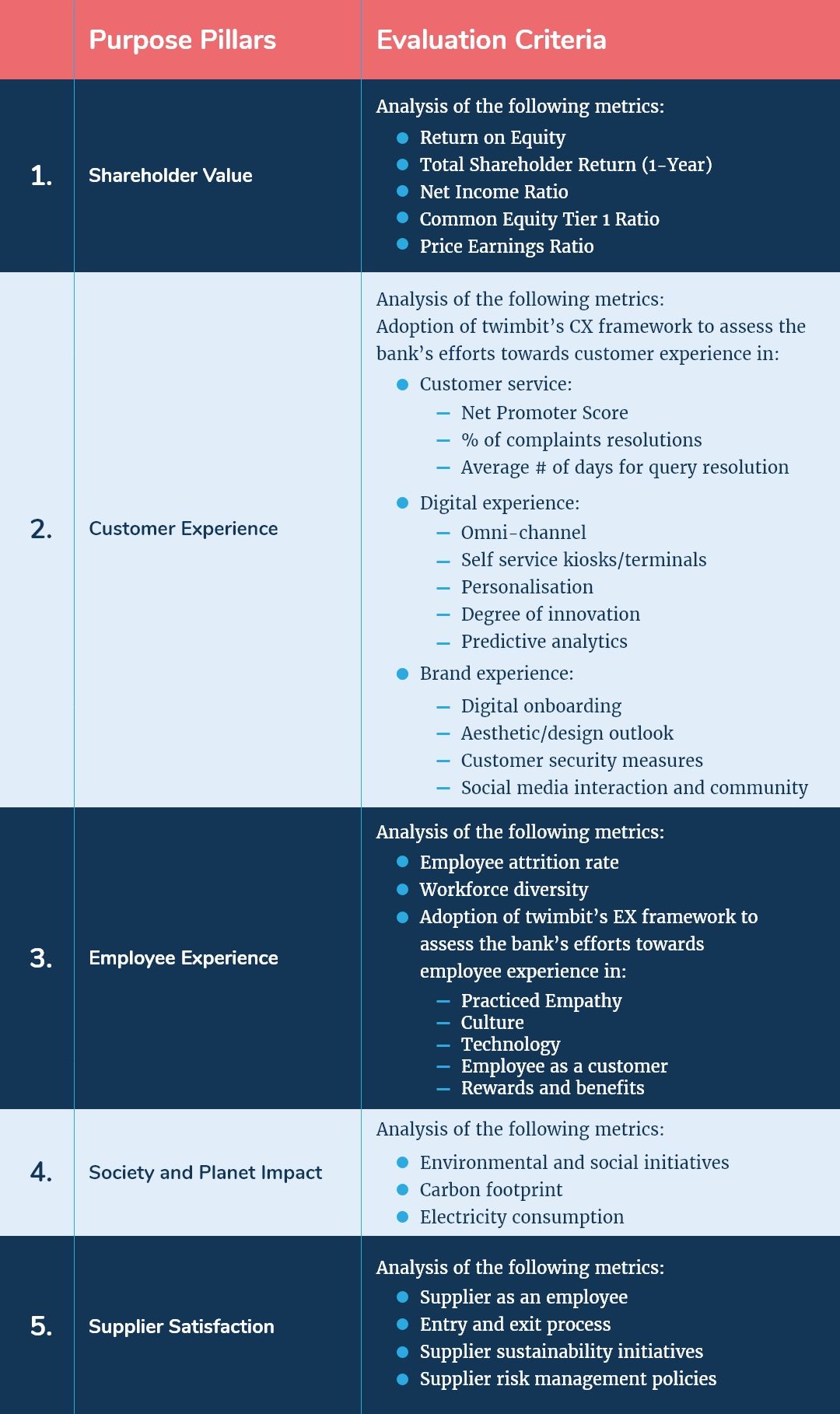

twimbit’s Purpose Index

Source: Refer to the methodology in Appendix A below

Bank of Baroda Group Financials- An overview as of 31st March 2021

| Bank Name | Bank of Baroda (BOB) |

| Headquarters | Mumbai, India |

| Operating revenue | USD 1.1 billion |

| Group net profit | USD 111 million |

| Total assets | USD 1.55 trillion |

| Employees | 82000+ |

| Countries in operation | 18 |

| Number of branches | 8214 |

| ICT spend | N/A |

| Number of customers | 131 million |

| Market capitalisation | USD 6.77 trillion |

| Operating revenue CAGR growth (2016-2020) | 15.2% |

2. Conversion rate to USD as of 31st March 2021 – 0.01366 USD

Shareholder value

| Return on equity (as of 31st March 2021) | 1.50% |

| Total shareholder return (1-Year) | 6.85% |

| Net income ratio | 50.1% |

| Common equity Tier 1 ratio | 14.99% |

| Price-earnings ratio (as of 31st March 2021) | 12.60 |

2. The P/E ratio is in the trailing method till 1st November 2021

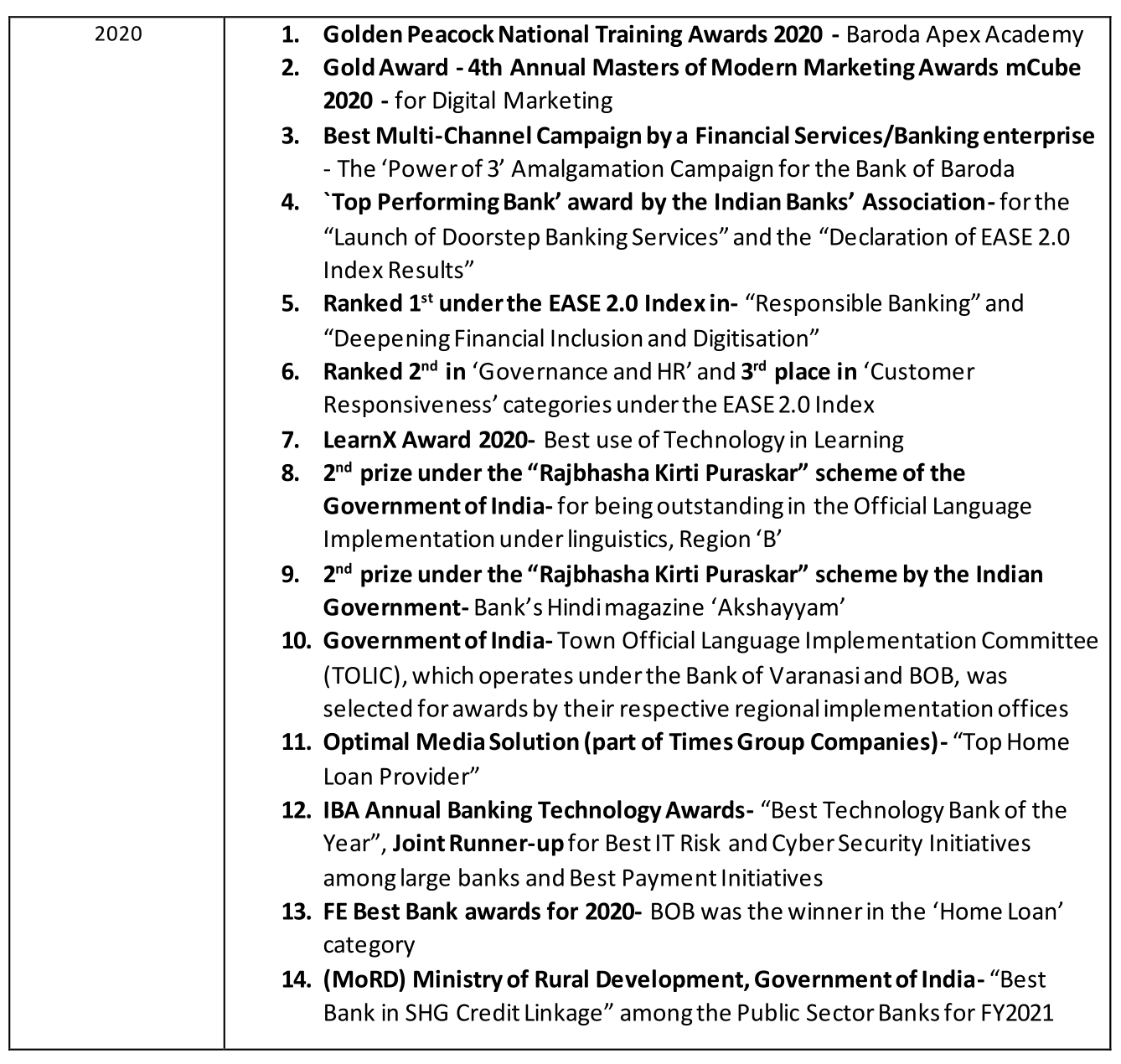

Awards

Bank of Baroda (BOB) and its strategic focus areas

BOB has embraced BOB-NOWW, a transformation journey to provide a better experience to every customer. The word NOWW stands for the bank’s effort to design and adopt a “new operating model and new ways of working.”

The goal for BOB is to build an industry-wide first operating model through new ways of working and a newly designed retail network that opens up growth potential across all businesses. It will also include the introduction of digitisation at all levels to optimise costs and increase productivity.

The bank devised strategies and took the following initiatives to remodel itself as the bank for the future. It has five foundational pillars, viz.,

Mobile-first and digital-led experiences: A critical part of BOB-NOWW is to drive the digitisation of banking processes and services by

- Creating an organisational structure and operating model that comprises cross-functional agile squads with representation from essential bank departments which will speed up the rollout of new digital banking services and journeys.

- Revamping existing customer journeys to bolster the BOB mobile banking app by offering the latest banking services (such as options for consumers to pay insurance premiums and invest in mutual funds).

- Digitising user interfaces at the branch level through self-service kiosks, allowing for faster and more direct transaction processing.

Reimagined network: Following its motto, “BOB Everywhere”, the bank is expanding its network,

- Through Business Correspondents (BC) by providing services to a bigger pool of customers in a larger geographical area

- In rural areas, through the adoption of accessible and small digital branch formats, providing consistent customer experience (CX) across the country

Unlocking growth across existing and new product lines:

- Strengthening business offerings across all revenue lines and focusing on international, corporate, MSME and wealth segments

- Plans to offer a full product stack of corporate banking solutions to its clients

- Launch of the corporate fee booster campaign, sales war room, and the revamp of the trade finance and supply chain finance platforms

- Redesigning its wealth management strategy to maintain, activate and deepen relationships with existing customers

- Hiring requisite talent to scale up its wealth management offering

New ways of working:

- “Work from Anywhere” for a few of its employees in some roles to enable a better work-life balance and improve employee productivity. It has already implemented a hybrid working model on a pilot basis. BOB will incorporate learnings from the pilot plan into its programme design.

- Launch of a bank-wide campaign called “Let’s Simplify” to crowdsource ideas and take them under consideration for implementation.

- Customer experience

BOB is constantly striving to set industry standards and pioneer new products, processes, and service delivery innovations critical to offering a smooth experience for its customers. As a result, it took the following measures:

- Monitored and improved client interactions across channels and channel capabilities to make banking from home easier

- Ensured that frequently used features were accessible via digital channels and the call centre. Customers could communicate with the contact centre 24 hours a day, 7 days a week in their preferred language. The bank expanded the linguistic capacity to nine regional languages (in addition to Hindi and English)

- Popularised the Customer Grievance Redressal System (a CRM package module) with timed auto-escalation, the attachment of documents, feedback on resolution quality, and the ability to reopen complaints

- Conducted surveys to assess customer satisfaction levels across segments

- Tracked the service level of the whole branch network through Mystery Shopping, Service Audits, and Workshops and performed these audits via video conference during the COVID-19 pandemic

- A sub-committee of the board of directors analysed customer input obtained through the “Voice of Customers” and compared the bank to its counterparts on numerous aspects to improve CX

- Ensured that all branches, ATMs, and e-lobbies had ramps, comprehensive notice boards (displaying pertinent and up-to-date information), and a designated queue for elderly folk. Branches received a makeover as well, with emphasis on improving CX through a better ambience and an expanded seating area, and a special focus on senior citizens and differently-abled customers

- Launched its super app named ‘bob World’ with the goal of bringing all banking services under one roof (by combining over 220 services into a single app that covers almost 95% of all retail banking services), which is also accessible to domestic and international clients

- Launched ‘Insta Click Savings Account,’ a paperless digital self-assisted internet savings account. It employs a new type of digital KYC (Know-Your-Customer) and an Aadhaar-based OTP authentication for customers, which is accessible via the bank’s website, a mobile phone, an iPad, a laptop, or a computer. This new feature activates accounts in real-time, and customers can also subscribe to various digital channels [like Internet banking, mobile banking, UPI (unified payments interface), and debit cards] through the product

- The bank took the following efforts to promote financial inclusion:

- Enrolment in microinsurance through numerous methods (including missed calls, net banking, mobile banking, SMS, Branch Correspondent, and branch).

- Services such as initiating a request for an SMS subscription, email statement, a debit card hot-listing are available. In addition, the Aadhaar look-up and Aadhaar OTP-based authentication of BC agents during transactions are also available at a BC point.

- The integration of the Pradhan Mantri Street Vendors’ Atmanirbhar Nidhi scheme’s (PM SVANidhi) portal for onboarding street vendors and supplying them with Unified Payments Interface (UPI) Quick Response (QR) codes.

- Under the KCC scheme, BOB partnered with Aquaconnect to generate formal credit for over a million farmers.

- In collaboration with KapitalTech, a fintech lender, to provide loans to the MSME sector following the Reserve Bank of India’s co-origination requirements (RBI).

- Employee experience

The bank is constantly launching new initiatives to grow and develop its human resources, including recruitment, addressing staff training needs, employee engagement, and competency building. It has implemented a number of new employee-centric initiatives as part of its organisational transformation projects (involving people, processes, and systems) and activities to reform core systems and practices.

During the year, BOB took the following initiatives:

Manpower Planning and Recruitment:

- Developed a new scientific manpower planning model for estimating skill-based personnel requirements at different levels. The model aids the bank in making important strategic decisions (including recruitment, deployment, promotions, and training)

- Hired specialised people with knowledge in niche and critical emphasis areas to expand its capabilities in several domain areas

Baroda GEMS “Growth and Empowerment Management System”:

- Introduced Baroda GEMS Performance Management System (PMS), a new scientific and objective Performance Management System that is also developmental and meant to identify areas of improvement for employees. This robust PMS paved the way for a series of revolutionary efforts, each aimed at realising previously unrealised productivity gains:

- Target-setting that is scientific and personalised, with a built-in market forecast.

- INSIGHT is a first-in-industry solution that provides employees with personalised performance metrics and forward-looking priorities, as well as system-generated feedback to help them improve their performances.

- There are pre-defined job, family and career path options that allow employees to follow a career of their choice, and focus is on the career path they pick.

- BRITE (Baroda Rewards for Individual & Team Excellence) is a comprehensive reward and recognition programme that connects performance and results.

Employee Assistance Programme:

- Introduced a ‘workplace counselling’ plan called ‘Employee Assistance Programme’ (EAP). BOB enlisted the help of a professional EAP service provider to provide counselling services via a number of channels (including face-to-face counselling, phone and videoconferencing, emails, and chats). Employees could now address issues like anxiety, depression, stress, family problems, any traumatic situation, motivation, personal development, work-life balance or any other issue through counselling.

Baroda Anubhuti Programme:

- This is an employee engagement programme aimed at encouraging teamwork and collaboration, as well as creating a joyful and enjoyable workplace

- BOB initiated initiatives to improve the overall employee engagement levels, like Employee of the Month, Spot recognition that captures “Wow” moments, a fun hour at all branches and offices, etc.

- Once every six months, all branches and offices participate in mandatory community service programmes

Measures amid the worldwide COVID-19 pandemic:

The following are some of the efforts taken by the bank to provide prompt assistance and support to its workers throughout the pandemic:

- Provision of isolation rooms for COVID-positive staff workers in cities where the virus was spreading rapidly, and hospital beds were scarce

- Employees reimbursed for hospitalisation and home quarantine expenditures related to COVID-19 treatment

- Payment of a flat sum of USD 333 to COVID-infected employees to cover miscellaneous expenses (such as treatment and transportation)

- Payment of USD 40,000 in ex gratia or additional financial aid to employees’ dependents in the event of death due to COVID-19

- Children of employees who died in harness as a result of COVID-19 are eligible for scholarships up to graduation

- Established a COVID helpline at zonal centres and the Corporate Office to allow employees to seek help in the event of a COVID-related emergency

- Provided a ‘Doctor-on-call’ facility for all its employees for any concerns related to general health and wellness

Learning and development:

The bank believes that learning and development plays a vital role in shaping the organisation’s human capital. It took the following initiatives:

- The bank has a sophisticated learning management system, Baroda Gurukul, which provides learning through a variety of channels (including Digital Library, Weekly Quizzes, Baroda Radio, e-learning modules, Baroda Tube, Margdarshak, etc.)

- Baroda Apex Academy carried on its training delivery and efforts by taking the following initiatives:

- Introduced Baroda e-Academy, a virtual teaching platform powered by Microsoft Teams

- Launched Baroda Tuber ‘Each One Teach Many’ campaign on Learners’ Day to encourage the use of peer-to-peer learning

- Developed a new onboarding and mid-career programme called the ‘We Lead’ Leadership Development Program. Following the COVID-19 outbreak, BOB re-evaluated its entire portfolio of learning offerings. It reset priorities on what would be the benchmark to adapt to a virtual or digital-only format, ensuring continuity and the spirit of the programme.

- Society and planet impact

BOB is committed to contributing to society’s wellbeing, particularly to the upliftment of the impoverished, in order to bring about long-term social change in their lives. Therefore, skills development through training for gainful employment, human welfare, and other social activities for women and farmers are among the bank’s primary focus areas:

- BOB has established 64 Rural Self Employment Training Institutes (RSETI) across the country to provide skill development training to rural and semi-urban youths to generate self-employment

- Established 85 Financial Literacy and Credit Counselling Centres (FLCCs) to give financial counselling and education to people in rural and urban regions about the various financial products and services offered by the official financial sector. These centres also engage in activities that encourage financial literacy, banking service awareness, digital banking, financial planning, and the alleviation of a person’s debt-related distress.

- The bank took the following steps to reduce its carbon footprint:

- The Indian Green Building Council awarded BOB a Green Building Certificate, a GOLD rating for the Baroda Corporate Centre and a SILVER rating for the Baroda Sun Tower Building in Mumbai (IGBC)

- Use of Solar energy to power 120 branches in rural and semi-urban areas

- Replaced traditional light fittings in all branches and offices with energy-efficient LED lights that use half the power of traditional lighting

Digital strategy

BOB is committed to digitisation and aims to shift transactions to digital channels as soon as possible, resulting in a better customer experience. The main goal of digital banking is to make banking products available to customers via digital channels. The following are the most important digital banking instruments:

- Mobile Banking: Added pre-approved Micro Personal Loan, passbook, Public Provident Fund (PPF) account opening, UPI facility, positive pay confirmation for inward cheques, debit card management, spend analyser, a Mini statement without login, and other features and services to the bank’s mobile banking application during the year

- ATM: For a pleasant experience, ATMs come equipped with user-friendly visual screens and simple instructions in the customer’s preferred language. Generation of green pins, bill payment, National Electronic Fund Transfer (NEFT) and other functions are also available

- Debit cards: A total of 31 campaigns were launched with merchants (such as Jio Mart, Ixigo, Myntra, Swiggy, EaseMyTrip, Yatra, Zomato, Uber, and others) to provide offers to debit card customers

- Internet Payment Gateway (IPG): Set up the bank’s IPG infrastructure to provide a digital payment system, Baroda e-Gateway, for its customers, allowing them to collect payments via their own website/e-commerce business by accepting credit/debit card and net banking payments

- Baroda FASTag (National Electronic Toll Collection – NETC): The bank’s FASTag is now available online and through TAB banking to customers of other banks

- BHIM Baroda Pay is a UPI system that combines many banking services, seamless fund routing, and merchant payments into a single mobile application. It also handles “Peer to Peer” collection requests, which can be scheduled and paid according to need and convenience:

- UPI Autopay: Introduced as part of UPI 2.0, this feature allows consumers to set up periodic e-mandates for recurring payments such as mobile bills, electric bills, EMI payments, entertainment/over-the-top (OTT) subscriptions, mutual funds, and so on

- UPI International: UPI International is a joint initiative of the National Payments Corporation of India (NPCI) and the Singapore NETS (Network for Electronic Transfers) to promote QR-based payments using the UPI application in Singapore Dollar (SGD). The account will be debited in INR, while the merchant receives compensation in SGD

- WhatsApp Banking: The bank launched WhatsApp Banking as a new age delivery channel for providing banking services to customers and non-customers using the WhatsApp Messenger application. Customers received 13 services, while non-customers received 5. In the next phase, BOB intends to integrate 11 other services into the platform, which will increase client convenience and the banking experience even further

- bob World: In 2020, a new super app with 220 features, enhanced capabilities, and a user-friendly interface was released

- Baroda TabIT: Through its TAB banking platform, the bank streamlined its customer onboarding process through tablet for rapid CASA opening, as well as a slew of services (Personalised Cheque Book, Personalised Debit Card, Mobile Banking with MPIN, UPI, and so on). BOB is now extending FASTag issuances and the on-boarding of merchants for availing UPI services

IT strategy

Digitisation is necessary for the continuous evolution and upgrade of IT infrastructure. Among the significant projects BOB carried out in FY2021:

- The Analytics Centre of Excellence has expanded its Big Data Lake (BDL) platform (ACoE). Internal sources include domestic and international core banking, treasury management systems, LLPS, mobile banking, and internet banking, as well as external sources such as Credit Information Bureau (India) Limited (CIBIL), CRIF High Mark Credit Information Services Pvt. Ltd (CRIF), Capital Line, and others

- BOB designed multiple dashboards with vivid visualisations, extensive Key Performance Indicators (KPI), and dimensions to deliver actionable insights to varied verticals. These dashboards address both business and regulatory or compliance requirements up to the branch level

- Developed multiple predictive models for retail, MSME, wealth cross-selling, treasury asset and liability management (ALM), collection management, among others, to assist BOB with revenue, cost and risk initiatives

- Completed Finacle 10’s CBS application upgrade for all 17 overseas locations

- Developed the Centralised Positive Pay System (CPPS) for Cheque Truncation System (CTS) clearing, enabling customers to reconfirm the key details of issued cheques through various alternate delivery channels and branches

BOB ecosystem

The bank involves itself in developing fintech partnerships, launching new products and reinventing business processes. These are initiatives during FY2021:

- Integrated the PSB59 loan site with the company’s internal loan processing system, LLPS, for its retail, MUDRA, and MSME products, allowing for the smooth flow of all information and thus improving the TAT (turnaround time).

- BOB also launched the Baroda StartUp programme in February 2020. It is also working on a specific credit product designed to meet the financial needs of start-ups.

- The BOB Innovation Centre (BOBIC) established the first partnership between a PSB and a technology institute in BFSI (Banking, Financial Services and Insurance) in association with IIT, Mumbai. They will be working on five important banking technology projects.

Security strategy

BOB has a well-defined framework for cybersecurity governance that operates through a combination of management structures, policy frameworks, and operations management. The bank is compliant with the NIST (National Institute of Standards and Technology) cybersecurity framework and the RBI cybersecurity framework. In addition to the existing controls, BOB is taking the following steps to enhance cybersecurity:

- Deception Technology, which tries to prevent cybercriminals who have infiltrated the network from causing any harm to the bank

- Conducted regular Random Early Detection (RED) team exercises to provide useful and objective information about the vulnerabilities and the efficacy of existing defences and mitigating mechanisms

- Contacted a reputable insurance provider to provide a Cyber Insurance Policy to safeguard businesses and individuals from internet-based hazards and frauds

- The bank implemented the following for a more secure experience:

- A web-based Enterprise Governance, Risk and Compliance for the systematic and integrated management of operational risk (SAS EGRC) and an operational risk management Statistical Analysis System (SAS)

- The control environment was enhanced by monitoring the Key Risk Indicators Program (KRI), the Risk Control and Self-Assessment Program (RCSA), and root cause analysis

- As part of Operational Risk Management and Root Cause Analysis, the bank built an internal loss data warehouse. It has also developed a CTMU to monitor all domestic transactions from a Know Your Customer/Anti-Money Laundering/Combating the Financing of Terrorism (KYC/ AML/ CFT) viewpoint to minimise and control operational risk at the transaction level

- The bank separated the consumer interface (front office) from transaction execution (back office) by centralising various back-office processes

ICT contracts

- Founding member of Blockchain consortiums- BIC (Blockchain Infrastructure Company) and Bank-Chain for Distributed Ledger technology

- Alliance with RazorPay for developer-friendly API and seamless integration technology

- BOB association with ToneTag for contactless proximity communication using sound waves

- Tie-up with Truecaller for offering UPI payment services of BHIM Baroda Pay UPI app to users on their app via a secured API gateway

9 Growth and Innovation opportunities

- #1 Cost to serve

BOB saw an increase of 9.17% in its operating profit with USD 277 million in 2021 compared to USD 253 million in 2020. While the growth was good for BOB, the bank also experienced a notable increase of 8.85% in operating expenses from USD 25.3 billion in 2020 to USD 27.6 billion in 2021. On the other hand, the cost-to-income ratio of the bank had decreased marginally from 49.97% in 2020 to 49.90% in 2021.

The bank witnessed an increase in personnel costs from USD 12.8 billion in 2020 to USD 15 billion in 2021. However, there was an overall decrease of 1,397 in the workforce count from 84,283 employees in FY2020 to 82,886 employees in FY2021. A possible inference is that the bank laid off non-performing staff and added employees with specialised competencies to support their digital growth objectives, hence the increase in personnel cost. Branch maintenance also amounted to USD 212 million in FY2021 compared to USD 356 million in the previous year. This decrease is the result of the merger of many branches.

There was a slight decrease in the net interest margin compared to the previous year from 2.73% in FY2020 to 2.71% in FY2021 and also a decrease in gross NPA from 9.40% in FY2020 to 8.87% in FY2021, which bode well for the bank.

While the bank is making an effort to become digitally efficient internally and externally – it must take stringent measures to manage its operating expenses. Therefore, BOB should focus on the following significant areas to optimise cost efficiency:

- In a low-interest-rate environment, BOB should detect payback risk in loans and attrition risk in deposits to manage a positive net interest margin. Additionally, the bank can develop a predictive behavioural model to adjust its interest-rate risk estimates and hedging strategies continuously

- The bank can focus on non-interest income and complementary revenue streams to offset the impact of substantial NPA provisions

- Consolidate its vendors to decrease costs and also maintain vendor relationships, so the bank gets optimal costs and thus cuts vendor costs in the long run

- Increase focus on retail and SME business with tight control on the asset quality as these are the businesses with the maximum market share

- BOB can apply RPA-enabled audit trails for red-flagging any high-cost inflexions by implementing transaction-level transparency

- #2 Transformation of the branch and its branch networks

BOB completed an integration with Dena and Vijaya Bank. As part of the integration, the bank has merged or rationalised 1,310 branches and 1,135 ATMs during 2020. Simultaneously, BOB has boosted its Business Correspondent (BC) network by 5,200 to 23,320.

From 2019 to 2020, BOB reduced its physical network costs by USD 144 million. Although the number of branches decreased from 9,482 to 8,214 in comparison to last year, this decrease in maintenance cost might be due to the optimisation of its branch network after amalgamation. The branches and ATMs in close proximity to each other have been brought together under one roof, thus reaping synergies from the merger.

Consequently, the maintenance cost of branch networks experienced a reduction. For this reason, the bank should continue its efforts to reduce non-performing branches or ATMs and focus on transforming the network through:

- BOB can replace ATMs with self-service kiosks, making it easier for consumers and saving costs in the process.

- The bank should transform high business volume and high-customer-headcount branches into flagship digitalised community hubs to enhance the in-branch experience and redefine customer engagement. To accomplish this, BOB should:

- Introduce smart counters – BOB can move many personnel services to smart counters, reducing the need for human tellers to work in bank branches. Furthermore, smart branch technology enables a personalised sales strategy and 24/7 access to the bank branch.

- BOB can establish an omnichannel user experience for all its customer touchpoints (internet banking, mobile banking, physical branches, virtual assistants, other automation processes, etc.). This holistic channel provides customers with a consistent experience across the board, resulting in overall higher banking efficiency.

- While high-traffic, high-visibility urban locations imperatively require bank staff, BOB can establish fully self-serviced branches for greater physical footprint penetration at lower costs. Moreover, these branches will be able to provide complete services through video conferencing.

- #3 Customer experience

The bank is in the process of leveraging CRM tools to use analytics and AI to transform and build digital capabilities. BOB believes that these digital tools could garner a more positive customer experience in the future. The bank uses technology to provide and manage its varied, strong portfolio of products and services, delivering them in a customer-centric and personalised manner.

The bank can further leverage its capabilities through AI and can work in these areas to optimise the customer experience journey:

- The bank should move towards providing an omnichannel experience to its customers so that they have the same digital and physical experience.

- BOB provides customer support 24/7. The contact centre handled 39.5 million customer calls during 2020. It can further gather and analyse data from the customer calls and personalise the services for a better customer experience.

- The bank takes up to 15 days to handle a complaint. It can prioritise chatbots, virtual assistants, and video conferencing to increase the number of complaints handled.

- It can also provide insights for customers into their saving and spending patterns with specific recommendations to help them meet their financial goals.

- BOB can introduce a gamified user interface to make the customer experience interactive rather than monotonous.

- It should also introduce virtual assistants and chatbots as a first port of call for customers.

- BOB could introduce a different platform to serve the high-net-worth individuals with more sophisticated investment needs.

- AI-powered voice banking is another suggestion to deliver proactive, personalised, and automated money management.

- The bank can create customer personas and hyper-personalised product offerings with the help of ML/AI models.

- It can establish a digital investment dashboard providing high-net-worth clients with a comprehensive snapshot of their portfolios, allowing them to monitor and manage their assets in real-time.

- #4 Employee experience and productivity

There have been notable investments in employee development and the presence of a flexible work atmosphere in BOB. Nevertheless, the bank should consider the following strategies:

- Expand its employee wellbeing plan by focusing on mental, emotional, spiritual, and physical wellbeing programs through:

- Gender-neutral parental leave

- Childcare facilities

- Domestic & family violence workplace support for women

- Use AI chatbot and virtual recruitment assistant to match suitable candidates with high-skill jobs.

- Provide hassle-free student loans to new hires to monitor their attrition rates, increasing employee loyalty.

- Supply confidential service and special fund access granted from a team of dedicated specialists towards employees experiencing financial hardship and needing help.

- #5 Migration of workload to the cloud

BOB invested over USD 130,000 in cloud technology. This is a very minimal spend as percentage of the overall IT budget. The bank can invest more in cloud technology to amplify its capabilities via these strategies:

- While regulations could limit the adoption of cloud, a starting point is the ability to use a cloud-based platform to streamline various talent management and HR-related tasks.

- Increase efficiency through cloud adoption, improving various additional activities beyond the customer and employee experience. For example, the bank can now extend data storage and data-driven activities across security, regulatory compliance, auditing, and pan-organisation communication pipelines to modernise its overall operating model.

- Shift most operations to the public cloud as the long-term strategy, enabling BOB to secure end-to-end encryption on all its confidential data within the cloud, achieve higher scalability and be more cost-efficient.

- #6 Neo banking

BOB has added significant features and integrated many functions into its mobile banking app, bob World, to make it more appealing. Still, it needs a transformational neo banking strategy to compete with other rising neobanks in India. It does this by having a podcast- ‘Fintalks@bobworld’ to appeal to millennials more. BOB also partnered with Interactive Avenues for a digital transformation that would cater more towards millennials and Gen-Zs under its digital banking platform.

It can implement these initiatives as well:

- Introduce an in-app virtual assistant to deliver proactive notifications, budgetary recommendations, as well as lending and investment choices to customers.

- Aim to hyper-personalise its products to fulfil customers’ unstated and hidden demands.

- Introduce customised debit cards, credit cards, and virtual cards.

- Give more flexibility to customers when navigating product possibilities by introducing bite-sized loan and investment solutions.

- Gamifying numerous consumer touchpoints. These include awarding badges for increased product usage, providing loyal customers with discount coupons, creating a leader board between friends and co-workers based on product purchases, as well as showcasing trending products.

- Enable multi-currency accounts with zero to minimal cross border remittance fees.

- The bank should integrate customer data from its legacy banking channels and leverage open banking; this will enable it to:

- Have access to historical customer transactions and credit history data

- BOB could utilise the same data to automate the application approval process at the back-end, helping it build a robust customer remediation process.

- The bank can introduce interactive dashboards, create online community hubs, blogs or resources on financial literacy functions to create a unique brand name.

- #7 Artificial intelligence (AI) in everything

BOB is at an early stage of adopting artificial intelligence (AI) capabilities. As it is in the early stage of adoption, the bank should begin with:

- Automating labour-intensive back-end and iterative daily tasks (like customer onboarding, document collation, book-keeping, sales recording, etc.) through RPA to reduce labour redundancy and increase the bank’s overall operational efficiency.

- Introduce a sophisticated and forward-looking credit profiling method for business banking customers. It can use predictive analytics to assess loan credibility beyond financial statement analysis. Other essential criteria that can be a part of the profiling mechanism include economic KPIs, market and industry trends, bank and system facility overviews, and more.

- The bank can leverage its data analytics capabilities to seek contextualised data insights that it can use to innovate its product offerings and delivery channels.

- BOB can execute AI-programmed marketing of products and targeted campaigns based on the past behaviour of customers.

- The bank can extend AI services beyond banking and focus on customer problems rather than just financial needs to become a trusted advisory service beyond banking.

- #8 Society and planet contribution

The primary areas BOB focuses on are skill development, human welfare and other social activities for women and farmers. However, it should aim to reduce its carbon footprint by using the following strategies:

- Building on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid in more areas

- Utilise energy-efficient devices by making one-time investments and saving costs in the long-term

- Use excess energy during low or off-peak times to decrease energy usage

- Reduce its carbon footprint even more by converting to pulper cards, eco ink and carbon control press machines

- Launch supporting projects in impoverished areas, which help to preserve biodiversity and drive reforestation while furthering local economic mobility

- #9 Cybersecurity

To enhance cybersecurity and avoid scams, the bank can implement the following initiatives:

- Enhance security and surveillance monitoring of malicious online activities, as scammers tend to resort to phishing to defraud customers

- Deliver a general security awareness programme to employees via an e-learning platform

- Invest in ML capabilities and security orchestration in a bid to stay ahead in the cyber arms race

- Implement a robust multi-factor authentication system and micro-segmentation to secure internal access to key applications and limit attack surfaces

- The bank can further develop its in-house:

- Risk-based vulnerability management programme to improve cyber risk prioritisation and mitigation efforts

- Crowdsourced cyber threat intelligence platform to provide predictive analysis of potential cyber threats and attacks

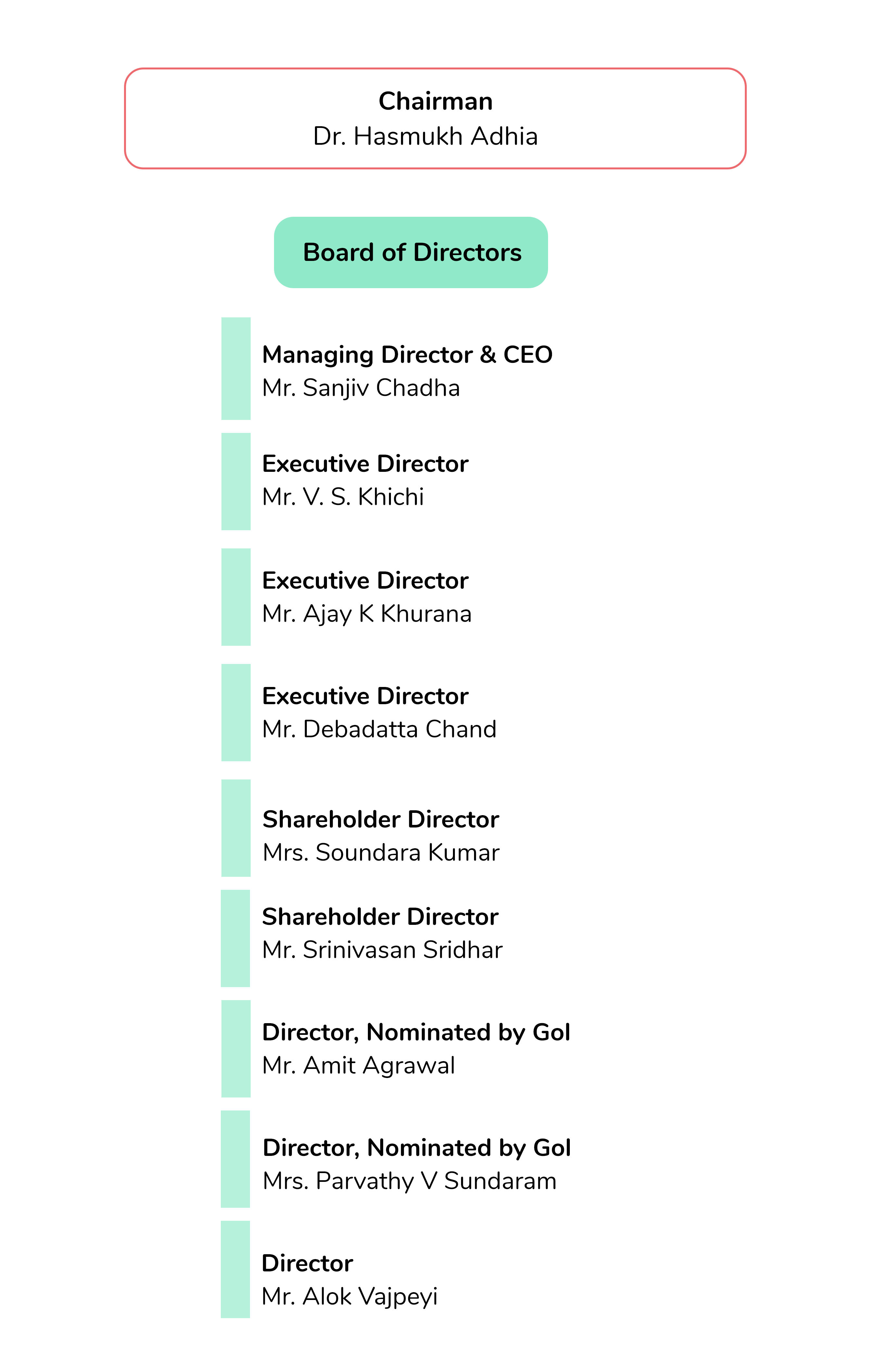

Organisation Structure

Executive Profile

Dr. Hasmukh Adhia

Non-Executive Chairman

Dr. Hasmukh Adhia is a non-executive Chairman of the Bank of Baroda. He has a Postgraduate degree in Accountancy and holds a Ph.D in Yoga from Swami Vivekanand Yoga University, Bangalore. He held the post of Secretary with the Department of Financial Services in the Ministry of Finance, Government of India before his posting as the Finance Secretary.

Mr. Sanjiv Chadha

Managing Director & CEO

Mr. Sanjiv Chadha has over 32 years of experience in the banking industry. He worked as the Deputy MD, SBI and MD & CEO of SBI Capital Markets Ltd., the Merchant and Investment Banking arm of SBI, before joining BOB. His areas of expertise include Retail Banking, Investment Banking, Corporate Finance, Structured Finance, Mergers & Acquisitions and Private Equity.

Quote

- Technology and Innovation, Times of India Article 2021

Today, we have 13 million customers using bob World, which is a very robust platform and scalable. The thought was to enable everything that can be done in the branch within the app.

Mr. V. S. Khichi

Executive Director

Mr. V. S. Khichi holds an MBA (Finance and Marketing) degree, with Professional Qualifications of CAIIB and Associate in Life Insurance. He worked as Field General Manager (Gujarat Operations) in Dena bank before joining Bank of Baroda.

Mr. Ajay K Khurana

Executive Director

Mr. Ajay K Khurana joined Bank of Baroda as an Executive Director in 2020. He has a postgrad degree in business management and a CAIIB professional qualification. Before joining the Board of Bank of Baroda, he was an Executive Director on the Board of Syndicate Bank. Mr Khurana has a diverse background as a result of his employment in key departments such as Audit, Information Technology Department, NPA Recovery, International Banking, Operations, and Corporate Credit.

Mr. Debadatta Chand

Executive Director

Mr Debadatta Chand was appointed as Executive Director of Bank of Baroda in 2021. He holds degrees in B.Tech, MBA, CAIIB qualified Banker with a Postgraduate Diploma in Equity Research and Certified Portfolio Manager. In addition to 27 years of experience in Commercial Banks and Developmental Financial Institution, Mr Chand has attained operational and strategic banking exposure with unique expertise in Treasury & Investment Banking and Market Risk Management.

Mr. Amit Agrawal

Director

Mr Amit Agrawal has been determined as the bank’s Government Nominee Director. He has served the Indian Administrative Service since 1993. He has been an alumnus of the Indian Institute of Technology Kanpur He serves as Additional Secretary with the Ministry of Finance in the Department of Financial Services.

Mrs. Parvathy V Sundaram

Director

Mrs Parvathy V Sundaram has been appointed to the bank’s Board of Directors as an RBI Nominee Director. Mrs Sundaram began her career as a commercial banker and, after a two-year tenure, transferred to the Reserve Bank of India in 1984, where she worked in every major department of the RBI across five locations.

Mrs. Soundara Kumar

Director

Mrs Soundara Kumar joined the board of directors as a representative of the bank’s shareholders for a three-year term. She received her bachelor’s degree in mathematics from Stella Maris College in Chennai. Then, she joined Bank of Baroda as a Probationary Officer in 1975 and has held several positions such as branch manager, SME manager, retail manager, and rural and agriculture manager (Financial Inclusion).

Mr. Srinivasan Sridhar

Director

Mr Srinivasan Sridhar joined as a director representing Shareholders of the Bank. He holds a B.Com(Hons.) degree from Delhi University and has a professional qualification as a Chartered Accountant. He has experience in Management Strategy, Client Coverage Models, Product and Distribution Strategies, Cost Optimization, etc.

Mr. Alok Vajpeyi

Director

Spanning nearly 40 years, Mr Alok Vajpeyi has a career in financial services and governance across global capital markets, investment and wealth management. He was appointed to the Board of Bank of Baroda in July 2021. Mr Vajpeyi is an Associate Member of the Institute of Chartered Accountants in England & Wales, having received a BSc (Econ) degree specialising in international trade & development, from the London School of Economics.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Bank of Baroda, (2021, March 31). Annual Report 2021

https://www.bankofbaroda.in/writereaddata/Images/pdf/AR2020-21.pdf

Wall Street Journal. Bank of Baroda financials. Retrieved October 15, 2021, from

https://www.wsj.com/market-data/quotes/IN/XBOM/532134/financials

Aquaconnect partners with Bank of Baroda to generate formal credit for over a million farmers. The Economic Times. (n.d.). Retrieved December 6, 2021, from

Bank of Baroda-KapitalTech tie-up to provide loans to MSMEs, small businesses. Zeebiz.com. Retrieved December 6, 2021, from