Key takeaways

- Average Year-on-Year (YoY) revenue increased marginally from 2.3% in Q3-2023 to 2.5% in Q2-2024.

- Aggregate revenue increased by USD 6.4 billion to USD 320.6 billion in Q3-2024, with India based telcos (Reliance Jio and Bharti Airtel) exhibiting double-digit growth.

- Robust revenue growth, cost-containment measures and operational efficiency efforts resulted in positive EBITDA change for ~76% of the analysed telcos.

- Nearly 38% of the telcos analysed reported minimal EBITDA variation, within a manageable range (-3% to +3%).

- Telcos maintained EBITDA margin stability of 37% due to cost-containment measures, operational efficiency initiatives, and continued incremental top-line growth.

- Bharti Airtel and Reliance continue to exhibit robust and stable EBITDA margins (above 50%), indicating resilience amidst global pressures.

- Network expansion initiatives in Middle East along with investment in digital infrastructure capabilities resulted in average CAPEX grow to 17.2% in Q3-2024.

- Nearly 45% of the 20 telcos analysed reported a YoY CAPEX growth in Q3-2024, as compared to ~40% in Q3-2023.

- Average ARPU growth remained stagnant (0.4% YoY growth), reaching USD 23.6 in Q3-2024, despite strong growth of Bharti Airtel and Reliance Jio in India and Millicom, Verizon and AT&T from the Americas.

- Tariff hikes facilitated ARPU growth amongst Indian telcos, whereas post-paid segment along with price hikes in Q3-2024 facilitated growth for US based telcos AT&T and Verizon. ARPU level remains stagnant for China based telcos owing to low pricing amidst intense competition.

- Telcos in select regions announced shutting down their legacy 2G/3G networks in order to reduce to reduce cost and facilitate subscriber migration to 4G/5G network.

- Global telcos continue to leverage AI, cloud technologies, and strategic partnerships to enhance network capabilities, improve customer experiences, and drive digital transformation, to cater to the evolving customer requirements.

Trending Global telcos performance insights

- AI investment and strategic expansion: Leading telecom operators are pursuing substantial investments in AI infrastructure and capabilities to establish competitive advantages and drive innovation. SK Telecom (SKT) exemplifies this trend with its USD 200 million investment in a US based AI infrastructure firm and plans for a regional AI hub. Additionally, AT&T partnered with Unsupervised, enhancing AI capabilities to analyse data and unlock opportunities exceeding USD 100 million.

- Fibre network expansion and infrastructure investments: As demand for high-speed internet grows, operators are committing to substantial fibre network expansions to enhance service reliability and meet connectivity needs.

- Bell Canada’s USD 5.1 billion (CAD 7.6 billion) investment to acquire Ziply Fiber, alongside AT&T’s USD 1 billion partnership with Corning, highlights a sector-wide emphasis to remain competitive and support data-intensive services.

- 5G, Network Evolution, and legacy network decommissioning: Telecom operators are modernizing networks by expanding 5G and phasing out older infrastructure.

- Deutsche Telekom plans to retire 2G by Jun – 2028, Telstra and Optus announced to shut down their 3G networks by Oct- 2024. Zain announced to shut its 3G network in Saudi Arabia by Jun – 2025, whereas Vietnam announced Sep – 2028 for 3G sunset.

- Mergers and market consolidation: Industry consolidation is accelerating as telecom companies seek to improve economies of scale and enhance their service portfolios through mergers and acquisitions.

- Vodafone’s merger with 3 UK would create a major telecom player in UK, while its deal with Digi to acquire stake in Telekom Romania Mobile further strengthens its positioning in Romania.

- Additionally, BT’s exploration of divesting its international unit represents a restructuring strategy to streamline operations and focus on core competencies.

- Leadership transitions and Strategic realignments: Several telecom leaders are preparing for transitions that signal shifts in strategic direction and adaptation to evolving digital priorities.

- For example, Airtel’s CEO Gopal Vittal plans to exit by 2026, potentially paving the way for new leadership and direction, while Axiata’s Wijayasuriya is stepping into a national role to lead Sri Lanka’s digital strategy.

- AI-Powered service enhancements and efficiency gains: As AI becomes vital for operational efficiency, telecom operators are embedding it into core functions.

- SK Telecom, in partnership with Samsung, utilizes AI to optimize 5G base station performance, positioning itself as a leader in AI-driven telecom infrastructure.

- Meanwhile, Verizon enhances fibre network protection by integrating AI and machine learning to prevent accidental fibre cuts, reinforcing network reliability.

- Spectrum and Infrastructure deals to expand network capacity: The growing demand for seamless connectivity is propelling spectrum acquisitions and infrastructure expansions.

- Verizon’s USD 3 billion tower deal with Vertical Bridge and its USD 1 billion spectrum purchase from UScellular exemplify how operators are fortifying network capacity to handle increased data traffic and future-proof their infrastructures.

- Regulatory Changes and Mobile licensing adjustments: Regulatory environments are shifting in response to market dynamics and evolving technology landscapes.

- South Korea’s recent decision to cancel a mobile license of “Stage X” serves as a case in point, showcasing how governments are refining policy frameworks to adapt to the changing telecom ecosystem.

- Meanwhile, the Malaysian Government awarded U Mobile a license to build the country’s second 5G network, aiming to accelerate nationwide 5G deployment alongside Digital Nasional Berhad.

- By awarding 5G licenses to Orange Egypt, Vodafone Egypt, e& Egypt, in addition to Telecom Egypt, Egypt’s National Telecom Regulatory Authority (NTRA) is likely to intensify competition among providers and also pave the way for rapid digital advancement.

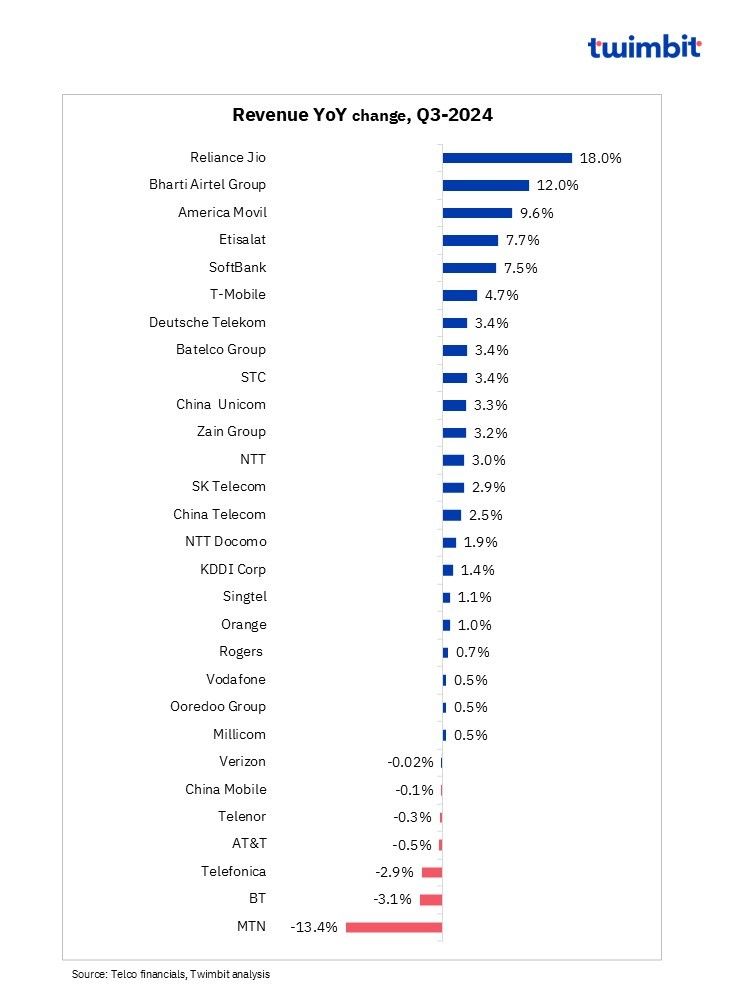

Revenue analysis of Global telcos: Q3-2024

Average revenue growth for leading global telcos increased marginally from ~2.3% in Q3-2023 to ~2.5% in Q3-2024

Approximately 76% of telcos achieved YoY revenue growth in Q3-2024 (as compared to 69% in Q3-2023). The combined revenue of the 29 analysed telcos increased by ~USD 6.4 billion to ~USD 320.6 billion in Q3-2024, with India based telcos (Reliance Jio and Bharti Airtel) exhibiting double-digit growth.

Exhibit 1: Revenue trends for Global telcos, Q3-2024

Key highlights

- India’s leading telcos Bharti Airtel and Reliance Jio reported robust revenue growth driven by strategic tariff increases and an expanding subscriber base resulting in strong performance in the mobility segment.

- In contrast, Chinese telecom operators have faced stagnancy in revenue growth challenges the start of FY-2023, particularly in FY-2024. This is largely due to their inability to effectively monetise 5G mobile services, as competitive pressures have kept prices low.

- Telcos in the Middle East, including Zain, Batelco, Etisalat, and Ooredoo, experienced overall revenue growth. This growth was fuelled by increased data service demand, supported by the ongoing expansion of 4G and 5G networks across most of the operating countries. Additionally, the growing contribution from beyond-connectivity offerings in both consumer and enterprise segments has been a significant growth driver.

- Conversely, companies such as MTN, Telefonica, Telenor reported revenue declines, primarily due to geography-specific factors which hindered overall revenue growth.

Reliance Jio

Reliance Jio’s revenue increased by 18% YoY to USD 3.8 billion (INR 317.1 billion) in Q3-2024. This growth was driven by tariff hikes in the mobility segment, subscriber growth in home broadband, and an expansion in digital services.

- A 7.4% increase in ARPU and a 4.2% rise in mobile subscribers, including an 18 million increase in 5G subscribers, contributed to the growth in mobile revenue.

- Jio’s home broadband service, Jio AirFiber, added 2.8 million connections, making it the fastest-growing fixed wireless operator globally.

Bharti Airtel

Bharti Airtel’s group revenue grew by 12.0% YoY to USD 5.0 billion (INR 414.7 billion) in Q3-2024, supported by strong performance in India and consistent growth in Africa.

- In India, revenue increased by 16.9% YoY to USD 3.8 billion (INR 315.6 billion), driven by improved mobile segment realizations and sustained momentum in the Homes and Airtel Business segments.

- In India, Airtel Business revenue increased 10.7% YoY to USD 675.1 million (INR 56.5 billion), Homes business revenue grew 17.3% YoY to USD 170.9 million (INR 14.3 billion) with strong customer additions, while Digital TV revenue rose 1.0% YoY to USD 90.6 million (INR 7.6 billion) in Q3-2024.

- Despite overall growth in ARPU and data customers, Africa’s revenue declined by 1.1% YoY to USD 1.2 billion (INR 101.6 billion), due to currency devaluation in Nigeria, Malawi, Zambia, and Tanzania.

America Movil

America Movil’s revenue grew 9.6% YoY to USD 11.8 billion (MXN 223.5 billion) in Q3-2024, led by growth in mobile services and fixed broadband revenue.

- Mobile service revenue grew by 5.2%, reporting its best performance in over a year, driven by growth in postpaid segment revenue.

- Fixed-line service revenue increased by 5.9%, driven by a 7.4% rise in broadband revenue and a 10.1% growth in corporate network revenue.

Additionally, growth in major geographies like Mexico, Brazil, Colombia, Peru, Argentina, and Central America facilitated overall revenue growth, which offset the minor declines reported in Ecuador, the Caribbean, and Austria.

Etisalat

Etisalat’s revenue increased by 7.7% YoY to USD 3.9 billion (AED 14.4 billion) in Q3- 2024, driven by growth across its telecom and digital verticals.

- Revenue in the UAE grew by 4.2%, supported by growth in mobile, fixed, and other segments.

- International subscribers grew by 6% YoY, reaching 163 million, mainly due to growth in Egypt and MoovAfrica, resulting in a 2.6% YoY revenue increase.

- Enterprise revenue was nearly flat, with a 0.8% YoY growth, primarily due to IoT project delays. However, the acquisition of Glasshouse in Sep-2024 is expected to boost future revenue growth.

SoftBank

SoftBank’s revenue increased by 7.5% YoY to USD 10.9 billion (JPY 1.6 trillion) in Q3-2024, primarily driven by growth in the Enterprise business segment and positive contributions from other operating segments.

- The Enterprise business revenue grew by 11.5% year-over-year to USD 1.5 billion (JPY 230.3 billion), led by growth in mobile and business solutions.

- Business solution segment revenue increased 28.9% YoY to USD 730.0 million (JPY 108.5 billion), on account of the business of WeWork Japan GK, in addition to incremental revenue from cloud services, IoT solutions and security solutions by catering to enterprise customers’ demand.

- The Consumer segment, accounting for 46.1% of overall revenue, grew by 4.8% YoY to USD 5.0 billion (JPY 745.2 billion), primarily driven by the mobile segment.

MTN

MTN’s revenue declined by 13.4% YoY to USD 2.3 billion (ZAR 42.0 billion) in Q3- 2024, primarily due to a decline in service revenue in Nigeria, impacted by subscriber losses in compliance with regulatory directives.

- Nigeria’s revenue fell by 35.6% YoY to USD 525.9 million (ZAR 9.4 billion), driven by rising inflation and currency depreciation.

- During Q3-2024, revenue from the Middle East and North Africa region decreased significantly (around 78%) to USD 15.5 million (ZAR 279 million), impacted by decline in Ghana and Afghanistan.

- Revenue from West and Central Africa declined by 6.2% YoY to USD 777.2 million (ZAR 14.0 billion), due to decline in Core d’Ivoire.

BT

BT’s revenue declined by 3.1% YoY to USD 6.6 billion (GBP 5.1 billion) in Q3-2024, due to declines in the Business and Consumer segments, which offset growth in the OpenReach segment.

- Business segment revenue declined by 6.8% YoY to USD 2.5 billion (GBP 1.9 billion), due to weaker performance in non-UK operations within global and portfolio channels.

- Consumer segment revenue fell by 1.7% YoY to USD 3.2 billion (GBP 2.4 billion), owing to intense competition.

- OpenReach segment revenue grew by 2.2% YoY USD 2.0 billion (GBP 1.6 billion), driven by broadband price increases and growth in FTTP and Ethernet bases.

Telefonica

Telefonica’s revenue declined by 2.9% YoY in Q3-2024 to USD 11.0 billion (EUR 10 billion), primarily due to foreign exchange headwinds (depreciation of the Brazilian real against the Euro) and impact of termination rate reductions and changes in the 1&1 business model in Germany.

Telenor

Telenor’s revenue declined by 0.3% YoY to USD 1.9 billion (NOK 20.0 billion) in Q3-2024, due to decline in the Asia and Amp segments, which offset marginal revenue growth from the Infrastructure segment and the Nordic region.

- Revenue from Asia decreased by 4.9% YoY to USD 449.6 million (NOK 4.8 billion) impacted by decline in revenue from Grameenphone Bangladesh, whereas Amp segment revenue decreased 26.5% YoY to USD 83.1 million (NOK 889 million).

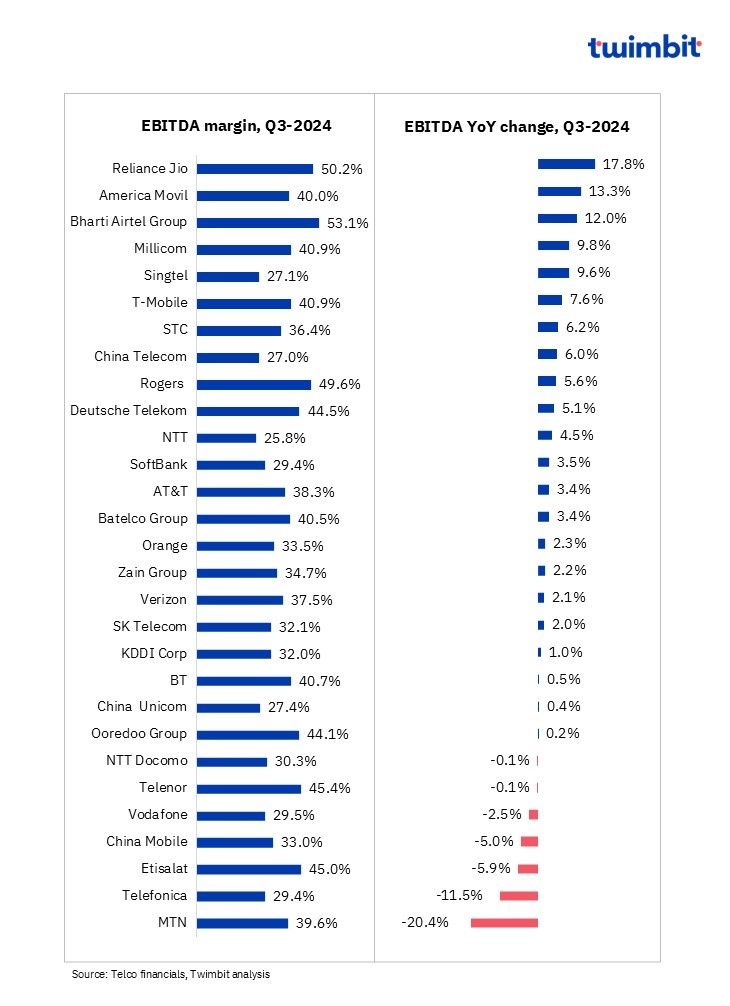

EBITDA analysis of Global telcos: Q3-2024

Average EBITDA margin for the leading global telcos stabilised at 37% in Q3-2024

Robust revenue growth coupled with improved operations, Cost control measures and operational efficiency initiatives resulted in stabilized EBITDA for ~76% of the analysed telcos. Nearly ~38 % of telcos reported a slight EBITDA variation, within a manageable range (-3% to +3%).

Exhibit 2: EBITDA and EBITDA margin trends for Global telcos, Q3-2024

Key highlights

- Robust revenue growth and improved operations contributed to strong EBITDA growth for Indian telcos Bharti Airtel and Reliance Jio, as well as America Movil.

- Increased cost savings and optimization efforts led to EBITDA growth for Millicom, Deutsche Telekom, Singtel, and STC Group.

- Rogers benefited from synergy realization related to the Shaw Transaction and ongoing cost efficiencies, which facilitated EBITDA growth.

- In China, telecom operators such as China Unicom and China Telecom experienced EBITDA growth. However, China Mobile’s EBITDA saw a slight decline due to a decrease in revenue.

- Macroeconomic factors, including currency fluctuations, higher inflation, and rising costs, negatively impacted EBITDA growth for telecom companies like MTN, Telefonica, and Etisalat.

Reliance Jio

Reliance Jio’s EBITDA increased by 17.8% YoY to USD 1.9 billion (INR 159.3 billion) in Q3-2024, driven by strong revenue growth and efficient utilization of operating capacities. The EBITDA margin remained stable at 50.2% in Q3-2024, compared to 50.3% in Q3 2023.

America Movil

America Movil’s EBITDA rose by 13.3% YoY to USD 4.7 billion (MXN 89.4 billion) in Q3-2024, driven by robust revenue growth from subscriber expansion. Consequently, the EBITDA margin increased by 130 basis points to 40.0% in Q3 2024.

Bharti Airtel

Bharti Airtel’s EBITDA grew by 12.0% YoY to USD 2.6 billion (INR 220.2 billion) in Q3-2024, driven by higher revenue growth, primarily from its Indian operations. The EBITDA margin remained stable at 53.1% in Q3 2024.

Millicom

Millicom’s EBITDA grew 9.8% YoY (10.2% organic basis) to USD 585 million in Q3-2024, driven by growth across its operating countries.

- Guatemala accounted for the highest EBITDA at USD 220 million in Q3-2024, with an 8.7% YoY growth due to service revenue growth and cost savings.

- Colombia experienced the highest EBITDA growth, increasing by 18.8% YoY to USD 133 million, driven by cost savings.

Singtel

Singtel’s EBITDA increased by 9.6% YoY to USD 735.5 million (SGD 970 million) in Q3-2024, attributed to improved performance, cost optimization efforts, and margin enhancement across key segments.

- Optus’s EBITDA grew by 10.2% YoY to USD 385.2 million (SGD 508 million), driven by improved mobile performance and disciplined cost management.

- NCS’s EBITDA increased by 37.1% YoY to USD 64.5 million (SGD 85 million), attributed to higher operating revenue, cost efficiencies, and improved margins.

- Singtel Singapore’s EBITDA increased by 1.6% YoY to USD 281.3 million (SGD 371 million), owing to increased operating income resulting from decline in operating expenses, owing to a reduction in the direct cost of sales and total manpower cost from a lower average headcount

Consequently, EBITDA margin increased from 25.0% in Q3-2023 to 27.1% in Q3-2024.

MTN

MTN’s EBITDA decreased by 20.4% YoY to USD 926.5 million (ZAR 16.6 billion) in Q3-2024.

- South Africa’s EBITDA grew by 0.4% YoY to USD 262.3 million (ZAR 4.7 billion).

- EBITDA from Nigeria declined by 49.9% YoY to ~USD 195 million (ZAR 3.5 billion), impacted by factors including naira devaluation, VAT introduction, higher inflation, and energy costs.

- Operational inefficiencies due to the Sudan conflict also contributed to the decline.

Telefonica

Telefonica’s EBITDA decreased by 11.5% YoY to USD 3.2 billion (EUR 2.9 billion) in Q3-2024, primarily due to foreign exchange headwinds from the depreciation of the Brazilian real against the euro. This resulted in the EBITDA margin decreasing by 290 basis points to 29.4% in Q3-2024.

Etisalat

Etisalat’s EBITDA decreased by 5.9% YoY to USD 1.8 billion (AED 6.5 billion) in Q3-2024, impacted by rising costs, EGP depreciation, and the absence of prior one-off savings. As a result, the EBITDA margin decreased by 650 basis points to 45.0% in Q3-2024.

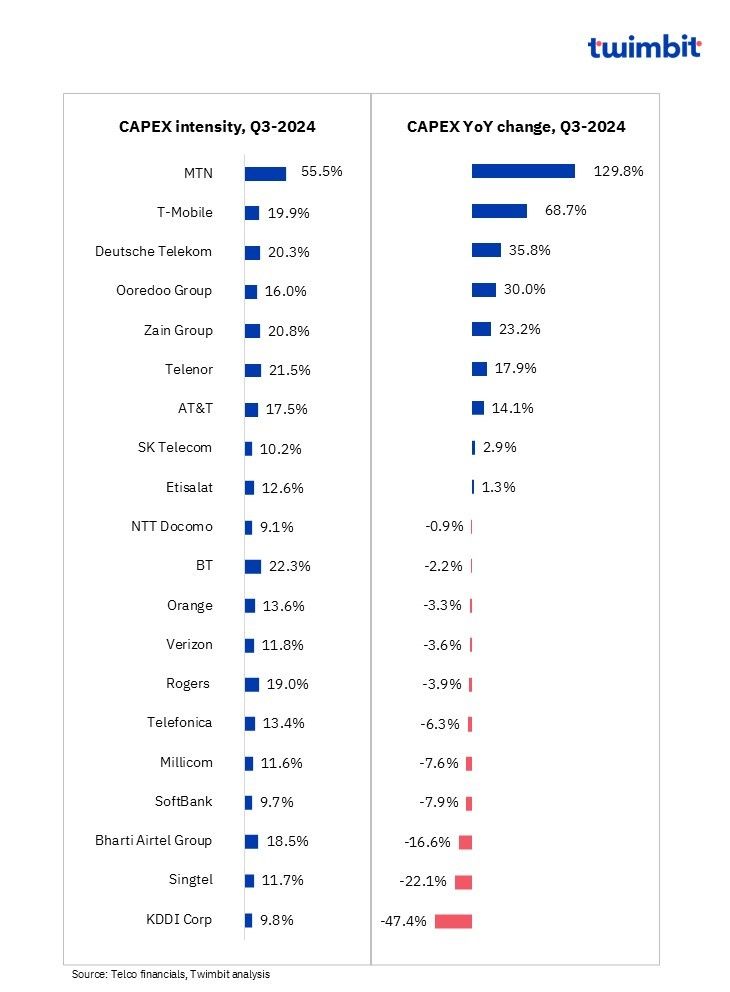

CAPEX analysis of Global telcos: Q3-2024

Average CAPEX intensity increased from 15.5% in Q3-2023 to 17.2% in Q3-2024, led by network expansion and digital transformation related investments

Nearly 45% of the 20 telcos analysed reported a YoY CAPEX decline in Q3-2024, as compared to ~40% in Q3-2023. The maturation of 4G/5G network rollouts in major markets like the US, India, China and Europe has resulted in lower spending by telcos in the regions.

Conversely, CAPEX spending by telcos continues to be driven by the ongoing 4G and 5G network deployments in the Middle East and Africa, fibre rollouts in North American and European markets, and investments in digital infrastructure, including cloud services, data centres, cybersecurity, and artificial intelligence.

Exhibit 3: CAPEX and CAPEX intensity trends for Global telcos, Q3-2024

Key highlights

- Investment in 4G and 5G network expansion, fibre rollout and digital capability investments continue to drive CAPEX spending in the Middle East region.

- Telcos such as SK Telecom, KT Corp, Softbank, and Singtel are focusing on data centres, cybersecurity, and AI-related investments as key areas of growth.

- In North America, Europe, and India, fibre rollouts have emerged as a primary investment theme, following the peak of wireless investments in FY-2023.

- In China, after substantial 5G investments, telecom operators are concentrating on strengthening digital capabilities, including cloud, big data, IoT, and 5G commercial projects like smart cities, factories, parks, and campuses.

MTN

MTN’s CAPEX surged by 129.8% YoY to USD 1.3 billion (ZAR 23.3 billion) in Q3-2024, driven by significant investments in network and platform expansion, particularly in South Africa and Nigeria

T-Mobile

T-Mobile’s CAPEX increased by 68.7% YoY to USD 4.0 billion in Q3-2024, primarily due to the integration of T-Mobile and Sprint networks.

This includes deploying and optimizing acquired Sprint PCS and 2.5 GHz spectrum licenses, as well as constructing and enhancing network infrastructure and deploying recently acquired C-band spectrum licenses to support future network capabilities.

Deutsche Telekom

Deutsche Telekom’s CAPEX rose by 35.8% YoY to USD 6.4 billion (EUR 5.8 billion) in Q3-2024, driven by network expansion and modernization initiatives, including 5G and fibre deployment, with US accounting for nearly for 70% of the total CAPEX.

Ooredoo

Ooredoo’s CAPEX increased by 30% YoY to USD 256.6 million (QAR 935 million) in Q3-2024, led by mobile and fibre network rollouts and expansions, along with spending on digital capabilities such as data centres and disaster recovery.

Zain

Zain’s CAPEX grew by 23.2% YoY to USD 340.7 million (KWD 104.1 million) in Q3-2024, driven by the expansion of 4G and 5G networks, fibre deployment investments, IT BSS and data centre modernization initiatives, and upgrades to transmission capacity.

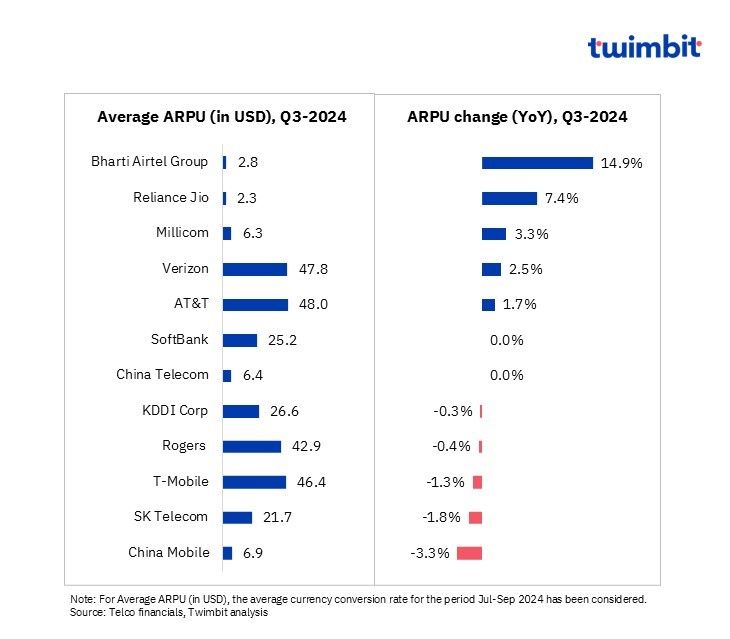

ARPU analysis of Global telcos: Q3-2024

Average ARPU remained stagnant (0.4% YoY growth), reaching USD 23.6 in Q3-2024

The growing data (4G/5G) subscriber mix and price increase initiated in Jul-2024 have increased ARPU for Indian telcos.

Healthy postpaid subscriber contributions resulted in the ARPU growth for the telcos in the Americas, including Verizon, AT&T and Millicom.

Intense competition has impacted the ARPU levels of telcos in China, as telcos are under pressure to keep the prices low.

Exhibit 4: ARPU trends for Global telcos, Q3-2024

Key highlights

During Q3-2024, Indian telcos experienced a significant increase in Average Revenue Per User (ARPU) due to tariff hikes implemented in Jul-2024, with Bharti Airtel maintaining its leadership position, followed by Reliance Jio. However, these tariff increases led to a subscriber shift towards the government-owned telecom operator, BSNL, which did not raise its tariffs.

The impact of these tariff hikes on ARPU is expected to become fully apparent over the next few quarters. In addition to the tariff adjustments, ARPU growth in the sector is anticipated to continue, driven by the migration of subscribers from 2G to 4G networks and an increase in post-paid subscribers. This transition is likely to further boost average data usage per customer in India.

- Bharti Airtel’s ARPU growth was also supported by an expanded subscriber base and a higher concentration of data users, resulting in increased mobile data and voice usage in both Africa and India.

- In Africa, ARPU rose by 5% YoY to reach USD 2.3, while in India, it increased by 14.9% YoY reaching USD 2.8 (INR 233).

- During Q3-2024, Reliance Jio reported a 7.4% YoY growth in ARPU, reaching USD 2.3 (INR 195.1), driven by strategic tariff revisions, strong subscriber growth, and increased data and voice consumption.

- Jio’s 5G subscriber base expanded to 148 million, up from 130 million in the previous quarter.

- Total data traffic grew by 24.0% YoY to 45.0 billion GB, and voice traffic increased by 6.4% YoY to 1.42 trillion minutes in Q3-2024.

In the Americas, telcos such as AT&T, Verizon, Rogers, and Millicom experienced an improvement in overall Average Revenue Per User (ARPU) levels, driven by an increase in postpaid subscriber counts and ARPU.

- During Q3-2024, AT&T saw a net addition of 403,000 postpaid phone subscribers, coupled with a slight reduction in churn rates, resulting in a 2.3% YoY growth in postpaid phone subscribers.

- The increase in ARPU from legacy plans, due to mid-Q3 2024 price hikes, further facilitated overall ARPU growth, which is expected to continue impacting Q4-2024.

- Similarly, Verizon added 238,000 postpaid phones, with a marginal reduction in churn rates, leading to a 1.9% YoY growth in retail postpaid phone connections in Q3-2024, reaching 124.5 million.

- The increasing adoption of its myPlan offering, along with promotional offers and bundled plans that include 5G and streaming services like Netflix, attracted more customers and drove ARPU levels.

- Millicom’s postpaid subscriber count rose by 12.7% YoY to 7.8 million in Q3- 2024, despite a nearly flat overall mobile subscriber count (+0.8% YoY growth).

- This likely contributed to Millicom’s overall ARPU growth of 3.3% (3.9% organically) YoY in Q3- 2024, as most of its operating countries experienced positive ARPU growth in local currency terms.

- Rogers maintained stable ARPU levels in Q3-2024, supported by a 367,000 increase in postpaid subscribers due to higher gross additions, which offset a 0.4 basis point increase in churn rates. However, its prepaid phone count declined to approximately 1.2 million due to lower gross additions during the period.

- For T-Mobile, a 6.2% YoY decline in prepaid ARPU in Q3-2024 offset the growth in postpaid ARPU, resulting in an overall ARPU decline by 1.3% to USD 46.4.

- Despite a net addition of 15,000 postpaid phones to reach 865,000 phones, and a 1.8% increase in postpaid ARPU driven by higher premium services and rate plan optimizations, the negative impact of the prepaid segment could not be fully mitigated.

Intense competition in the Chinese telecommunications market has exerted downward pressure on ARPU levels, as telcos strive to maintain low pricing.

- For China Telecom, ARPU remained relatively stable at USD 6.4 (CNY 45.6), even though the number of 5G package subscribers increased by approximately 12% YoY to 345 million in Q3-2024.

- Conversely, China Mobile experienced a 3.3% YoY decline in ARPU to USD 6.9 (CNY 49.5) during Q3-2024. This decrease occurred despite a 4.9% YoY growth in 5G network customers, reaching 539 million in Q3-2024, as both the average Minutes of Usage per User per Month (MOU) and Average Handset Data Traffic per User per Month (DOU) remained unchanged.

Key strategic developments: Q3-2024

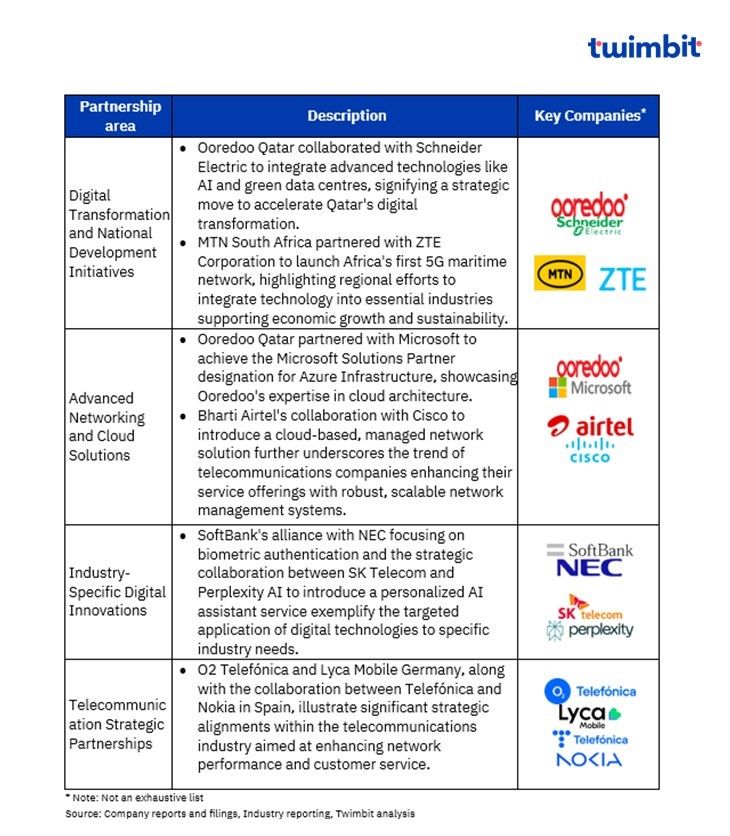

Key strategic partnerships and alliances: Q3-2024

Global telcos are actively adopting advanced technologies and forming strategic partnerships to drive digital transformation and enhance service offerings. From integrating AI and green data centres to deploying 5G networks and leveraging cloud solutions, these collaborations demonstrate a commitment to innovation and meeting the evolving needs of businesses and customers across various sectors.

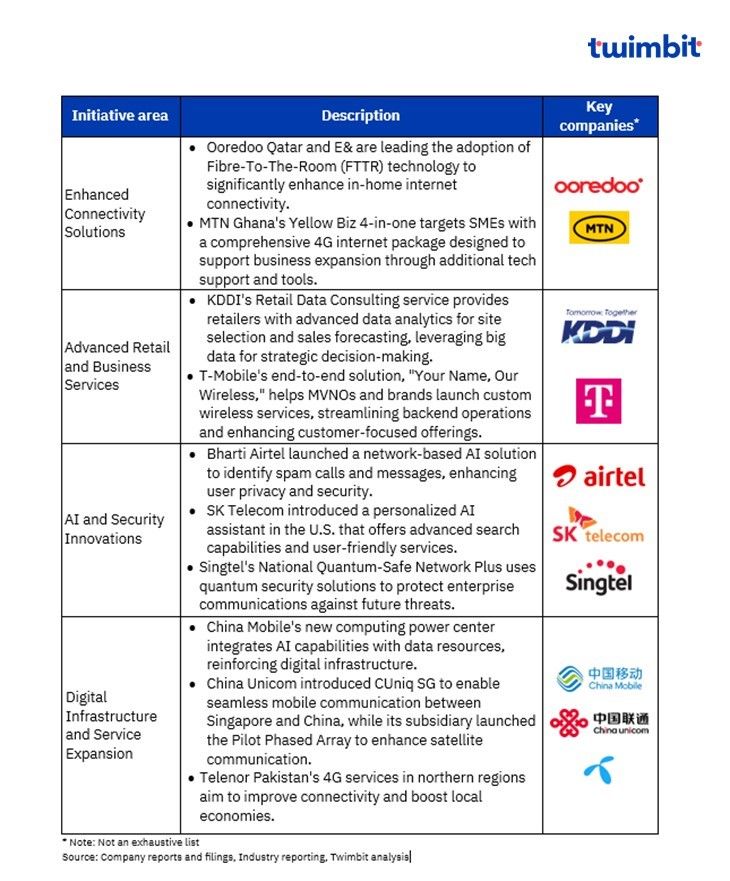

Key strategic initiatives: Q3-2024

Global telcos are actively adopting innovative technologies to enhance services and meet evolving customer needs. From advanced connectivity solutions like FTTR and 5G to AI-powered tools and quantum security, these initiatives highlight the industry’s commitment to innovation and improving customer experiences.

Key contract wins: Q3-2024

Global telcos continue to leverage AI, cloud technologies, and strategic partnerships to enhance network capabilities, improve customer experiences, and drive digital transformation. Such initiatives demonstrate a commitment to innovate and cater to the evolving needs of businesses and governments globally.

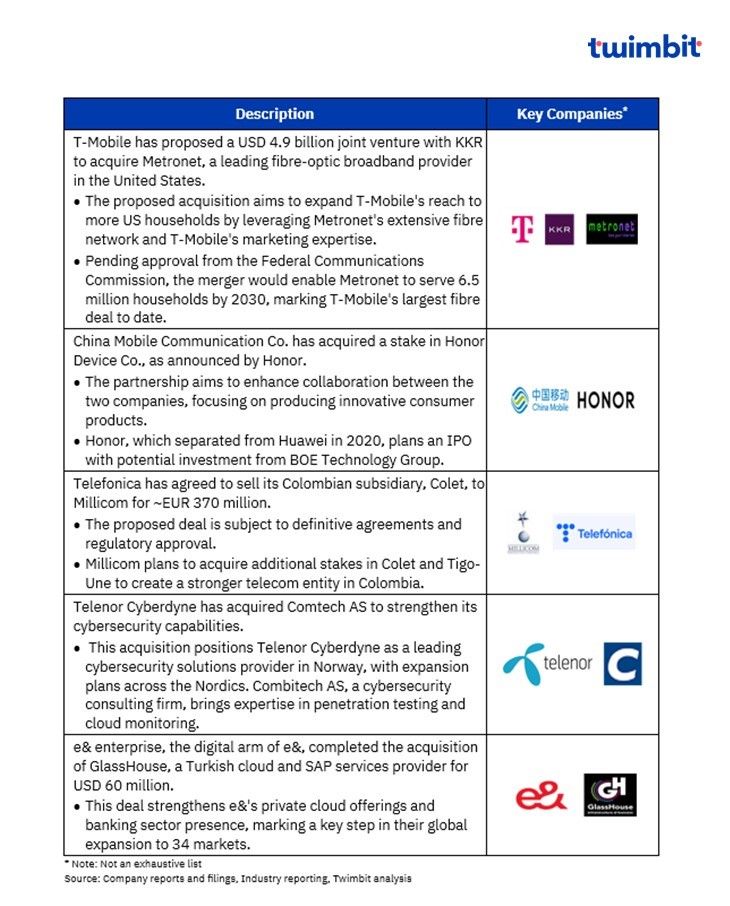

Key M&As and Divestures: Q3-2024

Global telecom industry is undergoing significant changes with telcos focussing on capabilities enhancements. T-Mobile is expanding its broadband reach, China Mobile is investing in Honor, Telefonica is streamlining operations, Telenor Cyberdyne is boosting cybersecurity, and e& enterprise is expanding globally.

Research Methodology and Assumptions

- The “Global telcos performance benchmarks: Autumn 2024” report presents key findings on the performance of 30 strategically selected leading telcos across diverse geographies, offering a comprehensive global perspective on telco performance. Key performance metrics analysed include Revenue, EBITDA, CAPEX, and ARPU for the period July- September 2024.

- This report leverages data acquired from telecommunications companies and includes extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the period from January to December.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate representing the average USD exchange rate for the period July – September 2024 (January-September, wherever applicable for 9M-2024) has been applied throughout the report.

- The report presents a comprehensive assessment of Revenue and EBITDA for 29 telcos each. Additionally, CAPEX and ARPU analyses encompass data from 20 and 12 telcos, respectively.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- Verizon’s ARPU has been standardized starting from Q3-2024, now representing the average ARPU computed using Consumer wireless service revenue and total wireless retail connections data for each quarter. Previously, Wireless retail post-paid ARPA was used for ARPU calculation.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.

Click here for more contents on telecom

Related Global telcos performance insights

Global telecom vendor performance indicators – Summer 2024

Global telcos performance benchmarks – Summer 2024