Key Takeaways

- The APAC telco landscape is experiencing a significant shift towards a more diversified revenue model, with the enterprise segment playing a crucial role. This trend is fueled by a strategic focus on non-connectivity services and digital solutions offerings, leading to promising growth prospects.

- APAC telco enterprise revenue surged 11.4% YoY to reach ~USD 121 billion in FY-2023, significantly outpacing overall telco overall revenue growth (4.9%).

- Increasing intensity by telcos in the enterprise segment highlights a strategic shift to become “one-stop shop” that offer comprehensive digital solutions beyond core connectivity, unlocking new revenue streams.

- The enterprise segment has become a key growth driver, accounting for an average of 22.0% of total revenue in FY-2023, up from 20.8% in FY2022.

- Nearly 43% of telcos surpassed the 25% enterprise revenue contribution threshold, with PCCW, Spark, Mobile One, StarHub and Chunghwa leading the pack.

- Around 73% of telcos witnessed relatively higher YoY revenue growth from enterprise segment in FY2022 -FY2023, with China-based telcos (China Unicom, China Telecom, China Mobile) leading enterprise revenue growth.

- Enterprise non-connectivity revenue contribution to overall revenue increased by 210 bps YoY to 13.4% in FY-2023, reaching USD 72.2 billion.

- Nearly 22% of telcos achieved significant non-connectivity revenue contribution (20% of overall revenue); with SingTel, Telstra, StarHub, Spark, and Telecom Malaysia leading the way.

- China-based telcos drive strong growth in non-connectivity by diversifying into AI, cloud computing, Big Data, IoT, and Smart Car solutions.

- Cloud, analytics, managed services, and AI have emerged as key growth enablers within the enterprise segment. Additionally, telcos offer financial services, content and media, and AR/VR gaming offerings for incremental revenue from the consumer segment.

- Twimbit estimates the shifting focus of telcos to “beyond connectivity” offerings as a key driver of future revenue growth. It will account for ~37.8% of overall revenue by 2027, signifying a strategic move beyond core services.

- Within the enterprise (B2B) segment, non-connectivity offerings are emerging as a critical growth strategy. By expanding their portfolio beyond core connectivity, telcos can cater to evolving enterprise needs with comprehensive solutions. Twimbit estimates the enterprise segment to account for ~29% of overall telco revenue by FY-2027.

Overview

There is considerable synergy between connectivity and broader ICT (Information and Communications Technology) offerings to enterprise customers. Furthermore, the evolving customer demand for complex solutions needs places telcos in a unique position to leverage their core assets and become strategic partners.

The initial foray into ICT services has yielded mixed results. A few have established themselves as credible contenders despite recording lower profit margins than their core business. Fortunately, this is likely to improve in the near future. Recognizing this, telcos must acknowledge this market’s “go-big-or-go-home” nature, requiring a significant scaling of their ICT service offerings.

Furthermore, telcos possess the expertise to provide comprehensive data and digital transformation consulting services for enterprise and mid-market segments. This data is essential for financial services, manufacturing, and the public sector, which grapple with complex compliance requirements, legacy system integration, and data unification. Hence, by offering data-driven and digitally enabled services to empower their business customer, leading telcos can actively address these challenges.

The increasing reliance on technology for core operations and innovation marks a compelling growth trajectory for telcos to embrace the ICT service opportunity fully. This presents a unique value proposition for telcos to reposition themselves as “Tech-co” and offer a comprehensive technology portfolio of – all-device connectivity, collaboration tools (unified communications and contact centres), cloud infrastructure, and robust cybersecurity solutions.

Historically, telcos have focused on building in-house ICT capabilities or resorting to large-scale acquisitions. Moving forward, a more strategic approach would encompass strategic partnerships with technology companies, effectively “wrapping” their services around core offerings. Additionally, targeted acquisitions can then be employed to fill any remaining gaps in the service portfolio.

The opportunity is now. By embracing a strategic and collaborative approach, telcos can capitalize on their existing strengths and become indispensable partners in the digital transformation journey of their business customers. However, achieving this feat requires a shift from replicating past successes to a forward-thinking vision. This new found vision should seek to leverage partnerships, selective acquisitions, and organic growth to establish itself as the trusted ICT orchestrator of the future.

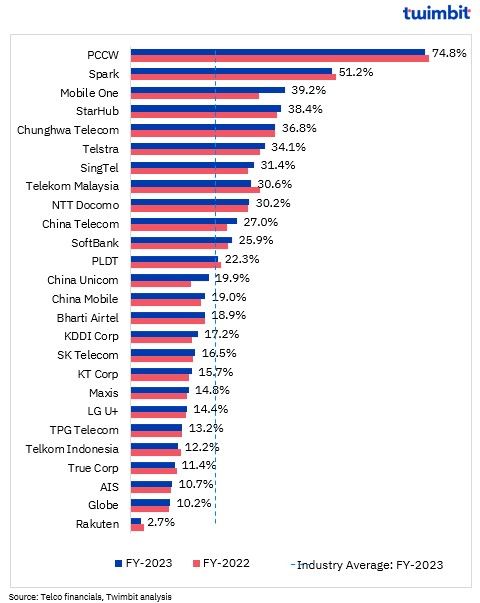

Enterprise revenue analysis of APAC telcos: 2023

Enterprise segment contributed 22.0% of the overall revenue of telcos in FY-2023, marginally higher from 20.8% in FY-2022

- Enterprise revenue for APAC telcos surged by an impressive 11.4% year-on-year (YoY), reaching ~USD 121 billion in FY-2023.

- This growth significantly outpaces the telco’s overall annual revenue growth of 4.6% in FY-2023, highlighting the strategic shift to transform into “one-stop shop” offering a comprehensive suite of digital solutions to enterprises.

- Telcos are unlocking new revenue streams and diversifying their offerings by expanding beyond core connectivity services.

- The enterprise segment has emerged as a key growth driver, accounting for a substantial 22.0% of total revenues (average across all telcos) in FY-2023, compared to 20.8% in FY-2022. This trend highlights the growing significance of the enterprise segment for future revenue growth for APAC telcos.

Exhibit 1: Enterprise revenue as a % of total revenue, 2022 – 2023

- Nearly 43% of the telcos achieved significant enterprise revenue contributions, surpassing the 25% threshold led by PCCW, Spark, Mobile One, StarHub and Chunghwa.

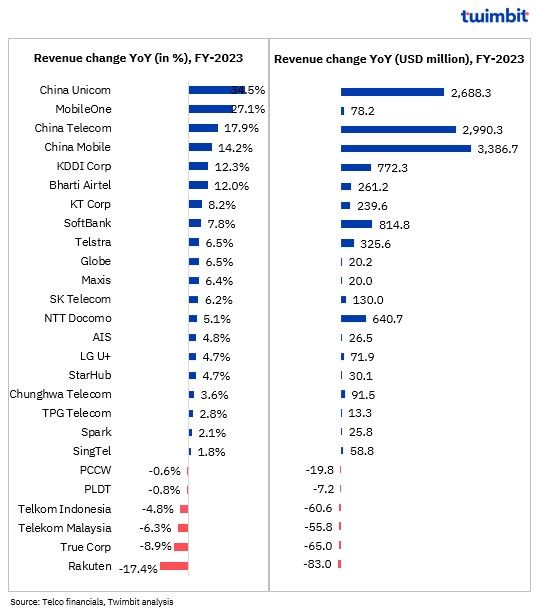

- Contrastingly, ~73% of the telcos witnessed YoY growth in overall enterprise revenue during FY2022 – FY2023.

- China based telcos (China Unicom, China Telecom and China Mobile), ranked amongst the among the leading 5 telcos to witness the highest enterprise revenue growth (YoY) in FY-2023.

Exhibit 2: Enterprise revenue trends, 2023

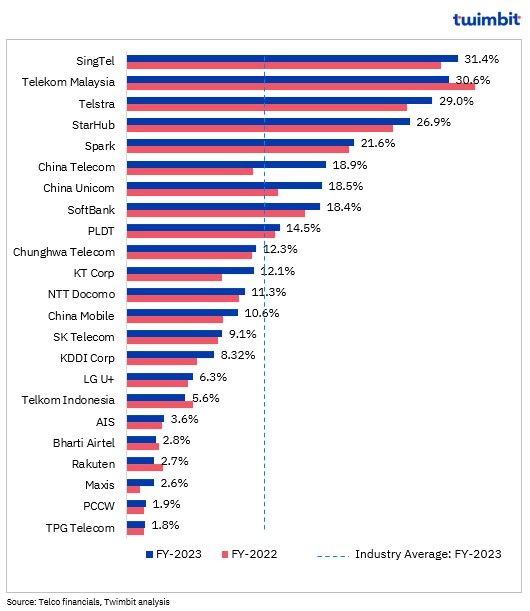

Enterprise non-connectivity revenue analysis of APAC telcos: 2023

Enterprise non-connectivity revenue contribution increased 10 basis points (bps) on a YoY basis in FY-2023 to reach 13.4%

- Enterprise non-connectivity segment revenue for APAC telcos grew 24.8% YoY to reach ~USD 72.2 billion in FY-2023.

- Nearly 22% of the telcos achieved significant non-connectivity revenue contribution (exceeding the 20% threshold) led by SingTel, Telecom Malaysia, Telstra, StarHub and Spark.

Exhibit 3: Enterprise non-connectivity revenue as a % of total revenue, 2022 – 2023

- Enterprise non-connectivity revenue contribution reached a significant 60.3% share of total enterprise revenues in FY-2023, compared to ~54% in FY-2022.

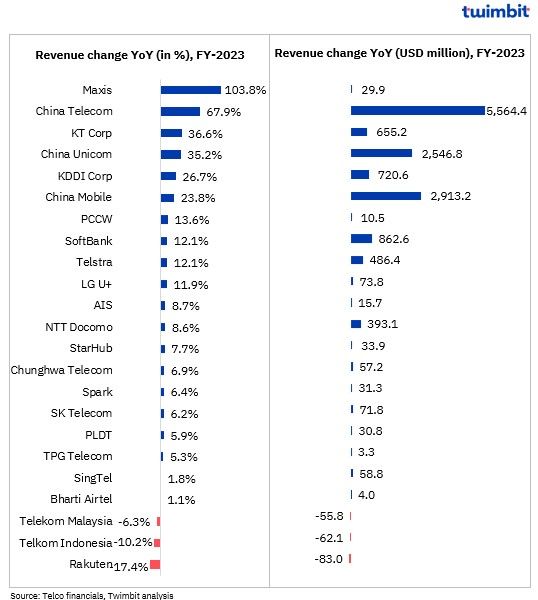

- The overall strong growth in the enterprise non-connectivity segment was primarily driven by China-based telcos (China Telecom, China Unicom and China Mobile), as they intensified diversification into areas apart from core network offerings such as AI, cloud computing and other digitalized service offerings such as Big Data, IoT, Smart cars etc.

Exhibit 4: Enterprise non-connectivity revenue trends, 2023

Enterprise Segment Performance of leading telcos

- PCCW’s enterprise segment experienced minimal YoY revenue growth in FY-2023, registering a slight decline of 0.6%. Despite this, the enterprise segment to revenue contribution accounted for 74.8%, the highest share amongst Asia-Pacific (APAC) telecommunication companies.

- This marginal decline can be attributed to a 2.3% YoY decrease in Hong Kong Telecom’s (HKT) International Telecommunication Services, reaching USD 932 million (HKD 7.3 billion).

- Non-connectivity revenue within the Enterprise segment demonstrated robust growth of 13.6%, representing 1.9% of the total enterprise revenue.

- This upsurge is attributed to increased revenue from external clients serviced by the Group’s “Other Businesses” segment. This segment primarily comprises the Solutions Business remaining after the 2022 deconsolidation of the ITS Business, along with corporate support functions.

- Spark’s enterprise revenue composition witnessed a strategic shift in FY-2023. While the enterprise segment remains significant, its representation as a percentage of total revenue declined to 51.2%, reflecting a 90-basis point (bps) decrease. Despite this compositional shift, the enterprise segment achieved a commendable YoY growth of 2.1%.

- The decline in the enterprise segment’s contribution to the overall revenue mix can be attributed to a 2.6% YoY decrease in IT services revenue during FY-2023.

- This decrease, coupled with a comparatively stronger overall YoY revenue growth of the telco, resulted in a net reduction in the enterprise segment’s relative contribution.

- Singaporean telecommunication companies MobileOne (M1) and StarHub exhibited robust performances within the enterprise sector during the 2023 fiscal year (FY-2023). Both operators secured a substantial portion of their total revenue from enterprise clients, exceeding the significant benchmark of 35%.

- M1 achieved an impressive 27.1% YoY increase in enterprise revenue in FY-2023, translating to USD 366.4 million (~SGD 492 million) – a noteworthy 39.2% of the company’s total revenue.

- M1’s enterprise business success is due to its ability to actively roll out innovative solutions that promote 5G adoption and simultaneously cultivate new revenue streams through scalable 5G industry solutions implemented domestically and internationally.

- Key initiatives in FY-2023 include the Pinnacle Multi-access Edge Computing (MEC) platform specifically designed for enterprises. Additionally, M1 adopted CSG’s Ascendon, a Software-as-a-Service (SaaS) platform, further enhancing its digital B2B service offerings.

- M1 also leverages its subsidiaries, AsiaPac and Glocomp, to continuously scale up its enterprise business, aligning with its strategic vision for regional expansion.

- StarHub’s enterprise segment demonstrated continued progress in FY-2023, with enterprise revenue expanding by 4.7% YoY to reach USD 674.6 million (SGD ~906 million). This growth translated to a significant contribution increase of 120 bps to 38.4% of overall revenue.

- The enterprise connectivity segment experienced a 1.9% YoY decline to USD 202.4 million (SGD 271.8 million).

- Voice services revenue witnessed a modest 2.1% YoY growth

- A 2.5% decline in Data & Internet services

- Non-connectivity revenue, encompassing Managed Services, Cybersecurity Services, and Regional ICT Services, emerged as a key growth driver and registered a robust 7.7% YoY increase to USD 472.2 million (SGD 634.1 million) despite declining Regional ICT Services.

- Managed Services: This segment displayed exceptional growth of 18% YoY to reach USD 74.5 million (SGD 100.1 million). This growth can be attributed to more project completions and an increased contribution from data centre-related services.

- Cybersecurity Services: Revenue in this segment surged by 16.3% YoY to USD 260.7 million (SGD 350.1 million), driven by a significant rise in project completions.

- Regional ICT Services: This segment experienced an 8.2% YoY decline in FY-2023 to approximately USD 136 million (SGD 182.5 million)

- The enterprise connectivity segment experienced a 1.9% YoY decline to USD 202.4 million (SGD 271.8 million).

- M1 achieved an impressive 27.1% YoY increase in enterprise revenue in FY-2023, translating to USD 366.4 million (~SGD 492 million) – a noteworthy 39.2% of the company’s total revenue.

- China’s telecommunications (Telco) sector has witnessed continued buoyancy in the enterprise segment, with leading operators experiencing significant annual revenue growth. This robust performance stems from a strategic focus on non-connectivity revenue streams, bolstering overall enterprise revenue figures.

- China Unicom exemplifies this trend, boasting an impressive 34.5% YoY growth in enterprise revenue, reaching USD 10.5 billion (CNY 74.1 billion) in FY-2023. This surge significantly elevated the enterprise segment’s contribution to overall revenue, rising from 15.5% in FY-2022 to 19.9% in FY-2023.

- A key driver of this expansion is China Unicom Cloud, which achieved a remarkable 41.6% YoY growth in revenue, reaching USD 7.2 billion (CNY 51 billion) in FY-2023. The company reports a staggering 186% annual growth rate in cloud resource sales, exceeding one million cores.

- China Unicom Cloud’s reach extended to critical national projects, with successful implementations for 21 national ministry-level endeavours.

- The company has played a pivotal role in building 19 provincial government clouds and supporting over 1,000 medical cloud projects throughout the year.

- China Telecom witnessed a robust expansion in its enterprise segment, with revenue contribution rising by 250 bps YoY to reach 27% of total revenue in FY-2023. This translates to an impressive 17.9% YoY growth in enterprise revenue, reaching ~USD 19.7 billion (CNY 138.9 billion).

- China Telecom Cloud was a primary growth driver for China Telecom, with the segment experiencing a staggering 67.9% YoY increase in revenue, reaching USD 13.8 billion (CNY 97.2 billion).

- This highlights China Telecom’s commitment to facilitate digital transformation for its enterprise and government clients through its cloud, Big Data, and AI offerings.

- The company reported a 35.3% annual increase in enterprise and government customers for the China Telecom Cloud in FY-2023.

- China Mobile also demonstrated strong growth in the enterprise segment, with revenue increasing by 14.2% YoY to reach approximately USD 27.2 billion (CNY 192.1 billion). The enterprise segment now accounts for 19% of China Mobile’s overall revenue in FY-2023, up from 17.9% in the previous year.

- The Data, Information and Communications Technology (DICT) segment was a key contributor to this growth, where revenue surged by 23.8% YoY to reach USD 13.8 billion (approximately CNY 107 billion). This trend coincided with a notable expansion in China Mobile’s corporate customer base, which grew by approximately 5.2 million to reach 28.4 million in FY-2023.

- Furthermore, China Mobile achieved impressive progress in 5G DICT projects, completing approximately 15,000 projects with a 22.4% annual increase. The contract value for these projects also witnessed significant growth, rising by 30.1% YoY to reach USD 6.7 billion (CNY 47.5 billion).

- Mobile Cloud revenue emerged as another growth engine for China Mobile, with a remarkable 65.6% YoY increase to USD 11.8 billion (CNY 83.3 billion) in FY-2023.

- Industry Cloud accounted for a substantial portion of this growth, reaching ~USD 10 billion (CNY 70.8 billion).

- China Unicom exemplifies this trend, boasting an impressive 34.5% YoY growth in enterprise revenue, reaching USD 10.5 billion (CNY 74.1 billion) in FY-2023. This surge significantly elevated the enterprise segment’s contribution to overall revenue, rising from 15.5% in FY-2022 to 19.9% in FY-2023.

- Japan based telcos witnessed YoY growth in enterprise revenue during FY-2023, exceeding an impressive 5% overall.

- KDDI reported 12.3% YoY increase in enterprise revenue, reaching ~ USD 7 billion (JPY 990.1 billion). This growth was driven by advancements in their Internet of Things (IoT) and data centre businesses.

- KDDI’s IoT connections surged by 31.7% YoY to 39.5 million, further bolstered by a combined figure of 45.5 million when including Soracom (acquired entity).

- Increased demand fueled a 21.7% YoY rise in data centre business revenue, reflecting KDDI’s continued strategic investments in Europe, North America, and Asia.

- SoftBank witnessed a 7.8% YoY increase in enterprise revenue in FY-2023, reaching USD 11.2 billion (JPY 1.5 trillion). This growth was primarily attributed to the expansion of their Business Solutions segment.

- Business solutions revenue experienced a strong 16.8% YoY increase, reaching USD 2 billion (JPY 275.3 billion). This was fueled by a significant rise in recurring revenue streams from cloud, security, and IoT offerings.

- NTT Docomo achieved 5.1% YoY growth in enterprise revenue, reaching USD 13.3 billion (JPY 1.8 trillion) in FY-2023. This growth can be attributed to their amplified focus on Digital Transformation (DX) solutions designed to address specific societal and industrial needs.

- Notably, enterprise revenue accounted for approximately 30.2% of NTT Docomo’s total revenue, with non-connectivity services within the enterprise segment contributing 11.3% and exhibiting an impressive 8.6% YoY growth.

- KDDI reported 12.3% YoY increase in enterprise revenue, reaching ~ USD 7 billion (JPY 990.1 billion). This growth was driven by advancements in their Internet of Things (IoT) and data centre businesses.

Key takeaways

1. Enterprise ICT offerings set to emerge as strategic revenue growth imperative

As the industry matures beyond basic digital adoption, B2B services will emerge as a vital differentiator to sustainable revenue streams. This transition necessitates an ideology shift from connectivity provider to technology solution provider. Telcos can achieve this evolution through internal innovation or strategic partnerships. Strategic acquisitions to bolster offerings can also be not ruled out. Partnerships foster robust ecosystems by integrating diverse service portfolios.

The development of B2B portfolios tailored to enterprise needs is crucial. This includes digitalizing enabler offerings like cloud computing, cybersecurity solutions, data analytics, and AI.

Telcos such as China Mobile and China Telecom exemplify the success of the strategy to gain ground in the enterprise business.

- China Mobile: Continue to focus on integrated development of its DICT (data, information and communications technology) capabilities. The enterprise segment revenue increased 14.2% YoY in FY-2023 to reach USD 27.2 billion (CNY 192.1 billion), with its corporate customer base increasing by ~5.2 million to reach 28.4 million

- China Telecom: Industrial Digitalisation offerings revenue increased by 11.8% YoY to reach USD 19.7 billion (CNY 138.9 billion) and its 5G networks covered more than 2,700 factories. It also continues building up its capabilities for Intelligent Cloud to offer full-stack public cloud and hybrid cloud. Intelligent cloud revenue increased 67.9% YoY in FY-2023 to USD 13.8 billion (CNY 97.2 billion).

Twimbit estimates the enterprise segment’s contribution to telco revenue will reach 29.2% by FY-2027.

2. Telcos to strategically adopt Generative AI to boost growth and efficiency

Telcos have been at the forefront in the adoption of Artificial Intelligence (AI) technologies. This strategic shift, characterized by a move from pilot projects to full-scale deployments, is driven by the potential of AI to unlock growth opportunities and enhance operational efficiency. This trend aligns with a broader movement of companies establishing ambitious visions for an AI-powered future.

Asian telecom operators are at the forefront of this transformation. Leading players such as SK Telecom, China Mobile, China Telecom, and Korea Telecom (KT) actively embrace AI.

- SK Telecom: Its “AI Pyramid” strategy exemplifies this commitment, with 12% of investments towards AI. This investment is expected to triple to 33% by 2028. (to be tripled by 2028) to capture emerging AI opportunities.

- China Mobile: Applying AI to the 10,000 potential parameters associated with each antenna (including coverage attributes and historical traffic volumes) has significantly improved network performance, with a 13% increase in outdoor downlink speeds and a 30% boost in indoor speeds.

- China Telecom: Adopts a broader approach and utilizes AI for various industry applications beyond core network optimization. This includes applications in urban management, emergency monitoring, and smart manufacturing. China Telecom has released Xingchen, an open-sourced 100 billion-parameter large language model (LLM) deployed internally for software development, network analysis, and business applications.

- KT Corp: Its AI initiative ventures in robotics, logistics, and contact centres have already yielded substantial returns (revenue of over USD 600 million). It plans to invest USD 5.4 billion by 2027 to enhance its AI competitiveness.

Across various functions, generative AI offers a compelling value proposition:

- Customer Service: Improved experiences, increased agent productivity, and fully digital interactions

- Marketing & Sales: Hyper-personalized offerings, deeper customer understanding, and faster content creation

- Network Operations: Optimized configurations, enhanced labour efficiency, social media insights for customer understanding, and improved network planning through unstructured data analysis

- Information Technology (IT): Accelerated software development and migration, reduced technical debt, and unlocking previously resource-constrained capabilities

- Support Functions: Streamlined back-office operations and improved employee productivity

While Gen-AI presents exciting possibilities, it remains a nascent technology with challenges. Hence, telcos must be prepared to invest in development and implementation, ensuring responsible and ethical use of this powerful tool.

“Beyond Connectivity” to take centre stage as telcos seek revenue diversification

Telecom operators are unlocking new value streams by strategically expanding to drive growth beyond core connectivity services. Traditionally reliant on connectivity offerings, telcos are increasingly shifting focus towards non-connectivity revenue streams, including financial services, content and media, mobile applications, extended reality (XR) content, and secure remote education solutions.

- AIS: The telco aims to transform into a “Cognitive Tech-Co” by focusing on video platforms, mobile money solutions, and digital marketplaces.

- TrueCorp: Through its subsidiaries, TrueCorp is expanding its enterprise presence by offering professional digital solutions and smart energy services.

For maximized success, telcos require a strategic selection of growth avenues which capitalize on their distinctive advantages and contribute value to the broader ecosystem. Twimbit estimates “Beyond Connectivity” revenue to reach 37.8% of total telco revenue by 2027, underlining the growing importance of this strategic shift.

Research Methodology and Assumptions

- “Enterprise business update for Asia-Pacific telcos 2024” report provides a summarized view of enterprise segment revenue performance of leading telcos in the APAC region for the year 2023.

- This report leverages secondary research methodologies and data provided by telecommunication companies (telcos) themselves. Twimbit employs a calendar year approach (January- December) for all telcos to ensure consistent comparison, regardless of their individual fiscal year ending periods.

- The research examined ~45 telcos across 20 Asia Pacific countries. Selection criteria included economic significance and reliable data availability. Enterprise segment revenue data was available for 26 telcos, whereas non-connectivity revenue was captured for 23 of those.

- For consistent analysis, a constant exchange rate (average for January-December 2023) has been applied when converting local currencies to USD.

- Enterprise segment revenue refers to services provided to business customers (large, medium, and small). It excludes consumer (B2C) revenue. The analysis considers the following sub-segments within the telco enterprise segment:

- Total Enterprise (Connectivity + Non-Connectivity): This includes voice, fixed-line, and data communications (leased lines, IP-VPN, SD-WAN, etc.) offered directly to enterprises. It also encompasses connectivity services like managed services and IoT specifically provided to businesses.

- Enterprise Non-Connectivity: This extends beyond core connectivity services and primarily includes cloud solutions, managed services (collaboration, contact centres, other IT services and applications), IoT, cybersecurity, etc. It excludes any connectivity solutions offered to business customers.

- The primary focus of the analysis was to understand the contribution of the enterprise segment’s performance and revenue to the telcos’ overall revenue. Additionally, a detailed peer comparison was conducted to identify leading telcos and their best practices.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers incase the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The data collected may be subject to reporting inconsistencies inherent to various telcos and hence can be leveraged for reference and guidance purpose. The analysis is based on publicly available information.

For more content on telecoms, click here

Recommended by Twimbit

APAC telcos performance benchmarks – Winter 2024