Key Takeaways

- Telecommunications operators across the Asia-Pacific region are increasingly broadening their service portfolios beyond traditional connectivity, positioning themselves as strategic enablers of enterprise digital transformation. By expanding into advanced ICT solutions, they are strengthening their role as essential partners in supporting their customers’ evolving digital agendas.

- Enterprise revenue for APAC telcos grew by 7.1% YoY, reaching ~USD 121 billion in FY-2024.

- Telecommunications operators are pursuing revenue growth by diversifying beyond traditional connectivity services, positioning themselves as comprehensive providers of enterprise digital solutions.

- The enterprise segment has become a key growth driver, accounting for an average of 22.8% of total revenues across APAC telcos in FY-2024, up from 22% in FY-2023.

- Approximately 38% of APAC telcos reported enterprise revenue contributions exceeding the 22.8% average threshold, led by Spark, MobileOne (M1), and StarHub—underscoring the growing strategic importance of the enterprise business for the region’s operators.

- Conversely, around 77% of telcos achieved YoY growth in overall enterprise revenue during FY-2024, indicating that although the enterprise segment is propelling growth, there remains scope for broader revenue improvement.

- Japan-based telcos – including Rakuten Mobile, KDDI Corp, and SoftBank—ranked among the top five telcos in the region with the highest YoY growth rates in enterprise revenue for FY-2024.

- Enterprise non-connectivity revenue contribution rose by 130 basis points YoY in FY-2024 to reach 14.6%, totalling approximately USD 73.2 billion.

- Nearly 48% of APAC telcos reported non-connectivity revenue contributions surpassing the 14.6% average, reflecting successful diversification efforts beyond traditional services.

- Non-connectivity revenue accounted for 60.5% of total enterprise revenues in FY-2024, exceeding the previous peak of approximately 57.3% recorded in FY-2023.

- The strong momentum in enterprise non-connectivity revenue was primarily driven by telcos based in Japan and China, who continue to deepen their expansion into digital and cloud-based services beyond core network offerings.

Enterprise revenue analysis of APAC telcos: FY-2024

- Enterprise segment contributed 22.8% (overall average) of the total revenue of telcos in FY-2024, marginally higher from 22% in FY-2023

- Enterprise revenue for APAC telcos grew by 7.1% YoY, reaching ~USD 121 billion in FY-2024.

- Telcos are capitalizing on the potential revenue growth opportunity by expanding beyond core connectivity services and unlocking new revenue streams.

- The enterprise segment has emerged as a key growth driver, accounting for a substantial 22.8% of total revenues (average across all telcos) in FY-2024, compared to 22% in FY-2023. This trend highlights the growing significance of the enterprise segment as a future revenue growth avenue for telcos in the APAC region.

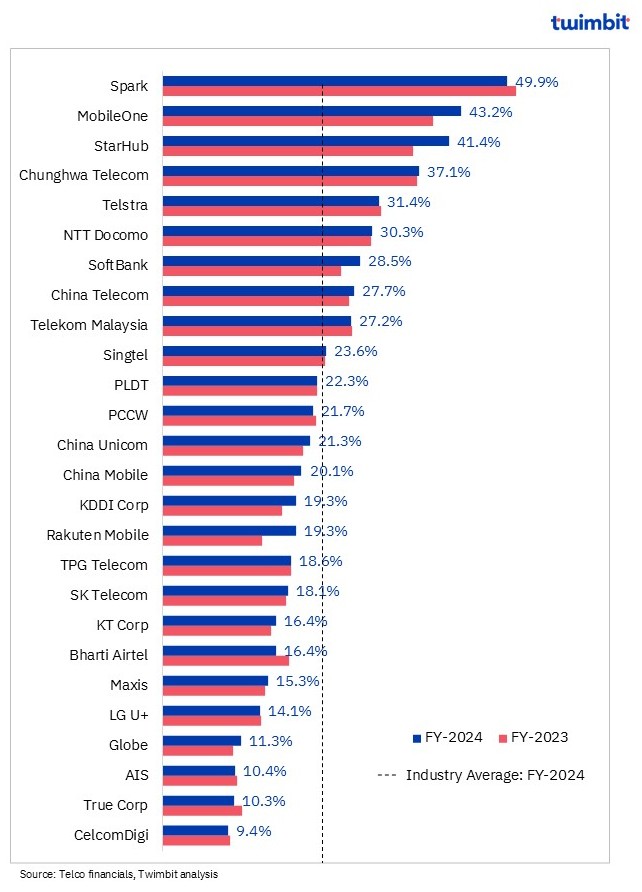

Exhibit 1: Enterprise revenue as a % of total revenue: FY-2024

- Nearly 38% of APAC telcos achieved significant enterprise revenue contributions, surpassing the average threshold of 22.8% the growing importance of enterprise business for telcos in the region.

- Contrastingly, ~77% of telcos witnessed YoY growth in overall enterprise revenue in FY-2024, indicating that while the enterprise segment is driving growth, there is still room for improvement in overall revenue performance.

- Japan-based telcos (Rakuten, KDDI Corp, and SoftBank) ranked among the top five telcos with the highest YoY growth rate in enterprise revenue during FY-2024. This highlights the strong competitive landscape in the Japanese market and the potential for telcos in other regions to emulate their success.

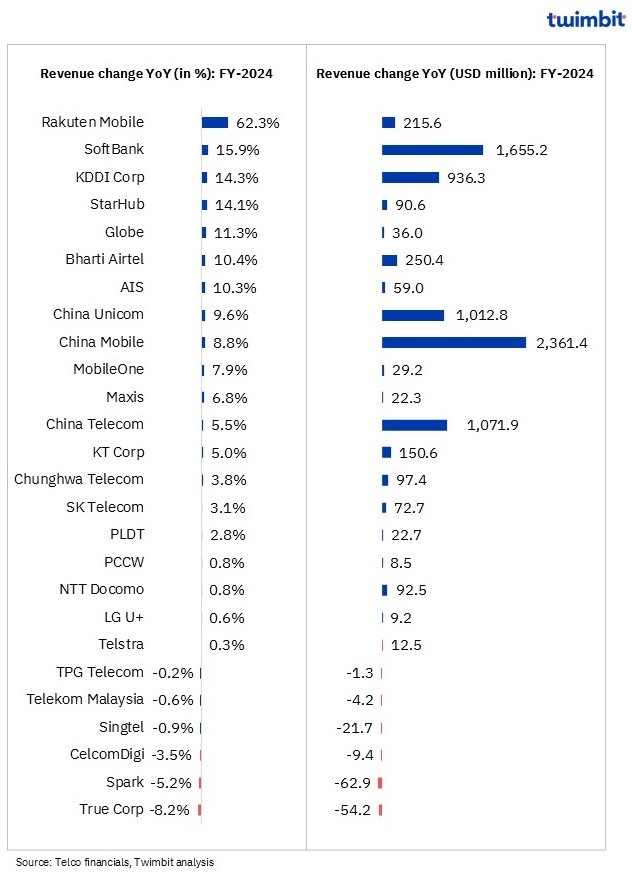

Exhibit 2: Enterprise revenue trends: FY-2024

Enterprise non-connectivity revenue analysis of APAC telcos: FY-2024

- Enterprise non-connectivity revenue contribution increased 130 basis points (bps) on a YoY basis in FY-2024 to reach 14.6%.

- Enterprise non-connectivity segment revenue for APAC telcos grew 13% YoY to reach ~USD 73.2 billion in FY-2024, highlighting the increasing diversification of telco offerings beyond traditional connectivity services.

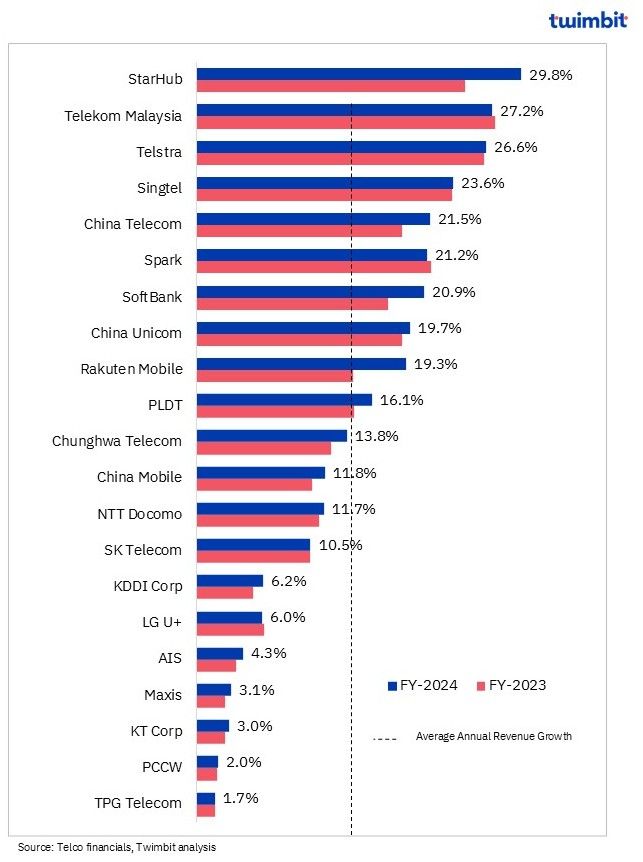

- Nearly 48% of APAC telcos achieved significant non-connectivity revenue contributions, surpassing the average threshold of 14.6%, led by StarHub, Telekom Malaysia, Telstra, Singtel, China Telecom, Spark and SoftBank.

Exhibit 3: Enterprise non-connectivity revenue as a % of total revenue: FY-2024

- Enterprise non-connectivity revenue contribution (for the telcos analysed) reached a significant ~60.5% share of total enterprise revenues in FY-2024, surpassing the previous high of ~57.3% in FY-2023.

- The overall strong growth in the enterprise non-connectivity segment was primarily driven by China-based telcos (China Telecom, China Mobile and China Unicom) and Japan-based telcos (Softbank, KDDI, Rakuten Mobile and NTT Docomo). These telcos intensified their diversification into areas beyond core network offerings, by targeting the enterprises with integrated solutions which included cutting-edge technologies such as AI, cloud computing, and other digitalized services like Big Data, IoT, and Smart cars.

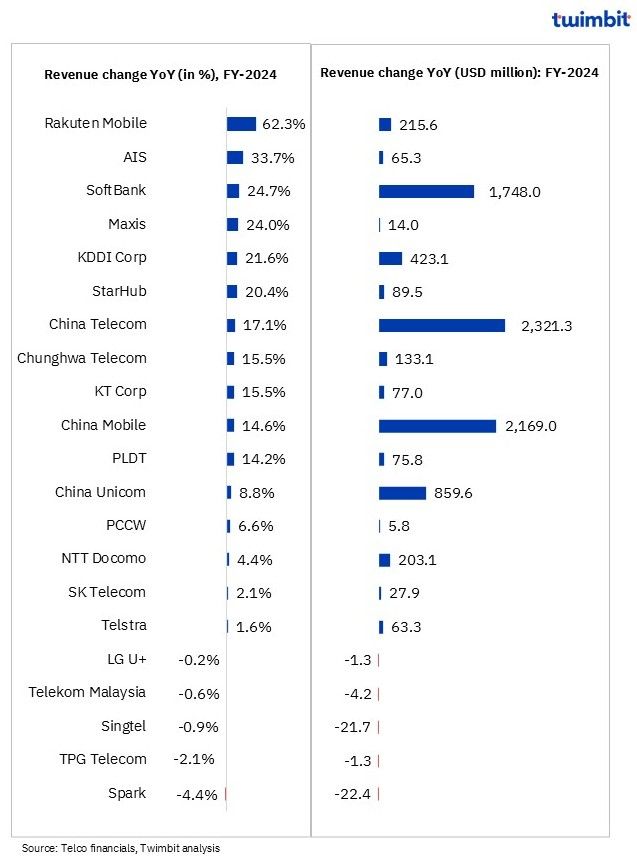

Exhibit 4: Enterprise non-connectivity revenue trends: FY-2024

Enterprise business performance of leading telcos

Spark’s enterprise segment continued to contribute a substantial share of total revenue, accounting for ~49.9% in FY2024. This represents a modest decline from 51.2% in FY2023, primarily reflecting a contraction in overall enterprise revenue.

- Total enterprise revenue decreased 5.2% YoY to ~USD 1.2 billion (NZD 1.9 billion) in FY-2024. The decline was largely driven by reduced demand for IT services, which more than offset gains in data centre and high-tech segments, resulting in an overall reduction in digital services revenue.

- The Enterprise and Government division experienced a downturn in IT services revenue, due to cost containment measures across government and corporate clients, reductions in mobile fleet deployments, shifts in product demand, and intensifying price competition in the mobile segment.

- In contrast, Spark’s data centre and high-tech businesses recorded robust growth, with YoY growth of 29.7% and 23.1%, respectively. The expansion of Spark’s 22MW data centre capacity played a significant role in driving higher billing volumes.

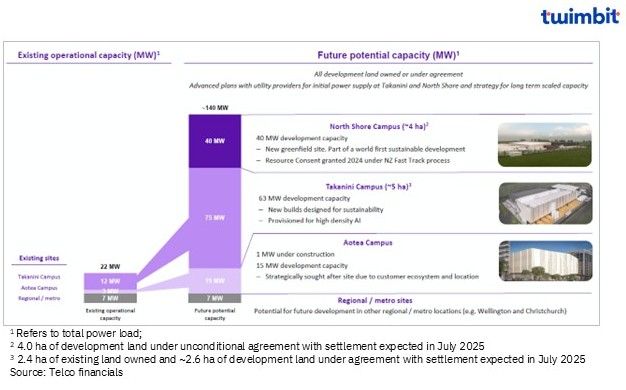

- Spark has identified its data centre strategy as one of four key long-term priorities aimed at creating sustainable shareholder value. The company plans to expand its total data centre capacity to 140MW, with 118MW currently in development across three sites in Auckland, underscoring its commitment to scaling digital infrastructure in New Zealand.

Exhibit 5: Spark data centre capacity and pipeline

Singapore-based telecom operators MobileOne (M1) and StarHub demonstrated strong performance in the enterprise segment in FY-2024. Both companies derived a significant share of their total revenue from enterprise clients, surpassing the market average benchmark of 22.8%.

- MobileOne (M1) recorded a 7.9% YoY increase in enterprise revenue, reaching ~USD 397 million (SGD 531 million) in FY-2024, which accounted for 43.2% of its total revenue. This growth was largely driven by the sustained momentum of its ICT business.

- To strengthen its enterprise segment, M1 has been deploying tailored enterprise solutions aimed at accelerating the adoption and application of 5G technologies. The company is also actively pursuing new revenue opportunities through scalable 5G solutions designed for industrial use cases, both domestically and in international markets.

- M1 continues to expand its enterprise capabilities through its subsidiaries, AsiaPac and Glocomp, in line with its strategic ambition for regional growth. In October 2024, the company acquired a 70% stake in ADG, a leading IT solutions provider in Vietnam, as part of its broader efforts to grow its enterprise footprint across the region.

- In a move to enhance operational efficiency and improve the client experience, M1 completed the migration of all enterprise clients to a new cloud-native digital platform in FY-2024. This transition resulted in cost savings of approximately USD 7.5 million (SGD 10 million). The company plans to fully decommission its legacy technology infrastructure by FY-2025, reinforcing its long-term commitment to becoming a key enterprise solutions provider in the Asia-Pacific region.

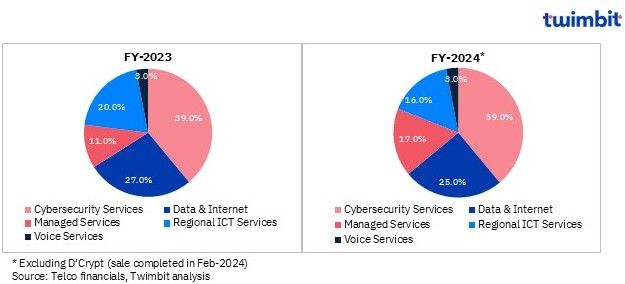

- StarHub’s enterprise segment continued to show solid progress in FY2024, with enterprise revenue rising by 14.1% YoY to reach approximately USD 733.5 million (SGD 980.9 million). This performance resulted in a 520 basis point (bps) increase in the segment’s contribution to total revenue, which reached 41.4% in FY-2024.

- A key driver of this growth was the expansion of non-connectivity services, which include Managed Services, Cybersecurity Services, and Regional ICT Services. Collectively, these offerings recorded a 20.7% YoY increase in FY-2024, underscoring StarHub’s efforts to diversify beyond traditional connectivity.

- Managed Services revenue grew by 16.5% YoY in FY-2024, underpinned by demand for modern digital infrastructure platforms and enterprise-grade solutions. Meanwhile, Cybersecurity Services revenue grew by ~26.2% YoY in FY-2024, supported by a sharp uptick in project completions and a robust order book.

- Regional ICT Services also delivered healthy growth of 13.1% YoY in FY-2024, primarily driven by the successful execution of large-scale projects and continued momentum in securing new contracts, reflecting sustained demand across regional enterprise clients.

Exhibit 6: Enterprise revenue mix of StarHub, FY-2023 and FY-2024

The enterprise segments of China’s leading telecom operators remained resilient in FY-2024, posting steady year-over-year growth. This momentum reflects a deliberate strategic shift toward non-connectivity revenue streams, with the three major operators collectively contributing ~USD 4.5 billion in incremental enterprise revenue during the year.

- China Unicom reported a 9.6% YoY increase in enterprise revenue, reaching USD 11.6 billion (CNY 83 billion) in FY-2024. As a result, the enterprise segment’s share of total revenue rose from 20.3% in FY2023 to 21.3% in FY2024.

- A major contributor to this growth was the Computing and Digital Smart Applications (CDSA) segment, which continued to scale with a focus on quality enhancements. Within this, China Unicom Cloud posted a 17.1% increase in revenue, while revenue from its internet data center (IDC) services rose by 7.4% on YoY basis in FY-2024.

- The company also saw significant progress in its intelligent computing business. This segment, which provides computing power services, recorded newly signed contracts valued at over USD 3.6 billion (RMB 26 billion) in FY-2024, reflecting growing enterprise demand for advanced digital infrastructure.

- China Unicom further strengthened its position in the digital government services space by integrating network, cloud, big data, and intelligent application capabilities. Revenue from intelligence services rose by 26.5% YoY to ~USD 1 billion (CNY 7.1 billion), while data services grew by 20.8% YoY, reaching USD 891 million (CNY 6.4 billion) in FY-2024.

- China Mobile’s enterprise segment reported 8% YoY growth in enterprise revenue in FY-2024. The revenue from enterprise segment reached USD 29.1 billion (CNY 209.1 billion) in FY-2024, resulting in the enterprise segment accounting for 20.1% of China Mobile’s overall revenue, up from 19% in the previous year

- The growth was primarily driven by the Data, Information, and Communications Technology (DICT) segment, which benefitted from an expanding corporate client base. China Mobile added ~4.2 million new enterprise customers during the year, bringing the total to around 32.59 million. The company also improved its competitive position in public tenders, increasing its contract win rate from 14.3% in FY-2023 to 16.4% in FY-2024.

- China Mobile secured over 700 large-scale 5G DICT projects—each valued at over USD 1.4 billion (CNY 10 billion)—reflecting strong demand for integrated enterprise connectivity solutions. In parallel, the company launched 24 AI-powered products and 39 AI+DICT applications, advancing its transition toward intelligent service offerings. These efforts contributed to a 5% YoY increase in dedicated 5G network revenue, which reached ~USD 1.2 billion (CNY 8.7 billion) in FY-2024.

- Mobile Cloud continued to serve as a key revenue enabler, with revenue rising by 20.4% YoY to ~USD 14 billion (CNY 100.4 billion) in FY-2024, reinforcing China Mobile’s role in cloud-based enterprise services.

- In the Internet of Vehicles (IoV) domain, China Mobile installed 14.43 million factory-connected IoT units in FY-2024, bringing the total number of IoV connections to 65.06 million. The company also formed strategic partnerships with 25 leading automotive manufacturers, further consolidating its position in the evolving “vehicle-road-cloud” ecosystem.

- China Telecom’s enterprise segment continued to expand in FY-2024, with revenue growing by 5.5% YoY to approximately USD 20.4 billion (CNY 146.6 billion). This growth raised the enterprise segment’s contribution to total revenue by 70 basis points, reaching 27.7% for FY-2024

- A major driver of this performance was China Telecom Cloud, which saw a 17.1% YoY increase in revenue, reaching USD 15.9 billion (CNY 113.9 billion) in FY-2024. The number of China Telecom Cloud business (2B) customers also rose by 8% to 4.9 million, reflecting broadening enterprise adoption of its cloud services.

- The cloud segment remains a central pillar of China Telecom’s broader strategy to accelerate digital transformation. The company has deepened the implementation of its “Cloudification and Digital Transformation” initiative, with continued investments in enhancing the intelligence, efficiency, and sustainability of its digital infrastructure. China Telecom’s cloud 2B customer base grew by 8% YoY, reaching 4.9 million, underscoring the sustained demand for enterprise cloud solutions.

- Additional enterprise growth came from Internet Data Center (IDC) services and security offerings. IDC revenue increased by 7.3% YoY to USD 4.6 billion (CNY 33 billion), while security services grew by 17.2% to USD 2.3 billion (CNY 16.2 billion) in FY-2024

- The telco has intensified its focus on artificial intelligence applications, serving over 10,000 scenario-specific enterprise clients. This includes more than 8,700 software-as-a-service (SaaS)-based industrial clients and involvement in over 1,600 AI + DICT projects supporting industry digitalization.

Exhibit 7: China Telecom’s “Cloud-intelligent Integrated” Computing capability

Japanese telecom operators reported YoY growth in enterprise revenue during FY-2024, with the combined enterprise income of Rakuten, KDDI, SoftBank, and NTT Docomo rising by ~USD 3.4 billion YoY in FY-2024.

- SoftBank’s enterprise revenue grew by 15.9% YoY to reach ~USD 12.1 billion (JPY 1.8 trillion). This growth was primarily driven by the expansion of its Business Solutions segment, which saw a substantial 49.4% YoY increase in revenue, reaching USD 2.7 billion (JPY 411.2 billion).

- The segment’s performance was bolstered by growing demand for digital transformation solutions, alongside the full acquisition of WeWork Japan GK and the purchase of UK-based AI chipmaker Graphcore. These strategic moves reflect SoftBank’s broader push to deepen its enterprise capabilities and technology portfolio in high-growth areas.

- The increase in enterprise revenue was also supported by higher contributions from cloud services, security solutions, and IoT offerings—reflecting growing demand from enterprise clients for digital transformation initiatives. Additionally, the consolidation of Cubic Telecom further contributed to the segment’s overall revenue expansion.

- NTT Docomo recorded modest growth (0.8% YoY) in its enterprise segment, with revenue reaching ~USD 12.4 billion (JPY 1.9 trillion) in FY-2024.

- This incremental growth reflects the company’s sustained focus on digital transformation (DX) solutions tailored to specific industry and societal challenges. Notable contributors included contact center solutions, as well as Secure Access Service Edge (SASE) and managed security services—areas that continue to see rising enterprise demand amid ongoing digitalization efforts in Japan.

- In contrast, Rakuten Mobile, the smallest among the major Japanese telecom operators by revenue, posted the highest YoY growth in enterprise revenue across the APAC region in FY-2024. The segment revenue reached ~USD 561.7 million (JPY 85 billion) in FY-2024, representing a remarkable 62.3% increase from the previous year.

- This performance was underpinned by Rakuten Symphony’s efforts to streamline its operational structure while continuing to execute on international projects. In early 2025, it opened two Radio Access Network (RAN) Proof-of-Concept (PoC) centers in collaboration with Kyivstar (Ukraine) and Telkom Kenya (Kenya), underscoring its ambition to position itself as a global leader in cloud-native network software.

- The telco expanded its portfolio with the launch of “Rakuten AI for Business,” a generative AI service for corporate clients. Priced at USD 6.6 (JPY 1,100) per license per month (inclusive of tax), the solution will be bundled with Rakuten Mobile’s corporate offerings as part of its strategy to explore new enterprise revenue streams in artificial intelligence.

- KDDI enterprise revenue grew 14.3% YoY in FY-2024, reaching ~USD 7.5 billion (JPY 1.1 trillion). The growth was primarily driven by expansion across several strategic domains, including IoT-related services, data centers, digital business process outsourcing (BPO), and adjacent areas.

- KDDI’s total IoT connections rose sharply by 22.2% YoY, reaching 48.5 million in FY-2024. This increase was bolstered by the integration of Soracom, a recently acquired IoT platform provider. As a result, revenue from IoT- related services grew to ~ USD 1.1 billion (JPY 173 billion) in FY-2024, reinforcing KDDI’s leadership in connected services.

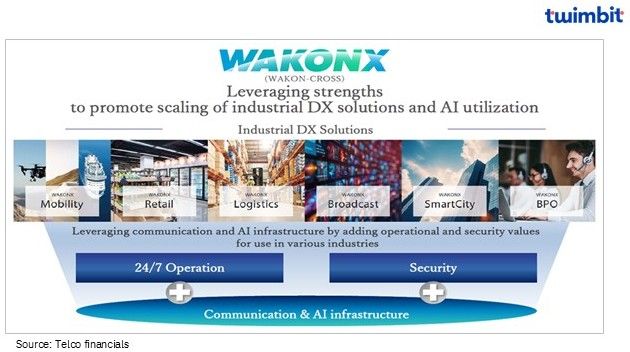

- In May 2024, KDDI introduced “WAKONX,” a new digital business platform under its enterprise brand, KDDI BUSINESS. Built on large-scale computing infrastructure, the platform enables the design and deployment of AI-enhanced mobile and fixed networks tailored to specific industry needs.

- In November 2024, KDDI reached an agreement to acquire full ownership of cybersecurity firm LAC. It intends to integrate LAC’s security services with its own network offerings to provide comprehensive cybersecurity solutions—from consulting to monitoring and operations—as a unified service.

Exhibit 8: KDDI’s WAKONX platform for digital transformation

Among the telecommunications operators that reported a YoY decline in enterprise revenue during FY2024 were True Corporation, Spark, CelcomDigi, and Singtel.

- True Corporation’s enterprise revenue contribution to overall revenue declined to 10.3% in FY-2024, compared to 11.4% in FY-2023. This decrease was primarily driven by a 58.3% reduction in interconnection revenue, resulting from the implementation of lower interconnection rates beginning in the first quarter of 2024, as well as the absence of a one-time litigation settlement gain of approximately USD 329 million (THB 1.2 billion) that had positively impacted results in the prior year.

- CelcomDigi also experienced a marginal decline in enterprise revenue contribution, falling from 9.8% in FY-2023 to 9.4% in FY-2024. This decline was largely attributable to a 6.1% YoY decrease in revenue from the fixed segment.

- Meanwhile, Singtel reported a 0.9% YoY decrease in enterprise revenue for FY-2024. The decline was primarily influenced by the performance of its cybersecurity subsidiary, Trustwave, following restructuring activities undertaken in Oct-2023.

Research Methodology and Assumptions

- The report “APAC Telcos Enterprise Business Update 2025” report presents a summarized view of the enterprise segment revenue performance of selected telcos in the APAC region for the period January – December 2024.

- The report has been prepared based on publicly available data and information disclosed by telcos, supplemented by extensive secondary research. A calendar year basis (1 January – 31 December) has been uniformly applied for analytical consistency, irrespective of their respective statutory fiscal year periods.

- The research scope includes approximately 48 telcos across 20 countries within the APAC region. Enterprise segment revenue data was available for 26 telcos, while non-connectivity enterprise revenue data was available for 21 of them.

- For purpose of consistent currency translation, a constant exchange rate based on the average for the period from 1 January to 30 June 2024 has been applied for conversion into United States Dollars (USD).

- The enterprise segment revenue considered in this report pertains exclusively to services rendered to business customers, including large enterprises, SMEs, and other commercial entities. This excludes revenue derived from consumer (B2C) operations. The enterprise segment has been further disaggregated into the following sub-categories:

- Total Enterprise Revenue (Connectivity + Non-Connectivity): Comprising services such as fixed-line voice, leased lines, IP-VPN, SD-WAN, and managed connectivity solutions, including IoT offerings tailored for enterprise use.

- Enterprise Non-Connectivity Revenue: Encompassing cloud services, managed IT solutions (e.g., collaboration tools, contact centre services), cybersecurity, IoT platforms, and other non-connectivity-based solutions targeted at enterprise customers. This excludes core network connectivity offerings.

- The data provided in the report are as reported by the respective telcos or on a calculated basis wherever feasible. These may or may not align with the exact numbers incase the respective telcos have either not disclosed or provided any reference for the above segments (or further sub-segment details).

- The principal objective of the analysis is to assess the contribution of enterprise revenue to total telco revenues and to benchmark peer performance across the region. The report further includes comparative insights into best practices among leading telcos.

Click here for more contents on telecom

APAC telcos performance benchmarks- Winter 2025