Trending Global telcos performance insights

AI investment and strategic expansion: Leading telecom operators are pursuing substantial investments in AI infrastructure and capabilities to establish competitive advantages and drive innovation.

- South Korean telcos continue to pioneer the AI investments. By virtue of their aggressive ongoing AI investments, SK Telecom and LG Uplus are targeting AI revenue of USD 18.5 billion and USD 1.4 billion respectively by 2028, whereas KT Corp has set the target at ~KRW 1.4 trillion by 2029.

- Telcos like Ooredoo and Deutsche Telekom focus on enhancing customer experience though launch of AI Hub and Magenta AI respectively. AI predictions enabled Telefonica to reduce its churn rate to lowest level in 20 years and the telco expects 15% of its growth over the next three years to come by applying AI.

Mergers and market consolidation: Industry consolidation is accelerating as telecom companies seek to improve economies of scale and enhance their service portfolios through mergers and acquisitions.

- Vodafone’s merger with 3 UK would create a major telecom player in UK, while its deal with Digi to acquire stake in Telekom Romania Mobile further strengthens its positioning in Romania.

- In Asia, China Mobile plans to acquire Hong Kong broadband provider HKBN for to expand its presence in Hong Kong, whereas Telstra acquired prepaid MVNO Boost Mobile to increase its prepaid subscriber base.

- STC increased its stake in Telefonica to 9.9% whereas Zain Group and e& completed full stake acquisition in infrastructure companies IHS Kuwait and PPF Telecom respectively.

Leadership transitions and strategic realignments: Key leadership transitions in leading telcos signal shifts in strategic direction and adaptation to evolving digital priorities to sustain competitiveness.

- Korean telcos are restructuring to prioritize AI and cloud services. KT announced a restructuring in 2025, which includes the creation of two new subsidiaries, whereas SK Telecom is also undergoing a major restructuring in 2025, dividing into seven business divisions to concentrate on two core areas. Meanwhile, Deutsche Telekom brought together its international and German wholesale operations under a single entity, a move to streamline its offering and meet customer demand for integrated services.

- Key leadership transitions across Bharti Airtel, Globe Telecom and LG Uplus also signals a new set of leaders taking charge.

Rising AI demand drives telco investments in data centres: By operating data centres, telcos can diversify beyond connectivity, monetize edge computing capabilities, and position themselves as end-to-end digital transformation partners for businesses

- In October 2024, Deutsche Telekom announced plans to add five new hubs to its 16 data centres to address growing AI demand and support its T-Systems unit. Similarly, French telecom operator Iliad committed USD 2.7 billion (EUR 2.5 billion) over the next decade to develop its OpCore data centre unit. Additionally, SK Telecom agreed to invest USD 200 million in Smart Global Holdings (SGH), a company specializing in high-performance solutions for data centres and enterprises.

- According to a 2024 analysis, telco mergers and acquisitions involving data centres have increased significantly. While there were just over 20 deals annually in 2019 and 2020, the numbers rose to 63 in 2022 and 48 in 2023.

Regulatory Changes and Mobile licensing adjustments: Regulatory environments are shifting in response to market dynamics and evolving technology landscapes.

- The mobile license of “Stage X”, stated to be South Korea’s fourth mobile operator, was cancelled for being unable to meet legal requirements. The Malaysian Government awarded U Mobile a license to build the country’s second 5G network, aiming to accelerate nationwide 5G deployment alongside Digital Nasional Berhad (DNB).

- Orange Egypt, Vodafone Egypt, e& Egypt were awarded 5G licenses by Egypt’s National Telecom Regulatory Authority (NTRA), thereby paving way for digital advancement.

- Meanwhile Iraq’s Government selected Vodafone to establish a government-owned 5G network.

AI-Powered service enhancements and efficiency gains: As AI becomes vital for operational efficiency, telcos are embedding it into core functions.

- Softbank partnered with Ericsson to explore AI integration with RAN to enhance network efficiency. The telco also introduced AITRAS to enhance AI capabilities on 5G networks, leveraging AI-RAN technology.

- SK Telecom partnered with Samsung to leverage AI to optimize 5G base station performance. Verizon integrated AI and machine learning to enhance fibre network protection by integrating to prevent accidental fibre cuts.

- Vodafone Idea (Vi) in India uses HCL Augmented Network Automation (HCL ANA) powered by AI to streamline the management of its complex, multi-vendor, multi-technology network for efficient operations.

Telcos and satellite companies’ collaboration gains momentum: The telco-satellite market has experienced significant momentum over the past two years, driven by efforts to establish ubiquitous connectivity through the integration of terrestrial and non-terrestrial networks.

- Leading telecom providers are partnering with satellite companies like AST SpaceMobile, Starlink, and Intelsat. AT&T and AST SpaceMobile have agreed to deliver a space-based broadband network by 2030. T-Mobile plans to launch Cellular Starlink Service in 2025, inviting users for beta testing, while Rogers introduced SpaceX’s Direct-to-Cell Service (4G LTE) in Canada in 2024.

- KDDI and SoftBank have collaborated with Starlink and Intelsat, respectively, to introduce satellite-based cellular connectivity services.

5G, Network Evolution, and legacy network decommissioning: With the rise of 4G and 5G technologies, legacy 2G and 3G networks are being gradually phased out as telecom operators modernize infrastructure to expand 5G coverage.

- Deutsche Telekom announced to retire its 2G network by 2028, while Telstra and Optus shut down their 3G networks in October 2024.

- In Saudi Arabia, Zain and Saudi Telecom Company (STC) aim to phase out 3G by 2025. In the UAE, major operators Etisalat and du have already significantly reduced 3G usage, with Etisalat set to fully decommission 3G by 2025.

- Leading telcos like Orange, Telecom Italia, and Movistar also plan to phase out 3G networks starting in 2025, aligning with the broader transition to 4G and 5G.

Revenue analysis of Global telcos: FY-2024

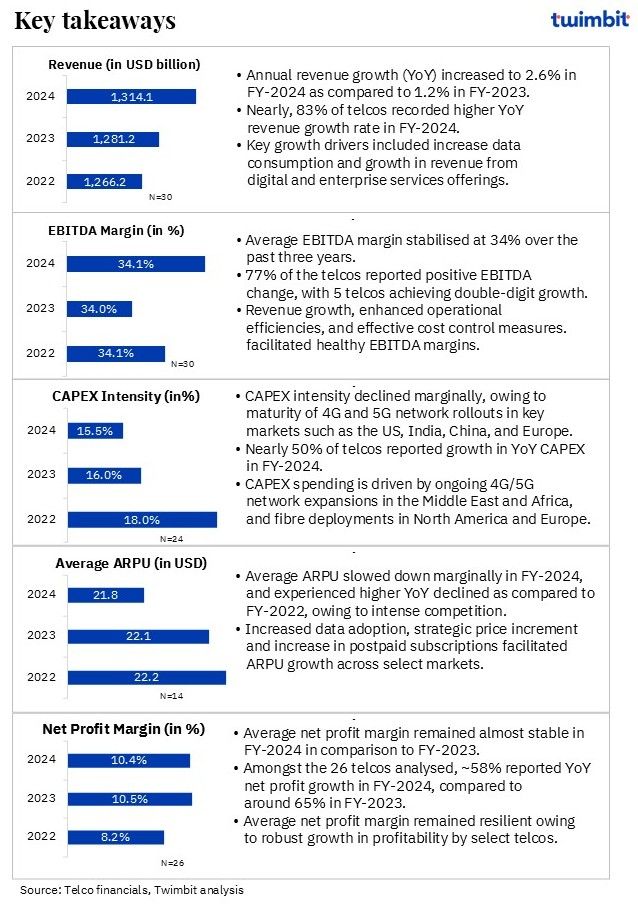

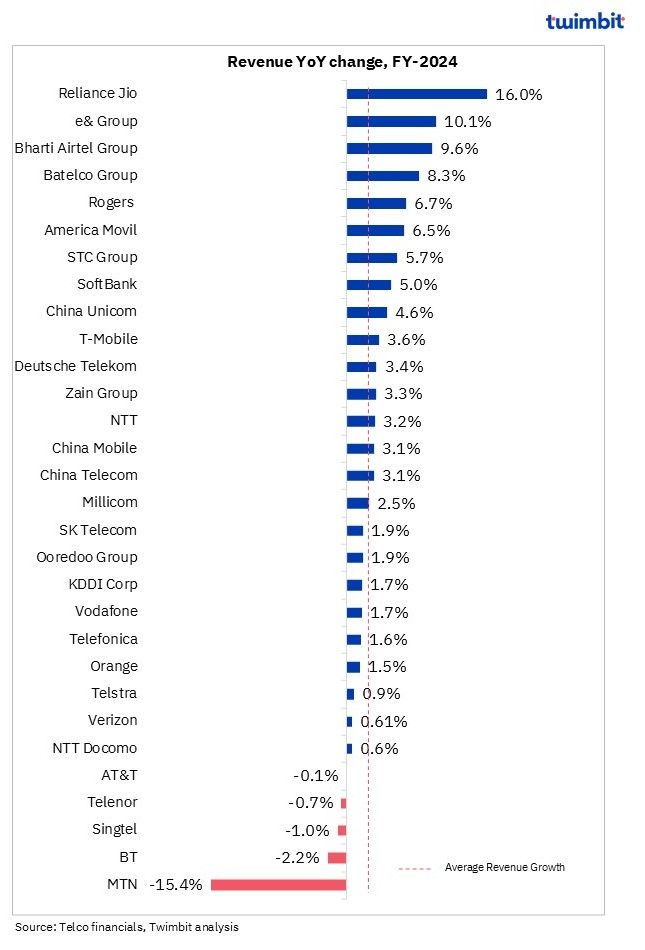

Average annual revenue growth for leading global telcos increased to 2.6% in FY-2024 as compared to 1.2% in FY-2023.

Nearly 83% of telcos recorded positive YoY revenue growth rates in FY-2024 as compared to ~80% in FY-2023. Cumulatively, this accounted for a total revenue of ~USD 1.3 trillion in FY-2024, representing an incremental growth of ~USD 33 billion.

Exhibit 1: Revenue trends for Global telcos, FY-2024

Key highlights

- Increased data usage facilitated by adoption of 4G/5G services facilitated growth in select markets like India and Zain Group operating subsidiaries.

- Enhanced ARPU through strategic focus on postpaid services, including bundled offerings and premium plans facilitated growth for telcos in Americas region.

- Substantial revenue contributions from digital services and enterprise solutions, leveraging advanced technologies emerged as revenue growth enabler for telcos like e& Group, KDDI, SoftBank.

- Diversification into international markets to mitigate risks associated with domestic market saturation. Increasing revenue contribution from geographic subsidiaries contributed to revenue growth for America Movil and Ooredoo group.

- Chinese telcos have faced slowing revenue growth over the past three years due to challenges in monetizing 5G amid intense competition. However, they have sustained growth by focusing on enterprise and digital services, including smart cities, data centre, cloud, and AI. In FY-2024, China Unicom’s Computing and Digital Smart Applications (CDSA) saw a 9.6% YoY increase, whereas China Mobile’s Business Market segment grew 8.8% YoY. Industrial Digitalization revenue rose 5.5% YoY for China Telecom.

Increase data usage and subscriber base expansion: Surging data usage and expanding subscriber base fuelled revenue growth, as telcos target new markets and monetize data with 4G/5G and tariff strategies.

- Reliance Jio’s revenue grew 16% YoY in FY-2024 to USD 14.7 billion (INR 1.2 trillion), driven by sustained tariff hikes and an improved subscriber mix. The rise in data consumption, with 5G subscribers reaching 170 million and data usage oaring to 32.3 GB per user per month, facilitated this growth.

- Bharti Airtel Group’s revenue increased 9.6% YoY in FY-2024 to USD 19.4 billion (INR 1.6 trillion), supported by overall subscriber growth (including strong growth in postpaid subscribers), data monetization, and tariff optimization resulting in incremental ARPU. Data usage per customer surged to 24.5 GB/month. The growth was also facilitated by the better performance of its Africa operations.

- Zain Group also reported strong performances across its operations in Iraq, Bahrain, Jordan, and KSA, with implied subscriber growth contributing to this success. Additionally, increased adoption of data and digital services across most of its operating geographies also propelled overall revenue growth.

Postpaid segment expansion: Growth in the postpaid subscribers also enhanced ARPU growth and revenue stability for telcos, as telcos focussed improving the subscriber mix through prepaid to postpaid migration.

- Rogers’s revenue grew 6.7% YoY to ~USD 15.1 billion (CAD 20.6 billion) facilitated by 3.6% YoY growth in wireless segment, which accounted 51.5% of the overall revenue in FY-2024. Postpaid phone subscribers rose 2.3% YoY, countering prepaid losses and supporting ARPU with lower churn.

- Millicom’s revenue grew 2.5% YoY to USD 5.8 billion in FY-2024, facilitated by overall subscriber growth. Overall subscriber grew 2.1% YoY to 41.5 million in FY-2024, with a 13.5% postpaid surge in postpaid segment, lifting ARPU via price increases and migration initiatives.

- Verizon’s revenue grew 0.6% YoY to USD 134.8 billion in FY-2024, facilitated by growth in Consumer segment. Growth of 1.4% in Wireless Retail Postpaid connection alongwith net-addition of 900,000 postpaid phones in FY-2024 (owing to adoption of myPlan offering, coupled with promotional offers and bundled plans including 5G and streaming services, attracted more customers and boosted ARPU).

- T-Mobile’s postpaid base grew 6.2% YoY, though ARPU edged down due to promotions, despite a 2% postpaid phone ARPU rise from premium plans.

Digital and Enterprise services adoption: A key revenue driving factor for telcos was growth in Digital and Enterprise segment for select telcos, as they strive to leverage digital services and enterprise solutions like cloud, IoT, and cybersecurity to diversify revenue in a competitive mobile landscape.

- e& Group’s revenue increased 10.1% YoY to USD 16.1 billion (AED 59.2 billion), facilitated by 9% growth in the Enterprise segment revenues, fuelled by cloud and cybersecurity growth.

- Softbank’s revenue increased 5% YoY in FY-2024 to USD 42.2 billion (JPY 6.4 trillion), facilitated by 16% growth in the enterprise segment led by business solutions offerings, signalling strong B2B demand.

- KDDI’s revenue increased 1.7% YoY in FY-2024 to USD 38.7 billion (JPY 5.9 trillion) with enterprise segment being a key revenue growth driver. Enterprise revenue increased 14.3% YoY in FY-2024, contributing 19.3% to total revenue, as compared to 17.2% in FY-2023.

- MTN’s Digital and Enterprise revenue 18.8% and 28.2% respectively YoY, driven by gaming, video, cloud, and IoT in South Africa, Nigeria, and Ghana.

International and subsidiary performance: International operations facilitated telcos offset domestic saturation, with subsidiaries in emerging markets boosting revenue growth.

- America Movil reported 6.5% YoY revenue growth in FY-2024 to USD 47.7 billion (MXN 869 billion), led by revenue growth across all its operating geographies including Mexico, Brazil, Colombia, Argentina, which offset the minor declines in Ecuador and Peru.

- STC Group’s revenue increased 5.7% YoY in FY-2024 to USD 20.3 billion (SAR 75.9 billion), supported by operations in Bahrain and Kuwait, highlighting a diversified approach.

- Ooredoo Group’s revenue increased 1.9% YoY in FY-2024 to USD 6.5 billion (QAR 23.6 billion) facilitated by growth in geographies like Iraq, Algeria, Kuwait, Tunisia, and Maldives.

Decline in legacy business and Operational challenges: Revenue setbacks from legacy tech phase-outs and geopolitical challenges push telcos to adapt strategically to sustain growth.

- MTN’s revenue declined 15% YoY to USD 10.3 billion (ZAR 188 billion), impacted by ongoing conflict in Sudan and continued weaking of Nigeria’s currency (Naira).

- Telenor’s revenue declined 0.7% YoY to USD 7.4 billion (NOK 80 billion) owing to decline in Infrastructure segment revenue, which was impacted due to Sweden’s 3G sunset and Norway’s legacy services decline.

- AT&T’s revenue declined 0.1% YoY to USD 122.3 billion in FY-2024, due to decline in Business wireline and equipment revenue, despite 1.0 million fibre and 1.7 million postpaid phone additions during the period.

EBITDA analysis of Global telcos: FY-2024

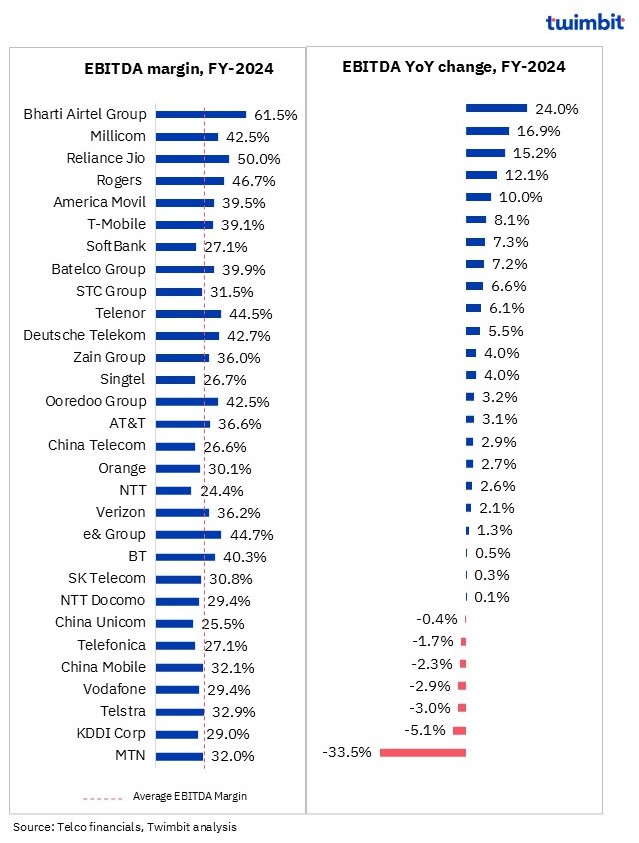

Average EBITDA margin for the leading global telcos stabilised at 34% levels in FY-2024

Robust revenue growth coupled with improved operations, cost control measures and operational efficiency initiatives resulted in YoY EBITDA growth for ~77% of the analysed telcos. Nearly 43 % of telcos reported a slight EBITDA variation, within a manageable range (-3% to +3%).

Exhibit 2: EBITDA and EBITDA margin trends for Global telcos, FY-2024

Key highlights

- Strong revenue growth and improved operations contributed to strong EBITDA growth for Indian telcos Bharti Airtel and Reliance Jio, as well as America Movil.

- Increased cost savings and optimization efforts led to EBITDA growth for like Millicom and Deutsche Telekom

- Rogers benefited from synergy realization related to the Shaw Transaction and ongoing cost efficiencies, which facilitated EBITDA growth.

- In China, telecom operators such as China Unicom and China Telecom experienced EBITDA decline. China Mobile’s EBITDA declined due increased operating expenses.

- Macroeconomic factors, including currency fluctuations, higher inflation, and rising costs, negatively impacted EBITDA growth for telecom companies like MTN and Telefonica.

Revenue growth and cost efficiency: Leading telcos witnessed increase in EBITDA, primarily driven by revenue growth and strategic cost-saving initiatives. Telcos are leveraging these efficiencies to enhance their financial performance and market competitiveness.

- Bharti Airtel Group reported a 24% YoY EBITDA growth in FY-2024, largely attributed to its thriving Indian operations, maintaining a stable EBITDA margin of 49.4%.

- Reliance Jio achieved a remarkable 15.2% YoY EBITDA increase in FY-2024, fuelled by robust revenue growth and optimal utilization of operating capacities.

- Millicom’s EBITDA grew 16.9% YoY in FY-2024, led by strategic revenue enhancements and cost-saving efficiency programs.

- SoftBank’s EBITDA grew 7.3% YoY in FY-2024 facilitated by overall revenue growth as well as rise in operating income.

Operational efficiencies and Strategic synergies: A focus on operational efficiencies and strategic synergies is propelling EBITDA growth, as companies streamline operations and capitalize on merger benefits.

- Rogers reported EBITDA growth of 12.1% YoY in FY-2024, benefitting from the full realization of synergies from the Shaw Transaction, alongside ongoing cost efficiencies, with positive EBITDA growth across Wireless, Cable, and Media segments.

- Ooredoo Group’s enhanced its EBITDA growth by 3.2% YoY in FY-2024, through a sustained focus on operational efficiencies.

Strong regional operations: Telcos with robust regional operations also experienced significant EBITDA growth, supported by stable margins and increased revenue across diverse markets.

- America Movil improved its EBITDA by 10% YoY in FY-2024, facilitated by strong performance in its operations across Mexico, Colombia, and Brazil, effectively offsetting declines in Peru.

- e& Group’s EBITDA grew 1.3% YoY in FY-2024, benefitting from strong telecom operations across its footprint, contributing to EBITDA growth.

Operational and financial challenges: Select telcos faced EBITDA decline due to increased operating expenses and financial impairments, which impacted their overall profitability and necessitating strategic financial management.

- MTN’s overall EBITDA was adversely affected by Sudan impairments and non-operational losses, including a significant loss on the disposal of MTN Guinea-Conakry.

- China Mobile’s EBITDA declined by 2.3% YoY in FY-2024, due to 2.7% YoY increase in its operating expenses.

Regional and segment-specific revenue declines: EBITDA decline for few telcos was due underperformance in specific regions and segments, highlighting the need for strategic adjustments to address these challenges.

- Telefonica’s overall EBITDA declined 1.7% YoY in FY-2024, owing to EBITDA performance challenges in Spain, Brazil, Chile, and Peru.

- Telstra experienced a 3% YoY decline in EBITDA, owing to lower revenue in its Fixed – C&SB and Fixed-Enterprise segments, thereby impacting the EBITDA in the aforesaid segments.

CAPEX analysis of Global telcos: FY-2024

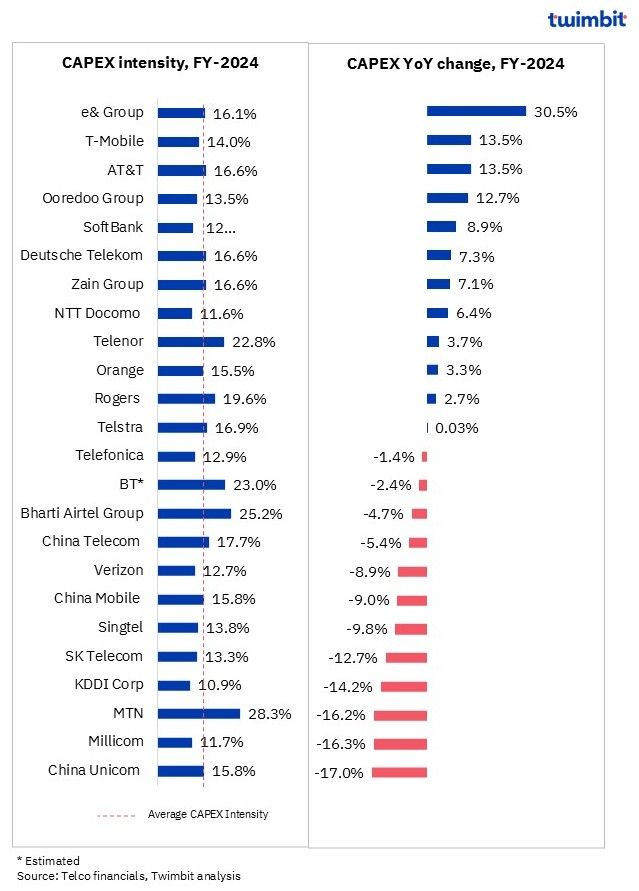

Average CAPEX intensity declined from 16% in FY-2023 to 15.5% in FY-2024, as 4G/5G network deployment reached completion in major markets

Nearly 50% of the 24 telecom companies analysed reported a YoY decline in CAPEX for FY-2024. This reduction is primarily due to the maturity of 4G and 5G network rollouts in key markets such as the US, India, China, and Europe, leading to decreased spending in these regions.

On the other hand, CAPEX investments by telecom operators remain strong, driven by ongoing 4G and 5G network expansions in the Middle East and Africa, fibre deployments in North America and Europe, and growing investments in digital infrastructure, including cloud services, data centres etc.

Exhibit 3: CAPEX and CAPEX intensity trends for Global telcos, FY-2024

Key highlights

- Investment in 4G and 5G network expansion, fibre rollout and digital capability investments continue to drive CAPEX spending in the Middle East region.

- Telcos such as SK Telecom, KT Corp, Softbank, and Singtel are focusing on data centres, cybersecurity, and AI-related investments as key areas of growth.

- In North America, Europe, and India, fibre rollouts have emerged as a primary investment theme, following the peak of wireless investments in FY-2023.

- In China, after substantial 5G investments, telecom operators are concentrating on strengthening digital capabilities, including cloud, big data, IoT, and 5G commercial projects like smart cities, factories, parks, and campuses.

Network expansion and modernization: Investments in network capabilities, including 5G and fibre deployment, are driving CAPEX growth to meet increasing service demands and support business expansion.

- e& Group’s CAPEX increased 30.5% YoY in FY-2024 to USD 2.6 billion (AED 9.5 billion), led by upgradation of network capabilities and frequencies and licenses acquisitions across local and international markets.

- Deutsche Telecom’s CAPEX grew 7.3% YoY in FY-2024 to USD 20.7 billion (EUR 19.2 billion), driven by network expansion and modernization initiatives, including 5G and fibre deployment in Europe.

- AT&T’s CAPEX increased 13.5% YoY in FY-2024 to USD 20.3 billion, as it prioritized fibre expansion to enhance network capacity and service offerings.

Data Centre and Connectivity expansion: Telcos are investing in data centre expansion and subsea cable systems to establish themselves as leaders in global connectivity.

- Ooredoo Group’s CAPEX increased 12.7% YoY in FY-2024 to USD 872.4 million (QAR 3.2 billion), as it focused on expanding data centre capacity and subsea cable systems to enhance global connectivity.

- Zain Group’s CAPEX increased 7.1% YoY in FY-2024 to ~USD 1.1 billion (KWD 327.5 million), as it focussed on 5G expansion, LTE enhancements and digital infrastructure investments.

Efficient capital deployment and prior investment impact: Previous significant investments in network infrastructure and strategic focus on efficient capital deployment and network investments has led to a reduction in CAPEX for some telcos.

- China Unicom experienced a decline in CAPEX due to a significant reduction of ~48% in Connectivity and Communications expenses, resulting in overall CAPEX declining by 17% YoY in FY-2024 to USD 8.5 billion (CNY 61.4 billion).

- Millicom’s CAPEX declined 16.3% YoY in FY-2024 to USD 677.4 million, owing to more efficient capital deployment and focused network expansion investments.

- MTN’s reported 16.2% decline in its CAPEX on YoY basis in FY-2024 to USD 2.9 billion (ZAR 53.3 billion) following lease modifications and planned reductions in deployment, particularly in Nigeria.

- China Telecom’s overall CAPEX declined 5.4% YoY in FY-2024 to USD 13 billion (CNY 93.5 billion), due to reduced spending on mobile networks. CAPEX spending on mobile networks reduced to 29% of overall CAPEX in FY-2024 as compared to 32% in FY-2023.

- Bharti Airtel Group’s CAPEX declined 4.7% YoY in FY-2024 to USD 4.9 billion (INR 409.5 billion), due to substantial investments made in previous years for 5G network deployment and infrastructure expansion in India.

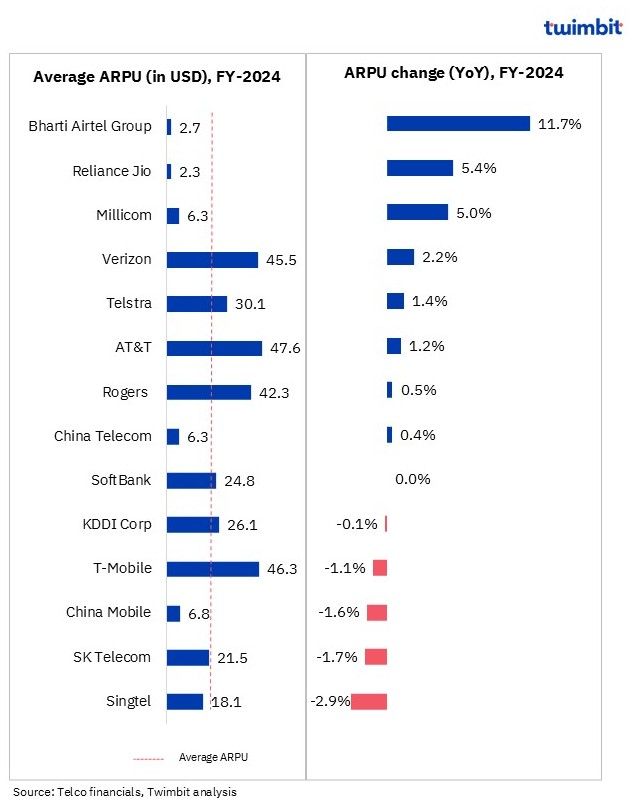

ARPU analysis of Global telcos: FY-2024

Average ARPU declined marginally by 1.5% YoY in FY-2024 to USD 21.8

- Nearly 60% of the analysed telcos reported YoY ARPU growth in FY-2024, increased data adoption, strategic price increment and increase in postpaid subscriptions.

- The growing data (4G/5G) subscriber mix, and price increase initiated in Jul-2024 have increased ARPU for Indian telcos.

- Healthy postpaid subscriber contributions resulted in the ARPU growth for the telcos in the Americas, including Verizon, AT&T and Millicom.

- Intense competition has impacted the ARPU levels of telcos in China, as telcos are under pressure to keep the prices low.

- Increased data and digital services usage in Middle East countries facilitated the ARPU growth for telcos in Middle East region.

Exhibit 4: ARPU trends for Global telcos, FY-2024

Key highlights

Telcos are continually refining strategies to sustain a balanced ARPU amid digital transformation and economic shifts. In FY-2024, ARPU performance varied significantly across different geographies. Key factors driving these results include the adoption of data services, innovative pricing strategies, improving postpaid subscriber mix and varying economic conditions, with each telco tailoring its approach to its unique market environment.

India: Surge in data usage and postpaid growth – In India, the impact of tariff hikes by major telcos is becoming increasingly evident, with a noticeable rise in ARPU. The migration of subscribers from 2G to 4G/5G networks and an increase in postpaid subscribers are likely to further boost average data usage per customer.

- Bharti Airtel saw its ARPU grow to USD 2.7 (INR 224.4) in FY-2024, supported by strong postpaid growth, data monetization, and tariff optimization. Data usage per customer surged to 24.5 GB/month.

- Reliance Jio experienced an ARPU increase to USD 2.3 (INR 190.5), driven by sustained tariff hikes and an improved subscriber mix. The rise in data consumption, with 5G subscribers reaching 170 million and data usage oaring to 32.3 GB per user per month, facilitated this growth.

Americas: Postpaid expansion and Strategic pricing – In the Americas, telcos like AT&T, Verizon, Rogers, and Millicom witnessed improvements in ARPU levels, fueled by an increase in postpaid subscriber counts and strategic pricing adjustments.

- AT&T added 1.7 million postpaid phone subscribers in FY-2024, resulting in a ~2% YoY growth in postpaid phone subscribers. The growth in postpaid ARPU, along with moderated churn, contributed to a 1.5% YoY increase in mobility revenues.

- Verizon added 900,000 postpaid phones during FY-2024. The adoption of its myPlan offering, coupled with promotional offers and bundled plans including 5G and streaming services, attracted more customers and boosted ARPU.

- Millicom saw its subscriber count rise by 2.1% YoY to 41.5 million, led by a 13.5% increase in postpaid subscribers. ARPU growth was driven by nominal price increases and efforts to migrate customers from prepaid to postpaid segments.

- Rogers achieved a 2.3% YoY growth in postpaid phone subscribers, offsetting declines in the prepaid segment. The growth in postpaid subscribers and reduced churn facilitated ARPU growth.

- T Mobile, however, witnessed a marginal decline in ARPU in FY-2024 on YoY basis, despite a 6.2% increase in Postpaid customers on YoY basis. However, the 2% increase in Postpaid phone ARPU led by Higher premium services, primarily high-end rate plans were partially offset by increased promotional activity, including the success of bundled offerings.

China: Navigating competitive pressures – In China, intense competition has exerted downward pressure on ARPU levels as telcos strive to maintain competitive pricing.

- China Telecom maintained a stable ARPU at USD 6.3 (CNY 45.6), despite a 10.3% YoY increase in 5G package subscribers to 351.5 million.

- China Mobile experienced a 1.6% YoY decline in ARPU to USD 6.8 (CNY 48.5), despite a 19% YoY growth in 5G customers. This decline was due to reduced revenue from wireless data traffic and voice services.

Middle East: Embracing Digital and Data services – In the Middle East, telcos saw ARPU growth driven by increased adoption of data and digital services, including FinTech offerings.

- Zain Group reported strong ARPU growth in emerging markets like Iraq (+25%) and Jordan (+7.3%), fueled by increased data and digital services adoption.

- Ooredoo Group saw growth in subscriber counts in Kuwait and Iraq, with ARPU rising by 0.2% and 1.5% respectively, driven by increased data and digital service usage.

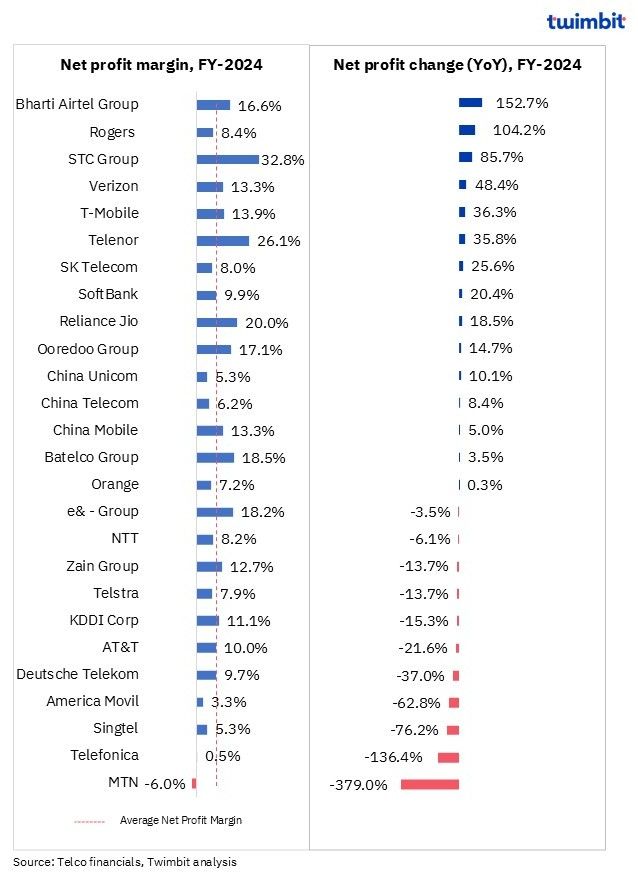

Profitability analysis of Global telcos: FY-2024

Increased expenses coupled with macroeconomic factors outpace revenue growth rates impacting the profitability of telcos

Amongst the 26 telcos analysed, ~58% reported YoY net profit growth in FY-2024, compared to around 65% in FY-2023. However, the average net profit margin remained resilient at 10.4% in FY-2024 as compared to 10.5% in FY-2023, owing to robust growth in profitability by select telcos.

Exhibit 5: Profitability trends for Global telcos, FY-2024

Key highlights

- Strategic asset sales and consolidation: Telcos are leveraging strategic asset sales and consolidations to significantly boost net profits, reflecting a keen focus on optimizing asset portfolios and capitalizing on market opportunities.

- Bharti Airtel Group’s profit surged 152.7% YoY in FY-2024 to USD 3.2 billion (INR 270.7 billion), driven by an exceptional gain from consolidating Indus Towers into Airtel in during Q4-2024.

- STC Group’s net profit grew 85.7% YoY in FY-2024 to USD 6.6 billion (SAR 24.9 billion), due to a USD 3.4 billion (SAR 12.9) billion gain from the sale of its controlling interest in subsidiaries TAWAL and Digital Infrastructure Company.

Operational efficiency and cost management: Enhanced operational efficiency and strategic cost management emerged as net income growth drivers, as telcos streamline operations and reduce expenses.

- Rogers reported 104.2% YoY growth in net income in FY-2024 to ~USD 1.3 billion (CAD 1.7 billion), primarily due to higher adjusted EBITDA and lower restructuring, acquisition, and other costs.

- Verizon net income grew 48.4% YoY in FY-2024, owing to reduced operating expenses, attributed to lower costs of services and wireless equipment.

Impairment reversals and financial adjustments: Reversals of impairments and strategic financial adjustments contributed to net income growth, highlighting the importance of financial agility in the telecom sector.

- Telenor’s net income grew 35.8% YoY to USD 1.9 billion (NOK 20.9 billion) in FY-2024, owing to a reversal of impairment related to True Corporation in FY-2023.

Increased operating and financing costs: Rising operating and comprehensive financing costs resulted in net profit decline, underscoring the challenges of managing expenses in a dynamic market environment.

- America Movil’s net profit declined -62.8% YoY in FY-2024, due to higher comprehensive financing costs, with significant foreign exchange losses.

- AT&T profit declined 21.6% YoY in FY-2024 to USD 12.2 billion, due to higher operating costs, including accelerated depreciation on wireless network equipment and increased device costs.

- MTN’s net profit saw a significant decline in FY-2024, primarily due to a USD 260.8 million (N400.4 billion) after-tax loss from its Nigerian operations. The company’s financial performance was further strained by record-high inflation and the devaluation of the naira, which increased operational expenses.

Impact of prior year’s gains: The absence of significant gains from the previous year impacted on current net profit figures, highlighting the volatility and challenges in maintaining consistent profit growth.

- Deutsche Telekom’s net profit declined 37% YoY in FY-2024, primarily due to the absence of gains from the deconsolidation of GD Towers in the prior year.

- Singtel experienced a 76.2% YoY decline in net profit, attributed to the absence of a one-off gain of ~USD 897 million (SGD 1.2 billion) from the previous year’s merger of its Indonesian associate Telkomsel with IndiHome.

- Impairments and Write-offs: Impairments and write-offs in specific regions have contributed to net profit declined for specific telcos emphasizing the need for strategic adjustments in asset management.

- Telefonica experienced a 136.4% YoY decline in net profit for FY-2024, primarily due to impairments related to its Latin American operations in Argentina, Peru, and Chile, following a write-off exceeding USD 2.1 billion (EUR 2.1 billion) in Q4-2024.

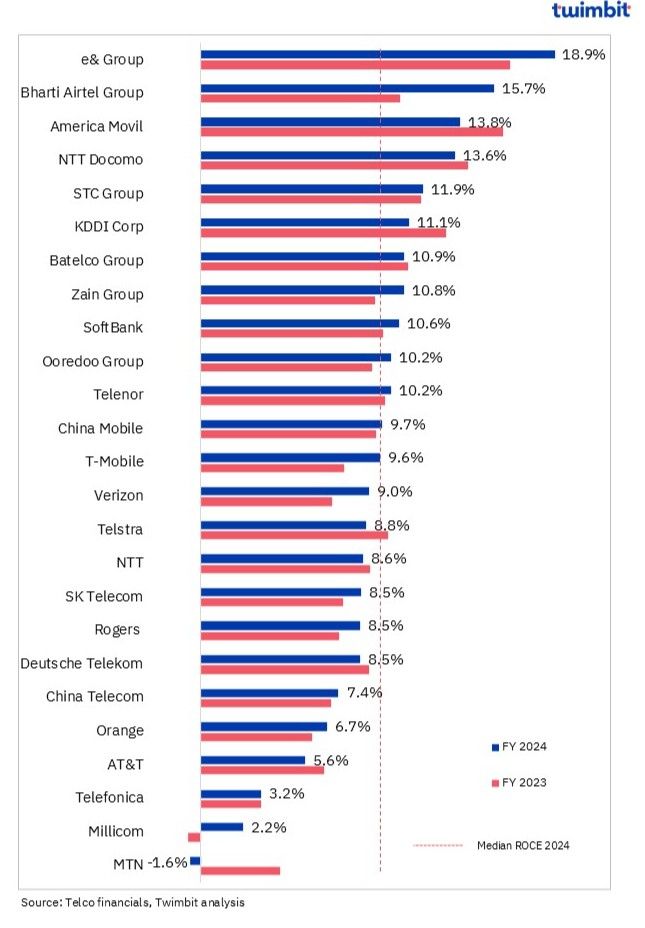

ROCE trends of Global telcos: FY-2024

ROCE improves for most of the Global telcos in FY-2024, indicating better capital utilisation

ROCE improved for ~60% of the telcos in FY-2024, with median ROCE being 9.7% in FY-2024, slightly higher as compared to 9.4% in FY-2023.

Growth in revenue alongwith increased profitability (due to a reduction in expenses) resulted in positive ROCE growth for majority of the telcos.

Exhibit 6: ROCE trends for Global telcos, FY-2023 and FY-2024

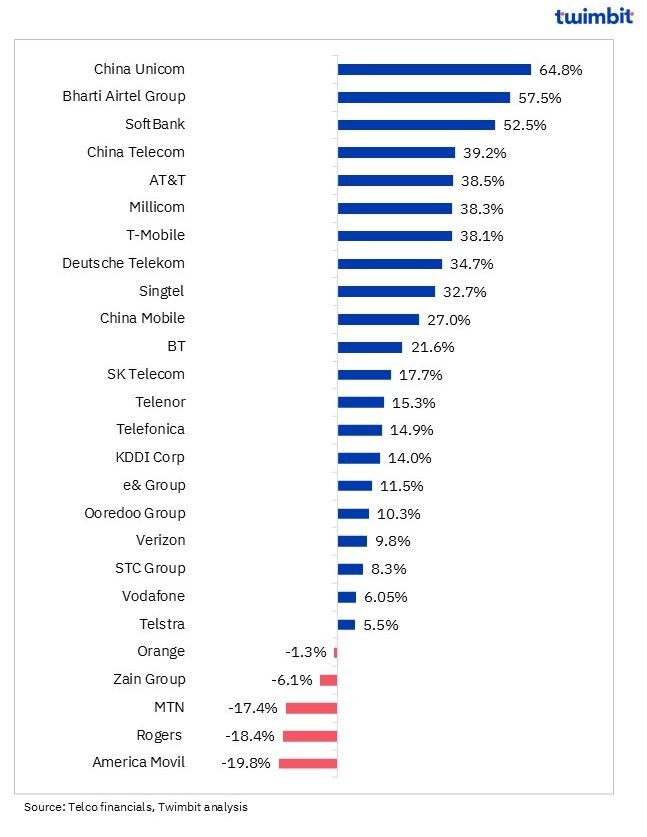

Total Shareholder Return of Global telcos: FY-2024

Total Shareholder Return (TSR) improves for majority of the leading global telcos in FY-2024, indicating better revenue growth and dividend payout

Nearly 81% of the telcos (including group conglomerates) reported positive Total Shareholder Return (TSR) in FY-2024.

An increase in share prices, coupled with dividend payouts, enhanced TSR; 80% of the 25 dividend-paying telecom companies experienced positive TSR.

Telcos in emerging markets, especially in Asia, are outperforming mature markets, with telecom companies from China and India leading the top TSR rankings.

China Unicom leads with a TSR of 64.8%, driven by its strong financial growth and pioneering role in 5G-Advanced technology.

Bharti Airtel Group’s TSR of 57.5% reflects its successful 5G expansion and strong market position in India’s dynamic telecommunications sector.

Exhibit 7: TSR for Global telcos, FY-2024

Key strategic developments: Q4-2024

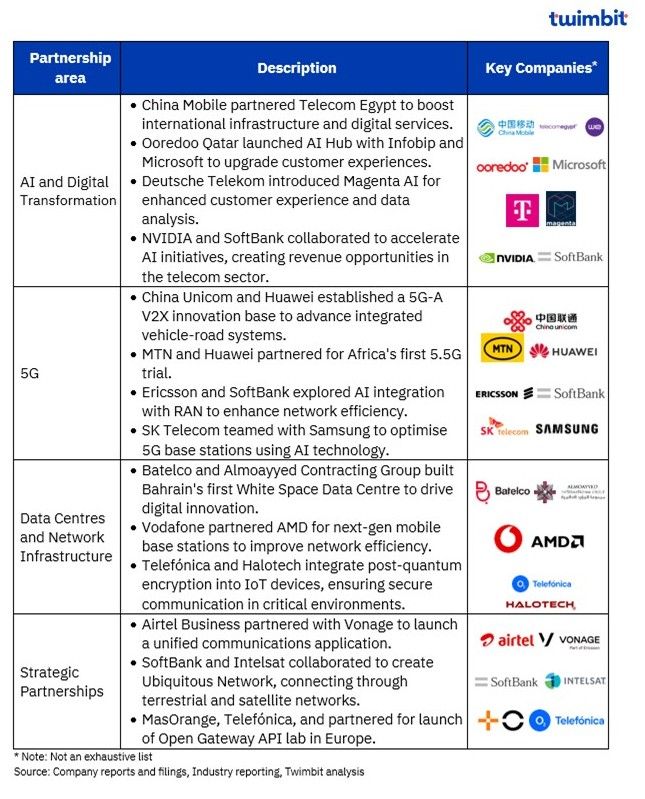

Key strategic partnerships and alliances: Q4-2024

Global telcos are making significant strides in AI integration, 5G innovations, digital transformation, data centres, and network infrastructure. These strategic partnerships and technological innovations, aim to enhance connectivity, improve customer experience, and drive digital transformation worldwide.

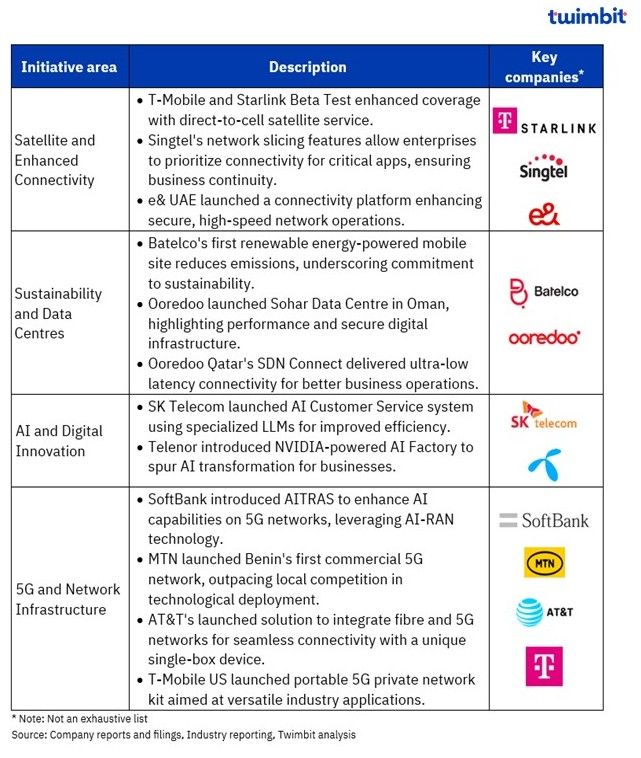

Key strategic initiatives: Q4-2024

Global telcos continue to spearhead innovative initiatives, including breakthroughs in AI integration, satellite connectivity enhancements, pioneering sustainable infrastructure, and launching cybersecurity solutions, aimed at driving digital transformation and improving global connectivity.

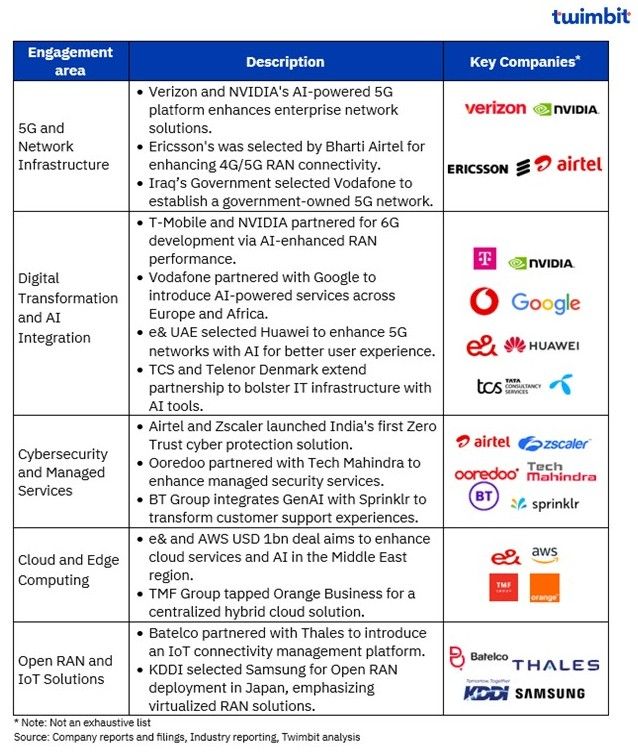

Key contract wins: Q4-2024

Global telcos are experiencing transformative developments with significant advancements in 5G deployment, digital transformation, AI integration, network infrastructure, and cybersecurity.

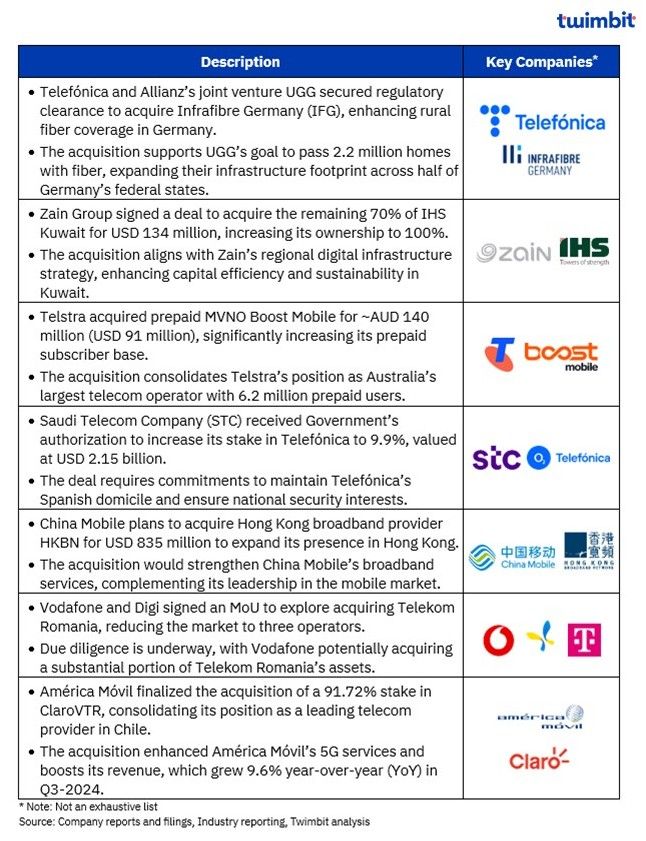

Key M&As and Divestures: Q4-2024

Global telcos are actively strengthening their positions through acquisitions, focusing on expanding infrastructure, enhancing service offerings, and realizing cost efficiencies. These mergers aim to boost market presence, improve operational scale, and create long-term value in an increasingly competitive industry.

Research Methodology and Assumptions

- The “Global telcos performance benchmarks: Winter 2025” report presents key findings on the performance of 30 strategically selected leading telcos across diverse geographies, offering a comprehensive global perspective on telco performance. Key performance metrics analysed include Revenue, EBITDA, CAPEX, ARPU, Profitability, ROCE and TSR for the period January – December 2024.

- This report leverages data acquired from telecommunications companies and includes extensive secondary research. Twimbit adopted a calendar year approach for data analysis, where FY signifies the period from January to December.

- To ensure consistency and facilitate accurate comparisons, a constant currency conversion rate representing the average USD exchange rate for the period January – December 2024 has been applied throughout the report.

- The report evaluates Revenue and EBITDA for 30 telcos. CAPEX and ARPU analyses cover data from 24 and 14 companies, respectively. Net profitability, ROCE and TSR assessment has been included for 26, 25 and 26 telcos respectively.

- Blended mobile ARPU has been incorporated wherever relevant to provide a more holistic view.

- The data presented in this report is based on the most current information available at the time of compilation. As such, it may not reflect subsequent developments. This report is intended for informational purposes only and should not be relied upon as a substitute for independent research.