The race to be the first AI Superpower and its implications for Southeast Asian businesses

In Q1 2020, Asia generated the largest search volume on Google for topics related to Artificial Intelligence, with an estimated 1 in 3 queries for AI-related topics. This includes interest shown in learning about AI, Machine Learning, data processing and Python (programming language) – a strong indication of the region’s growing interest in the field.

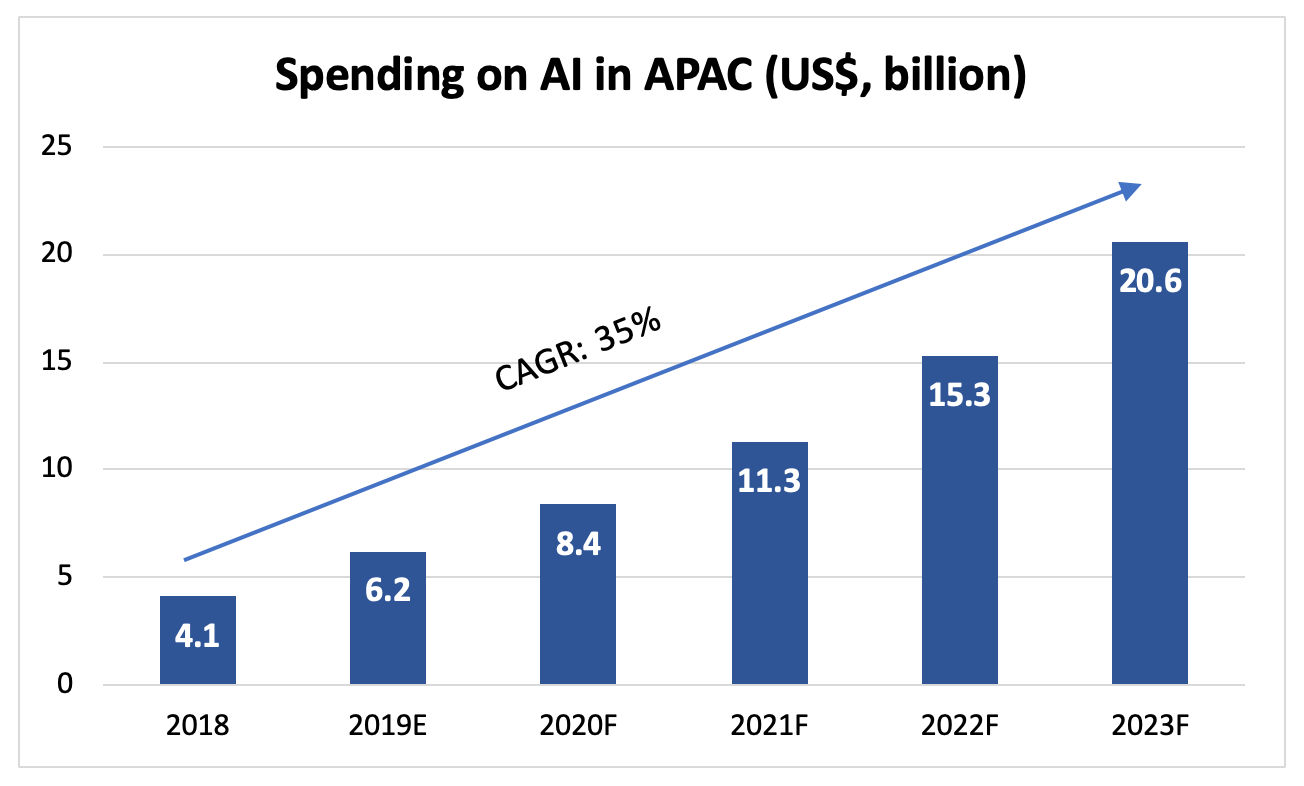

Investments in the region have kept up pace with general interest. It is estimated that spending on AI in Asia Pacific will reach $8.4 billion in 2020 and is on track to reach $20 billion by 2023 as shown in Figure 1 below.

China’s regional dominance

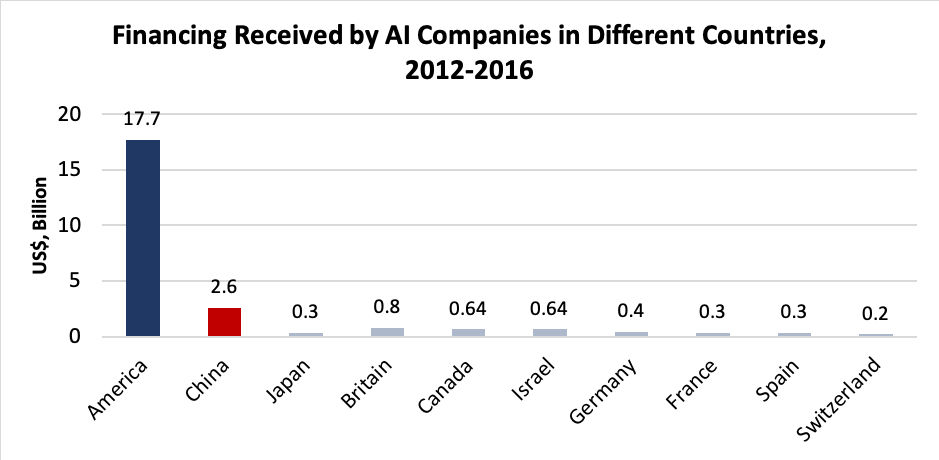

Historically, China has been the largest spender on AI systems in Asia Pacific, at around 70%. It has also been the largest receiver of financing in the region: in 2012-2016, China received US$2.6 billion. However, this was still far behind global leaders USA at US$17.9 billion.

Moving forward, we predict that China will continue to account for more than half of all spending in the region, backed by Beijing’s push to be the global leader in AI by 2030. Its national AI policy plan, unveiled in 2017, outlines an ambitious goal of developing a domestic AI industry worth $150 billion.

Despite a slow start, financing in China has accelerated: in the first half of 2018, Chinese companies raised $31.7 billion – a massive 73% of the global total of $43.5 billion.

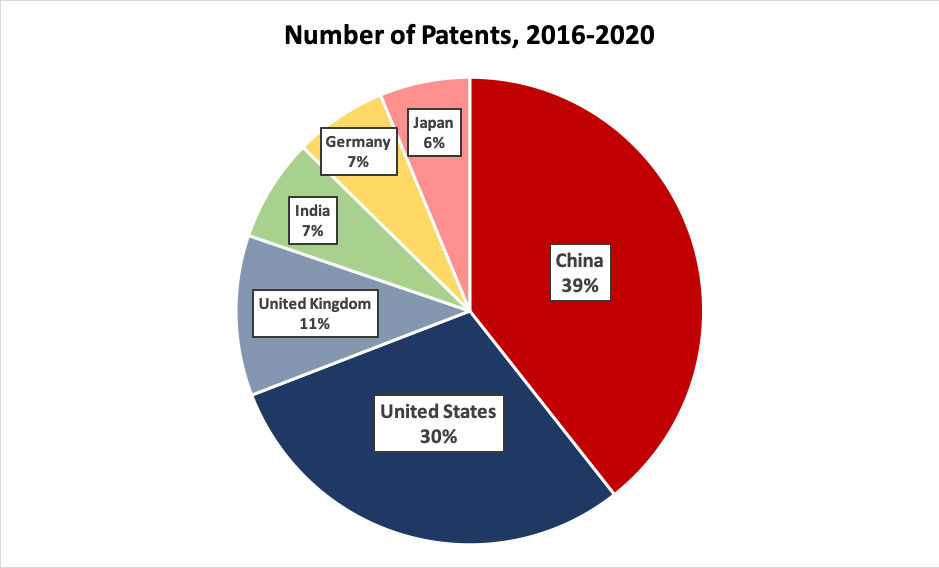

Additionally, China produces the largest volume of AI research globally. From 2016-2020, it filed the most patents related to artificial intelligence.

Despite its volume of research, a substantial portion of China’s AI talent pipeline will be educated in the USA. Currently, Chinese national comprise 40% of all international students majoring in mathematics and computer science, second only to India’s 41%. We expect to see an increasing proportion of homegrown AI talent in China, as more than 70 universities in China have introduced AI-related courses.

The above factors, coupled with China’s world-leading capabilities in computer vision, speech recognition and natural language processing, we believe that China is well-positioned to be Asia’s AI hub for the foreseeable future.

How should business in Asia Pacific leverage the situation and position themselves?

Acquiring a database will be a significant barrier to entry for foreign AI firms, as AI models require enormous volumes of data for “training”.

Local firms could leverage this by providing a unique value proposition to foreign AI companies, significantly reducing the time needed to acquire sufficient data.

Moreover, it is likely that having local partners to drive lead generation and sales is more advantageous than going at it alone. For example, companies across the cloud computing industry typically derive 80-90% of their revenue from partners.

In the long run, strategic partnerships would also be beneficial in providing some form of technology transfer through training programs.

It may be premature to declare China as a winner in the race to be the world’s first AI superpower. However, it is clear that there are opportunities for firms in other countries to leverage their respective positions to arrive at a win-win outcome for all stakeholders.