Open finance has evolved far beyond its regulatory roots to become a cornerstone of global financial innovation. As of 2025, the ecosystem spans banking, insurance, pensions, and cross-sector embedded finance, driven by rapid advances in API standardization, AI integration, and regulatory harmonization. Over 132 million active users now benefit from open finance globally, with transaction volumes in open banking payments exceeding 330 billion annually. Brazil’s Open Finance initiative alone processes over 96 billion API calls monthly.

- Key developments include:

- The rise of variable recurring payments (VRPs), reducing reliance on card networks

- AI-powered hyper-personalization

- Expansion into smart data ecosystems (energy, healthcare, mobility)

- Security investment surpassing USD 2.1 billion annually to protect APIs

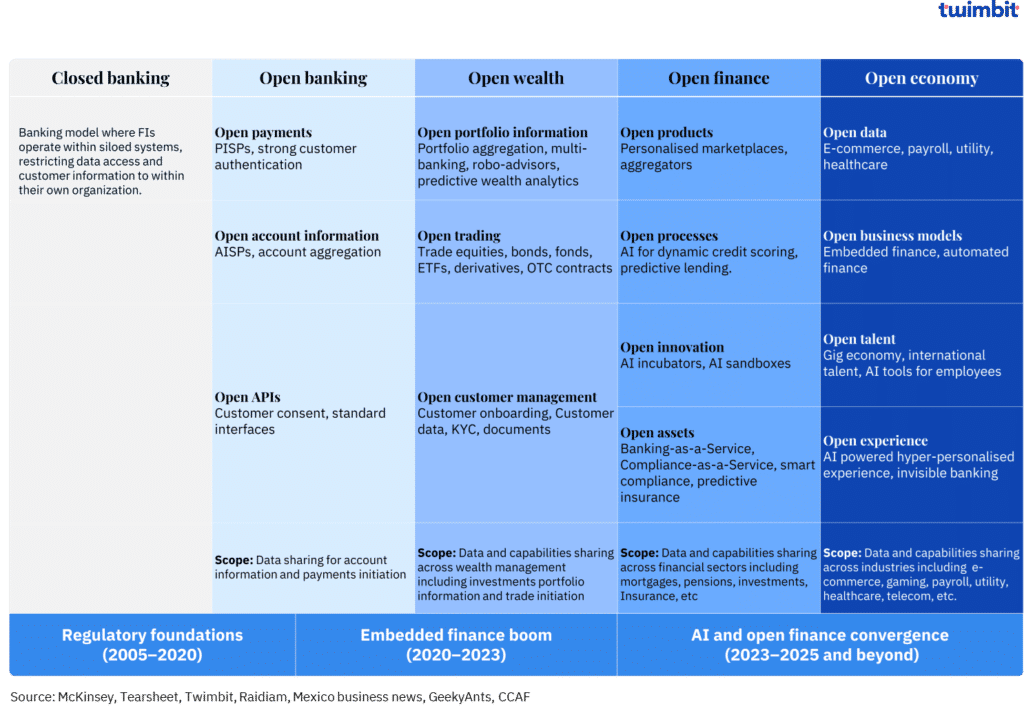

Open finance today

Generative AI now powers 70% of fraud detection systems in open finance, while large language models (LLMs) enable natural language financial assistants. Brazil’s ecosystem demonstrates scale: 40 million customers actively share data across 940 institutions. The EU’s Financial Data Access (FIDA) framework extends open finance to pensions and ESG data, creating unified financial identities.

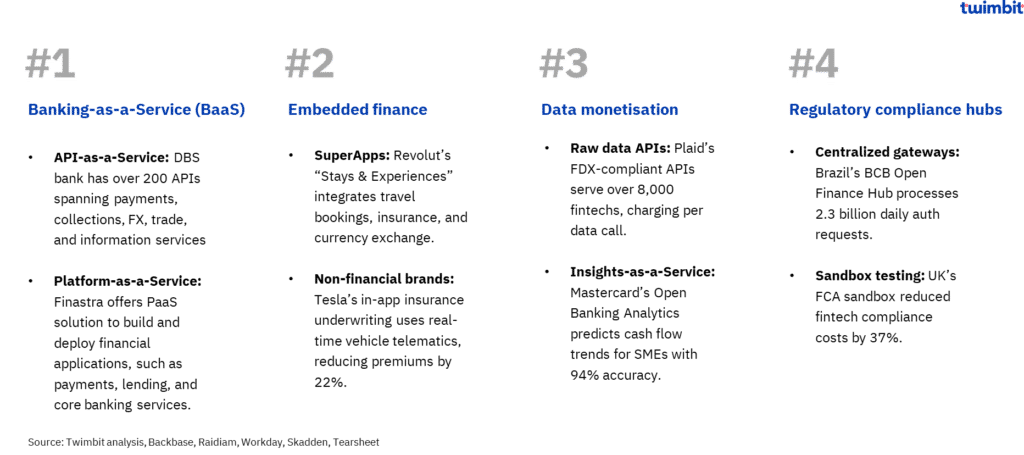

Open finance outcomes turned business models

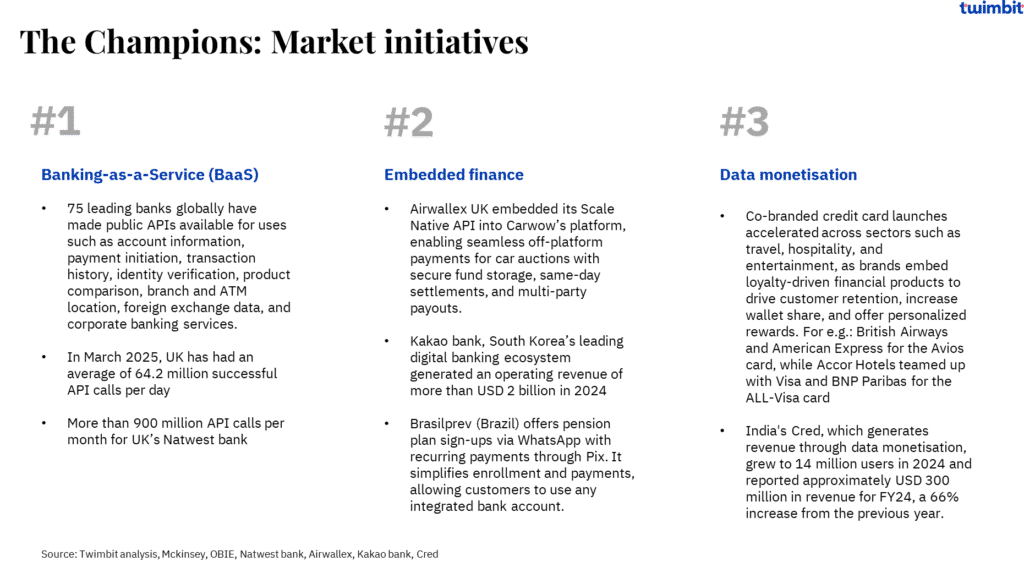

Open finance outcomes have transformed into innovative business models by enabling banks and fintechs to offer API-as-a-Service and Platform-as-a-Service, supporting the rapid deployment of diverse financial applications. The rise of embedded finance allows seamless integration of financial products into both financial and non-financial platforms, enhancing customer experiences and engagement. Additionally, data monetisation and regulatory compliance hubs are unlocking new revenue streams and streamlining compliance, driving efficiency and value across the financial ecosystem.

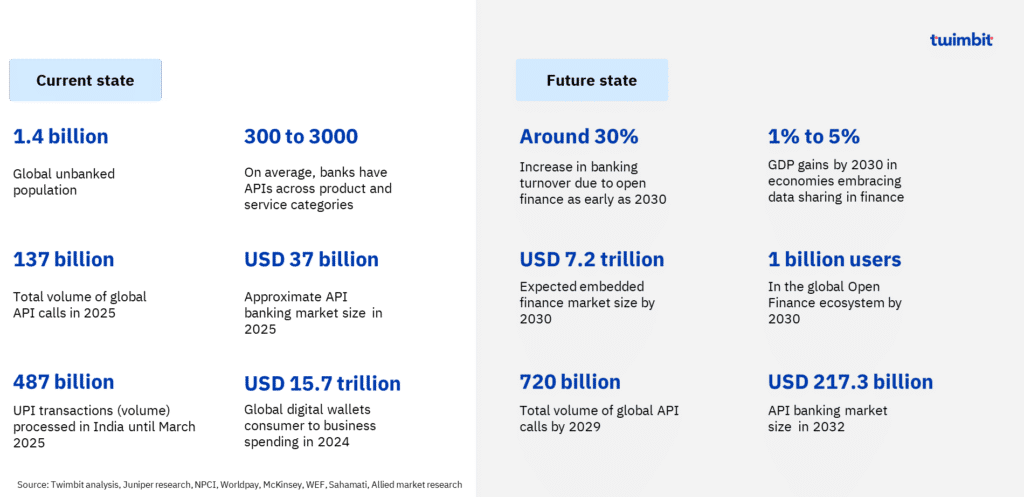

Growth opportunities for open finance

Open finance is unlocking vast growth opportunities by enabling broader access to financial services and fostering innovation across the ecosystem. As more institutions adopt open data sharing and embedded finance models, the reach and impact of financial products continue to expand globally. This transformation is driving greater inclusion, efficiency, and value creation for both consumers and businesses.

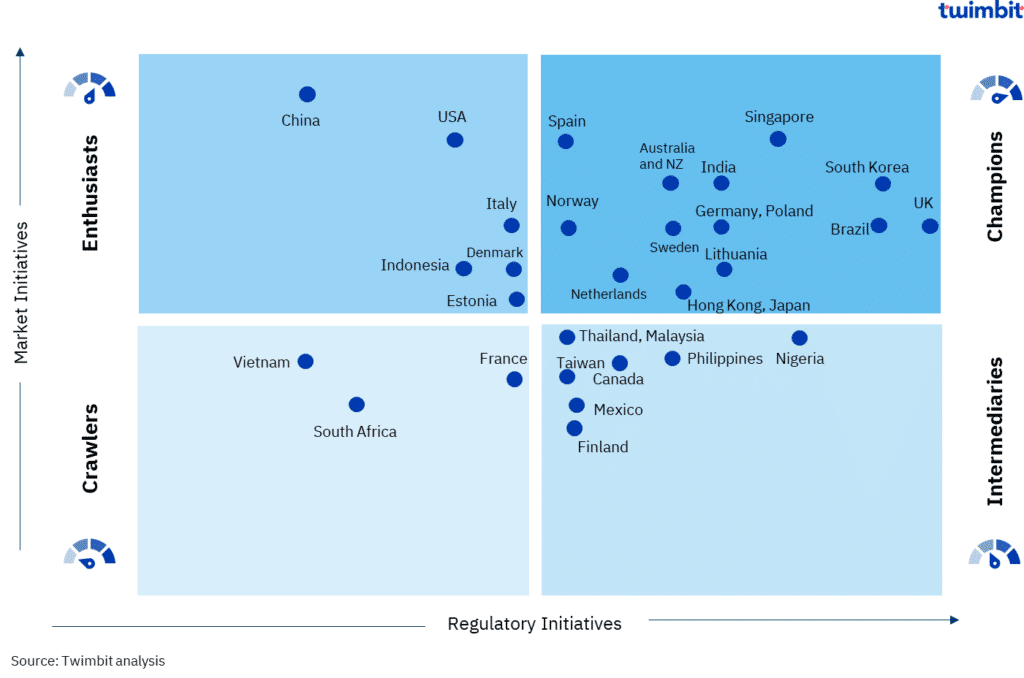

Twimbit’s Global Open Finance Maturity Index

We evaluated 32 countries that are disrupting the market with open finance systems. These countries are developing customer first solutions and making banking invisible by embedding financial and non-financial services from adjacent third-party ecosystems.

The Index maps the relative position of the leading countries across two main criteria:

Regulatory initiatives: We evaluated countries based on their government and regulatory body led policies, guidelines, and laws that govern and promote open finance activities. We considered the following five parameters in our evaluation:

- Open finance regulatory policy

- Governance framework

- Regulator defined use cases

- Open finance regulatory sandbox

- Data sharing compliance framework

Market initiatives: The factors that we looked for evaluation included innovations, integrations, AI readiness and monetization actions taken by major banks, neobanks, and fintechs in each country:

- BaaS

- API network (platforms, portals, number of APIs, delivery maturity)

- API products and service portfolios

- Reduced cost to serve

- Embedded finance

- Portfolio of marketplaces

- Revenue growth through marketplaces

- External partnerships with third parties, fintechs, and technology partners

- Data monetization

- Adopt new revenue models with the provision of data as a service

- Provide insights based on raw data to merchants and other partners

- Deliver improved outcomes by leveraging data

- AI Readiness

- Existence/nuance of national guidelines on ethical LLM/AI usage

- Use cases like fraud detection via ML powered APIs

- % FIs deploying AI tools

Based on our research, we have placed each country’s open finance maturity in four categories:

- Champions: These countries have exemplary ratings in regulatory initiatives and market maturity

- Enthusiasts: For these countries, market maturity is high and regulatory initiatives are still at a nascent stage

- Intermediaries: The countries in this category are mid paced in terms of both regulatory initiatives and market maturity

- Crawlers: These are the countries where we found that entry level regulatory initiatives and market maturity are yet to be achieved

What changed from 2023 to 2025?

The open finance landscape has rapidly evolved since our 2023 report, reflecting a period of accelerated innovation and regulatory progress. Countries worldwide have embraced new technologies, enhanced data-sharing practices, and a greater focus on AI integration. This momentum has paved the way for increased collaboration, maturity, and impactful transformation across global open finance ecosystems.

- Most countries have advanced due to proactive market initiatives and AI readiness.

- Thailand, Canada, the Philippines, and Taiwan have progressed from crawlers to intermediaries, driven by the introduction of new regulations.

- In October 2024, the Bank of Thailand (BOT) launched ‘Your Data,’ a data-sharing initiative aimed at individuals and small and medium-sized enterprises(SMEs).

- In December 2024, the Financial Consumer Agency of Canada (FCAC) announced the Consumer-Driven Banking Framework to advance open finance in the country.

- The EU published PSD3 to address existing challenges in PSD2.The update expands coverage to include broader financial data—such as savings and mortgages—and introduces stricter API performance and fraud liability standards for banks and third-party providers.

- In the U.S., the CFPB’s final rule under Section 1033 took effect on January 17, 2025, mandating consumer access to financial data for themselves and authorized third parties.

- European countries follow the AI Act for comprehensive AI regulation, while the UK has proposed its own AI framework bill. Canada introduced the Artificial Intelligence and Data Act (AIDA) to regulate AI use nationally.

- Although China does not have formal AI regulations, the government is actively promoting the adoption of AI across all industries, and many companies have already integrated it into their operations.

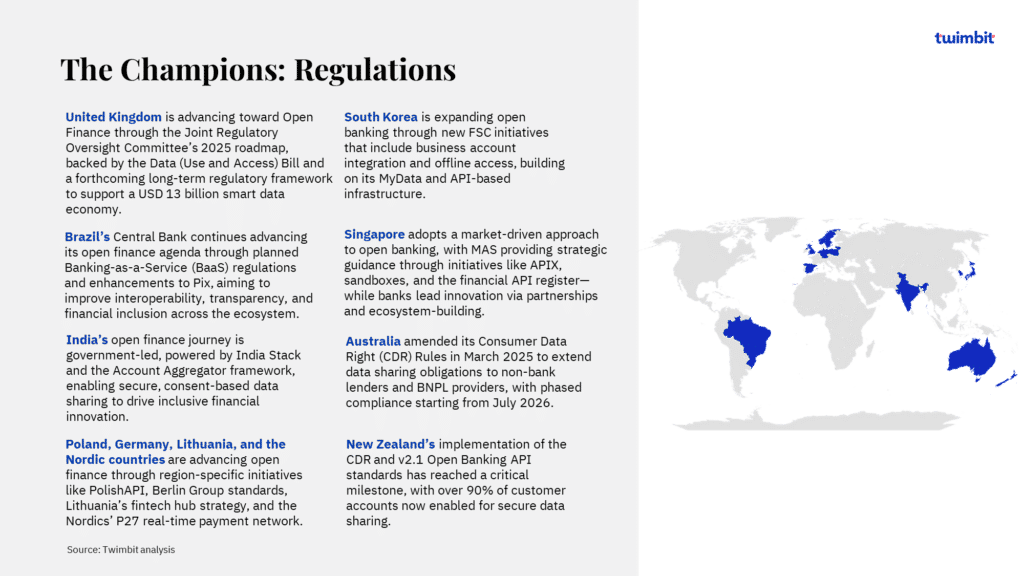

Deep dive into “Champions“

We observed that almost 50% of the countries that we evaluated came out to be champions in terms of both regulatory and market initiatives.

Open finance tomorrow

The next phase is open data ecosystems, where banks, fintechs, and third-party providers deliver AI-powered, hyper-personalized services across industries. Customers will benefit from unified access to financial and adjacent services through the app of their choice, powered by secure, consent-driven data sharing and real-time insights.

To achieve this, here are 10 critical enablers for open finance success:

- Standardize open data and interoperability protocols

- Adopt API-centric integration models

- Leverage microservices for agility and scalability

- Embed security and consent by design

- Modernize IT through Agile and DevSecOps

- Use enterprise AI for personalization and risk intelligence

- Adopt multicloud for resilience and portability

- Enable cross-industry data monetization

- Institutionalize ecosystem governance

- Establish continuous feedback and policy loops

Know more about open finance solutions by F5 here: F5 Global state of open finance 2025