Introduction: Key Highlights in Indonesia Telecoms Market

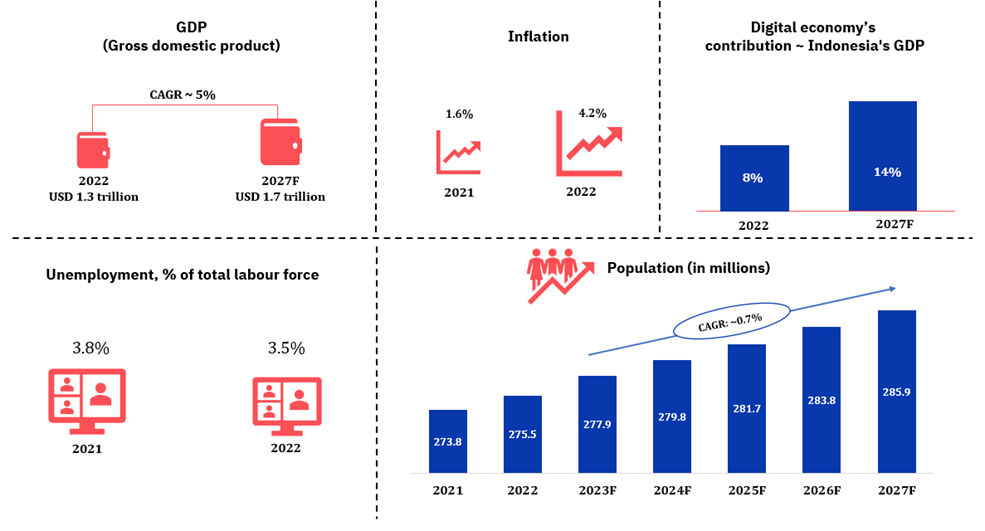

- Indonesia ranks as the third fastest-growing economy among G20 nations and is the largest economy in the vibrant ASEAN region. In 2022, the country’s GDP exhibited resilience, surging from USD 1.1 trillion in 2021 to USD 1.3 trillion, demonstrating an impressive growth rate of 5.3% compared to the global economy’s 3.6% growth.

- According to the IMF, Indonesia’s economy is projected to grow by 4.8% over 2022-23, outperforming the global average of 2.9%. The country is anticipated to maintain robust economic growth of approximately 5% from 2023 to 2027, with moderate inflation hovering around 3.5%.

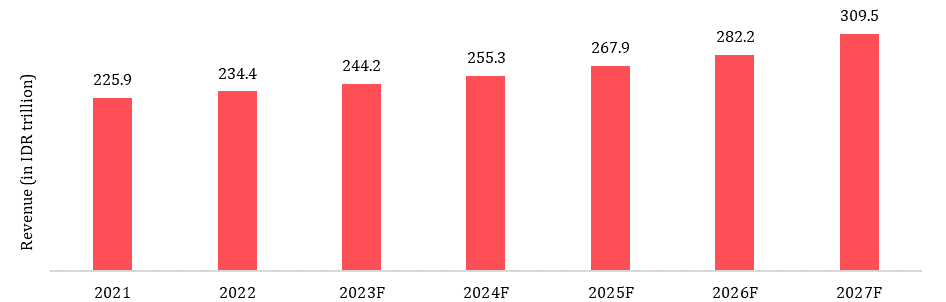

- With the blended ARPU level remaining almost stagnant and stable over the last 4 years, telcos have been shifting their focus to convergent offerings, strategically targeting the enterprise segment and the anticipated release of 5G spectrum that will unravel over the time period 2023-25. The overall telecom revenue is now estimated to grow at a higher rate (CAGR of 6.1% over 2023-27 as compared to 4.6% over 2018-22) to reach to reach IDR 309.5 trillion (~USD 20.7 billion) by 2027.

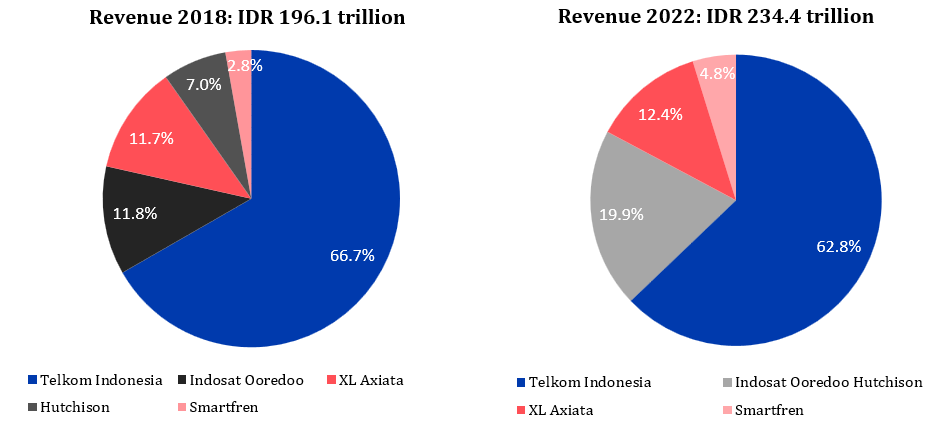

- Indonesia telecoms market is highly competitive and concentrated with the top three players accounting for almost 95% of the overall revenue in 2022. The landscape shifted significantly in 2022 due to the merger of Indosat Ooredoo and Hutchison 3, propelling Indosat Ooredoo Hutchison to secure the second position with a revenue market share of approximately 20%.

- Indonesia holds the fourth position worldwide in terms of mobile subscribers, boasting an impressive 352 million mobile cellular subscriptions as of 2022. It is expected to emerge as the third largest mobile market by subscriptions by 2025.

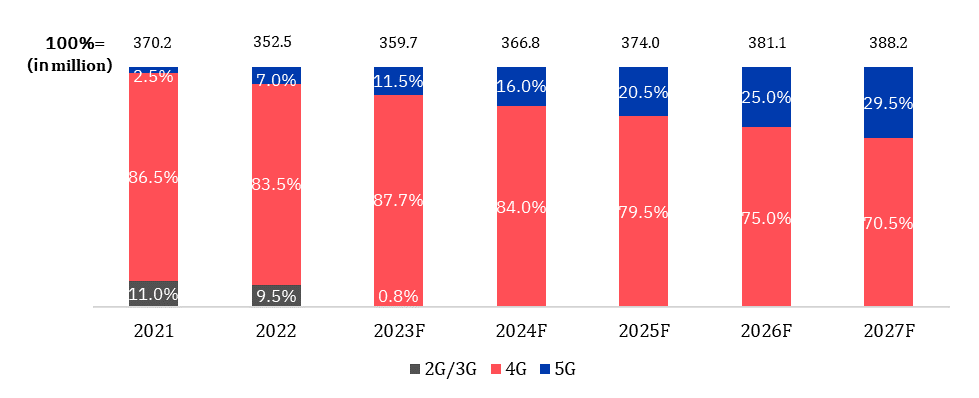

- 4G accounted for ~84% of overall subscriptions in 2022. With the anticipated release of the 5G spectrum over the time period 2023-25, we expect 5G subscriptions to account for ~30% of the overall subscriptions by 2027, and 4G accounting for more than two-third of the subscription count.

- The Indonesian Government Digital Roadmap “2021-2024” is driving the digital ambitions and telcos are emphasising on upgrading subscribers on 4G and 5G networks. However, the limited availability of the 5G spectrum is resulting in slow and selective 5G network deployment.

- The average blended ARPU for Indonesian telcos remained one of the lowest among their global counterparts at around IDR 35,700 (USD 2.38). ARPU has remained almost stagnant owing to stiff competition, resulting in aggressive pricing by telcos. Increasing adoption of 5G during 2025-26 is likely to drive ARPU growth.

- The Indonesia telecom industry is undergoing a transformative phase, marked by a shift towards non-connectivity revenue streams, a focus on the enterprise segment as a new revenue engine, and a strategic move towards convergent offerings.

Macroeconomic Overview

Indonesia is the fourth most populous country with 57% population living in urban areas. Looking ahead, we anticipate a steady population growth from 275.5 million in 2022 to 285.9 million in 2027, with CAGR of 0.7%. Demonstrating economic resilience, the GDP increased from USD 1.1 trillion in 2021 to USD 1.3 trillion in 2022, with 5.3%, and is projected to grow with a CAGR of 5% from 2023-2027 and inflation is expected to moderate at approximately 3.5%.

Furthermore, Indonesia’s digital economy is set to play a pivotal role in the nation’s growth. The contribution of the digital economy to the GDP is anticipated to soar from 8% in 2022 to 14% in 2027. Within the digital economy, E-Commerce holds the largest share with 62%, followed by Fintech with 27%.

In line with the economic growth, the ICT sector too is responding to increasing demand for telecommunications and data services, which is expected to grow significantly by 9.0% – 9.8% in 2023. Additionally, the upcoming general election in February 2024 is likely to influence regulations and market dynamics, impacting the telecom industry’s development.

Exhibit 1: Macroeconomic Indicators- Indonesia

Industry Snapshot of Indonesia Telecoms Market

A. Indonesia Telecoms Market Size and Growth

Indonesia telecom market registered a growth (CAGR) of 4.6% over 2018-22. The blended ARPU has stabilised over the last 4 years and the telcos are now exploring new revenue growth avenues by focusing on convergent offerings, prioritising digital/non-connectivity propositions, and strategically targeting enterprise segment. As a result, the overall market is estimated to grow at a relatively higher rate (CAGR of 6.1% over 2023-27) to reach IDR 309.5 trillion (~USD 20.7 billion) by 2027.

Exhibit 2: Indonesia telecom market revenue forecast in Indonesia, 2021-27F

Source: Telco financials, Twimbit analysis

B. Competitive Landscape

Until 2021, the race to become the second-largest revenue provider was fiercely contested, with Indosat Ooredoo and XL Axiata capturing market shares of 13.9% and 11.8%, respectively. In 2022, the market underwent a significant transformation following the merger of Indosat Ooredoo and Hutchison 3 Indonesia, giving rise to Indosat Ooredoo Hutchison. This strategic alliance propelled Indosat Ooredoo Hutchison to secure the second position in the market, boasting an impressive market share of approximately 20% in revenues.

Exhibit 3: Revenue market share of leading telcos, 2018 and 2022, Indonesia telecoms market

Source: Telco financials, Twimbit analysis

C. Mobile Subscription Growth

Between 2021 and 2022, there was ~5% decline in overall mobile subscriptions, primarily attributed to Telekom Indonesia, which experienced a decline from 176 million to 156.8 million subscribers during this period. All other telcos experienced a growth in subscriber count, driven by their ambitious efforts to acquire and expand 4G subscriptions.

Exhibit 4: Mobile subscriptions market share, 2021-22, Indonesia telecoms market

The overall subscriber count is projected to exhibit modest growth, with an anticipated CAGR of 1.9% from 2023 to 2027, resulting in approximately 388.2 million subscribers by 2027.

D. Subscriber Migration to 4G/5G services

The introduction of 5G technology in 2021, alongside the continued focus on 4G networks, led to a shift in subscribers from older 2G and 3G infrastructure.

The Indonesian Ministry of Communication and Information (Kominfo) prompted telcos to discontinue 3G offerings and prioritise 4G and 5G coverage expansion in 2022, which is likely to drive significant growth in advanced technology subscriptions from 2023 to 2027. Additionally, with the anticipated release of 5G spectrum gradually over the period 2023-25, we expect 5G subscriptions to account for ~30% of the overall subscriptions by 2030.

Exhibit 5: Mobile subscriber forecast by technology generation, 2021-27F, Indonesia telecoms market

E. Prepaid vs. Postpaid Trend

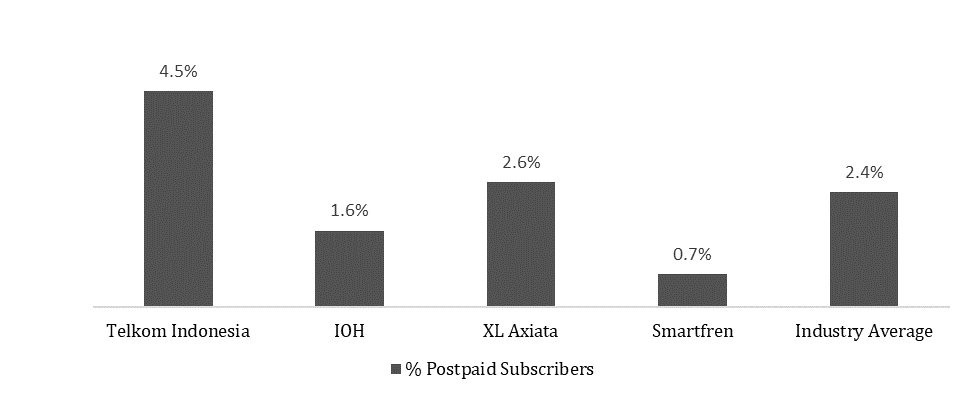

Indonesia telecoms market is predominantly prepaid, with a 97.6% prepaid penetration rate. Telkom Indonesia and XL Axiata are the market leaders in postpaid subscriber penetration, boasting 4.5% and 2.6% respectively. On the other hand, Smartfren lags with less than 1% postpaid penetration.

Exhibit 6: Postpaid Subscribers Penetration (%), 2022, Indonesia telecoms market

F. ARPU Trends

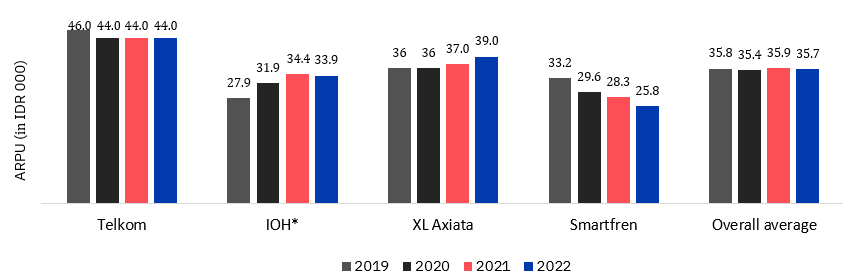

Despite the popularity of smartphones and tablets among consumers, in conjunction with the robust demand for fast data connectivity, mobile blended ARPU has remained almost stagnant over the period 2018-2022 in the range of ~IDR 34,000 (USD 2.7) – ~IDR 36,000 (USD 2.9) highlighting the competition intensity for subscriber acquisition, which has resulted in high prepaid subscription.

Smartfren and IOH reported ARPU figures of IDR 87,400 (~USD 5.7) and IDR 68,200 (~USD 4.4), respectively in the post-paid segment, while in the pre-paid segment, Smartfren and IOH reported ARPU figures of IDR 25,500 (~USD 1.7) and IDR 33,300 (~USD 2.2) respectively.

Exhibit 7: Blended ARPU for leading telcos, 2021-22, Indonesia telecoms market

Source: Telco financials, Twimbit analysis

G. Capital Expenditure and Infrastructure Upgrades

To support 4G capabilities and advance network infrastructure, telcos have increased their Capex. Telkom Indonesia’s Capex increased by 12.6% from 2021 to 2022, reaching IDR 34,156 billion (~USD 2.2 billion), with a focus on 4G and 5G site deployment. IOH reported a Capex of approximately IDR 22,000 billion (~USD 1.4 billion) in 2022.

Exhibit 8: Telcos tower ownership trend by technology, 2018-22, Indonesia telecoms market

Top Industry Challenges in Indonesia Telecoms Market

A. Churn reduction and ARPU improvisation

The Indonesian mobile market’s high prevalence of prepaid wireless subscribers, comprising approximately 97% of total mobile subscriptions in 2022, creates volatility as these subscriptions are frequently deactivated and customers can easily switch providers. Leading telcos like Telkom Indonesia (Telkomsel) emphasised on reducing churn, with sales activities being centered around pursuing renewal program to reduce rotational churn.

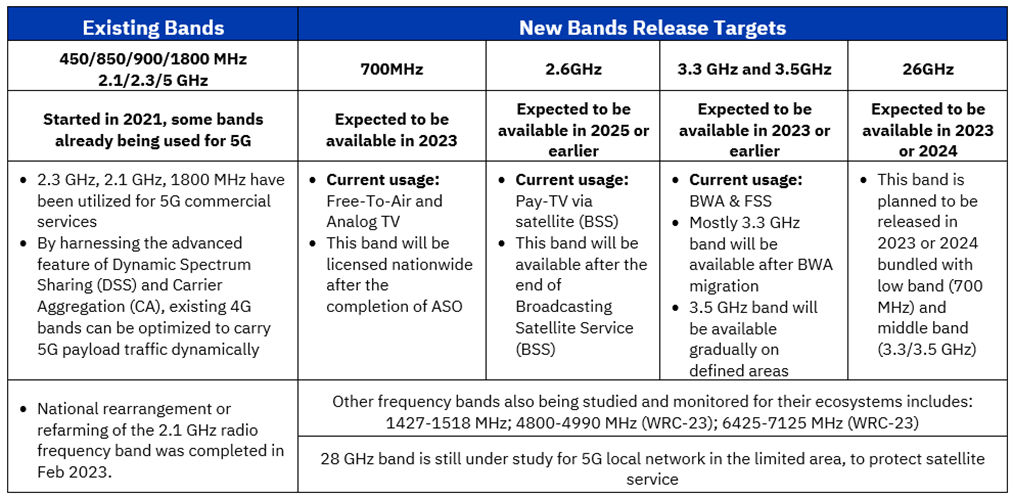

B. Lack of sufficient 5G spectrum availability

The lack of sufficient 5G spectrum availability has affected the launch of 5G services, which remain limited to select regions and larger cities. Telkom Indonesia was the first operator to launch 5G services in Jakarta in 2021, followed by IOH in two cities in 2022. Smartfren and XL Axiata are focusing on strengthening their 4G network.

Exhibit 9: 5G spectrum roadmap summary, 2022-25, Indonesia telecoms market

Source: Kominfo, 5Gnow.id, Twimbit analysis

To monetise 5G technology, telcos are forming strategic partnerships with technology vendors to enhance their network and infrastructure readiness ahead of spectrum allocation and service launches. For instance, XL Axiata has partnered with Huawei (for establishing smart city) and Juniper Networks (to accelerate the 5G network deployment). IOH has collaborated with ZTE, Ericsson, NEC and ADVA for 5G service offerings.

C. Data Protection Bill to further add to telcos cybersecurity expenses

In 2022, multiple alleged data breach incidents were reported, affecting state-owned telco IndiHome (owned by Telkom Indonesia) and an electricity company. The breaches involved sensitive information, including activation data for 1.3 billion telecom sim cards, records from the general election commission, and correspondences between the state intelligence agency and presidential office.

In response to the growing number of data leaks and breaches at government firms and institutions, the Indonesian parliament passed a Personal Data Protection (PDP) bill in September 2022.

This would require investments from telcos in cybersecurity infrastructure and possible realignment of their existing process to comply with Government regulations.

Key Trends and Growth Opportunities in Indonesia Telecoms Market

A. Increasing Focus on Non-Connectivity Revenue Streams

In recent times, Indonesia telecoms industry has been experiencing a notable shift towards diversifying revenue streams beyond traditional connectivity services. For example, Telkomsel established a separate subsidiary named INDICO in March 2022. The primary objective of INDICO is to spearhead the development of cross-sectoral services and solutions, leveraging technology innovation to accelerate the adoption of digital lifestyle solutions. By capitalising on its adjacent ecosystem’s assets and capabilities, Telkomsel aims to venture into cross-sectoral digital solutions beyond traditional telecom use cases.

This strategic shift towards non-connectivity offerings has proven to be fruitful for Telkomsel, as witnessed by the surge in its Digital Business revenue. Comparing Q2-2022 to Q2-2023, the Digital Business revenue witnessed a substantial growth of 17.4% on a year-on-year basis, soaring from IDR 2.6 trillion (USD 0.17 billion) to IDR 3.1 trillion (USD 0.21 billion).

B. Telcos focus on the enterprise segment as new revenue and value engine

Effectively capitalising on the vast B2B market opportunity necessitates a strategic shift in positioning and alignment of business priorities for telcos. To tap into this potential, telcos are positioning themselves as product engineering companies (Techcos) and establishing dedicated enterprise units.

For instance, Telkomsel established a specialised business division named “Telkomsel Enterprise” offering customised enterprise solutions, including business internet packages, IoT services, cloud computing, and managed services. It also established FMC Commercial Team, with 2 main tasks, namely Joint Operations and Joint Sales Services. Indosat Ooredoo Hutchison also offers a range of enterprise solutions through its “Indosat Business” segment.

To bolster enterprise offerings, telcos are forging collaborations with technology vendors. For example, IOH has partnered with IBM and Tech Mahindra to develop enterprise digital solutions for Cloud and 5G networks. Indosat Ooredoo also had partnered with Google in Oct 2021, to offer Indosat Digital Analytics (iDA) as a data insight & analytics platform to enterprises.

C. Focus shifting towards convergent offerings to boost revenue

Indonesian telcos are strategically positioning themselves as integrated service providers to enhance their operating efficiencies and utilisation, thus seizing growth opportunities and improving their ARPU. For example, in April 2023, Telkom Indonesia announced a spin-off agreement with its mobile subsidiary Telkomsel to integrate its fixed broadband business, IndiHome, as part of its Fixed Mobile Convergence (FMC) strategy. This move aims to strengthen Telkom Indonesia’s position in the market. Axiata group is also aiming to position XL Axiata as a converged mobile, fixed, and content service provider through its acquisition of Link Net, enabling it to capitalise on FMC and Fixed Broadband (FBB) market opportunities.

Conclusion

The Indonesian Government’s digital roadmap for 2021-2024 will drive the digital transformation agenda, and the emphasis on adopting 4G and 5G services will result in robust growth in the telecommunications landscape.

The fixed telephony market, currently dominated by incumbent Telkom Indonesia, is likely to face increased competition as telcos implement FMC strategies to boost ARPU levels. In the mobile segment, which is expected to be primarily 4G-driven over the next few years, intense competition is anticipated with the availability of 5G spectrum to telcos from 2023 to 2025.

Given the intense competition in the Indonesia telecoms market and the likelihood of further intensification, the industry is expected to see further consolidation as telcos explore options for consolidation or collaboration with other players to achieve operational efficiency. Earlier in October 2021, there were reports of XL Axiata and Smartfren exploring options of merger or network sharing arrangement. This trend aligns with the presence of only three major players in neighboring countries i.e. Philippines, Thailand, and Vietnam.

Explore more on telecoms: Here

You might also like: Japan telecom market update 2023

Upcoming report- an updated version of Malaysia telecoms update 2022