Key highlights

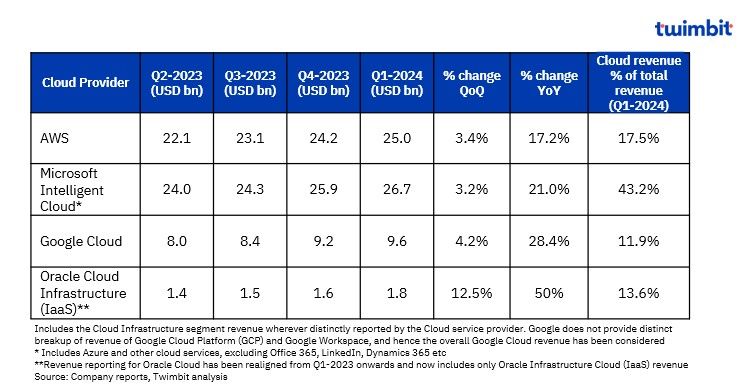

- The global cloud market witnessed a stellar Q1-2024. AWS, Microsoft, Google, and Oracle generated a combined USD 63.1 billion in revenue. This robust 21.2% YoY increase marks the highest YoY revenue growth rate in the past 5 quarters.

- Cloud revenue now constitutes a significant portion of these companies’ overall revenues, averaging around 21% in Q1-2024 which is slightly higher as compared to 19.9% in Q1-2023.

- AI (Artificial Intelligence) emerged as a key driver of cloud spending in Q1-2024, propelling earnings growth for leading providers. This trend is evident over the past 3 quarters, fueled by increased AI adoption.

- Microsoft Intelligent Cloud (MIC), Google Cloud and Oracle Cloud reported impressive YoY growth due to advancements in AI.

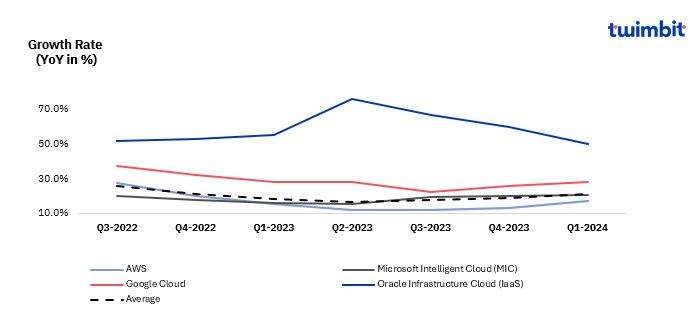

- AWS achieved a solid 17.2% YoY growth, reaching USD 25 billion, driven by infrastructure modernisation contracts and surging demand for its AI offerings.

- Microsoft’s cloud segment (MIC) reached USD 26.7 billion in Q1-2024, reflecting a strong 21% YoY increase primarily fueled by AI advancements within the cloud.

- Google Cloud delivered its highest revenue and profitability ever in Q1-2024, with USD 9.6 billion in revenue (28.4% YoY growth) and USD 900 million in operating income. Growth was driven by Google Cloud Platform (GCP) and Google Workspace, with a focus on infrastructure and platform services.

- Oracle Cloud Infrastructure (OCI) experienced exceptional YoY growth of approximately 50%, reaching USD 1.8 billion in revenue for Q1-2024. This surge is attributed to large contracts securing cloud infrastructure capacity for its Gen2 AI infrastructure.

- Tech giants like Google, AWS, and Microsoft compete for dominance in AI workloads, marking a fiercely competitive cloud computing market. Major players like Google, AWS and Microsoft eliminated egress fees which would enable them to attract customers and is likely to benefit organisations using hybrid/multi-cloud architectures. However, the long-term implications of this move remain unclear.

- Cloud strategic partnerships in Q1-2024 centred around AI, highlighting the rapid growth of Generative AI, which is expected to drive demand for global data centre capacity.

- Major players strategically expand their data centre footprints and launch new global cloud regions, focusing on Middle East & Africa and Latin American geographies.

Exhibit 1: Revenue growth rate (YoY) of Cloud service providers, Q1-2024

Exhibit 2: Revenue trends and growth of Cloud service providers, Q1-2024

Cloud Infrastructure providers

A. Amazon Web Services (AWS)

Overview

- In Q1-2024, AWS generated revenues of USD 25 billion (17.5% of Amazon’s total revenue) to achieve a 17.2% YoY (year-over-year) increase. This growth is attributed to:

- Infrastructure modernisation contracts secured from risk-averse customers seeking to optimise their IT infrastructure.

- Surge in demand for AWS AI offerings, indicating a growing embrace of AI solutions by enterprises.

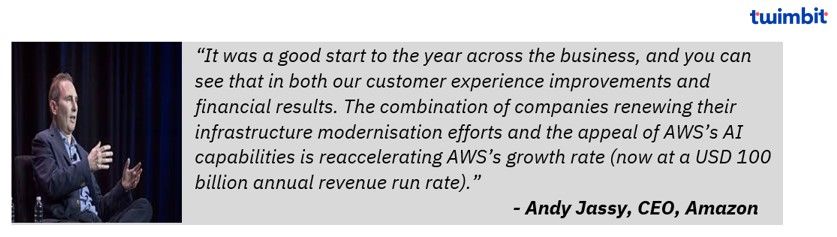

- AWS is pivotal in Amazon’s strategy to stay ahead in the highly competitive big-tech AI race. While the unit experienced a temporary revenue slowdown in 2023, effectively utilising its AI portfolio has reversed this trend, attracting new clients to its cloud platform.

- Amazon projects an annual revenue run rate of USD 100 billion for AWS, supported by the ongoing migration to the public cloud, which is still in its early stages of widespread adoption.

- AWS’s strong positioning in Generative AI is likely to translate into significant benefits as this technology gains wider traction.

- The robust demand for AI solutions prompts Amazon to plan strategically and increase capital investments in data centre capacity throughout 2024. This expansion will ensure sufficient resources to meet the growing needs of its cloud customers.

AWS global footprint

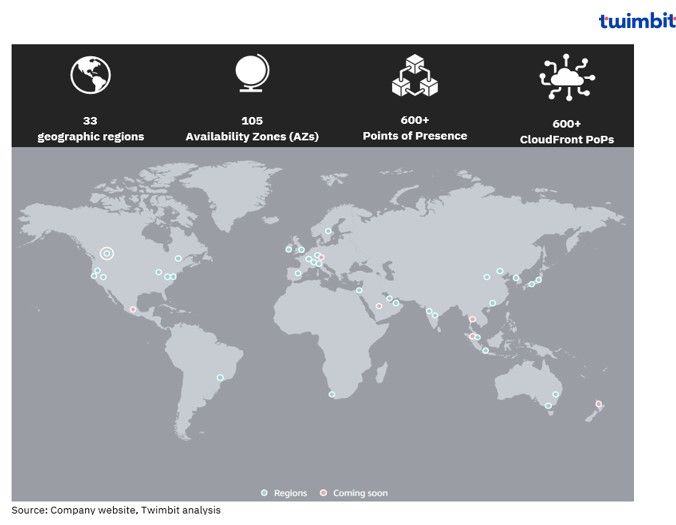

- AWS Cloud has 105 Availability Zones across 33 geographic regions globally.

- Announced plans for 18 more Availability Zones and 6 more AWS Regions in Malaysia, Mexico, New Zealand, the Kingdom of Saudi Arabia, Thailand, and the AWS European Sovereign Cloud.

- AWS Local Zones are available in 16 US metropolitan areas and 17 outside the US, with a new Local Zone in Miami, Florida.

Exhibit 3: AWS Cloud global capabilities

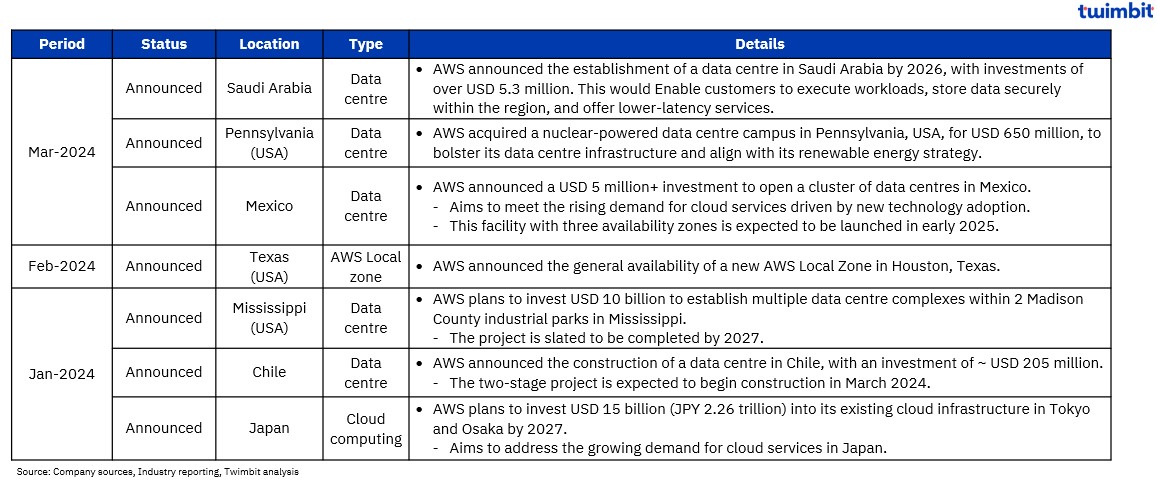

Exhibit 4: AWS Cloud – Key launches and announcements

- AWS aims to expand its cloud presence globally with significant capability enhancements in the Middle East, Americas and APAC regions

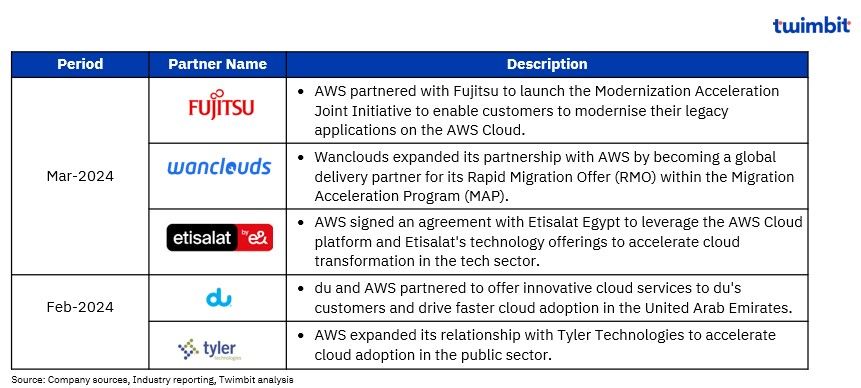

Key partnerships

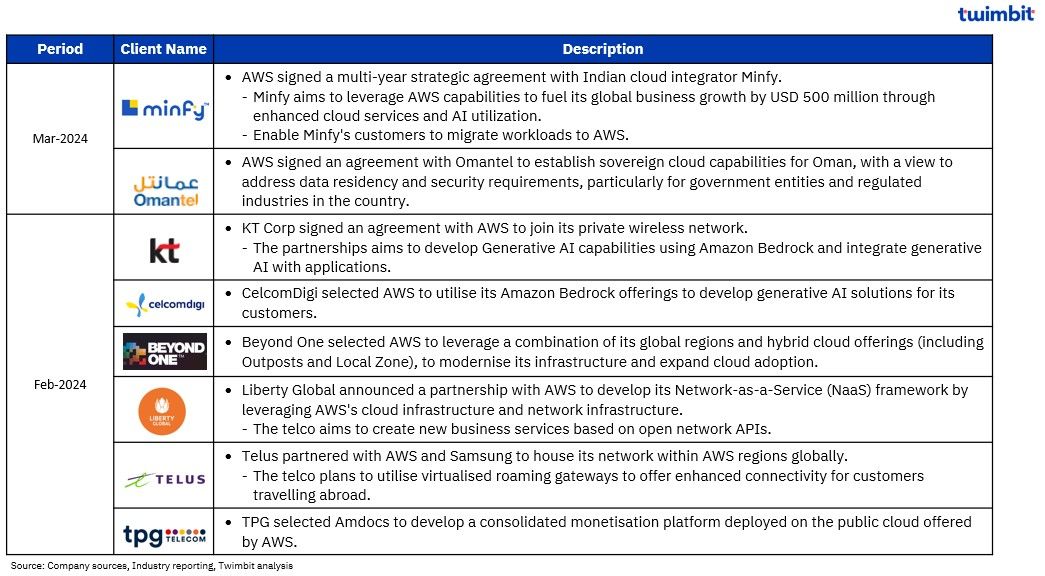

Key contract wins

B. Microsoft Intelligent Cloud (MIC)

Overview

- Microsoft achieved a 17% YoY revenue increase in Q1-2024, reaching USD 61.9 billion. This growth was driven by AI (Artificial Intelligence) advancements, particularly within the cloud segment.

- The MIC segment of Microsoft’s revenue contributed 43.2% in Q1-2024. This marks the highest MIC contribution since 2021, with a 140 basis points YoY growth compared to 41.8% in Q1-2023.

- Microsoft’s cloud segment, MIC, reached record revenue of USD 26.7 billion in Q1-2024, reflecting 21% YoY growth. MIC revenue surpassed the 16.3% growth achieved in Q1-2023, highlighting accelerated momentum.

- The surge in revenue is attributed to the strong demand for Microsoft’s consumption-based offerings, including server products, Azure, and a comprehensive suite of other cloud services.

- Server products and cloud service revenue increased 24% YoY to reach USD 24.8 billion in Q1-2024, driven primarily by the continued expansion of Azure and other cloud services, which witnessed a 31% growth.

- Server product revenue also displayed a healthy 6% YoY increase, fueled by the growing demand for Microsoft’s hybrid solutions in multi-cloud environments.

- Microsoft’s management projects a stable outlook for Q2-2024, with MIC revenue estimated between USD 28.4 billion – USD 28.7 billion. Azure and other cloud services revenue are anticipated to maintain impressive growth, with a projected increase of 30% – 31% in constant currency.

- Microsoft’s strategic decision to integrate AI technology from OpenAI across its products demonstrates a significant impact. Over 65% of Fortune 500 companies now leverage Microsoft’s Azure OpenAI Service.

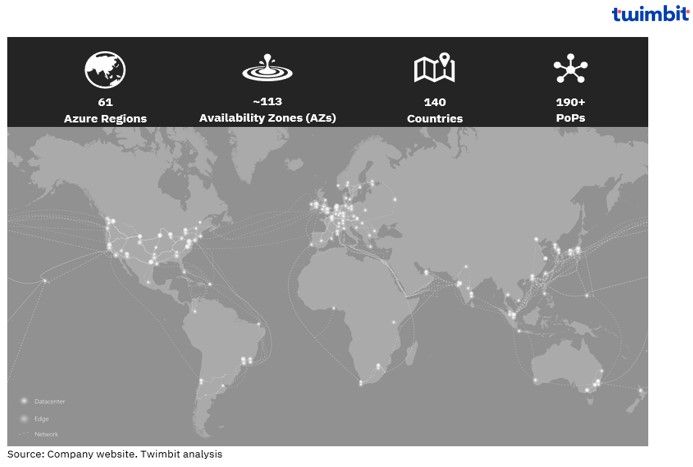

Microsoft Cloud global footprint

- MIC has a presence across 61 regions, and its Azure infrastructure comprises 300+ physical data centres.

Exhibit 6: Microsoft Cloud – Key launches and announcements

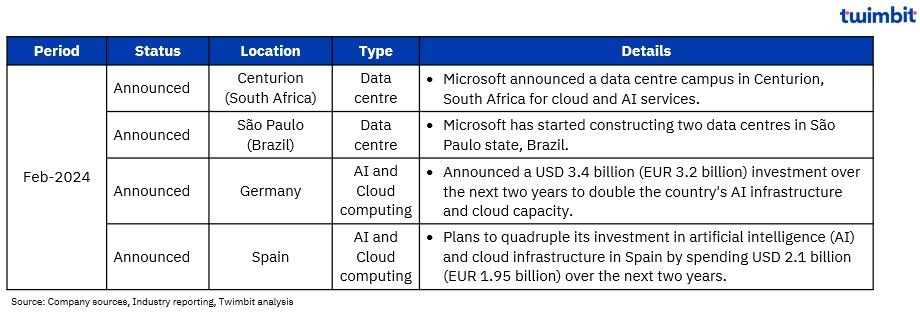

- In anticipation of surging demand for AI services, Microsoft is undertaking a strategic global expansion of its data centre network. This commitment is reflected in the significant capital expenditure of USD 14 billion allocated during the quarter.

- During Q1-2024, Microsoft announced plans to expand its cloud presence in the European, African and Latin American region by building new data centres and strengthening its cloud infrastructure capabilities.

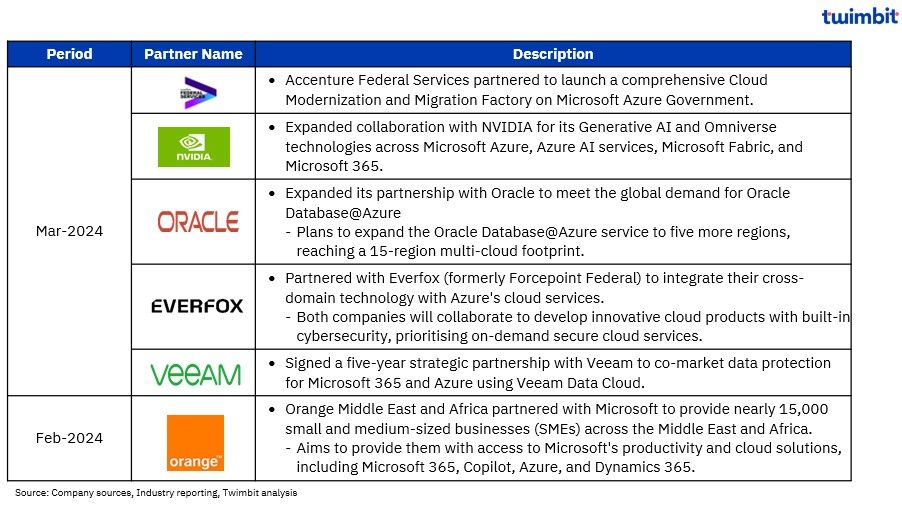

Key partnerships

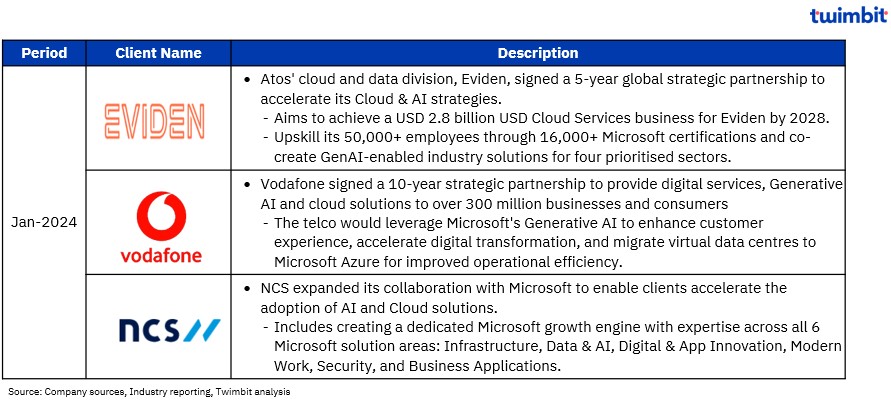

Key contract wins

- Microsoft’s strategic decision to weave OpenAI technology across its product portfolio is yielding significant results. This is exemplified by over 65% of Fortune 500 companies leveraging Microsoft’s Azure OpenAI Service.

- Customer adoption is surging, as evidenced by the more than 80% YoY increase in Azure deals exceeding USD 100 million and the doubling of deals exceeding USD 10 million.

Google Cloud

Overview

- Google Cloud segment revenue reached USD 9.6 billion in Q1-2024, growing by 28.4% YoY. This growth was driven by Google Cloud Platform (GCP) and Google Workspace, with infrastructure and platform services leading the way within GCP.

- Cloud revenue contribution to overall revenue reached 11.9% in Q1-2024, up from 10.7% in Q1-2023.

- Google Cloud reported its highest cloud revenue and profitability in Q1-2024, with an operating income of USD 900 million (as compared to USD 191 million in Q1-2023).

- Accounted for ~9.4% of the overall Google Cloud revenue in Q1-2024, as compared to 2.6% in Q1-2023.

- Google’s continued investment in AI and increased proliferation among enterprises continue to drive revenue growth.

- Nearly 60% of the funded GenAI startups and ~90% of GenAI unicorns are Google Cloud customers.

- YouTube and Google’s cloud business are projected to reach a combined annual run rate of over USD 100 billion by year-end 2024.

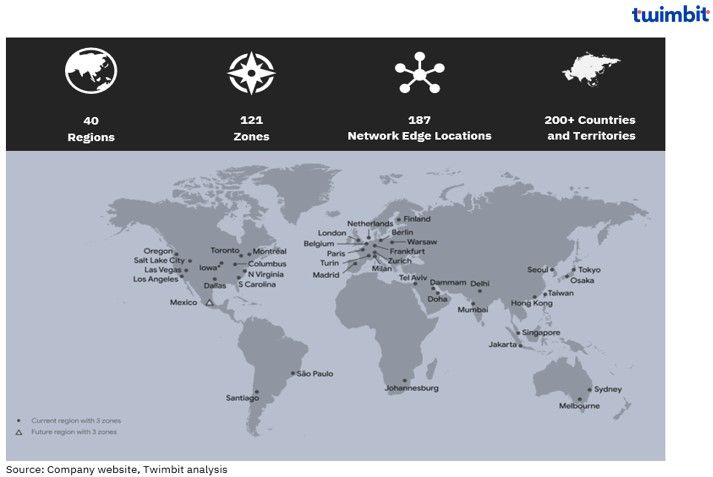

Google Cloud global footprint

- Google currently operates in 40 regions with 21 Zones across 200+ countries.

- Plans to operate in new regions, including Austria, Greece, Malaysia, Mexico, New Zealand, Norway, Sweden and Thailand.

Exhibit 7: Google Cloud global capabilities

Exhibit 8: Google Cloud – Key launches and announcements

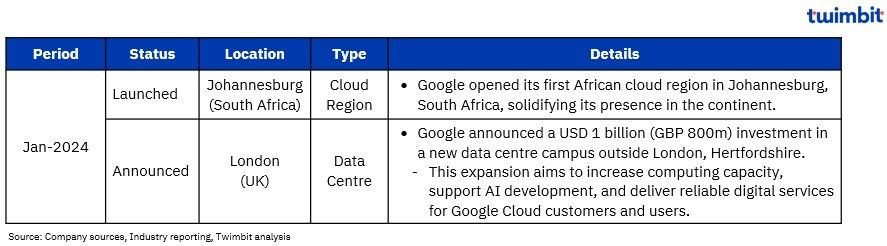

During Q1-2024, Google expanded its presence in Africa through a new cloud region launch in South Africa and announced the opening of a data centre in the UK.

Key product initiatives

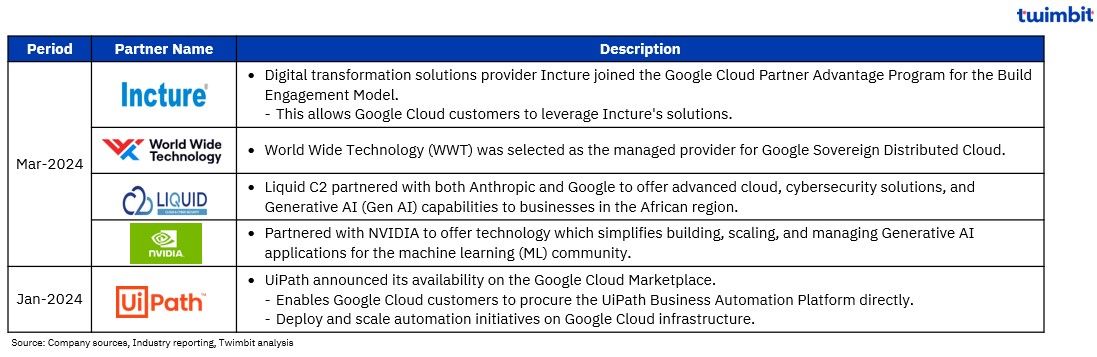

Key partnerships

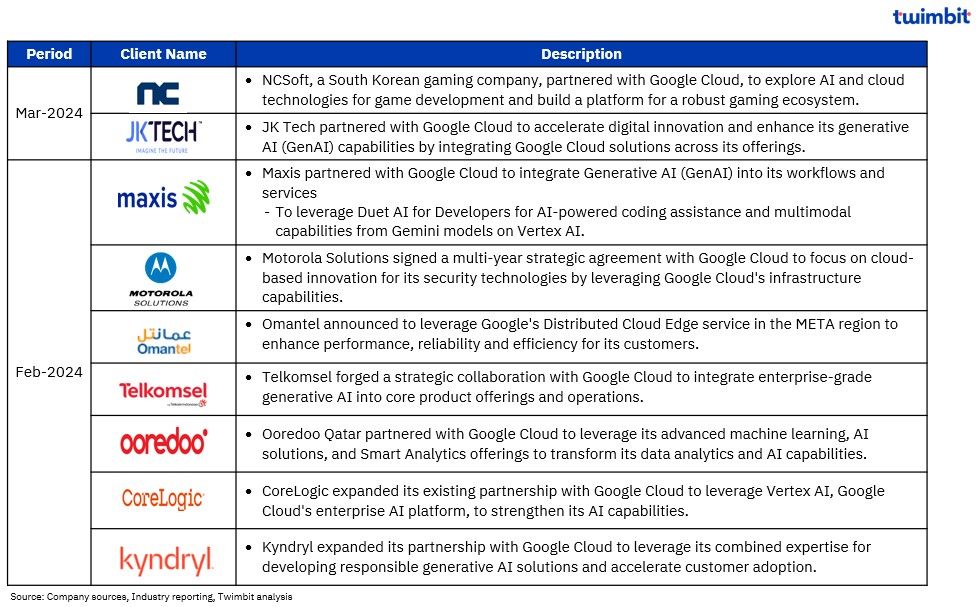

Key contract wins

Oracle Cloud

Overview

- Oracle Cloud Infrastructure (OCI – IaaS segment) delivered exceptional YoY growth, surging by approximately 50% to reach USD 1.8 billion in revenue for Q1-2024.

- This impressive trajectory has propelled OCI’s contribution to overall revenue to its highest point since 2021, reaching 13.6% in Q1-2024. This marks a significant increase from 9.7% in Q1-2023.

- The surge in large cloud infrastructure contracts in Q1-2024 significantly boosted Oracle’s total Remaining Performance Obligations (RPOs) by 29%, exceeding USD 80 billion.

- Despite data centre expansion, this robust demand for OCI’s Gen2 AI infrastructure underscores the technology’s leading-edge capabilities.

- Consequently, Oracle anticipates that 43% of its current USD 80 billion RPOs will be recognised as revenue within the next 4 quarters, further solidifying OCI’s sustained growth trajectory.

- Oracle has strategically positioned itself as a leader in Generative AI with the general availability of its OCI Generative AI offering. This advancement is expected to drive significant adoption and revenue contribution from AI services.

- Oracle plans a substantial investment increase of ~33% to solidify its global presence, allocating nearly USD 10 billion towards data centre construction and expansion initiatives between June 2024 and May 2025.

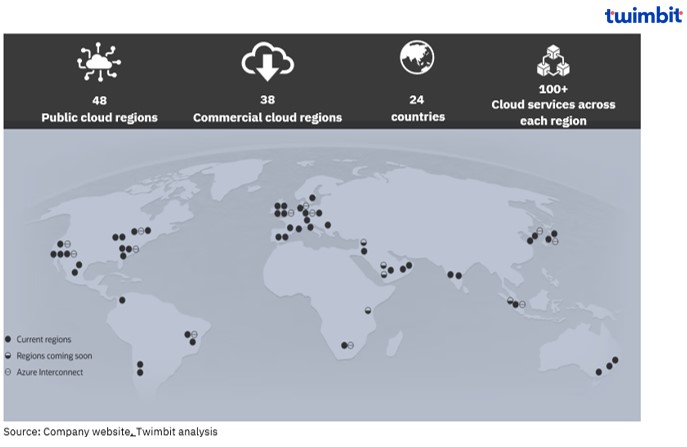

Oracle Cloud global footprint

- Oracle offers 100+ cloud services across 48 Public cloud regions across 24 countries.

- Offers dedicated EU Sovereign Cloud regions and distinct government clouds for the US, UK, and Australia to address regional data residency regulations.

- Isolated cloud regions cater to US national security requirements.

Exhibit 9: Oracle Cloud global capabilities

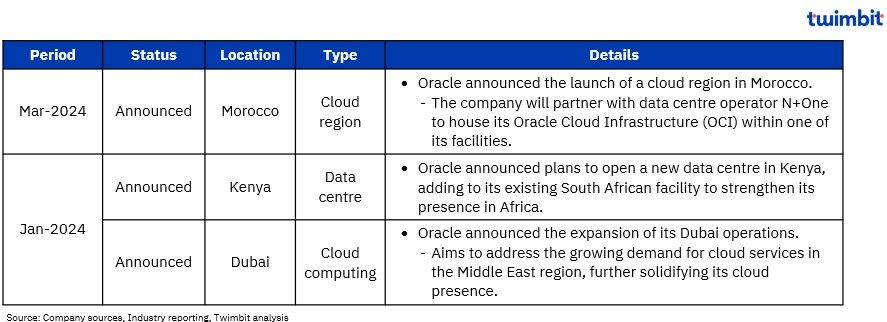

Exhibit 10: Oracle Cloud – Key launches and announcements

- Oracle continues to strengthen its foothold in the Middle East and Africa (MEA) region during Q1-2024 through strategic data centre deployments.

- To further amplify its global presence, it intends to significantly ramp up investments by ~33% to nearly USD 10 billion on data centre construction and expansion initiatives between June 2024 – May 2025.

- This represents a substantial increase from the estimated spending of USD 7 billion – USD 7.5 billion for the previous period (June 2023 – May 2024).

Key product initiatives

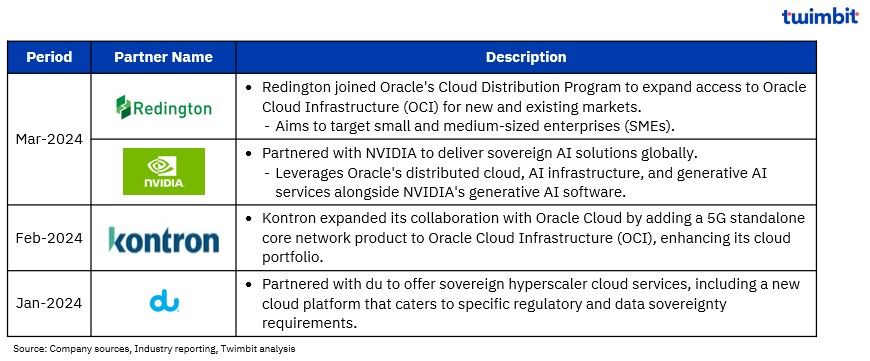

Key partnerships

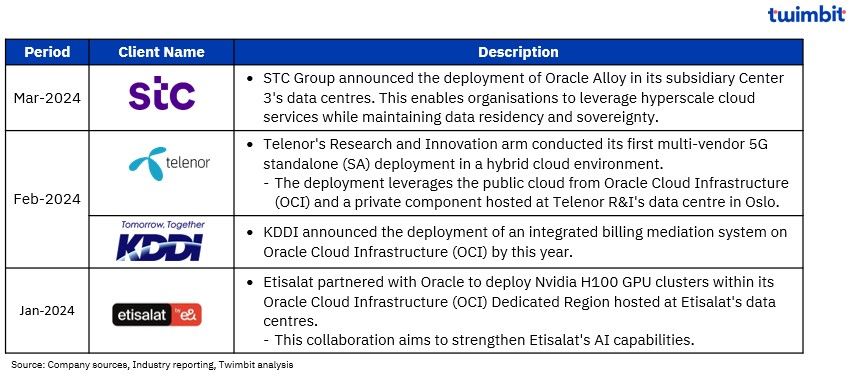

Key contract wins

Research methodology and assumptions

- The “Cloud Stories – Spring 2024” report provides brief financial insights of the leading 4 cloud infrastructure providers (AWS, Microsoft Intelligent Cloud, Google Cloud and Oracle Cloud). The report also provides information related to product initiatives, partnerships, and contract wins for the period January – March 2024.

- The report primarily leverages company websites and publicly disclosed information from major cloud service providers.

- The report analyses aggregate performance and future plans of leading providers and is used to project potential demand trends, wherever applicable.

- The report aligns Oracle’s fiscal year with the calendar year by considering Q3-FY2024 equivalent to Q1-CY2024.

- Oracle Cloud revenue reporting (IaaS + SaaS) has been realigned from Q1-2023 onward and now tracks only Oracle Infrastructure Cloud (IaaS) revenue.

- Previous quarter figures may differ slightly from prior reports due to the focus on Microsoft Intelligent Cloud (MIC), which encompasses Azure and related services.

- Specifically for Google, the revenue numbers are for Google Cloud, encompassing various services like Workspace, Google Cloud Platform, data & analytics platforms, infrastructure, and collaboration tools. It’s important to note that Google doesn’t report GCP revenue separately but as part of the broader Google Cloud segment.

Click here for more contents on telecoms

Recommended by Twimbit

APAC telcos performance benchmarks – Winter 2024