Learn, ideate and collaborate on the biggest innovation opportunities

India, the new hub of neobanks

@ Varnika Goel

Your browser doesn’t support HTML5 audio

By providing people with the right incentive structure and behavioural nudges, we can help get customers ready to adopt digital financial services. -Nilesh Agarwal, co-founder CEO, Yelo

Regulatory initiatives

Introduction

Reserve Bank of India’s guidelines does not allow a 100% digitalisation of banks. In India, neobanks are not granted their banking licences. The neobanks provide financial services by partnering with licensed banks. For example, Digibank, a neobank launched by DBS bank in 2016 received approval from RBI to operate as a wholly-owned subsidiary of DBS. Digibank is DBS bank’s digital spin-off and operates as an independent neobank.

Payments bank

A type of bank gaining recognition in India is the Payments bank. Payments banks offer their services completely online. They are recognised as payments banks under Section 22 of the Banking Regulation Act, 1949. While these banks can accept deposits i.e., current deposits, and saving banks deposits (up to INR 1,00,000), issue ATM or debit cards, and offer retail banking and intra-banking transactions services, they cannot issue loans or credit cards to their users.

However, in 2019, Paytm payments bank in collaboration with CITI Bank launched India’s first unlimited cashback credit card which is offered to limited customers based on their digital behaviour. Moreover, to access the services provided by payments banks, the customer must have an existing bank account with a traditional bank. Thus, we classify payments bank under the digital platform category of neobanks. To further read about the type of neobanks, read the article Neo banking 2.0: The new face of banking in the Asia Pacific

On tap licensing framework

Moreover, in December 2019, RBI issued guidelines for on-tap licensing of small finance banks (SFBs) in the private sector, which allow the creation of banks specifically targeting the unserved and underserved small business units, small and marginal farmers, and micro and small industries. These guidelines enable payments banks, such as Fino payments bank, Airtel payments bank, and Paytm payments bank, microfinance banks and non-banking financial institutions (NBFCs) to apply for the licence. The entities must have a track record of conducting business for 5 years in addition to a minimum paid-up capital of INR 200 crore to convert into small finance banks.

Snapshot of India’s neobanks

Table 1: Profile of India’s neobanks

Name

Founding year

CEO

Annual revenue

FinoPayments Bank

2006

Rishi Gupta

US$ 93.85 Million (Net revenue FY20)

SBI YONO*

2017

Rajnish Kumar

Undisclosed

Kotak 811*

2017

Uday Kotak

Undisclosed

Digibank*

2016

Surojit Shome

Undisclosed

NiYo

2015

Vinay Bagri

Undisclosed

Open

2017

Anish Achuthan

Undisclosed

RazorPay X

2014

Harshil Mathur

US$ 18.9 Million (FY19)

Yelo

2014

Nilesh Agarwal

US$ 1.18 Million (FY18)

InstantPay

2013

Shailendra Agarwal

US$ 14.6 Million (FY18)

Hylo

2019

Vishal Gupta

Undisclosed

Payzello

2017

Pruthiraj Rath

Undisclosed

IPPB**

2018

J Venkatramu

US$ 6.57 Million*** (FY19)

Ezo Bank

2019

Gauravkumar Kate

Undisclosed

Zeta

2015

Bhavin Turakhia

Undisclosed

Jupiter

2019

Jitendra Gupta

Undisclosed

Finin

2019

Suman Gandham

Undisclosed

Namaste Credit

2014

Gaurav Anand

Undisclosed

Walrus

2019

Bhagaban Behara

Undisclosed

Slice

2016

Rajan Bajaj

Undisclosed

Fi

2019

Sujith Narayanan

Undisclosed

Jio Payments Bank****

2016

H Srikrishnan

US$ 2.8 Million (FY18)

NSDL Payments Bank

2014

G.V. Nageswara Rao

US$ 29.6 Million (FY19)

Paytm Payments Bank

2010

Satish Kumar Gupta

US$ 204.5 Million (FY19)

Airtel Payments Bank

2017

Anubrata Biswas

US$ 64.6 Million (FY20)

Revolut

2021

Paroma Chatterjee

Undisclosed

Source: Twimbit analysis *These neobanks are built on their own parent banks’ existing funds. **Setup under the Indian Post, Department of Post, Ministry of Communication with 100% equity owned by Government of India ***IPPB revenue include their total business stemming from both the digital spin-off and traditional offline banking activities. **** Jio Payments Bank is a joint venture between SBI (30%) and Reliance industries (70%). Note: Zyro, and Atlantis are newly formed neobanks in 2020 with limited to no available information.

Table 2: Learning list of India’s neobanks funding capital

Name

Fino payments bank

Total funds raised

US$ 52 Million

Equity round 1

US$ 37.6 Million (July 2016)

Equity round 2

US$ 20.3 Million (Jan 2017)

Name

NiYo

Total funds raised

US$ 55.2 Million

Seed capital

US$ 1 Million (July 2016)

Series A

US$ 13.2 Million (Jan 2018)

Series B

US$ 35 Million (July 2019)

Corporate round

US$ 6 Million (August 2020)

Name

Open

Total funds raised

US$ 37.4 Million

Seed capital

US$ 2.4 Million (May 2018)

Series A

US$ 5 Million (Jun 2018)

Series B

US$ 30 Million (Feb 2019)

Name

RazorPay X

Total funds raised

US$ 124.7 Million

Seed capital

US$ 2.6 Million (March 2015)

Series A

US$ 9 Million (Oct 2015)

Venture capital 1

US$ 100,000 (July 2016)

Series B

US$ 20 Million (Jan 2019)

Series C

US$ 75 Million (Jun 2019)

Venture capital 2

US$ 28 Million (Oct 2019)

Name

InstantPay

Total funds raised – Seed capital

US$ 4.6 Million (Dec 2016)

Name

Zeta

Total funds raised – Corporate round

US$ 60 Million (July 2019)

Name

Jupiter

Total funds raised

US$ 26 Million

Seed capital

US$ 24 Million (Nov 2019)

Venture capital

US$ 2 Million (April 2020)

Name

Namaste Credit

Total funds raised – Series A

US$ 3.8 Million (April 2018)

Name

Slice

Total funds raised

US$ 28.6 Million

Seed capital

US$ 500,000 (Feb 2016)

Series A

US$ 2 Million (Oct 2017)

Series A

US$ 14.9 Million (September 2018)

Debt financing

US$ 3.4 Million (Sep 2019)

Debt financing

US$ 1.4 Million (Oct 2019)

Series B

US$ 6.2 Million (June 2020)

Name

Fi

Seed capital

US$ 13.2 Million (Jan 2020)

Series B

US$ 30 Million (Feb 2021)

Name

Paytm Payments Bank

Total funds raised – Two venture capital rounds

US$ 28.2 Million

Name

Airtel Payments Bank

Total funds raised – Initial investment

US$ 484.3 Million

In-depth neobank analysis on the 5-building block framework

Customer centricity:

Every established neobank in India exemplifies a superior experience for their customer and fulfils at least one parameter under customer-centricity.

Figure 1: India’s neobanks represent all customer centricity parameters

Note: Revolut is a newly launched neobank in India and it’s public interface is not live yet. As a result, we are not commenting on their customer-centricity.

Customer reach:

Out of the 27 neobanks in India:

InstantPay serves over 50 million across all 3 customer segments- SME, rural, and Millennials.

Revolut serves the 500,000+ businesses (SME) and 15 million+ people (millennial) globally.

67% of the neobanks exclusively serve the millennial segment.

Figure 2: Customer segment and total number of customers

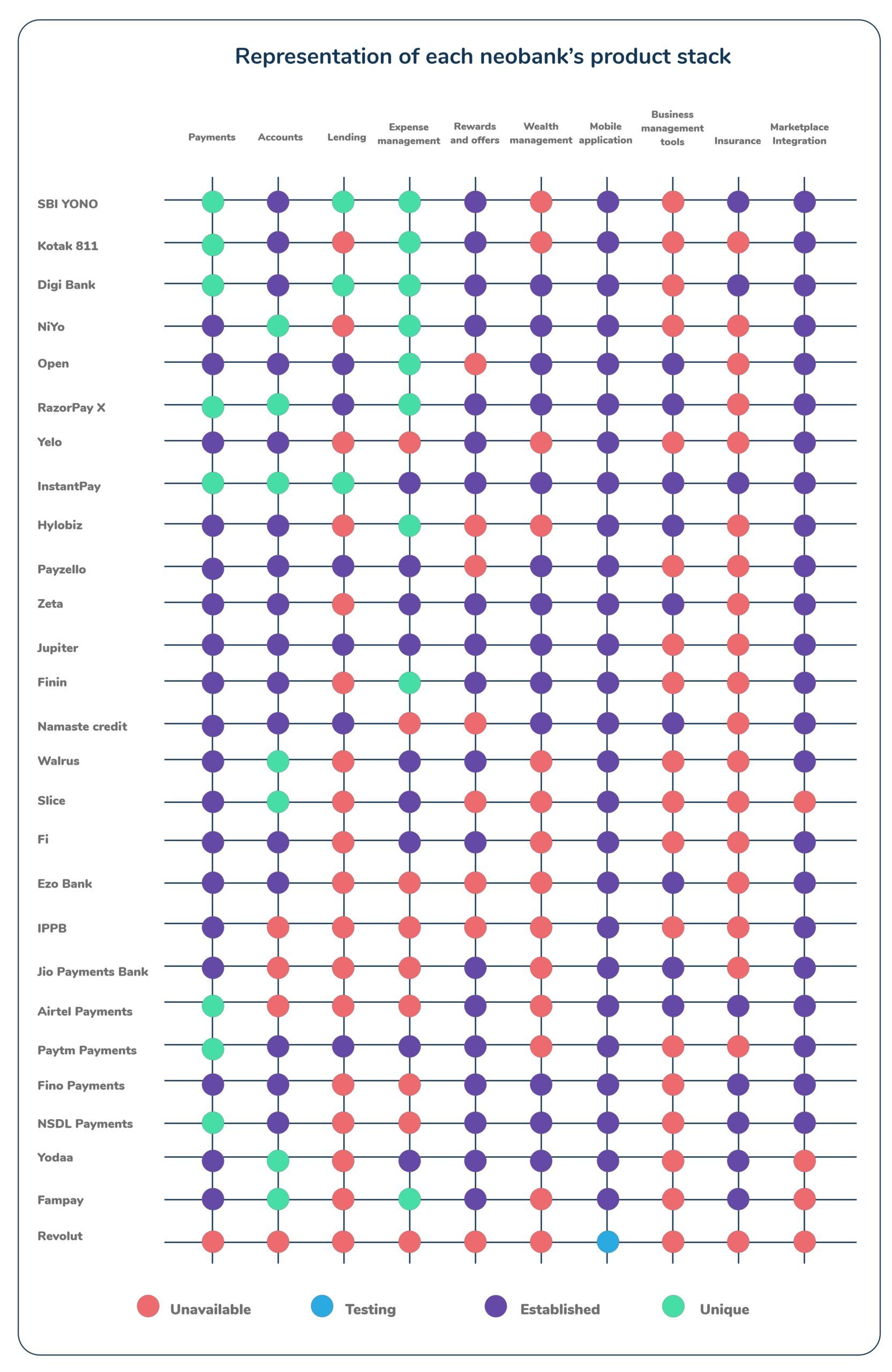

Product stack:

8 of the 27 neobanks in India offer their customers with unique payments options such as virtual debit cards, split payments, and credit cards.

Digital platforms Razorpay X, InstantPay, NiYo, Walrus, and Slice have unique accounts such as multi-currency, and teen and kids’ account.

Digibank, SBI YONO and InstantPay provide business/personal overdraft facilities in addition to offering basic loan services.

Methodology: Each neobank’s product stack is a representation of 4 key parameters across 11 product types

Unavailable: Does not have a product type in their stack

Testing: The product is currently in the pilot-testing phase, not live to all customers

Established: The product is a part of their stack and fully available for customers

Unique: A unique offering within a product type which is exclusively provided by the neobank

Figure 3: Representation of each neobank’s product stack

Partnership ecosystem:

Since RBI does not allow the 100% digitalisation of banks, the neo banks in India collaborate with traditional banking institutions to offer financial services. The major banking partners are State Bank of India (SBI), ICICI Bank, Kotak Mahindra Bank, IDFC First Bank, Yes Bank, HDFC Bank, RBL Bank, Federal Bank and Lakshmi Vilas Bank.

The leading network/payment provider in the Indian neo banking arena are Rupay, Mastercard and Visa.

Top insurance partners for Indian neobanks include Bharati AXA, Tata AIA, Aviva, Birla Sun Life, Punjab National Bank, Kotak Life Insurance, ICICI Prudential Life Insurance, and Bajaj Allianz.

Figure 4: Partnership ecosystem of India’s neobanks

Open Banking:

The open banking ecosystem in India has grown tremendously with the advent of Unified Payments Interface (UPI), thus enabling consumers to make real-time payments with ease. Several banks have taken the initiative to build their own Open Banking ecosystems such as API gateways, API stack players, account aggregators and so on.

Table 3: API Developers for India’s neobanks

Name

Sandbox/Developer

Fino Payments Bank

PayRupees AePS

SBI YONO*

SBI API Developer

Kotak 811*

Kotak developer connect

Digibank*

DBS Developers

Open

Open developers

RazorPay X

Razorpay API

InstantPay

InstantPay API

Zeta

Zeta Fusion

Jio Payments Bank

JioMoney Developers

Paytm Payments Bank

Paytm Developer

Airtel Payments Bank

Airtel Smart Api

Revolut

Revolut Developer Portal

Note: The list is not exhaustive and is based on the publicly available data

Indian neobanks’ outlook

A high mobile and internet penetration rate in addition to the largely unbanked population proves that India is a market ripe for neo banking.

The new recommendations made by the Indian inter-ministerial panel on fintech to the Department of Financial Services and RBI to test new fintech innovations in a restricted ecosystem and to examine the benefits of granting full banking licences to banks while allowing them to operate completely online will boost the financial inclusion thrust in India.

The sudden surge of neobanks in the Indian banking sector indicates that the market is lucrative for technology-based platforms, thus enabling superior user experience with the secondary infrastructure of a traditional bank to mitigate risk.

Two scenarios will exist as the future of neobanks

Firstly, neobanks will become the primary interface and a daily transactional bank for customers. Whereas traditional banks form the secondary interface and a long-term saving bank.

Secondly, India will witness a consolidation of multiple small neobanks in a single super application with a targeted approach to each customer segment (Gen Z, millennials, businesses, rural, and agriculture).

Annexure:

Table 4: List of Indian neobanks’ investors

Name

Investors

Fino Payments Bank

BPCL, ICICI Bank

NiYo

Horizons Ventures, Tencent Holdings, JS Capital, Social Capital, Prime Venture Partners

Open

Speedinvest, Tiger Global Management, 3one4 Capital, Tanglin Venture Partners, BetterCapital AngelList syndicate, Unicorn India Ventures, BEENEXT, AngelList, ISME ACE, Recruit, Amrish Rau and Jitendra Gupta

RazorPay X

Matrix partners, Tiger Global management, GMO Venture partners, Ribbit Capital, Sequoia Capital India, Mastercard and 33 angel investors

Yelo

Omdiyar network, Matrix partners, Flourish ventures, Better capital

Bedrock capital, Hummingbird venture, Matrix partners, 3one4 capital, Greyhound capital, Global founders capital, Sequoia capital India

Finin

PointOne Capital, Astir venture, Unicorn India Ventures

Namaste Credit

Nexus Venture Partners

Walrus

Raven Sastry, Brijesh Thakkar, Raghunandan G, Better Capital

Slice

Better Capital, Gunosy, Das capital, Pegasus Wings Group Kunal Shah

Fi

Sequoia capital India, Ribbit capital, Hillhouse Capital Group

NSDL Payments Bank

India Alternatives Private Equity Fund

Paytm Payments Bank

Vijay Shekhar Sharma – Lead investor

Airtel Payments Bank

Bharti Airtel and Bharti Enterprises

Note: The list is not exhaustive and is based on the publicly available data

End notes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

Akshita Maruthavanan, Research Intern, contributed to this research by assisting in writing, conducting preliminary analysis and conceptualising the topic.