Japan telecom ecosystem has earned a distinguished reputation as a trailblazer in technological advancement, consistently setting the stage for innovation and rapid adoption. Operators aim to shift their focus to next-generation technologies such as IoT, big data, AI, and M2M to diversify revenue streams. As 5G adoption brings challenges and opportunities, Japan telecom market is at the forefront of this transformative wave. This report delves into the dynamics of the Japan telecom market. It covers the following:

- Key Highlights (executive summary)

- Industry snapshot (key industry figures)

- Top industry challenges

- Top growth opportunities

- Top trends in the market

- Conclusion

Key highlights in Japan telecom market

- Japan telecom market is a highly mature and competitive market led by innovative telcos such as NTT Docomo, KDDI, SoftBank, and Rakuten.

- Japan telecom market recorded nearly 196.5 million subscribers in 2022. Around 67% of the total subscribers were 4G users, 30% were 5G users, and only 3% were 3G users. Nearly all 3G subscribers will migrate to 4G or 5G networks by 2024.

- Tariff reductions and regulatory pressures have negatively impacted the mobile ARPU over the past few years. However, the telecommunications industry is expected to show signs of improvement and stabilizing ARPU in the coming years.

- Japan telecom operators have demonstrated remarkable innovation and diversification beyond traditional connectivity services, achieving an impressive 22.2% contribution from non-connectivity revenues.

- Enterprise business has emerged as the growth engine, with 18.3% of total revenues on an aggregate basis.

- Infrastructure sharing for collaboration and cost optimization has become a common trend in Japan.

- Fibre and PayTV services are imperative to shape the operator landscape, as they can meet the growing demand for video experiences, multi-brand strategies, and low-price bands.

Industry snapshot of Japan telecom market

1. Mobile subscribers in Japan telecom market

Japan emerged as an early adopter of 5G services in Asia, initiating commercial deployments in March 2020. Following South Korea and Mainland China, Japan became the third country in East Asia to introduce commercial services, positioning itself as a frontrunner in regional 5G adoption.

Major market participants, including, NTT Docomo, KDDI, SoftBank, and Rakuten, have all made significant strides in deploying 5G networks. The former three participants commercially launched their services in March 2020, while Rakuten commenced operations in October 2022.

The telecom ministry aims to encompass 95% of the population by the end of the 2023 financial year. All major operators are fully aligned with these ambitious growth targets.

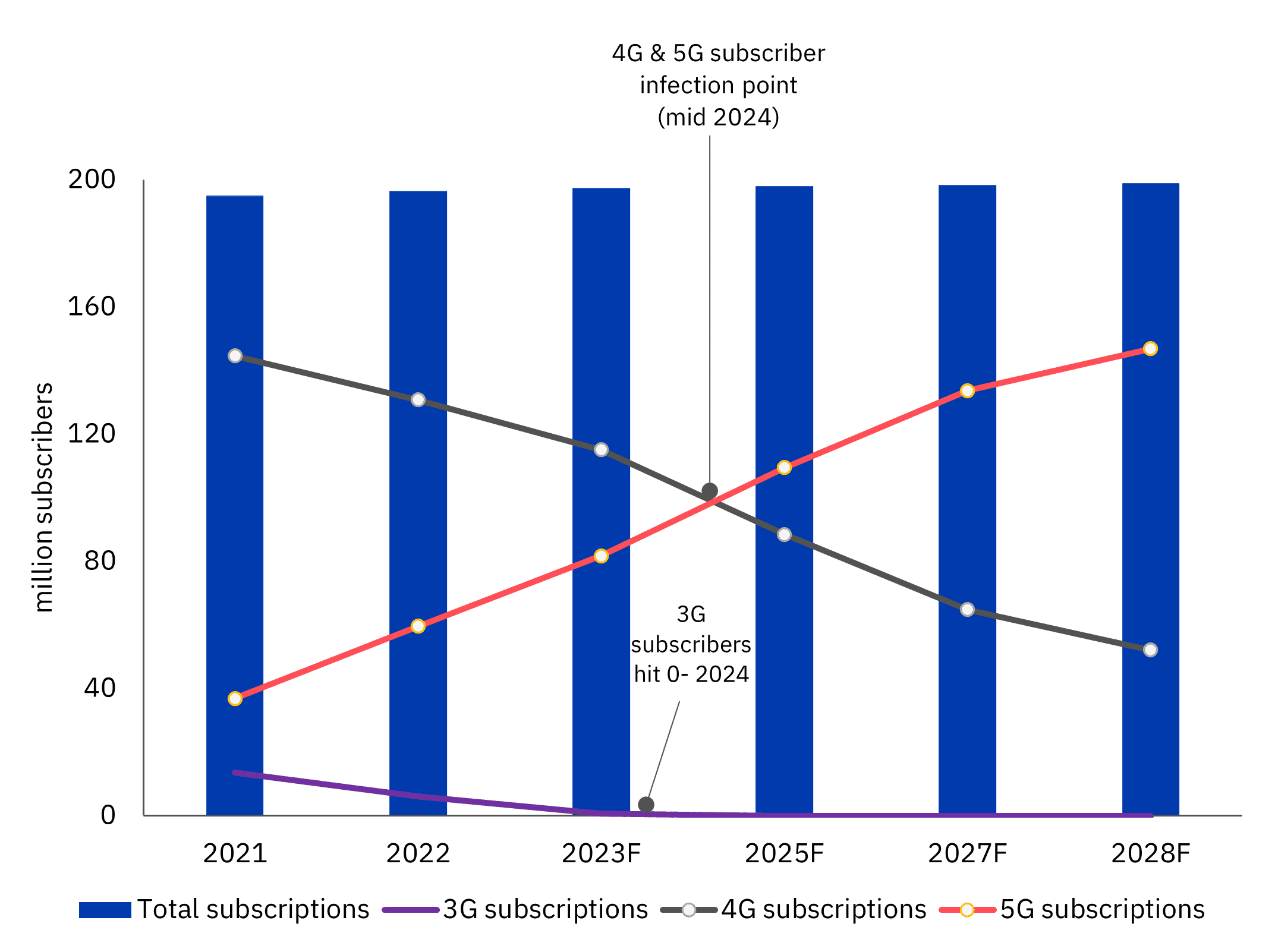

Exhibit 1: Number of subscribers by network generation (2021-2028F)

Japan recorded approximately 196.5 million subscribers in 2022. 67% of the total were 4G users, 30% were 5G users, and only 3% were 3G users. The market has reached saturation and is expected to experience stagnant growth. In the coming years, 5G subscribers will hold the majority and will capture around 75% of the total market by 2028.

The transition from 3G to 4G has accelerated significantly, and analysts predict that 3G subscribers will reach zero by 2024. For instance, KDDI ceased 3G services in March 2022, with SoftBank and NTT Docomo planning to switch off their 3G services in January 2024 and March 2026, respectively.

2. Major market participants in Japan telecom market

Leading telcos such as NTT Docomo, KDDI, SoftBank, and Rakuten spearhead innovation and characterize Japan’s telecom market as a mature and fiercely competitive industry.

The popularity of smartphones and tablets among consumers, in conjunction with the robust demand for fast data connectivity, has propelled the mobile market in Japan. Despite this, the industry blended ARPU declined by 4.4% YoY, from JPY 4,145 (US$ 31.8) in FY 2022 to JPY 3,964 US$ 30.4) in FY 2023 due to regulatory pressures.

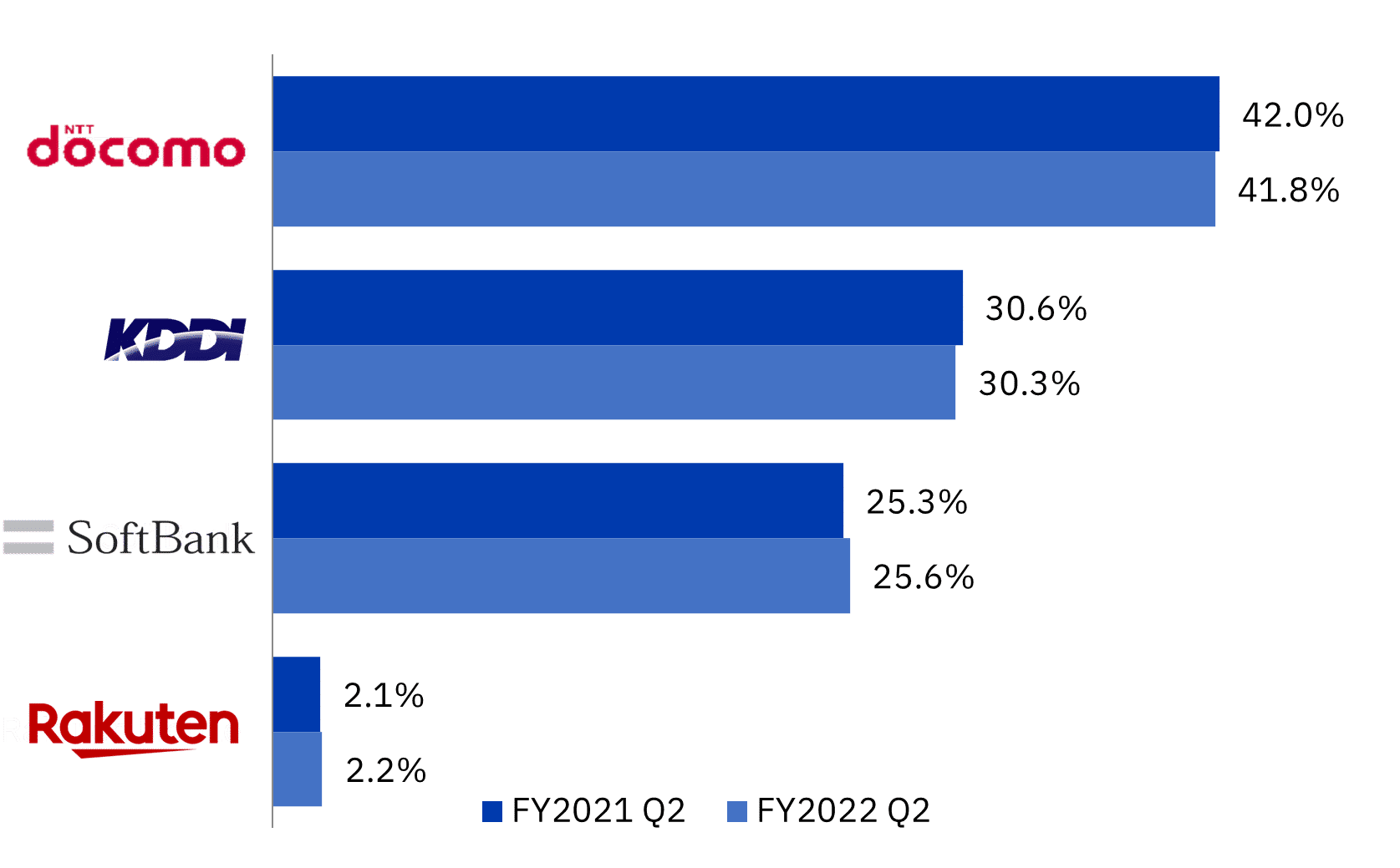

Exhibit 2: Share of mobile communications contracts- Q2 2022 (Inclusive of aspects concerning service provision to MVNOs) (Q2 2022)

NTT Docomo continues to remain ahead of its competitors. In Q2 2022, NTT Docomo achieved a 41.8% market share, establishing itself as the winner, followed by KDDI (30.3%), SoftBank (25.6%) and Rakuten (2.2%).

NTT Docomo is the largest telco in Japan and a subsidiary of the incumbent telephone operator NTT. NTT Corp also announced plans to consolidate NTT Docomo as a wholly-owned subsidiary in September 2020. This consolidation aims to foster closer collaboration within the wider NTT Group.

As Japan’s second-largest telecommunications provider, KDDI Corporation offers mobile cellular services under the “au by KDDI” brand. In addition, the telco offers ISP network and solution services under the brand name “au one net.” KDDI also provides long-distance and international voice and data communications services i.e. “au Hikari” and the ADSL broadband service i.e. “ADSL One”.

SoftBank, the third largest telco in Japan, is part of the broader technology conglomerate, SoftBank Group. The CEO, Son Masayoshi, continues to spearhead SoftBank, remaining active in the telecom’s investments, including 5G initiatives and other emerging technologies.

Rakuten entered the market in 2014. It is a subsidiary of the Rakuten Group, a leading Japanese e-commerce and internet services company. Despite being a comparatively smaller player than the top three, its strong existing customer base and brand presence has allowed it to gain a respectable market share. Additionally, Rakuten offers competitive mobile and broadband services, emphasizing its strength in the digital ecosystem.

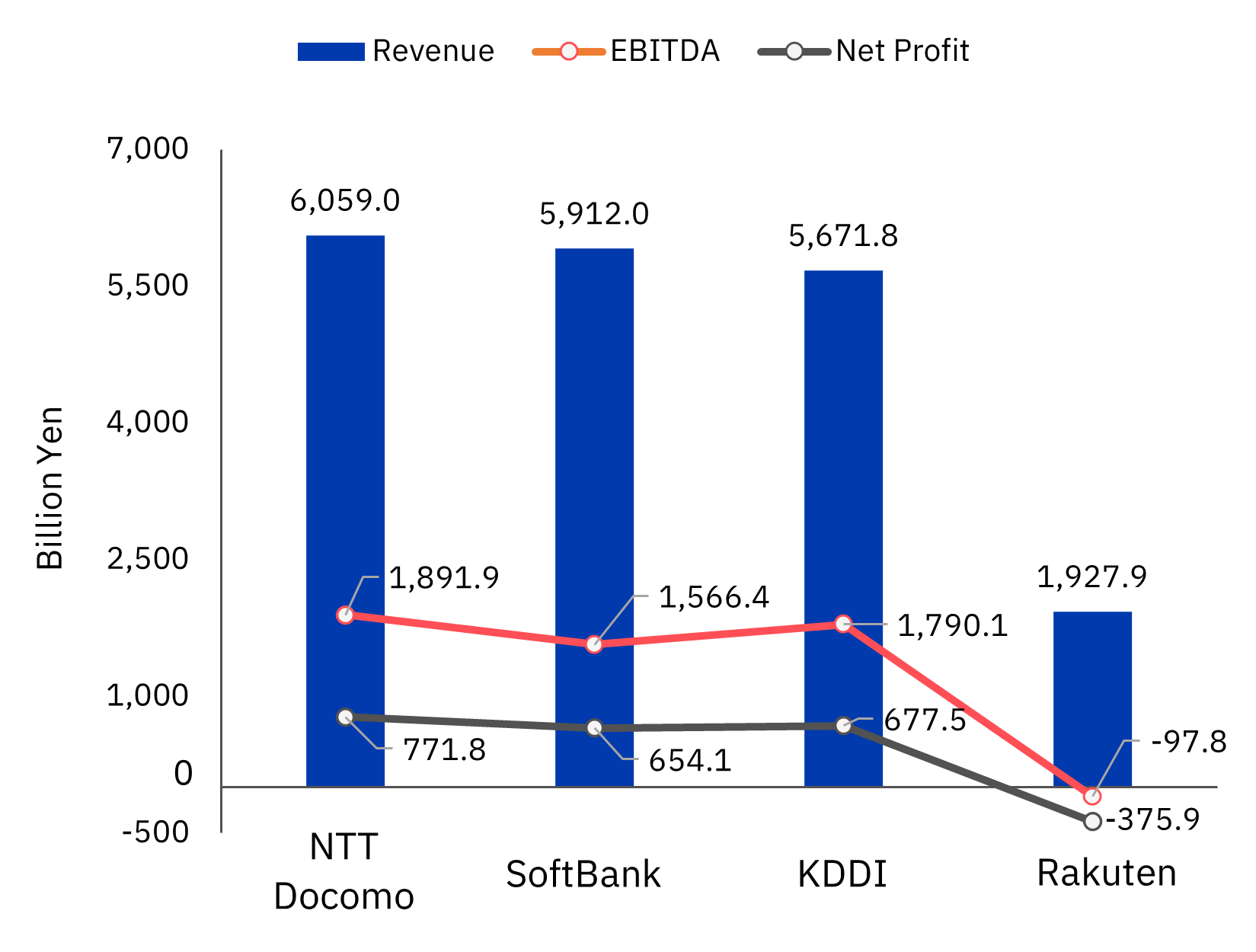

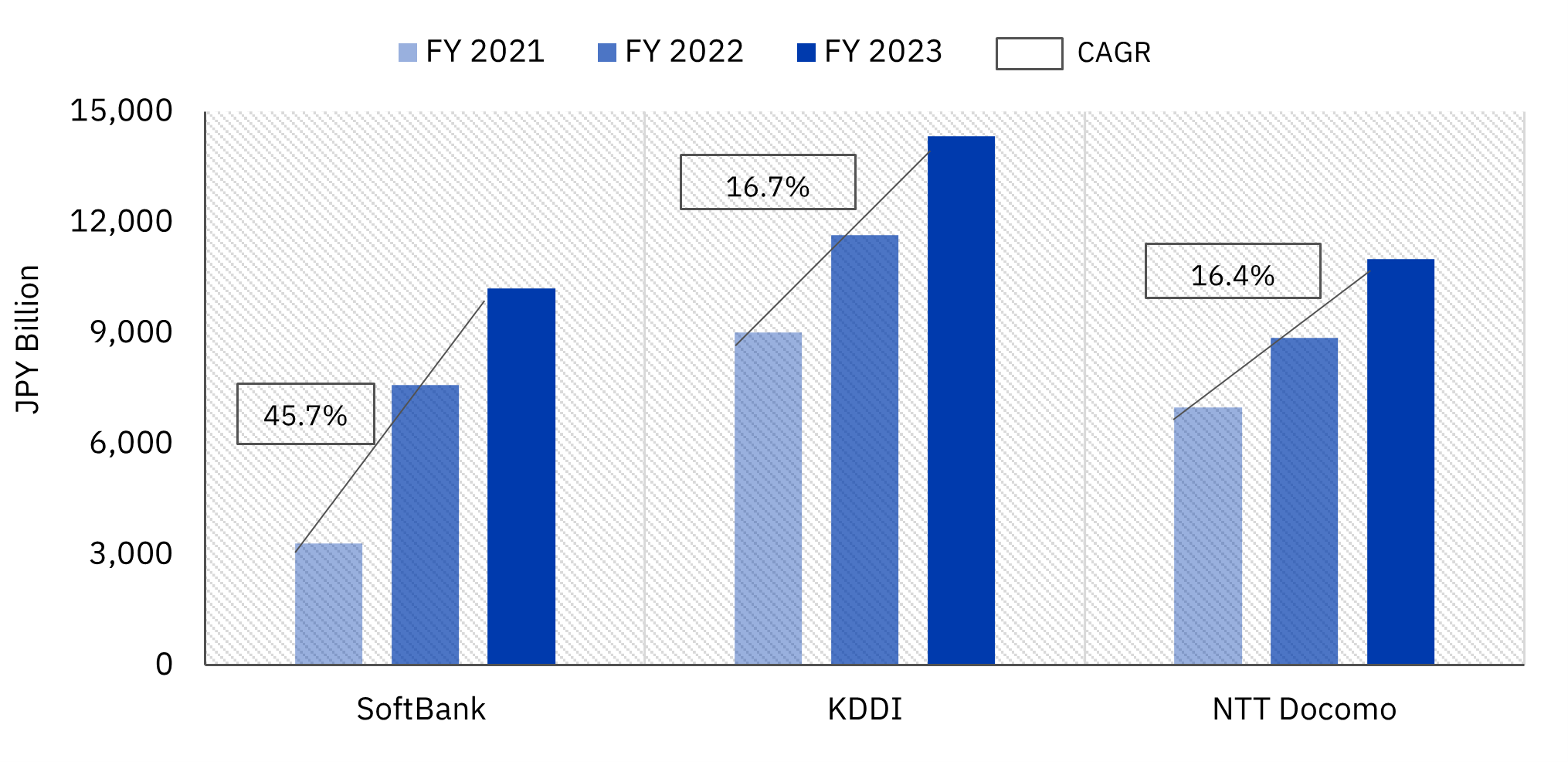

Exhibit 3: Financial performance of telcos (FY2022-23)

Source: Annual reports and filings, Twimbit analysis

Top industry challenges in Japan telecom market

1. Competitive intensity and regulation limit the ability to increase ARPU for connectivity services

Mobile ARPU in Japan ranks among the highest in Asia Pacific, with an industry blended ARPU of JPY 3,964 (US$ 30.4) as of the year ending March 2023. However, three major factors have led to a significant decline in mobile ARPU. These include:

- Regulatory pressure to lower prices

- The entry of Rakuten with its one-price unlimited data plans

- Cheaper packages and greater flexibility by MVNOs (mobile virtual network operators)

- A) Regulatory pressure to lower prices

Since 2015, the Japanese government has implemented extensive measures to lower prices and enhance mobile service affordability. These efforts include:

- An effort to decrease mobile prices by 40% as announced by Former Prime Minister Yoshihide Suga in August 2018.

- Cheaper data plans by telcos, including NTT Docomo’s and KDDI’s, with up to 40% in tariff reductions from May to June 2019.

- Additional regulations included a law banning bundled packages and proposed limitations on handset discounts and contract termination penalties.

- B) The entry of Rakuten with one-price unlimited data plans

Rakuten disrupted the market by launching one-price unlimited data plan services in April 2020. Following this, the incumbent operators responded by lowering their prices and launching MVNOs. NTT Docomo and KDDI lowered their prices in response to Rakuten’s unlimited plan services. SoftBank launched “SoftBank on Line” MVNO/brand to counter competition in March 2020

- C) Cheaper packages and flexibility by MVNOs

The decision to launch cheaper packages and flexibility has enabled MVNOs to carve out a niche in the market. Specifically, it achieved this by:

- Targeting lower-value users with affordable mobile data plans.

- Providing data connectivity for secondary devices like tablets and personal computers with e-SIMs.

However, MVNOs will have to slash prices further to compete with the three big telcos. This decision could leave MVNOs financially unsustainable, leading to their eventual move out of the market and potentially worsening consumer choice.

2. Transforming 5G Capex into profitable enterprise services

- High cost of deploying and expanding 5G networks

Japanese government aims for 97% coverage by March 2026 and 99% coverage by 2030; meeting these targets requires substantial investments.

Telcos struggle to make a compelling business case to realize an ARPU uplift from offering 5G services. Additionally, telcos face intense competition from OTT (over-the-top) players in mobile gaming, which could be a key driver for 5G services.

- The complexity of catering to diverse enterprise needs

Enterprise business is the biggest potential growth driver for 5G services. The potential applications in manufacturing, logistics, healthcare, and transportation require significant customization to enable digital transformation and improve operational efficiency.

To achieve the deep industry expertise collaboration with ecosystem players is essential. The skill set required from the sales, pre-sales and solutions teams is quite different from the existing capabilities of telcos. This is the single biggest challenge for telcos as they look to ramp up their enterprise business growth.

Top growth opportunities in Japan telecom market

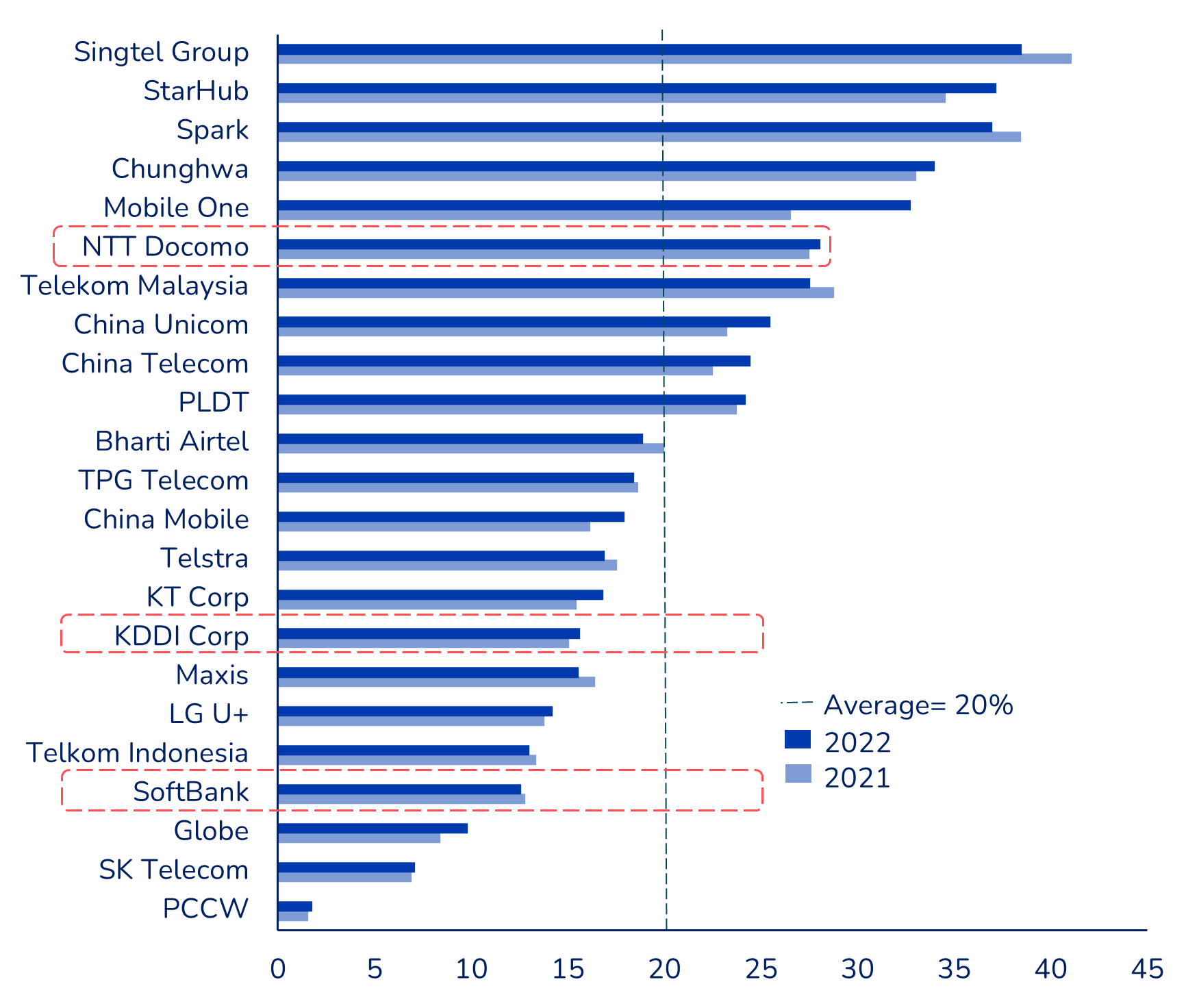

1. Diversification into non-connectivity streams

Japanese telcos have demonstrated remarkable innovation and diversification beyond traditional connectivity services.

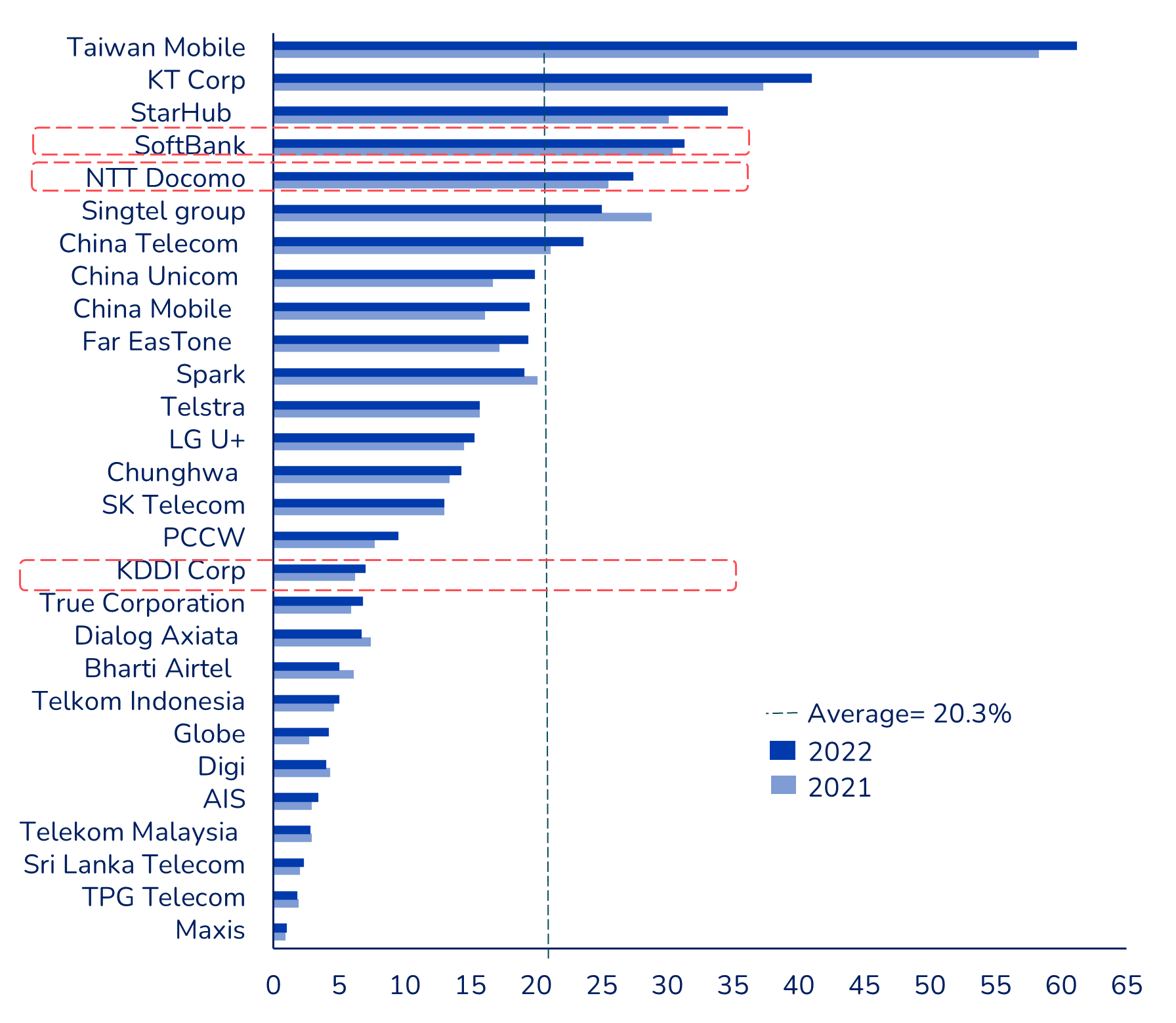

Our analysis of the top 28 telcos in the Asia Pacific region highlights that on an average, non-connectivity revenues accounted for 20% of total revenues. However, the top 3 Japanese telcos surpassed this average with an impressive 22.2% contribution from non-connectivity revenues.

Furthermore, these revenues experienced a robust average growth rate of 9.7%, outperforming the overall revenue growth rate of 3.5% in 2022 YoY. Notably, SoftBank emerged as the most diversified telco in the region.

Exhibit 4: Top Telcos percentage contribution of non-connectivity revenues to total revenue (Asia Pacific) in 2022

2. Financial services: A lucrative venture enabling a cashless future

Driven by the surge towards a cashless society, telcos ventured into financial services and witnessed significant growth

In FY 2023, the transaction value for financial/payment services of;

- KDDI increased by 22.9% YoY, reaching JPY 14,388 billion (US$110 billion)

- NTT Docomo increased by 24.2% YoY, reaching over JPY 11,000 billion (US$ 84.3 billion).

- SoftBank increased by 34.2% YoY, reaching JPY 10,200 billion (US$78.2 billion).

All three telcos sustained robust growth, with an impressive aggregate growth rate of 26.4% YoY, a cumulative of US$ 272.5 billion

SoftBank emerged as the frontrunner, exhibiting the highest growth rate, primarily driven by the QR code payment business. Furthermore, Softbank strategically leveraged PayPay to expand its fintech presence, capitalizing on its large user base (over 54 million registered users).

Exhibit 5: Financial and payment transactions, JPY bn (2021 to 2023 year ending March

3. Enterprise business records 18.3% of total revenues on an aggregate basis

While Japanese telcos have made significant strides in the enterprise segment, there remains substantial untapped potential for growth.

Our analysis of enterprise business revenues among 23 Asia Pacific telcos reveals that, on an average, they accounted for 20% of total revenues. However, the top 3 Japanese telcos fell slightly below this average, reaching 18.3%.

These telcos are well positioned in the cloud, data centres, IoT, AI, and big data, leveraging these applications to address real-time societal challenges.

Exhibit 6: Top Telcos percentage contribution of enterprise revenues to total revenue (Asia Pacific telcos) in 2022

- KDDI recorded the highest growth rate in enterprise revenues of 7.8% YoY in 2022, driven by the DX (NEXT core) business growth.

- The NEXT core has three broad segments (Corporate DX, Business DX, and Business infrastructure services).

- NTT Docomo charted the highest % contribution of enterprise revenues to a total of 28.5% in 2022.

- Enterprise revenues became a major contributor to the overall profit increase of NTT Docomo.

- NTT Docomo targets large enterprises by reinforcing integrated solutions and SMEs by providing DX support solutions.

- SoftBank offers an extensive service lineup of 100+ digital products & services.

- The telco emphasized growth in recurring revenue, comprising over 70% of the business, through cloud, security, IoT, data centre, & digital services.

- The cloud revenue increased by 24%, and security revenue increased by 22% in Q1-Q3 2022 compared to Q1-Q3 2021.

4. The emergence of Private 5G in Japan

Japan is the second largest private 5G market in APAC, with numerous deployed sites and applicants for private 5G deployments. Regulatory authorities have designated specific frequency bands (4.6-4.8GHz and 28.2-29.1GHz) for private networks, prioritizing the industry sector.

Japan has a local licensing process for private networks and plans to expand rural base stations, focusing on sectors like manufacturing, transportation & logistics, smart cities, and enterprise campuses. As a result, Japan is among the top countries in APAC for private 5G market readiness.

Exhibit 7: Market readiness benchmarking of Asia Pacific countries on Private 5G

Analysts predict Japan will increase its expenditure on private 5G networks from US$ 111 million in 2022 to US$ 700 million by 2027, with anticipated deployments in manufacturing, airports, and ports. In the mid-term, sectors such as mining, energy & utilities, healthcare, education, and others will likely embrace private 5G.

Top trends in Japan telecom market

Infrastructure sharing

Infrastructure sharing is vital for the growth of the telecom industry in Japan, as it can help accelerate 4G and 5G deployment, optimize bandwidth usage and build a sustainable 5G infrastructure.

- Rakuten formed a joint venture with TEPCO called Rakuten Mobile Infrastructure Solutions in July 2022.

- The collaboration utilizes TEPCO’s extensive network assets to accelerate the deployment of 4G and 5G mobile base stations.

- NTT Docomo partnered with JTOWER, the country’s first ‘Infra-Sharing’ company, in March 2022 to promote Infra-Sharing in its existing towers.

- The agreement includes 6002 telco towers to be transferred to JTOWER for a max of JPY 106.2 billion (US$ 922 million).

- The MIC approved a plan enabling mobile telecom operators to share frequencies with TV stations at specific times to optimize bandwidth usage in July 2021.

- KDDI and SoftBank reached an agreement to build 5G infrastructure in rural Japan through a joint construction management company in July 2019.

Bundling Fiber and PayTV services

- Japan is ranked among the top ten global IPTV market. It has a thriving multi-channel Pay-TV industry, with services accessible nationwide via cable TV, satellite, IPTV and video-on-demand services.

- The increasing availability of competitively priced subscription packages and a growing number of providers will fuel the demand for IPTV over the period 2023-26.

- Mobile operators are boosting their video-streaming services with the rollout of 5G.

- NTT DOCOMO has a tie-up with the Japanese subsidiary of Walt Disney (US) to stream Disney films for a fixed monthly fee.

- KDDI has a similar deal with Netflix (US).

- SoftBank offers content from TVer and Hulu (US).

Explore more on Telecoms: Here

Here is another insightful read for you- Unveiling the best: Benchmarking APAC telcos in Q1 2023