Strong credit growth, improved asset quality, and higher interest income continue to be key factors for the strong financial results of India’s banking sector in Q3 2023.

- The loan portfolio of the leading 8 banks grew by 23.2% YoY (year-on-year) from USD 932.27 billion in Q3’22 to USD 1148.56 billion in Q3’23.

- Better collection efficiencies and a pickup in the economy have improved asset quality.

- Decreasing interest margins due to rapid increases in benchmark interest rates.

- 250 basis points (bps) increase in the repo rate since May 2022 and is currently at 6.5%.

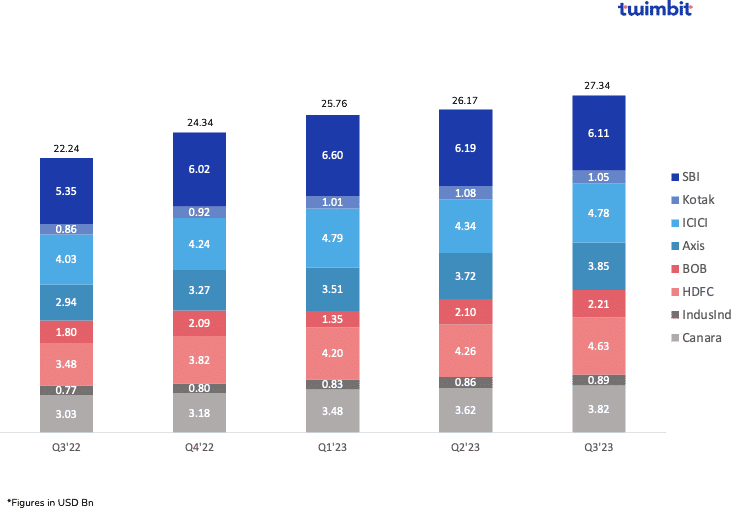

Revenue

Net revenues grew by 22.9% YoY to USD 27 billion

This growth for the leading 8 banks was primarily driven by an 18.7% increase in net interest income and a 26.56% increase in non-interest income. Of the leading 8, Canara Bank reported a decline in non-interest income by 4% from USD 0.59 billion in Q3’22 to USD 0.56 billion in Q3’23.

Regarding net revenues, HDFC recorded the highest at 33.1%, from USD 3.48 billion to USD 4.63 billion (Exhibit 1). Similarly, the bank recorded the highest increase in net interest income at 30.3% and the second-highest increase in non-interest income at 41%. These played a significant role in improving the bank’s overall growth.

Conversely, SBI charted the lowest net revenues among the leading 8 at just 14.15%, increasing from USD 5.35 billion to USD 6.11 billion. In dollar value, SBI reported the second-highest increase among all the banks analysed, following HDFC.

Exhibit 1: Net revenues of the leading 8 Indian Banks

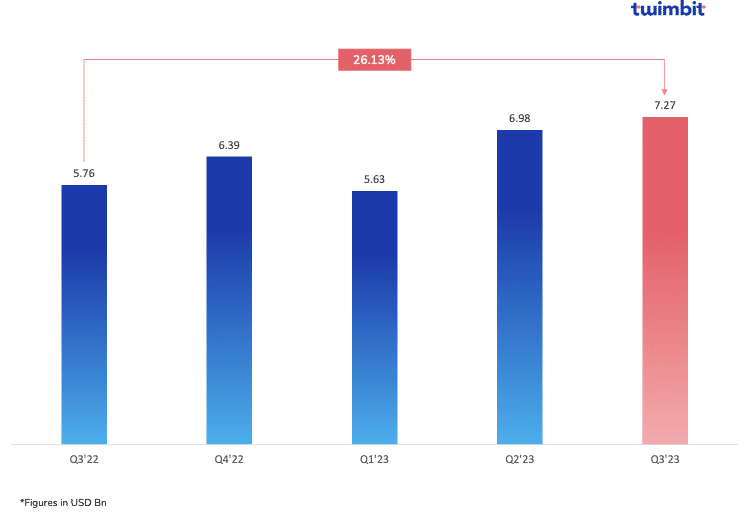

Profitability

Net profits grew by 26% YoY to USD 7.3 billion

HDFC reported the highest growth in its net profits at 50.67%, from USD 1.29 billion in Q3’22 to USD 1.94 billion in Q2 2023 due to its strong loan growth, which grew by 57.5% in Q3 2023. Its net interest income also rose by 30.3%, driven by loan growth.

While Q2 2023 depicted the dominance of public sector banks with an average growth of 113.60% in their net profits, this was not the case for Q3 2023. Now, both the public and private sectors are recording similar growth in net profits, with;

- Average net profit growth of public sector banks at 27.82%

- Average net profit growth of private sector banks at 26.89%

The combined profit of the three public sector banks increased by 16.9% to USD 2.71 billion in Q3 2023. In contrast, the combined profits of the five private banks rose by 32.37% from USD 3.44 billion to USD 4.55 billion in Q3’23.

Exhibit 2: Consolidated net profits of the leading 8 Indian Banks

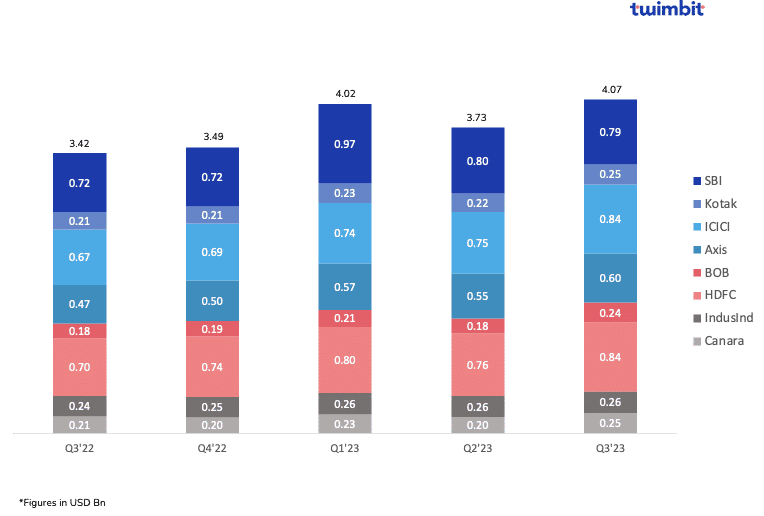

Fee-based income

Fee incomes grew by 19.13% to USD 4.07 billion

Of the leading 8 banks, all but IndusInd bank reported double-digit growth in their fee incomes. Bank of Baroda reported the highest increase at 31.75%, from USD 180 million to USD 240 million. Fee-based income constituted 48% of the bank’s non-interest income.

The most significant factor for the banks’ fee income is due to the high demand for:

- Mutual funds

- Other investment options

- Corporate banking services

Exhibit 3: Fee incomes of the leading 8 Indian Banks

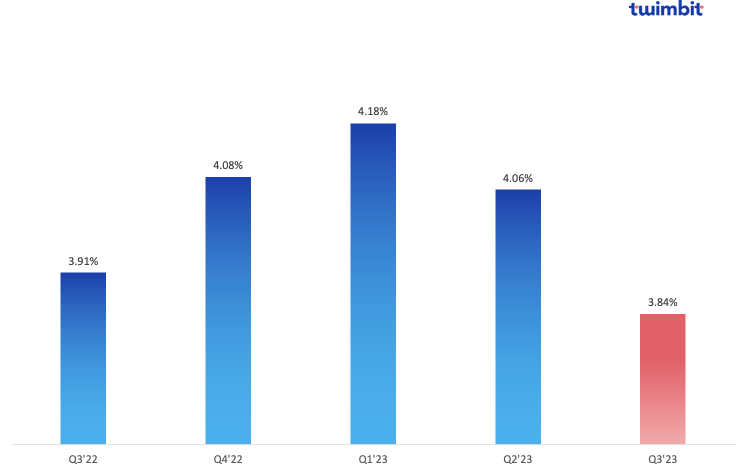

Net interest margins (NIM)

NIM take a further dip in Q3 2023

As approximately 80% of the loans are based on floating interest rates, banks experienced a significant increase in interest income when repo rates began to rise.

On the liabilities side, most deposits are fixed, which means that higher interest rates only affect newly acquired and renewed deposits. However, due to peaking interest rates and the convergence of deposit rates, Indian banks are facing a reduction in their high-interest margins in the previous quarters.

NIMs decreased over the previous quarter (Exhibit 4), with 3 of 8 banks witnessing a decline in NIMs from Q2 2023 to Q3 2023. This decline was substantial enough to drive down the overall average NIM for all eight banks.

Irrespective, Indian banks still have a higher NIM than banks in other countries in APAC. These high NIMs are due to a credit surge, higher lending rates by the RBI, and the low cost of holding deposits.

Exhibit 4: Consolidated net interest margins of the leading 8 Indian banks

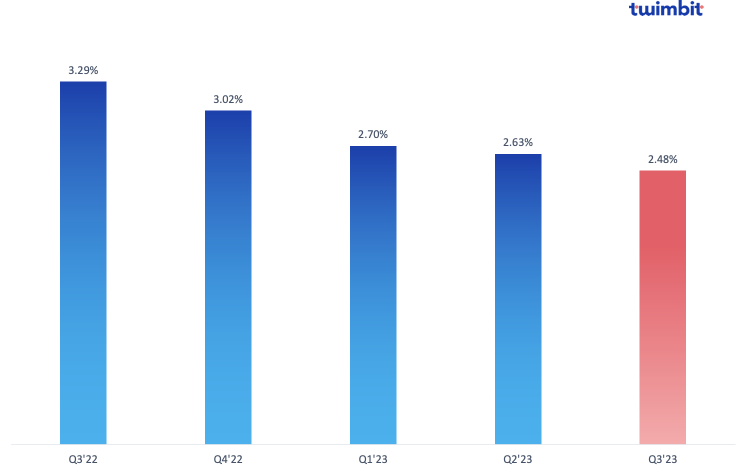

Non-performing assets (NPA)

NPA fell by 81 basis points (bps) in Q3 2023

The average non-performing assets (NPAs) of the leading 8 banks witnessed an 81 basis point decline, resulting in a current NPA of 2.48% (Exhibit 5).

Of the leading 8, 3 are public sector banks. Despite operating with a higher NPA ratio, these banks recorded the highest decline in their NPAs by an average of 30.1% compared to the decline witnessed by private banks at an average of 13.45%.

Conversely, only HDFC recorded an increase in its NPA from 1.2% in Q3’22 to 1.34% in Q3’23. Indian banks have been able to control their NPAs due to the following:

- Improved credit appraisal and monitoring to identify potential NPL early and apply corrective measures

- Stringent credit checks to assess applicants’ creditworthiness and risk of default

These initiatives help India avoid disbursing loans to applicants below the acceptable credit risk level.

Exhibit 5: Consolidated non-performing assets of the leading 8 Indian banks

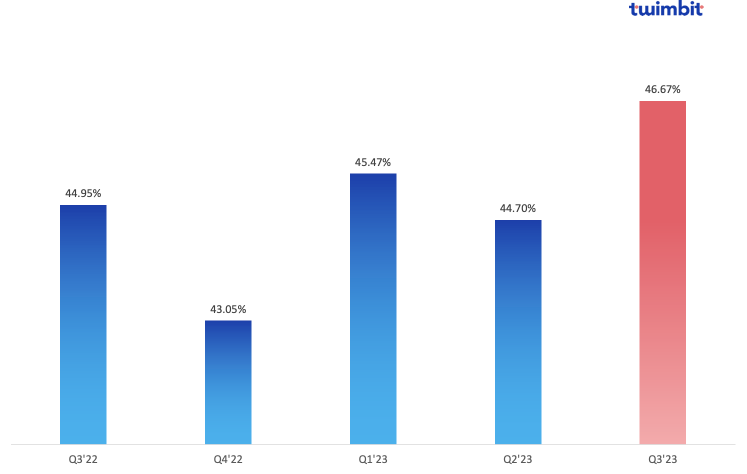

Cost efficiency (CE)

CE for Indian banks increased by 1.72% between Q3 2022 and Q3 2023

Indian banks have been more efficient in their operations than peers in other regions. However, their average cost efficiency increased to 46.67% in Q3 2023 from 44.95% in Q3 2022 (Exhibit 6).

Of all the banks analysed, only SBI has its cost efficiency above the threshold value of 50%. During the period analysed, the bank’s cost-efficiency ratio vastly increased from 52.06% in Q3 2022 to 61.39% in Q3 2023.

This significant increase in the bank’s cost efficiency was due to a 34.6% increase in operating expenses from USD 2.79 billion in Q3 2022 to USD 3.75 billion in Q3 2023. The growth was primarily driven by a 47% increase in staff-related expenses. On the other hand, the operating income for the bank increased by 14.15% from USD 5.35 billion to USD 6.11 billion.

Exhibit 6: Consolidated cost-efficiency ratio of the leading 8 Indian banks

Top Initiatives by Indian Banks

Axis Bank

Axis Bank has partnered with RBI Innovation Hub to launch two lending products powered by the Public Tech Platform for Frictionless Credit (PTPFC).

Kisan credit cards (KCC) for agricultural growth:

- The initiative will initially be launched in Madhya Pradesh, catering to the agricultural community in the region.

- Eligible customers can access KCC with a credit limit of up to USD 1920 (INR 160,000).

- The application process is entirely digital, eliminating the need for customers to provide physical documents.

Unsecured MSME loans for business growth:

- The bank is introducing unsecured lending on the PTPFC platform to bolster the growth of MSMEs.

- Unlike the region-specific KCC, these loans will be available throughout the country.

- Eligible applicants can secure loans of up to USD 12000 (INR 1 million), enabling business expansion.

ICICI Bank

ICICI Bank has launched ‘iFinance’, which enables retail and sole proprietor customers to get a consolidated view of their savings and current accounts across all banks in one place.

- Users can securely link and view all their bank accounts, including savings and current accounts, in one place for easy access.

- The facility offers a comprehensive overview of income and expenses, aiding users in effective financial monitoring.

- Users can monitor spending and access category-specific expenditure details, enhancing overall financial management.

- This service allows users to link or unlink accounts in real time, providing greater control and convenience.

- Users can download consolidated account statements for all their linked bank accounts, streamlining financial record-keeping.

State Bank of India (SBI)

SBI has launched a mobile handheld device for financial inclusion. The technology-driven initiative aims to empower financial inclusion and extend essential banking services to the masses. The Customer Service Point (CSP) agents can reach out to customers wherever they are.

The device will provide five core banking services in the initial phase, including cash withdrawals, cash deposits, fund transfers, balance enquiry and mini statements. These services account for 75% of transactions conducted at CSP outlets. There are plans to further expand service offerings, including account opening, card-based activities, enrolment under social security schemes and remittances.

Canara Bank

Canara Bank has become the first Indian bank to launch the UPI-interoperable Digital Rupee mobile app for Central Bank Digital Currency (CBDC) transactions.

- The Canara Digital Rupee app enables users to make seamless transactions by scanning merchant UPI QR codes and simplifying payments with digital currency.

- The app empowers merchants to accept digital currency payments through the existing UPI QR codes, eliminating the need for a separate onboarding process.

The approaching festive season is anticipated to drive increased consumer expenditures, thereby maintaining the demand for retail loans. Nevertheless, the banking regulatory authority has expressed apprehension over a significant surge in unsecured loans, primarily personal loans and credit cards. And although these loans pose higher risks, they significantly contribute to profit margins due to their associated higher interest rates.

To learn about how the top 3 Singapore banks performed in Q3 2023, click here.

To learn about how the top 5 Indonesian banks performed in Q3 2023, click here.

To learn about how the leading banks in the Philippines performed in Q3 2023, click here.

To learn about how the leading banks in South Korea performed in Q3 2023, click here.