Introduction: Key Highlights

- The Malaysian economy experienced a robust resurgence in the year 2022, marked by a remarkable GDP growth rate that reached a 22-year peak at 8.7%. This positive trend is expected to persist, with a projected CAGR of 4%-5% forecasted for the period from 2023 to 2027.

- The telecommunications market in Malaysia is characterized by its high competitiveness, with the top three telcos—Telekom Malaysia, Maxis, and CelcomDiGi—accounting for a substantial share (~90%) of the total revenue in 2022. The competitive landscape experienced a significant shift in 2022 due to the merger of Digi and Celcom, resulting in the combined entity (CelcomDiGi) securing the second position with a revenue market share of ~32%.

- Malaysian telcos are strategically concentrating their efforts on driving revenue through avenues such as fibre broadband deployment, 5G service offerings, digital initiatives, and targeted approaches towards the enterprise sector.

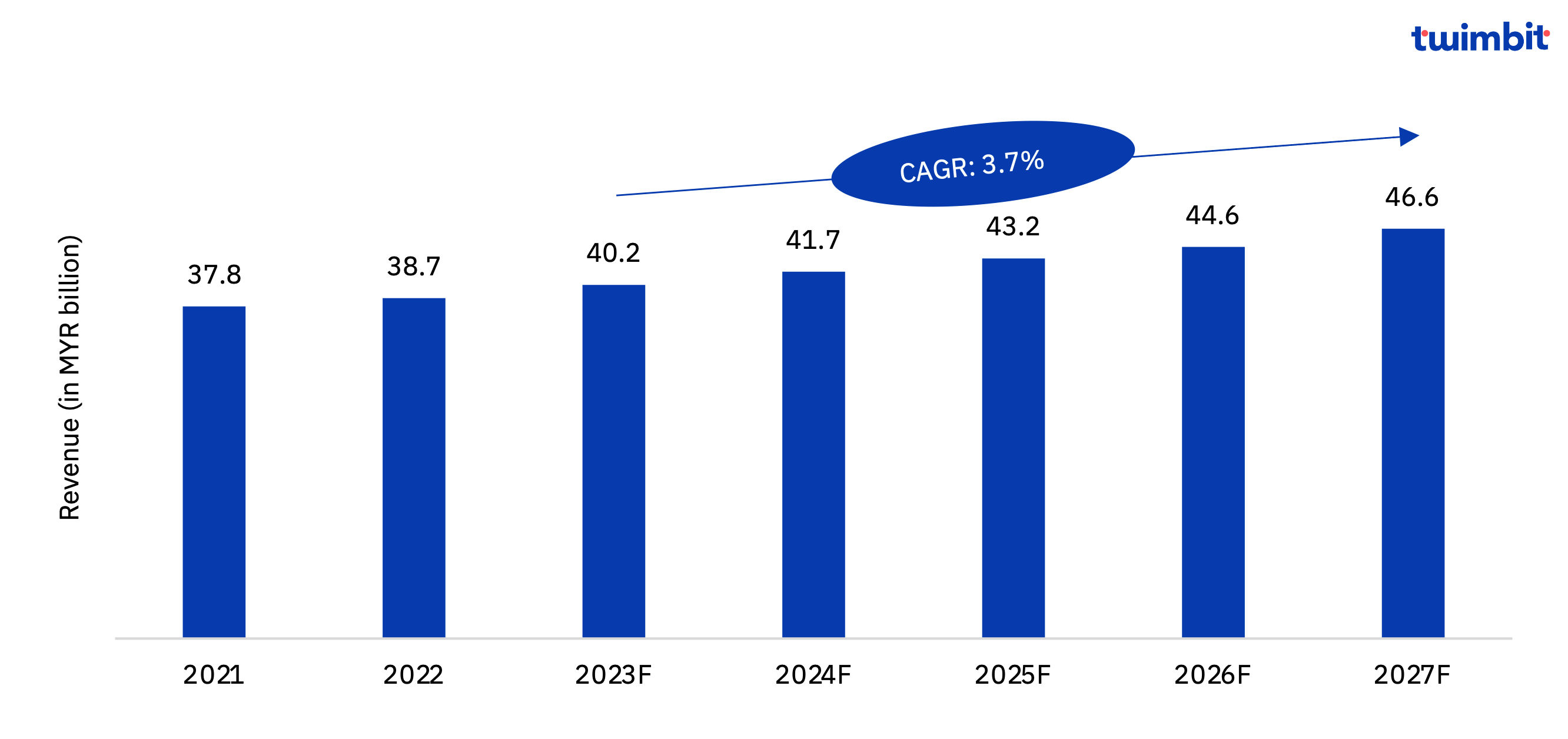

- The Government’s initiative to offer affordable telecom services will drive the overall market revenue. Malaysia’s overall telecom market revenue is estimated to grow at a CAGR of 3.7% between 2023-27, to reach ~USD 10.6 billion (MYR 46.6 billion) by 2027.

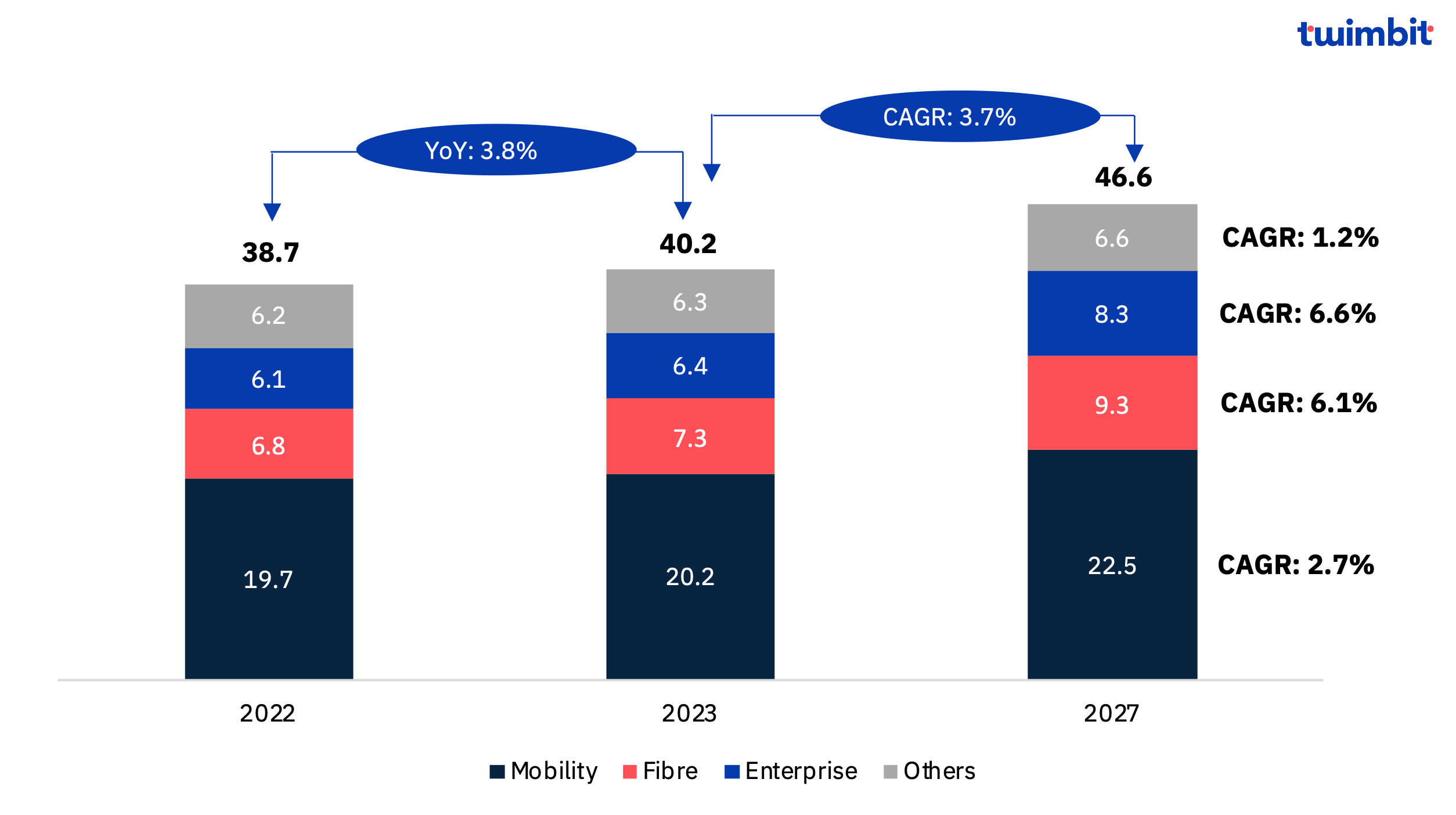

- The Malaysian telecommunications market is poised for significant expansion, primarily propelled by robust growth in the enterprise and fixed broadband segments. Telcos are enhancing their digital capacities in areas like AI, Cloud, and Cybersecurity to address the increasing demands of business digitalization. Projections indicate that the enterprise sector is anticipated to experience a CAGR of 6.6% from 2023 to 2027, while fixed broadband subscriptions are expected to surge by 8.2%, resulting in an overall revenue growth of 3.7% over the same period from 2023 to 2027.

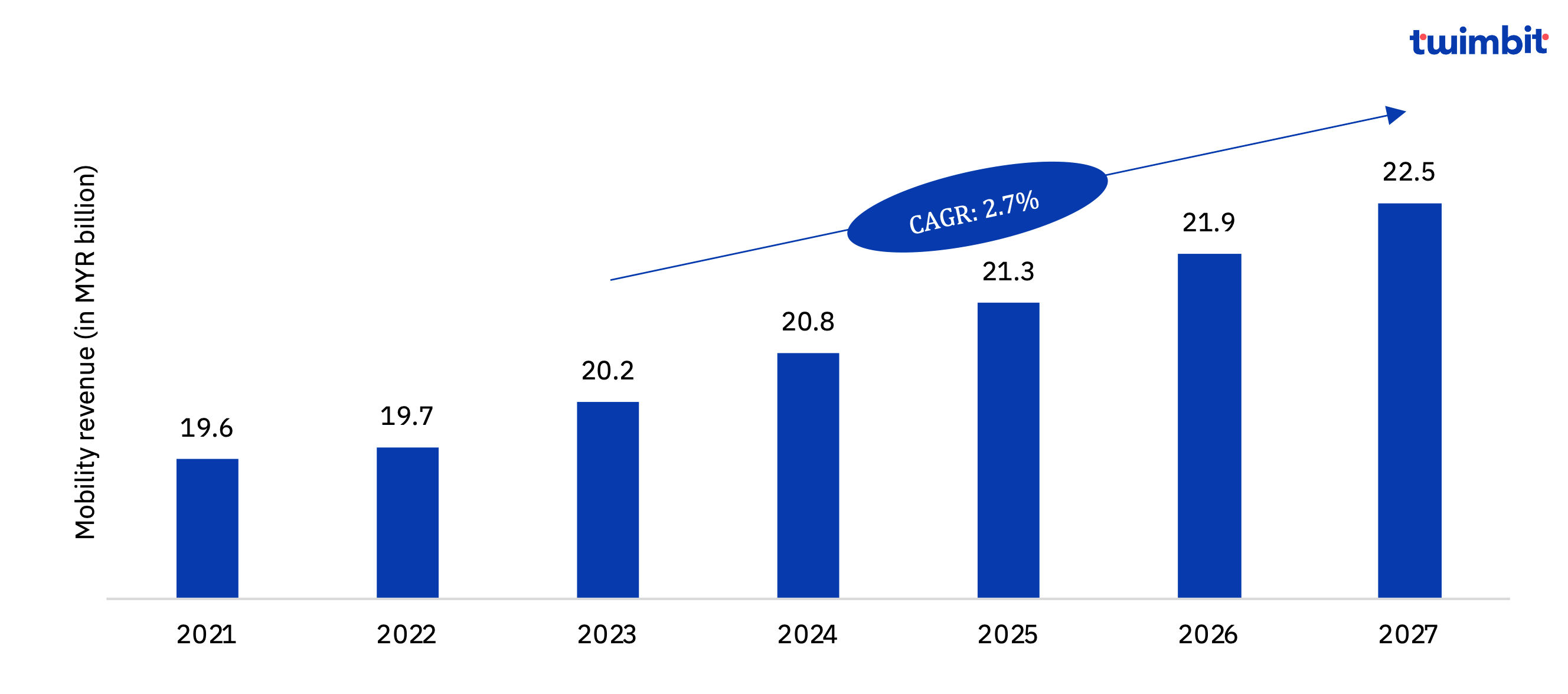

- However, the overall mobile segment revenue is estimated to witness a modest growth of ~2.7% over 2023-27 to reach ~USD 5.1 billion (MYR 22.5 billion) by 2027, owing to stagnancy in ARPU level existing due to high competition level.

- The Blended ARPU for telcos has experienced a decline, and this trend is likely to persist due to the launch of the “Unity Package” by the Malaysian Government, aimed at providing affordable internet access. While this might lead to a mild dilution of ARPU in the midterm, stability in ARPU is anticipated over the longer term.

- Total mobile subscribers in Malaysia are estimated to grow to 53.4 million in 2027 with a CAGR~1.6% (2023-2027), while fixed broadband subscribers will grow with a CAGR of ~8.2% (2023-2027) to reach 6.4 million by 2027.

- Telcos in Malaysia are promoting their 5G services to increase the adoption. Additionally, the Malaysian Government intends to divest its stake in Digital National Berhad (DNB) once certain network rollout targets are achieved and plans to implement a second 5G wholesale network rollout. As a result, 5G subscription penetration to the overall mobile broadband subscriptions is predicted to surge from 0.8% in 2021 to ~22.6% by 2027 to reach 12 million subscribers in 2027.

- Aligned with the Government’s JENDELA initiatives, telcos are consistently expanding their network infrastructure to deliver improved broadband services, particularly in underserved regions. Telekom Malaysia has consistently recorded the highest Capital Expenditure (Capex) since 2019, followed by Maxis and Celcom.

- The Malaysian telecommunications market is currently undergoing a phase of digital inclusion, which is likely to intensify driven by increased adoptions of high-speed mobile internet plans synchronous with increase in 5G adoption, enhancing customer experiences through digital technology utilisation, and boosting revenue through convergent offerings.

Macroeconomic Overview

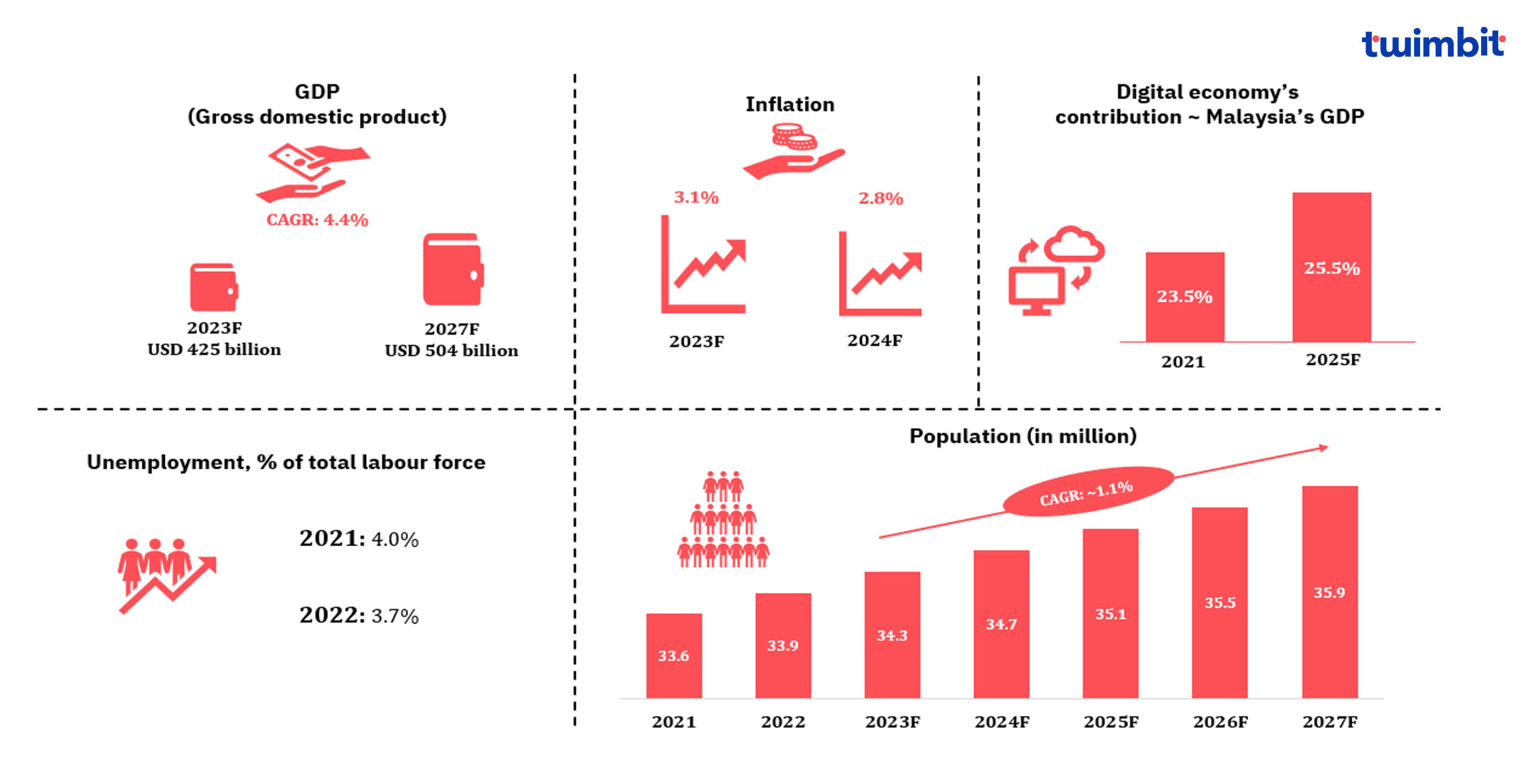

In 2022, the Malaysian economy experienced a robust resurgence, rebounding from the pandemic-induced downturn. The GDP growth rate reached an impressive 8.7%, the highest in 22 years. This resurgence was propelled by the reopening of economic activities and a resilient export performance, which grew by 21.3% (YoY) to reach ~USD 51.4 billion (MYR 231.4 billion). As a result, domestic demand rebounded significantly, driven by the normalization of market conditions and improved labour market indicators.

For the year 2023, the economy is projected to achieve a growth rate of ~4.6%. Nevertheless, this growth trajectory is expected to come with challenges, primarily stemming from an escalation in the cost of living. This could result in elevated inflation levels, potentially impacting the purchasing power of both consumers and businesses. The GDP is forecasted to maintain a CAGR of ~4.4% from 2023-27, ultimately reaching a value of ~USD 504 billion by 2027.

The global economic slowdown may contribute to a moderation in inflation rates. The prevailing inflation rate of 4% in 2022 is expected to decrease in 2023 and 2024, reaching 3.1% and 2.8%, respectively.

Despite the existing potential challenges, investment prospects remain promising, especially in the context of sustained digitalization efforts and governmental reforms aimed at enhancing the business environment.

Exhibit 1: Malaysia macro-economic indicators

The digital economy stands as one of the fastest growing sectors in Malaysia. In 2021, Malaysia Digital Economy Blueprint and Digital Investment Office were established, aimed at streamlining investments in the digital sphere. The objective is to attract a substantial USD 16.1 billion in digital investments by 2025, contributing ~25.5% to the GDP, as against to the 23.5% contribution observed in 2021.

Malaysia’s industrial landscape has undergone a transformative shift, with a noteworthy pivot toward electronics and integrated circuit manufacturing. This sector is poised to become a critical driver of the country’s economic growth. In 2022, electrical and electronics products accounted for a substantial 38% of total merchandise exports, marking a significant year-on-year increase of 30%.

Industry Snapshot

A. Telecom Market Size and Growth

The Malaysian telecommunications market has exhibited a consistent growth pattern and subsequent stabilization of ARPU levels across the sector.

In response to these trends, telcos are strategically positioned to enhance their revenue streams through a slew of measures such as expansion of fibre broadband networks, harnessing the potential of 5G technology to bolster data-driven revenues, promoting a diverse array of digital offerings, and judiciously directing efforts towards the enterprise sector.

Exhibit 2: Telecom revenue forecast in Malaysia, 2021-27F

Source: Telco financials, Twimbit analysis

Driven by these factors, the overall telecommunications market is anticipated to undergo a modest growth trajectory, with a CAGR growth of 3.7% over 2023-27 eventually reaching approximately USD 10.6 billion (MYR 46.6 billion) by 2027.

Exhibit 3: Revenue of key segments, 2022 and 2027F

Source: Telco financials, Twimbit analysis

The Malaysian telecommunication market will be driven by higher growth in the enterprise and fixed broadband market. Malaysian telcos are actively working enhancing their digital capabilities in fields like AI, Cloud, and cybersecurity to meet the digitalization needs of businesses. Consequently, the enterprise segment is expected to achieve a relatively higher growth rate with CAGR ~6.6% from 2023-27.

The overall fixed broadband subscription is estimated to grow at a CAGR of 8.2% over 2023-27, resulting in overall fixed broad broadband revenue to grow at a CAGR of 6.1% during the same period. This growth can be attributed to the telecommunications companies’ efforts to expand and bolster their networks as part of the JENDELA initiative, which has further driven the growth of fixed broadband (fiber) subscriptions. Additionally, the government’s focus on reducing retail fixed broadband pricing plans has contributed to this positive trend.

However, over the period 2023-27, overall mobility revenue will grow with a CAGR ~2.7% and will remain the largest revenue contributor for Malaysian telecommunication companies and the Blended ARPU is expected to stabilize, with the increasing adoption of 5G.

B. Competitive Landscape

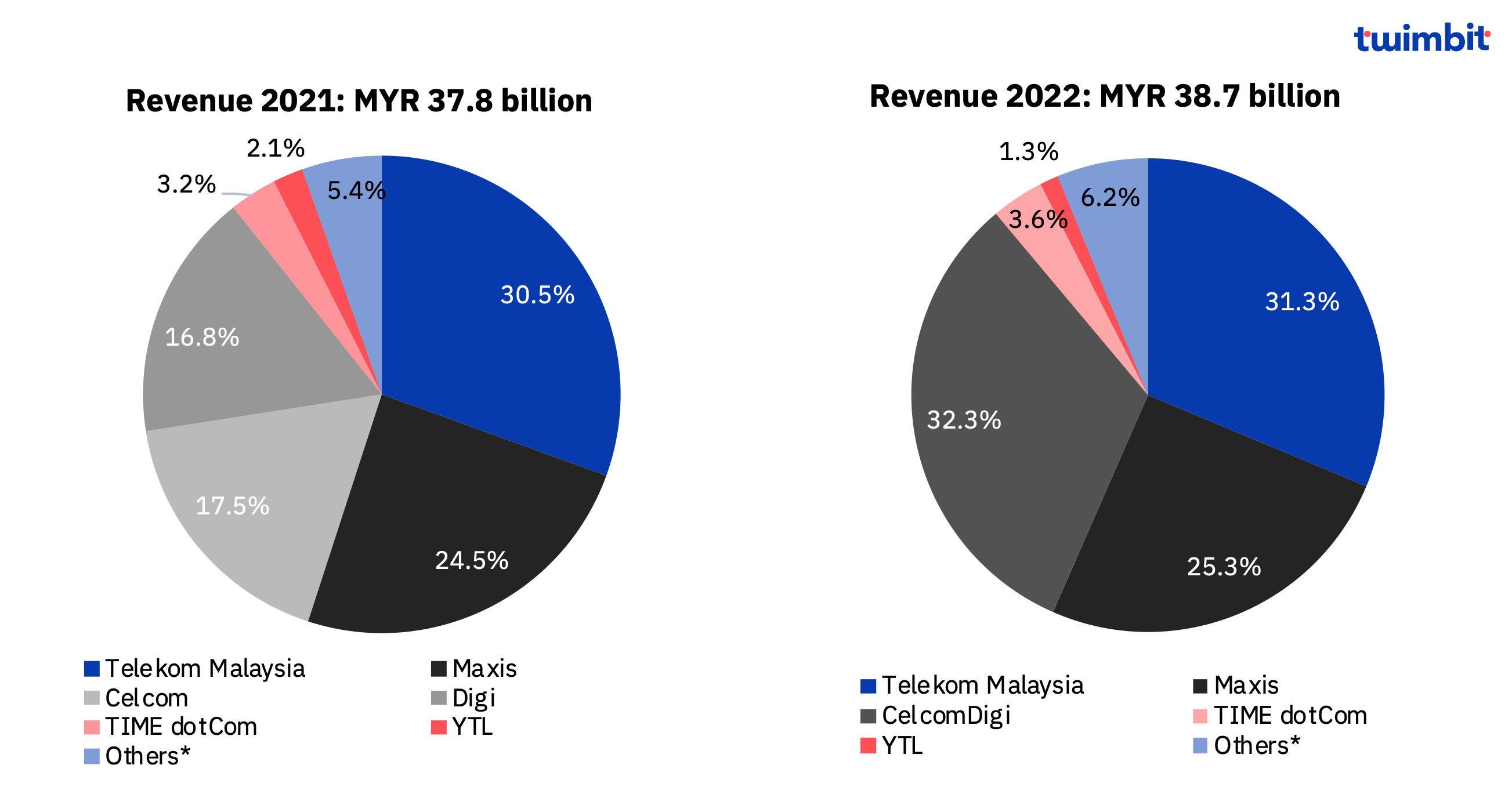

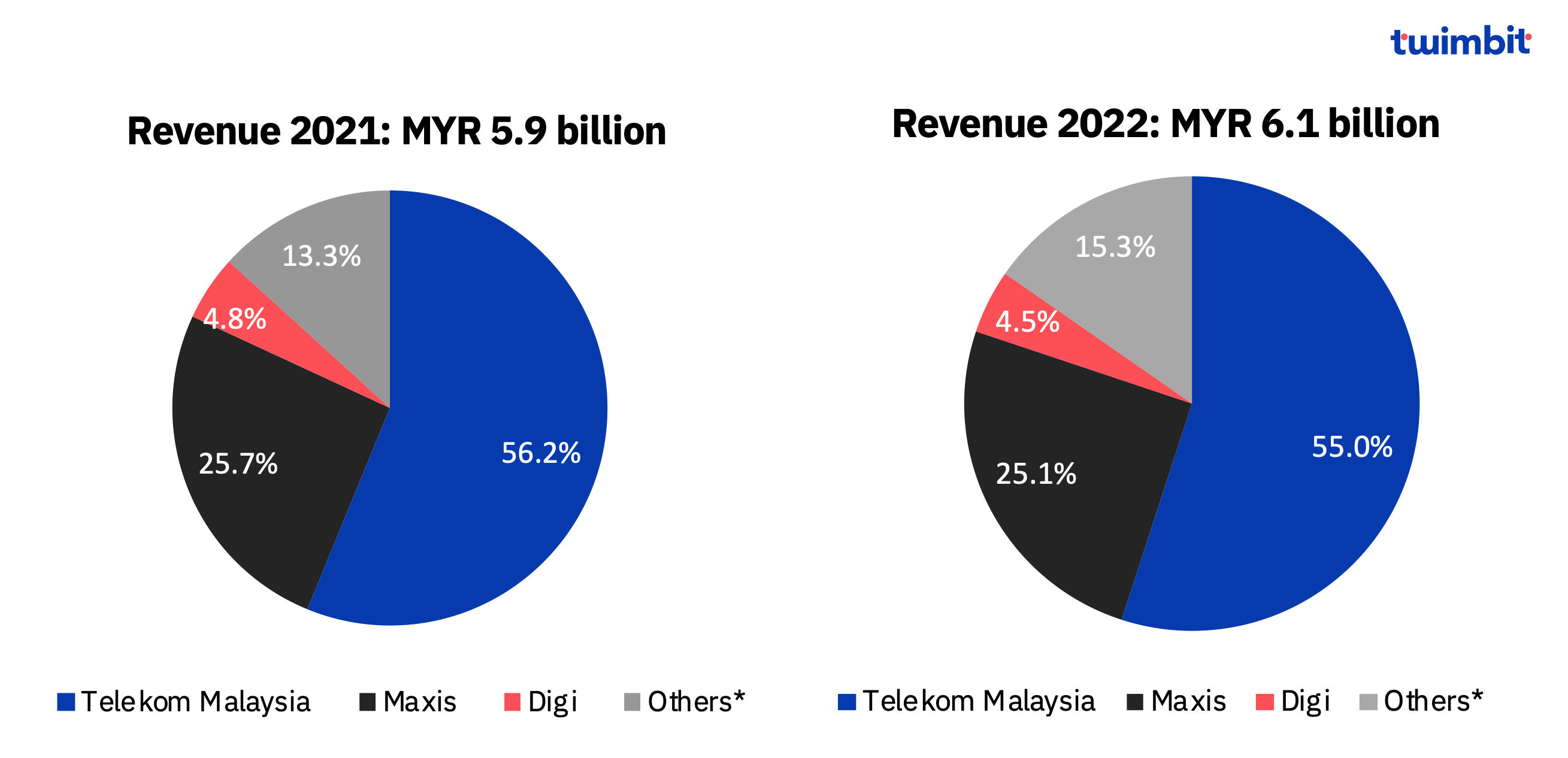

The telecom market landscape witnessed a dynamic shift post the establishment of CelcomDigi in December 2022, formed by merger of Celcom and Digi. The third (Celcom) and fourth largest ranked telco (Digi) in 2021, merged to emerge as the market leader in terms of revenue share in 2022, displacing Telekom Malaysia. This strategic amalgamation facilitated CelcomDigi in achieving a notable revenue market share of ~32% among all telcos in the year 2022.

Exhibit 4: Revenue market share of leading telcos, 2021 and 2022

Note: CelcomDigi was formed as a result of the merger between Celcom and Digi on 1st Dec 2022

*Includes other providers like U Mobile, Sacofa, Allo Technology, Macro Lynx etc.

Source: Telco financials, Twimbit analysis

In 2022, the top three telcos collectively held approximately 90% of the revenue share. Other notable players in the telecom services sector included U Mobile, YTL, and TIME dotCom. Over the period 2019-22, Telekom Malaysia managed to maintain its revenue share, while Maxis and TIME dotCom saw slight increases in their respective revenue shares.

The state-owned incumbent Telekom Malaysia accounted for the largest revenue share until 2021. In 2021, Telekom Malaysia accounted for the largest revenue share (~31%) followed by Maxis (~25%), Celcom (17.5%) and Digi (16.8%) in 2021.

Mobility market in Malaysia

A. Mobility revenue forecast, 2021-2027F

With an increasing penetration of mobile subscriptions, owing to aggressive 5G promotion by telcos, the overall mobility revenue is estimated to witness a modest growth of ~2.7% over 2023-27 to reach ~USD 5.1 billion (MYR 22.5 billion) by 2027. Telcos are expected to compete aggressively in pricing their services and concentrate on acquiring new customers. In conjunction with these factors and the government’s efforts to provide affordable packages, the ARPU is anticipated to maintain a stable downward trend until 2027.

Within the framework of the 12th Malaysia Plan (2021-2025), the Malaysian Government launched the JENDELA action plan, with an estimated value of around USD 5.1 billion (MYR 21 billion). This strategic endeavor is designed to enhance digital connectivity through the optimization of infrastructure efficiency and the maximization of spectrum utilization. The JENDELA plan unfolds in two distinct phases: Phase 1 (2020-22) entailed the discontinuation of 3G networks by December 2021 in favor of prioritizing 5G technology for digital transformation, while Phase 2 extends from 2022 to 2025.

Exhibit 5: Mobile revenue forecast, 2021-27F

B. Mobility subscription forecast, 2021-2027F

Telcos are predominantly offering 5G services either free of charge or as part of bundled packages with 4G plans, available in areas with 5G network coverage. Celcom and Telekom Malaysia’s Unifi mobile have promoted the complimentary 5G upgrade as a limited time offer, while Digi provides 5G as an option for its prepaid subscribers as booster options.

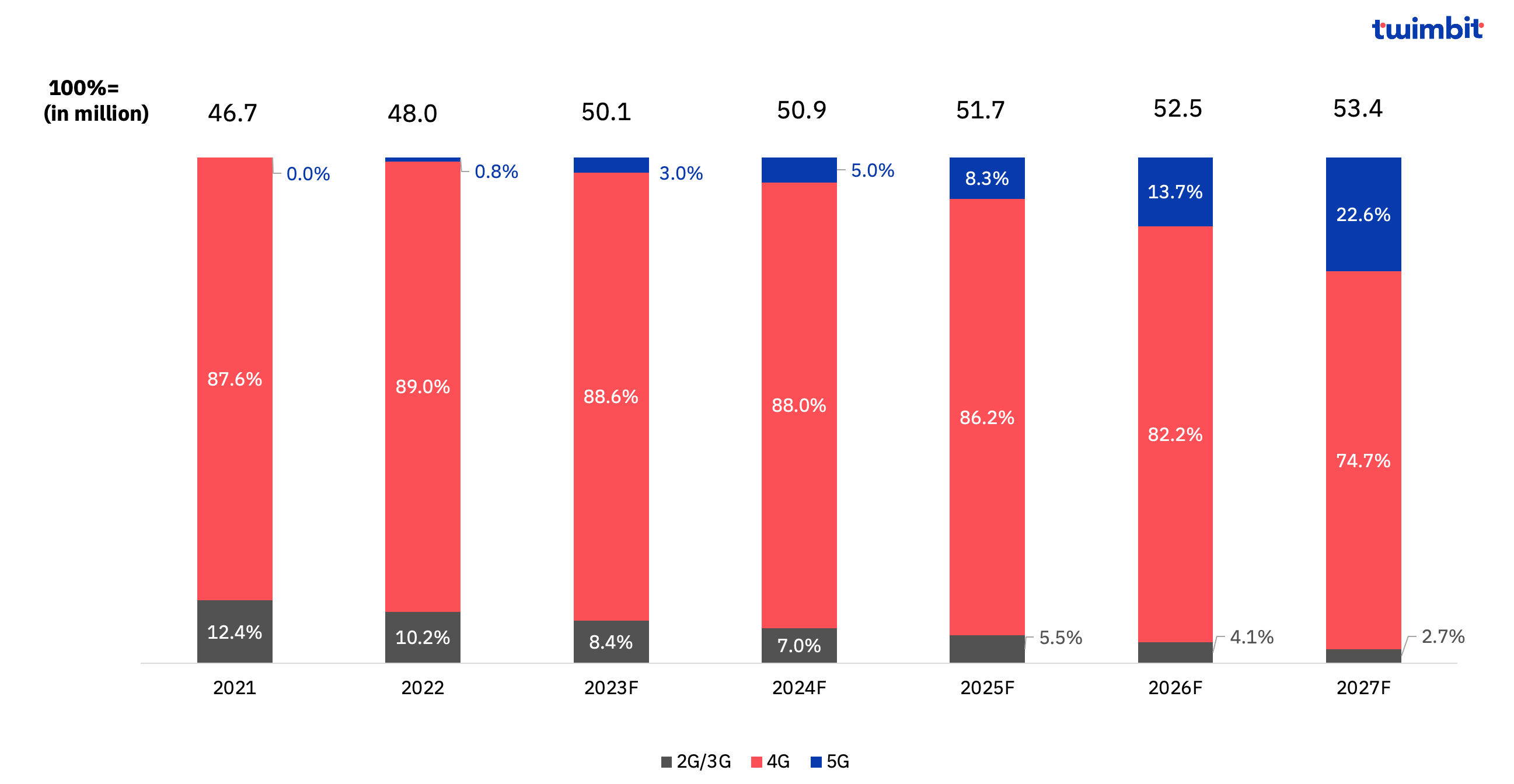

Under the influence of the JENDELA plan, which oversaw the gradual phase-out of 3G networks by the end of 2021, there was a notable increase in 4G subscriptions. In 2021, 4G subscriptions made up 87.6% of total mobile subscriptions, marking a significant rise from 82.9% in 2020. This shift was further accelerated by telcos launching aggressive 5G promotional campaigns to expand their subscriber base, with government support playing a role. As a result, 5G adoption is expected to gather momentum. Considering these developments, the projected trend indicates a substantial increase in 5G adoption, growing from approximately 3% of total subscribers to approximately 23% by 2027, equivalent to around 12 million subscribers.

Exhibit 6: Mobile subscription forecast by technology generation, 2021-27F

While the MCMC claims to have surpassed the initial targets set by the first phase of the JENDELA program, 5G adoption remains relatively low, with only 0.4 million 5G subscribers by the end of 2022. The JENDELA program aimed for population coverage of 40% by 2022, 70% by 2023, and 80% by 2024. As of August 2023, DNB asserted it had achieved 68.8% coverage in populated areas of Malaysia with its 5G network.

From 2023 to 2027, the adoption of 5G technology is poised to emerge as a new growth avenue for telecommunications companies, potentially addressing last-mile connectivity challenges by offering 5G as a fixed wireless access alternative for users. Additionally, the advent of 5G is expected to open revenue-generating opportunities for telcos in enterprise segments and industrial applications.

In the consumer market, telcos may encounter challenges in charging premium prices for 5G services due to intense competition and a less enthusiastic response to 5G adoption until 2022.

C. Prepaid vs. Postpaid subscription trend, 2019-22

In comparison to the other ASEAN countries, postpaid subscriptions still constitute a substantial portion of the total subscriptions in Malaysia.

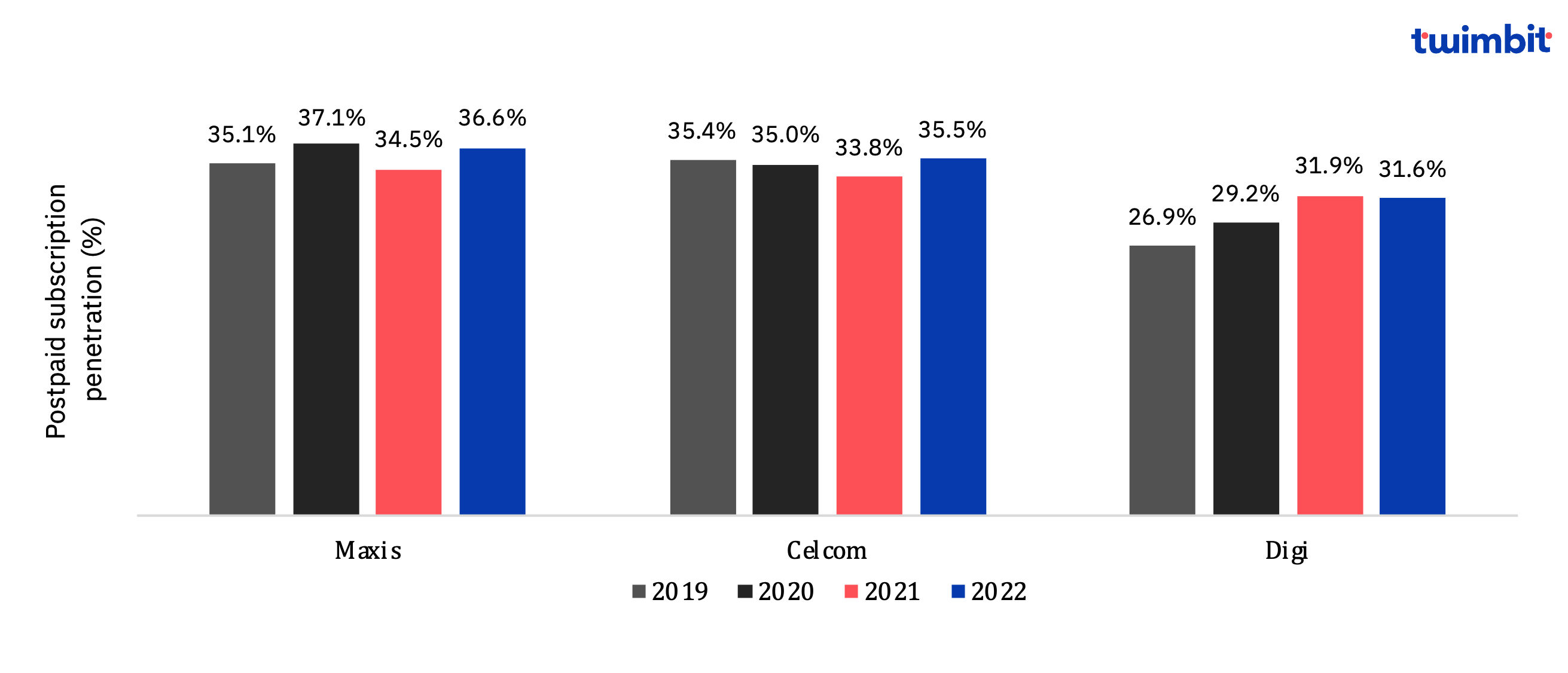

The proportion of postpaid subscriptions has remained steady at approximately 30% over the past four years. For all the major operators, postpaid subscriptions have increased marginally over the period 2019-22, owing to increased data allowance being offered.

Exhibit 8: Postpaid subscription penetration for leading players (%), 2019-22

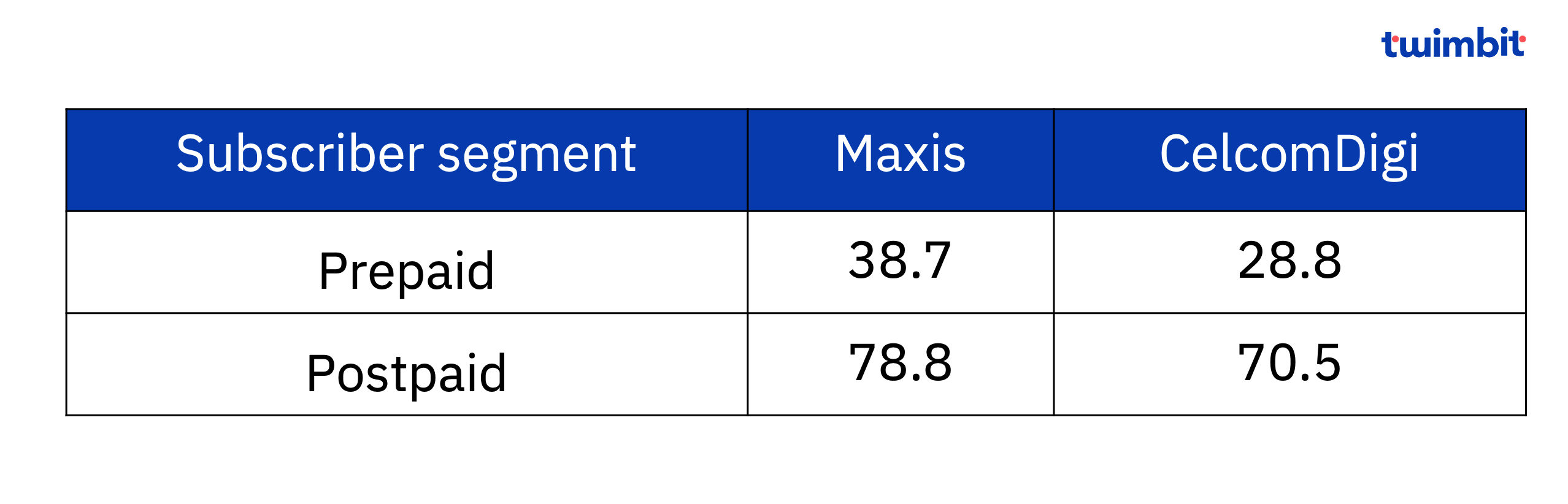

In the year 2022, Maxis held the highest proportion of postpaid subscribers within the overall subscriber base, followed by Celcom and Digi. However, the combined entity CelcomDiGi emerged as the leader in prepaid subscriptions. In 2022, CelcomDiGi accounted for a substantial 13.3 million prepaid subscribers, constituting a notable 66.6% of its total mobile subscription count.

D. ARPU trends for key telcos, 2019-22

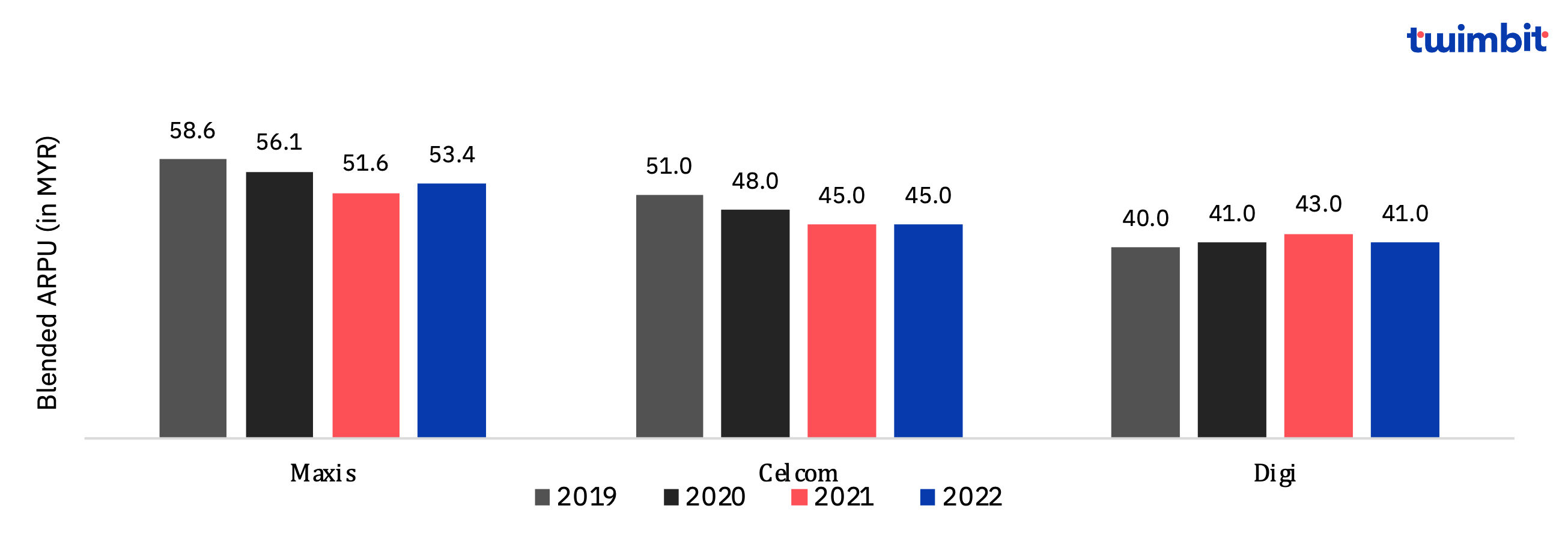

Amidst the intens competition, the blended ARPU has declined over the last four years. Maxis continue to have a relatively higher blended ARPU, due to premium pricing, and higher penetration of postpaid customer base.

In December 2022, the Malaysian Government, introduced the “Unity Package” to offer affordable internet access for lower-income individuals. CelcomDiGi, Maxis, U Mobile, Telekom Malaysia, and YTL joined an initiative offering a prepaid mobile plan at about USD 6.8 (MYR 30) for 6 months. This plan is more affordable than current options, providing 2X validity and 3X the speed. While it may draw cost-conscious and low-data users, it could have impact on the ARPU in the prepaid segment.

Exhibit 9: Blended ARPU for leading telcos, 2019-22

In 2022, Maxis experienced a rise in its blended ARPU, primarily due to the growth of its prepaid segment. The telco has launched personalized HotlinkMU promotions, leading to an improvement in its prepaid ARPU. Maxis’ Hotlink also introduced a new prepaid plan featuring enhanced internet passes, offering prepaid customers a wider range of options and greater flexibility to meet their needs.

Exhibit 10: Prepaid and Post-paid ARPU of leading telcos, 2022

Source: Telco financials, Twimbit analysis

Fixed Broadband market in Malaysia

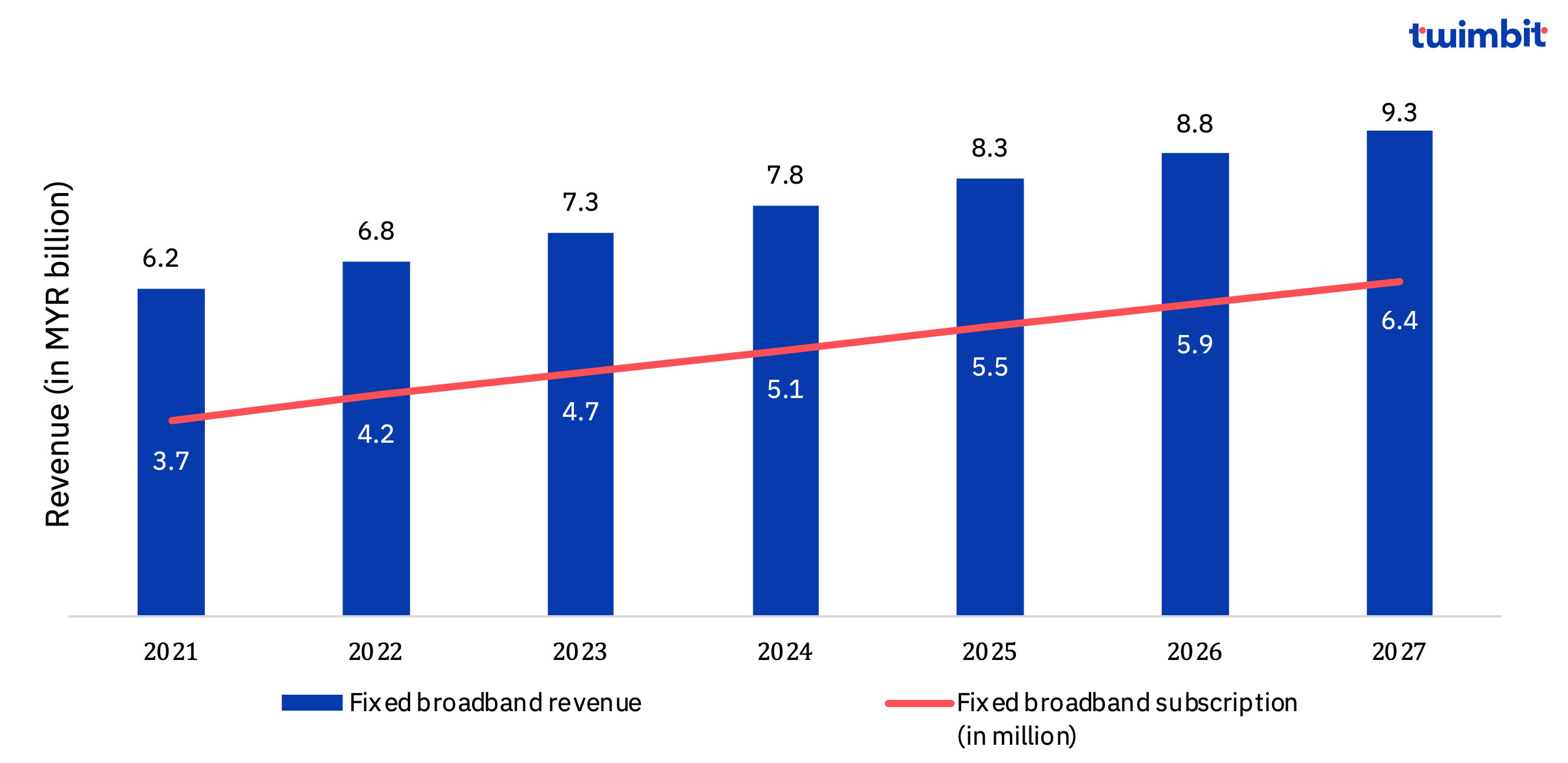

A. Fixed broadband revenue and subscription forecast, 2021-2027F

Source: MCMC, Telco financials, Twimbit analysis

The initiatives by telcos to expand and build network as a part of JENDELA initiative resulted in the fixed broadband subscription growth. As a result, the fixed broadband subscription is estimated to grow at a CAGR of 8.2% over 2023-27. This would account for a population penetration of ~18% by 2027 as compared to ~12% in 2022.

Exhibit 11: Fixed broadband revenue and subscription forecast, 2021-27F

The fixed broadband adoption is likely to grow as the government intends to reduce the fixed broadband price plans. The adoption growth is likely to stabilize over the next few years and negating the marginal decline in the ARPU. The fixed broadband subscriber is estimated to grow with a CAGR ~8.2% over 2023-27 to reach 6.4 million, which will drive the growth in fixed broadband revenue with a CAGR ~6.1% over 2023-27 to reach ~USD 2.1 billion (MYR 9.3 billion) by 2027.

B. Competitive Landscape

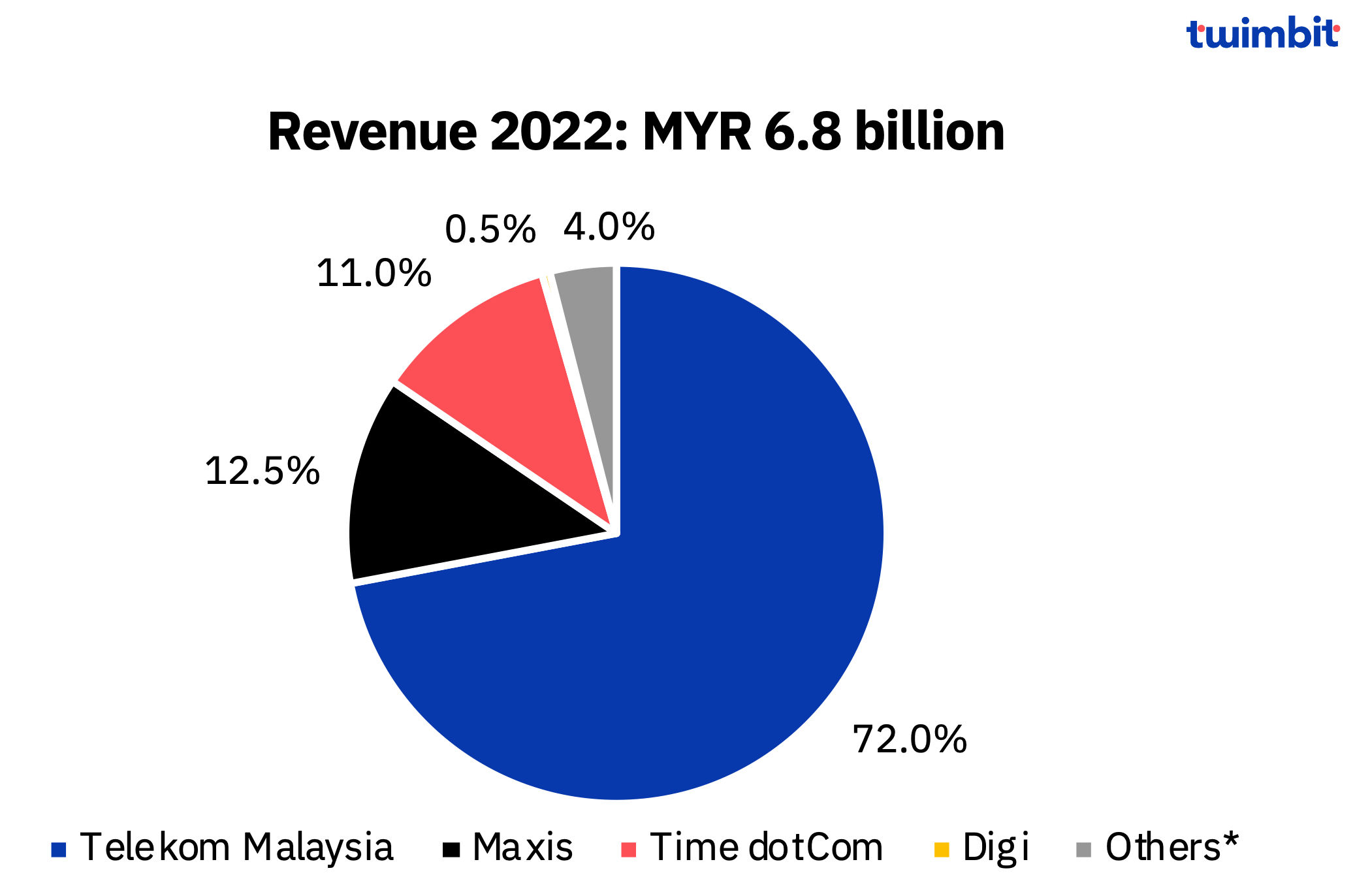

Malaysia’s fixed broadband market is primarily a duopoly with the leading two telcos – Telekom Malaysia and Maxis accounting for majority (~88%) of the revenue and subscriber market share. Other prominent players include CelcomDiGi, U Mobile and TIME dotCom.

Telecom Malaysia accounted for 72% of the fixed broadband revenue in 2022. During the period 2021-22, its revenue increased by 7.2% driven by growth in its overall fixed broadband subscriber count. The strong growth in the fixed broadband subscribers in its Unifi (fibre based broadband offering) and Streamyx (copped based broadband service) segments, negated the comparative marginal decline in ARPU, thereby resulting in higher revenue for Telekom Malaysia.

Exhibit 12: Fixed broadband revenue share of leading telcos, 2022

* Includes other providers like U Mobile, Sacofa, Allo Technology, Macro Lynx etc.

** Includes other providers like Time dotcom, U Mobile, Sacofa, Allo Technology, Macro Lynx etc.

Source: MCMC, Telco financials, Twimbit analysis

In 2022, Telekom Malaysia had over 3.0 million fixed broadband subscribers, with a significant increase in Unifi fiber broadband users, surpassing 2.9 million. However, Streamyx (Unifi Lite) subscribers declined to 75,000 in 2022 from 750,000 in 2019. Telekom Malaysia plans to transition all Streamyx subscribers to fiber broadband by 2025. However, Maxis saw a 13.2% growth in consumer home connectivity connections in 2022, reaching approximately 0.7 million, with stable ARPU at around USD 24.8 (MYR 109). This growth was due to bundled offerings providing unlimited internet to mobile and fiber service subscribers.

To gain market share, telcos are introducing various broadband plans, while the government aims to reduce fixed broadband prices. A lower-priced ‘Pakej Perpaduan’ plan was launched in February 2023, offering 30Mbps downlink speeds for ~USD 15 (MYR 69) per month. The Mandatory Standard on Access Pricing (MSAP) came into effect in March 2023, with further price reductions contingent on access agreements between service providers.

Enterprise market in Malaysia

A. Enterprise revenue forecast, 2021-2027F

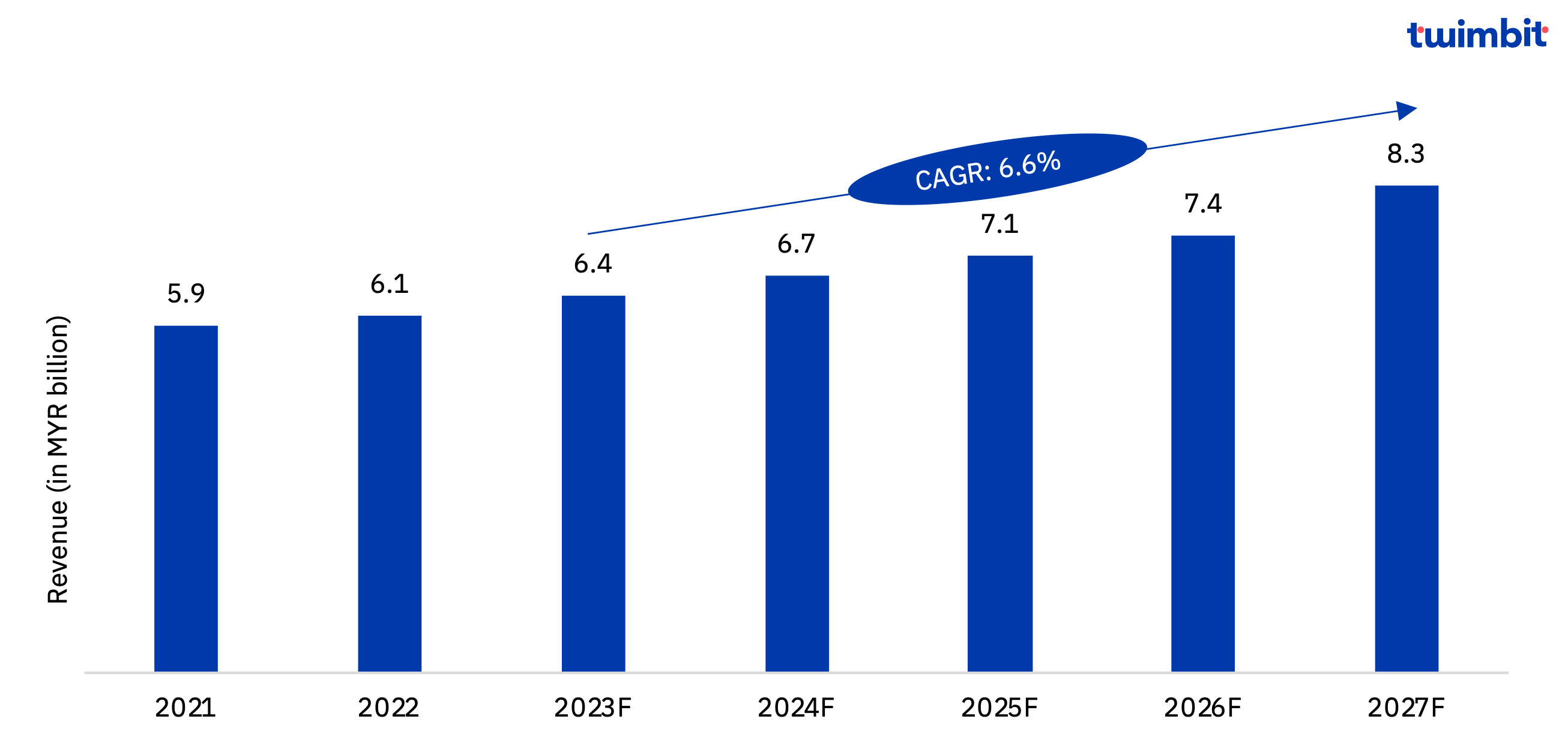

Driven by the focus to strengthen digital capabilities and catering to the enterprise requirements, coupled with the further intensification of the 5G adoption, the enterprise services revenue is estimated to grow at a CAGR of 6.6% over 2023-27 to reach ~USD 1.9 billion (MYR 8.3 billion), accounting for ~18% of the total revenue by 2027.

Exhibit 13: Telco’s enterprise services revenue forecast, 2021-27F

B. Competitive landscape

The enterprise segment in the telecommunications industry exhibits a high degree of consolidation, characterized by the dominance of a few key players. Leading telecommunication companies have managed to secure a significant market share despite the fierce competition and are consistently pursuing innovative strategies to enhance revenue in the enterprise sector.

The enterprise revenue segment was estimated to be ~USD 1.4 billion (MYR 6.1 billion) in 2022. Telekom Malaysia and Maxis exert dominant influence, collectively contributing to ~80% of the overall revenue share.

Exhibit 14: Enterprise revenue market share of leading telcos, 2021-22

Source: Telco financials, Twimbit analysis

Telecom companies are adapting to meet diverse enterprise demands. For instance, in July 2022, Telekom Malaysia introduced “Credence,” a company specializing in cloud and digital services, serving over 6,000 enterprises and 2,800 government clients. In contrast, Maxis is investing in technology to enhance cyber resilience, focusing on data protection, cloud, APIs, IoT, and 5G. They’ve opened the Maxis Business Innovation Centre and supported 25,000 SMEs in their digital transformation.

In April 2023, CelcomDigi launched CelcomDigi Business to provide digital solutions, including Cloud and Cybersecurity. They also partnered with South Korea’s SK Telecom to develop Malaysia’s first mobile metaverse platform.

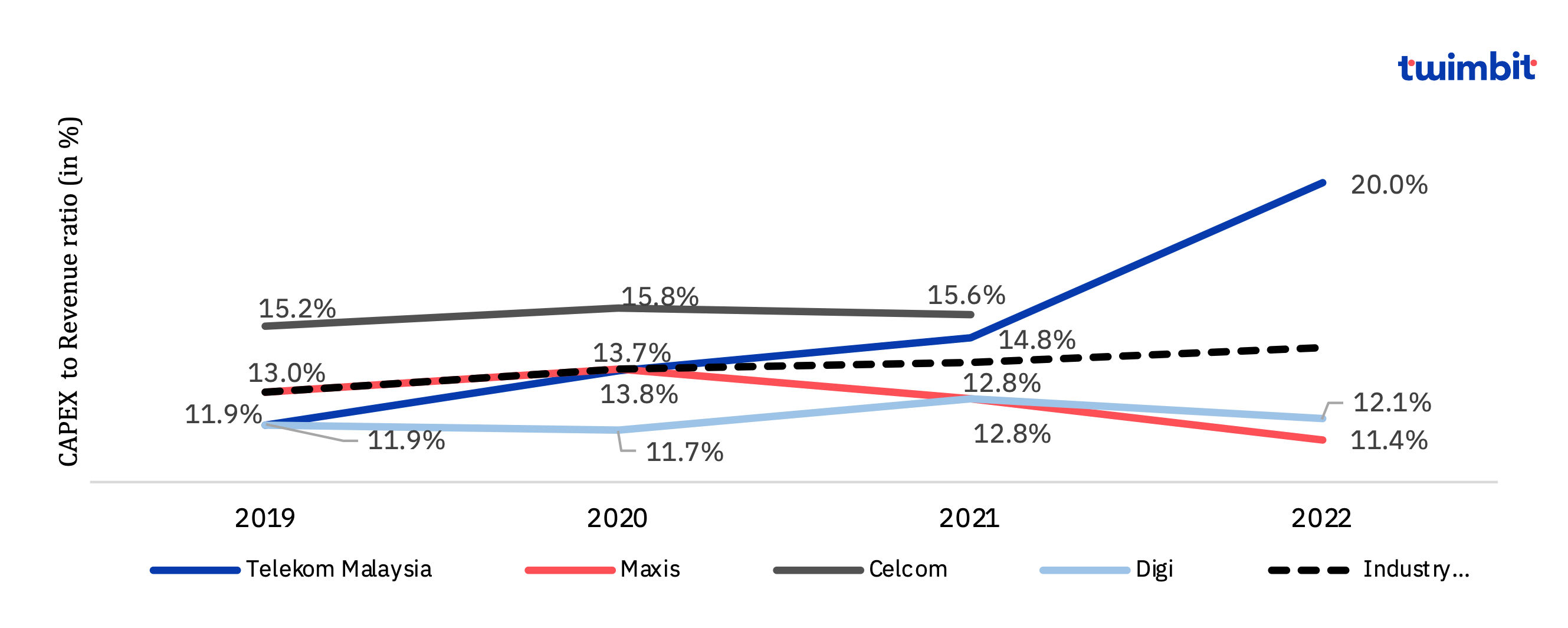

Capital Expenditure and Network Infrastructure Upgrades

In line with the Government’s JENDELA initiatives, telcos continue to expand their network infrastructure, with a view to offer enhanced quality broadband service especially in the underserved geographies to narrow the digital divide and promote inclusive socio-economic development.

Telekom Malaysia continues to have the highest CAPEX since 2019 followed by Maxis and Celcom. Telekom Malaysia’s CAPEX increased by 42.8% over 2021-22 to reach ~USD 0.5 billion (MYR 2.4 billion). This was telco’s highest CAPEX spending since 2017, keeping in mind the pace of transformation and meeting the market demand and majority of the spending was on fibre network provisioning, with some portion being spent on 5G. It extended its reach to 500,000+ households and premises in 2022, along with augmentation of network infrastructure to accommodate the burgeoning customer demand, including deployment of 7,000+ 4G/5G backhaul sites and integration of 2,600 5G sites into the core network.

Exhibit 15: Telcos CAPEX intensity trend, 2019-22

2022 Capex data for Celcom has been calculated using CelcomDigi and Digi reported numbers

Source: Telco financials, Twimbit analysis

Aligned with the strategic roadmap outlined by the JENDELA initiative, Maxis undertook significant infrastructure enhancements in 2022, including establishment of 157 new sites, upgradation of 1,847 mobile sites, and extending its reach to over 7 million premises.

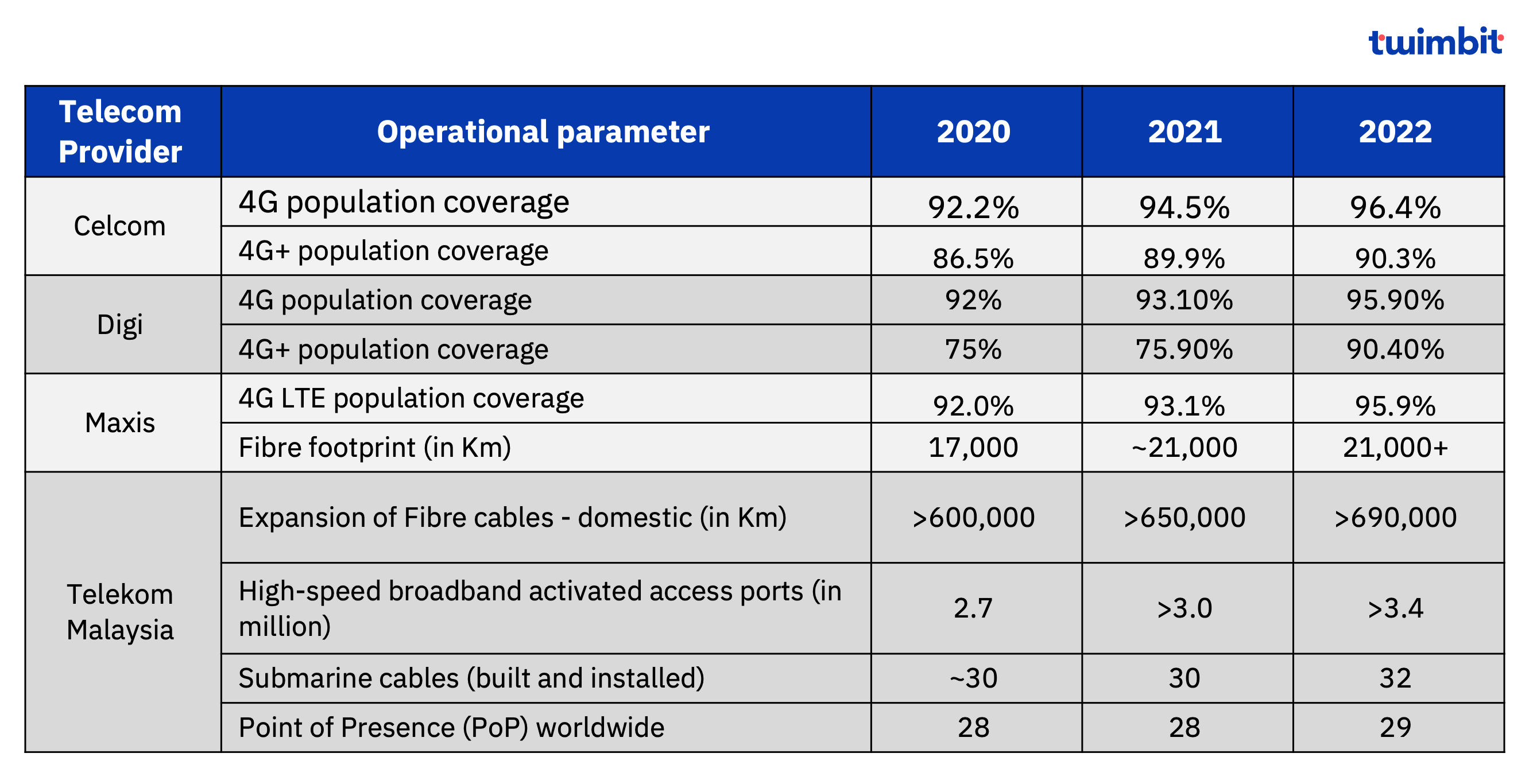

Exhibit 16: Telcos network operation indicators, 2020-22

CelcomDiGi, in congruence with its strategic direction, continued to augment its network presence. During the year 2022, it embarked on new site construction (65 new sites) and site upgrades (1,489 sites) in select rural and remote areas.

Telcos are also forging agreements with networking vendors for building and modernization of networks. In 2023, CelcomDiGi partnered with Huawei and ZTE for its RAN network modernization. Telekom Malaysia’s partnership with ZTE focuses on building a hybrid cloud 5G core network to enable it to support future technologies and applications.

Key Trends and Growth Opportunities

A. Telcos leverage digital capabilities to offer enriched customer experience

The existing competition level has compelled the telcos to focus on three major aspects (differentiation, customer retention and meeting the customer expectations), to prevent customer churn and drive revenue. Telcos are adopting digital tools and capabilities for customer acquisition and selling their product offerings to existing as well as potential new customers.

Maxis invests in IT and digitalization, with a Digital Care Program featuring a chatbot, MAX, leading to a 2.5x YoY increase in Digital Sales in 2022. Telekom Malaysia offers a self-diagnosis app within MyUnifi, and CelcomDigi focuses on touch-free initiatives for efficiency.

Personal enriched customer experience offered to the customers by leveraging the digital channels would enable the telcos to reduce their Opex as well as Capex. Additionally, it would also result in higher engagement value. This is a key for telcos to thrive and succeed in a competitive market like Malaysia, where data connectivity and access speed might not be the relevant differentiating factor for the telcos.

B. Focus shifting towards convergent offerings to boost revenue

Malaysian telcos are strategically shifting toward convergent offerings to enhance their value beyond pricing. For example, Maxis saw increased subscriptions in postpaid and home fiber services in 2022 due to bundled offerings, including unlimited services for customers with both fiber and mobile subscriptions. Telekom Malaysia’s Unifi mobile expanded its product range with lifestyle devices and digital solutions, offering bundled plans with streaming apps and premium channels.

Convergent offerings create a dual revenue stream for telcos, leveraging the launch of 5G services and the integration of connected devices. 5G technology provides high-speed access for launching new services and applications while bundling 5G with IoT-connected devices enables telcos to introduce new capabilities within bundled offerings.

Conclusion

The Malaysian Government, through the establishment of the Malaysia Digital Economy Blueprint and the Digital Investment Office in 2021, has set its sights on attracting a substantial USD 16.1 billion in digital investments by 2025. This targeted investment influx is projected to contribute ~25.5% to the GDP, marking an increase from the observed 23.5% contribution in 2021. Furthermore, as telcos concentrate on advancing the commercial rollout of 5G services and harnessing fibre infrastructure for integrated offerings, a robust demand for their services is anticipated.

However, the period 2023-24 may present challenges for telcos, driven by heightened competition, particularly with the emergence of CelcomDiGi. Additionally, regulatory changes are on the horizon, including the potential divestment of the government’s stake in DNB, once the latter attains its network rollout objective. Furthermore, the prospect of allowing a second 5G network rollout once the coverage reaches 80% of the population, coupled with considerations like the introduction of 5G wholesale fees and the imposition of a Mandatory Standard on Access Pricing (MSAP) for fibre services, may result in higher operational costs and lower profitability for telcos.

Notwithstanding these challenges, the provision of affordable and accessible connectivity offerings by telcos, coupled with government-supported regulations, will persistently work to narrow the digital divide between rural and urban areas. Concurrently, increased user participation in the digital marketplace is poised to drive digital inclusion, thereby fostering an upward trajectory for the Malaysian digital economy.

Explore more content on telecoms: here

Read our country update- Indonesia Telecoms Update 2023