Key Takeaways

- The leading five telecom vendors achieved notable revenue growth, recording a combined YoY increase of 5.4% on a constant currency basis in Q2 2023.

- Ericsson and Nokia continued to deliver strong performance in their enterprise business, driven by growing demand for the deployment of private wireless networks.

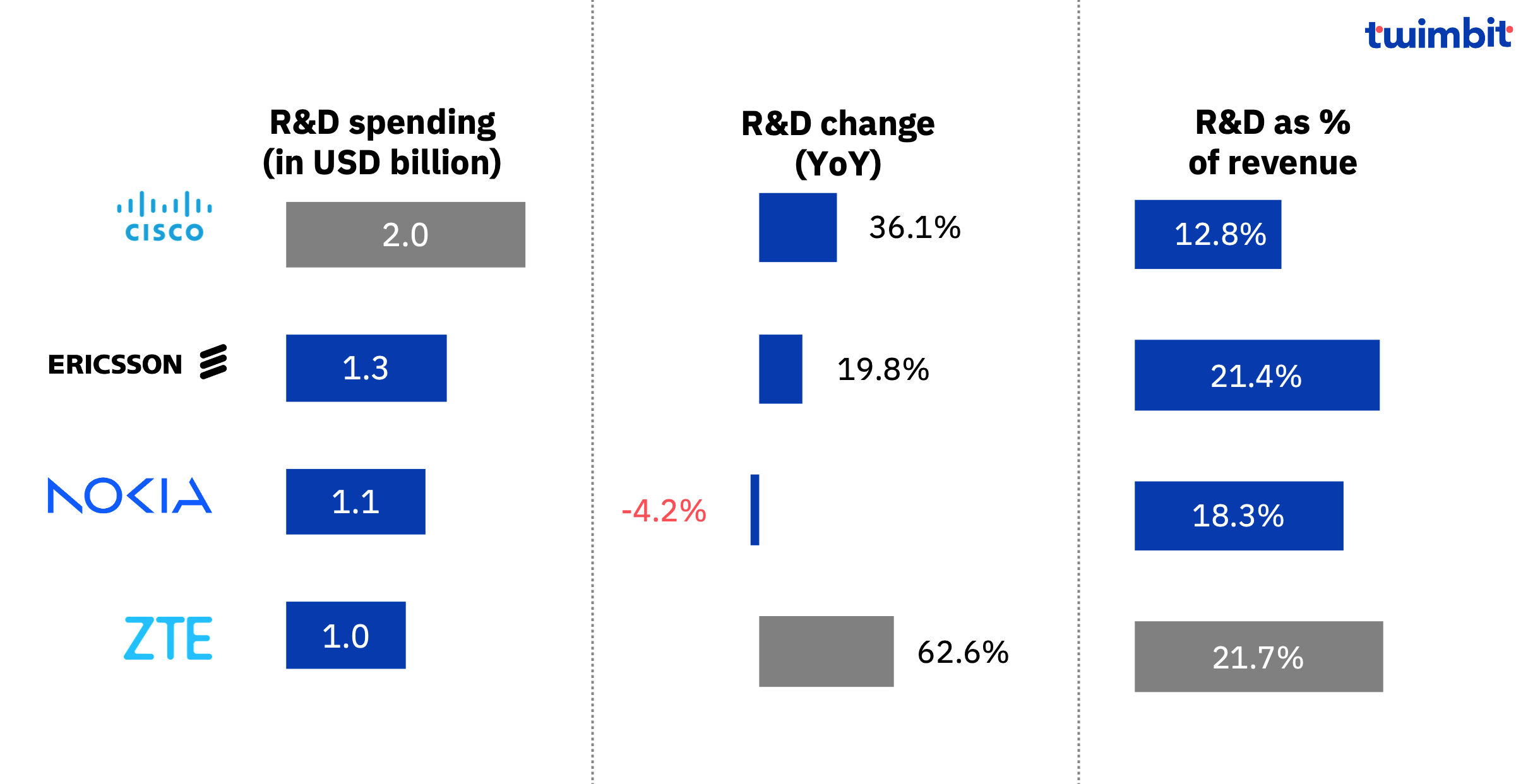

- A strong focus on R&D remains critical for vendors, enabling them to sustain innovation and uphold their competitive advantage.

- ZTE demonstrated a remarkable 62.6% surge in R&D spending, while both Ericsson and ZTE allocated over 20% of their revenue to R&D endeavours.

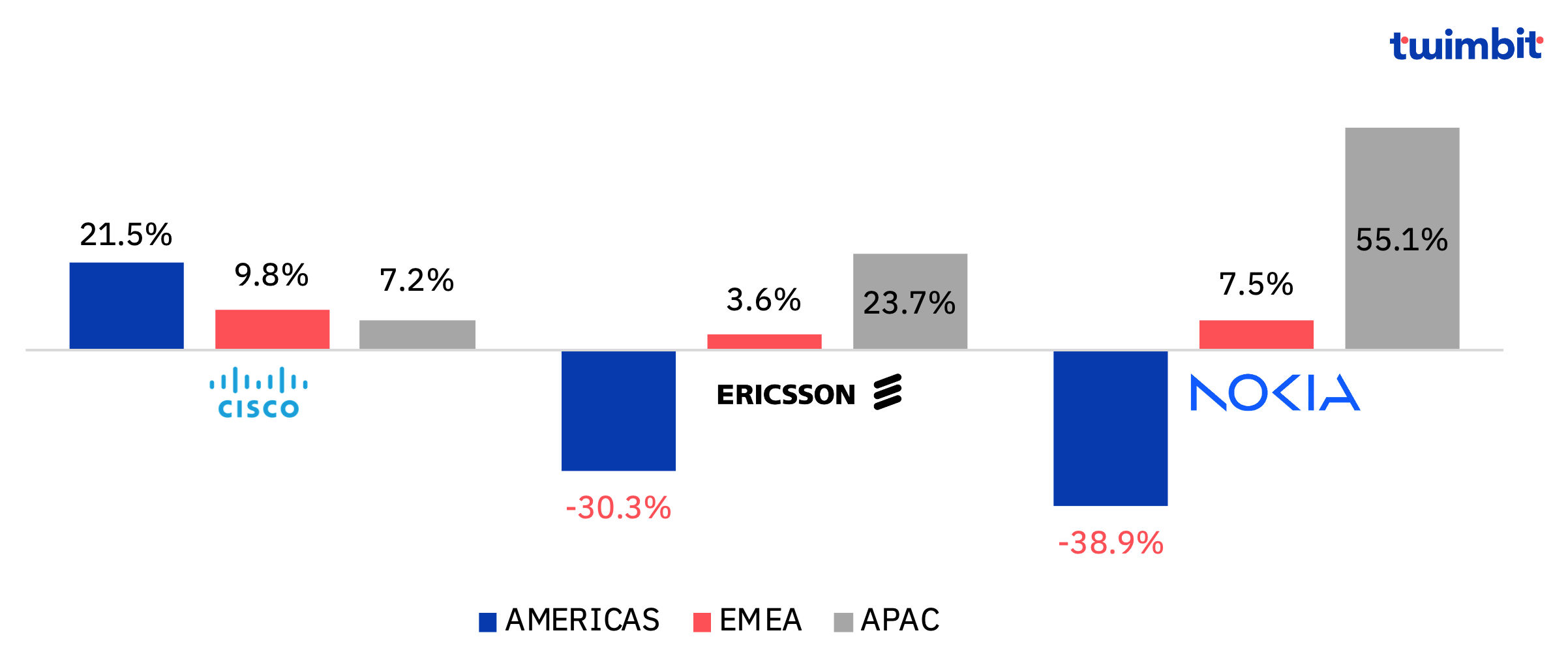

- Cisco achieved revenue growth across all geographic segments, reflecting its strong global performance.

- Despite managing to achieve remarkable success in the Indian market, Ericsson and Nokia encountered challenges in the Americas region. Additionally, ZTE demonstrated impressive strength, with 71% of its revenue coming from its domestic market.

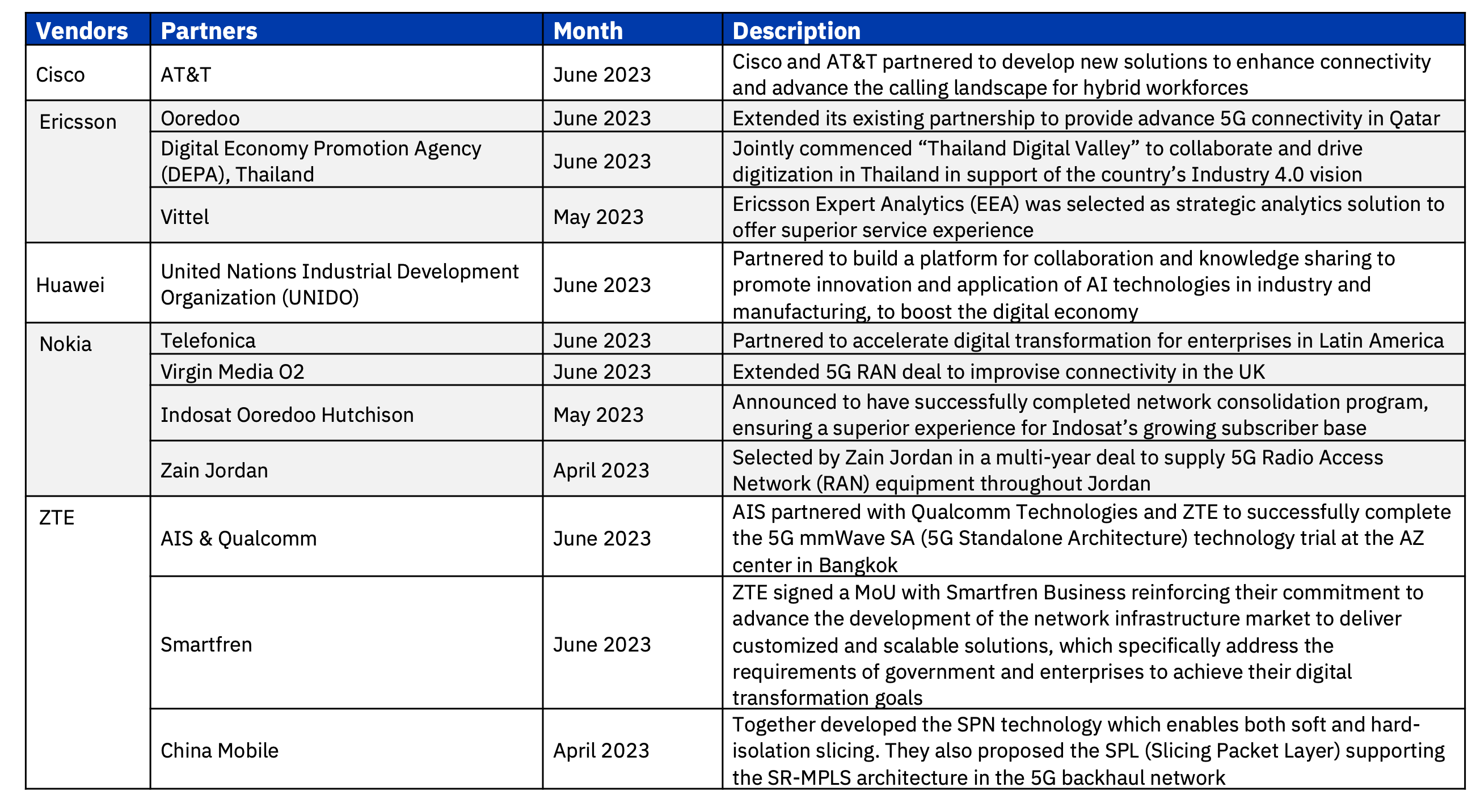

- Prominent partnerships during Q1 2023 featured Ericsson collaborating with Thailand’s Digital Economy Promotion Agency (DEPA), Huawei teaming up with the United Nations Industrial Development Organization (UNIDO), and Nokia forming an alliance with Telefonica.

This report offers a comprehensive evaluation of the Q2 2023 performance of prominent global telecom vendors including Cisco, Ericsson, Huawei, Nokia, and ZTE. The report’s primary focus is to provide valuable insights into the benchmarking of their carrier and enterprise business operations. It’s important to highlight that Chinese equipment vendors have not revealed their quarterly earnings based on segments and geographical areas. However, we have recorded their revenue breakdown by segments for H1 2023.

Financial Performance

Cisco achieves impressive growth, while Nokia and ZTE navigate challenges

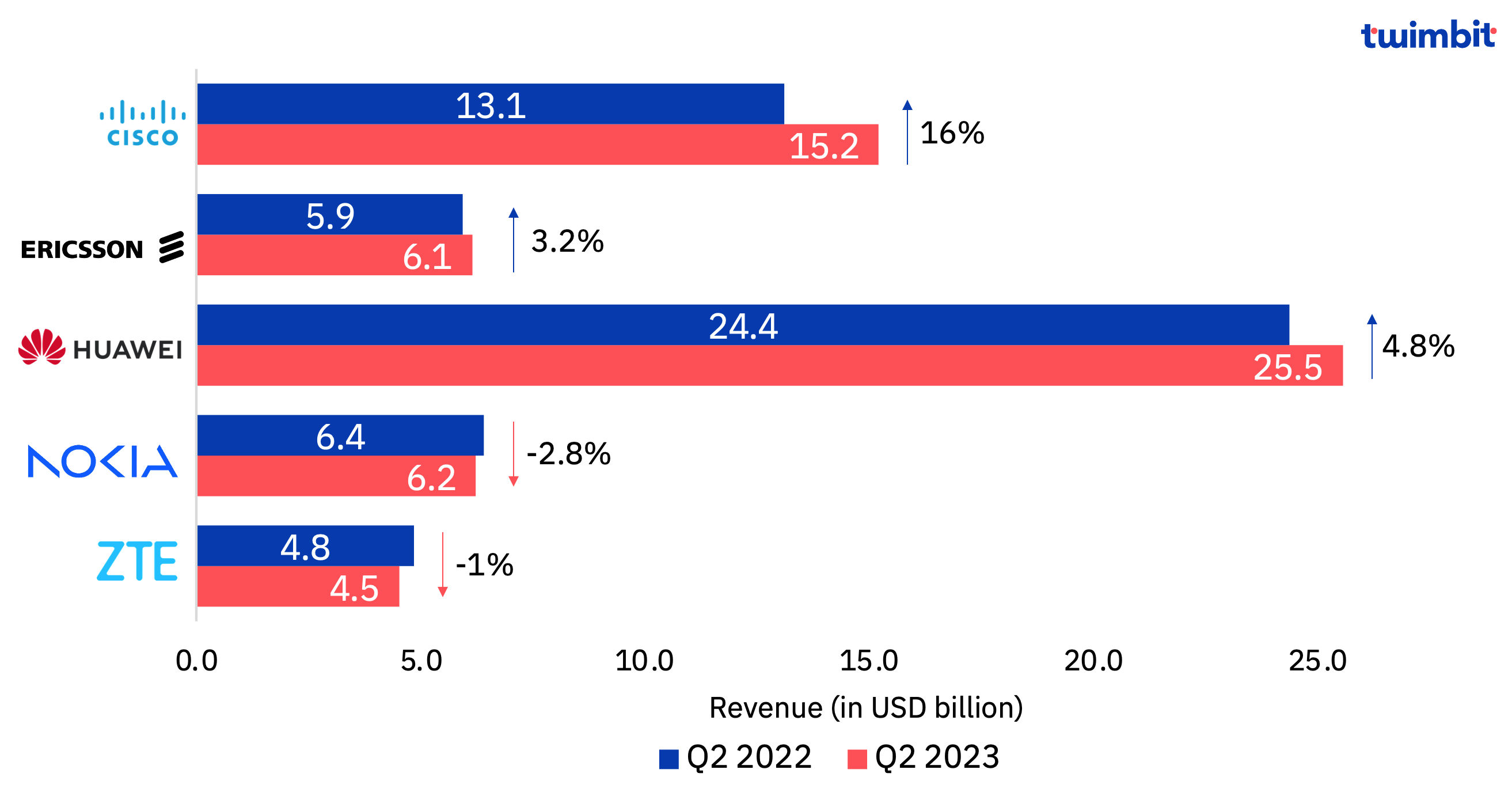

The financial results of the top five telecom vendors in Q2 2023 underscore a blend of progress and challenges. Factors such as the rollout of 5G, regional dynamics, and strategic collaborations have played pivotal roles in shaping their performance trajectories. Collectively, the foremost five telecom equipment vendors recorded a 5.4% growth on a constant currency basis. The revenue performance of these vendors during this period can be summarized as follows:

Exhibit 1: Revenue trends YoY basis, Q2 2023

Note:

1. USD conversion is on constant currency basis

2. Cisco’s financial performance is from May 2023 to July 2023

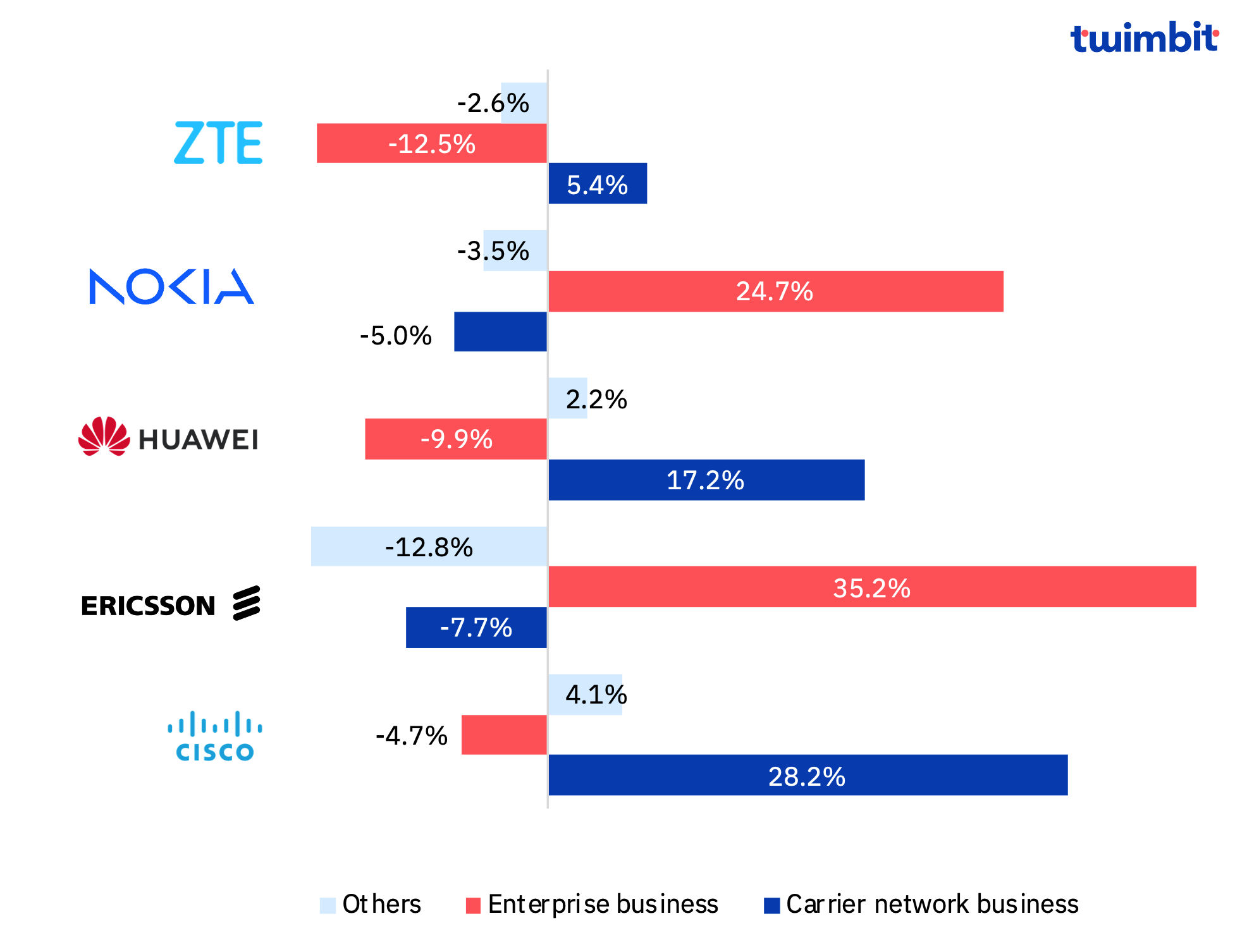

Ericsson and Nokia experience robust growth in their enterprise business, fuelled by the rising demand for 5G deployment. However, Cisco continues to rely on its carrier network business as a key revenue driver in Q2 2023, while its enterprise business witnessed a decline.

Exhibit 2: Revenue growth by customer type, Q2 2023

Note:

1. ZTE and Huawei segment revenue increase is for H1 2023 only

2. Cisco’s financial performance is from May 2023 to July 2023

Cisco

Cisco demonstrated substantial revenue growth of 16% to reach an impressive USD 15.2 billion. This surge was driven by a commendable 20.3% growth in product revenue, totalling USD 11.6 billion, complemented by a 4.1% increase in service revenue, summing up to USD 3.6 billion.

Cisco’s carrier network business experienced a noteworthy growth rate of 28.2%. This surge can be primarily attributed to the Secure, Agile Networks within this segment, which took the lead, achieving a remarkable growth rate of 33.3%.

Ericsson

Ericsson achieved a robust revenue of USD 6.1 billion, which incorporates a notable USD 0.4 billion contribution from Vonage, signifying a commendable growth of 3.2%. This growth trajectory was influenced by the strategic reshaping of Ericsson’s business composition post the Vonage acquisition.

Capitalizing on its advanced 5G technology, Ericsson is strategically harnessing its potential to propel growth within its enterprise domain. Furthermore, the company is actively driving a cultural transformation, a strategic endeavour aimed at accelerating its growth trajectory and, in turn, shaping the landscape of the communications industry. Ericsson’s enterprise division marked a remarkable 35.2% growth, a figure inclusive of Vonage’s contribution. However, when Vonage is excluded, the enterprise sector still achieved a noteworthy growth of 29.4% when compared to the same period in the previous year. Besides that, challenges surfaced within Ericsson’s carrier network division, primarily due to reduced sales in the Americas—a region that had previously thrived on 5G advancements. Similarly, the ‘Others’ segment experienced a decline, stemming from the divestiture of the IoT business in Q1 2023.

Huawei

Huawei achieved a revenue of USD 25.5 billion during Q2 2023, representing a substantial 4.8% YoY increase. Notably, the overall performance aligned closely with projected expectations.

Huawei carrier network business generated revenue of USD 23.9 billion in H1 2023 (Jan-June), with an increase of 17.2%, while its consumer business grew by 2.2% to reach USD 14.8 billion in H1 2023. Huawei enterprise business faced a significant decline of 9.9%.

In the realm of Huawei’s carrier network business in H1 2023 (January-June), this segment generated revenue amounting to USD 23.9 billion, marking a surge of 17.2%. Similarly, Huawei’s consumer business experienced growth, albeit more modest, with a 2.2% increase, resulting in a total revenue of USD 14.8 billion during the same H1 2023 period. However, digital power and cloud businesses for Huawei experienced growth, but were unable to offset overall decline. Notably, Huawei’s newly introduced components for intelligent connected vehicles continue to gain traction and competitiveness within the market.

Nokia

Nokia witnessed mixed headwinds in Q2 2023, with both positive and challenging dynamics. Notably, their enterprise division exhibited noteworthy growth, with a substantial increase of 24.7%. Similarly, their ‘Others’ segment saw a modest uptick of 2.2%. However, this growth was inadequate to offset the 5% decline in their carrier network business, ultimately leading to an overall revenue contraction of 2.8%. During this period, Nokia’s revenue stood at USD 6.2 billion.

Nokia’s enterprise growth stemmed from gains in the private wireless sector, driven by double-digit expansion. Impressively, Nokia has amassed a clientele exceeding 635 private wireless customers, a testament to their position in the market. During Q2 2023, Nokia further solidified their standing by onboarding 90 new enterprise clients, thereby elevating their total customer count to over 685.

While Nokia’s submarine networks faced a 15% decline, this was effectively counterbalanced by a 10% increase in their licensing business, thereby contributing to growth within their other segments.

ZTE

ZTE faced a blend of opportunities and challenges in Q2 2023, as its revenue reached to USD 4.5 billion in same period, a decrease of 1% YoY. ZTE have 71% of its revenue from domestic market only.

ZTE’s carrier network business showcased positive growth during H1 2023 (January-June), with an increase of 5.4%. However, this upswing was not adequate to offset the downturn observed in both their enterprise and consumer sectors. Specifically, their enterprise business faced a decline of 12.5%, while the consumer business saw a decline of 2.5%, during the same H1 2023 timeframe.

R&D Performance

ZTE’s robust R&D investment fuels accelerated innovation

Exhibit 3: R&D performance of vendors, Q2 2023

Note:

1. Cisco’s financial performance is from May 2023 to July 2023

2. Huawei does not report R&D expense on a quarterly basis

Cisco

Cisco witnessed a significant 36.1% YoY increase in its R&D spending, reaching an impressive USD 2.0 billion during Q2 2023. This expansion was fuelled by the company’s strategic choice to increase its investment in ICT R&D internationally at its second largest R&D centre in India outside the US. R&D spending as a share of total revenue increased by 190 basis points to 12.8%.

Ericsson

Ericsson’s Q2 2023 saw a significant uptick of 19.8% in R&D spending. Notably, this growth was primarily driven by strategic initiatives in the enterprise segment, effectively offsetting the decline in R&D expense for networks and segment other. Ericsson’s heightened R&D spending within the enterprise segments from pivotal moves such as the Vonage acquisition, aimed at expanding their portfolio of enterprise wireless solutions. Consequently, R&D spending as a proportion of the total revenue witnessed a substantial increase of 300 basis points, resulting in R&D accounting for 21.4% of the total revenue.

Nokia

Nokia reported a 4.2% YoY decline in its R&D expenses. Despite this decrease, the impact on the allocation of R&D spending as a proportion of revenue was relatively modest, declining by a marginal 30 basis points, resulting in R&D accounting for 18.3% of the total revenue. Notably, this decline can be largely attributed to the strategic restructuring undertaken within specific segments during Q1 2023.

ZTE

ZTE’s continued to expand innovative services in the second curve during Q2 2023, with computing power infrastructure products driving progress. R&D investment increased by 62.6% YoY amounted to USD 1 billion, accounting for 21.7% of its revenue. ZTE has substantially enhanced competitiveness across all its business sectors by reinforcing the capabilities of Data Technology, Information Technology, and Communications Technology (DICT) infrastructure products and solutions.

Geographic performance

Vendors reported strong growth in APAC

Exhibit 4: Regional revenue trends, Q2 2023

Note:

1. Cisco’s financial performance is from May 2023 to July 2023

2. Huawei and ZTE don’t report geographic wise revenue on quarterly basis

Cisco

Cisco’s performance exhibited remarkable growth across all major regions. Notably, the Americas region experienced a substantial 21.5% increase, while the EMEA region achieved a commendable 9.8% growth, and the APAC region marked a noteworthy 7.2% expansion. The growth observed in the Americas was primarily attributed to a surge in service revenue, underscoring the significance of Cisco’s service-oriented approach.

The growth in the APAC was significantly influenced by strategic investment made in India for manufacturing. This was underpinned by India’s burgeoning digital economy, positioning the country as a pivotal hub for innovation and business within Cisco’s strategic landscape. This was further fortified by the establishment of a new manufacturing operation in India, strategically designed to cater to the escalating demand from Indian as well as global customers. This strategic move also plays a crucial role in enhancing and diversifying Cisco’s supply chain.

Ericsson

Ericsson encountered challenges in the Americas, but this was successfully offset by a substantial growth in EMEA and the APAC region with 3.6% and 23.7% respectively.

A particularly remarkable highlight was the exceptional revenue surge of 74% observed in the Southeast Asia, Oceania, and India segment. This growth was underpinned by significant market share gains in the burgeoning 5G sector within India. However, Ericsson’s North American business experienced a decline of 37%. This was partially offset by a 3% growth in the Latin America region, primarily attributed to the ongoing deployments of 5G infrastructure. In Northeast Asia, Ericsson encountered a 31% decline, which can be attributed to reduced investments in several 5G frontrunner markets. This reduction followed elevated 5G investment levels witnessed in 2022, signifying a natural adjustment phase in the trajectory of 5G adoption and investment.

Nokia

Nokia navigated a landscape marked by challenges across various regions, with the notable exceptions of India and Europe. Particularly noteworthy was the remarkable 333% growth witnessed in India, which effectively countered the 8% decline in the Asia-Pacific (excluding China) region, as well as the substantial 18% decline observed in China. The strong growth in net sales in India was related to mobile networks, as 5G deployments continued to ramp up in Q2 2023. Network Infrastructure also saw strong growth, mainly driven by Optical Networks.

Europe’s net sales were notably influenced by the growth in Nokia Technologies, a division exclusively reported within the European context. Excluding Nokia Technologies, net sales across Europe exhibited a robust double-digit growth rate, propelled by expansion across all business groups. Notably, IP Networks and Fixed Networks within the Network Infrastructure segment performed particularly well, complemented by the sustained momentum within Mobile Networks.

The Middle East and Africa region experienced growth primarily driven by Network Infrastructure and Cloud and Network Services, although these gains were somewhat balanced by a decline within the Mobile Networks sector.

Key Partnership

Vendors accelerate growth with partnerships

Exhibit 5: Key partnerships, Q2 2023

Research Methodology and Assumptions

- Data collection has been done basis of secondary research in reference to the information provided by the telecom equipment vendors’ websites and financial reports and filings.

- The performance of the telecom equipment vendors in Q2 2023 is indicative of their overall performance and can be used to predict future trends in the market.

- The report covers the second quarter of 2023 for each of the telecom equipment vendors. Notably, Cisco’s fiscal year concludes in July. To align their reporting cycle with the calendar year, Q4 FY 2023 is considered equivalent to Q2 CY 2023.

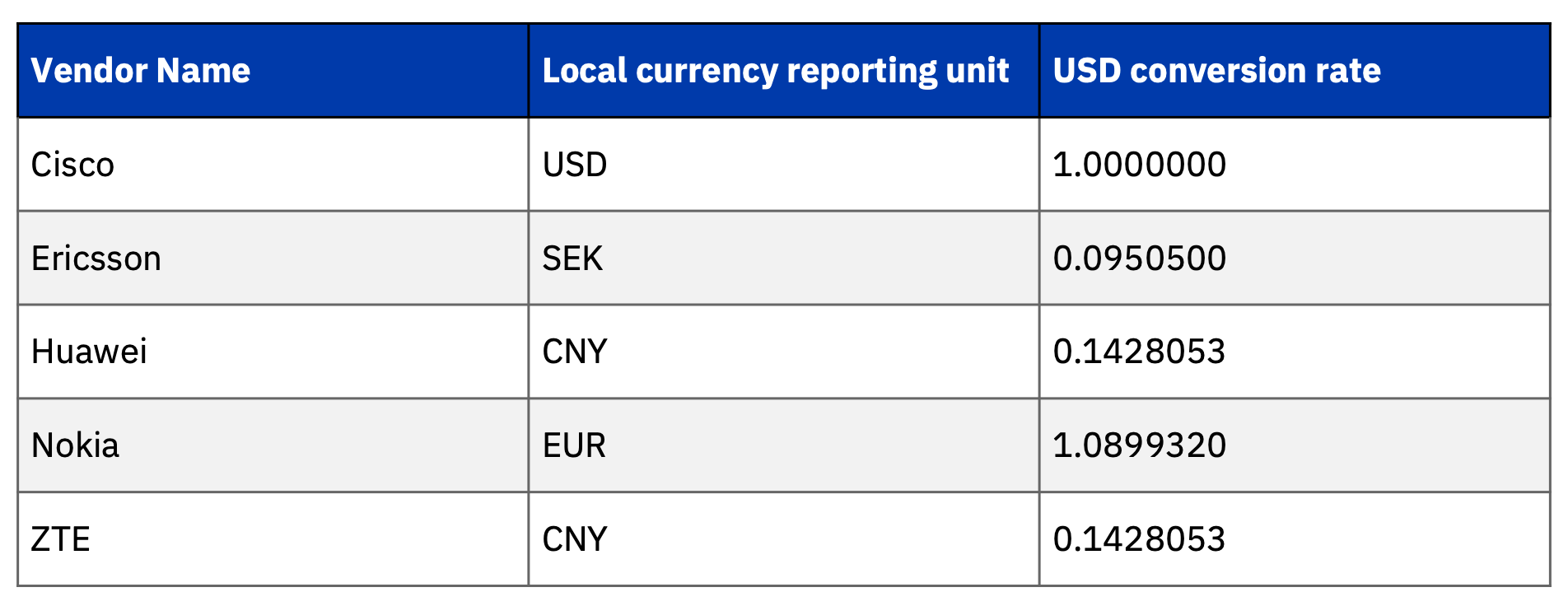

- For fair representation, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value for the period April-June 2023. The below table reflects the currency conversion rate used in this report:

Thank you for reading! Reach out to us for any feedback

You might also like:

Global telecom vendors update – Q1 2023

Cloud stories – Q2 2023

Indonesia Telecom Update 2023

Japan telecom market update