Key Takeaways

- The high maturity of 5G deployments and a slowdown in consumer spending impacted the revenue growth of telecom vendors.

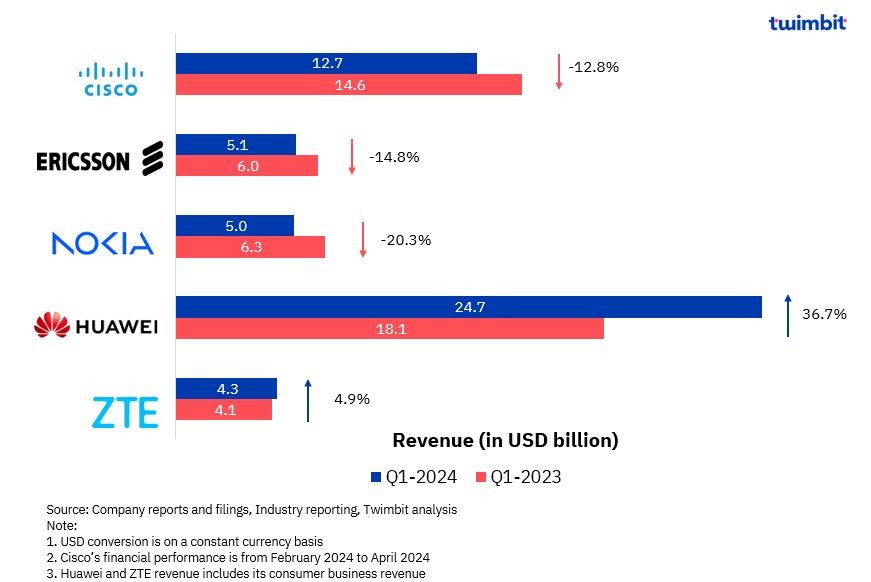

- The top 5 telecom vendors’ annual revenue reached USD 51.9 billion in Q1-2024. The revenue growth witnessed a modest decline of 20 bps to reach 5.7% YoY in Q1-2024 compared to YoY growth of 5.9% in Q1-2023.

- Huawei and ZTE sustained revenue growth in Q1-2024, whereas revenue declined for Cisco, Ericsson and Nokia.

- Diversification into areas apart from core network offerings such as AI, cloud computing and other digitalisation projects has facilitated revenue growth for Huawei and ZTE.

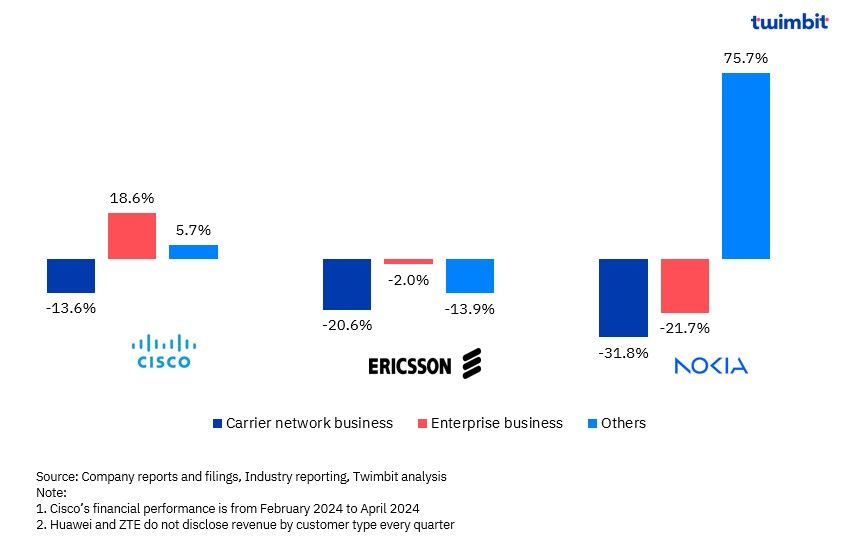

- Carrier Network revenue declined for all the vendors, while the enterprise segment experienced mixed results, with Cisco witnessing revenue growth.

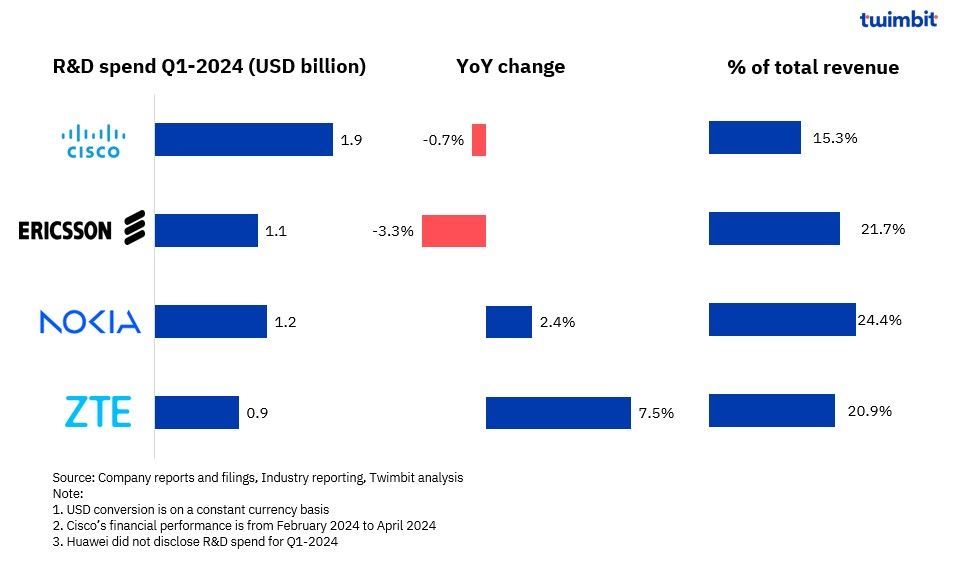

- R&D expenses grew for Nokia and ZTE but declined for Cisco and Ericsson.

- All major vendors are positioning themselves as full-stack ICT providers to further drive revenue growth instead of being equipment suppliers.

- AI is quickly becoming a key focus area as growth shifts towards software and services related to network management and optimisation.

- Cisco’s revenue declined by 12.8% YoY due to weak customer spending across all the regions.

- Ericsson’s revenue fell by 14.8% YoY due to lower sales in North America and APAC, coupled with carrier network challenges.

- Nokia’s revenue declined by 20.3% YoY due to carrier network issues and weakness in the Americas and APAC region.

- Huawei’s revenue surged 36.7% YoY, driven by a strong recovery in the consumer segment and growing contribution from new businesses.

- ZTE’s revenue grew 4.9% YoY as it capitalised on opportunities arising from China’s digital transformation and artificial intelligence applications.

Financial Performance

Huawei and ZTE lead in revenue growth, with the top 5 telecom vendors recording a rise of 5.7% in Q1-2024 (slightly lower compared to Q1-2023)

The top 5 telecom vendors’ revenue grew by 5.7% YoY (year-on-year) in Q1-2024 to USD 51.8 billion, led by positive contributions from Huawei and Cisco. This growth was slightly lower than the 5.9% YoY growth rate in Q1-2023, as 5G deployment nears completion in most developed markets.

The revenue performance of these vendors during Q1-2024 can be summarised as follows:

- Revenues for Huawei and ZTE grew by 36.7% and 4.9%, respectively

- Cisco, Ericsson and Nokia’s revenues declined by 12.8%, 14.8%, and 20.3%, respectively

Exhibit 1: Leading telecom vendor revenue trends YoY basis, Q1-2024

5G maturity in developed markets such as North America, Europe and India has caused a slowdown in investments among telecom vendors. As a result, the carrier network business of Cisco, Ericsson and Nokia faced challenges in Q1-2024. Diversification into areas apart from core network offerings such as AI, cloud computing and other digitalisation offerings enabled APAC vendors (Huawei and Cisco) to negate the impact of 5G CAPEX reductions by the major telcos based in China.

Exhibit 2: Leading telecom vendor revenue trends by customer type, Q1-2024

Cisco

- Q1-2024 revenue declined by 12.8% YoY to USD 12.7 billion (steepest decline since 2009).

- This is primarily due to the decline in product revenue (18.6%), which offsett the growth in services revenue (5.7%).

- Carrier network business represents 51.3% of the total revenues.

- 13.6% YoY decline to USD 6.5 billion due to reduced consumer spending.

- Enterprise business represents 19.7% of total revenues.

- 18.6% YoY growth to USD 2.5 billion due to enterprise and cloud market weaknesses.

- Revenue momentum remains positive in software-heavy segments in Q1-2024.

- Security grew by 36.1%

- Collaboration grew by 0.2%

- Observability grew by 26.3%

- The acquisition of Splunk (completed in March 2024) contributed USD 413 million in revenue in Q1-2024, bolstered Cisco’s software portfolio and increased ARR (annual recurring revenue) by ~USD 4.2 billion post-acquisition.

- Total ARR (annualised recurring revenue) increased ~22% YoY to USD 29.2 billion, and product ARR increased ~44% YoY to USD 15.5 billion.

- Total subscription revenue (including Splunk) grew 12% YoY to USD 6.9 billion, whereas it grew 5% YoY without Splunk.

- Cisco’s product ARR grew 44% YoY to USD 15.5 billion, whereas it grew 9% YoY without Splunk.

- The acquisition of Isovalent, an open-source cloud-native networking and security provider, strengthened Cisco’s secure networking capabilities across public clouds. Security revenue increased 36.1% YoY to reach USD 1.3 billion.

- Cisco named Gary Steele (CEO of Splunk) as President of Go-to-Market with immediate effect. Gary would collaborate with Chuck Robbins (Chairman and CEO of Cisco) to execute Cisco’s strategic plans and goals, leading the Splunk team through its integration process with Cisco.

- Cisco and Splunk sales teams are collaborating for cross-selling and upselling combined solutions to ~5,000 customer accounts that have the potential to become meaningful Splunk customers.

Ericsson

- Q1-2024 revenues declined by 14.8% YoY to USD 5.1 billion (SEK 53.3 billion).

- Carrier network business represents 63.2% of total revenues.

- Revenue for the segment declined by 20.6% YoY to USD 3.2 billion (SEK 33.7 billion).

- Revenues from South East Asia, Oceania and India declined by ~42%, which negated the growth in North America, Europe and Latin America.

- Enterprise business represents 35.7% of total revenues.

- Revenues declined by ~2.0% to USD 1.8 billion (SEK 19 billion)

- Cloud software and service revenues declined 2.6% YoY to ~USD 1.3 billion (SEK 13.0 billion)

- This drop was primarily in Managed Network Services due to descoping and contract exits.

- Enterprise revenue declined 0.4% YoY to USD 574.3 million (SEK 5.9 billion). This drop was attributed to reduced Global Communications Platform sales, influenced by the company’s decision to scale back operations in select countries to comply with legal requirements. Additionally, revenue growth was impacted by the loss of low-margin customer contracts, as announced by the company in Q4-2023.

- Intellectual property rights (IPR) licensing revenue rose ~24% to USD 240.5 million (SEK 2.5 billion) because of a new contract signed in the quarter, including retroactive revenue for unlicensed periods.

- Ericsson expects the sales to stabilise during H2-2024, driven by its recent contract wins and normalisation of the customer inventory levels in North America.

Nokia

- Q1-2024 revenue declined by 20.3% YoY to ~USD 5.0 billion (EUR 4.7 billion) due to weaknesses in Network Infrastructure, Mobile Networks, and Cloud and Network services segments.

- Carrier network business accounted for 69.3% of total revenue in Q1-2024.

- Revenue declined 31.8% YoY to USD 3.5 billion (EUR 3.2 billion) due to low spending levels in the Americas and India.

- Network infrastructure sales declined ~26% YoY to USD 1.8 billion (EUR 1.7 billion) due to macroeconomic uncertainty, customer spending re-evaluation and inventory consumption limitations.

- IP Networks segment declined by 24% YoY.

- Optical Networks segment declined by 35% YoY.

- Fixed Networks segments declined by 23% YoY.

- Mobile network sales declined 39.3% YoY to USD 1.7 billion (EUR 1.6 billion) due to telcos’ normalisation of network deployment across key regions. These include:

- North America: Weak demand due to low deployment activity levels with lower market share at one North American customer.

- India: Moderation in 5G deployments, owing to the significant investment already made in 2023.

- EMEA: slower 5G deployments amidst ongoing macroeconomic uncertainty, offsetting growth in the Middle East and Africa.

- Enterprise segment represents 9.5% of total revenues in Q1-2024.

- Revenues for the segment declined by 21.7% YoY to USD 481.1 million (EUR 443 million).

- This drop was due to inconsistency in revenue inflows from webscale customers.

Huawei

- Q1-2024 revenue 36.7% YoY to reach USD 24.7 billion (CNY 178.5 billion) as the company continues to seize opportunities in digitalisation, intelligence, and decarbonisation.

- Earlier, had reported fastest growth in FY-2023 over the last four years, driven by strong recovery in its consumer segment and growing contribution from new businesses like smart car components, thereby accelerating its recovery from US sanctions.

- The company also reported over five-fold increase in net profit. Net profits increased 564% YoY to reach USD 2.7 billion (CNY 19.7 billion) in Q1-2024.

ZTE

- Revenue increased by 4.9% YoY to USD 4.3 billion (CNY 30.6 billion) in Q1-2024 as it capitalises on the opportunities arising from China’s digital transformation and artificial intelligence applications.

- To cope with complex external environment challenges, ZTE pursues a business strategy of “precision and pragmatism for steady growth”.

- It transitioned from full connectivity to a “connectivity + computing power” provider to expand its addressable market and addresses the challenge arising from reduced CAPEX by China’s telcos.

R&D performance

R&D spending witnessed a muted growth of 0.7% YoY in Q1-2024, led by Nokia and ZTE

Exhibit 3: Leading telecom vendor R&D spending trends, Q1-2024

Cisco

- Cisco’s R&D spending witnessed a modest decline of 0.7% YoY in Q1-2024 to US 1.9 billion, reaching 15.3% of its total revenue.

- R&D expenses declined owing to lower headcount-related expenses and reduced contracted services spending.

- This partially offsets the higher expenses from share-based compensation, cash compensation from acquisitions and higher discretionary spending.

Ericsson

- Ericsson’s R&D expenses declined 3.3% YoY to USD 1.1 billion (SEK 11.6 billion) in FY-2023, representing 21.7% of its revenue.

- This decline was primarily due to cost-reduction initiatives, partly offset by salary increases and higher variable incentive accruals.

Nokia

- To sustain its technology leadership, Nokia’s R&D expenses increased 2.4% YoY to USD 1.2 billion (EUR 1.1 billion), driven by a margin increase in R&D investments in its Mobile Networks and Nokia Technologies segments.

- The R&D allocation as a percentage of revenue increased by 540 bps to 24.3% in Q1-2024.

ZTE

- ZTE’s R&D expenses increased 7.5% YoY in Q1-2024 to USD 0.9 billion (CNY 6.4 billion), accounting for 20.9% of the overall revenue.

- A deep focus on R&D enables ZTE to sustain a strong impetus for business innovation and product enhancement/competitiveness.

- The strong focus is on integrating AI technology with terminals to drive product innovation and intelligent upgrades, thus constructing a smart ecosystem.

Geographic performance

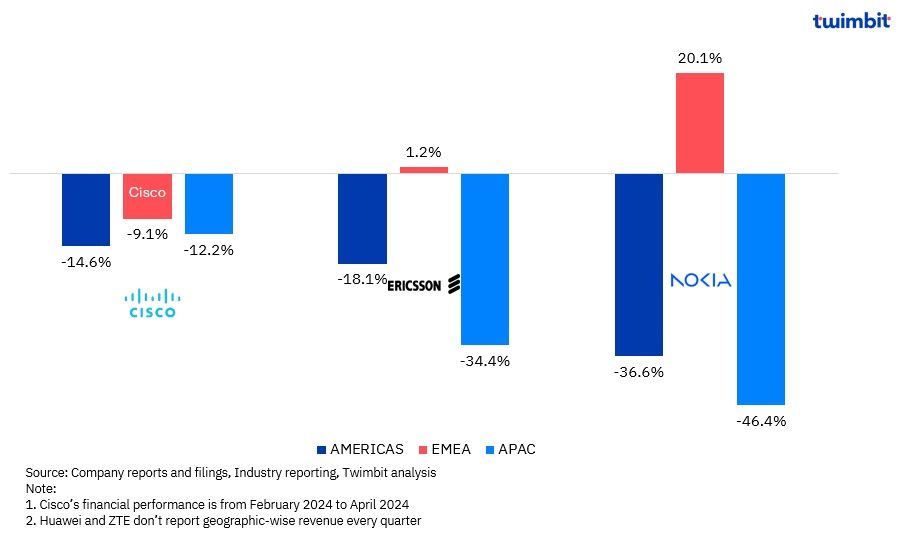

EMEA emerged as the only region with revenue growth, while major telecom vendors witnessed revenue decline in the Americas and APAC region

Exhibit 4: Leading telecom vendor regional revenue trends, Q1-2024

Cisco

- Cisco’s Q1-2024 performance saw revenue decline across all the regions, with the APAC region recording the highest decline of 12.2% YoY.

- Revenue from the Americas region declined 14.6% YoY in Q1-2024 to USD 7.4 billion. This was due to a ~21% decline in product revenue across each of its customer markets.

- Product revenue declined in the United States, Canada, Mexico and Brazil by 21%, 6%, 27% and 18%, respectively, on a YoY basis in Q1-2024.

- EMEA revenue declined by ~9.1% YoY in Q1-2024 to USD 1.4 billion due to a 14% decline in product revenue across each customer market.

- United Kingdom, Germany and France reported a decline of 9%, 18% and 8%, respectively, in product revenue during the period.

- Revenue from the APAC region declined 12.2% YoY to ~USD 1.9 billion, owing to a ~19% decline in product revenue across all its customer markets.

- Product revenue decreased in Japan, India, Australia, and China by 11%, 17%, 22% and 32%, respectively, on a YoY basis.

Ericsson

- Revenue from the APAC region declined 34.4% YoY in Q1-2024 to USD 1.1 billion (~SEK 12.0 billion), impacted by weaker Network sales.

- This was primarily due to a ~42% sales decline in South East Asia, Oceania and India.

- Reduction in the CAPEX investments by telcos owing to high investments in FY-2023 with an annual decrease in sales in the Philippines and Malaysia.

- EMEA revenue increased by a modest 1.2% YoY to USD 1.5 billion (SEK 15.1 billion) in Q1-2024, primarily driven by increased sales in the Middle East and Africa, as revenue across Europe remained stable.

- Sales from the Middle East and Africa grew 10.7% YoY to USD 448.5 million (SEK 4.7 billion), driven by 5G investments across several markets.

- The Americas revenue declined by 18.1% YoY to USD 1.6 billion (SEK 16.7 billion) in Q1-2024, dragging down overall company growth.

- This decline stemmed primarily from reduced network spending (5G CAPEX investments) by telcos in North America, resulting in revenue declining by 17.6% YoY to USD 1.3 billion (~SEK 14 billion).

Nokia

- In Q1-2024, Nokia experienced revenue decline in the Americas and APAC region, except for EMEA (20.1% YoY growth).

- Americas revenue declined 36.6% YoY to USD 1.3 billion (EUR 1.2 billion).

- North America region declined by 38.1% YoY, and the Latin America region declined by 25.4% YoY.

- This decline was due to weaknesses across the 3 network business groups: Mobile Networks and Network Infrastructure (IP Networks, Fixed Networks and Optical Networks).

- APAC revenue declined 46.4% YoY to ~USD 1 (EUR 947 million), impacted by the Mobile Networks and Network Infrastructure business groups.

- The normalisation of 5G investments in India after significant deployments in FY-2023 primarily resulted in revenue decline and other geographies, including China and the Rest of APAC countries.

- EMEA region reported revenue growth of 20.1% YoY to USD 2.5 billion (EUR 2.3 billion), primarily driven by the increase in revenue from Nokia Technologies (the revenues from which are entirely reported in Europe).

- Catch-up net sales of over USD 434.4 million (EUR 400 million) facilitated the revenue growth.

- Excluding Nokia Technologies, EMEA net sales declined primarily due to Mobile Networks and Cloud and Network Services, while Network Infrastructure declined marginally.

- Revenue from the Middle East and Africa increased 5.5% YoY to USD ~500 million (EUR 460 million), driven by growth in Mobile Networks and Optical Networks within Network Infrastructure.

- Europe’s net sales declined mainly in Mobile Networks, while Network Infrastructure saw mixed trends, with growth in IP Networks offset by declines elsewhere.

Key strategic developments

Advancements in 5G, cloud, network slicing, high-speed data transmission, network deployments and upgrades continue to drive telecom engagements

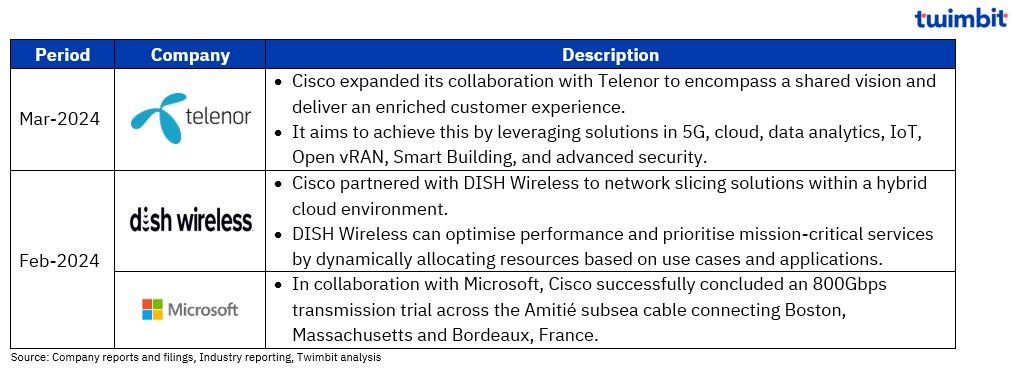

Cisco

- Cisco’s partnership focuses on innovative projects in 5G, cloud, network slicing, and high-speed data transmission.

Exhibit 5: Cisco – Key strategic developments, Q1-2024

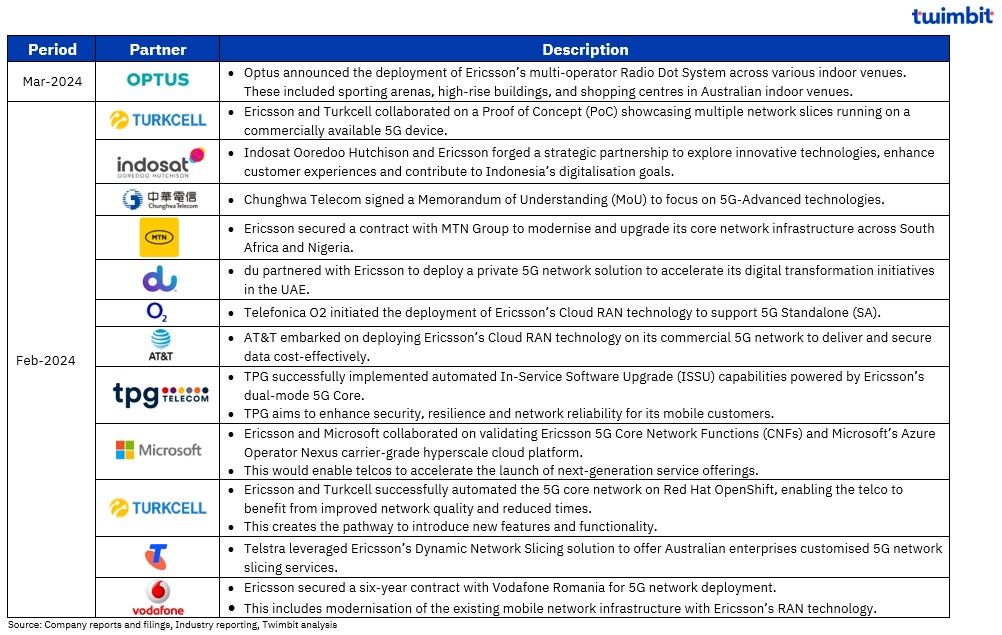

Ericsson

- Ericsson remains a key vendor in 5G development, with its partnerships focusing on network deployments, technology exploration, and infrastructure upgrades globally.

Exhibit 6: Ericsson – Key strategic developments, Q1-2024

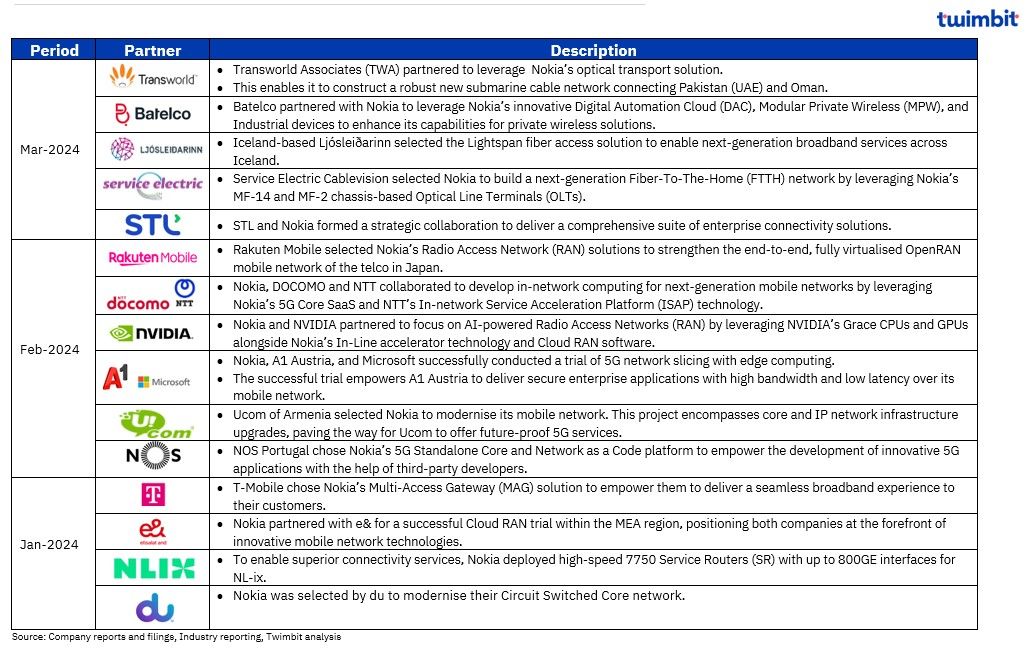

Nokia

- Nokia forges strategic partnerships globally to focus on areas like advancement in network technologies, including fiber optics, 5G, private wireless networks, and in-network computing.

Exhibit 7: Nokia – Key strategic developments, Q1-2024

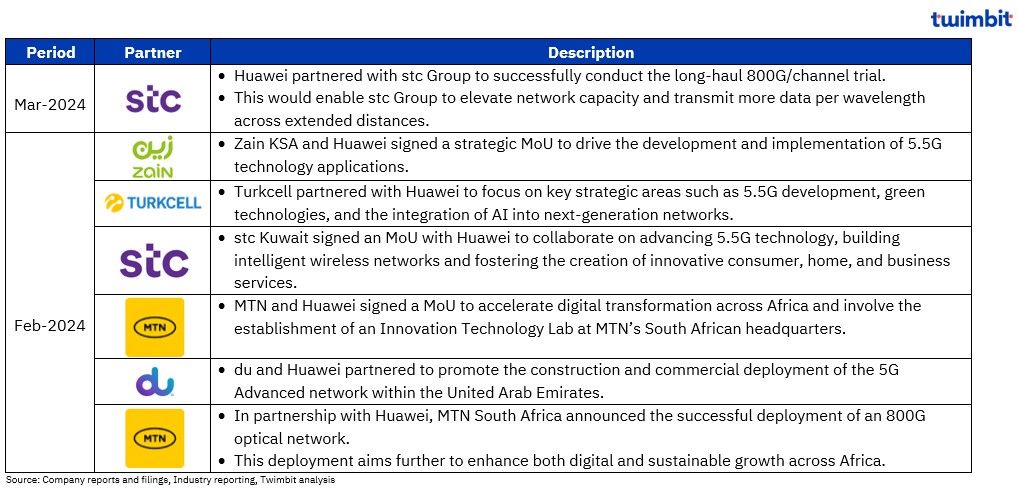

Huawei

- Huawei continues to pursue partnerships with leading companies globally for network technology advancements through initiatives like 5.5G development, high-speed data transmission, and AI integration.

Exhibit 8: Huawei – Key strategic developments, Q1-2024

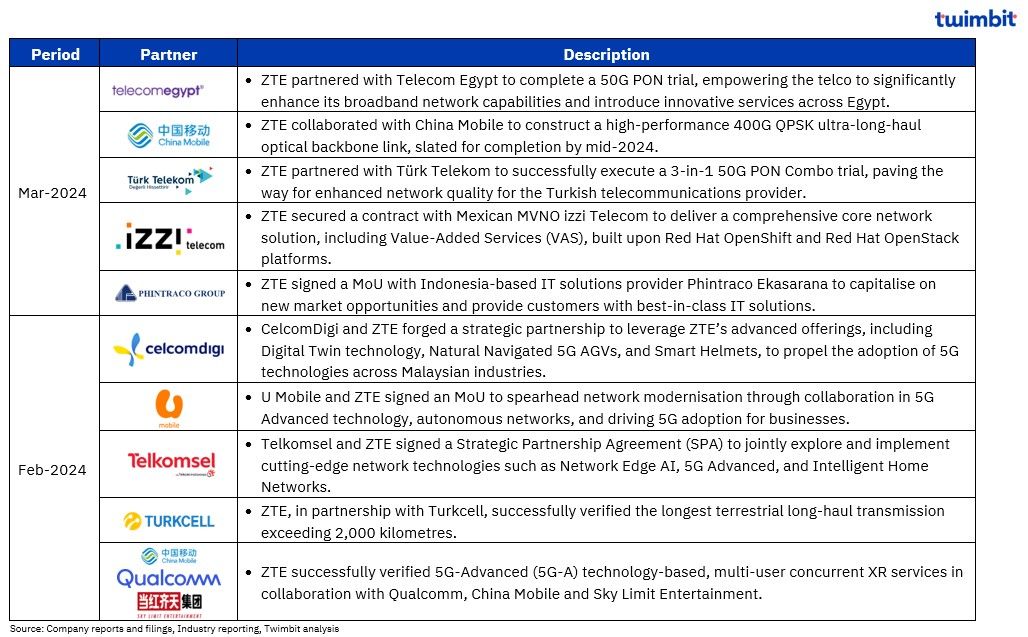

ZTE

- ZTE is partnering with global telecommunication companies to advance network technologies like 5G, high-speed transmission, and network solutions.

Exhibit 9: ZTE – Key strategic developments, Q1-2024

Research methodology and assumptions

- The report “Global telecom vendor updates: Spring 2024” provides brief insights into the financial and operational performance of leading telecom vendors (Cisco, Ericsson, Nokia, Huawei and ZTE) for the period January-March 2024.

- This report harnesses insights gleaned from official sources, financial reports, and regulatory filings of leading telecom equipment vendors, providing a robust foundation for analysis.

- The Financial performance for Q1-2024 serves as a powerful leading indicator, offering invaluable insights into future market trends and potential disruptions.

- The report provides actionable insights for benchmarking carrier and enterprise business operations against these key vendors.

- A brief summary of key strategic developments for Q1-2024, encompassing product launches, partnerships, and contract wins, provides a holistic understanding of vendor strategies and their potential impact on the market.

- All local currency figures have been converted to USD using an average exchange rate calculated for January – March 2024 to facilitate fair comparison.

For more content on telecoms, click here

Recommended by Twimbit

Top APAC telcos to ace beyond connectivity revenue 2024

Enterprise business update for Asia-Pacific telcos 2024

APAC telcos performance benchmarks – Winter 2024