Company insights

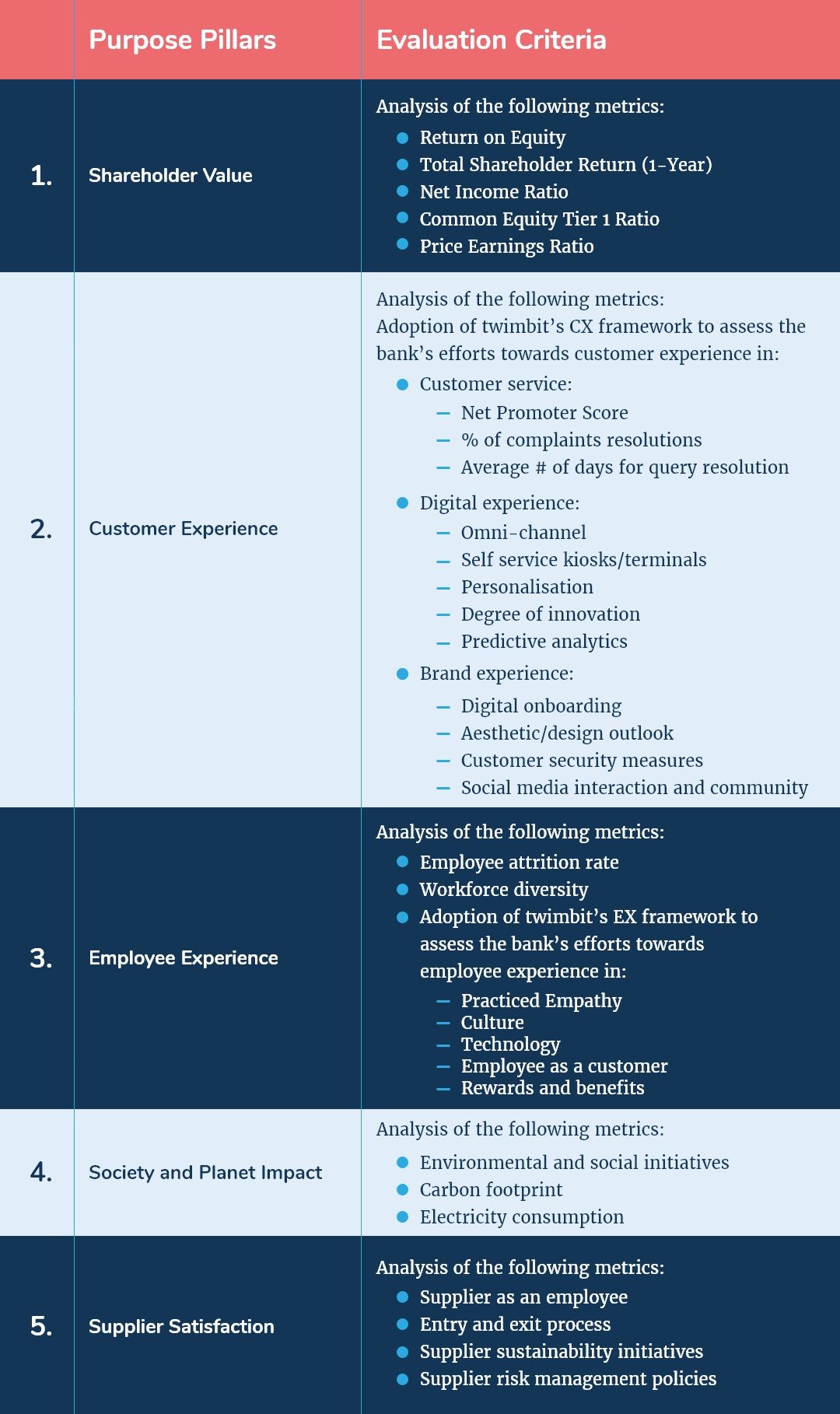

twimbit Purpose Index

Source: Refer to the methodology in Appendix A below

Industrial and Commercial Bank of China (Group financials)- An overview as of 31st December 2020

| Bank Name | Industrial and Commercial Bank of China (ICBC) |

| Headquarters | Beijing |

| Operating revenue | USD 122.5 billion |

| Group net profit | USD 48.36 billion |

| Total Assets | USD 5.105 trillion |

| Employees | 424,000 |

| Countries in operation | 49 |

| Number of branches | 16,623 |

| Fintech investments | USD 3.65 billion |

| Number of customers | 680 million |

| Market capitalisation | USD 292.4 billion |

| Operating Revenue CAGR growth (2016-2020) | 4.5% |

2. Conversion rate to USD as of 31st December 2020 – 0.1531 USD

Shareholder value (31st December 2020)

| Return on Equity (as of 31st December 2020) | 11.95% |

| Total Shareholder Return (1-Year) | 14% |

| Net Income Ratio | 39.7% |

| Common Equity Tier 1 Ratio | 13.18% |

| Price Earnings Ratio (as of 31st December 2020) | 4.2 |

Awards

| 2020 | The Banker: Rank 1st Among the Top 1000 World Banks for the eighth consecutive year Fortune: Rank 1st Among commercial banks in the Global 500 for the eighth consecutive year Forbes: Rank 1st In the Global 2000 for the eighth consecutive year Brand Finance: Rank 1st Among the Top 500 Banking Brands for the fifth consecutive year China Council for Brand Development: Rank 1st In the “Corporate Brand Value List” for the fifth time Global Finance: Best Bank in China, Best Corporate Bank in China, Most Creative Bank in China The Asset: Best Bank in China, Best Bond Advisor in China, Best Insurance Custodian Bank in China Asiamoney: Best Retail Bank for Online Banking 2020, Overall Best Gold Bank, Best Bank for Domestic Debt Capital Markets 2020 The Asian Banker: Best Mega Retail Bank in China, Best API and Open Banking Implementation, Best Asian International Cash Management Bank in the Asia Pacific The Chamber of Hong Kong Listed Companies: The Hong Kong Corporate Governance Excellence Awards China Banking Association: Effectiveness Award: Supporting China’s Winning the “Three Critical Battles”, Practicing the Belt and Road Initiative, Best Inclusive Finance |

ICBC and its strategic focus areas

- Business strategy

ICBC aims to focus on driving a new high-quality development pattern and commits itself to putting customers first. The bank plans to change monetary policies to maintain the quality, pace, size, and price of investment and financing. It will also promote the stabilisation of the size of funds. In addition, the bank wants to improve service quality and optimise its financing structure to ensure funding accuracy.

In 2020, ICBC saw an increase in corporate customers by 545,000 at the end of 2020, a 7% increase in corporate settlement accounts, and a 10.2% increase in global cash management customers. The bank’s domestic branches disbursed an aggregate of USD 63 billion in international trade finance. Despite the pandemic, ICBC saw good growth in its business. Success was mainly due to the following initiatives:

- Multi-dimensional expansion, flexibility in pricing, and innovation in products to increase the number of deposits

- Established an online warehouse receipt financing business with Shanghai Futures Exchange (SCPE) to provide financial support to SMEs. Promotion of commercial paper brokerage business to other enterprises happened through SCPE’s “Discount Connect” platform

- Launched the “emergency material management system” and “ICBC e-Government Service” online donation and management systems to help with work resumption during the pandemic

- Introduced a new professional assessment system for investment consultants to improve its collaborative work mechanism with wealth consultants

- Adjustment of credit strategy to support economic development

- Provision of emergency loans with deferred principal and interest repayment to SMEs

- Launched the Anti-epidemic Loan, Reopen Loan and Employment Loan programs to assist SMEs

- Promoted the electronic reform of local non-tax collection to aid government reforms

- Customisation of selective products on-demand and the extensive development of advisory business

- Customer experience

The bank aims to be the customers’ first choice and upholds its strategy of pursuing development and services that benefit the people. Accordingly, ICBC will continue developing products, improving banking quality, and building its ecosystem based on customer demands. Doing so helps ICBC improve its service process holistically and reduces customer legwork, ultimately improving customer experience and customer satisfaction.

In 2020, ICBC undertook the following initiatives to move forward and achieve the objectives above:

- The bank boosted three types of online products, which include:

- Quick Lending for Operation: This product aided financing scenarios such as settlements, tax, cross-border and medical security financing by speeding up data integration and the application of tax, credit reference, logistics, and power.

- e-Mortgage Quick Loan: A loan that relies on an online assessment of collateral, risks, and business approvals to enhance the efficiency of business and customer experience.

- ICBC e Credit: A crucial part of the digital supply chain, which grants credit to the whole industrial chain, spread over 2000 such chains.

- ICBC created a cloud-based retail business. It launched Personal Mobile Banking Version 6.0 to accelerate the integration of mobile banking and physical outlets. ICBC also made innovations to launch interactive online “cloud outlets” and “cloud studios” for customer managers to provide 24/7 contactless financial services. The bank also initiated the “Cloud Outlet” service on mobile banking and a WeChat mini program using a new service model of “Customer self-service + Remote operator assistance and verification”, making it easier for customers to handle over 40 items of businesses.

- It introduced an extensive service platform for the digitalisation of rural areas. This will provide one-stop services to rural customer groups. The customer groups involve rural collective organisations, village-run enterprises, and villagers in areas such as government affairs, finance, rural affairs, party affairs and finance, etc.

- ICBC provided over 120 services, including new card opening, e-banking registration, and domestic transfer and remittance to rural consumers who could not access services through portable intelligent terminals.

- The bank boosted its global payroll payment service, allowing customers to pay salaries home and abroad. In addition, it vigorously promoted “Corporate Wallet”, which is a digital currency payment tool. The tool enables customers to use corporate digital wallets for scenarios such as “ICBC e BillPay”, “ICBC e-Corporate Payment”, and QR code-based charging.

- The launch of personalised cards such as wedding cards and graduation season cards, and special debit cards.

- ICBC rolled out “ICBC e-Corporate Payment” for core enterprises in the supply chain as well as government affairs. The bank also introduced the O2O payment mode and a small-value quick payment feature for customers’ capital safety and convenience with corporate online settlement services.

- ICBC renovated old and core-potential outlets to provide a strong hardware guarantee for customer service.

- ICBC Cloud Banking became the first bank to launch “Home Agent Customer Service” by Cloud Desktop. It also upgraded the ICBC intelligent robot “Gino (Gong Xiao Zhi)”, which represents ICBC intelligent services

- The bank implemented the GBC interconnection strategy and built more than 1,200 outlets, specialising in government service. This service provides one-stop solutions for social security, provident fund, business administration, and taxation. It helps enhance the service capabilities of outlets.

- The bank propelled to upgrade its service brand “ICBC Sharing Stations” for inclusive service and people’s benefit. It provided intimate and meticulous services to grassroots workers such as sanitation workers and couriers.

- It established nearly one hundred outlets that could provide featured services for the elderly customer groups to enhance the comprehensive service capabilities.

- ICBC launched 18 financial ecosphere cloud products in education, medical care and enterprise services, facilitating intelligent government affairs and digital transformation of enterprises.

- Employee experience

ICBC effectively guarantees the input of HR in key strategic areas and business lines by following improvement ideas for HR efficiency, such as serving strategy, scientific configuration, reducing consumption and enhancing efficiency. These ideas will strengthen the formation of professional talent teams. The move will also invigorate staff vitality with an entrepreneurial spirit and start a new chapter – serving the new development pattern and promoting high-quality development. To achieve the objectives mentioned above, ICBC deployed the following initiatives in 2020:

- Conducted training on job knowledge and skills, as well as new products, business, and process promotion to enhance the employee performance growth

- Promoted training options, such as live-streaming classrooms, e-learning, and online training camps during the pandemic

- Organised “ICBC Innovation Contest”, a cultural program themed “red finance”, “One ICBC One Family”, and “ICBC Culture Stories” to bring employees together

- Conducted online employee satisfaction surveys in the HR management system

- Boosted the “ICBC Stars” brand to leverage the online recruitment process, ensuring quality and efficiency of hires during the COVID-19 pandemic

- Opened a “New Stars School” under ICBC University as a premium platform for bank-university cooperation and training

- Established an emergency reserve of medical supplies, including PPE kits and also organised events focusing on employee care for better employee experience during the pandemic

- Provided online lectures and psychological counselling to ease employee stress

- Organised visits to employees on special occasions, such as birthdays, childbirths, and provided hospitalisation for serious diseases and retirement

- Carried out various events for employees, such as health preservation events, matchmaking and dating services for single employees, as well as season-based events

- Promoted gender equality mechanisms in the workplace and strictly implemented the laws and regulations on protecting women workers’ rights and interests.

- Society and planet impact

ICBC aims at alleviating its social responsibilities towards the environment, society, corporate governance, poverty alleviation, and green financing. The bank invested up to USD 282.57 billion in green loans for green industries, inclusive of energy conservation and environmental protection, clean production, and green services.

Furthermore, the bank took the following initiatives in 2020:

- Embraced green finance strengthening as a long-term strategy to transition to green and low-carbon production and lifestyles in response to climate change

- Employed a complete investment and financing instrument kit with six key focuses (loan, bond, stock, agency, lease, and consultant) to improve investment and financial assistance for green industries continually

- Implemented paperless meetings and training sessions to push energy-saving technological transformation forward, also accelerated the smart park project constructions

- ICBC Data Center optimised air- and water-cooling loads, chemically cleaned condensers of water-cooled centrifuge sets, and implemented energy-saving measures, including energy-saving technologies for free cooling, smart operation, energy-saving modes for linked computer room air conditioners, and the strict management of hot/cold aisle separation in computer rooms

- Increased vehicle use efficiency, established a diverse business vehicle pattern, and directed employees to use safe, healthy, and environmentally beneficial modes of transportation

- Participated in voluntary tree planting activities to increase employee awareness in environmental protection

- Security strategy

ICBC aims to maintain a balance between development and security for better risk management. It plans to adopt forward strategy planning by seeing the bigger picture and managing risks in time. To achieve that, the bank integrated risk investigation and management, coordinated the advancement of risk prevention and improved the top-level risk management design.

ICBC undertook the following initiatives to provide an overall secured experience:

- Developed a new voiceprint-recognition risk control measure to provide identification and fraud risk judgment data quickly and invisibly, thereby vastly improving the level of intelligent risk control and customer service

- Upgraded the “ICBC Brains” intelligent anti-money laundering system for peers, covering the entire anti-money laundering process, including knowing your customer(KYC), customer risk classification, and suspicious transaction monitoring. Enhanced “ICBC e-Security” and developed nine product systems, including a blacklist service, as well as risk, intelligence, association, and dynamic monitoring, to effectively prevent external fraud risks

- Pushed the production and operation capacity of technical support, monitoring and analysis, emergency response, performance planning and management and control to a whole new level

- Upgraded the monitoring system for business operations and increased the monitoring computing efficiency from a minute to 10-second levels

- Performed the annual switch of information systems locally and disaster recovery drills non-locally for business continuity

- Ran a campaign to enhance the security-defensive capability of the security team, helping them reach the top tier and ace regulatory security competitions

- Strengthened its security capability output to provide security-related assistance in developing industrial level situation awareness and research network

- Established an information security operation center (SOC) to accelerate the transition of the security protection strategy into a practical one. Also formed a compound financial technology talent team comprised of experienced and qualified individuals

Digital strategy

The bank aims to be technology-driven for a stronger push towards fulfilling the new development pattern and promoting high-quality development. ICBC also plans to accelerate its digital transformation, fully implement the technological innovation plan and the e-ICBC strategic upgrading program, and grow into a technology bank. As part of its initiatives in 2020, the bank did the following:

- Made strides by building three major platforms, i.e., the global cash management platform, the small and micro-financial service platform, and the “ICBC Pooling” platform:

- The global cash management platform: It helps enterprises improve the efficiency of fund management by providing them with treasury management cloud services.

- The small and micro-financial service platform: ICBC provides SMEs with 24/7 all-inclusive financial services. The services include payment convenience, foreign exchange settlement account opening through mobile terminal, investment and financing.

- The “ICBC Pooling” platform: It introduced unique solutions to enhance the service capability of clients for the supply chain. It includes services like “Supply Chain Cloud,” “Government Procurement Cloud,” “Medicine Purchase Cloud,” and “Construction Cloud”.

- Launched an intelligent customer service platform and introduced ICBC Custody Mobile Banking to provide a full spectrum of custody services1 to customers.

- Upgraded Personal Mobile Banking by developing online county-specific services using dialects in different regions, making it accessible to all.

- Introduced ICBC UnionPay Unlimited Digital Platinum Card, an online-only digital card for its premium customers. This card takes seconds to apply and activate and offers a comprehensive range of high-end services geared toward an ICBC cardholder’s “Platinum” lifestyle.

- Established a financial ecosystem on ICBC e-Life, consisting of WeChat Applets, WeChat official accounts, and online campaign pages by building a platform for credit card spending. It has features like password resetting, credit limit increase, and online instalments. The platform also has three scenarios, namely bonus points, shopping, and instalments with sub-brands and promotion campaign seasons. These include e-Food Coupons, e-Top-selling Products, and e-Coffee; “Top-selling Season, Travel Season and Digital Season”. It also supports the live broadcast of marketing campaigns

- Created ‘ICBC e-BillPay’, a smart bill payment platform for convenient bill payments, donations, and community involvement

- Connected with the cross-border financial blockchain service platform of the State Administration of Foreign Exchange. This brought about the launch of a “single window” financial service based on the intensive advantage in customs import and export data

- Established the “Cross-border e-Business Connect”, a comprehensive service platform with domestic and foreign payment institutions and cross-border e-business platforms to develop new business patterns.

- Cooperated with 13 provincial agricultural and rural departments in over 28 cities, leading to the development and launch of a management platform for the rural development fund

- Promoted the “ICBC e-Government Service” to provide “government service + financial service” to national exhibitions like the online Canton Fair and China International Import Expo

- Came up with four new services, namely:

- Intelligent travel: Launched three core products, namely, ETC, unconscious payment, and a QR code payment service for public transport. It also rolled out the “e-Ride” mini-program, supporting all kinds of scanning codes for rides, covering 200 cities across China

- Healthcare and social security: Pioneered an innovative service program called the “Commercial Medical Cloud”, integrating the internet, medical devices and finance. ICBC also issued electronic vouchers for medical insurance and launched the medical insurance clearing mobile payment platform in 10 provinces and regions

- Intelligent campus: “Campus Affairs Management Cloud” provides parents, students and schools with integrated services, including payment, management, and epidemic prevention and control

- Intelligent justice: Served the reform of the national judicial system and promoted the judicial auction platform of ICBC Mall in a total of 258 courts

- ICBC Mobile:

- ICBC pioneered Mobile Banking 6.0, creating “Customer Manager Cloud Studio” and “Cloud Outlet” and introducing features such as vocal print login, AR recognition of foreign currency, and AI intelligent recommendation.

- It catered to a lower-tiered market consisting of farmers and business merchants through the launch of exclusive financial services – the “Beautiful Home”.

- There is an optimisation of the “Happy Life”, a version for elderly persons to provide seamless mobile financial services.

- ICBC also introduced “contactless” functions, like the conversion of LPR interest rates and credit card repayments from other banks, the modification of card passwords, and online ordering and offline mailing services through mobile banking code scanning instead of bank cards during the pandemic.

- ICBC Mall:

- The bank upgraded ICBC Mall by introducing an interactive shopping experience with new features, including face registration and APP aggregate payment. It also focused on key areas, namely procurement, travel, and cross-border e-commerce.

- ICBC Link:

- ICBC Upgraded to the 5.0 version of ICBC Link for refined user experience, made possible by optimising the functional layout, process and experience of the main interface.

- There was also the launch of the WeChat mini program for customer managers to integrate communication and transactions.

- The bank also pioneered the “gold red packet”, the first gold accumulation model integrating financial service and social intercourse in the banking sector.

- ICBC e-Life:

- The bank established an open ecosystem consisting of campaign pages, APP, WeChat applets, WeChat official account, and a live account to transform global operations.

- This includes scenarios such as shopping, catering, accommodation, travel, entertainment, education, health, urban services, and poverty alleviation and inclusiveness.

- E-Life consists of six special columns – shopping, credit bonus points, instalment, in-app purchase, poverty alleviation, and recreation.

- Mobile payment:

- This initiative cultivated three-party payments and consumption scenarios and issued coupons sponsored by Beijing and Wuhan municipal governments.

- The mobile payment carried out more than 100 activities on 30 themes, such as “Cloud Vegetable Buying”, “Traveling with Peace of Mind”, and “ICBC Food Season” during the pandemic.

- ICBC e-Wallet:

- The e-wallet application covered areas such as government affairs, people’s livelihood services, transportation, membership management, house purchase services, consumer finance, and other scenarios.

- It introduced an online payroll service model that adopted a fully online account opening and payroll payment process.

IT strategy

With massive progress in ecosystem development, the bank invested heavily in 5G+ABCDI (AI, BLOCK-CHAIN, Cloud Computing, Big Data and IoT). ICBC will continue to build its digital capabilities through further construction of 5G, data centres, new digital infrastructure, reinforcing production, operation safety and cloud computing. The bank will continue to accelerate management system and mechanism reforms while boosting digital business forms, digital transformation and bank upgrades developments.

As part of its 2020 initiatives, ICBC worked towards enhancing these platforms to build its digital businesses:

- ICBC Cloud Platform: This platform provides cloud services such as Education Cloud, Party Building Cloud, Property Management Cloud and HR Cloud. It has 33000 tenants.

- API Open Platform: The platform offers customisable and component-based API services, allowing users to access over 120 products across 18 categories and over 1,900 application interfaces, gradually increasing open capacity and partner numbers. It has 10000 partners.

- Ju Fu Tong: More than ten industries, including government service, transportation, medical care, tourism, and agriculture, have been promoted to use the “Ju Fu Tong”, a scenarios-embedded comprehensive financial service. It connects 110 platforms.

- ICBC Enterprise Mobile Banking: Based on the needs of corporate customers, the bank developed Enterprise Mobile Banking 3.0, which includes new technology applications such as voiceprint authentication, digital-human customer service, and OCR recognition. Functions such as Quick Lending for Operations, e-Mortgage Quick Loan, foreign exchange settlement, credit report enquiry, and payroll payment are also available. Account opening reservations, online application reservations, and settlement account information changes are some new online and offline integrated services. It has 3.06 million active users.

- The bank also expanded cooperation for mutual benefits and developed the blockchain platform for resettlement fund management and a smart social security public service platform.

The bank also deepened the integration and innovation of technology and business and advanced the construction of new infrastructure through:

- Established a series of new enterprise-level technology platforms based on 5G+ABCDI to set up an application mechanism that covers forward-looking trend tracking, study and prediction, key technology research breakthrough, and the implementation of business scenario innovation

- Introduction of a new cloud computing platform, while the scale of IaaS infrastructure cloud and PaaS platform service cloud remained in a leading position

- Established an open platform core banking system, consisting of the core business infrastructure support framework, account system, and products and services

- Built a platform of big data and artificial intelligence (AI) with an in-depth perception and open application

- Created an automatically controllable AI technical system to perform functions like reading, listening, thinking, speaking and acting. Also constructed a one-stop AI modelling workstation to apply AI technologies, including Robot Process Automation (RPA), machine learning, optical character recognition (OCR), and knowledge map through facial, voiceprint, iris recognition and other biometric features recognition capabilities

- Developed “ICBC Blockchain+” to apply blockchain technology in multiple fields, including charitable funds, medical services, engineering construction and bank confirmations

- Built an audio and video platform to assist in developing cloud outlets, cloud counters, and other contactless customer service modes using an IoT technology system that integrates “end, side, and cloud.”

- Constructed 5G Messaging as a Platform (MaaP) and completed piloting in MaaP business with China Mobile

ICT contracts

- Collaboration with Huawei for Digital Multimedia Banking Solution, the Safe Financial Cloud Solution, and the CloudFabric Cloud Data Center Network Solution

- Partnership with Gemalto for Dual interface payment cards

- Use of Facephi technology for facial recognition as an authentication system

5 Growth and innovation opportunities

- #1 Cost to serve

The Bank’s continually refined its cost-cutting strategy as operating expenses were at USD 31 billion, down by USD 182 million or 0.6 per cent from the previous year. It set aside approximately USD 31 billion in impairment losses on assets in 2020, an increase of USD 3,630 million or 13.2 per cent over the previous year. The bank’s Cost to Income Ratio (CIR) went from 25.79 per cent in 2019 to 24.76 per cent in 2020. Net interest margin, on the other hand, went down by 0.15% from the last year with a figure of 2.15 % compared to 2.30% in 2019.

Despite the bank’s efforts to become digitally efficient internally and externally, it incurs a personnel cost of USD 16.5 billion. The cost accounts for 16% of the bank’s operating revenue and 39% of the overall operating expenses. While the bank is keeping its cost-efficiency ratios low with effective cost-cutting strategies, branch transformation, and digital operability, it can concentrate on the following to further offset the decline in interest margins and revenues:

- Reduce the impact of substantial impairment costs by driving focus towards non-interest income and complementary revenue streams

- Create RPA-enabled audit trails for red-flagging any high-cost inflexions by implementing transaction-level transparency

- Use predictive behavioural models to revise interest-rate risk models and hedging strategies continuously

- Reduce call centre use for customer query management and sales and instead use AI-driven virtual assistants and chatbots for iterative functions

- Replace man-hours with cognitive process automation for routine and daily back-end tasks

- #2 Transformation of the branch and its branch networks

By the end of 2020, the bank’s physical network consisted of 15,800 outlets, 25,167 self-service banks, 79,672 intelligent devices, and 73,059 ATMs, with a trading volume of USD 904.5 billion. The number of SME business centres increased to 324. Despite the bank’s effort to introduce cloud centres and studio on its mobile banking app to provide 24/7 financial assistance, it still operates a vast physical branch and branch network. The overall expense contribution to run and maintain the physical infrastructure accounts for USD 4.3 billion, about 3.5 % of the bank’s revenue and 13.5% of overall expenses.

The bank should focus on reducing its physical infrastructure by:

- Expanding its cloud outlet AR capability and create augmented branches that imitate real physical branch experiences

- Increasing self-service banks that enable anytime banking and equip them with full-branch capabilities

- Downsizing the ATM network to increase the usage of e-wallet for low to high volume transactions

- #3 Customer experience

A third-party survey shows that the bank’s customer satisfaction reached 86.4%. ICBC has made massive headway in delivering a seamless customer experience by investing in technologies such as 5G+ABCDI. The bank established innovative Mobile banking 6.0 and created ‘customer manager cloud studio’ and ‘cloud outlet’ with features like vocal print login, AR recognition of foreign currency, and AI intelligent recommendation. However, it can further leverage its capabilities through AI and machine learning and can work in these areas to optimise the customer experience journey:

- Personalised insights: Under its existing digital framework, the bank has heavily focused on including features that make transactional banking simple for customers. The bank should invest in understanding the customer’s behaviour patterns, life journey needs, and spending through Al and ML tools. An expanded understanding could aid in creating unique persona-based product packages:

- A customised Product Stack/Portfolio to provide each consumer with a personalised experience by addressing all key touchpoints:

- Personalised offer – a model based on the next best recommendation

- Customised goal – transparency, along with clearly stated goals based on previous interactions with customers

- Individualised tracking – ease of engagement

- Enhance its chatbots and in-app virtual assistant (Gino) to deliver proactive notifications, budgetary recommendations, and lending and investment choices to customers

- Attempting to hyper-personalise its products to fulfil unstated and hidden customer demands

- Gamifying numerous consumer touchpoints, such as awarding badges for increased product usage, providing loyalty program customers with discount coupons, creating a leader board between friends and co-workers based on product purchases, and showcasing trending products.

- A customised Product Stack/Portfolio to provide each consumer with a personalised experience by addressing all key touchpoints:

- #4 Employee experience and productivity

ICBC has made significant investments in employee development and offers a flexible work atmosphere. However, the bank should consider the following services for its employees:

- Clearly define the expectations for all senior leaders to build a culture of clear accountabilities in their respective divisions

- Design personalised employee upskilling programs based on the employee level and adopt effective leadership development coaching to prepare them for future roles

- Create a platform or forum where employees can reach the bank leaders easily to have face-to-face discussions with leaders and influential external speakers. This will help employees share their aspirations and extend their horizons outside the workplace

- Incorporate rewards and benefits that go beyond insurance, stock options, house rentals, and leases. Ideas include:

- Giving employees the option to work on cross-department projects for lateral career advancements

- Periodical career breaks and approved leaves for social cause contributions, such as volunteering in relief camps for teaching, food and medical support work, as well as cleaning drives

- Provide hassle-free student loans to new hires for controlling attrition rates, hence increasing employee loyalty

- #5 Society and planet contribution

The bank made arrangements for advancing ecological civilisation and responding to climate change. It recognised the critical role of green finance in the transition to green and low-carbon production and lifestyles, and saw green finance strengthening as a key long-term strategy.

ICBC Data Center cut overall energy consumption by 2,125,200 KWH, an equivalent to reducing carbon dioxide emissions by 2,118,824 Kgs – just slightly over the weight of 14 blue whales.

ICBC should seek to reduce its energy usage and carbon footprint with these measures:

- Use energy-efficient devices by making one-time investments and saving costs in the long term

- Reduce its carbon footprint by switching to pulper cards, eco ink and carbon control press machines. It should also introduce digital-only cards for all its customer segments.

- Build on-site solar facilities and signing renewable agreements to add new wind and solar electricity to the grid.

The bank can also launch support projects in impoverished areas, which help to preserve biodiversity and further local economic mobility.

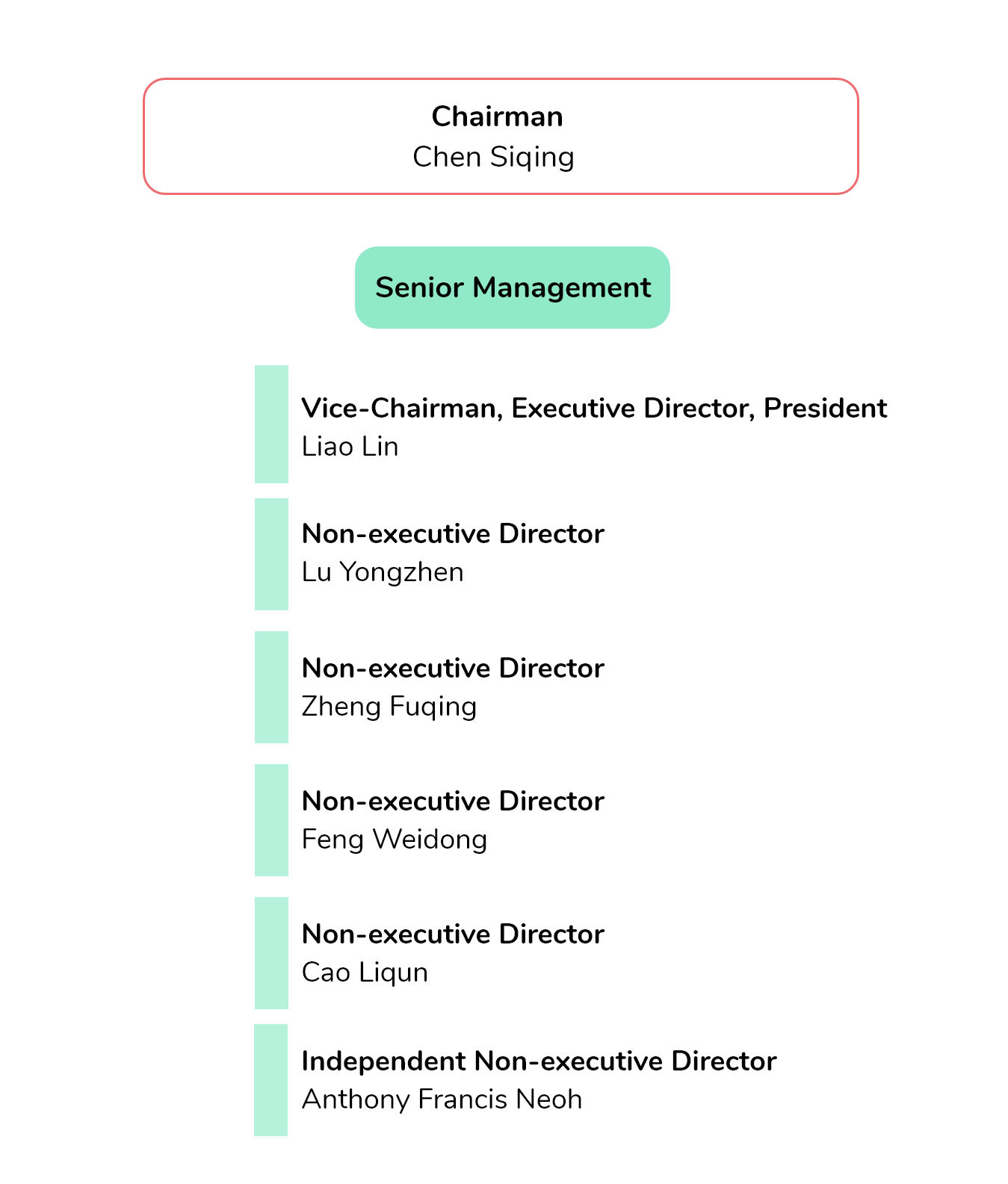

Organisation structure: Leadership

Executive profile

Chen Siqing

Chairman and Executive Director

Chen Siqing served as Chairman and Executive Director of ICIB since May 2019. He joined the Bank of China in 1990. Siqing graduated from Hubei Institute of Finance and Economics. He also has an MBA from Murdoch University, Australia. In addition, Siqing is a Certified Public Accountant as well as a seasoned economist.

Quote

- Risk Management, Annual Report 2020

We earnestly balanced between development and security to ensure better performance in risk control of new loans and risk disposal of existing ones

Liao Lin

Vice-Chairman, Executive Director, President

Liao Lin held the position of Vice Chairman, Executive Director and President of the Bank since March 2021. In addition, he was the Executive Director of the Bank since July 2020, and its Senior Executive Vice President and Senior Executive Vice President and concurrently the Chief Risk Officer from November 2019. Liao Lin graduated from Guangxi Agricultural University. He also obtained a Doctorate in management science from Southwest Jiaotong University and is a senior economist.

Lu Yongzhen

Non-executive Director

Lu Yongzhen has served as Non-executive Director of the Bank since August 2019. He joined Huijin in 2019. He obtained Bachelor and Master degrees in History from Peking University and a Doctorate in Economics, which he completed with the Southwestern University of Finance and Economics. He is also a researcher.

Zheng Fuqing

Non-executive Director

Zheng Fuqing has been working as the Non-executive Director of the Bank since February 2015. He has graduated from the Party School of the Central Committee of CPC, majoring in law theory. He is also an economist.

Feng Weidong

Non-executive Director

Feng Weidong has served as Non-executive Director of the Bank since January 2020. He has obtained a Bachelor’s degree in Economics from Dongbei University of Finance & Economics and a Doctorate from Beijing Jiaotong University. He is also a senior accountant, researcher, non-practising certified public accountant. Finally, Feng is a recipient of the Special Government Allowance accorded by the State Council of China.

Cao Liqun

Non-executive Director

Cao Liqun has served as Non-executive Director of the Bank since January 2020. She joined Huijin in 2020. Her qualifications include a Bachelor’s degree in Law from China University of Political Science and Law, a Master’s degree in Finance from Renmin University of China, and finally, a Master’s degree in Public Administration from Peking University. Cao is also an economist.

Anthony Francis Neoh

Independent Non-executive Director

Anthony Francis Neoh has served as Independent Non-executive Director of the Bank since April 2015. He has a Law degree which is from the University of London. He also has an Honorary Doctorate of Law, which he obtained from the Chinese University of Hong Kong. Lastly, Neoh holds an Honorary Doctorate of Social Sciences from Lingnan University.

Appendix A

- twimbit Purpose Index

We evaluate Asia Pacific’s top banks to understand whether their strategic objectives, market positioning, and operational efficiency align with continued sustainability and profitability. In evaluating the respective bank’s focus areas and performance, we base our analysis on five purpose pillars and score each bank on them.

Endnotes

Industrial & Commercial Bank of China Ltd, (2020, December 31). Annual Report 2020.

http://v.icbc.com.cn/userfiles/Resources/ICBCLTD/download/2021/2020AnnualReport.pdf

Industrial & Commercial Bank of China Ltd, (2020, December 31). Sustainability Report 2020.

http://v.icbc.com.cn/userfiles/Resources/ICBCLTD/download/2021/2020shzrEN202103.pdf

Wall Street Journal. Industrial & Commercial Bank of China Ltd financials. Retrieved June 30, 2021, from

https://www.wsj.com/market-data/quotes/HK/1398/financials/annual/income-statement

1 Custody services

The asset custody services of the Group refer to the business that the Group as trustee approved by regulatory authorities, signs custody agreement with clients and takes the responsibility of trustee in accordance with relevant laws and regulations. The assets under custody are recorded as off-balance sheet items as the Group merely fulfils the responsibility as trustee and charges fees in accordance with these agreements without retaining any risks or rewards of the assets under custody.

Page no. 175, Fiduciary Services

http://v.icbc.com.cn/userfiles/Resources/ICBCLTD/download/2021/2020AnnualReport.pdf