Key highlights:

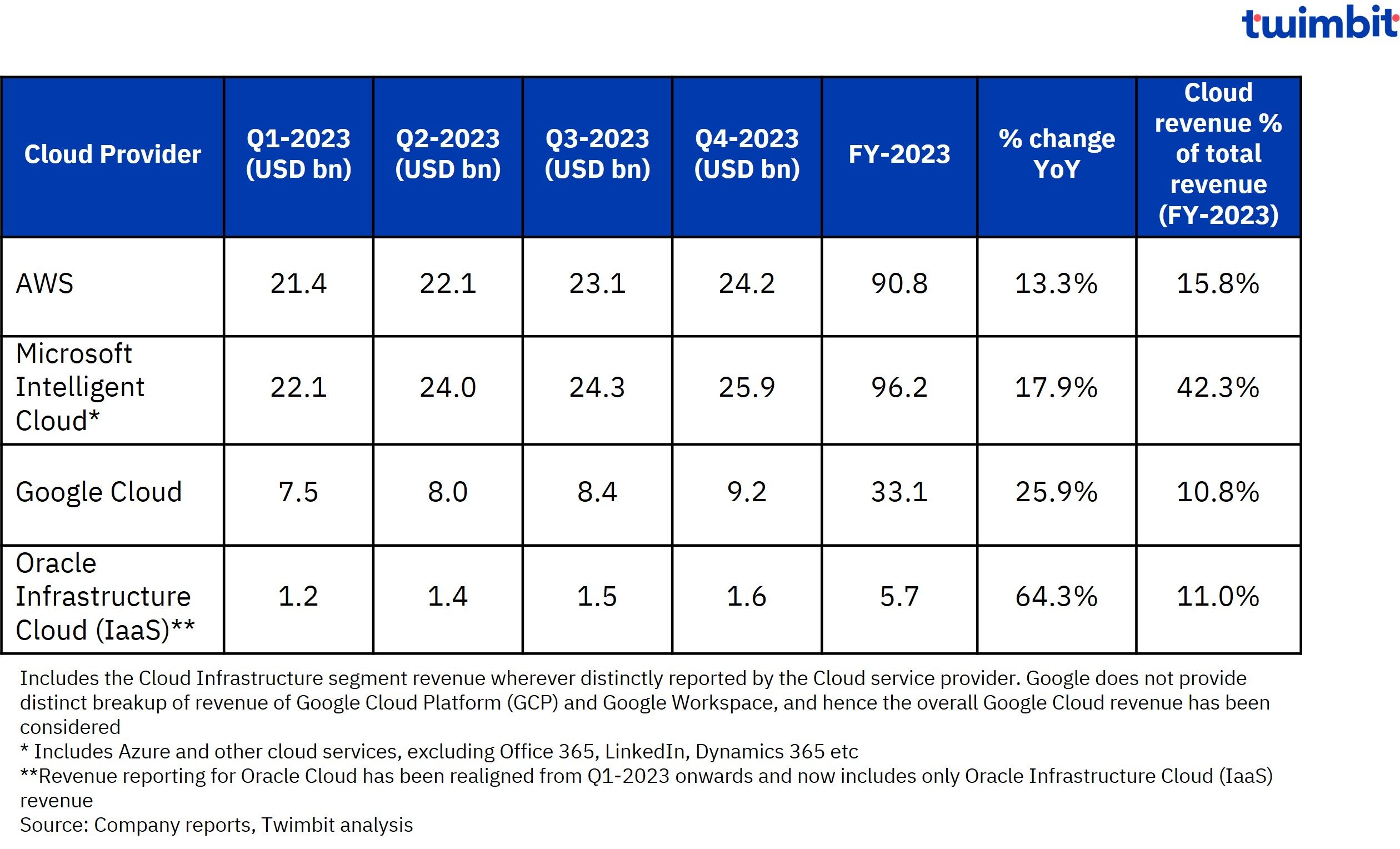

- The global cloud computing market witnessed robust growth in FY-2023, with the top four players – AWS, Microsoft, Google, and Oracle – generating a combined USD 220 billion in revenue. This represents a 17.1% YoY increase, surpassing the previous year’s growth and highlighting the industry’s momentum. Generative AI sits at the heart of this surge, driving interest from both providers and customers alike.

- Cloud revenue now constitutes an average of 18.9% of total revenue for these leading players, up from 18.1% in FY-2022, demonstrating its growing strategic significance within their broader business strategies.

- AI is poised to be a major growth driver as enterprises increasingly leverage its capabilities to optimize their existing cloud operations and unlock new value.

- 2023 saw a wave of investments and strategic actions by leading cloud vendors in AI, driven by surging demand for computational power to fuel technological advancements.

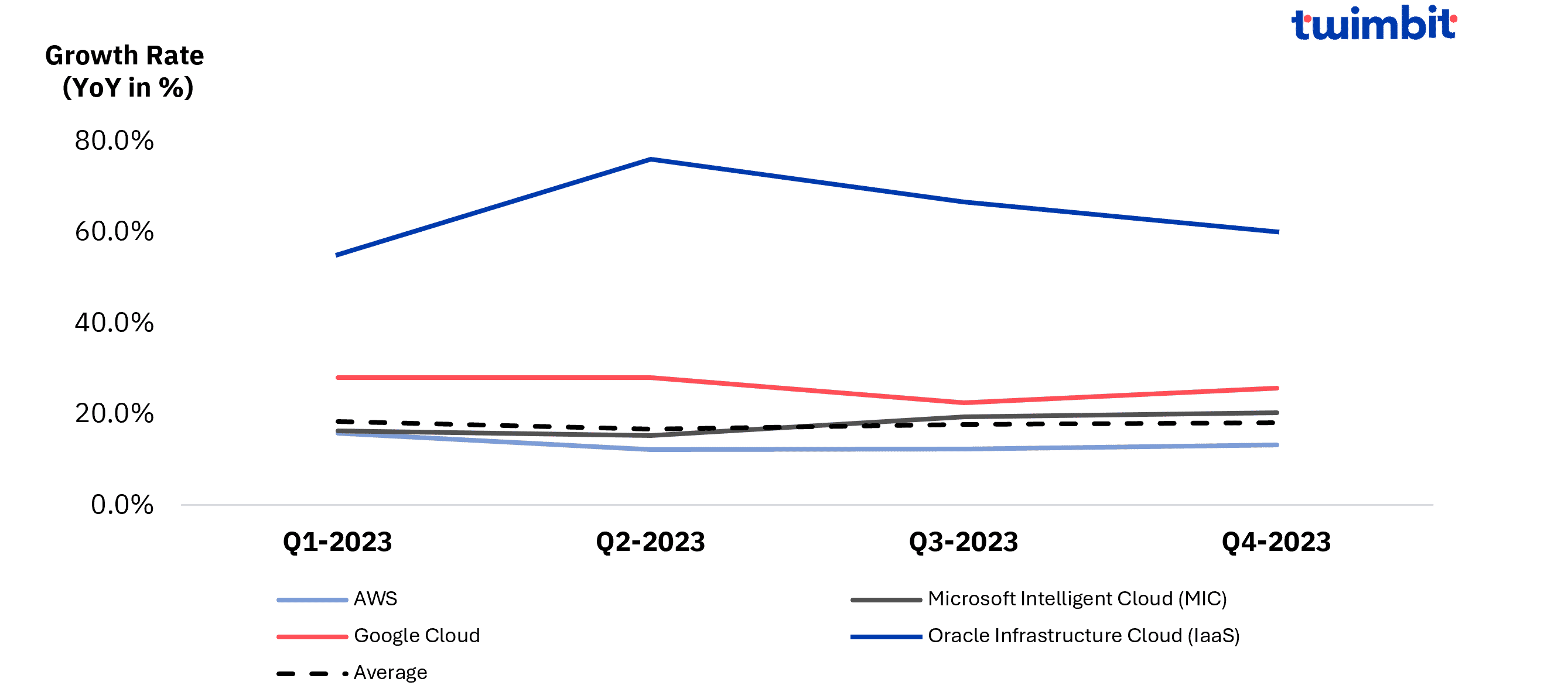

- AWS achieved a 13.3% YoY growth in cloud revenue in FY-2023, reaching USD 90.8 billion. This growth was primarily fueled by traction in AI-related cloud services, larger client commitments, and accelerated cloud migrations.

- Microsoft’s cloud segment, MIC, reached new heights in FY-2023, generating USD 96.2 billion in revenue, up by 17.9% YoY. This growth is fueled by strong demand for its server products and Azure cloud services.

- MIC continues to be core revenue driver, accounting for 42.3% of total revenue in FY-2023 and experiencing a 2.3 percentage point YoY rise.

- To further solidify its position, in Dec-2023, Microsoft launched Microsoft Cloud for Sovereignty, expanding its security and compliance capabilities across all Azure regions.

- Google Cloud achieved revenue of USD 33.1 billion in FY-2023, a 25.9% YoY increase. This growth translated to a 1.5 percentage point increase in its share of Google’s overall revenue, reaching 10.8%.

- Moreover, Google Cloud achieved a remarkable feat by turning consistently profitable throughout the year, recording an overall profit of USD 1.7 billion in FY-2023, a stark contrast to the previous year’s operating loss of USD 1.9 billion.

- Oracle Cloud Infrastructure (OCI) IaaS segment displayed robust growth, expanding by 64.3% YoY and generating USD 5.7 billion in revenue in FY-2023.

- It had the highest growth rate among its peers, indicating significant momentum in Oracle’s cloud business, driven by consistent growth across all quarters.

- Leading cloud providers are optimizing cost structures through cutting-edge next-generation servers and rack-scale architectures. This ensures sustainable long-term growth while catering to the ever-growing demand for cloud services.

- Moreover, hyperscalers are embracing vertical integration and investing in custom-designed chips (CPUs, smartNICs, accelerators) either independently or in collaboration with partners, to further enhance cost management and infrastructure optimization.

- Fueled by the rapid growth of generative AI, the demand for global data center capacity is bound to increase. Recognizing this opportunity, major players like AWS, Microsoft, Google, and Oracle are strategically expanding their data center footprints and launching new cloud regions across the globe.

- Latin America, the Middle East, and Asia-Pacific are rapidly evolving into critical growth markets, attracting significant investments from all major players. Examples include:

- Oracle: Focused expansion in Latin America (Mexico, Chile, Colombia).

- Microsoft: Targeted investments in Europe (Italy, Poland, Spain) and the Middle East (Israel).

- AWS: Prioritized Asia-Pacific countries (Australia, Singapore, Malaysia, India) with a USD 15.5 billion investment in Japan, building upon prior investments.

- Google: Entered the Japanese market with a significant investment in the Inzai data center (operational since March 2023)

- The recent USD 15.5 billion investment in Japan by AWS highlights their aggressive push to dominate the Asia-Pacific market. This move follows a long-standing commitment, with over USD 10 billion invested in the region since 2012. Additionally, Google’s entry into Japan with the Inzai data center showcases the intensified competition.

Exhibit 1: Revenue growth rate (YoY) of Cloud service providers in FY-2023

Exhibit 2: Revenue trends and growth of Cloud service providers in FY-2023

Cloud Infrastructure providers

A. Amazon Web Services (AWS)

Overview

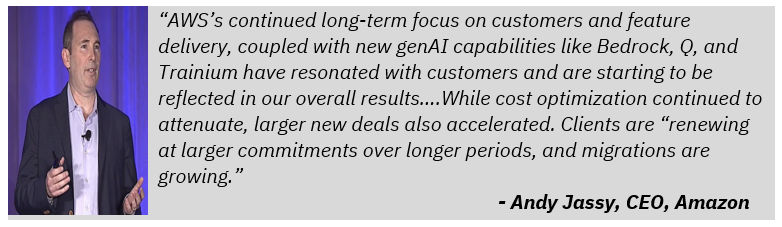

- In 2023, AWS continued to be a key driver of Amazon’s growth, generating USD 90.8 billion in revenue (15.8% of Amazon’s total revenue) and achieving a 13.3% YoY increase. The growth was fueled by a surge in AI-related cloud services, larger client commitments with longer contract periods, and an increase in cloud migrations.

- Operating income also grew 7.8% on YoY basis in FY-2023 to USD 24.6 billion, representing 66.8% of the group’s total.

- Generative AI remains a strategic focus for AWS, with CEO Andy Jassy emphasizing its potential to revolutionize customer experiences and business processes

- This commitment is evident in Q4-2023 releases like the Q chatbot for developers and the Trainium2 chip for AI model training. Additionally, partnerships like the Nov-2023 collaboration with NVIDIA on AI training chips further solidify this focus.

- Seeking to enhance efficiency, Amazon announced a year-long extension of server lifespan, potentially boosting Q1-2024 operating income by USD 900 million.

- Industry sources suggest an upcoming restructuring of AWS’s 60,000-strong cloud business sales team. This move is aimed at consolidating teams with conflicting sales strategies and improving efficiency.

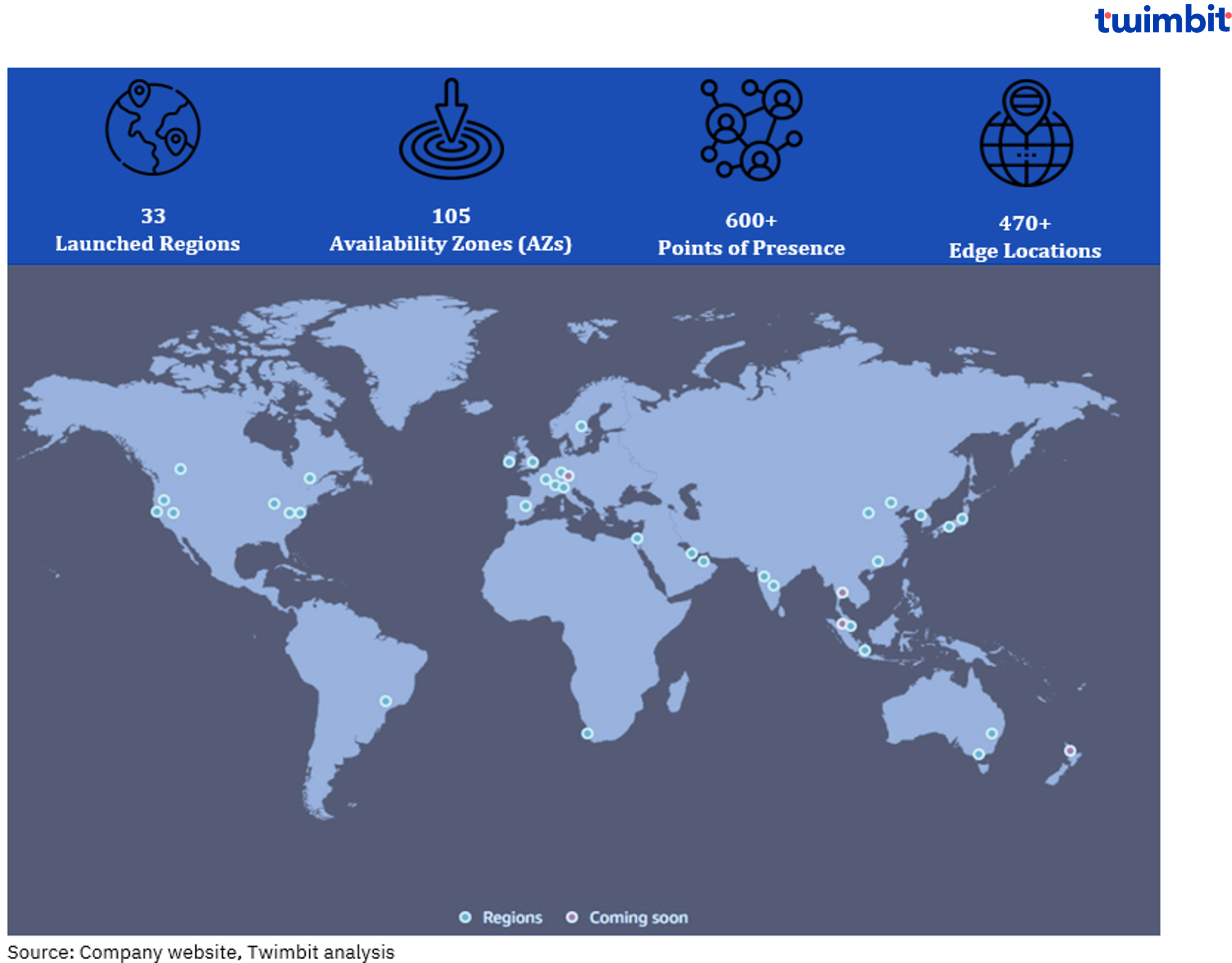

AWS global footprint

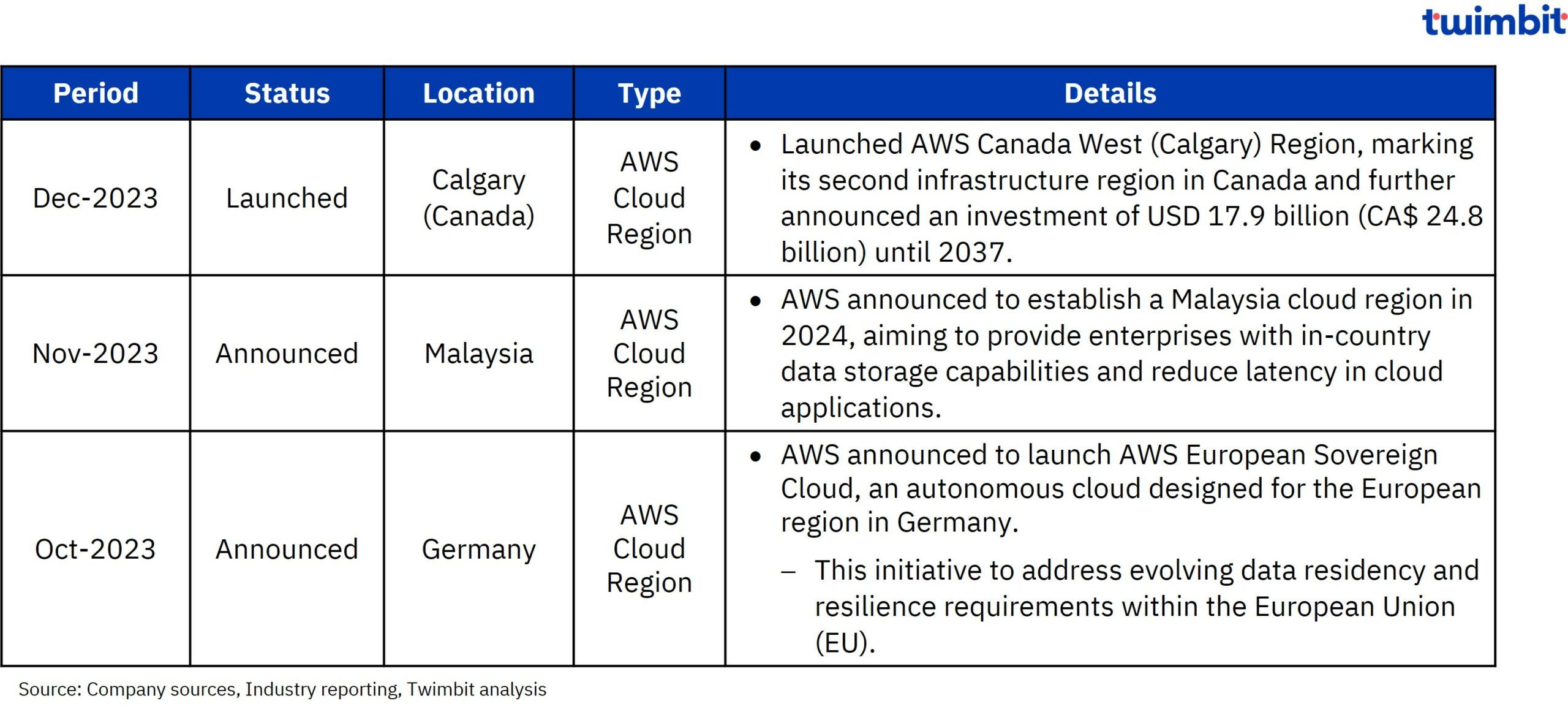

- AWS has 105 Availability Zones across 32 geographic regions worldwide. It also has plans for 12 more Availability Zones and 4 more AWS Regions in Germany, Malaysia, New Zealand, and Thailand.

- AWS Local Zones are available in 16 US metropolitan areas and 17 outside US. It also plans to expand Local Zones to 18 new locations in 16 countries, including Australia, Austria, Belgium, Brazil, Canada, Colombia, Czech Republic, Germany, Greece, India, Kenya, Netherlands, Norway, Portugal, South Africa, and Vietnam.

Exhibit 3: AWS Cloud global capabilities

Exhibit 4: AWS Cloud – Key launches and announcements

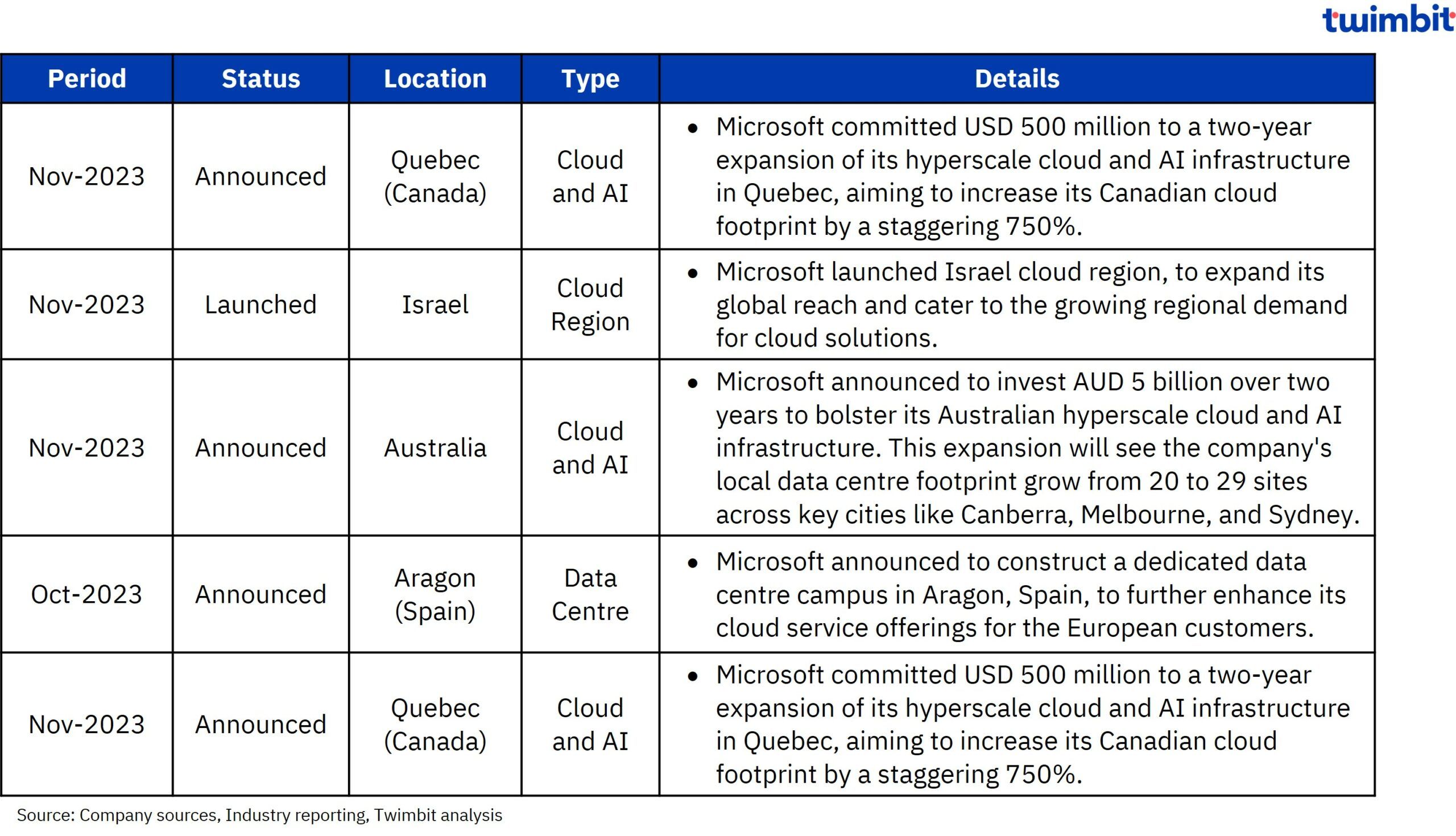

AWS continues to expand its presence globally with significant capability enhancements across Germany, Malaysia and Canada during Q4-2023.

Key product initiatives

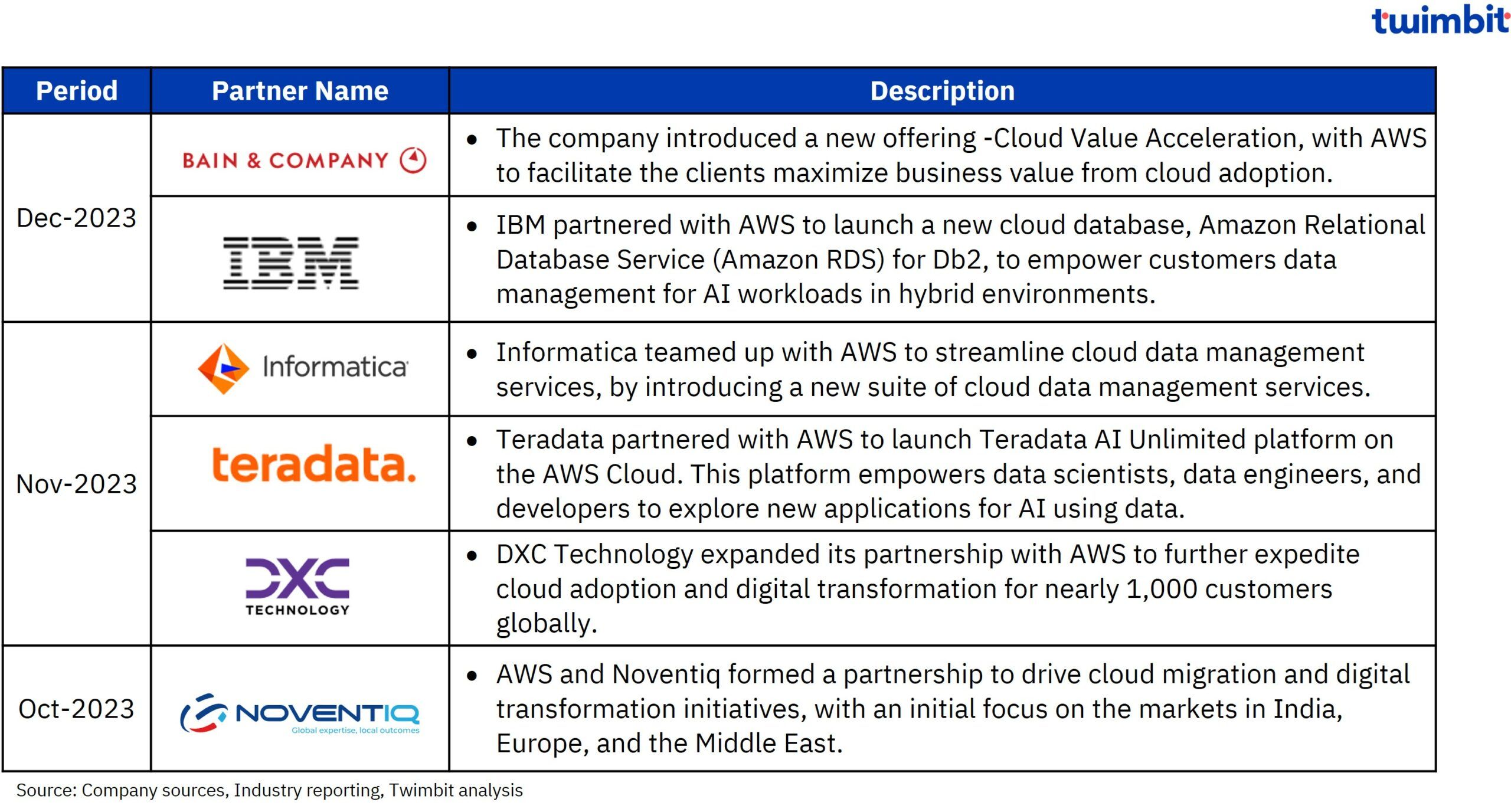

Key partnerships

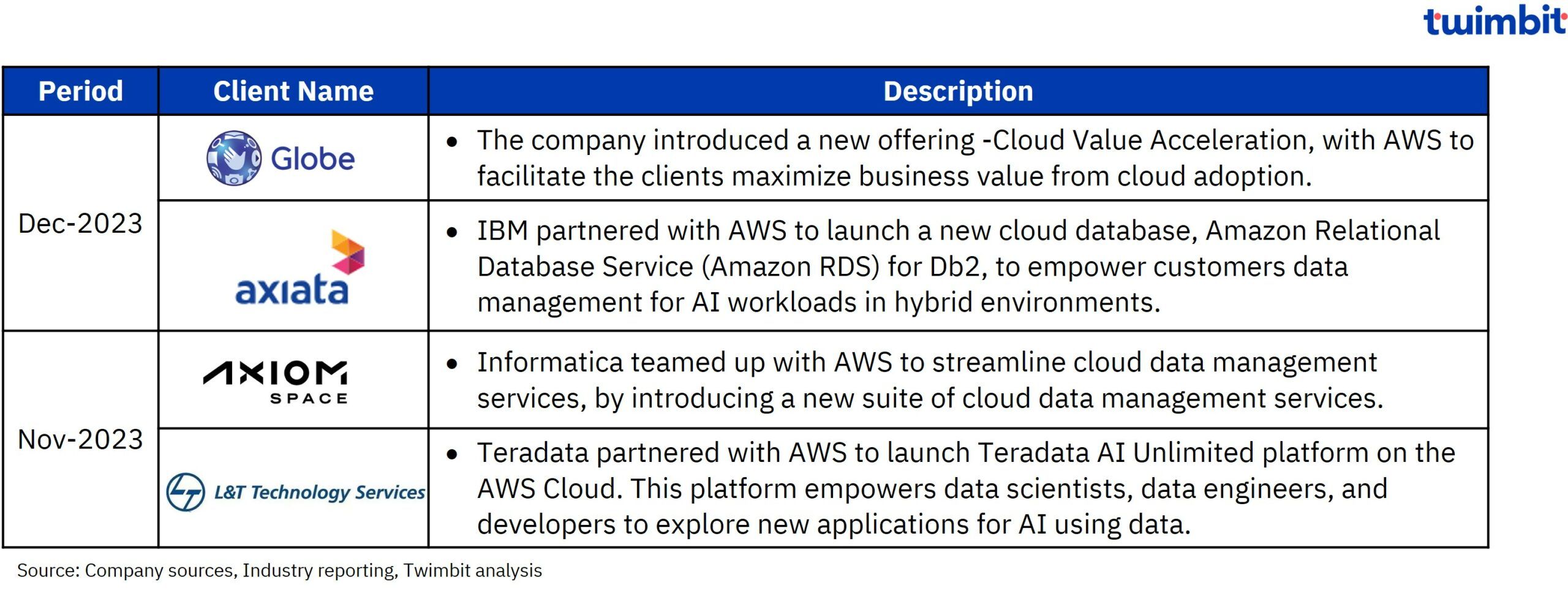

Key contract wins

B. Microsoft Intelligent Cloud (MIC)

Overview

- Microsoft’s cloud segment (MIC) achieved record revenue of USD 96.2 billion in FY-2023, growing 17.9% YoY. This growth was fueled by strong demand for its consumption-based offerings, including server products, Azure, and other cloud services.

- However, annual MIC revenue growth has been declining since 2020, reaching 17.9% in FY-2023 compared to 21.7% the previous year.

- Regardless of the slowdown, MIC remains the cornerstone of Microsoft’s revenue, accounting for a significant 42.3% share in FY-2023 and experiencing its own 2.3 percentage point YoY growth.

- Server product and cloud services revenue grew 19.4% YoY, driven by continued adoption of Azure and other cloud services.

- Server product revenue itself remains robust, fueled by demand for Windows Server and SQL Server in multi-cloud environments.

- Azure and other cloud services witnessed significant growth, fueled by consumption-based offerings and integrated AI services.

- The commercialization of its AI-powered coding assistant – Microsoft Copilot in Sep-2023, is expected to further drive Azure adoption in the coming years.

- Azure’s success reflects broader cloud optimization trends and the rising demand for AI services, which Microsoft strategically integrates across its solutions. This is evident by the growing number of Azure AI customers, reaching 53,000 by Dec-2023,with over a third added in the past year.

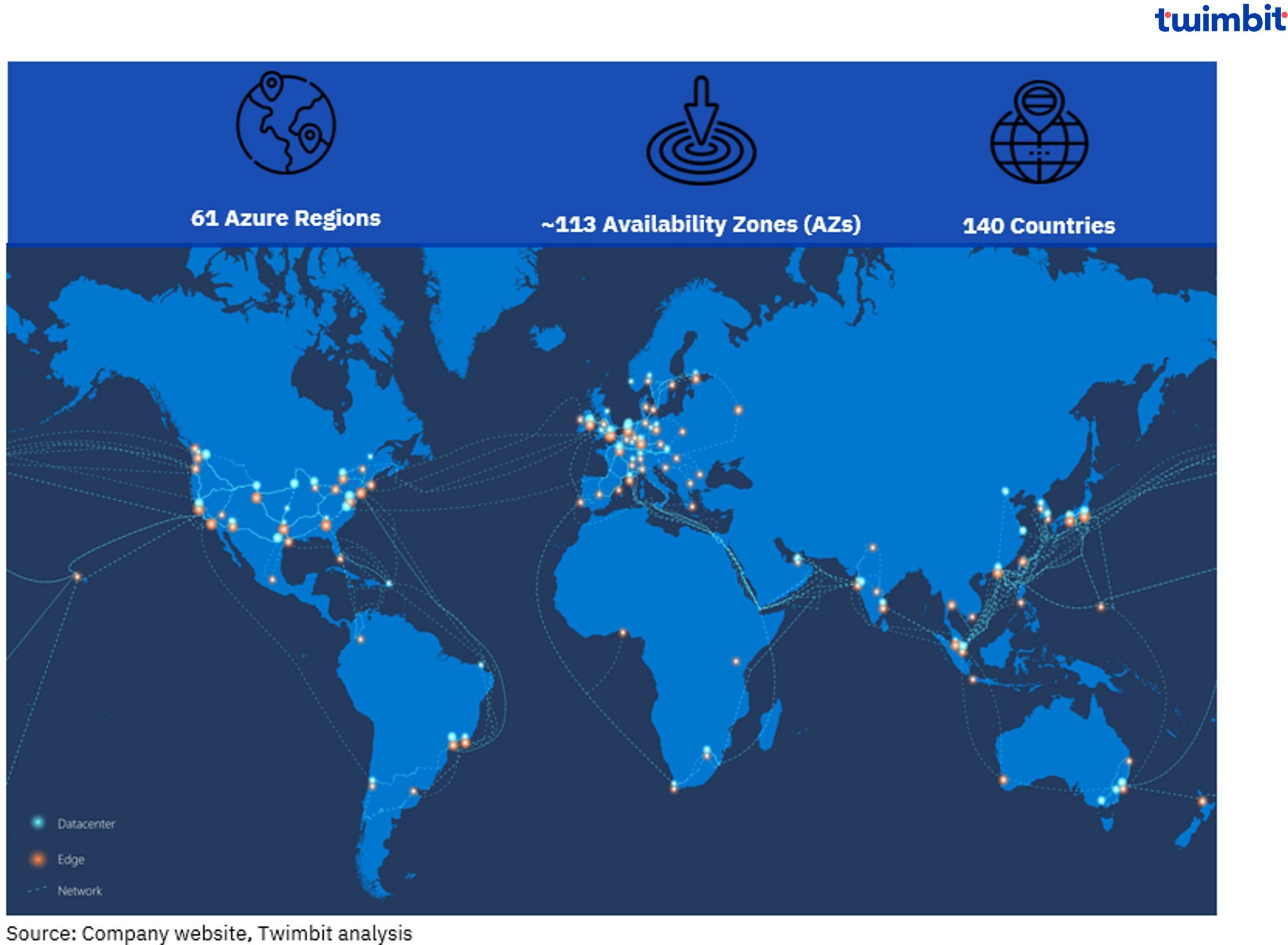

Microsoft Cloud global footprint

MIC has presence across 61 regions and its Azure infrastructure comprises of 300+ physical datacentres.

Exhibit 5: Microsoft Cloud global capabilities

Exhibit 6: Microsoft Cloud – Key launches and announcements

During Q4 of 2023, Microsoft announced plans to expand its presence in the European and Middle East regions, with plans to enhance its cloud capabilities further.

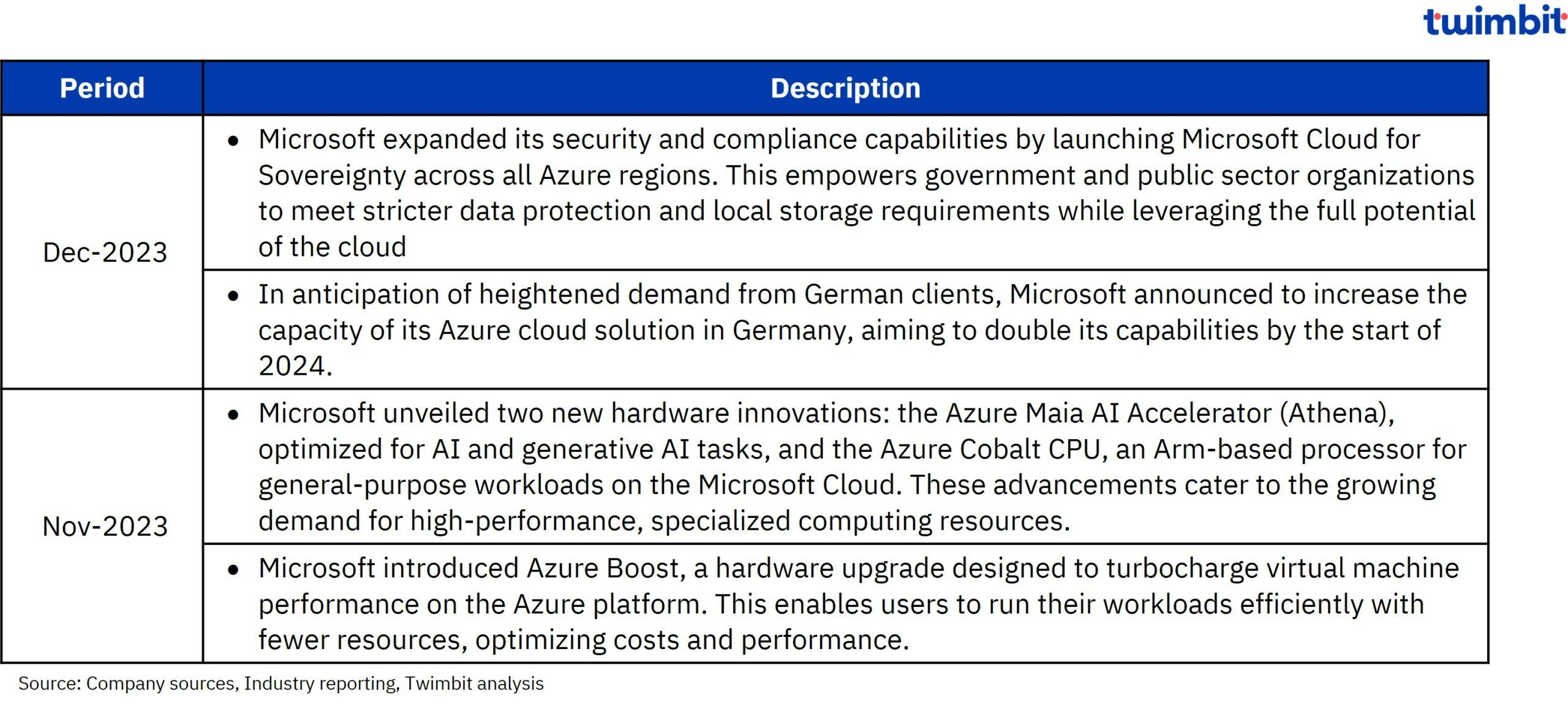

Key product initiatives

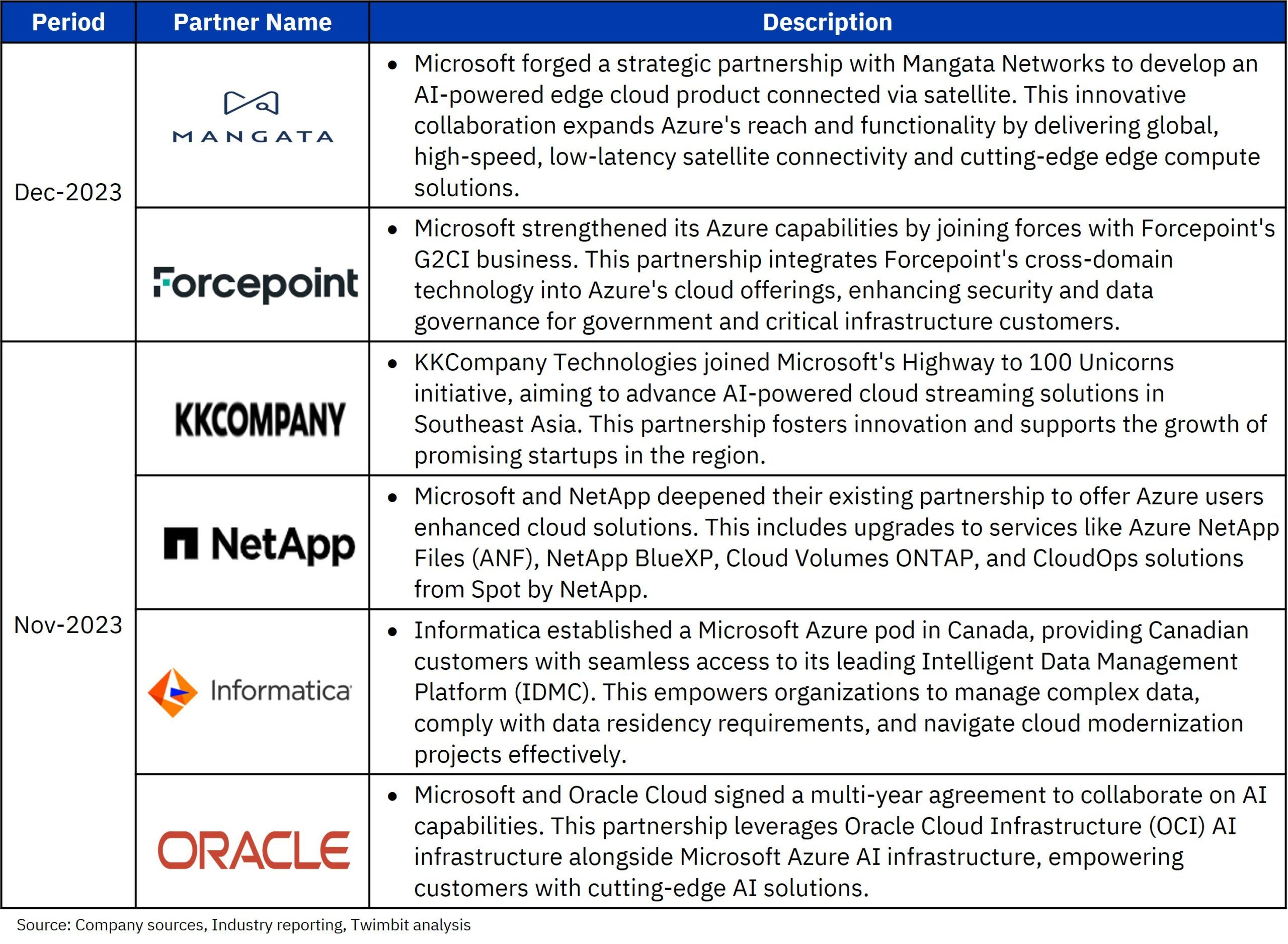

Key partnerships

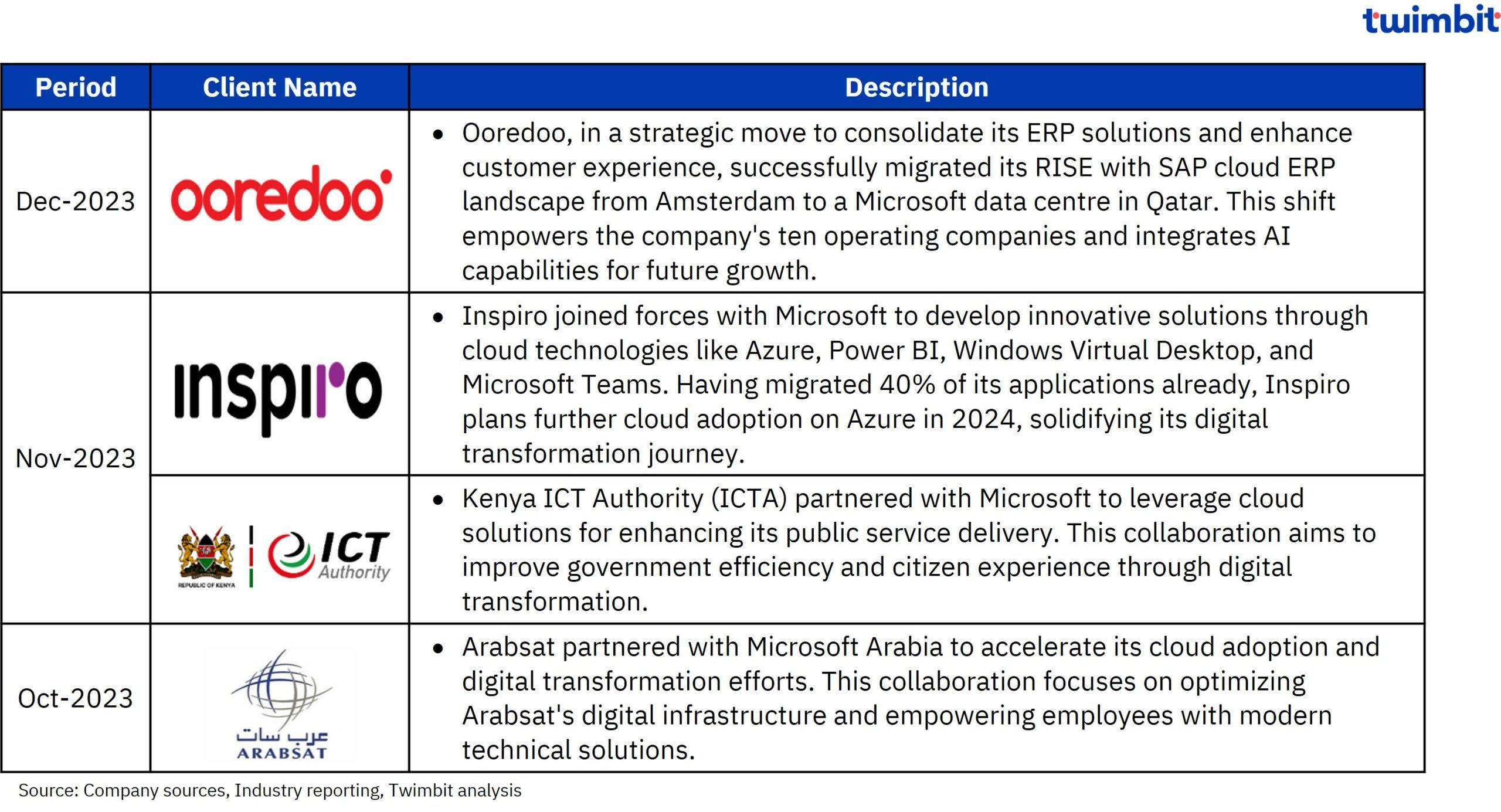

Key contract wins

C. Google Cloud

Overview

- Google Cloud segment revenue reached USD 33.1 billion in FY-2023, growing 25.9% YoY.

- This growth was primarily driven by Google Cloud Platform (GCP) and Google Workspace, with infrastructure and platform services leading the way within GCP.

- Q4-2023 revenue growth slowed to 25.7% YoY, compared to 32.0% in Q4-2022, driven by Gen-AI and product initiatives.

- Cloud revenue contribution to overall revenue increased to 10.8% in FY-2023, up from 9.3% in FY-2022.

- Google Cloud reported its highest cloud revenue and profitability in FY-2023, with an operating income of USD 1.7 billion (compared to a loss of USD 1.9 billion in FY-2022).

- However, the Google Cloud revenue growth rate (on YoY basis) has been slowing down over the past few quarters, and the YoY revenue growth rate was the lowest in the last two reported quarters of FY-2024.

- High revenue growth rate offset increase the in-compensation expenses largely driven by headcount growth was key factor driving operating income growth.

- Additionally, reduction in costs driven by the change in the estimated useful lives of its servers and certain network equipment also benefitted the operating income growth.

Google Cloud global footprint

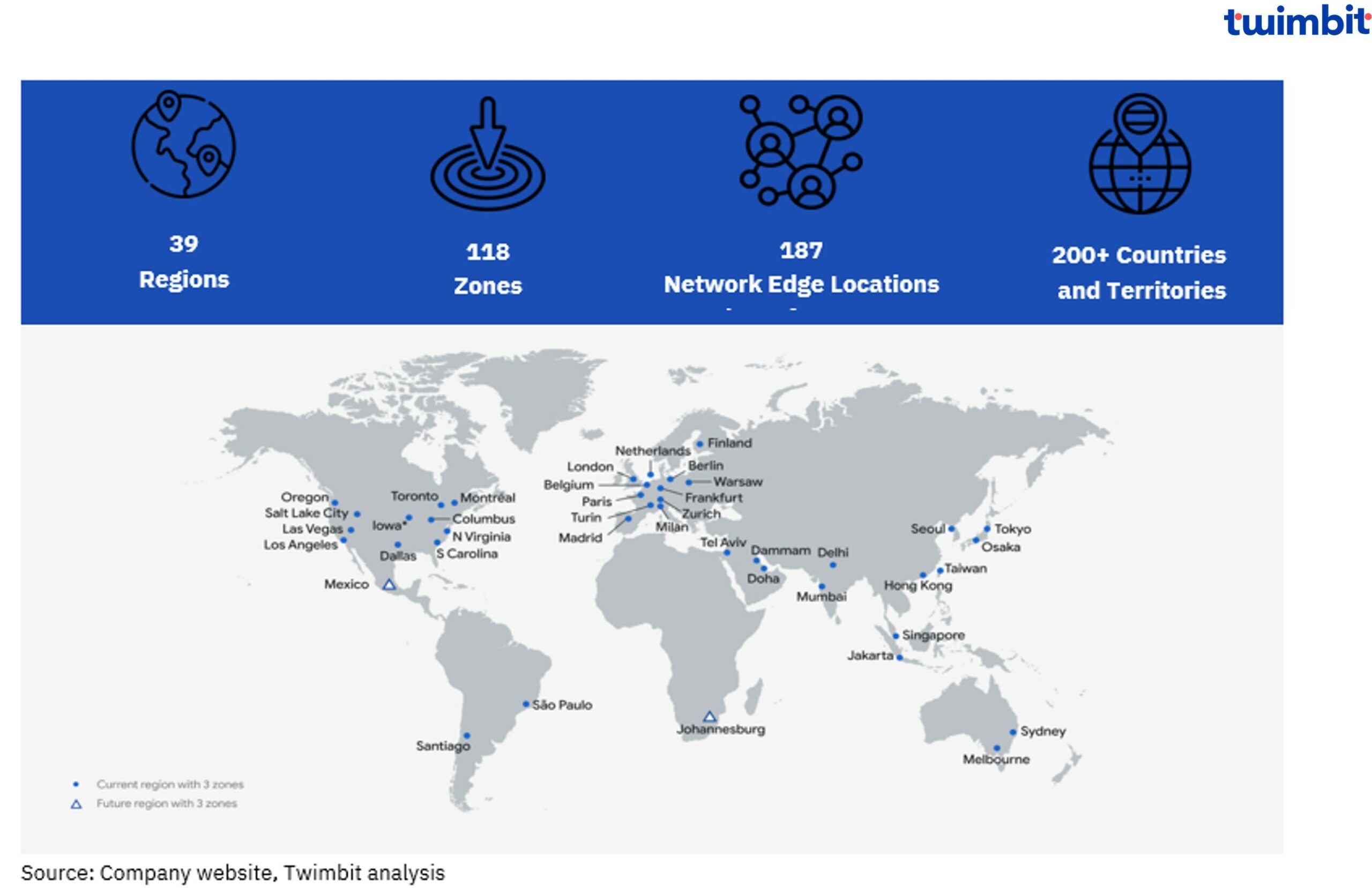

- It currently operates in 39 regions with 118 Zones across 200+ countries.

- Plans to operate in new regions including Mexico, Malaysia, Thailand, New Zealand, Greece, Norway, South Africa, Austria and Sweden.

Exhibit 7: Google Cloud global capabilities

Exhibit 8: Google Cloud – Key launches and announcements

During Q4-2023, Google expanded its presence in the Middle East region, by opening a new cloud region in Saudi Arabia.

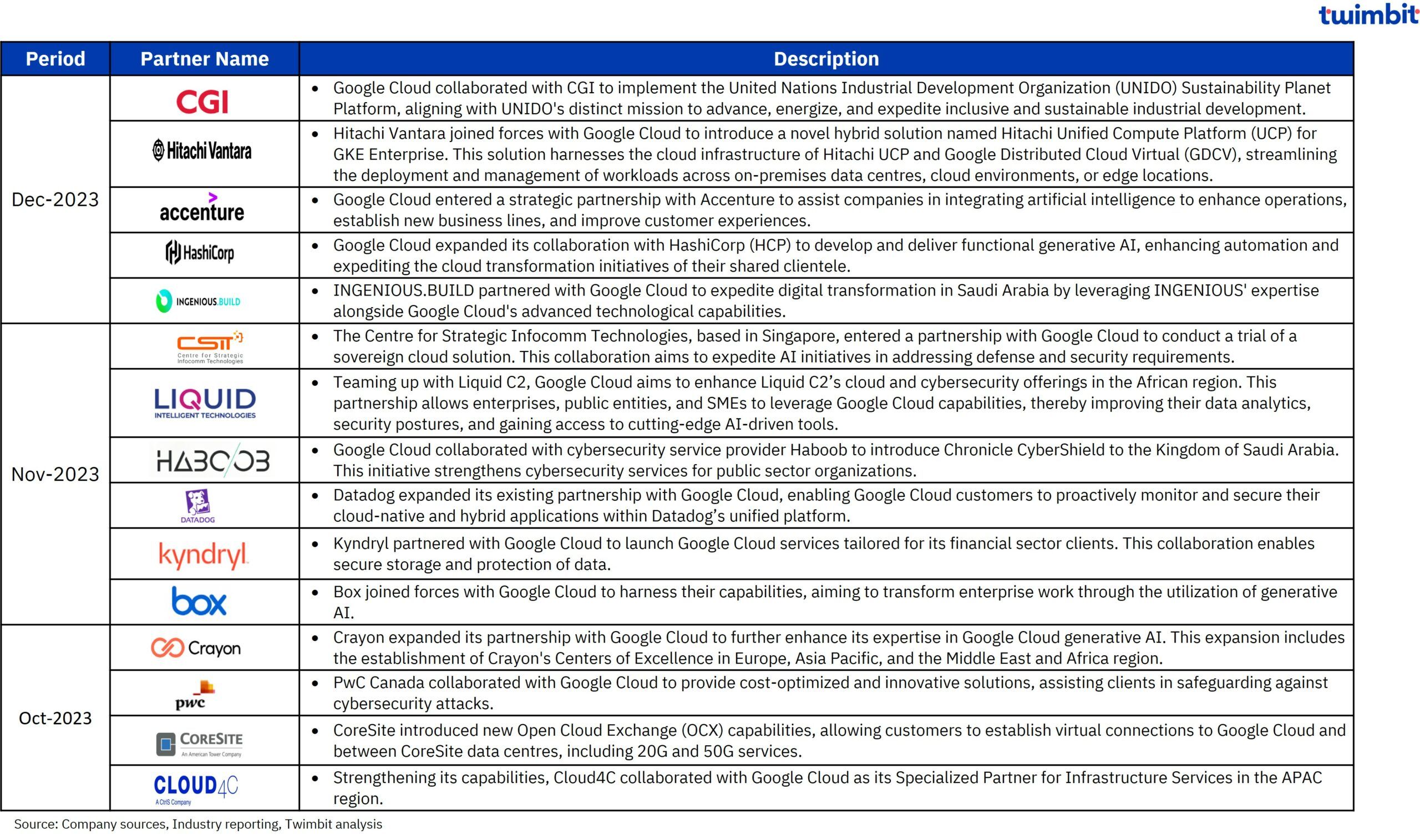

Key partnerships

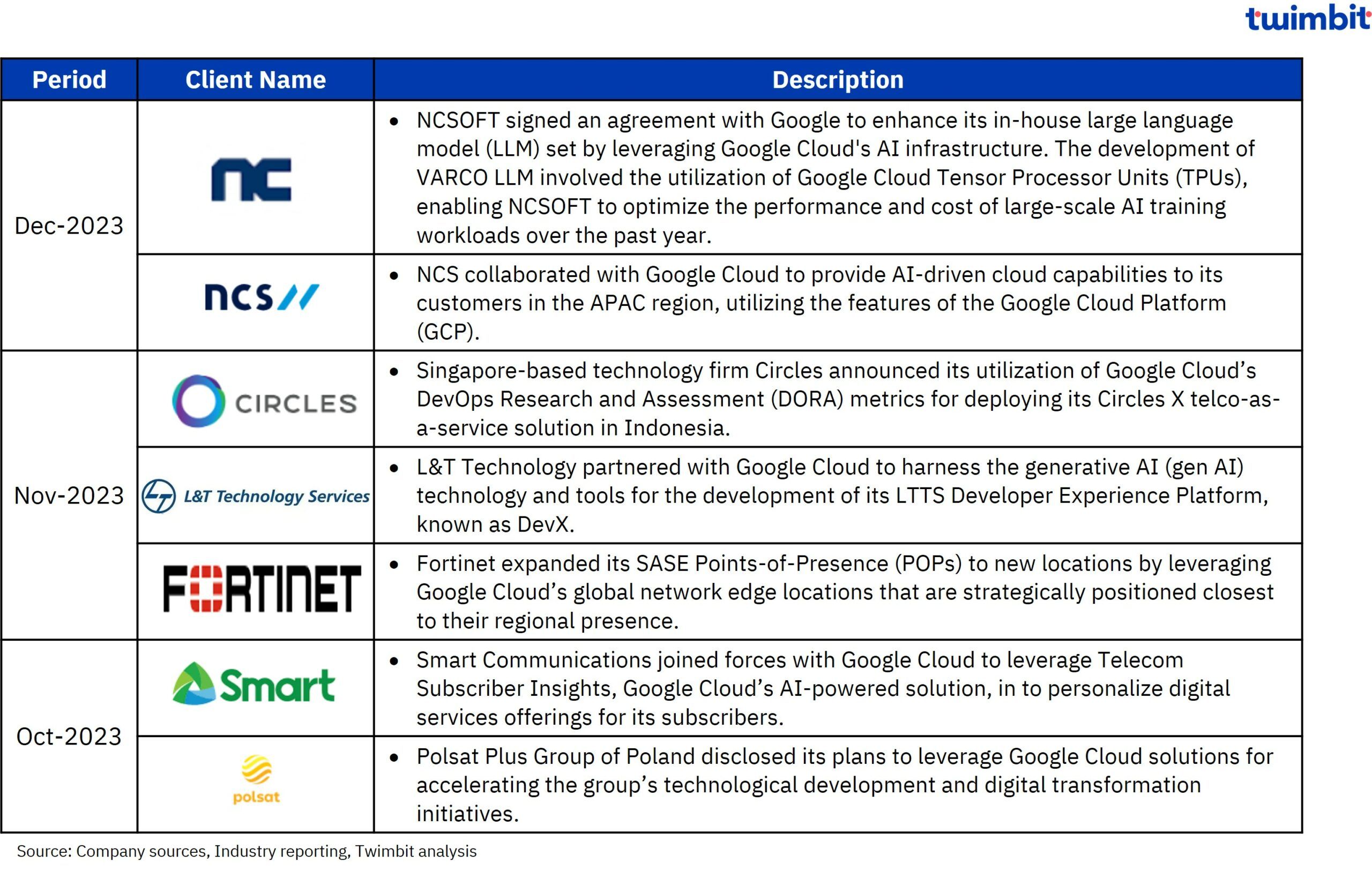

Key contract wins

D. Oracle Cloud

Overview

- Oracle Cloud Infrastructure (IaaS) segment displayed stellar growth, expanding by ~64.3% on YoY basis and reaching USD 5.7 billion revenue in FY-2023.

- The strong growth rate was owing to the continued growth in the OCI- IaaS segment revenue in all the quarters of FY-2023.

- Revenue increased by 60% in Q4-2023 (YoY basis) to reach USD 1.6 billion, as compared to 53.1% revenue growth (YoY basis) in Q4-2022.

- Revenue increased by an average 64.3% YoY for all the quarters in FY-2023.

- Oracle’s Infrastructure Cloud (IaaS) segment saw its contribution to overall revenue jump from 7.5% in FY-2022 to 11% in FY-2023, reflecting its impressive growth trajectory.

- This surge was driven by consistent quarterly growth throughout FY-2023, culminating in a peak contribution of 12.4% in Q4-2023, the highest since Oracle began reporting IaaS as a distinct segment.

- This was driven by continued growth in the OCI- IaaS segment revenue in all the quarters of FY-2023 and the contribution reached 12.4% in Q4-2023, the highest since Oracle started reporting its IaaS segment distinctly.

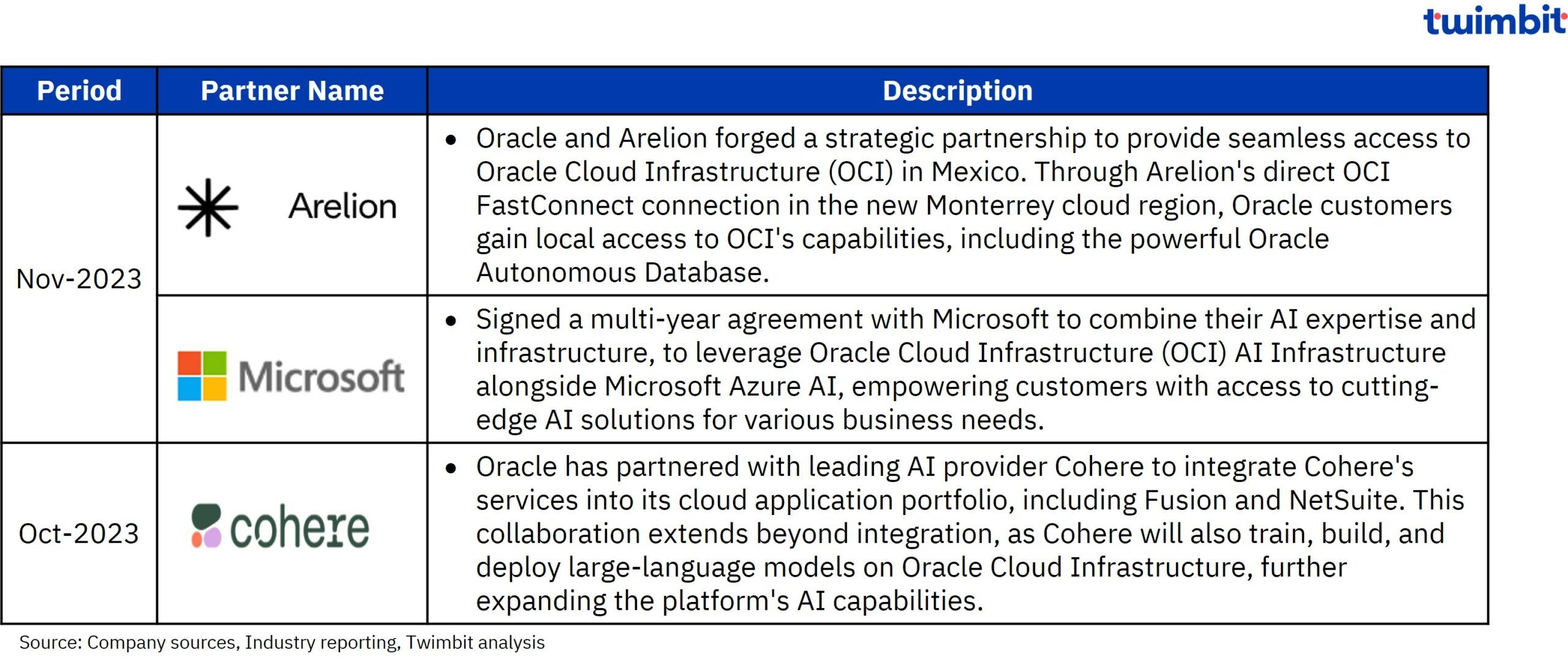

- Oracle announced a strategic partnership with Microsoft Azure for 20 co-located data centers, expanding its multi-cloud strategy.

- Oracle’s announcement of sovereign data center orders from several countries including Bangladesh, Italy, Japan, Saudi Arabia and New Zealand, highlights the growing importance of data residency in the cloud computing landscape.

- To accelerate revenue growth, Oracle plans to migrate half of Cerner’s Millennium customers to OCI by February 2024, leveraging a subscription model.

- Oracle completed the acquisition of Cerner (health information systems supplier) for USD 28.3 billion in Dec-2021, to strengthen its presence in the healthcare segment.

Oracle Cloud global footprint

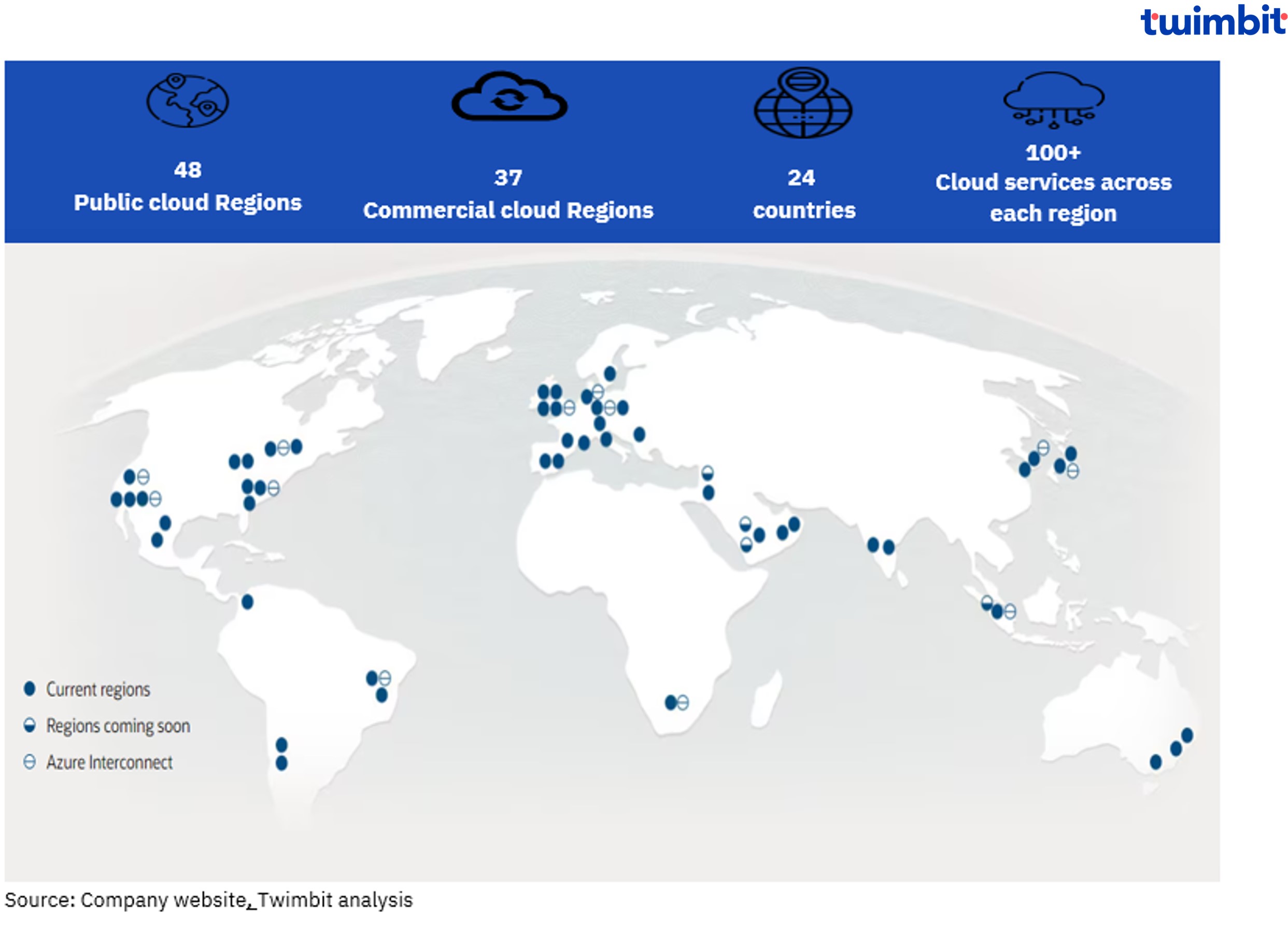

- Oracle offers 100+ cloud services across 48 Public cloud regions across 24 countries, including 6 regions in LATAM.

- Offers dedicated EU Sovereign Cloud regions and distinct government clouds for the US, UK, and Australia to address regional data residency regulations. Also, isolated cloud regions cater to US national security requirements.

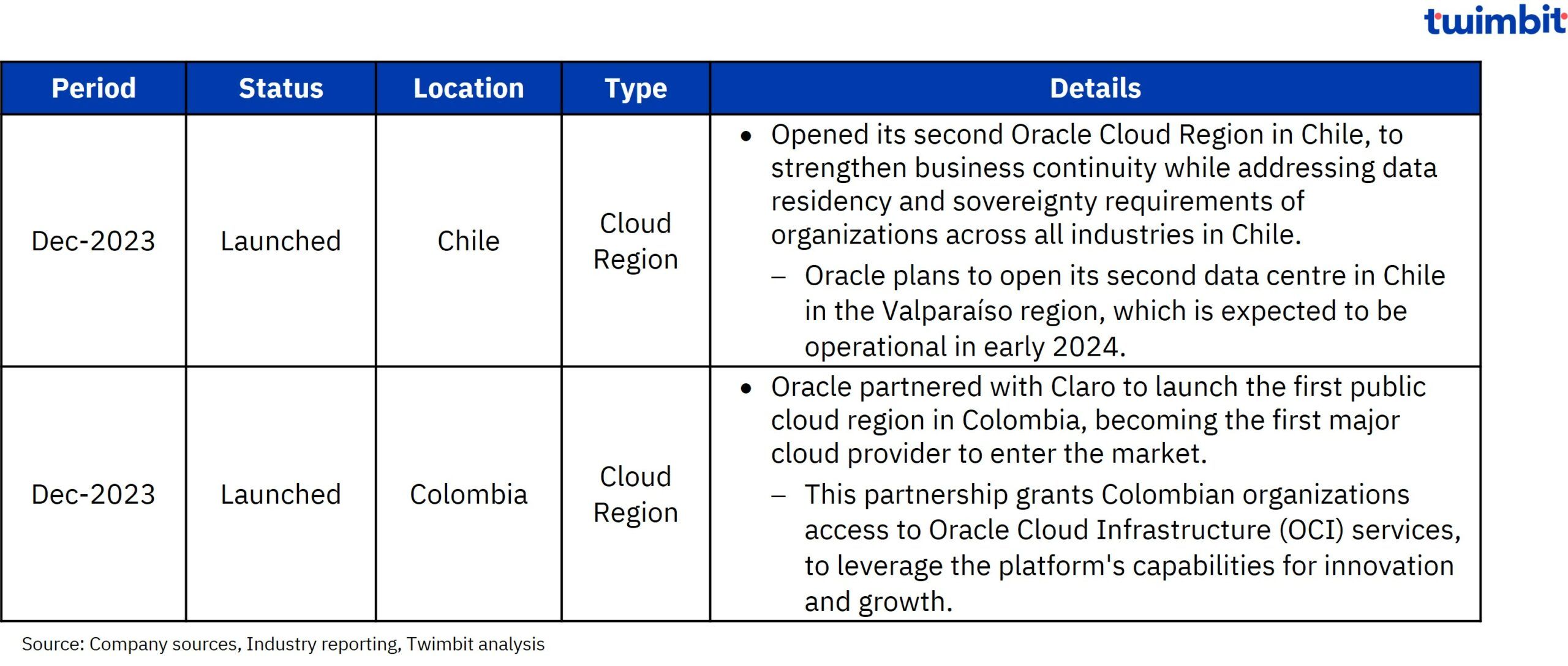

- In LATAM, Oracle has six cloud regions, with presence in Brazil, Mexico and Chile. Launch of the first cloud region in Colombia further strengthened its presence in the region.

Exhibit 9: Oracle Cloud global capabilities

Exhibit 10: Oracle Cloud – Key launches and announcements

- During Q4-2023, Oracle continued to strengthen its cloud presence particularly in the Latin American region and became the first hyperscaler to have two regions in the country.

- It also plans to build 100 new cloud data centres and expand the size and services of its existing 66 centres.

Key product initiatives

Key partnerships

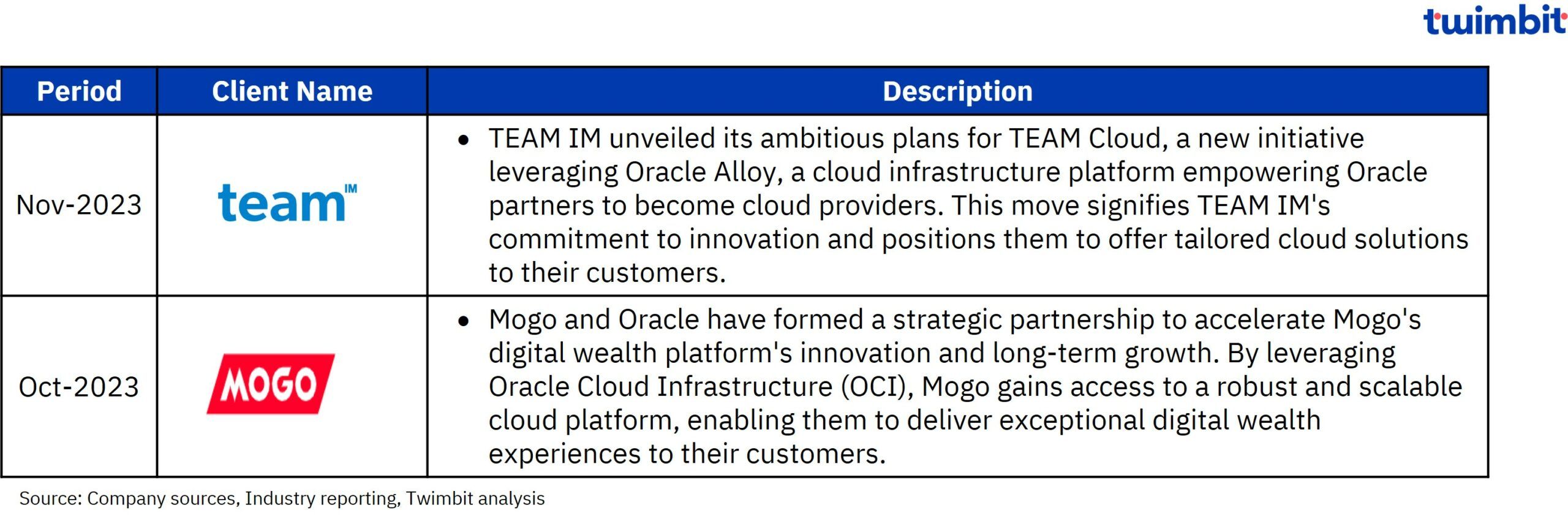

Key contract wins

Research methodology and assumptions

- The report primarily leverages company websites and publicly disclosed information from major cloud service providers.

- Analyses aggregate performance and future plans of leading providers is used to project potential demand trends, wherever applicable.

- The report covers Q4-2023 for all four providers, analyzing product initiatives, partnerships, and contract wins. Also, aligns Oracle’s fiscal year with calendar year by considering Q2-FY2024 as equivalent to Q4-CY2023.

- Oracle Cloud revenue reporting (IaaS + SaaS) has been realigned from Q3-2023 onward and now tracks only Oracle Infrastructure Cloud (IaaS) revenue.

- Previous quarter figures may differ slightly from prior reports due to the focus on Microsoft Intelligent Cloud (MIC) encompassing Azure and related services.

- Specifically for Google, the revenue numbers are for Google Cloud which encompasses various services like Workspace, Google Cloud Platform, data & analytics platforms, infrastructure, and collaboration tools. It’s important to note that Google doesn’t report GCP revenue separately, but rather as part of the broader Google Cloud segment.