With RM 254.3 billion in assets, as of 30 June 2022, HLB (Hong Leong Bank) stands respectably, ranking as the 5th largest banking group in Malaysia by assets. During this time, it also ranked as the 4th largest bank by market capitalisation.

The success of HLB has translated to its extensive network of 232 branches and 1,044 self-service terminals spanning Asian nations, such as Malaysia, Singapore, Hong Kong and Vietnam.

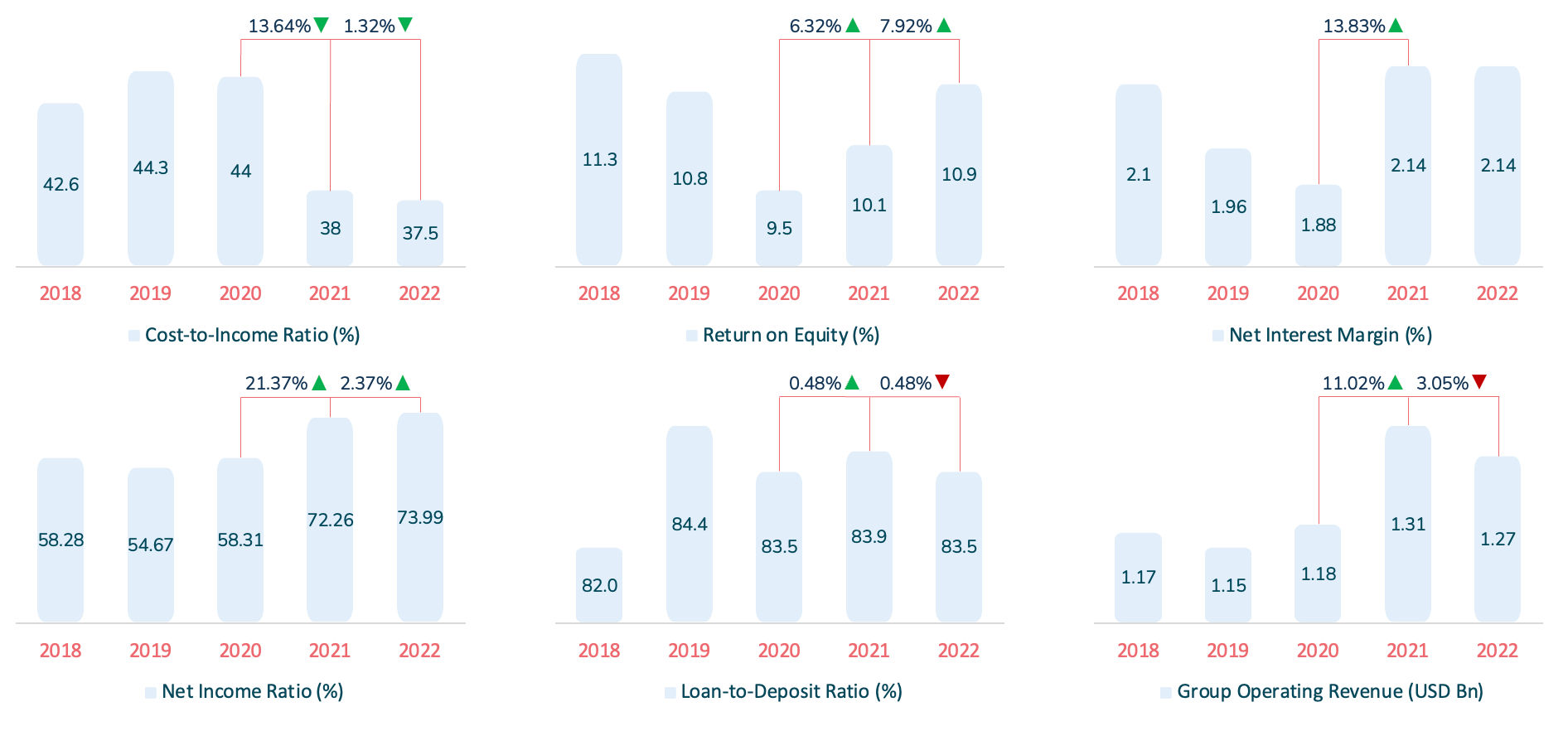

Operational efficiency at HLB

The bank has been working hard, implementing various efforts to manage operating expenses tightly. The result – a significant improvement in the cost-to-income ratio, dropping from 44% in FY2020 to 38% in FY2021 and decreasing further to 37.5% in FY2022.

As for HLB’s NIM (net interest margin), it has remained mostly the same from FY2021 at 2.14%, driven by an increase in net interest income. This rise can be attributed to the bank expanding its loans and financing portfolio across key segments.

Charting on a higher note, the bank fits well within the ideal LDR (loan-to-deposit ratio) range of 80%-90%, as indicated by its performance over the past five years (Figure 1).

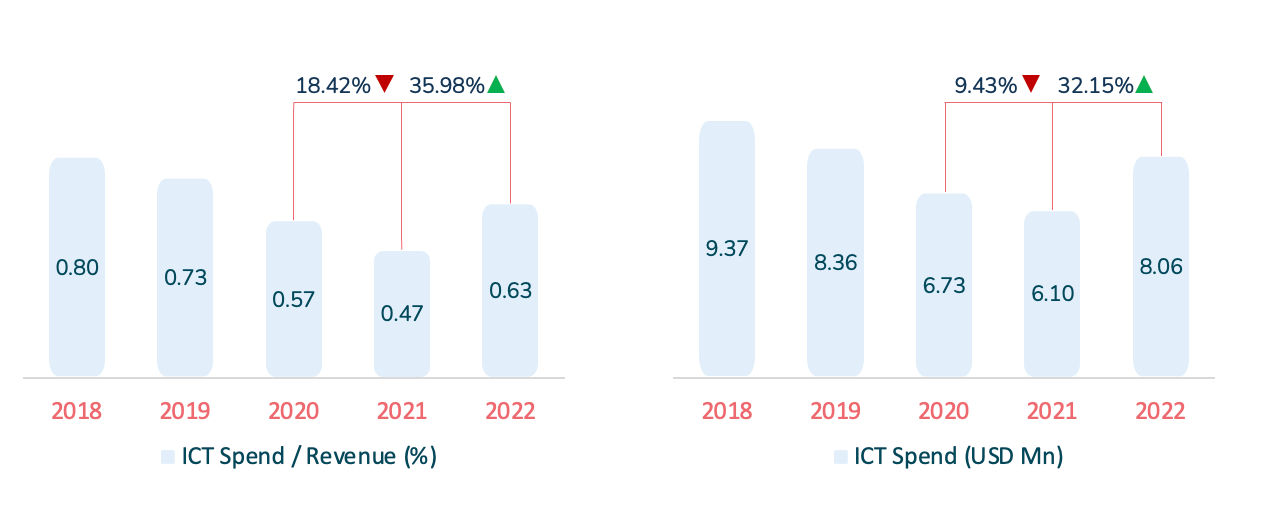

While HLB’s ICT spending witnessed a downward trend between FY2018-FY2021, results from FY2022 express the bank’s increasing sentiment towards technology (Figure 2). However, the percentage of ICT spend-to-revenue is still lower than other Malaysian banks covered in this benchmarking study (e.g., RHB, Maybank).

HLB’s strategic focus areas

- #1 Digital at the core

Taking a nosedive into the digital space, HLB went all in, only to emerge even stronger by the end of 2022. HLB has achieved the following:

- 1.9 million users on the HLB Connect app and >2.34 million on the HLB Connect online platform.

- 91% of all banking transactions were digital, conducted via the HLB app and the web platform, resulting in a 23.6% increase from FY2021.

- 18% growth in customer base across all digital platforms.

HLB also launched the following:

- ConnectFirst is geared towards business customers and scaling regional growth to cater to business customers’ needs in the digital era.

- An online Business Account Application feature that reduces online onboarding time for new-to-bank business customers from 7 days to as little as 30 minutes.

- The BizBuddy app (launched in FY2022) empowers business owners to accept customer payments via various QR code options, monitor transactions in real-time, and instantly refund any same-day purchase cancellations.

Adding to this, HLB has automated the analysis of customers’ bank statements, shortening the bank statement/credit assessment turnaround time from 2 hours to as little as 1 minute.

- #2 Building services around customers

HLB is determined to drive seamless and convenient banking by meeting customers’ needs and establishing a presence on various platforms.

HLB’s Shopee store (established in FY2021)

- HLB has become the first Malaysian bank to establish an online store on Shopee, quickly becoming an important channel in driving CASA growth.

- Although the store currently offers 8 HLB CASA products, it has accumulated over 100,000 followers while maintaining a shop rating of 4.8 since its launch.

- HLB has successfully opened over 33,000 new CASA accounts for its customers through this channel alone. HLB’s presence on Shopee cannot be understated, as it enables customers to open a bank account without a physical branch visit.

Apply@HLB

Customers can open a bank account through the:

- Apply@HLB app,

- or by scheduling a visit with the bank’s Deposit Relationship Manager, who will complete the onboarding process through HLB’s Customer Onboarding and Servicing iPad solution, which was developed in-house.

In fact, 85% of all new customers in FY2022 were onboarded digitally, either through the Apply@HLB app or via the iPad.

- #3 Enriching employee growth

A fulfilled, empowered workforce is a strong foundation for any business. And HLB understands this perfectly, with a clear aim to foster professional career growth by encouraging employees to experience multiple career paths within the organisation. As a result, HLB organised its first Career Day in FY2022 to offer insights into different career paths available within the bank.

The 70:20:10 Learning Framework by HLB encourages employees to take the first step, be proactive and own their growth development.

- 70% on-the-job learning.

- 20% learning from others.

- 10% structured learning.

In HLB, all employers must fulfil a minimum of 40 hours of training per fiscal year, with at least one training day focused on digital or sustainability subjects or both. In addition, over 50,000 e-learning courses are available to the workforce via the Disprz platform on HLB@Workday.

A holistic approach is vital to ensure employee well-being is always treated with utmost care. Expanding upon the concept, HLB created PlusVibes, the bank’s mobile-first well-being platform, to help employees build personal resiliency and strength, both physically and mentally. In October 2022, PlusVibes was relaunched with new features and improved user functionality. In addition, employees can connect with a qualified counsellor via the app if they require further assistance.

- #4 Environmental and social impact

HLB has made strides in reducing its environmental footprint in FY2022. The bank’s energy-saving measures have witnessed the bank’s Scope 2 emissions fall by 17.3% in FY2022 compared to the baseline year (FY2019). Overall, HLB’s energy, water, and paper consumption fell by 6%, 19%, and 34.6%, respectively, from the previous year.

HLB Singapore launched Southeast Asia’s first biodegradable debit card to enhance sustainability efforts. The card is created from bio-sourced materials, making it 82% biodegradable and minimising its ecological footprint.

The bank invests in continuous efforts to improve financial literacy and accessibility. For example, the HLB@School and HLB@Kampung initiatives aim to promote financial literacy and drive the movement toward a cashless ecosystem in both schools and rural areas of Malaysia. These initiatives overarch to educate students with the essential knowledge necessary to manage finances and bridge the country’s socioeconomic gap.

Finally, HLB also launched a first-of-its-kind ’talking ATM’ to serve visually impaired customers in Kuala Lumpur and Penang to drive financial inclusion.

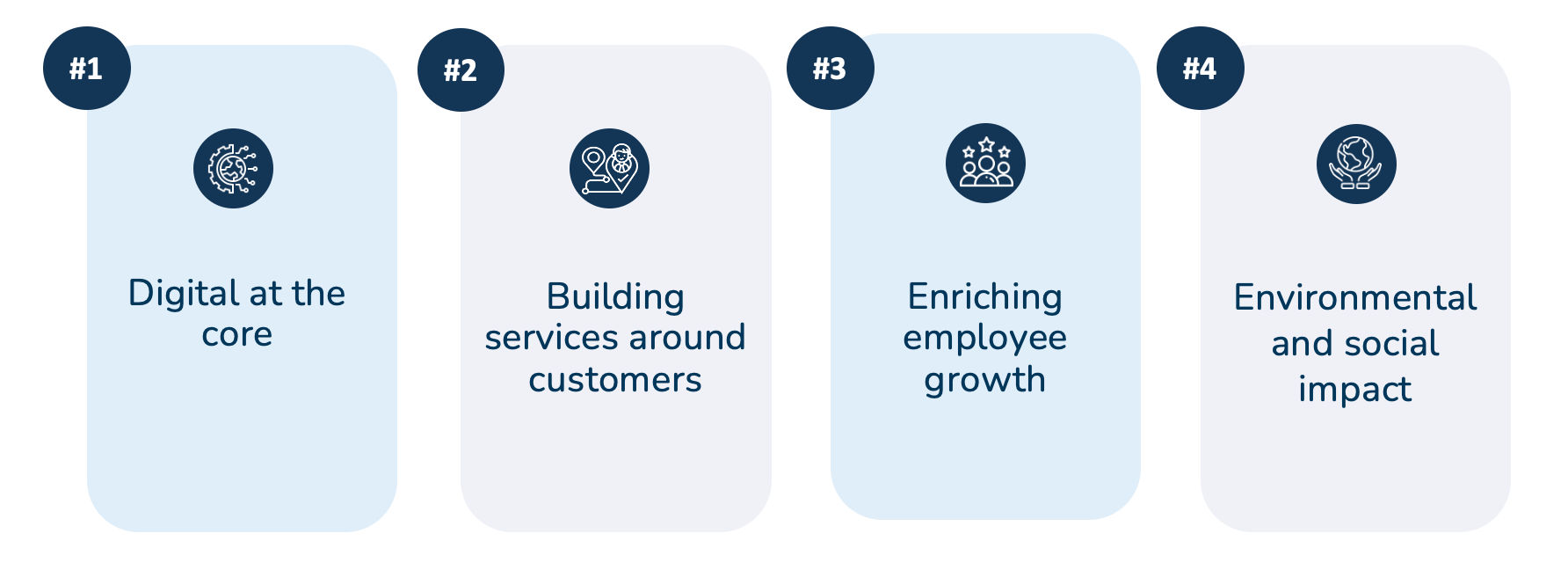

HLB’s digital strategy

HLB plans to deliver its digital strategy through the following (Figure 4).

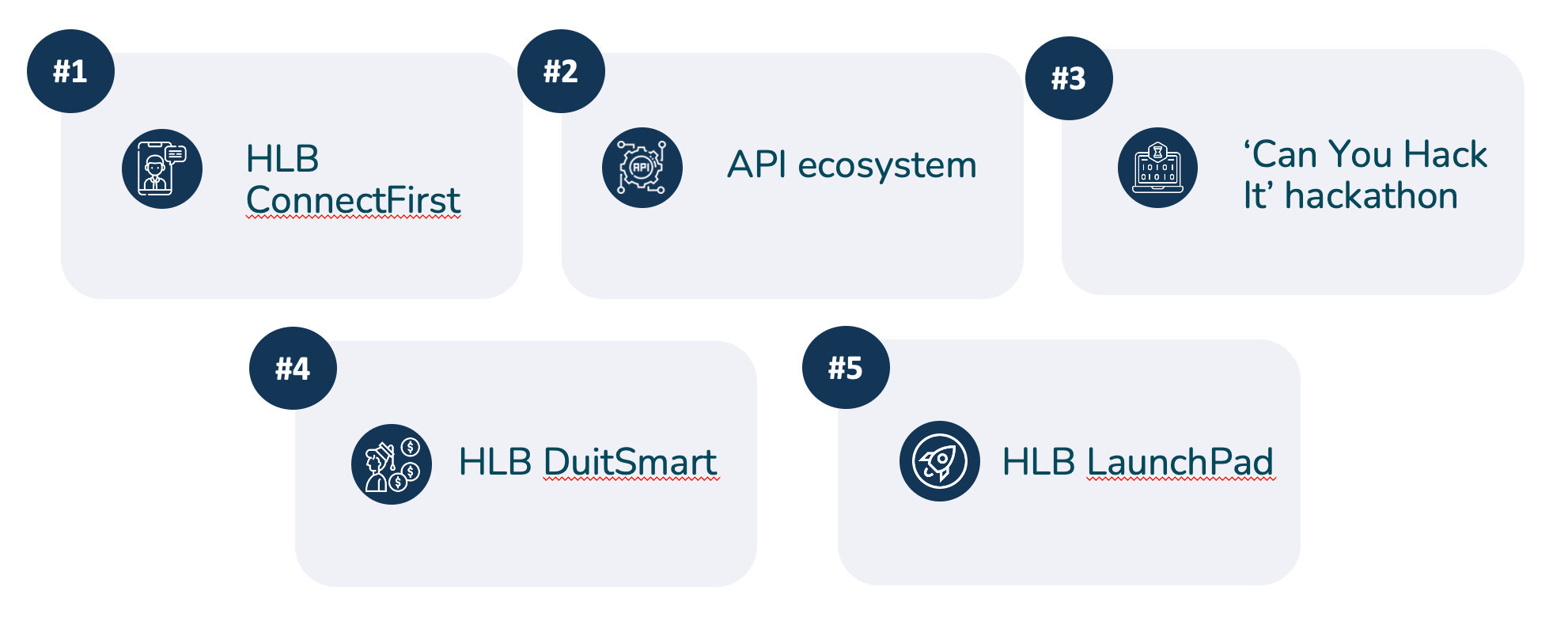

HLB’s technology innovation

- #1 HLB ConnectFirst

Being the next-generation digital banking platform for its business customers, HLB ConnectFirst provides a consolidated view of customer payments, transactions, and accounts alongside an intuitive UI/UX interface that runs smoothly across all devices.

In addition, HLB ConnectFirst allows users to view account balances, authorise transactions, and access biometric-enabled eToken capabilities. Since the launch of the ConnectFirst platform, HLB’s digital business customers have grown 11% YoY to nearly 100,000, averaging 1.5 million financial transactions per month.

- #2 API ecosystem

With HLB continuously working to develop its existing API ecosystem, the bank introduced corporate settlement API in FY2022. This enables customers to integrate their various operating systems with ConnectFirst. For example, customers can integrate their payroll and accounting systems with ConnectFirst to allow seamless processing and payments of their payrolls. In addition, the platform can support multiple single, online, and bulk payments/transfers.

In addition to the corporate settlement API, HLB has built and enabled an API for third-party SMEs. This API allows the third party to integrate and use HLB’s payment rails to enable instant transfers from the third party’s wallet to any financial institution in Malaysia.

- #3 Can You Hack It hackathon

In October 2022, HLB organised the “Can You Hack It” hackathon to build a pipeline for fit-for-future talents. HLB designed the program to co-create innovative solutions focused on re-imagining banking experiences through hyper-personalisation and the Metaverse.

In fact, participants were expected to create unique and personalised customer experiences that exploit the full potential of what the Metaverse has to offer. The previous year’s hackathon focused on solving ESG problem statements.

- #4 HLB DuitSmart

As the bank’s flagship financial literacy program that launched in 2019, it continues strong, inching closer to its goal – make financial knowledge simple and accessible for all Malaysians through bite-sized and easily digestible content.

HLB DuitSmart further aims to foster enthusiastic learning and application of financial principles. In FY2022, HLB DuitSmart was piloted through online workshops at secondary schools and tertiary education institutions, and garnered very positive feedback.

- #5 HLB LaunchPad

With a 2017 launch, the program continues to support and mentor tech entrepreneurship and startups, leveraging digital to develop innovative solutions for better and more sustainable business resilience. In FY2022, HB selected three partners (Datacultr, Alfie Tech, and Qresit) to focus on solving sustainability-related pain points to make a positive ESG impact.

Growth opportunities for HLB today

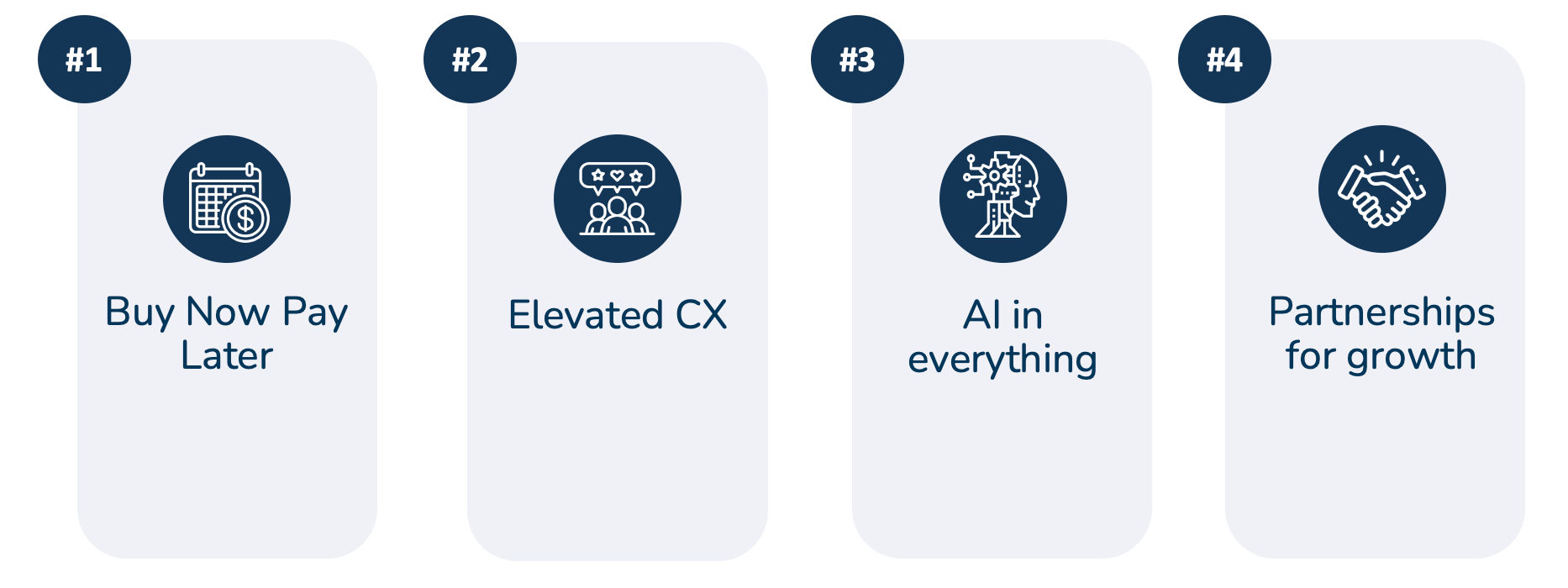

- #1 Buy Now Pay Later (BNPL)

HLB currently offers the Flexi Payment Plan (FPP) as its BNPL solution for the Malaysian market.

Flexi Payment Plan (FPP)

- Available to all HLB credit card customers via HLB Connect, either on the online banking platform or the app.

- Allows customers to convert any retail transaction of:

- >RM 500 into a 6-month instalment plan

- >RM 1,000 into an 18-month instalment plan

- >RM 2,000 into a 36-month instalment plan.

- Fixed interest rate of 8.99% per annum, but currently offers a rate of 0%-3.88% as part of a promotion until March 2023.

In comparison, a major competitor in the Malaysian BNPL market is Atome. Atome offers their BNPL service via the Atome app and provides a standard 3-month instalment plan for items purchased with their partners. However, Atome does not charge interest for its BNPL services; instead, it charges partner merchants a service fee. On top of that, Atome also charges their customers a flat fee of RM 30 for late payments.

HLB can strengthen its position as a BNPL player by implementing the following:

- Convert its current 0% interest rate on 3-month instalment plans to a permanent offering.

- Offer BNPL to existing customers with debit cards to increase attachment rates.

- Partner with merchants to promote their BNPL service by offering discounts on purchases when using the bank’s BNPL option.

- Leverage its resources as an established financial institution to develop innovative BNPL offerings, such as implementing AI to analyse customers’ transaction histories to determine credit

- Utilise its reputation as a trustworthy institution to the bank’s advantage to promote and attract more customers.

- #2 Elevated CX

HLB maintained good CX performance in FY2022, with customer satisfaction scores of 4.41 out of 5 and 4.28 out of 5 from its mobile and internet banking users, respectively. HLB also reduced unscheduled downtime by 48% compared to the previous year.

Its in-house CX Lab drives HLB’s efforts to provide an exceptional customer experience.

- Promotes cross-departmental cooperation while providing conducive settings for product idea generation and prototyping.

- Gathers insights through various techniques, including A/B testing, gaze tracking, quantitative and qualitative research, and ethnographic research.

- Enables the CX Lab to evaluate and act upon comprehensive consumer insights to better address consumer needs.

In FY2022, the Lab ran the following:

- 27 customer research projects,

- 59 usability testing sessions,

- 13 post-launch evaluation initiatives.

Currently, HLB’s ‘Built Around You’ ethos takes the form of multiple apps and platforms catered to specific customers (e.g., HLB Connect for retail customers, HLB ConnectFirst and BizBuddy for business customers, and HLB Pocket Connect for junior customers). In addition, the bank has chatbots on its web platform and mobile apps to handle customer queries.

However, HLB’s apps and platforms lack personalised insights that can enable the bank’s customers to make better informed financial decisions. HLB should also integrate ML into its platforms to allow customers to receive personalised prompts regarding their spending and saving habits.

Additionally, HLB should explore the potential of gamification in elevating the customer experience. For example, HLB’s Pocket Connect app for junior savers has the ‘Earth Hero’ mission to encourage young customers to earn, save, and spend while contributing to reforestation efforts. HLB should also extend this offering to its adult customers via the HLB Connect app to boost environmental appreciation efforts and encourage customers to engage with the app (e.g., CIMB’s OctoMissions).

HLB can also pursue customer journey mapping to run parallel with the CX Lab. Customer journey mapping is a method of visualising customer interactions, allowing employees to truly understand and empathise with their customers and, by extension, result in more innovative ways to meet customers’ needs. The top leaders of HLB can actively partake in these efforts by owning customer journeys (e.g., DBS) or being involved with the bank’s existing CX Lab.

- #3 AI in everything

HLB has two AI-powered chatbots, each to serve customers and employees. The AI chatbot for customers is present on the bank’s web platform and apps, while the employee-centric chatbot is called HALI.

HALI was launched in 2018 to answer queries related to the policies and procedures of HR and Branch Operations Support. In 2019, HLB implemented HALI alongside a Virtual Recruitment Assistant in its recruitment process to match suitable candidates with high-skill jobs.

Further opportunities for HLB to expand use cases within the organisation include:

- Using AI as a powerful tool for credit scoring to reduce bias and drive financial inclusion.

- Implementing AI in fraud prediction and detection (e.g., CIMB).

- #4 Partnerships for growth

In FY2022, HLB partnered with Payments Network Malaysia (PayNet) to launch ‘Project Cashless Kampung’ in Sekinchan as part of the bank’s efforts to ensure all its residents would have access to banking services and facilities. The project’s initial phase will see HLB facilitating account opening and debit card issuance for residents without requiring them to visit a bank branch.

Apart from this, HLB completed the 4th iteration of its mentorship program, HLB LaunchPad, in collaboration with ecosystem partners. HLB LaunchPad aims to nurture young Malaysian entrepreneurs and foster collaboration with emerging fintech practitioners and tech-savvy startups.

HLB also engages with social enterprises. For instance, the bank onboarded its 5th social enterprise (Benak Raya Enterprise) in FY2022.

While partnerships to enable financial inclusion and mentor startups are commendable, the bank should also focus on technology partnerships to enable growth. HLB should also explore opportunities for technology partnerships in blockchain-based smart contracts (e.g., OCBC, UOB), which will enable finance documents to be securely verified. Concurrent to this, HLB should explore the application of smart contracts for:

- Internal business.

- Retail consumers.

- Peer-to-peer transfers.

- Trade finance.

Conclusion

HLB is committed to providing impactful and seamless digital experiences for its customers. The bank is continuously devising ways to support business customers, striving towards financial inclusion through its app for junior customers and social enterprise partnerships. However, HLB can push the envelope of its customer offerings by exploring new possibilities, such as BNPL and smart contracts, as well as the integration of AI into more use cases within the bank.