We expect the global RAN market to grow at a healthy rate over the following years as operators race to launch commercial 5G. The transformation to an open and disaggregated architecture is underway, as it reduces the time to market. This note talks about the outlook for Open RAN, growth drivers and challenges for telcos as they adopt the same.

For the purpose of sizing the market opportunity, this research defines open RAN as an evolving network architecture that has:

- The ability to disaggregate baseband leading to split architecture as a pre-requisite, with the baseband decomposed into separable decentralised and centralised units.

- The disaggregation should allow the interoperability of equipment from diverse vendors or ecosystems, achieved through an open fronthaul interface.

- Disaggregated components may be deployable in virtual or cloud environments.

Open RAN based solutions are gradually maturing to the point where they may be considered a mainstream option. As a result, key technology vendors are not only including or aiming to include open RAN solutions in their portfolios, but significant telcos have begun to deploy these solutions in their operational networks.

1. Open RAN deployments gaining traction with large group operators worldwide

North America

- Dish: Partnered Fujitsu, Mavenir, and Altiostar to deploy 100% open RAN-compliant 5G SA network by 2023

- Verizon: Deploy mmWave and mid-band 5G with open RAN-compliant equipment supplied by Samsung, Nokia, and Ericsson

- AT&T: Gradually adding open RAN-compliant equipment into their existing network from 2021

Europe

- Vodafone UK: Committed 2,500 sites to open RAN deployment, aims to extend 4G and 5G coverage to rural places in the UK

- Deutsche Telekom: Launched multi-vendor Open RAN 4G and 5G network in Germany; further expansion will take place across 2021-2022

- Telefonica O2: Completed open RAN trials with new vendors – Altiostar, Supermicro, and GigaTera Communications

Japan

- Rakuten: Deployed around 22,500 4G Open RAN sites to reach 88.6% population coverage with its 4G infrastructure

- KDDI: Partnered with Fujitsu to adopt Open RAN-compatible 5G radio unit for the construction of a virtualised 5G base station

Emerging Asia

- Axiata: Conducted open RAN (2G & 3G) field pilots at selected sites in Malaysia, Indonesia, and Sri Lanka; partnerships with Mavenir, Parallel Wireless, and Infosys as its systems integrators

MENA

- MTN: Partnered with Voyage, Tech Mahindra, Altiostar, Mavenir, and Parallel Wireless to accelerate 4G and 5G service coverage via open RAN

LATAM

- Internet para Todos Peru: Aims to provide 4G mobile internet connectivity to users in remote regions of Peru, it deployed hundreds of new sites using Parallel Wireless fully virtualised and automated Open RAN architecture

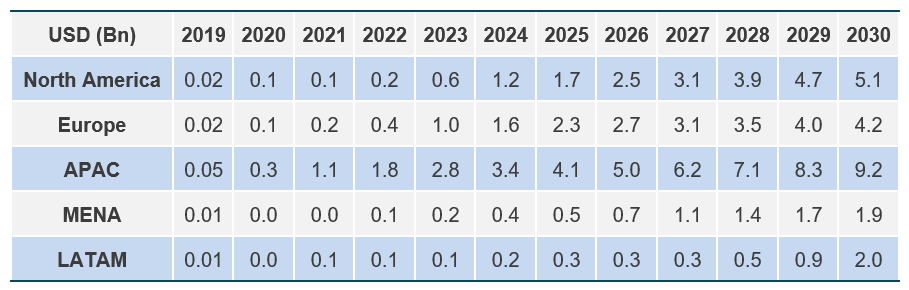

2. Open RAN opportunity for telco public networks reaches USD 22.3 billion by 2030

The global Open RAN opportunity arising due to disaggregation and the virtualisation of telco public networks is from:

- Regional prominent operators’ investment in Open RAN for near-term investment (within 3-4 years) and comments from key decision-makers in leading MNOs on their long-term commitment to Open RAN (as mentioned above)

- The global RAN market revenue is estimated based on forecasted shipment units and the average pricing per unit for small cells and macro cells combined:

- RAN market is further broken down into 3G, 4G and 5G

- RAN market is split into five regions (North America, Europe, APAC, MENA, and LATAM)

twimbit estimates the Open RAN market to reach USD22.3 billion by 2030

- Early adopters and deployment trials drive the inception growth of the Open RAN market.

- twimbit forecasts the penetration rate for Open RAN to grow up to 3X from 2023 – 2027; the momentum will continue towards to end of the decade when Open Ran will dominate more than half of the total RAN market

- Real-world deployment by early adopters is a vital proof-of-concept example that boosts up confidence for other operators to pursue an open RAN framework

- Innovation features such as the RAN Intelligent controller (“RIC”) will spur the Open RAN adoption; The telco industry is urging for innovative elements that will help operators to revitalise their legacy revenue model

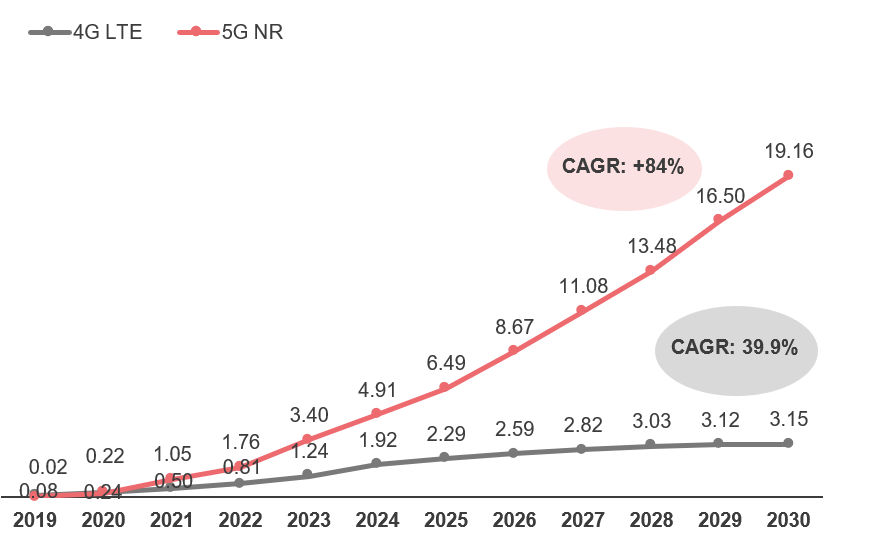

3. 5G to drive open RAN investments, accounting for 86% of total opportunity

4G LTE

- Despite major MNOs gradually decreasing their CAPEX on 4G, twimbit expects that open RAN for 4G will see an opposite trend

- One of the key drivers is that operators are leveraging open RAN to expand its 4G coverage in difficult-to-reach areas where the lower CAPEX will be more economically viable to deploy

- Besides, there are also operators in emerging economies that overhaul existing 4G infrastructure with an open RAN framework, paving for the future the Open RAN migration roadmap

5G NR

- The open RAN technology is set to grow together with the 5G network; the inception phase is fueled with greenfield operators and leading MNOs that initiate selective deployments and trial programmes

- With technology maturity comes rising confidence, the Open RAN market for 5G will see trajectory growth starting from 2024

4. Asia Pacific will continue to lead operator investments in open RAN

- APAC started higher in the Open RAN market compared to North America from 2020 to 2021. Japanese operators primarily drive this, including Rakuten, KKDI, Softbank and NTT DoCoMo.

- APAC did not show significant growth as the Chinese RAN vendors remain antagonistic towards Open RAN. Therefore, it is unlikely to see wide adoption amongst Chinese operators in the near term.

- Part of the EU and UK governments have imposed new regulations on operators to remove Huawei equipment from their 5G networks. This causes a majority of operators in western Europe to explore Open RAN as a new deployment approach.

- From 2026, Open RAN will see more significant growth across all regions. Technology maturity and trials validation will accelerate the migration from legacy RAN to open interface.

5. Government incentives has been a catalyst for building open RAN momentum

- Government incentivisation

- US: Injected US$ 750 million in funding over 10 years to accelerate the development of Open RAN solutions

- UK: Multiple grants released through OFCOM for open RAN lab, R&D, trials and deployment incentives

- India: The Indian government has encouraged local vendors to develop local telecom equipment supply chains under its “Make in India” incentives

- Other governments that implement incentives and facilities for open RAN development include Germany, Taiwan, and Japan

- Low-cost rural deployment

- Bridging the digital divide by extending network coverage in rural areas is much easier for operators with the lower deployment cost of Open RAN

- Brownfield operators are likely to deploy and test commercial Open RAN in rural areas before migrating to urban areas, allowing operators to evaluate the quality of multiple vendors better and learn how to manage the disaggregated structure

6. Lower CAPEX is a key attraction for greenfield operators

The new entrants to the telco industry will most likely adopt open RAN deployment as the lower CAPEX allows them to scale up faster, grabbing the target market share at better profit margins .

CAPEX for operators in 2020:

- Dish Network (US) – USD 413.7 million

- Rakuten – JPY 262.80 billion (USD 2.3 billion) in 2020

7. Diversity in the supplier ecosystem benefits operators

- Disaggregated and virtualised networks

- Split or distributed architecture is a pre-requisite for 5G networks

- Open RAN will benefit from the fast virtualisation of RAN

- TCO optimisation and vendor flexibility

- Use of general-purpose hardware and commoditisation of radio units

- Vendor diversity to break market monopolies

- Shifting political landscape

- Governments introduced 5G supply chain diversification support programs

8. In near term, concerns over integration and performance impact open RAN adoption

- Complex integration and interoperability challenges

- The combination of a broad range of solutions from multiple vendors increases the likelihood of incompatibilities and the complexity of system integration.

- Performance and feature parity

- Conversely to traditional vendors’ solutions, the new players’ solutions in the market have yet to be proven, and their performance claims have yet been experienced by operators globally.

- Legacy and backward compatibility

- Most open RAN solutions today focus on 4G and 5G technology. Parallel Wireless is one prominent vendor to offer a common stack for 2G, 3G, 4G, and 5G open RAN solutions. There is limited participation from vendors in addressing challenges arising from integrating open RAN solutions to existing legacy networks.

- Secure, consistent network performance

- When compared to traditional architectures deployed massively across highly densified and demanding networks, a major concern is the technology maturity of Open RAN solutions. It is critical to provide feature parity, constant network performance, and high quality of experience.

- Maintenance capabilities

- The growing number of vendors at a single site can make maintenance and network operations more complex in the initial stages.