Executive summary

Global telecom operators delivered measured growth in Q2-2025, with revenues expanding by 3.5% YoY to USD 339.1 bn and EBITDA margins holding steady at 36.1%. Beneath this stability, however, the industry’s performance reflects sharp divergence across markets.

Mature markets are grappling with structural headwinds. Telcos like Telefonica, BT, and Singtel reported revenue declines as regulatory limits, foreign exchange (FX) volatility, and consumption shifts weighed on topline momentum. Even where EBITDA held steady, profitability remained defensive, underlining the limits of traditional connectivity models.

Capital allocation is tilting toward AI and fibre. Select operators like SK Telecom, Zain, and Etisalat, lifted capex sharply, repositioning networks as AI-ready platforms for cloud and enterprise services. Meanwhile, incumbents such as AT&T, Deutsche Telekom, and Telstra placed fibre at the centre of long-term strategies, anchoring convergence across broadband, enterprise, and 5G backhaul.

ARPU growth is bifurcated. Tariff discipline and postpaid migration lifted ARPU at Jio, Airtel, and America Movil, while saturation dragged down Rogers, Softbank, and Singtel. Stability at SK Telecom and China Telecom highlighted defensive strength, yet the broader trend shows pricing power remains uneven across markets.

Frontier innovations are reshaping competitive advantage. Satellite-enabled direct-to-device connectivity, Edge AI deployment, and quantum-based network optimization are no longer futuristic bets, they are early markers of how telcos are redefining geography, agility, and efficiency in their networks.

The Q2-2025 results highlight the telecom industry’s decisive shift beyond traditional connectivity, emphasizing the importance of scale, capital discipline, and frontier innovations as key differentiators. Operators that integrate robust ecosystems with next-gen AI infrastructure are outpacing their peers, whereas those in saturated, regulation-heavy markets face stagnation without bold strategic pivots.

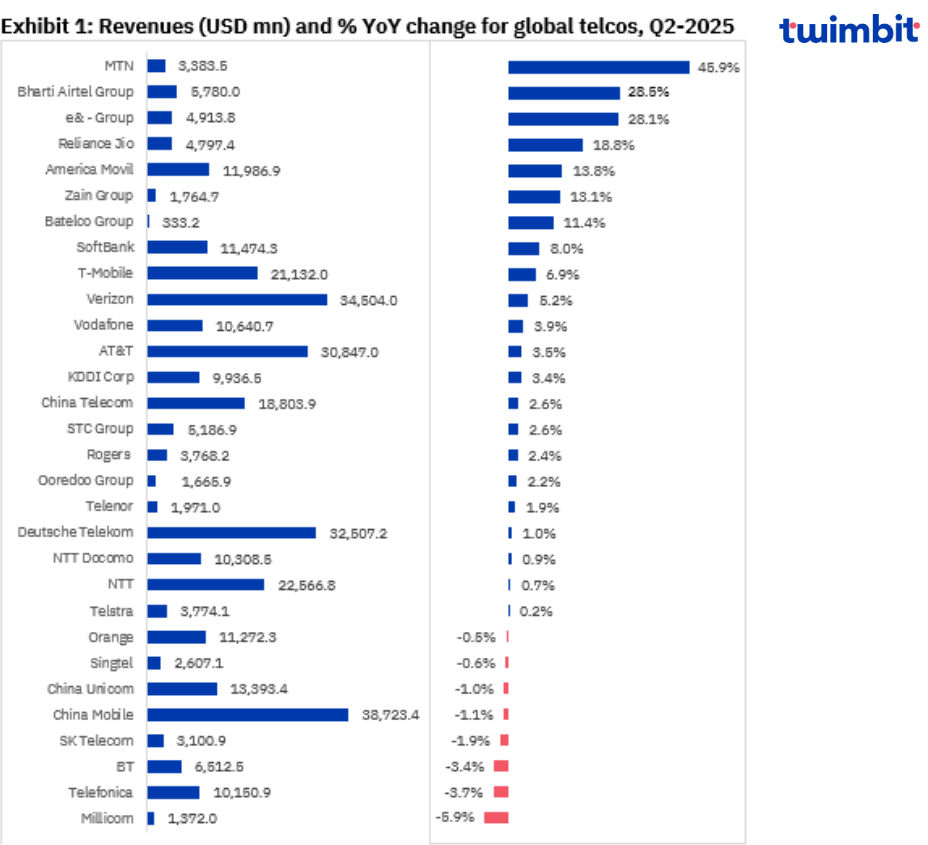

Revenue analysis of global telcos: Q2-2025

Average revenue growth for global telcos in Q2-2025 is 3.5% on a YoY basis.

The 30 telcos achieved a combined revenue of USD 339.1 bn (YoY net new revenues of USD 11.5 bn) in Q2-2025. Only 8 of the 30 telcos analysed had a declining YoY quarterly revenue.

- Scale players reap the benefits of market momentum and diversification: Large-scale operators are leveraging subscriber growth, diversified service portfolios, and ecosystem expansion to deliver robust revenue gains. Their ability to monetize scale differentiates them from regional peers.

Reliance Jio: Revenue surged 18.8% YoY to USD 4,797.4 mn, powered by mobility, home broadband, and digital services. Strong adoption of 5G services and the home broadband offerings continues with accelerated addition in subscribers and in the number of home-connects.

Bharti Airtel Group: Revenue grew 28.5% YoY to USD 5,780 mn, driven by India, Africa, and home services. Home broadband customers rose 37.7% YoY to 11 mn, led by fibre expansion. Going forward, the operator exited its commodity enterprise business, shifting focus to IoT, security, and cloud.

Etisalat Group: Achieved 28.1% YoY growth to USD 4,913.8 mn, driven by enterprise and international markets such as Egypt along with acquisition of PPF telecom.

Zain Group: Revenues grew 13.1% YoY, benefiting from strength across core markets including Jordan, Saudi Arabia, and Iraq.

MTN: Revenues increased 45.9% YoY in Q2-2025, aided by the growth in largest markets, namely, Nigeria and Ghana. Among the segments, data services remained a key driver.

- Equipment sales and non-core revenue as growth buffers: Where service revenues stagnate, operators are increasingly leaning on equipment sales, system solutions, or media to sustain growth. This highlights both revenue diversification and dependence on cyclical, non-core streams.

Verizon: Growth of 5.2% YoY, with a 25.2% surge in wireless equipment sales, offsetting declines in legacy broadband. Verizon added 209,000 net residential fixed-wireless broadband customers to reach 2.5 million customers, 50% more than a year ago.

AT&T: Revenue up 3.5% YoY to USD 30,847 mn, largely from 15.9% growth in equipment sales, suggesting that AT&T’s cheaper plans were luring customers away from its rivals.

Rogers: Revenues increased by 2.4% YoY to USD 3,768.2 mn, supported by equipment sales and media revenues tied to NHL playoffs. The operator also became a majority owner of Maple Leaf Sports & Entertainment, signalling a focus on media revenues.

Vodafone: 3.9% YoY growth in revenues to USD 10,640.7 mn, where service revenue gains balanced business revenue declines.

Deutsche Telekom: Revenues stable with growth of 1.0% YoY, with US market and system solutions growth offsetting weaker German business. The operator continued to invest in network infrastructure, extending its leadership in both fixed and mobile networks.

- Saturated markets face structural revenue pressures: In mature, high-penetration markets, revenue growth is slowing or reversing. Competitive intensity, regulatory headwinds, and shifting consumption patterns are eroding topline momentum.

BT: Revenue fell 3.4% YoY, with the consumer segment hit hardest due to weaker handset sales and challenging international trading.

Telefonica: Declined 3.7% YoY, reflecting adverse FX movements, particularly BRL vs EUR. The numbers highlight inconsistency across its international empire, fuelling expectations of a major rethink of its future shape and structure.

SK Telecom: Revenue down 1.9% YoY after subscriber losses from asset sales and a major cybersecurity incident, and the subsequent expenses and discounts that will be provided to customers.

China Mobile: Marginal 1.1% YoY decline, with sharp drops in voice and wireless data offset partially by other services.

Singtel: Revenues dipped 0.6% YoY, as enterprise growth at NCS was offset by weakness in Optus and Singapore retail.

Telstra: Slight 0.2% YoY decline, with only high-end mobile sales providing growth support.

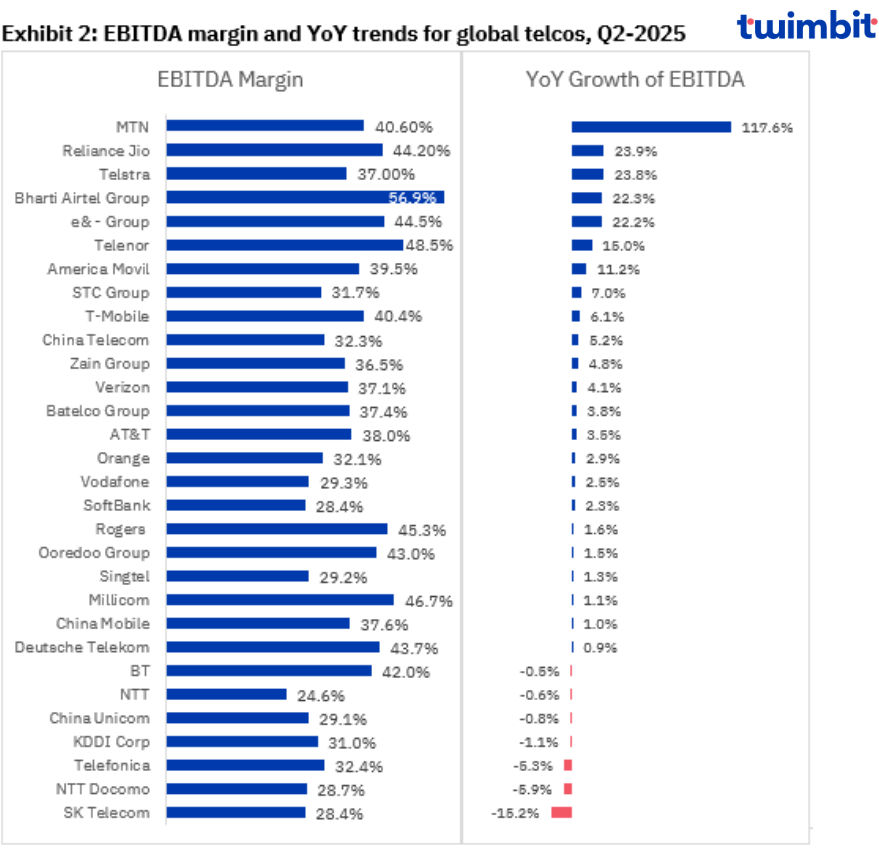

EBITDA analysis of global telcos: Q2-2025

Average EBITDA margin for global telcos stabilized at 36.1% in Q2-2025.

In Q2-2025, scale leaders like Jio, Airtel, Etisalat, and Telstra delivered strong EBITDA gains, while operators such as Telefonica and Vodafone faced FX and regulatory headwinds. Mature incumbents including AT&T and Verizon showed stability, but profitability stayed defensive.

- Scale converts growth into margin power: Market leaders are proving that size alone is not enough, what matters is how scale is monetized. Operators with deep ecosystems are turning subscriber growth and product diversification into superior margin expansion.

Reliance Jio: EBITDA grew 23.9% YoY to USD 2,119.2 mn, margins increased to 44.2%, powered by a stronger product mix.

Bharti Airtel Group: EBITDA rose 22.3% YoY with margins at 56.9%, driven by scale in India and Africa. The operator is focusing on high-margin services, leveraging leadership in IoT and growth in proprietary cloud solutions.

Etisalat Group: EBITDA increased 22.2% YoY to USD 2,187.6 mn, but margins slipped to 44.5%. The acquisition of e& PPF Telecom, strong enterprise demand, and narrowing losses in digital ventures supported EBITDA growth.

Telstra: EBITDA surged 23.8% YoY, driven by mobile and enterprise momentum alongside lower labour costs boosting structural efficiency gains.

- Market-specific shocks and adjustments: Local disruptions, whether regulatory shifts, FX moves, or one-off events—can materially alter short-term profitability. Leaders need to balance resilience with quick recovery mechanisms.

Telefonica: EBITDA declined 5.3% YoY, margin slipping marginally to 32.4%, weighed down by FX headwinds. The company is expanding its customer base slowly, with modest fiber gains and minimal 5G improvements.

Vodafone: EBITDA rose 2.5% in Q2-2025 with margins stable at 29.3%. Growth was muted by regulatory pressures in Germany, which weighed on service revenues. Comparisons were also impacted by higher other income in the prior year from the Indus Towers stake sale.

BT: EBITDA fell 0.5% YoY as weak handset sales dragged topline, partly offset by cost transformation efforts.

Deutsche Telekom: EBITDA rose to USD 14,204.2 mn with a 0.9pp margin gain, reflecting efficiency offsets despite challenges in domestic revenues.

- Mature incumbents deliver stability, not breakthroughs: For traditional incumbents, EBITDA growth is modest at best. Profitability here signals stability and defensive positioning rather than transformative upside.

America Movil: EBITDA grew 11.2% YoY to USD 4,738.1 mn, but margins slipped to 39.5% due to higher equipment import costs.

AT&T: EBITDA rose 3.5% YoY, margins flat at 38.0%, reflecting balanced execution amid rising costs. Wireless segment EBITDA margin also declined slightly year over year due to higher customer acquisition costs.

MTN: EBITDA growth of 117.6% YoY in Q2-2025 achieved, aided by the sale of its Guinea-Bissau subsidiary to Mexican telecom firm, Telecel. This transaction aligns with MTN’s strategic divestment from smaller West and Central African (WECA) markets.

Verizon: EBITDA increased slightly to USD 12,807 mn, margin steady at 37.1%.

Rogers: EBITDA up 1.6% YoY to USD 1,706.4 mn, supported by cable and media segments. This shows shifting focus from legacy services to broader diversified sources of unlocking value.

Batelco Group: EBITDA rose 3.8% YoY to USD 124.7 mn, signalling steady but incremental growth.

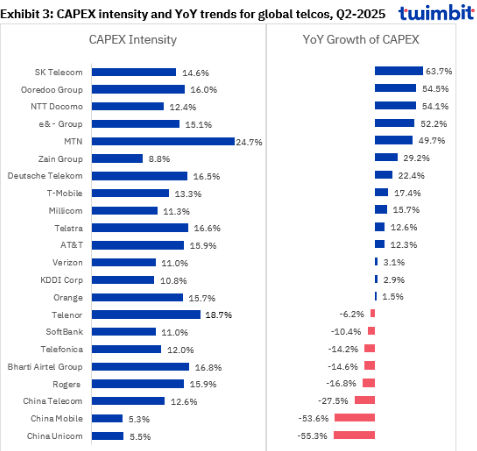

CAPEX analysis of global telcos: Q2-2025

Average CAPEX intensity stood at 12.3% in Q2-2025.

In Q2-2025, telcos shifted capex priorities SK Telecom, Zain, and Etisalat invested heavily in AI-ready networks, while Telenor, Airtel, China Telecom, and Unicom scaled back as 5G rollouts peaked. AT&T, Deutsche Telekom, and Telstra anchored long-term strategies on fibre to drive convergence and resilience.

- Telcos bet on AI-ready infrastructure: The sharp rise in capex by select operators shows that the next competitive frontier is no longer just faster networks, but networks built to power AI, cloud, and enterprise-grade services.

SK Telecom: Growth of 63.7% YoY capex, pivoting from pure 5G upgrades to building AWS-backed AI data centres and AI-driven service quality enhancements.

Zain Group: 29.2% YoY increase in Capex, attributed a low base effect and to fund AI-led initiatives, signalling an intent to reposition as a digital infrastructure player.

Etisalat Group: 52.2% YoY, deploying capital across Pakistan, Afghanistan, and UAE with a clear tilt toward enterprise diversification and modernisation.

- The end of the 5G buildout cycle: For operators in mature markets, the slowdown in capex is not hesitation, it is the natural endgame of 5G deployment. The strategic question now is how well they monetize what has already been built.

Telenor: Decline of 6.2% YoY in capex, as Nordic 5G rollouts near completion while intensity now stands at 18.7%.

Bharti Airtel: 14.6% YoY decrease reported, having front-loaded 5G spend in India, now shifting towards cloud services, IoT, data centres and partnerships.

China Telecom: Capex declining 27.5% YoY, signalling a pivot from network expansion in mobile segment to rigorous investment scrutiny. The operator displays continued focus on industrial digitalisation business.

China Unicom: 55.3% YoY decrease in capex, emphasizing leaner, utilization-driven networks rather than headline-grabbing rollouts.

- Fibre as the new anchor asset: Even as mobile grabs headlines, fibre is emerging as the long-term anchor of telcos’ capital plans. Operators see fibre not just as connectivity, but as a platform for converged services like home broadband, enterprise solutions, and 5G backhaul.

AT&T: Growth of 12.3% YoY capex to USD 4,897.0 mn, with fibre at the core of its growth strategy. The planned legacy copper infrastructure shut down by 2029 underscores a decisive pivot to next-gen infrastructure.

Deutsche Telekom: Strong capex growth in the US and Europe reflects fibre-centric upgrades. These investments strengthen its convergence play and sustain competitiveness against cable peers.

Telstra: Capex increased by 12.6% YoY in Q2-2025, focused on reinforcing fixed-line infrastructure. Fibre expansion supports bundling of mobile, broadband, and enterprise services while enhancing 5G backhaul.

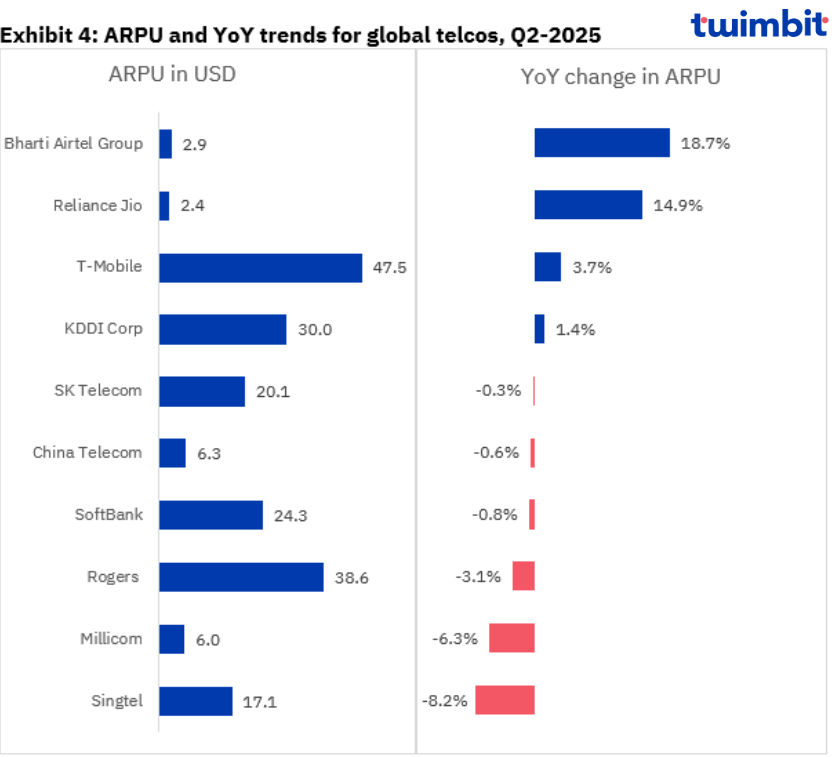

ARPU analysis of global telcos: Q2-2025

Stagnant ARPU growth with only 4 telcos out of 11 reporting growth in ARPU.

In Q2-2025, Jio, Airtel, and America Movil lifted ARPU through tariff hikes and postpaid growth, while Rogers, Softbank, Singtel, and Millicom faced declines in saturated markets. SK Telecom and China Telecom held ARPU steady, showing resilience amid churn and tariff pressures.

- Tariff discipline becomes the growth engine: Operators with pricing power are no longer chasing volumes alone, they are systematically using tariff hikes and premium plan migration to push ARPU upward, even in highly penetrated markets.

Reliance Jio: ARPU rose 14.9% YoY to USD 2.4, reflecting bundle repricing and higher per-user data traffic. The realignment of base tariff positions Jio to capture stronger pricing power, boosting short-term profit margins and potentially driving sustainable earnings growth.

Bharti Airtel Group: ARPU climbed from USD 2.4 to USD 2.8, demonstrating how tariff rationalization, postpaid additions and better product mix can unlock sustainable growth. Shift to higher tariff plans is expected to drive ARPU growth and improve profitability.

America Movil: ARPU gains across most regions came from a deliberate pivot toward postpaid-heavy portfolios, which offer better ARPU metrics.

- Saturation drags on consumer value capture: In mature markets, competition and regulatory limits are squeezing ARPU, showing that connectivity alone no longer guarantees pricing power. Growth requires differentiation beyond core mobile services.

Rogers: ARPU fell 3.1% YoY to USD 38.6, underscoring competitive intensity in Canada’s slowing market. Future growth will rely on ARPU recovery and subscriber expansion, with bundling strategies and network quality supporting long-term top-line and margin improvements.

Softbank: ARPU slipped 0.8% to USD 24.2, reflecting limited headroom without diversification in Japan’s saturated mobile sector.

Singtel: ARPU dropped 8.2% YoY to USD 17.0, as rising data demand failed to offset consumer segment decline.

Millicom: ARPU decreased to USD 6, highlighting pricing fragility and the urgency of bundled value creation.

- Holding ground amid structural shocks: Flat ARPU in the face of disruption is a sign of resilience. Operators that can maintain user value despite subscriber churn or tariff cuts show strong defensive positioning and customer stickiness.

SK Telecom: ARPU remained broadly stable (–0.3%) despite cybersecurity-driven subscriber loss in the recent quarter. The upcoming decision from regulators on penalties for the major data leak could result in significant financial impact, driving down ARPU in future quarters.

China Telecom: ARPU dipped only 0.6% YoY to USD 6.32, signalling the offsetting effect of family services and data uptake.

Frontier innovations shaping global telco trends

Satellite-enabled direct-to-device connectivity

Operators in several countries, including Telstra (Australia) and T-Mobile (USA) are partnering with satellite providers like SpaceX’s Starlink to enable direct-to-handset services. This allows even standard smartphones to send text messages or remain connected via satellite, bypassing traditional network infrastructure.

This innovation is redefining the geography of connectivity, making telecom services possible in remote or underserved regions without new tower builds. It enhances resilience and coverage, creating a competitive differentiator in markets with vast rural or hard-to-reach areas.

Edge AI for real-time network insights and service delivery

Telecom operators globally are embedding AI capabilities directly at the edge of the network, closer to end users and devices. This allows for real-time analytics, predictive maintenance, improved service quality, and reduced latency.

Edge AI transforms telecom networks into agile, self-optimizing systems. By processing data locally, operators improve responsiveness, lower operational costs, and create opportunities for new, latency-sensitive applications such as AR/VR and industrial IoT.

Quantum-based network optimization

NTT DOCOMO used D-Wave’s quantum computing to cut peak-load paging signals by ~15%, while TIM applied it to 5G site planning, achieving tenfold faster deployment, showing quantum’s immediate impact on network efficiency and rollout.

These operators are practically demonstrating how quantum computing can improve decision-making latency and infrastructure efficiency. Rather than waiting for quantum to mature, they are extracting commercial value now, optimizing traffic flows and capital deployment, while paving the way for future scalability in 6G networks.

Research methodology and assumptions

Blended mobile ARPU has been incorporated wherever relevant for a more holistic view.

The “Global Telcos Performance Benchmarks – Summer 2025” report offers crucial insights into the performance of telecom companies. It analyses key financial indicators such as Revenues, EBITDA, CAPEX and ARPU for Q2-2025 (Apr – Jun 2025).

This report utilizes data collected from telecom firms and extensive secondary research. Twimbit follows a calendar year for its data analysis, with FY representing January to December.

To maintain consistency and enable accurate comparisons, the report applies a constant currency conversion rate, reflecting the average USD exchange rate for April – June 2025.

The report evaluates Revenue and EBITDA for 30 and 30 telecom companies, respectively. CAPEX and ARPU analysis cover data from 22 and 10 companies, respectively.