Key highlights

Strong credit growth and improved asset quality remain key factors for India’s banking sector in Q4-2023.

- The leading 8 banks’ loan portfolio grew by 23.9% YoY (year-on-year) from USD 1.1 trillion in Q4-2022 to USD 1.3 trillion in Q4-2023.

- The growth is primarily driven by retail and service sectors.

- Demand for home loans and vehicle loans is leasing growth in the retail portfolio, supported by schemes like credit guarantee schemes and working capital loans for better-rate corporates, as well as gold loans.

- Better collection efficiencies and a pickup in the economy have improved asset quality.

- Decreasing interest margins due to rapid increases in benchmark interest rates.

- 250 basis points (bps) have increased in the repo rate since May 2022 and are currently at 6.5%.

- ICICI Bank has partnered with IIT Kanpur to bolster the startup ecosystems to empower startups in grasping foreign trade policies via workshops and seminars.

- IndusInd Bank collaborates with Indraprastha Gas Limited (IGL) to facilitate the acceptance of the digital rupee and the Central Bank Digital Currency (CBDC) by RBI.

- Canara Bank inaugurated its new Data and Analytics Centre (DnA) in Bengaluru, designed as a hub of excellence with modern facilities for innovation and collaboration.

Revenue highlights

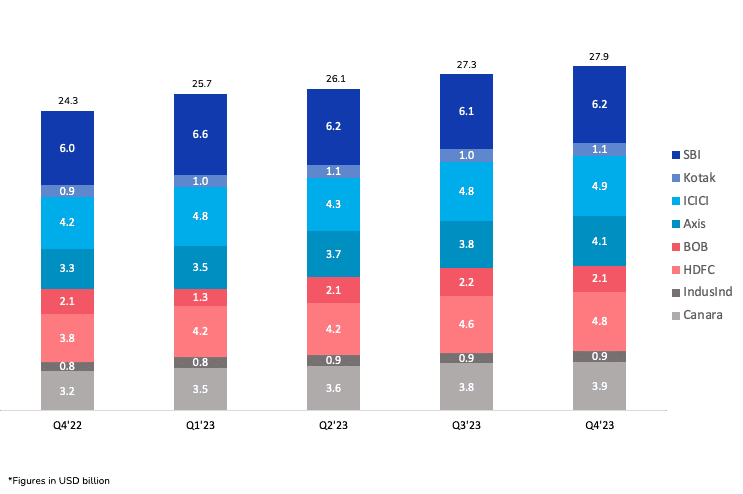

Net revenues for leading banks grew by 15% YoY to USD 27.9 billion in Dec 2023

Growth for the top 8 banks in India was primarily driven by an 11.2% increase in net interest income and an 11.9% increase in non-interest income.

HDFC Bank

- Highest net revenues at 25.8% from USD 3.8 billion to USD 4.8 billion in Q4-2023

- The highest increase in net interest income at 23.9% and non-interest income at 31.1%

Bank of Baroda

- Net revenues declined by 0.6% from USD 2.08 billion to USD 2.07 billion in Q4-2023

- Non-interest income declined by 8.6% from USD 0.7 billion in Q4-2022 to USD 0.61 billion in Q4-2022

Exhibit 1: Net revenues of the leading 8 Indian banks, Q4-2022 to Q4-2023

Profitability

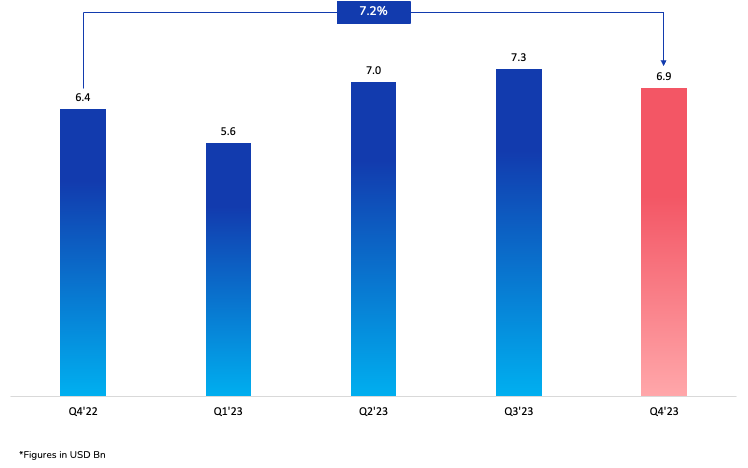

Net profit grew by 7.2% YoY in Q4-2023, to USD 6.9 billion

While both public and private sector banks reported similar growth in net revenues for the previous quarter, this was not the case in Q4-2023. In Q4-2023:

- Average net profit growth of public sector banks at 5.2%

- Average net profit growth of private sector banks at 17.6%

The combined profit of the 3 public sector banks declined by 15.9% to USD 2.1 billion in Q4-2023. In contrast, the combined profits of the 5 private banks rose by 22.6% from USD 3.9 billion to USD 4.7 billion in Q4-2023.

HDFC Bank

- Highest net profit growth at 33.5%, from USD 1.5 billion to USD 2 billion in Q4-2023, driven by strong loan growth of 62.3% in Q4-2023

- Net interest income increased by 23.9%, driven by loan growth

Exhibit 2: Consolidated net profits of the leading 8 Indian banks

Fee-based income

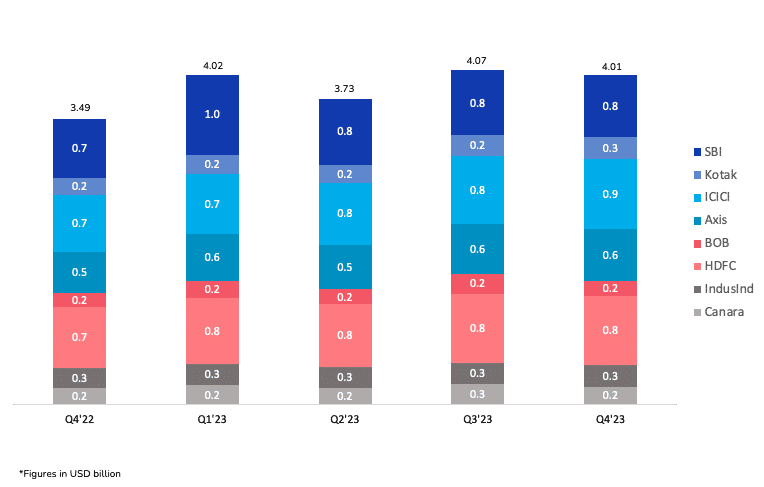

Fee incomes grew by 15.3% to USD 4 billion

All except IndusInd, Bank of Baroda and SBI reported double-digit growth in fee incomes. Kotak Mahindra Bank reported the highest increase at 26.5%, from USD 206 million to USD 260 million in Q4-2023, with fee and service income constituting 93% of the bank’s other income.

Exhibit 3: Fee incomes of the leading 8 Indian banks

Net interest margins (NIM)

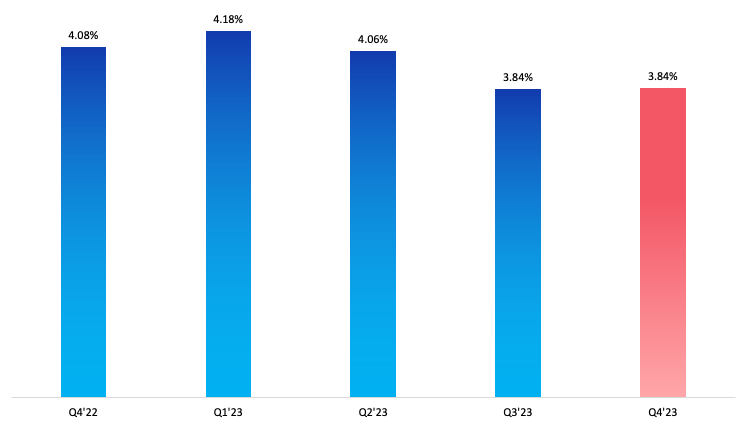

NIM declined by 24 bps

As approximately 80% of the loans are based on floating interest rates, banks experienced a significant increase in interest income when repo rates began to rise.

Regarding liabilities, most deposits are fixed, meaning higher interest rates only affect newly acquired and renewed deposits. However, peaking interest rates and the convergence of deposit rates caused a reduction in Indian banks’ high-interest margins in the previous quarters.

NIMs have remained constant over the previous quarter (Exhibit 4). All but IndusInd Bank witnessed a decline in NIMs from Q4-2022 to Q4-2023.

Regardless, Indian banks still have a higher NIM than other countries in APAC due to a credit surge, higher lending rates by the RBI, and the low cost of holding deposits.

Exhibit 4: Consolidated net interest margins of the leading 8 Indian banks

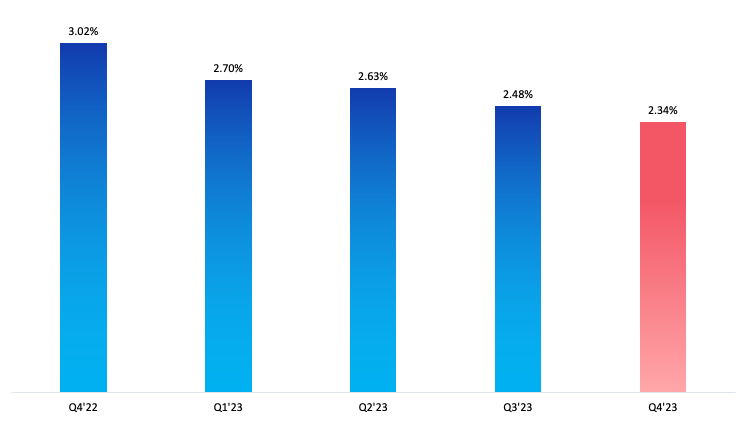

Non-performing assets (NPA)

NPA fell by 69 bps in Q4-2023

The average non-performing assets (NPA) of the leading 8 banks witnessed a 48 basis point decline, resulting in a current NPA of 2.3% (Exhibit 5). All but HDFC Bank reported a decrease in their NPAs. Of the leading 8, 3 are public sector banks.

- The 3 public banks recorded a decline in NPA by an average of 26.8%

- Private banks recorded a decline in NPA at an average of 13.9%.

Amongst the private sector banks, HDFC Bank recorded an increase in NPA from 1.2% in Q4 2022 to 1.26% in Q4-2023. Indian banks have been able to control their NPAs due to:

- Improved credit appraisal and monitoring to identify potential non-performing loans (NPL) early and apply corrective measures

- Stringent credit checks to assess applicants’ creditworthiness and risk of default

These initiatives help India avoid disbursing loans to applicants below the acceptable credit risk level.

Exhibit 5: Consolidated non-performing assets of the leading 8 Indian banks

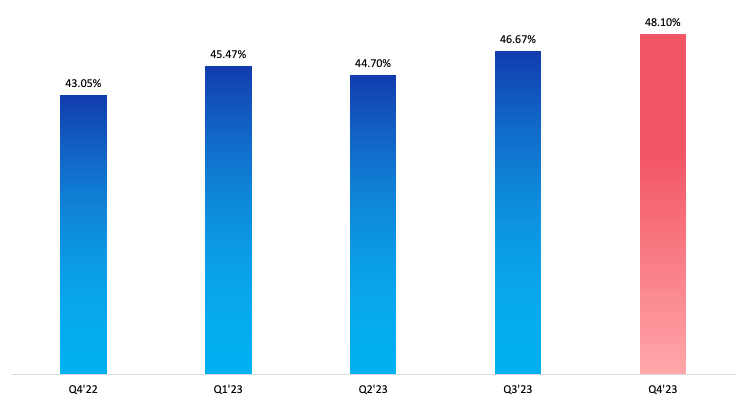

Cost efficiency (CE)

CE for Indian banks declined by 11.8% between Q4-2022 to Q4-2023

The average cost efficiency increased from 43% in Q4-2022 to 48.1% in Q4-2023 (Exhibit 6). Canara Bank and SBI have their cost efficiency above the threshold value of 50%.

SBI

The cost-efficiency ratio of SBI vastly increased from 49.1% in Q4-2022 to 60.3% in Q4-2023. This was due to:

- 27.2% increase in operating expenses from USD 3 billion to USD 3.8 billion in Q4-2023

- 31.2% increase in staff-related expenses and a 21.1% increase in the overhead. The increase in staff expenses is due to provisions on account of a one-time increase in pension liabilities at a uniform rate of 50% and Dearness Relief (DR) Neutralisation.

- The increase in staff expenses is due to provisions on account of a one-time increase in pension liabilities at a uniform rate of 50% and Dearness Relief (DR) Neutralisation.

On the other hand, the operating income for SBI increased by 3.5% from USD 6 billion to USD 6.2 billion.

Exhibit 6: Consolidated cost-efficiency ratio of the leading 8 Indian banks

Ket initiatives by Indian banks

- ICICI Bank

ICICI Bank signed a MoU with IIT Kanpur, to support the startup ecosystem.

- The partnership aims to empower startups and innovators at the Startup Incubation and Innovation Centre (SIIC).

- Focus on supporting incubates by improving their understanding of foreign trade policies through workshops and seminars.

- IIT Kanpur and ICICI Bank are committed to offering comprehensive support to early-stage ventures.

- IndusInd Bank

IndusInd Bank collaborates with Indraprastha Gas Limited (IGL) to facilitate the acceptance of the digital rupee and the Central Bank Digital Currency (CBDC) by RBI.

- Customer Access – Customers can pay digital rupees at select IGL stations in Delhi NCR, promoting the use and acceptance of India’s digital currency.

- UPI Interoperability – Customers can utilize UPI interoperability to scan any UPI QR using their Digital Rupee App across all IGL stations, enhancing convenience and accessibility.

- User-friendly Experience – The Digital Rupee solution is available on iOS and Android, ensuring a user-friendly experience. It has features like peer-to-peer (P2P) and peer-to-merchant (P2M) payments with full UPI QR interoperability.

- Canara Bank

Canara Bank inaugurated its new Data and Analytics Centre (DnA) in Bengaluru.

- The data centre is designed as a hub of excellence with modern facilities for innovation and collaboration.

- The inauguration marked a milestone as the bank entered partnerships for data lakehouse implementation and an Advanced Analytics Platform in the Cloud.

- This enabled various analytics initiatives focused on customer experience, business generation, and employee upskilling with AI/ML.

- Canara Bank organized the DACOETHON Hackathon, where finalists competed on themes like customer experience, fraud prevention, and default prediction.

Outlook for Q4 FY 2023-24

The expectation for banking credit is to expand within the 14-15% range for FY 2024-25. The Indian banking sector is poised for a positive 2024, with stable interest rates, a robust GDP, and decreasing inflation expected to drive lending and deposits. Investments in technology and infrastructure further support growth opportunities.

The sector’s resilient foundation – strengthened asset quality, robust capitalization, and sustained profitability positions the sector well to navigate uncertainties. With a keen focus on innovation, adaptive strategies and prudent risk management, the Indian banking sector strives for a future characterised by sustained progress and resilience.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for 8 banks.

- The three public sector banks talked about in the report are SBI, Bank of Baroda and Canara Bank, meanwhile, the five private sector banks are HDFC Bank, ICICI Bank, IndusInd Bank, Kotak Mahindra Bank and Axis Bank.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To know about how the leading 8 Indian banks fared compared to Q3-2023, click here.