Company Insights

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

HSBC (Group financials)- An overview as of 31st December 2020

| Bank Name | HSBC |

| Headquarters | Hong Kong |

| Operating income (as of 31st December 2020) | USD 50.4 billion |

| Group net profit (as of 31st December 2020) | USD 12.1 billion |

| Total assets | USD 2.98 trillion |

| Employees | 232,957 |

| Countries of operation | 64 |

| Number of branches | Not available |

| Technology spend (as of 31st December 2020) | USD 5.5 billion |

| Number of customers | 40 million |

| Market capitalisation | USD 107.23 billion |

| Operating revenue CAGR growth (2016-2020) | 0.08% |

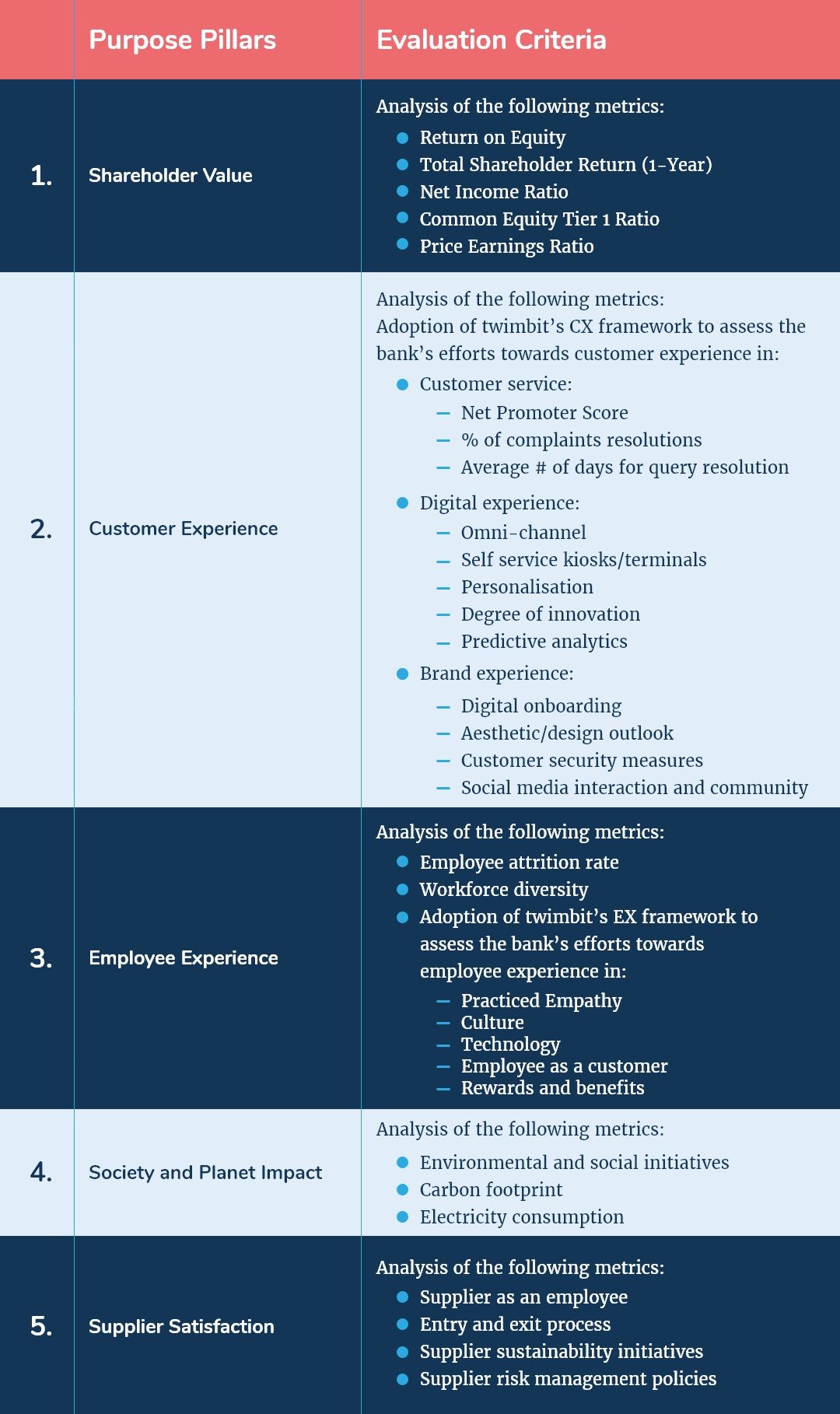

Shareholder value (31st December 2020)

| Return on Equity (as of 31st December 2020) | 2.3% |

| Total Shareholder Return (1-Year) | 12.1% |

| Net Income Ratio | 9.67% |

| Common Equity Tier 1 Ratio | 15.9% |

| Price Earnings Ratio (as of 31st December 2020) | 27.27% |

Awards

| 2020 | Euromoney Awards for Excellence 2020 World’s Best Bank for Sustainable Finance World’s Best Bank for Transaction Services Hong Kong’s Best Bank The Banker Innovation in Digital Banking Awards 2020 Best Digital Bank in Asia Asia Insurance Industry Awards 2020 Life Insurance Company of the Year PWM Wealth Tech Awards 2020 Best Global Private Bank for Digital Customer Experience Stonewall Stonewall Top Global Employers List – 2020 |

HSBC and its strategic focus areas

- Business strategy

The business strategies HSBC has for 2021 focuses on adapting to the fundamental shifts in the financial services sector, such as a low-interest-rate environment and increased digital engagements. In each of its global businesses, the bank aims to invest in areas where it is strongest and has further opportunities for growth. More specifically, the bank intends to achieve double-digit growth in profit after tax (PAT) in Asia.

- Wealth and personal banking

- HSBC is focusing on growing its wealth revenue by more than 10% of the compound annual growth rate, investing over USD 3.5 million in Asia until 2025.

- The bank aims to serve high and ultra-high net worth customers in Southeast Asia, China and Hong Kong.

- HSBC is focusing on growing its wealth revenue by more than 10% of the compound annual growth rate, investing over USD 3.5 million in Asia until 2025.

- The bank aims to serve high and ultra-high net worth customers in Southeast Asia, China and Hong Kong.

- Commercial banking

- HSBC aims to become a leader in supporting cross-border trades and serving mid-market corporates.

- The bank will invest USD 2 billion over five years to 2025 across global platforms, such as Global Liquidity and Cash Management as well as Global Trade and Receivables Finance and Foreign Exchange, to drive more fee-related income.

- It will also develop front-end ecosystems to drive its international mid-market client acquisitions at scale.

- Global banking and markets

- HSBC will focus its investments towards enhancing digital platforms for its Asian propositions. These include structured products, and foreign exchange, market access, and execution capabilities in Global Markets and Securities Services.

Initiatives for 2020

- HSBC Pinnacle– The bank launched a new financial planning business in mainland China, offering insurance solutions and wealth services outside branches. The wealth advisors provide a single tailored proposition for multiple needs, such as life and health protection, education savings, retirement and legacy planning. HSBC aims to deliver a seamless customer experience between digital channels and wealth planning experts.

- Partnership with SHOPLINE– The Hong Kong-based ecommerce shopping platform supports over 250,000 merchants online. HSBC is helping SHOPLINE by integrating advanced digital capabilities, such as Business Collect and PayMe for Business, into the platform’s propositions.

- Supporting Rolls-Royce with a capital markets drive– Rolls-Royce, the blue-chip FTSE 100 engineering company, needed to raise additional liquidity due to the COVID-19 outbreak. HSBC acted as the joint global coordinator on a USD 2billion fully underwritten rights issue, receiving strong support from Rolls-Royce shareholders with a 94% take-up. The rights issue was the largest equity capital markets transaction the bank acted on in the U.K. in 2020. This move demonstrates the bank’s expertise in offering holistic solutions to clients across equity and debt.

- Customer experience

HSBC aims to harness the power of digital by providing products and services that merge seamlessly into the lives of its customers. It is also deploying technology to support customers and businesses relentlessly through the COVID-19 pandemic.

- Making banking simpler and faster

- Introducing video meetings for customers on the onset of COVID-19 and expanding the use of chatbots for day-to-day queries.

- Launching digital and in-app chat services for customer queries and complaint resolution across eight new markets.

- Personalised services

- The bank is deploying statistical, machine learning (ML) and visualisation techniques to convert data into behavioural signs.

- It analyses shopping patterns, land use, journey to work, and foot traffic to decide where to position a branch or ATM.

- Helping businesses grow

- The securities services division is developing client solutions for fast access to data and more control of their assets and transactions.

- The Smart Serve platform provides a more secure front-end digital Know-Your- Customer solution.

- Responding to business needs

- The bank supported customers facing financial pressures due to lockdown restrictions. It provided lending support to 237,000 wholesale customers globally through government schemes and its very own initiatives.

- HSBC offered repayment holidays and trade finance solutions to support customers with their supply chains during the pandemic. It also launched online portals for various government-initiated loan schemes.

- The bank set up a team to help oversee the provision of loans and expediting the turnaround time for loan requests.

- Providing instant customer support

- HSBC is launching a new wealth assistant bot in mainland China, enabling customers to get immediate help with investment decisions.

- The bank’s mobile banking app provides instant messaging and a 24-hour bot to support corporate and personal customers.

Initiatives for 2020

- Wealth View– The wealth management business introduced a simplified version of its online platform, Wealth View, to facilitate easier portfolio analysis and transactions.

- HSBC Kinetic– The bank introduced a new SME proposition, HSBC Kinetic, for its UK SME customers. Through this app, customers can submit an online application for a Business Bounceback loan from the U.K. Government and do their day-to-day banking digitally.

- Blockchain for efficiency– Within the global trade business, blockchain is replacing paper-driven credit processes previously guaranteed a seller his payments. This fast and secure alternative has reduced the credit processing time from 5-10 days to a few hours.

- VisionGo- Launched a digital platform in Hong Kong where entrepreneurs and small businesses can network and share their knowledge.

- The bank launched new apps, websites and security platforms in 16 markets for improving the digital banking experience.

- HSBC Scholar program– The bank introduced a platform within the WeChat ecosystem mainly catering to customers in mainland China planning to fund overseas education for their children. It provides practical guidance on overseas education. For instance, it highlights the top places to study and best areas to live, information on setting up utilities in a destination country or getting insurance.

- HSBC Community– This is the bank’s digital initiative to reward customers for gaining financial knowledge.

- Life insurance product– In Hong Kong, the bank built an algorithm to make the application for a basic life insurance product easier. It analyses a range of data, such as credit transaction information, to rate a customer’s eligibility for the product. By doing so, it relieves customers from answering extensive application questions.

- Employee experience

HSBC is striving to build an inclusive work environment, one that emphasises wellbeing, invests in learning, and prepares its people for the future of work.

- Diversity and inclusion

- As a part of its diversity and inclusion initiatives, HSBC is launching the global ethnicity inclusion programme and moving forward with its global disability confidence programme.

- The bank is running a self-identification campaign to collect and report employee ethnicity data in 21 countries as part of a global diversity data project.

- Building skills of the future

- HSBC has invested in a flagship ‘future skills’ programme to prepare its staff for the changing skills required in the future workplace.

- The bank is deploying technology to improve career development by matching employee skills and aspirations with its business needs.

- Supporting self-development

- HSBC University is a platform for learning via an online portal, a network of global training centres and third-party providers.

- The bank’s career portal includes guidance on career development and change management. It also highlights information on giving back to the organisation and communities in which HSBC operates.

- The bank launched a global mentoring system in 2020 to enable colleagues to match with a mentor or mentee.

- Digital adoption in HR management

- The bank is transforming its HR services and employee experiences, along with empowering its workforce.

- HSBC has deployed digital HR services, making it easier for the bank’s people to make data-driven decisions and access HR content, services and support.

Initiatives for 2020

- During the year, HSBC achieved its target of having at least 30% women holding senior leadership positions.

- Cyber hub- The bank’s cyber hub brings together training, insights, events and campaigns on how to combat cyber-crime. It also supports the senior management in understanding and applying ethical practices using Big Data and AI.

- Digitalisation in HR

- Technical adoption has improved payroll, workforce administration, employee data management and communications, helping HSBC manage talent, succession, career development and performances.

- By increasing the access to data and insights, HSBC is enhancing the ability of its leaders to leverage talent within the bank and improve decisions made about their teams.

- The bank has also adopted a new cloud-based technology that focuses on improving services and innovation rather than expensive maintenance and upgrades to legacy, on-premises technology.

- The bank supports the Technovation Girls programme, which inspires girls globally to design and code applications that solve problems in their community.

- Society and planet impact

The bank’s primary goal is to transition towards a low carbon future. HSBC is setting sustainability standards not just for its operational activities but also inculcating these criteria in its supply chain and lending decisions.

- Becoming a net-zero bank

- The bank is making changes within its operations and those of its customers through the financing portfolio.

- It aims to bring its operations and supply chain to net-zero by 2030.

- HSBC will also ensure that it is financing the carbon emissions of portfolio customers in accordance with the Paris Agreement goal.

- HSBC will provide between USD 750 billion and USD 1 trillion of sustainable financing to its customers.

- Reducing operational emissions

- At present, electricity contributes 92% towards the bank’s carbon emissions. HSBC aims to reduce this figure by 50% in the next ten years by transitioning towards renewable energy.

- The bank will also encourage the use of technological solutions for employee and customer connectivity to minimise travel emissions.

- Unlocking new climate solutions

- The bank will donate USD 100 million to a program that supports new and scalable climate solutions. It is working with various partners to accelerate investment in natural resources, clean technology and sustainable infrastructure.

Initiatives for 2020

- Sustainable financing

- Supported the Egyptian government in launching the Middle East’s first sovereign green bond.

- Helped a German household goods company, Henkel, to issue the first plastic reduction bond.

- Issued the first transition Islamic bond to enable Etihad, a Middle Eastern airline, to become more sustainable.

- Sustainable infrastructure

- Finance to Accelerate the Sustainable Transition-Infrastructure (‘FAST-Infra’)- This initiative, established under the One Planet Lab, aims to develop a globally standardised labelling system for sustainable infrastructure investment

- Backing new technologies and innovations

- HSBC aims to connect financing and fresh thinking by helping climate solutions projects to scale. It provided USD 7.1 million to its non-governmental organisation partners during FY2020 to get the programme underway.

- HSBC Pollination Climate Asset Management- The bank launched this program in August 2020 in partnership with Pollination, a climate change advisory and investment firm. Through this venture, the bank will set up investment funds for projects that protect the environment over the long term and reduce greenhouse emissions. It is the first large-scale venture to invest in natural capital as an asset class.

Digital Strategy

The bank’s digital strategy aims to increase and accelerate investments in technology to enhance customer capabilities in return. In order to deliver a personalised and engaging customer experience, HSBC is deploying the following strategies:

- Commitment to customer-centricity- The bank wants timely and relevant insights and bite-sized content, including gamified learning, networking platforms and social-sharing functionalities.

- Engaging experiences- Through AI-driven technology in gamification and personalised online activities, HSBC helps customers become more financially aware and engaged.

- Harnessing the benefits of blockchain- The bank is implementing distributed ledger technology, including blockchain, to improve efficiency, transparency and security for its clients.

Initiatives for 2020

- Digital banking features

- Digital onboarding- Customers can apply to open a current account online in just 10 minutes and get approval within 60 seconds.

- Global money account- Customers can transfer multiple currencies within seconds using the app at no extra cost. This feature, currently available in the US and UAE, allows customers to spend like a local when travelling internationally.

- PayMe- The bank’s social payment app in Hong Kong makes it easy to split bills with friends for restaurant bills, joint gift purchases or bulk orders. The app has handled a 47 per cent rise in peer-to-peer transactions in 2020.

- Global wallet- This feature simplifies international business dealings. Customers can hold, send, and receive cash in multiple currencies, easily and securely, using a single global account.

- Machine learning (ML) at ATMs- HSBC uses ML to inform how it distributes cash to ATMs in Hong Kong. Its data tool forecasts withdrawal patterns accounting for location, holidays and events. It also ensures that the right amount of cash is available at every place, thus cutting down on deliveries and being environment-friendly.

- Digital smart branch features

- Digital video wall- A screen displaying the latest updates and offers on products and services.

- Digital interactive board- An interactive board for effective collaboration, presentation and review of a customer’s financial needs.

- Digital service kiosks- A simplified platform to offer over 35 banking, payment and credit card services.

- Digital ATM notices- A display to easily stay updated on the bank’s regulatory notices.

- Digital account opening- Simplified account opening with reduced turnaround times.

- Video banking- Virtual assistance by service managers for a customer’s banking needs.

- HSBC Omni Collect– It is a one-stop solution that enables businesses to offer multiple payment options to customers. Omni Collect gives a consolidated view of digital collections across multiple channels, including bank transfers, card payments and e-wallet transactions. It supports online and in-store payments, consolidating them into a single interface. Thus, businesses obtain a seamless customer experience.

- LiveSign– The bank launched LiveSign, a feature that allows customers to sign digitally and submit documents without visiting a bank branch.

- HSBCnet Mobile– The bank upgraded its corporate banking mobile app, making it easier for clients to manage their finances, pay employees and forecast cash flows anytime, anywhere.

- Digital bonds– The bank launched the contour blockchain trade platform, offering customers better speed, simplicity and working capital efficiency. It tested blockchain technology to facilitate a fully digitalised bond issuance.

- XiaoLingTong– Adding gamification to digital banking, HSBC launched ‘XiaoLingTong’ where customers can play as an avatar. It allows customers to acquire knowledge in areas like investing and retirement planning. By doing so, they accumulate points and unlock benefits like exclusive product offers.

- VisionGo- Many small and medium-sized business entrepreneurs (SMEs) often looked for support with the basics of running a company, including finance, legal, human resources and marketing. HSBC created an AI-enabled platform in Hong Kong for peer-to-peer knowledge sharing to suit this purpose, called VisionGo. This community has already become the largest in the country as of Q12021.

- In-branch robot assistant- HSBC introduced ‘Pepper’, a robot in its flagship branch in Manhattan. The robot answers basic customer questions and guides them to the respective advisor at the branch. Therefore, it makes the branch visit smoother and more efficient for the customer while not eradicating human intervention.

IT Strategy

HSBC aims to spend between USD 5 billion and USD 5.5 billion in technological capabilities between 2020-2022 to drive down its cost base to at least USD 31 billion by 2022. Besides automation in client processes, an essential area of technological investments is cybersecurity strength.

- HSBC is investing in the use of AI and advanced analytics techniques to manage financial crime risk. It has also published principles for the ethical use of Big Data and AI.

- The bank is modernising its data and analytics infrastructure by investing in advanced capabilities in the cloud, visualisation, ML and AI platforms.

- HSBC prioritises its IT expenses towards enhancing cybersecurity capabilities, such as Cloud Security, metrics and data analytics, identity and access management, and third-party security reviews.

Initiatives for 2020

- HSBC launched an investigative tool, a global social network analytics platform, which supports the detection of high-risk activity across its trade finance business. By using a contextual monitoring approach, the platform has improved the accuracy and efficiency of its operations. It removes delays in approving genuine customer transactions while focusing attention on the behaviour concerned.

- The bank is applying ML techniques to improve its financial crime detection accuracy and speed.

- The Commercial Banking (CMB) business of HSBC developed a new global product inventory and lifecycle management system to help ensure optimal product governance. This system uses cloud technology to provide an improved way of managing products from approval all the way through to demise. H

HSBC and its ICT Contracts

- The bank has signed Amazon Web Services (AWS) as its long-term strategic partner to accelerate digital transformation and deliver personalised banking services. It will be deploying this technology across all lines of business. By migrating to cloud technology, the bank is automating key processes and enhancing operational efficiency. With the aim of developing new personal banking digital products, HSBC will adopt several AWS services such as storage, database, analytics, ML, and security.

7 Growth and Innovation Opportunities

- #1 Cost to serve

- The bank’s operating expenses decreased by USD 1.1 billion or 3% as it reduced performance-related pay and reduced discretionary expenditure during FY2020.

- Despite this decline, its cost-to-income ratio increased from 59.3% in FY2019 to 62.5% in FY2020. This incline can be explained by a USD 5.7 billion or 10% decline in the bank’s operation revenue due to lower global interest rates in all of the bank’s global businesses.

- Profit before tax of USD 12.1 billion was 45% lower than in 2019, primarily from a rise in expected credit loss (ECL) and a fall in revenue.

- ECL increased by USD 6.2 billion, mainly from charges in the first half of 2020 relating to the global impact of the COVID-19 outbreak on the forward economic outlook. There were also higher charges against specific customers in 2020, particularly in the oil and gas and wholesale trade sectors.

- Going forward, HSBC should aim to focus on industries that have a strong potential to recover and grow post the pandemic, namely healthcare, transportation and logistics, e-commerce and property and building materials sectors.

- A sound net interest margin management in a low-interest rate climate is achievable by identifying repayment risk in loans and attrition risk in deposits. The bank can use predictive behavioural models to revise its interest-rate risk models and hedging strategies continuously.

- HSBC should also increase focus on non-interest income and complementary revenue streams to offset the impact of high impairment charges.

- #2 Transformation of branch and its branch networks

HSBC has split its branch network into three formats, i.e. full-service, self-service, and cash service branches. The bank adopted modern technology within its branches, such as an in-branch robotic assistant, Pepper, and ATMs using ML. It also has plans to reduce its US branch network by around 30% to simplify the business and lower costs. Overall, between 2008 and 2020, over 13,000 bank branches closed in the US, representing 14% of all branches.

- Going forward, the bank can revamp its branch into a community hub, where individuals can connect with executives and socialise. They will also have access to all banking services and facilities. Some of the options include cafes, lounges, and pop-up stores.

- HSBC can also utilise its physical footprint for conducting workshops in and around topics like investments, savings, wealth management, retirement planning, etc.

- #3 Customer experience

- Personalised products– The bank should look at its customers’ journey from beginning to end and apply human-centred designs to develop relevant solutions. To develop and launch targeted financial products, the bank should:

- Form strategic partnerships with fintechs to collectively develop ‘pay-as-you-use’ products to give its customers a more flexible choice to switch between a myriad of product ranges.

- Offer byte-sized loan and investment products to make the customer journey towards their financial goals seamless.

- Employ predictive analytics and algorithms to show customers relevant products based on their preferences and saving or investing habits.

- Augmented and virtual reality capabilities- The bank has already adopted AI and ML to enhance customer experience. However, the neobanks in the Asian and UK markets are adopting aggressive digitalisation strategies. To remain a preferred bank amongst millennials, HSBC can go further to integrate Augmented and Virtual Reality (AR/VR) into its mobile banking apps. By using AR/VR glasses, customers can visit a bank branch virtually in an exclusively VR environment. It will enhance customer experience and reduce costs for HSBC, as it no longer needs to invest in physical locations.

- Additional mobile app features – The bank’s existing mobile banking app focuses primarily on supporting customers with their transactional needs to conduct quick and convenient digital banking. The bank can deploy the following strategies to strengthen its capabilities further:

- HSBC launched FinFitness, an initiative to encourage financial fitness for its customers. It measures fitness levels based on financial habits, knowledge and planning. Going forward, the bank should include this feature in its commercial banking mobile application by adding budgeting tools and a monthly spending tracker.

- The mobile app should include a bill prediction feature using ML to identify recurring bills and provide a timeline for upcoming payments.

- The app can implement evidence-backed recommendations to reduce spending and manage savings.

- #4 Business segment expansion

The bank’s wealth and personal banking businesses in mainland China have consistently recorded a negative revenue stream since FY2018. Its strategy for 2021 involves capturing opportunities to serve high and ultra-high net worth segments in China. Therefore, it has launched HSBC Pinnacle, a new financial planning business in the country. Under this initiative, the bank is planning to hire 3000 wealth professionals over four years. However, HSBC should also focus on reinventing its wealth management business by pushing towards digitalisation:

- HSBC should launch a mobile-based wealth management application for its high-net-worth customers to make transactions, monitor investment portfolios, and explore products such as mutual funds and bonds.

- The app should incorporate a digital dashboard with a 360-degree view of the customer’s entire financial situation, incorporating their financial life goals against their assets and liabilities.

- The bank’s financial advisors should be able to co-browse the customer’s wealth management tool in real-time to provide quicker and more effective services.

- It should adopt big data and analytics to provide more accurate data-driven financial advice than based on the human experience of the financial advisor alone.

- #5 Employee experience

- HSBC has invested heavily in employee development programs and provides a flexible work environment for building a productivity conducive work culture. However, to increase overall retention and stickiness of employees, the following are some facilities which the bank can provide to its personnel:

- Give its employees the option to work on cross-department projects for lateral career advancements.

- Extend pre-natal and child-bonding leaves with childcare assistance.

- Provide digital training for senior professionals to prepare them for the future of work.

- Creating a monthly piggy bank for Netflix, Spotify, gyms, etc.

- Building customisable compensation plans to include flexible share incentives, as well as fixed and variable components.

- As one of the largest employers from the banking industry, the bank should continue to adopt best practices for employee wellbeing by focusing on things such as:

- Sponsoring volunteer programmes to build a more empathetic and ethical workforce.

- Financing 100% of the education loans of its employees to attract and retain the fresh graduates they hire.

- Appoint a liaison for mental health and meditative programs.

- #6 Neo banking

One of the strategic focus areas for HSBC is to develop front-end ecosystems to drive international mid-market client acquisition at scale. Moreover, there remains a huge opportunity for penetration in the Asia Pacific as 46% of the SME funding demand remains unserved, which accounts for USD 2.414 trillion. To capture this market, HSBC should consider a revitalised digital brand that connects with the SME sector. It can adopt the following strategies:

- Identify and create a line of credit for SMEs who are potential first-time borrowers and don’t have access to credit facilities via traditional banks.

- Develop business advisory and management tools that will allow SMEs to make smart investment and banking decisions over digital platforms.

- Collaborate with e-commerce websites to extend credit to small vendors who wish to enter the online marketplace.

- Reduce merchant interchange reimbursement fees and roll out tactical card acquisition and usage campaigns, including low merchant discount rates.

- Provide personal and business overdraft facilities in addition to offering basic loan services to the SME sector.

- Adopt a flexible and fast loan approval mechanism that can provide same-day lending decisions to existing SME customers.

- #7 Society and planet impact

- HSBC has undertaken several initiatives to help its clients achieve their sustainability goals by unlocking innovative climate solutions. Moreover, the bank has set out minimum sustainability standards for suppliers under its ‘ethical code of conduct’.

- The bank’s energy consumption and carbon emissions are significantly higher than its regional competitors in the Asia Pacific. Electricity consumption contributes to 92% of the bank’s total carbon emissions. While it is currently working on shifting towards renewable energy, HSBC could also undertake some ‘green office’ measures. It can adopt the following strategies:

- Consciously create environmental-friendly green products, such as virtual cards, pulper cards, eco ink, and carbon control press machines.

- Launch supporting projects in impoverished areas, which help to preserve biodiversity and drive reforestation while furthering local economic mobility.

- Furthermore, to effectively transition towards renewable energy, HSBC could build on-site solar facilities and sign renewable agreements to add new wind and solar electricity to the grid.

- HSBC can minimise the amount of paper and plastic waste within branches and institute a 3R policy- reduce, reuse and recycle approach for waste management:

- Bank on plastic use within office premises

- Use of own cups, bottle and cutlery

- Recycled water used in washrooms and pantry

- Reduction in usage of paper for documentation

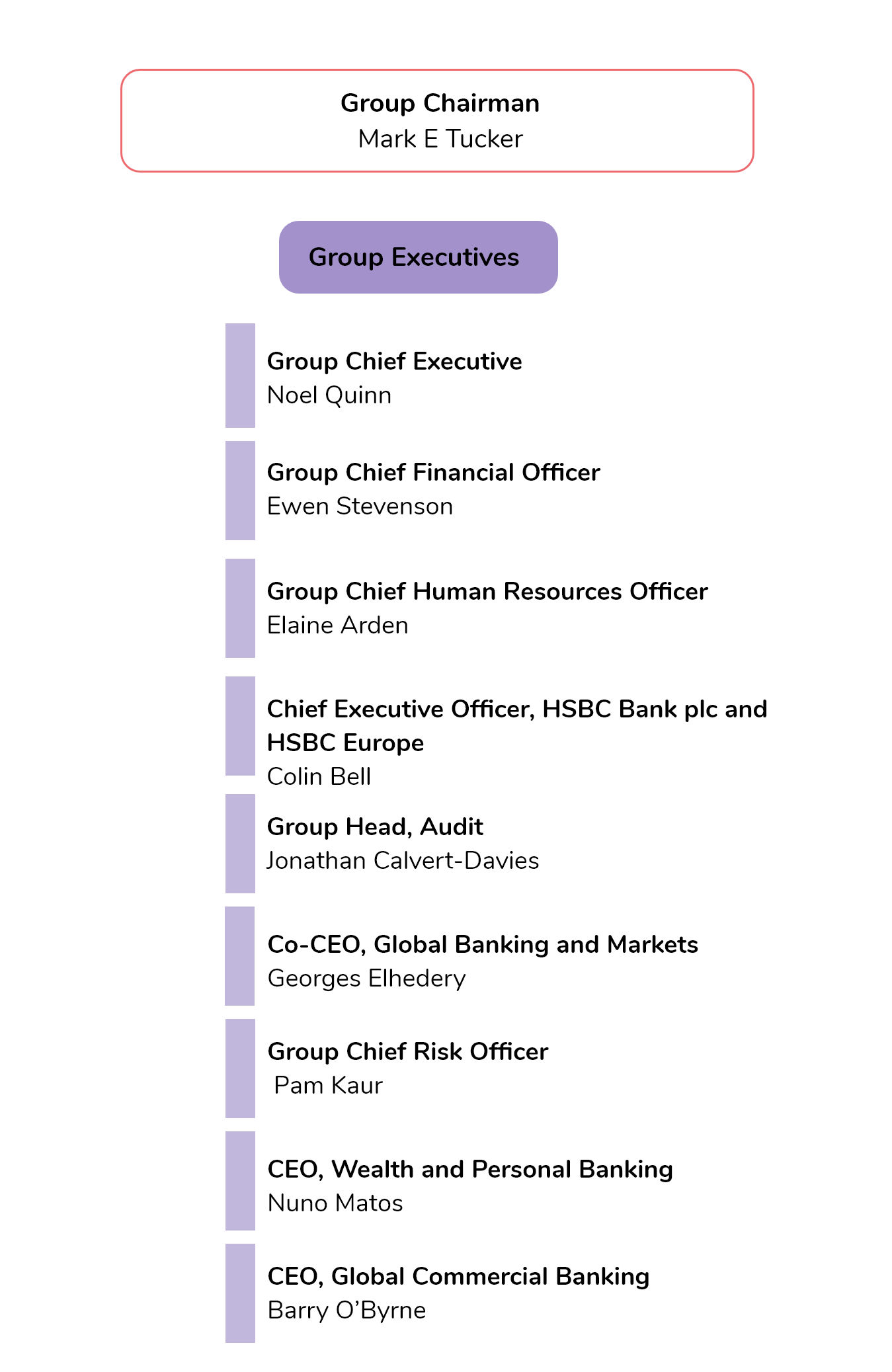

Organisation structure: Leadership

Executive Profile

Mark E Tucker

Group Chairman

With over three decades’ experience in the financial services sector of Asia and the UK, Tucker has immense knowledge of the industry and the markets in which HSBC operates. He previously held the position of Group Chief Executive and President of AIA Group Limited (‘AIA’).

Noel Quinn

Group Chief Executive

Noel Quinn has more than 30 years’ BFSI experience in the U.K. and Asia, of which there are over 28 years with HSBC. He was formally appointed as the Group Chief Executive in March 2020 and held the role as an interim from August 2019. Quinn also has experience in various management roles across HSBC since he joined the bank in 1992.

Quote

- Championing inclusion, Annual Report 2020

I believe passionately in building an inclusive organisation in which everyone has the opportunity to fulfil their potential.

Ewen Stevenson

Group Chief Financial Officer

Ewen Stevenson has over 25 years’ experience in the banking industry. He has served as an adviser to major banks and as an executive of large financial institutions. Stevenson was Chief Financial Officer of the Royal Bank of Scotland Group plc from 2014 to 2018.

Elaine Arden

Group Chief Human Resources Officer

Elaine joined HSBC as its Group Chief Human Resources Officer back in 2017. Before this appointment with the bank, she was at the Royal Bank of Scotland Group as its Group Human Resources Director. Arden is one of the members of the Chartered Institute of Personnel and Development and a fellow of the Chartered Banker Institute.

Colin Bell

Chief Executive Officer, HSBC Bank plc and HSBC Europe

Colin Bell joined HSBC in July 2016. Recently, the bank appointed him as Chief Executive Officer to HSBC Bank plc and also HSBC Europe on 22 February 2021. Bell has previously worked as the company’s Group Chief Compliance Officer and also led the Group transformation oversight programme.

Jonathan Calvert-Davies

Group Head, Audit

Jonathan Calvert-Davies joined HSBC as its Group Head of Audit in October 2019 and is a standing attendee of the Group Executive Committee. He has three decades of experience providing assurance, audit and advisory services to the banking and securities sectors in the U.K., the U.S. and Europe.

Georges Elhedery

Co-Chief Executive Officer, Global Banking and Markets

Georges Elhedery joined HSBC in 2005. He has since held the position of co-Chief Executive Officer for Global Banking and Markets in March 2020. Elhedery also heads the Markets and Securities Services division of the business.

Pam Kaur

Group Chief Risk Officer

Pam Kaur has held the role as the bank’s Group Chief Risk Officer since January 2020. She initially joined HSBC in 2013. Kaur previously was the Head of Wholesale Market and Credit Risk, as well as the Chair for the enterprise-wide non-financial risk forum.

Nuno Matos

Chief Executive Officer, Wealth and Personal Banking

Nuno Matos joined HSBC in 2015. The bank recently appointed him as the Chief Executive Officer of Wealth and Personal Banking, effective 22 February 2021. Matos was previously the Chief Executive Officer of HSBC Bank plc and also HSBC Europe, a role he held since March 2020.

Barry O’Byrne

Chief Executive Officer, Global Commercial Banking

Barry O’Byrne joined HSBC back in April 2017. The bank then appointed him as its Chief Executive for Global Commercial Banking in February 2020, which he also served on an interim basis since August 2019. O’Byrne previously worked as the Chief Operating Officer for Global Commercial Banking.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

HSBC, (2020, December). Group Annual Report

https://www.hsbc.com/investors/results-and-announcements/annual-report

HSBC, (2020, December). Environmental, social and governance (‘ESG’) review

https://www.hsbc.com/investors/results-and-announcements/annual-report

HSBC, (2020, December). Financial review

https://www.hsbc.com/investors/results-and-announcements/annual-report

Driving digital progress, (December, 2020). HSBC

https://www.hsbc.com/news-and-media/hsbc-news/driving-digital-progress

Getting smart about using data, (July, 2020). HSBC

https://www.hsbc.com/insight/topics/getting-smart-about-using-data

Digital banking: transcending transactions, (May, 2021). HSBC

https://www.hsbc.com/insight/topics/digital-banking-transcending-transactions

Harnessing the benefits of blockchain, (December, 2020). HSBC

https://www.hsbc.com/news-and-media/hsbc-news/harnessing-the-benefits-of-blockchain

A world of business opportunity in your wallet, (May, 2021). HSBC

https://www.hsbc.com/news-and-media/hsbc-news/a-world-of-business-opportunity-in-your-wallet

Gurinayat Brar, Research Intern, contributed to the research in conducting a preliminary literature review and conceptualising the article.