Key Takeaways

- Top 5 telecom vendors witnessed revenue growth of 4.4% YoY in FY-2023, led by Cisco and Huawei, offsetting declines from Ericsson and Nokia. Overall growth dropped by 6 percentage points as compared to YoY growth in FY-2022, due to maturing 5G deployments in developed markets and challenging macroeconomic scenarios.

- Cisco’s revenue increased by 7.7% YoY, driven by strong carrier network sales and global expansion.

- Ericsson’s revenue fell by 3% YoY, due to lower sales in North America (its key market) and carrier network issues.

- Nokia’s revenue declined 10.6% YoY due to carrier network issues. APAC growth could not compensate for the regional weakness in the Americas and EMEA region.

- Huawei’s revenue surged 9.6% YoY with growth across all segments (Carrier network, Enterprise, and Consumer) and regions (Americas and APAC).

- ZTE’s revenue grew 1.1% YoY as revenue growth in the carrier network business compensated for the revenue decline in the enterprise segment.

- Overall carrier network business revenue, increased by 2.6%, driven by increased spending by telecom operators on network upgrade and expansion.

- Overall enterprise sales grew from 18.2% in FY-2022 to 19.2% of total revenue in FY-2023, reflecting a focus on digitalisation initiatives like cloud, security, and AI.

- All vendors (except Cisco) increased R&D spending, to explore new cloud, security, and AI revenue growth opportunities.

- India boosted revenues for Cisco, Ericsson, and Nokia owing to rapid 5G rollouts. However, Indian telcos plan to regulate CAPEX spending in 2024 after heavy investments in 2023 (with early signs visible in Q4-2023).

- Cisco, Ericsson, and Nokia announced workforce reductions as cost-saving measures to address declining sales and the saturated 5G market.

- Cloud-native solutions, 5G, Open RAN, network monetisation, and optical networks are key themes shaping telecom engagements in FY-2023.

- The market is expected to stabilise as operators focus on 5G Standalone, Open RAN architecture and monetising 5G services to meet growing capacity needs and new use cases.

Financial performance

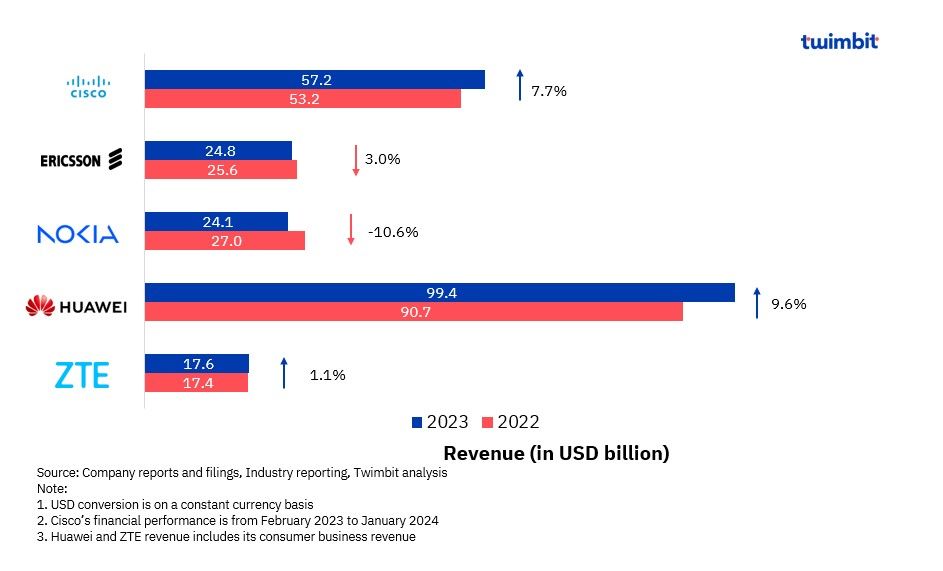

Revenue growth of top 5 telecom vendors rise by 4.4% FY-2023, led by Cisco & Huawei; growth slows from FY-2022

The top 5 telecom vendors’ revenue grew a modest 4.4% YoY in (year-on-year) FY2023, driven by revenue growth from Cisco and Huawei. This growth was lower than the 5.0% YoY growth over FY2021-FY2022, as 5G deployment nears completion in most of the developed markets.

The revenue performance of these vendors during 2022-2023 can be summarised as follows:

- Huawei, Cisco, and ZTE revenues grew by 9.6%, 7.7% and 1.1% respectively.

- Ericsson and Nokia’s revenues declined by 3.0% and 10.6% respectively.

Exhibit 1: Leading telecom vendor revenue trends YoY basis, 2022-2023

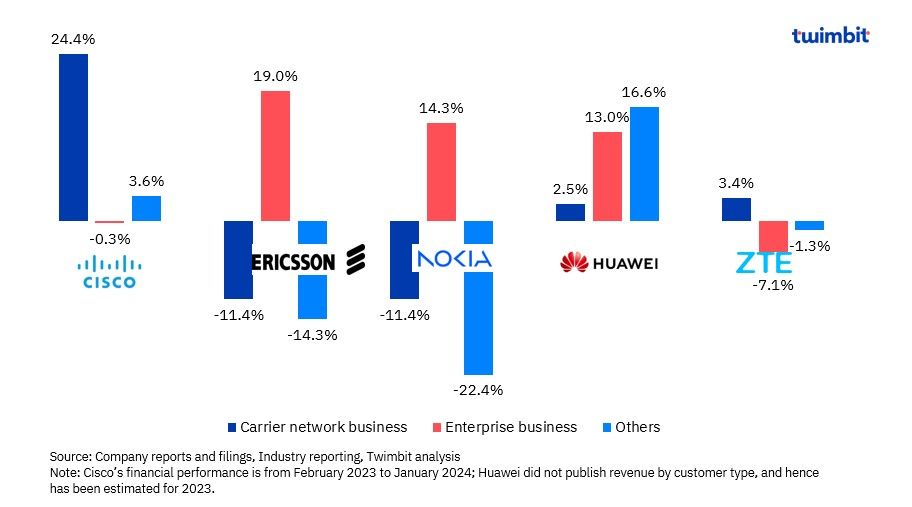

5G maturity in developed markets such as North America has caused a slowdown in investments among telecom vendors. As a result, enterprise business has grown in Ericsson and Nokia, whereas their carrier network business faced challenges in FY-2023.

Exhibit 2: Leading telecom vendor revenue trends by customer type, 2022-2023

Cisco

- FY-2023 revenues grew by 7.7% YoY to USD 57.2 billion

- Carrier network business represents 55.2% of the total revenues.

- 24.4% YoY growth to USD 31.6 billion, driven by campus and data centre switching offerings.

- Enterprise business represents 15.3% of total revenues.

- 0.3% YoY decline to USD 8.7 billion, due to enterprise and cloud market weaknesses.

- Customer success and product adoption are vital for recurring revenue streams through software subscriptions.

- Revenue momentum remains positive in software-heavy segments (Security, Collaboration, Observability).

- The acquisition of Splunk, completed in March 2024, will further bolster Cisco’s software portfolio and increase ARR (annual recurring revenue) potential by ~USD 4 billion post-acquisition.

- The acquisition of Isovalent, an open-source cloud-native networking and security provider, will strengthen Cisco’s secure networking capabilities across public clouds.

- Cisco announced a 5% workforce reduction (approximately 4,000 jobs) to align expenses & investments with the current market environment and address:

- Existing competitive pressure from Ericsson, Nokia and Arista Networks.

- Global economic concerns.

- Slower-than-expected product deployments.

Ericsson

- FY-2023 revenues declined by 3% YoY to USD 24.8 billion (SEK 263.4 billion).

- Carrier network business represents 65.1% of total revenues.

- 11.4% YoY decline to USD 16.2 billion (SEK 171.4 billion)

- The ~80% YoY growth in Southeast Asia, Oceania, and India could not offset North America’s (Ericsson’s most significant market) decline.

- Enterprise business represents 33.9% of total revenues.

- ~19.0% YoY increase to USD 8.4 billion (SEK 89.4 billion)

- Cloud software and service revenues grew 5.1% YoY to USD 6.0 billion (SEK 63.6 billion).

- Enterprise revenue grew 76.4% YoY to USD 2.4 billion (SEK 25.7 billion), driven by to strong growth in enterprise wireless solutions.

- Intellectual property rights (IPR) licensing revenue rose 7.1% YoY to USD 9 billion (SEK 9.1 billion) on account of 5G license renewals.

- Ericsson announced cost-saving measures, including job reductions.

- 8,500 job reductions (~8% of global headcount) across different countries in H2-2023 and 2024.

- The closure of field service operations in August 2023 impacted 750 jobs.

Nokia

- FY-2023 revenues declined by 10.6% YoY to USD 24.1 billion (EUR 22.3 billion) due to weaknesses in Network Infrastructure, Mobile Networks, and Nokia Technologies.

- Carrier network business (represents 79.3% of total revenue).

- 11.4% YoY decline to USD 19.1 billion (EUR 17.7 billion) primarily due to CAPEX normalisation by Indian telecom operators and cautious spending by North American Communication service providers (CSPs).

- Network infrastructure sales declined 11.2% YoY to USD 8.7 billion (EUR 8.0 billion) due to macroeconomic uncertainty, customer spending re-evaluation and inventory consumption limitations.

- IP Networks, Optical Networks, and Fixed Networks segments declined by 9%, 13%, and 18% YoY, respectively.

- Fixed network revenue, however, grew 5% YoY, driven by government-funded projects, and it is expected to continue growing in 2024.

- Mobile network sales declined 8.2% YoY to USD 10.6 billion (EUR 9.8 billion) due to telcos’ normalisation of network deployment across key regions. These include:

- North America: Depleted inventories and cash flow prioritisation

- India: Normalisation of 5G network deployment pace

- Europe: Relatively slower 5G deployments amid ongoing economic uncertainty

- Enterprise segment revenue (represents 10.3% of total revenue) in FY-2023.

- The segment reported a 14.3% YoY revenue increase to USD 2.5 billion (EUR 2.3 billion), driven by the acquisition of nearly 400 new enterprise customers and strong performance in private wireless, with over 710 customers compared to 560 in the previous year.

- To address declining sales and adjust to a changing 5G equipment market, Nokia announced a cost reduction plan, which includes

- Reduction of up to 14,000 jobs by 2026 to reduce cost base from ~USD 872 million (EUR 800 million) to ~ USD 1.3 billion (EUR 1.2 billion).

- Nokia restructured its India operations in February 2023 to reduce its headcount by 250 and consolidate business verticals into three major business verticals under the new structure — mobile networks, cloud and network services and network infrastructure.

- The restructuring reflects the challenging business environment in India, characterised by reduced 5G capital expenditures from major telecom providers, including Bharti Airtel, Reliance Jio, and Vodafone Idea.

Huawei

- FY-2023 revenue increased by 9.6% YoY to USD 99.4 billion (CNY 704.2 billion) driven by strong growth in its consumer business.

- Carrier network business revenue increased by 2.5% YoY to USD 41.1 billion (CNY 291.1 billion), representing ~41.3% of overall revenue in FY-2023.

- Enterprise business represents ~21.4% of total revenue.

- The segment witnessed 13.3% YoY growth to USD 21.2 billion (CNY 150.5 billion), driven by steady YoY growth of 21.9% and 3.5% in its cloud computing and digital power businesses, respectively.

- Consumer business revenue increased 17.3% YoY to USD 30.4 billion (CNY 215.5 billion), driven by increased acclaim of the HUAWEI Mate 60 Series and the HarmonyOS ecosystem.

ZTE

- FY-2023 revenue increased by 1.1% YoY to USD 17.6 billion (CNY 124.3 billion).

- Carrier network business represents 66.6% of total revenue.

- The segment witnessed 3.3% YoY growth to USD 11.7 billion (CNY 82.8 billion), driven by growth in wireless and wireline products.

- Enterprise business represents 10.9% of total revenues.

- Revenue declined 7.1% YoY to USD 1.9 billion (CNY 3.6 billion) as government and corporate business revenue from domestic integration projects, data centres, and the international market declined.

- Consumer revenue declined 1.3% YoY to USD 3.9 billion (CNY 27.9 billion) due to the international market’s decline in revenue from home terminal and handset products.

R&D performance

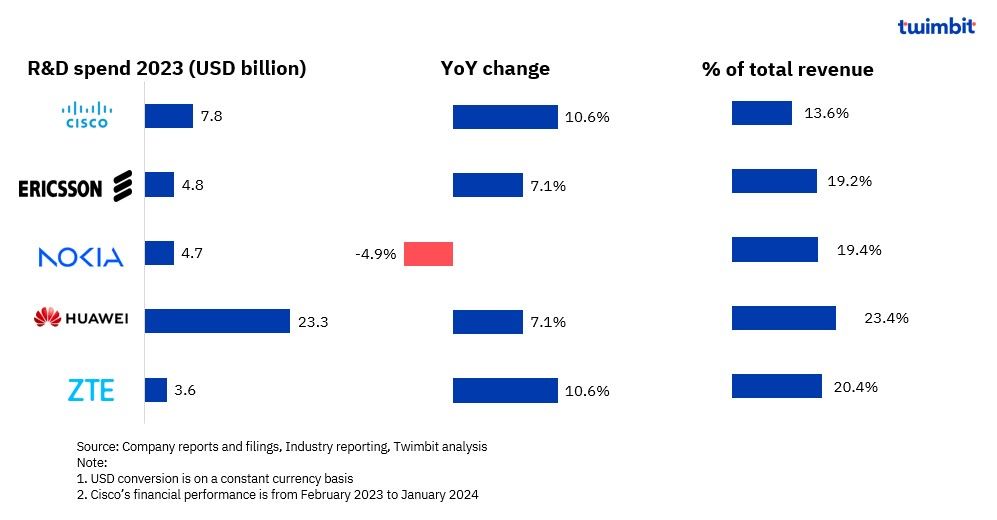

Telecom vendors R&D spending climbs in FY-2023, led by Huawei and Cisco

Exhibit 3: Leading telecom vendor R&D spending trends, 2022-2023

Cisco

- Cisco significantly increased its R&D spending by 10.6% YoY in FY-2023 to USD 7.8 billion, reaching 13.6% of its total revenue.

- The acquisition of Splunk (expected to be completed in Q2-2024) aligns with its strategic focus on strengthening its cloud, security, observability, and AI capabilities through targeted M&As, further bolstering its internal R&D efforts.

Ericsson

- Ericsson’s R&D expenses grew 7.1% YoY to USD 4.8 billion (SEK 50.7 billion) in FY-2023, representing 19.2% of its revenue.

- The enterprise segment saw increased R&D investments in Enterprise Wireless Solutions due to the full-year consolidation of Vonage.

- Despite the overall R&D increase in FY-2023, Ericsson reported a 1.5% decline in R&D expenses in Q4-2023, reaching USD 1.2 billion (SEK 13.0 billion).

- This is due to a decrease in networks, cloud software and services, offsetting growth in the enterprise segment.

Nokia

- Nokia’s R&D expenses declined 4.9% YoY to USD 4.7 billion (EUR 4.3 billion) in 2023, primarily due to network infrastructure and mobile network segments.

- Network infrastructure segment – R&D expenses declined by 3.7% YoY to USD 1.4 billion (EUR 1.3 billion).

- Mobile networks segment – R&D expenses declined by 10% YoY to USD 2.2 billion (EUR 2.0 billion).

- The R&D allocation as a percentage of revenue increased to 19.4% despite the decline.

Huawei

- Huawei’s R&D expenses increased 2.0% YoY to USD 23.3 billion (CNY 164.7 billion) in FY-2023, accounting for 23.4% of its total revenue.

- Huawei continues to invest in basic research and open innovation in domains like cloud and computing, intelligent automotive components, and foundational technologies. It also invests in developing new business domains, ecosystem building, and digital transformation.

- In FY-2023, nearly 114,000 (or ~55% of its total employee count) worked in R&D.

ZTE

- ZTE’s R&D expenses increased 17.1% YoY in FY-2023 to USD 3.6 billion (CNY 25.3 billion), accounting for 20.4% of the overall revenue.

- The company’s focus and competitiveness drove the increase in R&D investment in critical technologies, including 5G and 5G-A, chip, server and storage and innovative business.

Geographic performance

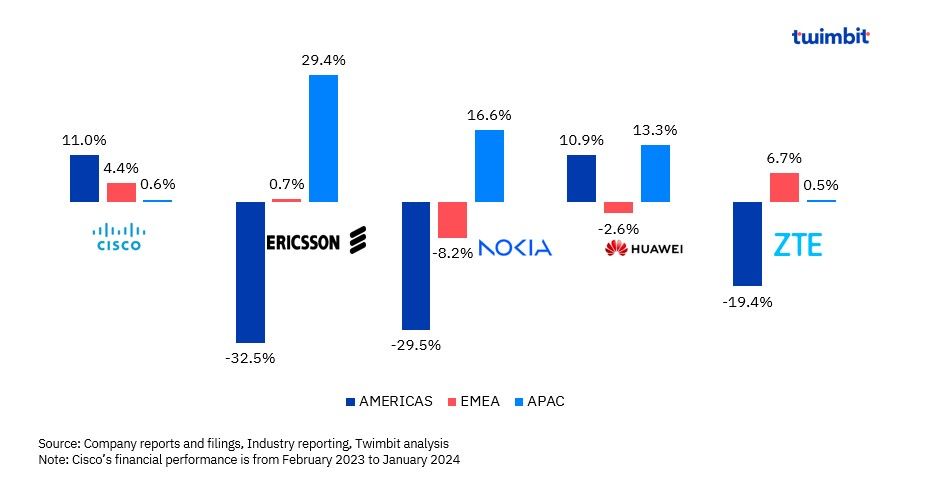

APAC remains the primary growth driver for telecom vendors, while the Americas and EMEA exhibit regional variations in performance

Exhibit 4: Leading telecom vendor regional revenue trends, 2023-2024

Cisco

- Cisco’s FY-2023 performance saw revenue growth across all regions, with the Americas emerging as the top contributor and achieving the highest YoY growth rate (11.0%), outpacing both EMEA (4.4%) and APAC (0.6%).

- The robust performance in the Americas was primarily driven by a surge in service revenue, highlighting the success of Cisco’s service-oriented approach, resulting in revenue reaching USD 34.2 billion in FY-2023. This strategy emphasises recurring revenue streams through software subscriptions and support services.

- While growth in APAC revenue was modest, reaching USD 8.1 billion in FY-2023, the region continues to hold significant strategic potential. Partnerships with Indian telecommunication providers for 5G rollout offer promising opportunities.

Ericsson

- Ericsson experienced strong regional revenue disparity in FY-2023, with strong revenue growth of 29.4% YoY in the APAC region, while its revenue from the EMEA region was almost flat at 0.7% YoY growth. However, the Americas region revenue decline of 32.5% on YoY basis offset the growth in other regions, resulting in an overall revenue decline.

- Ericsson experienced a strong performance in the APAC region, with revenue reaching USD 7.3 billion (SEK 77.3 billion) in FY-2023. This growth was primarily driven by Southeast Asia, Oceania, and India, with a ~62% YoY increase in sales from India. Sales in North East Asia declined by 10.5% as telcos in several markets have finalised the first build-out phase of 5G.

- EMEA revenue increased to USD 6.6 billion (SEK 70.3 billion) in FY-2023. Increase in network spending by telcos in the Middle East primarily driven by new 5G investments in select Middle East countries. This offset the decline in revenue from the Europe region, which witnessed lower Capex spending owing to higher investments made by the telcos in previous years.

- The Americas region’s revenue declined to USD 7.3 billion (SEK 77.5 billion) in FY-2023, dragging down overall company growth. This decline stemmed from reduced network spending by telcos in both North and Latin America, as they focused on managing inventory levels after high investments in 2021 and 2022.

Nokia

- Nokia experienced revenue decline in the Americas and EMEA region, except for APAC (16.6% YoY growth).

- Americas revenue declined 29.5% YoY to USD 7.3 billion (EUR 6.8 billion) due to weakness in both North America (down 31.6% YoY) and Latin America (down 14.5% YoY).

- Strong decline in North America revenue (down by 31.6% YoY) reflected weakness in Mobile Networks and Network Infrastructure as customers continued to evaluate their spending and digest inventories. To a lesser extent, Cloud and Network Services also declined.

- Latin American revenue declined by 14.5% due to reduced network infrastructure sales across IP Networks and Fixed Networks, partially offset by a slight increase in Mobile Networks and Cloud and Network Services.

- EMEA revenue declined 8.2% YoY to USD 8.6 billion (EUR 7.9 billion), primarily due to a decline in the Europe region, which offset growth in the Middle East and Africa.

- Europe revenue dropped 11.8% YoY, impacted by declines in Nokia Technologies, Network Infrastructure (particularly IP and Fixed Networks), and Mobile Networks.

- Middle East & Africa revenue grew 41.1% YoY, driven by Mobile Networks and Network Infrastructure, partially offset by the Cloud and Network Services decline.

- APAC revenue grew 16.6% YoY to USD 6.9 billion (EUR 6.4 billion), primarily led by exponential growth in India of USD 3.1 billion (EUR 2.8 billion).

- Sales in Asia Pacific, including China, declined during the period due to reduced Network Infrastructure and Cloud and Network Services. Additionally, revenue from India declined in Q4-2023, primarily in Mobile networks, signifying normalisation of the 5G network deployments initiated in 2022.

Huawei

- Huawei’s EMEA revenue growth witnessed challenges, while its Americas and APAC revenue grew in FY-2023.

- Americas revenue grew 10.9% YoY to ~USD 5 billion (CNY 35.4 billion), driven by steady growth in its ICT infrastructure, digital power and cloud computing, as customers increased investment and industries accelerated digital, intelligent, and low-carbon transformation initiatives.

- EMEA revenue declined 2.6% YoY to USD 20.5 billion (CNY 145.3 billion).

- APAC region revenue witnessed the highest growth of 13.3% YoY to USD 72.4 billion (CNY 512.3 billion), driven by strong revenue growth in China.

- Revenue from China grew 16.7% YoY to reach USD 66.6 billion (CNY 471.3 billion), driven by growth across all its business domains, including cloud computing, digital power and consumer business.

ZTE

- Revenue increased across its operating geographies, with APAC accounting for ~81% of total revenue in FY-2023.

- China continued to be the largest revenue-contributing geography and accounted for 69.6% of the total revenue in FY-2023 (up by 1.5% YoY), driven by its involvement in the deployment of construction of 5G and GB-grade optical networks.

Key strategic developments

Cloud-native solutions, 5G, Open RAN, network monetisation and optical networks are the key themes driving telecom engagements

Cisco

Exhibit 5: Cisco – Key strategic developments, Q4-2023

Ericsson

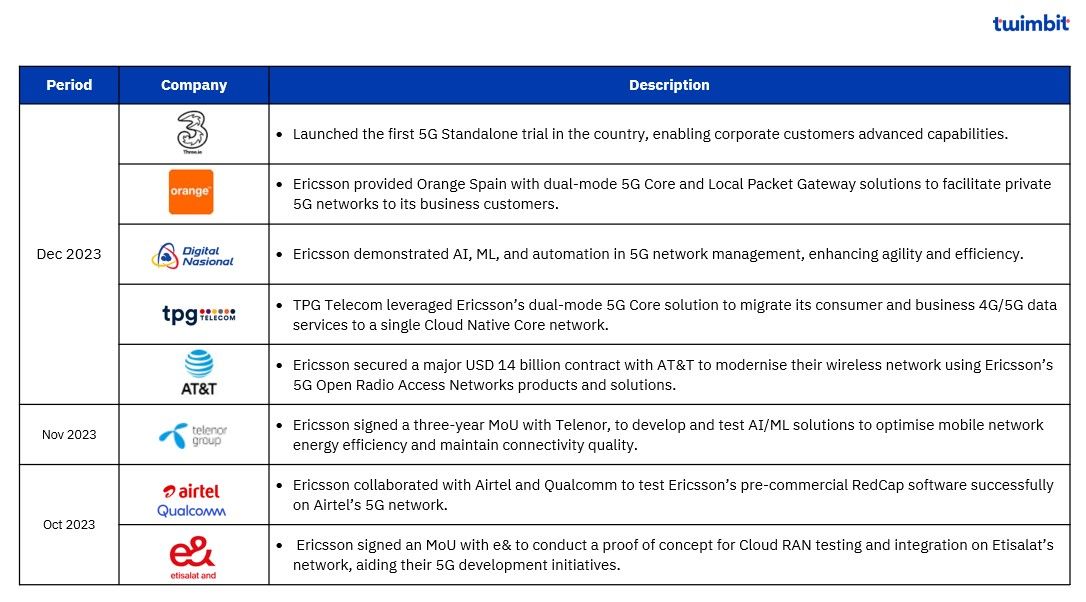

Ericsson remains a key vendor in 5G development, collaborating with diverse partners on innovative projects. Its key focus areas include 5G Standalone, private networks, network management efficiency, cloud-native solutions, and Open RAN.

Exhibit 6: Ericsson – Key strategic developments, Q4-2023

Nokia

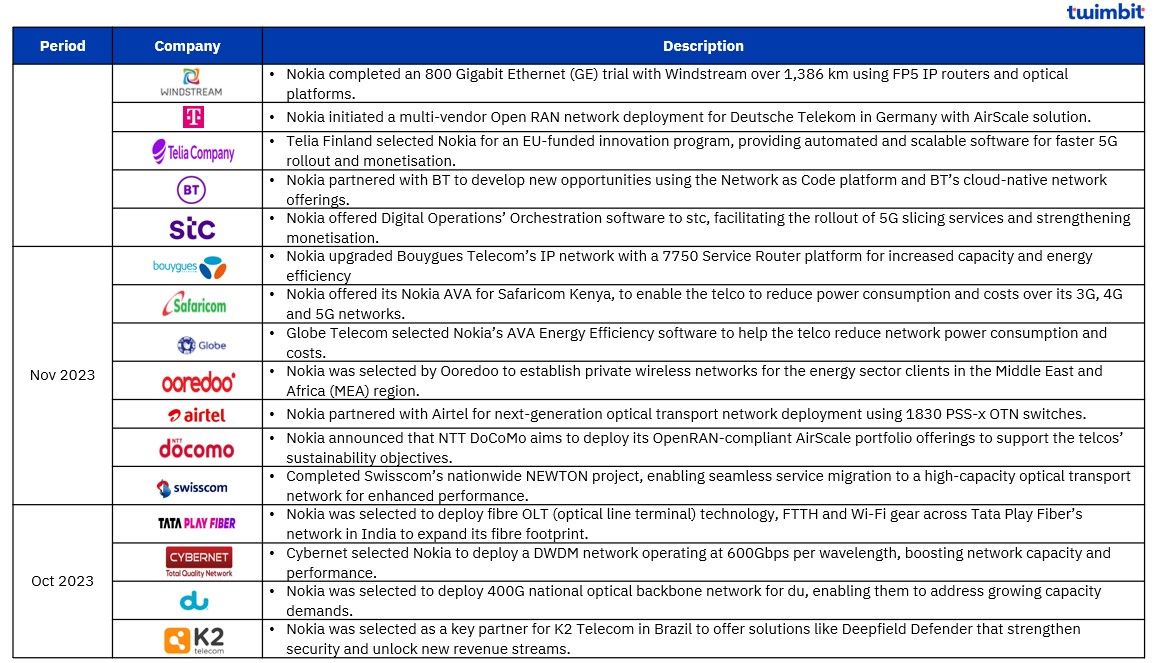

Nokia announced the divesting of its “Device Management and Service Management Platform” businesses to Lumine Group as a part of its strategic initiative. This will help Nokia focus more on its core CNS (Cloud and Network Services) portfolio and strategic investments.

The company is globally involved in network modernisation projects, leveraging its expertise in 5G, Open RAN, and optical networking. Strategic partnerships with major players drive innovation and expand Nokia’s reach in new markets.

Exhibit 7: Nokia – Key strategic developments, Q4-2023

Huawei

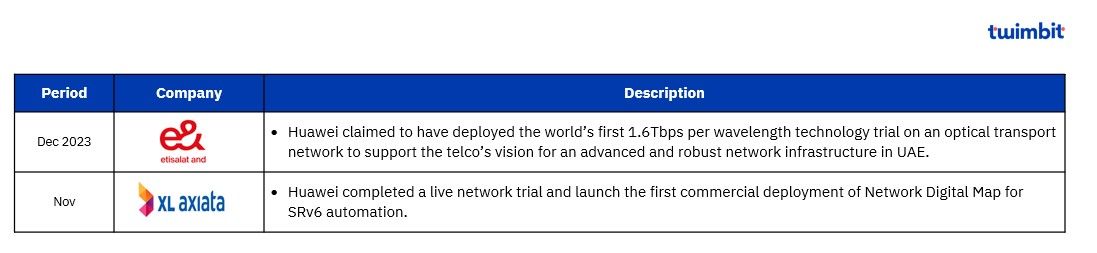

Huawei advances network technology with the world’s first 1.6Tbps trial and launches the industry’s first commercial Network Digital Map for SRv6 automation.

Exhibit 8: Huawei – Key strategic developments, Q4-2023

ZTE

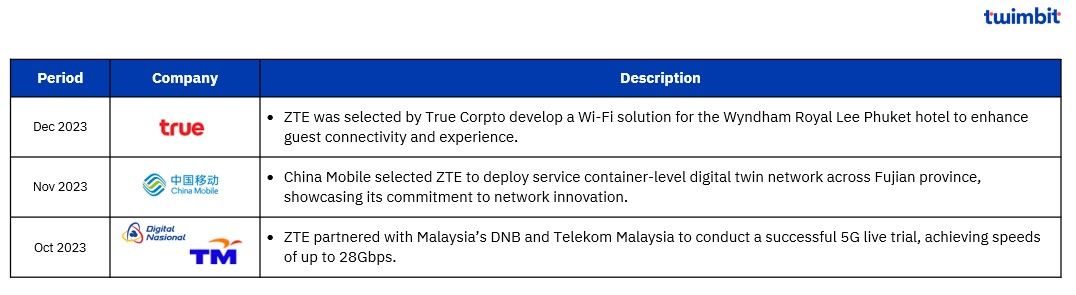

Exhibit 9: ZTE – Key strategic developments, Q4-2023

ZTE pursued strategic partnerships to offer solutions for hospitality, network intelligence, and cutting-edge 5G capabilities.

Research methodology and assumptions

- The report leverages secondary research, analysing information from official websites, financial reports, and regulatory filings of leading telecom equipment vendors.

- The performance data for FY-2023 and Q4-2023 is a reliable indicator of overall financial performance and provides valuable insights into future market trends.

- This comprehensive analysis delves into the FY-2023 performance of 5 prominent global players, including Cisco, Ericsson, Huawei, Nokia, and ZTE.

- The report aims to deliver actionable insights into benchmarking carrier and enterprise business operations across these key vendors.

- Key strategic developments for Q4-2023, encompassing product initiatives, partnerships, and contract wins, are meticulously evaluated to provide a holistic understanding of vendor strategies.

- All local currency figures have been converted to USD using an average exchange rate calculated for January-December 2023 to facilitate fair comparison.

Click here for more contents on telecom

Recommended by Twimbit

Thailand telecom market updates – 2024 edition