Introduction

Digital transformation in ASEAN

As financial barriers fall and digital adoption rises, ASEAN is becoming a global leader in cross-border payment innovation. Consumers are shifting from cash and traditional banking to digital solutions for greater convenience. SMEs, the backbone of ASEAN’s economy, benefit from easier access to financial services and cross border trade.

Rise of digital payment solutions

Among the various digital payment solutions, QR codes and Account-to-Account (A2A) payments have seen remarkable adoption rates. QR codes enable seamless payments across countries and A2A facilitates direct account transfers, enhancing speed and efficiency. By 2030, the combined gross transaction value (GTV) for

account-to-account (A2A) and e-wallet transactions is projected to reach US $2,100- US $2,400 billion.

Market growth and regional initiatives

This shift is more than a technological upgrade. It is reshaping how Southeast Asia’s fast-growing population conducts commerce. Widespread QR code adoption, the rise of A2A payments, and initiatives like Project Nexus are driving change. With a 4.6% annual growth rate, ASEAN is outpacing China, the U.S., and the EU.

This report explores cross-border payment developments across ASEAN member countries, highlighting key developments and trends shaping the future of financial transactions in the region.

Thailand

The Bank of Thailand (BOT) is exploring tokenization for cross-border transactions in collaboration with the Hong Kong Monetary Authority through initiatives like San and Ensemble. These projects aim to improve the security and efficiency of digital payments. In partnership with countries such as Singapore, Malaysia, and Indonesia, Thailand has integrated its real-time payment (RTP) networks, significantly accelerating cross-border transactions.

Growth in transactions and spend per transaction

- Online transactions: Average growth rate of online transactions 53% in June 2024.

- Point-of-sale transactions (including e-money): Maintained steady growth, around 50-60% since mid-2023.

- ATM transactions: Grew over 100% in 2022 and early 2023 but slowed to under 10% YoY in 2024, with some months showing slight declines.

- Debit card transactions: Grew over 100% YoY since 2022, dropped to 46% in June 2024.

- Credit card usage: Turned negative in early 2024 and rebounded to 26% YoY growth by June 2024.

- Outbound card transactions from Thailand reached US $1.94 million (THB 69.3 million) in H1 2024.

- Four-year growth in foreign card spending saw a 163% rise from US $4.8 billion (THB 149 billion) in H1 2020 to H1 2024.

Challenges

Despite significant advancements in digital payments, Thailand’s cross-border payment ecosystem still faces several challenges.

- Interoperability issues make cross-border transactions difficult due to inconsistent payment systems and QR standards.

- Outdated legacy systems in 14% of Thai banks create inefficiencies and increase operational costs.

- Financial institutions operating in Thailand encounter a variety of regulatory standards that differ not only from each other but also from those in neighbouring countries.

- SME payment challenges result from high fees, limited banking services, and delays in cross-border payments.

Initiatives

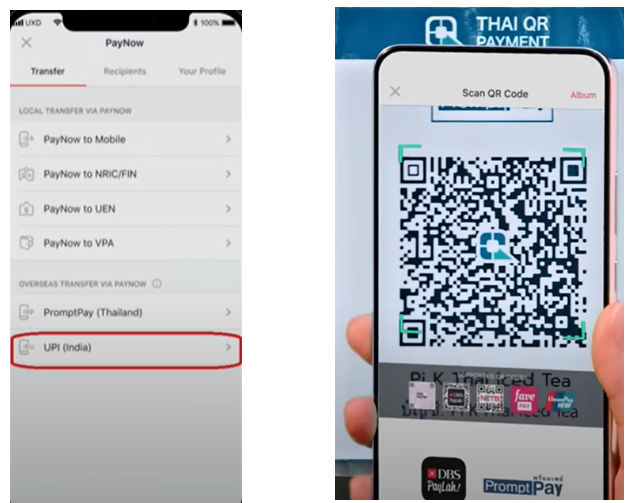

- QR Code scan – KASIKORNBANK enables Thai travellers to pay instantly in Singapore by scanning QR codes through banking apps, using blockchain for secure transactions.

- Stablecoins for remittances – SCB has partnered with Lightnet to use stablecoins for stable, cost-effective cross-border payments. Unlike volatile cryptocurrencies, stablecoins offer price stability, making them ideal for transactions and remittances.

- Fast payment systems (FPS) – Project Nexus aims to standardize connections for seamless cross-border payments.

Innovation opportunities

- Blockchain powered payment system- It is a digital payment network that uses blockchain technology to process transactions securely and instantly across borders.

- Traditional banks and fintech companies collaborate to provide innovative cross-border solutions for SMEs.

Impact of these initiatives and innovations:

- SME transactions completed in under five minutes

- Daily transfer limits of THB 25,000 (US $735)

- Reduced remittance costs encouraging formal channel usage

Singapore

Singapore’s payment landscape is among ASEAN’s most advanced, led by banks and digital wallets. Apps like DBS PayLah! dominate with seamless P2P and P2B transfers. QR payments are growing among small merchants due to lower fees. However, B2B transactions still rely on traditional wire and bank transfers for cross-border payments.

Challenges

Despite Singapore’s reputation as a leader in digital payment solutions, there are notable challenges, especially in the B2B sector. Many businesses still depend on wire and bank transfers for cross-border.

- Reliance on traditional bank transfers, which are often slow and costly. B2B cross-border payments can take several days to process, with fees ranging from US $10 to US $25 per transaction, not including foreign exchange costs

- Managing compliance with varying regulatory requirements

- Achieving full interoperability remains a challenge due to differences in technical standards and operational procedures

- Businesses still rely on manual processes

- Limited consumer awareness

Initiatives

- PayNow-PromptPay linkage facilitates real-time cross-border transactions between Singapore and Thailand .

- Digital economy agreements simplify compliance and enhance cross-border transactions by reducing duplicative processes like KYC checks.

- Major Payment Institution (MPI) License Initiatives promote competition and support secure, efficient payment solutions for SMEs in international trade.

- PayNow-UPI linkage allows users in Singapore and India to transfer funds instantly between bank accounts and e-wallets.

- Adoption and consumer awareness

Innovation opportunities

PayNow-PromptPay Linkage

- Speed – Transfers complete in under five minutes, far quicker than traditional methods that take 1-2 business days.

- User Experience – Money can be sent using just a mobile number, eliminating the need for full bank account details.

PayNow-PromptPay process overview

- Registration: Users link their mobile number or national ID to their bank account to register for PayNow (Singapore) or PromptPay (Thailand).

- Transfer: Users select PayNow/PromptPay in their banking app, enter the recipient’s number/ID, and specify the amount.

- Real-time processing: Transactions are processed instantly, enabling 24/7 cross-border transfers.

- Security: Strong security measures protect user data and transactions.

- Convenience: Simplifies payments and reduces transaction fees compared to traditional remittance services.

Impact of these initiatives and innovations:

- Real-time cross-border transfers in under five minutes

- Eliminating the need for complex bank details

- Streamline KYC checks & regulatory processes

- Reduction in hidden banking fees and FX costs

- Consumer awareness initiatives help bridge knowledge gaps, encouraging more people to switch from manual transfers to instant digital payments.

Malaysia

Malaysia is driving regional efforts to improve cross-border payment systems, including initiatives like QR-code connectivity and Project Nexus. These projects aim to streamline transactions, reduce costs, and foster financial integration in Southeast Asia and beyond.

Challenges

Achieving seamless interoperability across borders remains a challenge.

- Interoperability issues: Inconsistent payment systems and QR code standards hinder seamless cross-border transactions.

- Digital payment gaps: Urban areas have advanced digital payment infrastructure, while rural regions lack reliable internet and modern technologies, limiting SME participation in the digital economy.

Initiatives

- E-wallets: Alipay+ collaboration allows travelers to use e-wallets at 1.8 million merchant touchpoints in Malaysia.

- Surge in total payment value of Touch ‘n Go e-wallet: The overseas QR payment feature of TNG eWallet saw its TPV increase by over 170 times between March 2023 and March 2024,

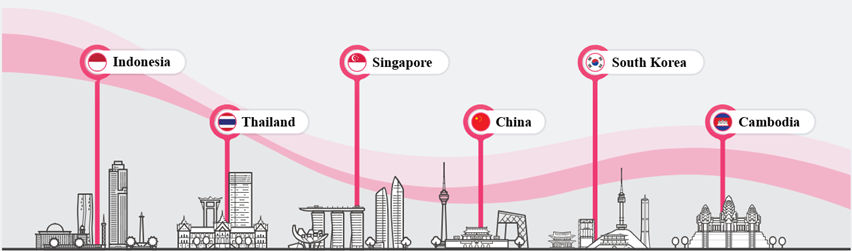

- Real-time transactions: DuitNow enables instant money transfers with Singapore, Indonesia, Thailand, China, South Korea and Cambodia.

- Multi-currency wallets: Developing wallets integrated with national payment schemes.

- Blockchain: Leveraging blockchain for cross-border remittances.

Innovation opportunities

- Real time retail payment platform (RPP): The Malaysian government is advancing real-time payments

- Transparent & real-time foreign exchange rates

- Seamless cross-border QR payments

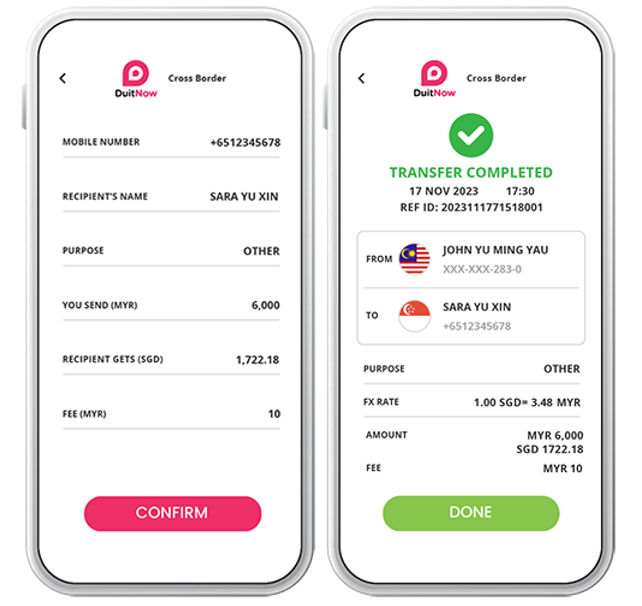

Through a partnership with PayNow Singapore, Malaysians can now instantly do fund transfer via DuitNow using their mobile banking or e-wallet apps. Transfers can be made to any PayNow-registered mobile number in Singapore.

Impact of these initiatives and innovations:

- Accurate, upfront currency conversion eliminates hidden fees

- Faster transactions for businesses and individuals

- DuitNow enables instant transfers, reducing costs and delays

- Cross-border e-wallets boost financial inclusion by helping the unbanked & underbanked populations participate in the digital economy

Malaysia collaborated with central banks to enable cross-border payments via DuitNow QR. Malaysian tourists in Indonesia, Singapore, Thailand, and China can now use their preferred mobile banking or e-wallet apps to scan QR codes (QRIS, NETS, PromptPay, Alipay) for payments at participating merchants.

QR-Code connectivity for local currency settlements

Malaysia, along with Indonesia, Thailand, Singapore, and the Philippines, agreed to establish QR-code connectivity to facilitate local currency settlements across borders. The primary goal of this initiative was to reduce transaction costs and streamline payments for both consumers and businesses.

Key features:

- Cross-border local currency settlements: Facilitating payments in local currencies between these nations.

- QR Code connectivity: Enables easy, instant payments using QR codes across borders.

By 2026, these initiatives will lower transaction costs, enhance trade, and streamline financial flows across Southeast Asia and India

Indonesia

Cross-border QRIS payments in Indonesia have become increasingly popular among foreign tourists from Malaysia, Singapore, and Thailand.

Bank Indonesia (BI) has highlighted a surge in the use of the Quick Response Code Indonesia (QRIS) system by international visitors within the country.

Increased usage among foreign tourists:

| Country | MoM Increase | Growth Hotspots |

| Singapore | 28% | Jakarta, Riau |

| Thailand | 13% | Jakarta, West Java |

| Malaysia | 8% | Hendarta, Jakarta, West Java |

Growing use of QRIS by Indonesians abroad:

| Country | MoM Increase | Growth Insights |

| Thailand | 9% | QRIS usage by Indonesian citizens grew |

| Malaysia | 4% | QRIS usage by Indonesian citizens increased |

Currently, cross-border QRIS is available for use in Indonesia’s neighbouring countries, including Malaysia, Singapore, and Thailand. The system is integrated with mobile banking applications from several registered Indonesian banks, such as Bank Central Asia (BCA) and Bank Mandiri.

Challenges

As cross-border payment networks expand, several operational and regulatory challenges emerge.

- High costs of transactions

- Limited access to payment solutions for SMEs due to stringent requirements imposed by banks and payment service providers

- Interoperability among various payment systems

Initiatives

- PingPong’s payments license in Indonesia aims to lower costs for low-value transactions.

- Bank Rakyat Indonesia (BRI) has partnered with Nium to improve real-time international transfers, enhancing access for underserved communities.

- Bank Indonesia has mandated the use of QRIS for payment interoperability since January 2020.

- The Indonesian government is encouraging fintech growth by allowing non-banks to issue e-money for retail payments.

Innovation opportunities

Indonesian Standard QR Code (QRIS):

- Facilitates transactions using local currencies across member states

- More inclusive financial ecosystem that benefits both consumers and businesses

Impact of these initiatives and innovation:

- Low-value cross-border transactions at reduced fees

- Real-time international money transfers with lower costs

- Standardized QR codes simplify transactions

- Simplified onboarding for SMEs, enabling easier cross-border trade & e-commerce expansion

- Seamless QR-based payments encourage tourism & retail spending

Vietnam

Vietnam is actively advancing its cross-border payment systems to enhance economic integration in Southeast Asia. With a focus on improving payment efficiency and reducing transaction costs, the country is working on strengthening interoperability with regional and global financial networks, supporting both trade and tourism.

Market growth:

Transaction value increase

- Overall Growth: The total value of digital payment transactions increased by 15.9%.

- NAPAS 24/7 Fast Transfer: This service experienced a significant uptick:

- Volume Growth: 34.7% increase.

- Value Growth: 16.4% rise.

- System Share: Accounts for 93.5% of all NAPAS system transactions.

Rise of VietQR Payments

- Transaction Volume: Increased by 2.2 times compared to the previous year.

- Transaction Value: Rose by 2.6 times, demonstrating its growing importance in Vietnam’s payment ecosystem.

Challenges

When it comes to cross-border transactions, Vietnam still faces key challenges that hinder seamless payments with regional and global market.

- Regulatory fragmentation leads to inconsistent digital payment standards across ASEAN, complicating cross-border transactions and compliance.

- Limited financial literacy among individuals and small business owners hampers adoption of digital financial services, stalling economic growth.

Initiatives

- Vietnam has signed a MoU (Memorandum of understanding) with ASEAN member countries to develop a cross-border payment system for faster, affordable, and transparent retail transactions via QR codes and instant payments.

- State Bank of Vietnam (SBV) and the National Bank of Cambodia (NBC) has launched a cross-border QR payment system for payments in domestic currencies.

- NAPAS 24/7 fast transfer system enhancement

- VIB and Flywire partnership enables Vietnamese students to pay fees to global educational institutions in their local currency through a user-friendly online platform

5. Enhancing interoperability with initiatives like the national QR code framework (VietQR)

Innovation opportunities

- Standardized payment protocols

- Real-time, 24/7 cross-border transactions

- Unified QR payment system across banks and e-wallets

- API-driven payment systems to improve scalability, security, and processing speed

Impact of these initiatives and innovations:

- Low-cost tuition payments for Vietnamese students

- Faster, cheaper international payments support SME growth

- Standardized QR payments simplify transactions for travellers and merchants

Phillipines

By 2025, the Philippine payments landscape will be shaped by cross-border e-commerce growth, global digital wallet connectivity, and advanced security frameworks.

- Cross-border shopping: 34% of Filipino shoppers made monthly overseas purchases in 2024, up from 27% in 2023, driven by innovations like video commerce.

- E-wallets and connected commerce: E-wallets simplify transactions, enabling Filipinos to participate in a borderless economy.

Challenges

Despite growth opportunities, several challenges hinder the effectiveness and adoption of cross-border payment systems in the Philippines.

- Cross-border payments incur remittance fees averaging 6%

- Multiple validations and compliance checks increase delays and costs.

- Full interoperability across platforms remains a challenge, limiting payment solution effectiveness.

Initiatives

- Wholesale central bank digital currencies (CBDCs) by 2029 could streamline cross-border payments by reducing reliance on traditional banking and enabling faster settlements.

- Alipay+ and GHL Systems have partnered to enable cross-border digital payments for Philippine businesses.

- Wise connects to InstaPay, enabling instant cross-border payments in the Philippines.

Innovation opportunities

Integrate NEFT/ UPI for cross-border transfers so that larger amounts are processed in under 24 hours.

Impact of these initiatives and innovations:

- Direct central bank transactions reduce intermediaries

- Supports tourism and e-commerce growth

- More affordable cross-border remittances

Despite the growing shift toward digital payments, Cambodia, Laos, Brunei and Myanmar continue to face significant challenges in building a seamless and inclusive payment ecosystem:

- Regulatory & compliance barriers – Evolving regulations create uncertainty for businesses and slow the adoption of new payment technologies.

- High digital infrastructure costs – Building robust payment systems is expensive, especially for smaller banks and rural areas with limited resources.

- Financial inclusion gaps – Many citizens still lack access to digital payment tools, limiting adoption despite fintech efforts.

- Interoperability issues – Limited system compatibility prevents seamless cross-border and cross-platform transactions, restricting ASEAN-wide integration.

- Underdeveloped digital payment ecosystems – The slow rollout of mobile payments and digital banking infrastructure hampers financial innovation and accessibility.

Addressing these challenges will be crucial for fostering a more inclusive and efficient digital payment landscape in these nations.

Cambodia

Cambodia faces several significant challenges in cross-border payments. These challenges are influenced by both internal economic conditions and broader regional trends.

Initiatives to strengthen regional payment connectivity:

- Cambodia-Malaysia cross-border QR payment system– Enables payments via QR codes between the two countries.

- Phase One: Cambodian consumers can make retail payments in Malaysia by scanning DuitNow QR codes at participating merchants.

- Phase Two (Upcoming): Malaysian travellers will be able to use KhmerQR (KHQR) codes for payments in Cambodia.

Key Stakeholders:

- NBC (National Bank of Cambodia)

- PayNet (Payments Network Malaysia Sdn. Bhd.)

- Maybank (Sponsoring and settlement bank)

- Participating financial institutions from both countries

2. Bakong and Alipay+ partnership- In October 2024, the NBC partnered with Ant International to launch cross-border QR code payments via Alipay+. This integration allows users of 12 international payment apps to make transactions in Cambodia using KHQR codes.

International Payment Apps:

- Alipay

- AlipayHK

- Touch ‘n Go e-wallet

- GCash

- Kakao Pay

- Others

3. Cambodia-India payment system linkage- This initiative aims to expand the Bakong payment system’s reach, enhancing economic activities between the two nations.

Impact of these initiatives:

- Expansion of customer base through easier cross-border transactions.

- Provision of access to international tourists and consumers.

- Stimulate economic growth by simplifying payments and reducing transaction barriers.

- Financial inclusion & digital adoption

- Enhanced economic connectivity

Brunei

Brunei faces several challenges in cross-border payments. These challenges stem from both technological and regulatory aspects, impacting the efficiency and effectiveness of its payment systems.

Initiatives

Based on the Digital Payment Hub (DPH) initiative:

- ASEAN QR code integration: The DPH enables cross-border payments via QR codes between Brunei and ASEAN countries. By 2025, DPH will add QR payments and “request-to-pay” features for international payments.

- Cross-Border payment efficiency: Brunei customers can pay in ASEAN, and ASEAN visitors can use local apps for payments in Brunei.

- Bilateral connections: Technical connections are required for seamless payments across ASEAN.

- Full functionality: Full cross-border functionality is expected post-2025.

- Collaborative development: The DPH is a joint effort between Bruneian banks and Darussalam Assets.

Impact of these initiatives:

- Faster transactions: Enabling quicker and more cost-effective cross-border payments.

- QR & fast payments: Promoting QR code-based and fast payment solutions for seamless transactions.

- Support for SMEs: Enhancing access to international markets and simplifying trade and remittances for SMEs.

- Economic growth: Stimulating regional trade, investment, and economic activity.

Laos

The cross-border payment landscape in Laos is undergoing transformation, driven by regional cooperation and advancements in digital payment technologies.

Initiatives

The initiatives are part of a broader push to improve financial connectivity in the region, making cross-border transactions more seamless and efficient for consumers and businesses alike.

- Cross-border QR payment linkage & regional integration: Laos and Thailand launched QR payment linkages

- Micropayment systems & digital adoption: Kip-Dong system enables Vietnam-Laos QR payments, driving mobile banking and e-wallet adoption in Laos.

Impact of these initiatives:

- Improvement in cross-border payment interoperability

- Increase in mobile banking and e-wallet adoption

- Boost in demand for cross-border payment solutions and regional growth

Myanmar

In 2024, Myanmar’s involvement in cross-border payment systems within the ASEAN framework is shaped by significant regional initiatives aimed at enhancing financial connectivity and inclusion. Despite ongoing challenges, particularly due to the political situation in Myanmar, various efforts are underway to integrate its payment systems with those of other ASEAN nations.

Myanmar’s participation in Project Nexus is crucial for its integration into regional payment systems. Currently, Myanmar lacks a fully operational FPS, which poses a barrier to its participation. However, efforts are being made to develop such systems with support from international partners like the Bill and Melinda Gates Foundation and the Monetary Authority of Singapore.

Conclusion

By 2030, the ASEAN payments market will reach US $1 trillion, driven by innovation, regional cooperation, and digital infrastructure. The NIPL-Liquid Group partnership to enable QR-based UPI payments across 10 countries including Malaysia, Thailand, Philippines, Vietnam, Cambodia, Singapore, South Korea, Japan, Taiwan, and Hong Kong will further enhance cross-border payment integration. This collaboration strengthens ASEAN’s payment systems, making transactions faster, cheaper, and more inclusive, driving economic growth and financial inclusion across the region.